Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

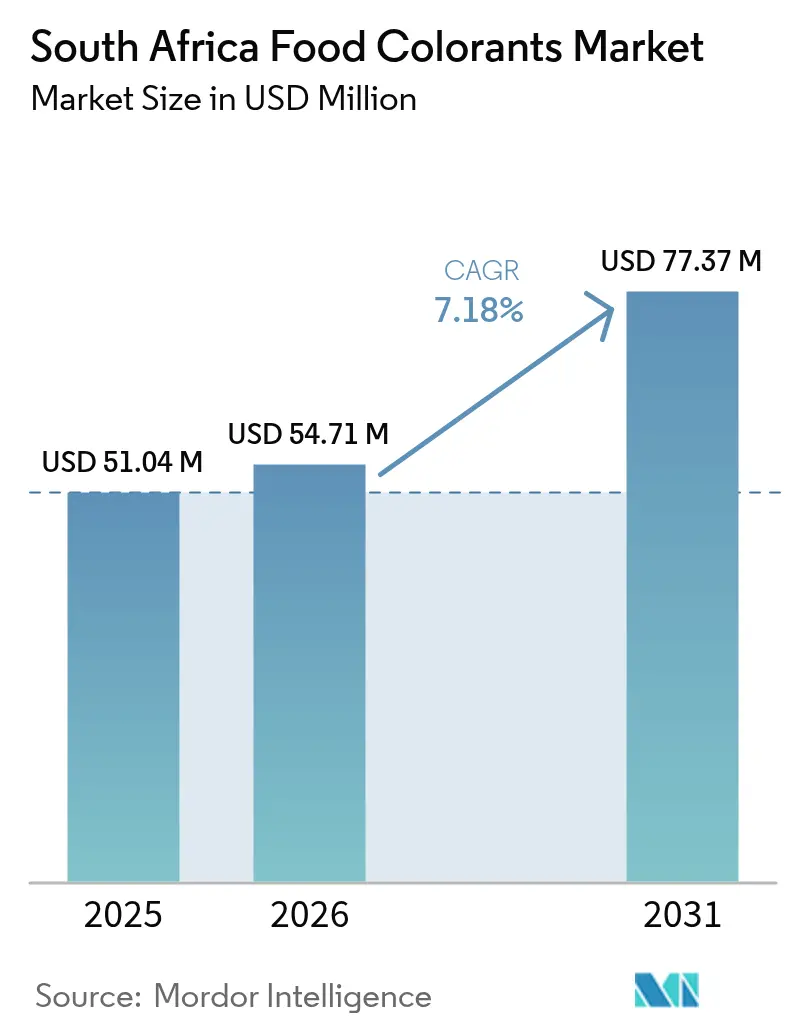

| Base Year Market Size (2025) | USD 51.04 Million |

| Market Size (2026) | USD 54.71 Million |

| Market Size (2031) | USD 77.37 Million |

| Growth Rate (2026 - 2031) | 7.18% CAGR |

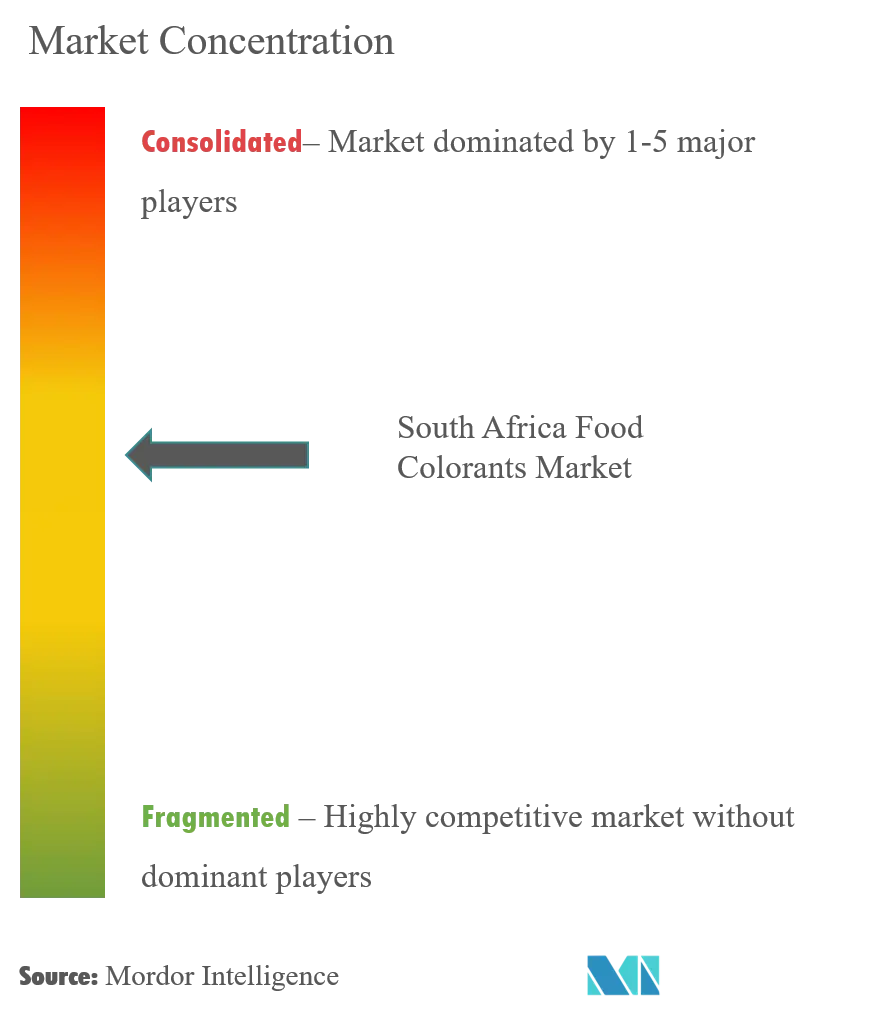

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Africa Food Colorants Market Analysis by Mordor Intelligence

South Africa food colorant market size in 2026 is estimated at USD 54.71 million, growing from 2025 value of USD 51.04 million with 2031 projections showing USD 77.37 million, growing at 7.18% CAGR over 2026-2031. This growth is driven not just by an uptick in processed food volumes, but more so by a pronounced shift towards plant-derived pigments. This shift comes as retailers, regulators, and consumers heighten their scrutiny of additive labels. The surge in demand for natural reds, yellows, and blues aligns with South Africa's robust USD 44 billion packaged-food sector, predominantly driven by the bakery, confectionery, and beverage segments. In Gauteng's manufacturing hub, multinational suppliers and agile local extract specialists frequently clash over pricing and technology. While there's a rising inclination towards natural colors, cost pressures in value-tier snacks and challenges in achieving neon shades keep synthetic colors in play. Thus, the market's future champions will be those suppliers who can offer natural pigments with synthetic-like durability at a modest premium, rather than those merely pursuing the lowest price per kilogram.

Key Report Takeaways

- By type, natural color accounted for 55.18% of the South African food colorant market share in 2025, while synthetic color is projected to achieve the fastest growth rate at 8.30% CAGR through 2031.

- By color, red led the market with a 27.01% share in 2025, while blue is poised for the most significant expansion at an 8.42% CAGR through 2031.

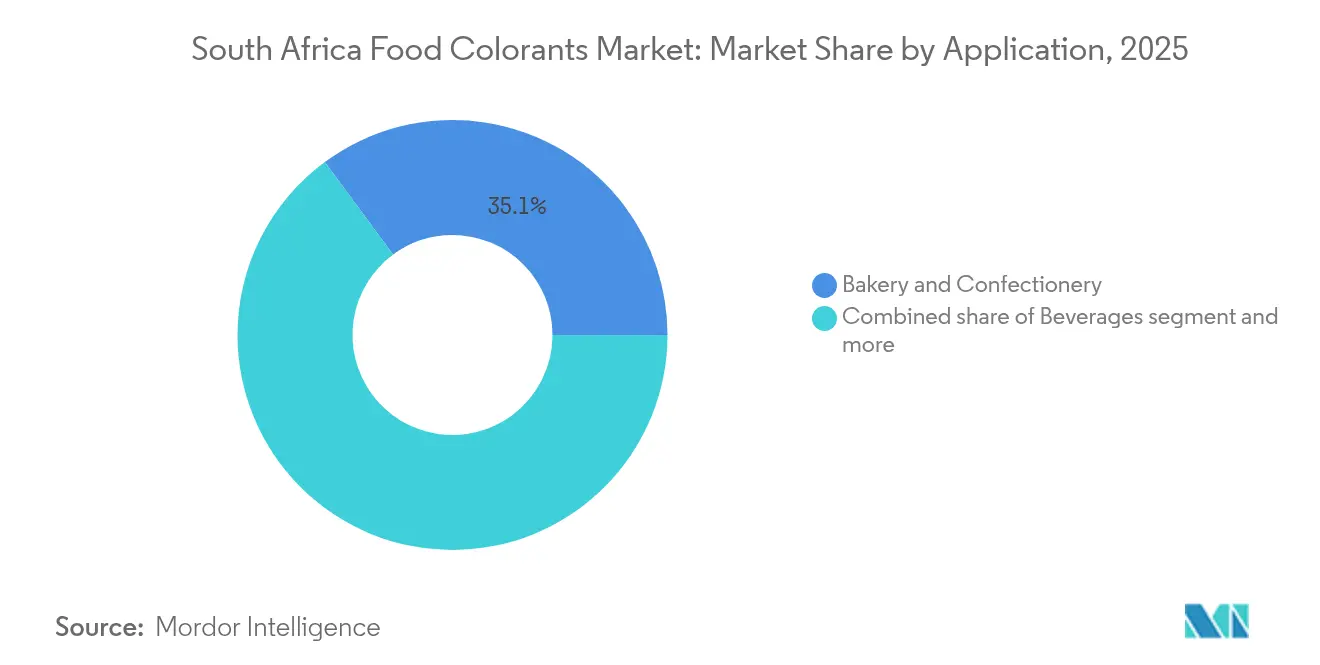

- By application, bakery and confectionery applications topped the chart with a 35.12% revenue share in 2025, and beverages are anticipated to grow at an 7.92% CAGR during the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Food Colorants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer demand for clean-label products | +1.2% | National, concentrated in Gauteng and Western Cape urban centers | Medium term (2-4 years) |

| Expansion of packaged snacks, ready-to-eat meals, beverages, and convenience foods requiring visual appeal | +1.0% | National, with retail penetration in Johannesburg, Cape Town, Durban | Short term (≤ 2 years) |

| High penetration of bakery products requiring color enhancement across demographics | +0.9% | National, driven by in-store bakery expansion in Shoprite, Pick n Pay, Woolworths | Medium term (2-4 years) |

| Development of advanced extraction and stabilization techniques improving natural colorant performance | +0.8% | Global innovation hubs (EU, North America) with adoption in South African manufacturing | Long term (≥ 4 years) |

| Increased demand for color stabilization in processed meat and seafood products | +0.6% | National, with export-oriented facilities in coastal provinces | Medium term (2-4 years) |

| Rising demand for yogurt, ice cream, cheese, and plant-based alternatives requiring stable colors | +0.7% | National, accelerated by plant-based dairy launches in Gauteng | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Demand for Clean-Label Products

In South Africa, consumers are increasingly scrutinizing ingredient lists, echoing global clean-label trends but with a distinct local flavor. In 2024, incidents of food fraud, particularly the use of industrial dyes in spice mixes, intensified skepticism towards synthetic additives. This led to more rigorous audits by retailers. Major retail chains now mandate suppliers to not only disclose the origins of colorants but also to certify adherence to the South African Bureau of Standards regulations. This effectively raises the bar for the use of synthetic formulations. The impact of this shift is evident: industry supplier surveys indicate an 18% year-on-year surge in the adoption of natural colorants in premium bakery and dairy products in 2024. Additionally, the Department of Health's enforcement of the updated Foodstuffs Act, which emphasizes clearer E-number labeling, further favors recognizable plant extracts such as turmeric and beetroot[1]Source: South African Government, “Updated Foodstuffs, Cosmetics and Disinfectants Act,” gov.za. Brands that openly highlight their natural sourcing are finding favor on the shelves of Woolworths and Pick n Pay. Here, middle-income consumers are even willing to pay a 10-12% premium for products they perceive as safer.

Expansion of Packaged Snacks, Ready-to-Eat Meals, Beverages, and Convenience Foods Requiring Visual Appeal

In urban South Africa, dual-income households are driving a 9% annual growth in ready-to-eat meal purchases. On crowded supermarket shelves, visual appeal has become a critical factor in signaling freshness and quality to consumers. Today, colorants that maintain their vibrancy under LED (Light Emitting Diode) retail lighting and during extended ambient storage are now a baseline requirement for successful product launches. The beverage segment highlights this trend: energy drinks and flavored sparkling waters, designed for Gen-Z consumers, use bold, Instagram-worthy colors to stand out, especially in a market where consumers cannot taste products before purchasing. Sensient Technologies, in 2024, introduced heat-stable natural yellows specifically for South African beverage clients. This initiative reflects formulators' understanding that color fading during pasteurization often results in consumer dissatisfaction and retailer delistings. Snack manufacturers face similar challenges. For example, potato chip coatings and extruded corn puffs must retain their color intensity through high-temperature frying—a challenge that natural carotenoids, enhanced through microencapsulation, are effectively addressing.

High Penetration of Bakery Products Requiring Color Enhancement Across Demographics

In South Africa, food colorant consumption continues to grow, fueled by in-store bakery expansions at Shoprite and Spar. These bakeries are competing with visually appealing products such as rainbow layer cakes, pastel-colored cupcakes, and artisan breads featuring activated charcoal or beetroot swirls. Consumer demographics play a key role: township bakeries, which serve cost-conscious families, often choose synthetic colorants due to their affordability. On the other hand, upscale patisseries in Sandton focus on natural colorants to align with their health-conscious branding. However, maintaining consistent color remains a technical challenge because of variations in baking temperatures and dough pH (potential of hydrogen) levels. To address this, BASF introduced pH-buffered natural reds in 2024, specifically for South African bakery clients. This innovation resolves anthocyanin instability in alkaline doughs, enabling clean-label red velvet formulations that previously depended on synthetic Red 40. This development is strategically important as export-oriented bakeries targeting European Union (EU) markets must comply with restrictions on certain synthetic dyes. For these bakeries, natural alternatives are not just a marketing preference but a regulatory requirement.

Development of Advanced Extraction and Stabilization Techniques Improving Natural Colorant Performance

Precision fermentation and enzyme-assisted extraction are narrowing the gap between natural and synthetic colorants. This shift carries significant weight for South Africa's ingredient sector, which heavily relies on imports. Israeli biotech Phytolon has developed betalain-based blues through yeast fermentation. These offer 3-5 times the stability of the traditionally used spirulina-derived phycocyanin, especially under heat and light stress. This advancement directly addresses a longstanding challenge in beverage formulations. Meanwhile, GNT Group has commercialized a spirulina stabilization technology in 2024, which received FDA clearance. By employing protective colloids, this technology extends the shelf life of dairy products. This breakthrough allows yogurt producers in South Africa to safely substitute Brilliant Blue FCF without the usual reformulation concerns. Furthermore, methods like ultrasound-assisted extraction and supercritical CO2 techniques have enhanced pigment yields from raw materials by 20-30%. This advancement has slashed the cost premium of natural colorants, bringing it down from 40% to a mere 15% compared to their synthetic counterparts. By embracing these innovations, South African manufacturers not only align with the tightening export standards of the EU but also carve out a distinct niche in the domestic premium market.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Natural pigments prone to degradation under heat, light, and oxidative conditions during storage | -0.8% | National, acute in ambient-temperature distribution networks | Short term (≤ 2 years) |

| Complex registration, testing, and approval processes for both synthetic and natural colorants | -0.6% | National, with spillover effects from EU and US regulatory alignment | Medium term (2-4 years) |

| Bans or restrictions on specific synthetic colors in certain applications | -0.5% | Global, affecting South African export-oriented manufacturers | Medium term (2-4 years) |

| Difficulty in achieving certain color shades with natural alternatives | -0.4% | National, concentrated in beverages and confectionery | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Natural Pigments Prone to Degradation Under Heat, Light, and Oxidative Conditions During Storage

In South Africa's retail environment, where glass-fronted refrigerators and ambient-temperature displays are common, anthocyanins (natural pigments responsible for red, purple, and blue colors in plants) can lose 30-50% of their color intensity after just 48 hours of UV light exposure. This creates a significant challenge for manufacturers. Similarly, chlorophyll-based greens, when exposed to acidic pH (potential of hydrogen), shift to an olive-brown hue, limiting their use in citrus-flavored drinks and salad dressings. While betalains, derived from beetroot, are more stable than anthocyanins, they still degrade when exposed to metal ions. These ions are commonly found in municipal water supplies used by food processors. Such technical challenges lead to reformulation cycles, delaying product launches by 3-6 months and increasing research and development costs by 15-20% compared to projects using synthetic colorants. Technologies like lipid shells, alginate beads, and protein complexes can help mitigate some degradation pathways. However, these solutions add USD 2-4 per kilogram to ingredient costs, reducing profit margins in price-sensitive categories like value-tier snacks and beverages. Manufacturers in South Africa, catering to both local and export markets, face the added complexity of maintaining two distinct formulations: one optimized for the country's ambient distribution and another designed for the European Union's (EU) refrigerated supply chains.

Complex Registration, Testing, and Approval Processes for Both Synthetic and Natural Colorants

In South Africa, novel natural colorants require 18-24 months to gain approval from the South African Bureau of Standards (SABS). This process involves toxicology studies, allergen testing, and stability validation to ensure suitability under local climatic conditions. A regulatory update from the Department of Health in 2024 now requires additional documentation for colorants derived from genetically modified organisms (GMOs). This change significantly impacts fermentation-based pigments produced by companies such as Phytolon and Nextferm. Smaller ingredient suppliers often struggle with these regulatory demands due to a lack of dedicated regulatory affairs teams, leaving the market open to multinational corporations with established government connections. Synthetic colorants face similar challenges. Any new synthetic dye must undergo evaluation by the Joint FAO/WHO Expert Committee on Food Additives (JECFA) and comply with Codex Alimentarius standards before South African regulators can grant provisional approval [2]Source: Department of Health, Republic of South Africa, "Regulation Related to Food Colorant," health.gov.za. As a result, there is typically a 2-3 year delay between global colorant innovations and their availability to South African manufacturers. During this time, competitors in Kenya and Nigeria often gain first-mover advantages in regional export markets. This regulatory complexity disproportionately affects mid-sized food processors, who cannot afford to maintain inventories of multiple colorant options while awaiting approvals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Natural Dominance Masks Synthetic Resilience

In 2025, Natural Color captured 55.18% of the market share, driven by the increasing demand for clean-label products and retailer mandates for easily recognizable ingredients. However, Synthetic Color is projected to grow at a strong compound annual growth rate (CAGR) of 8.30% through 2031, outpacing the growth of Natural Color. This growth is primarily attributed to cost pressures in value-tier snack products and the superior technical performance of synthetic dyes, especially in applications requiring neon brightness or stability under extreme pH conditions. Synthetic formulations continue to dominate categories such as hard candies, sports drinks, and extruded cereals, where natural alternatives often fade or introduce undesirable flavors at effective dosing levels.

Precision fermentation is increasingly redefining the boundary between natural and synthetic colors. For instance, Phytolon's yeast-derived betalains are classified as natural under most regulatory standards but deliver stability comparable to synthetic dyes. This hybrid positioning appeals to premium brands that aim to maintain clean-label credentials while ensuring high performance in their products.

By Color: Red Leads, Blue Surges on Beverage Innovation

In 2025, red colorants accounted for 27.01% of the market share, supported by the use of beetroot extract in processed meats, paprika oleoresin in snacks, and carmine in premium confectionery. On the other hand, blue is the fastest-growing color, with a compound annual growth rate (CAGR) of 8.42%. This growth is fueled by beverage manufacturers catering to the rising social media-driven demand for visually appealing products like gradient drinks and color-changing cocktails. Historically, natural blue colorants have faced challenges due to the pH sensitivity of spirulina. Specifically, phycocyanin, a pigment derived from spirulina, turns gray-green when the pH drops below 4.5, making it unsuitable for applications such as carbonated soft drinks and fruit juices.

GNT Group's 2024 Food and Drug Administration (FDA)-approved stabilization technology addresses this issue by using protective colloids to enhance the retention of blue hues in acidic beverages. This advancement has enabled major players like Coca-Cola and PepsiCo to reformulate their sports drinks with natural spirulina. The importance of this innovation cannot be overstated, as blue remains the only primary color without a reliable natural alternative. This creates a competitive advantage for suppliers who can effectively resolve the stability challenges, positioning them to dominate the market.

By Application: Bakery Anchors, Beverages Accelerate

In 2025, the Bakery and Confectionery sector secured a significant 35.12% market share, driven by the strategic expansion of in-store bakeries at major retailers like Shoprite and Spar. These retailers are leveraging visually appealing and innovative products to attract customers, offering items such as ombre cakes, galaxy-themed cupcakes, and macarons made with natural colors. This focus on visual novelty has enabled them to differentiate themselves in an increasingly competitive market. The sector's ability to adapt to evolving consumer preferences for unique and aesthetically pleasing products has been a key factor in maintaining its strong market position.

The beverage segment, on the other hand, is projected to experience the fastest growth, with a compound annual growth rate (CAGR) of 7.92%. This growth is fueled by the rising popularity of ready-to-drink teas, plant-based milk alternatives, and energy drinks, which are using color as a primary tool to stand out in crowded retail coolers. However, the segment faces stringent technical requirements. Colorants used in beverages must endure ultra-high-temperature (UHT) processing at 135°C, remain stable within a pH range of 2.5-4.5, and resist fading under LED retail lighting for a period of 6-9 months. Reflecting the industry's focus on quality and innovation, Sensient Technologies introduced heat-stable natural yellows in 2024, specifically tailored for South African beverage manufacturers. This launch highlights the willingness of clients in this segment to pay a 25-30% premium for high-performance solutions that meet these demanding standards.

Geography Analysis

South Africa's food colorant market is expected to grow at a compound annual growth rate (CAGR) of 7.18% through 2031. This growth is largely driven by urbanization in key provinces like Gauteng and Western Cape, where dual-income households are fueling demand for visually appealing convenience foods. By 2024, South Africa is set to become sub-Saharan Africa's most advanced food processing hub, with Johannesburg and Cape Town hosting manufacturing clusters for major players such as Tiger Brands, Pioneer Foods, and Nestlé South Africa. Regulatory alignment with Codex Alimentarius standards has opened up export opportunities to the European Union (EU) and the Middle East .However, South Africa's broader list of approved synthetic colorants compared to Europe has created a two-tier market. While domestic-focused brands prioritize cost-effective formulations, export-oriented companies are reformulating products with natural alternatives. Additionally, stricter labeling requirements introduced in 2024 by the South African Bureau of Standards (SABS) and the Department of Health mandate E-number disclosure and allergen warnings, encouraging the use of transparent, natural formulations.

Gauteng province leads the market, accounting for approximately 41.62% of national food colorant demand. This is due to the concentration of large-scale bakeries, beverage bottlers, and snack manufacturers serving Johannesburg and Pretoria's combined population of 15 million. In the Western Cape, the wine and fruit processing industries are driving niche demand for natural anthocyanins and carotenoids, which align with clean-label requirements for export markets. KwaZulu-Natal's coastal seafood processors are increasingly adopting natural astaxanthin to meet Marine Stewardship Council (MSC) certification standards for exports to Japan and the EU. On the other hand, the Eastern Cape and other rural provinces are slower in adopting natural colorants due to price sensitivity and limited cold-chain infrastructure, which makes shelf-stable synthetic formulations more practical.

South Africa's reliance on imports for specialty natural colorants-such as spirulina from China, annatto from Peru, and carmine from Peru-poses challenges related to currency fluctuations and supply chain disruptions. To mitigate these risks, ADM's planned 2025 acquisition of botanical-extract suppliers aims to strengthen the supply chain for natural colorants, ensuring greater stability for manufacturers in the region.

Competitive Landscape

The South Africa Food Colorant Market is moderately concentrated, with competition involving multinational ingredient companies such as Chr. Hansen (now Oterra), Sensient Technologies, DSM-Firmenich, and Cargill, alongside specialized suppliers of natural extracts and regional manufacturers of synthetic dyes. The market is divided between natural and synthetic colorants. Leading companies are investing in technologies like precision fermentation and encapsulation to create heat-stable natural blues and greens, while regional players focus on maintaining competitive pricing for synthetic options. ADM's (Archer Daniels Midland) acquisition of Totally Natural Solutions in April 2025, for an undisclosed amount, highlights the growing urgency to secure intellectual property in botanical colors, especially as titanium dioxide bans expand beyond the European Union (EU), intensifying competition in natural-extract supply chains.

Opportunities for innovation are particularly evident in natural blue colorants, where spirulina's pH instability presents technical challenges. Phytolon's betalain-based fermentation technology is addressing this issue by offering 3-5 times greater stability under heat and light stress compared to phycocyanin. Emerging biotechnology companies, such as Israeli startup Phytolon and Denmark's Nextferm, are using yeast fermentation to produce pigments, bypassing agricultural supply chains. This approach reduces risks related to seasonality and geopolitical factors, which can significantly impact crop-based extracts. These advancements pose a challenge to traditional natural colorant suppliers who depend on raw materials like Peruvian annatto and Chinese spirulina, where harvest failures or export restrictions can cause raw material costs to double within a single quarter.

Technological advancements are becoming a key factor in determining market leaders. For example, GNT Group's FDA (Food and Drug Administration)-cleared spirulina stabilization technology, commercialized in 2024, uses protective colloids to improve shelf life in dairy applications. This innovation allows South African yogurt manufacturers to replace Brilliant Blue FCF (Fast Green FCF) without the need for reformulation, providing a competitive advantage in the shift toward natural colorants.

South Africa Food Colorants Industry Leaders

-

Sensient Technologies

-

BASF SE

-

Cargill Inc.

-

Archer Daniels Midland

-

Givaudan

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: ADM completed the acquisition of Totally Natural Solutions, a New Zealand-based supplier of hop extracts and botanical colorants, strengthening its natural color portfolio and securing supply-chain access to proprietary plant varieties.

- April 2025: Sensient Technologies launched a heat-stable natural yellow colorant derived from turmeric oleoresin, specifically formulated for South African beverage clients requiring UHT processing at 135°C.

- December 2024: Döhler Group expanded its natural color portfolio with encapsulated beetroot extracts containing antioxidant co-factors, extending color stability in processed meats by 40% during refrigerated storage.

South Africa Food Colorants Market Report Scope

The South Africa Food Colorants Market is segmented by Type as Synthetic food colorants, Natural food colorants, and Others, by Application as Bakery, Meat poultry & Seafood products, Dairy & Frozen Products, Beverages and Confectionery, and Others.

By Type

| Natural Color |

| Synthetic Color |

By Color

| Blue |

| Green |

| Red |

| Yellow |

| Others |

By Application

| Bakery and Confectionery |

| Dairy Products |

| Snacks and Cereals |

| Beverages |

| Others |

| By Type | Natural Color |

| Synthetic Color | |

| By Color | Blue |

| Green | |

| Red | |

| Yellow | |

| Others | |

| By Application | Bakery and Confectionery |

| Dairy Products | |

| Snacks and Cereals | |

| Beverages | |

| Others |

Key Questions Answered in the Report

What is the projected value of the South Africa food colorant market by 2031?

The market is forecast to reach USD 77.37 million by 2031, growing at a 7.18% CAGR.

Which color segment is expected to grow fastest in South Africa?

Blue pigments are projected to register the quickest 8.42% CAGR as stabilized spirulina and fermentation-derived blues gain traction.

Why are synthetic colors still used despite clean-label trends?

Cost sensitivity in value-tier snacks and the superior stability of certain synthetic dyes keep them relevant, yielding an 8.30% CAGR for the synthetic segment through 2031.

Which applications will drive future pigment demand?

Beverages are set to expand fastest at an 7.92% CAGR as ready-to-drink teas, energy beverages, and plant-based milks rely on vibrant, stable hues.

Page last updated on: