Market Overview

| Study Period | 2020 - 2031 |

|---|---|

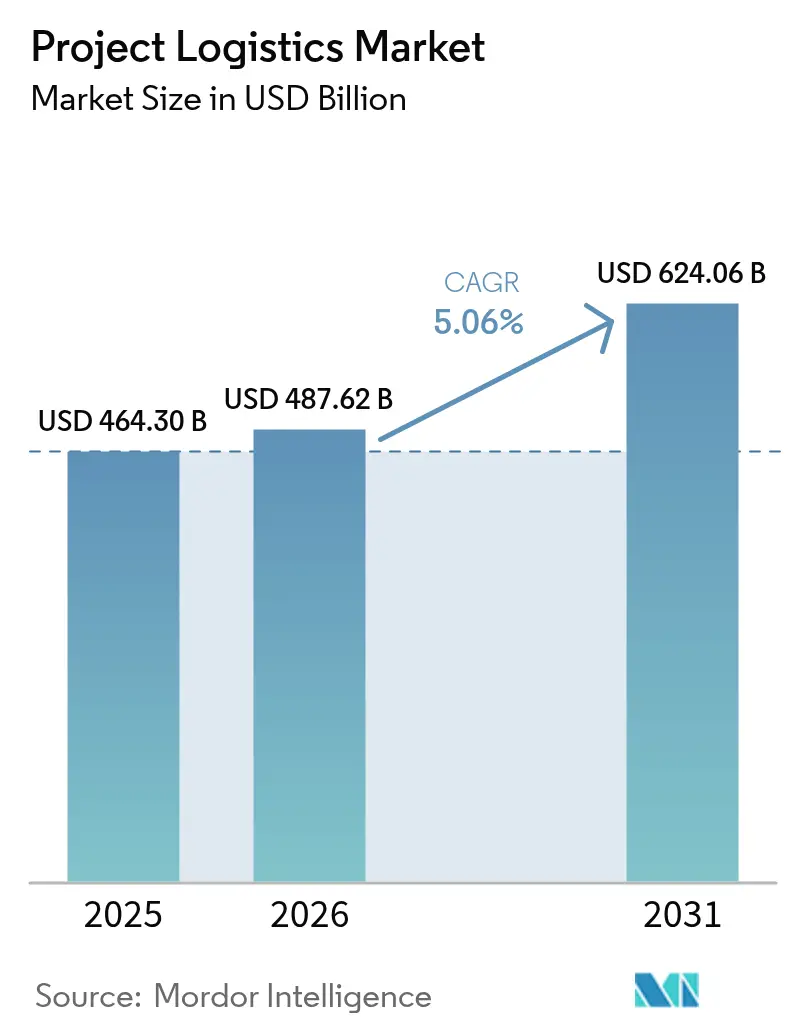

| Market Size (2026) | USD 487.62 Billion |

| Market Size (2031) | USD 624.06 Billion |

| Growth Rate (2026 - 2031) | 5.06% CAGR |

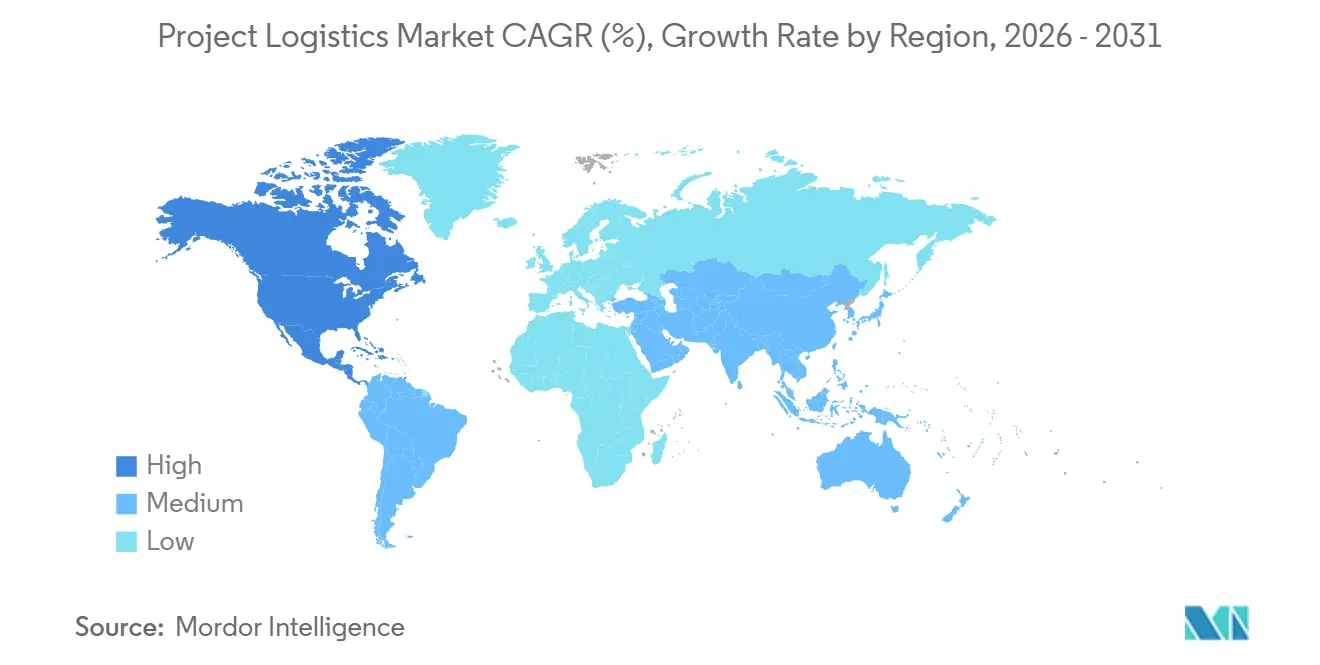

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Project Logistics Market Analysis by Mordor Intelligence

The Project Logistics Market size was valued at USD 464.30 billion in 2025 and is estimated to grow from USD 487.62 billion in 2026 to reach USD 624.06 billion by 2031, at a CAGR of 5.06% during the forecast period (2026-2031).

Specialized services for oversized, heavy-lift, and breakbulk cargo are moving from a supporting role to a core value lever as capital spending centers on energy transition, defense procurement, and advanced manufacturing. Persistent tightness in heavy-lift vessel capacity is pushing shippers to secure equipment early, which strengthens the position of integrated logistics providers that own terminals, barges, and specialized fleets. Multimodal diversification continues after the Middle Corridor’s traffic growth in 2024, with inland waterways and rail gaining relevance in routing plans that hedge geopolitical risk. Policy changes in major markets are adding planning complexity and encouraging pre‑positioned inventory, especially for renewables and grid components. Investments in visibility platforms and engineered handling are becoming points of differentiation as clients demand execution reliability over rate‑only bids.

Key Report Takeaways

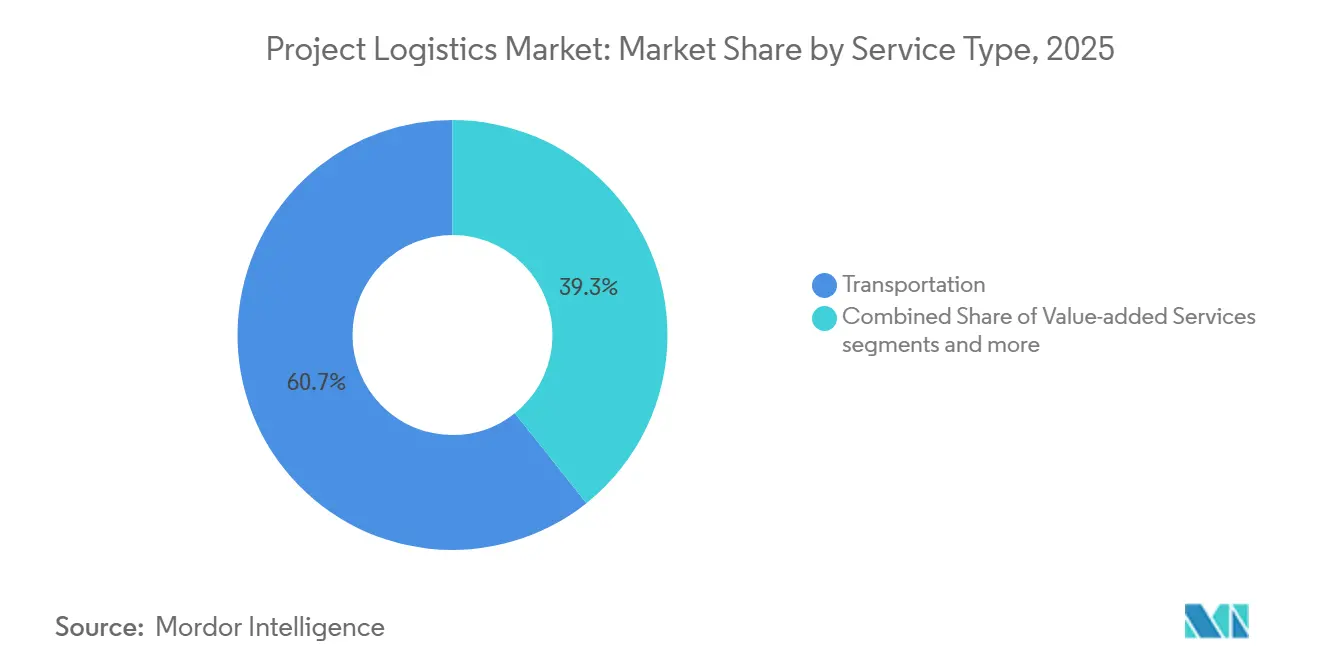

- By service, transportation services led with 60.71% project logistics market share in 2025, while warehousing, distribution, and inventory management are projected to expand at a 5.24% CAGR through 2026-2031.

- By cargo type, oversized cargo accounted for a 32.61% share in 2025, while heavy-lift cargo is projected to grow at a 5.65% CAGR through 2026-2031.

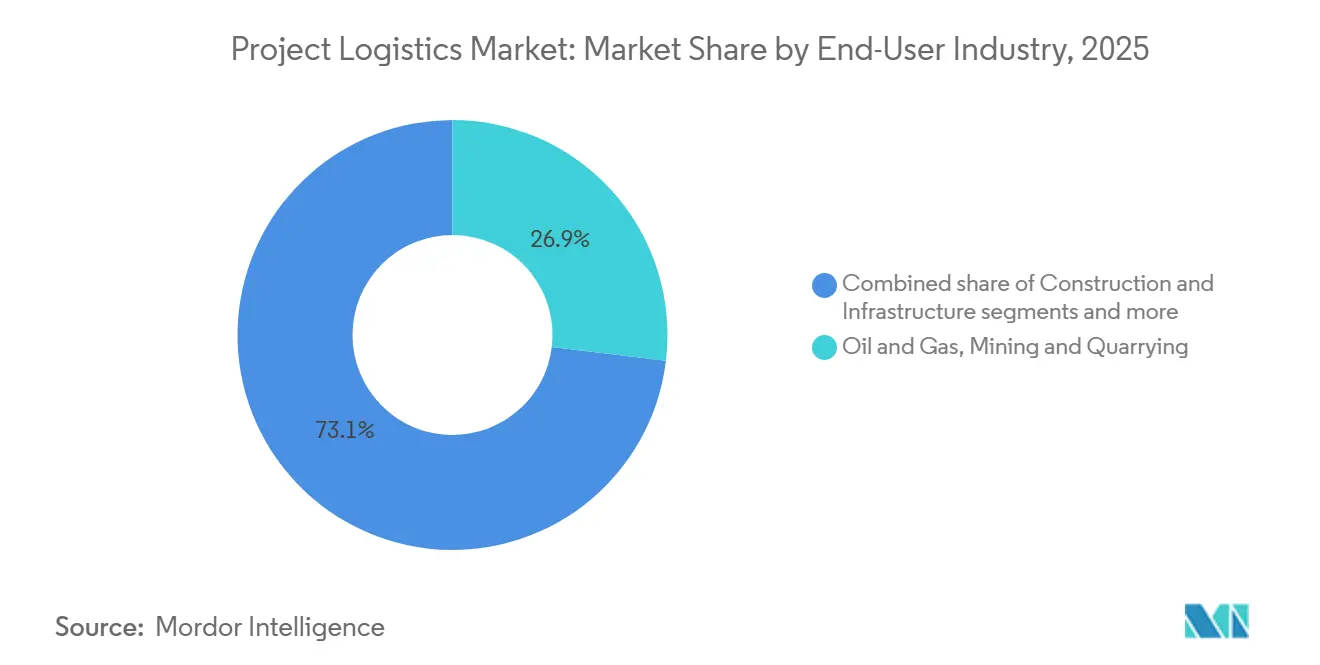

- By end-user industry, oil and gas projects held 26.91% share of the project logistics market size in 2025, while energy generation and transmission is projected to grow at a 5.90% CAGR through 2026-2031.

- By geography, Asia-Pacific held a 38.90% share in 2025, while North America is projected to record the fastest growth at a 6.49% CAGR through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Project Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Oil & Gas and Energy Sector Installations | +1.2% | Global, concentrated in Middle East, North America core basins, offshore West Africa | Medium term (2-4 years) |

| Development of Renewable Energy Projects | +1.8% | Global, highest in APAC (China, India), Europe (Germany, Netherlands), emerging in Middle East | Long term (≥ 4 years) |

| Adoption of Multimodal Transport Solutions | +0.7% | Europe and North America regional hubs, Asia inland corridors (Middle Corridor, China–Europe rail) | Short term (≤ 2 years) |

| Government Initiatives for Port and Rail Connectivity | +0.9% | North America, Central Asia, India | Medium term (2-4 years) |

| Focus on Specialist Handling and Value-Added Services | +0.6% | Global, premium demand in semiconductor and data center hubs | Short term (≤ 2 years) |

| Artificial Intelligence and Data Center Construction | +0.8% | North America, Asia-Pacific, Middle East | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of Oil & Gas and Energy Sector Installations

Oil and gas capital programs are increasing logistics complexity as operators transport larger, heavier modules through congested corridors with limited fleets. Tight heavy-lift vessel capacity drives early bookings, benefiting logistics providers with specialized assets. Vertical integration is rising, with providers adding engineered lifting and modular transporters for turnkey scopes. LNG and petrochemical projects rely on modular construction, requiring advanced load-out and route management. Middle Eastern energy investments and offshore West Africa projects sustain demand for semi-submersible ships and dynamic positioning expertise. Asset-backed providers aligned with project pipelines offer fixed-price, schedule-certain contracts, reducing client exposure to spot-rate fluctuations. This trend is shifting the project logistics market toward asset-backed execution models emphasizing scale and engineering depth.

Development of Renewable Energy Projects

Wind and solar buildouts are reshaping cargo flows with large components, tighter interconnection schedules, and transport decarbonization. Germany’s 2025 onshore wind capacity approvals have accelerated, compressing permitting times and speeding up component staging at ports. Logistics providers are adopting low-emission inland shipping and sustainable aviation fuel to reduce transport emissions. Circularity in batteries and power electronics is driving reverse logistics for collection and refurbishment, expanding bidirectional cargo cycles. Chinese renewable investments in Asia, Africa, and Latin America are influencing heavy component transport patterns. As grid-scale storage and offshore wind grow, specialist handling and compliance are becoming key in project logistics.

Adoption of Multimodal Transport Solutions

Route diversification is reshaping the project logistics market as shippers spread risk across multiple transport modes for project schedules. The Rhine corridor uses inland vessel shuttles to reduce road congestion and emissions, requiring pre-booking. The Middle Corridor shows hybrid rail-sea chains can cut lead times versus ocean routes, though handoffs and border processes need strong coordination. Digital platforms now provide real-time tracking and customs updates, aligning inland drayage and site windows for critical modules. Industry bodies are digitizing paperwork to reduce delays and improve cross-border processes. These changes are driving integrated quotes blending air, ocean, and inland delivery under unified control.

Government Initiatives for Port and Rail Connectivity

Public investment is easing constraints on oversized and heavy-lift cargo, particularly in North America. The Bipartisan Infrastructure Law is enhancing surface transportation, rail, and ports, improving berth depths, cargo handling, and inland connectivity for renewable components and LNG modules.[1]“U.S. Department of Transportation Accomplishments Overview,” U.S. Department of Transportation, transportation.gov The Railroad Crossing Elimination Program reduces delays on freight lines moving transformers, blades, and generators, supporting better drayage and rail scheduling. Grants for inland waterways modernize locks, marshalling yards, and lifting infrastructure for out-of-gauge cargo. Digital documentation standards streamline customs and intermodal handoffs, addressing cross-border delays. Rising compliance expectations in public tenders favor certified logistics providers, reducing schedule risks and improving project execution reliability.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Requirements for Heavy Equipment and Fleet | -0.9% | Global, acute in emerging markets with limited leasing infrastructure | Medium term (2-4 years) |

| Coordination Challenges Across Multiple Stakeholders | -0.6% | Cross-border projects and megaprojects with 10+ contractors | Short term (≤ 2 years) |

| Complex Customs and Regulatory Compliance | -0.7% | High in emerging markets, regulatory changes in US/EU | Long term (≥ 4 years) |

| Infrastructure Bottlenecks in Emerging Economies | -0.8% | Sub-Saharan Africa, South Asia, Central Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Requirements for Heavy Equipment and Fleet

Engineered moves require costly specialized gear, locking up capital and raising break-even thresholds. Providers owning heavy-lift fleets mobilize quickly but face higher asset risks during demand dips or delays. Mid-sized firms often rent equipment, but long lead times force clients to trade margin for schedule certainty. Heavy-lift operations also require certified personnel, specialized yards, and safety systems, adding fixed costs. This capital intensity reshapes competition as integrated providers secure availability by bringing more scope in-house. In emerging markets, limited leasing and financing options favor international firms with stronger balance sheets, narrowing bidders for the heaviest cargo and benefiting providers with multi-year pipelines.

Coordination Challenges Across Multiple Stakeholders

Complex projects involve multiple actors with varying priorities, where minor delays can escalate costs. Coordinating over 1,000 daily deliveries to a site requires precise orchestration to avoid congestion, crane downtime, and missed milestones. Digital tools now enable door-to-door tracking and customs updates, streamlining multimodal handoffs and site activities. Efforts to digitize consignment documentation aim to reduce delays, though adoption remains inconsistent among smaller forwarders and customs authorities.[2]“Driving Digital Progress and Navigating Trade Changes,” FIATA, fiata.org Oversized cargo permits often require detailed surveys, escorts, and time-bound movements, adding paperwork and dependencies. Cross-border rules for axle loads, bridge clearances, and environmental reviews further increase administrative burdens and risks.[3]“Oversize Transport Permit Bulletin, Q4 2025,” Chongqing Wulong District Government, cqwl.gov.cn Providers with engineered planning and digital control towers are better positioned to manage these complexities at scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Transportation Commands Revenue, Warehousing Gains Strategic Importance

Transportation services accounted for 60.71% of the project logistics market in 2025, driven by road, rail, ocean, and air transport for heavy modules and out-of-gauge equipment. Warehousing and inventory management is the fastest-growing segment, projected to grow at a 5.24% CAGR as clients add buffer capacity near fabrication yards and ports. Inland waterways in Europe are gaining share through scheduled vessel shuttles, reducing emissions and stabilizing delivery windows. Digital control towers are becoming standard, improving shipment visibility, customs status, and on-site sequencing. Air transport plays a niche role for critical-path components like control systems that protect commissioning dates. Rising compliance expectations make certified handling and dangerous goods capabilities essential in Europe and North America.

Warehousing growth reflects a shift from just-in-time to just-in-case strategies for renewables, grid equipment, and industrial modules. Providers are adding bonded hubs with kitting, subassembly, and last-mile integration to cut on-site labor and absorb upstream variability. Reverse logistics for batteries and electronics adds two-way cargo flows requiring specialized storage, diagnostics, and safety systems. European corridor services now use low-emission inland vessels to stage wind components and handle steady flows for grid projects. Single-provider contracts bundle engineered handling, customs brokerage, and site logistics with transport, prioritizing schedule certainty over rate-only solutions. This shift reshapes bid evaluations toward execution reliability, compliance, and multimodal orchestration.

By Cargo Type: Oversized Dominates, Heavy-Lift Accelerates on Modular Construction Demand

Oversized cargo held a 32.61% share of the project logistics market in 2025, driven by blades, transformer casings, and pressure vessels requiring route surveys, escorts, and permits. Heavy-lift cargo is expected to grow at a 5.65% CAGR through 2031, fueled by modularization in LNG plants, offshore wind, and advanced manufacturing. Providers with engineered lifting systems and SPMTs can secure turnkey moves for high-value modules. Renewable shipments are supported by inland waterways and port staging, easing delivery for large components under tight permits. Execution risks in last-mile turns emphasize the need for experienced teams managing local route surveys and escorts.

Breakbulk steel and packaged machinery remain vital for industrial builds, though growth is shifting to heavier, integrated units, reducing on-site assembly. Battery and electronics logistics now include reverse flows for diagnostics and recycling, requiring specialized handling. Inland waterway expansion and barge shuttles reduce road congestion for heavy profiles. The market sees more engineered moves needing monitoring, shock sensors, and climate controls to protect sensitive modules. Risk management and insurance increasingly rely on compliance and traceable handling throughout transit.

By End-User Industry: Strategic Shifts in Project Logistics from Heavy Modules to Renewable Integration

Oil and gas, mining, and quarrying will account for 26.91% of demand in 2025, driven by upstream and midstream programs prioritizing large modules and tight commissioning sequences. Energy generation and transmission are projected to grow at a 5.90% CAGR, with increasing exposure to grid-scale components and offshore wind foundations as approvals accelerate and installation windows tighten. Germany's 2025 onshore wind approvals and compressed permit lead times are boosting logistics activity in inland waterways and marshalling yards. Reverse logistics for batteries and power electronics is becoming standard in European deployments, aligning with regulatory and safety requirements. In North America and the Middle East, heavy modules for energy and industrial projects sustain steady flows of engineered transport and lifting.

Industrial manufacturing, data centers, and specialized facilities require high-touch moves with controlled environments and precise staging. Providers are investing in warehouse automation and visibility platforms to enhance throughput and reduce errors, focusing on on-time, in-sequence delivery over cost. Chinese renewable investments are influencing routing and sourcing for EPC and component suppliers in Southeast Asia and Sub-Saharan Africa. The project logistics market is adapting with multi-country footprints, certified dangerous goods handling, and structured reverse flows to meet regulatory and warranty requirements. These shifts highlight orchestration skills, multimodal design, and compliance depth as key award criteria.

Geography Analysis

Asia-Pacific is expected to hold a 38.90% project logistics market share in 2025, driven by large-scale energy and industrial programs and its role in component fabrication and export staging. Supply chains for wind, grid equipment, and energy exports are shaping port and inland network priorities. Chinese overseas renewables investment is sustaining corridors into Southeast Asia, the Middle East, and Africa, boosting demand for heavy-lift and breakbulk capacity. Inland waterway and coastal feeder services are easing port congestion and supporting heavy module staging. Providers are aligning footprints and certifications to meet rising documentation and dangerous goods handling standards.

North America is projected to grow at a 6.49% CAGR, supported by infrastructure funding, port modernization, and rail improvements. The Bipartisan Infrastructure Law is enabling upgrades that reduce schedule risks for projects with tight installation windows. Logistics providers are expanding bonded hubs and value-added services to stage renewable components closer to sites. Digital visibility platforms are improving reliability in multimodal chains, supporting the project logistics market as energy transition projects accelerate.

Europe is scaling wind and grid investments while tightening emissions and documentation requirements. Germany’s momentum has increased demand for inland waterway shuttles and port-side staging for wind components. Scheduled Rhine services are reducing road congestion and improving delivery predictability. Digital documentation efforts are advancing, though uneven adoption sustains manual fallbacks. In the Middle East, industrial and energy programs are driving investment in bonded logistics hubs and last-mile services. South America’s corridors are strengthening as European providers connect Iberia to Brazil and other markets, supporting offshore wind and mining sectors.

Competitive Landscape

The project logistics market remains fragmented, with a broad base of regional specialists and a handful of global players scaling through integration, engineered handling, and visibility platforms. Scale providers continue to consolidate networks and fleets to absorb demand swings and offer fixed-price turnkey solutions that smaller firms cannot match under volatile spot conditions. Vertical integration is accelerating as firms bring heavy-lift capabilities in-house to reduce mobilization lead times and secure schedule control on complex engineered moves. In bids, clients emphasize proven execution reliability, compliance credentials, and transparent visibility over rate-only competition, which amplifies the advantage of integrated platforms.

Global leaders are complementing network scale with targeted technology and sustainability moves that resonate with energy and industrial customers. Sustainable aviation fuel commitments are helping address Scope 3 emissions linked to critical-path air movements, which improves the emissions profile of urgent shipments in green supply chains. Engineered heavy-lift capacity remains a differentiator, as ownership of cranes, strand jacks, and SPMTs enables rapid response to tight construction windows and reduces reliance on constrained rental markets. European inland waterway services are expanding to support wind and grid logistics, which adds new routing options and lowers reliance on limited road permits. Providers are also deepening vertical expertise in aerospace, energy, and data center logistics to align handling standards and certifications with sensitive, high-value equipment.

Technology adoption is now a core competitive axis in the project logistics market as providers roll out control towers and on-site orchestration that reduce errors and congestion. Platforms that deliver door-to-door visibility and exception management are becoming requirements in complex, multimodal bids that hinge on tight sequencing across modes and jurisdictions. Specialist partners in Germany and other markets emphasize engineered route surveys and permit handling for out-of-gauge cargo, which speeds approvals and reduces change orders during execution. Providers that demonstrate consistent performance in high-intensity programs, including data centers with hundreds to over 1,000 daily deliveries, can command premiums for assured timelines. Compliance, dangerous goods handling, and documented quality systems continue to shape award decisions and formalize a two-tier market based on certified capabilities and asset depth.

Project Logistics Industry Leaders

Deutsche Post DHL

Rhenus Logistics

CEVA Logistics

Kuehne + Nagel

EMO Trans

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Rhenus Logistics completed its acquisition of 100% of Grupo Totalmédia in Portugal, adding 16 logistics platforms and 3.5 million annual shipments to strengthen Iberian and Latin American corridor connectivity.

- December 2025: CEVA Logistics has acquired Fagioli Group, bolstering its project logistics operations with the expertise of over 1,000 specialists.

- November 2025: DSV reported Q3 2025 results and confirmed accelerated progress on the Schenker integration, citing network and fleet synergies expected to strengthen execution in complex projects.

- November 2025: DHL Group signed a three-year agreement with Phillips 66 to purchase over 240,000 tonnes of sustainable aviation fuel to reduce Scope 3 emissions tied to air shipments.

Global Project Logistics Market Report Scope

The Project Logistics Market is Segmented by Service (Transportation, Warehousing, and Value-Added Services), by Cargo Type (Oversized, Heavy-Lift, Breakbulk, and Others), by End-User (Oil & Gas/Mining, Energy Generation, Construction, Manufacturing, Aerospace, and Others), and by Geography (North America, South America, Asia-Pacific, Europe, and Middle East & Africa). Forecasts are in Value (USD).

By Service

| Transportation | Road |

| Rail | |

| Air | |

| Sea | |

| Warehousing, Distribution and Inventory Management | |

| Value-added Services and Others |

By Cargo Type

| Oversized (Out-of-Gauge) Cargo |

| Heavy-Lift Cargo |

| Breakbulk Cargo |

| Others |

By End-User Industry

| Oil and Gas, Mining and Quarrying |

| Energy Generation and Transmission (Includes Renewable Energy) |

| Construction and Infrastructure |

| Manufacturing and Industrial Plants |

| Aerospace and Defense |

| Others (Maritime and Shipbuilding, Telecommunications, etc.) |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East and Africa | United Arab of Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Service | Transportation | Road |

| Rail | ||

| Air | ||

| Sea | ||

| Warehousing, Distribution and Inventory Management | ||

| Value-added Services and Others | ||

| By Cargo Type | Oversized (Out-of-Gauge) Cargo | |

| Heavy-Lift Cargo | ||

| Breakbulk Cargo | ||

| Others | ||

| By End-User Industry | Oil and Gas, Mining and Quarrying | |

| Energy Generation and Transmission (Includes Renewable Energy) | ||

| Construction and Infrastructure | ||

| Manufacturing and Industrial Plants | ||

| Aerospace and Defense | ||

| Others (Maritime and Shipbuilding, Telecommunications, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab of Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the project logistics market?

The project logistics market size was USD 464.3 billion in 2025 and is projected to reach USD 624.06 billion by 2031 at a 5.06% CAGR from 2026 through 2031.

Which service lines are leading growth in the project logistics market?

Transportation led with 60.71% of 2025 revenue, while warehousing, distribution, and inventory management is the fastest-growing service with a projected 5.24% CAGR through 2031.

What cargo types are most important in the project logistics market?

Oversized cargo held a 32.61% share in 2025, and heavy-lift cargo is projected to grow the fastest at a 5.65% CAGR through 2031 as modular construction expands.

Which end-user segments drive demand in the project logistics market?

Oil and gas projects accounted for 26.91% of 2025 demand, while energy generation and transmission is projected to grow at a 5.90% CAGR on the back of wind and grid investments.

Which region will grow the fastest in the project logistics market through 2031?

North America is projected to grow the fastest at a 6.49% CAGR due to infrastructure funding, port and rail upgrades, and accelerated permitting that improve schedule reliability.

How are leading companies differentiating in the project logistics market?

Leaders are integrating engineered heavy-lift assets, expanding bonded hubs and value-added services, adopting visibility platforms, and committing to sustainable fuel to secure schedule-certain execution and emissions reductions.

Page last updated on: