Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.08 Billion |

| Market Size (2031) | USD 6.51 Billion |

| Growth Rate (2026 - 2031) | 9.80% CAGR |

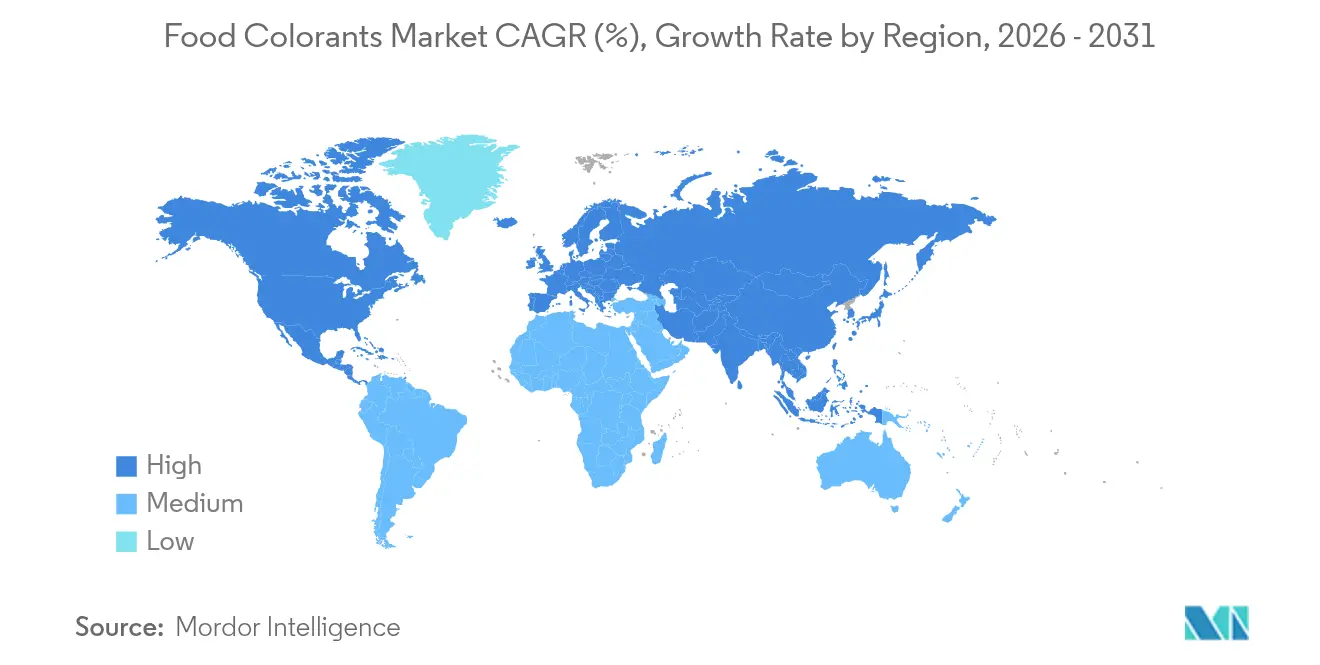

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

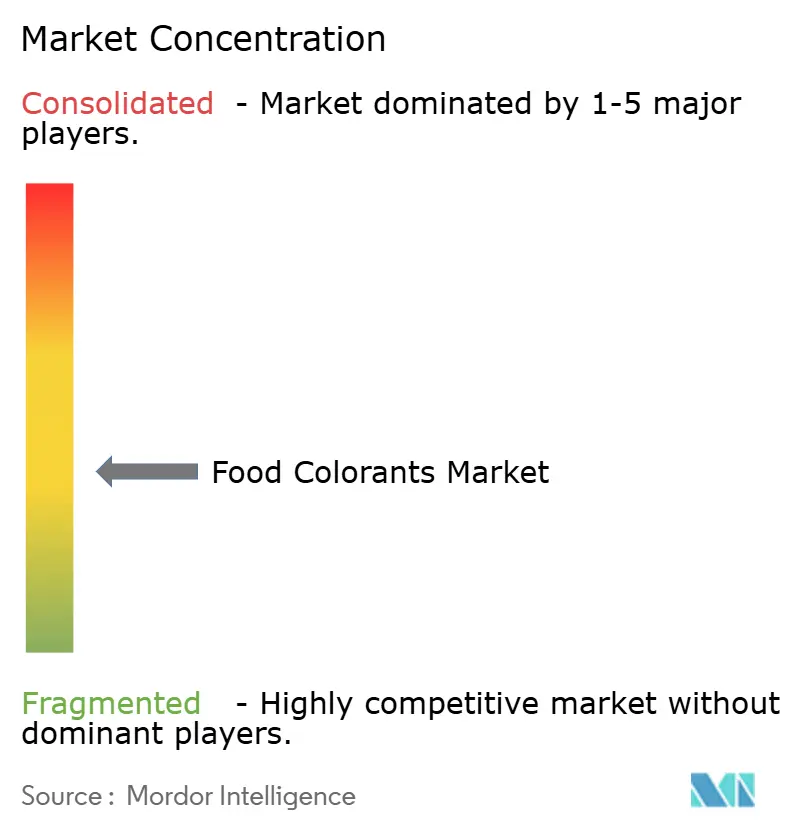

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Food Colorants Market Analysis by Mordor Intelligence

The food colorants market size reached USD 3.68 billion in 2025, stood at USD 4.08 billion in 2026, and is forecast to reach USD 6.51 billion by 2031, expanding at a CAGR of 9.80% during 2026-2031. The market growth is driven by increasing restrictions on synthetic dyes, rising demand for clean-label product reformulations, and new regulatory approvals that expand the availability of plant-based colorants. Europe currently leads the market due to strict regulations on food additives, while the Asia-Pacific region shows significant growth potential, particularly in China and India, where packaged food industries are increasingly adopting natural colorants at a large scale. Advancements in precision fermentation technology and improved extraction methods are reducing the historical cost and performance differences between natural and synthetic colors, enabling manufacturers to compete on quality rather than price alone. The market is experiencing increased competitive activity, with large companies securing upstream raw material supplies while new entrants focus on specialized color development and fermentation-derived ingredients.

Key Report Takeaways

- By product type, natural colorants captured 59.62% of the food colorants market share in 2025, whereas synthetic colorants recorded the highest 10.10% CAGR through 2031.

- By color, red shades led with 31.74% revenue share in 2025; purple shades are forecast to grow at a 10.71% CAGR between 2026-2031.

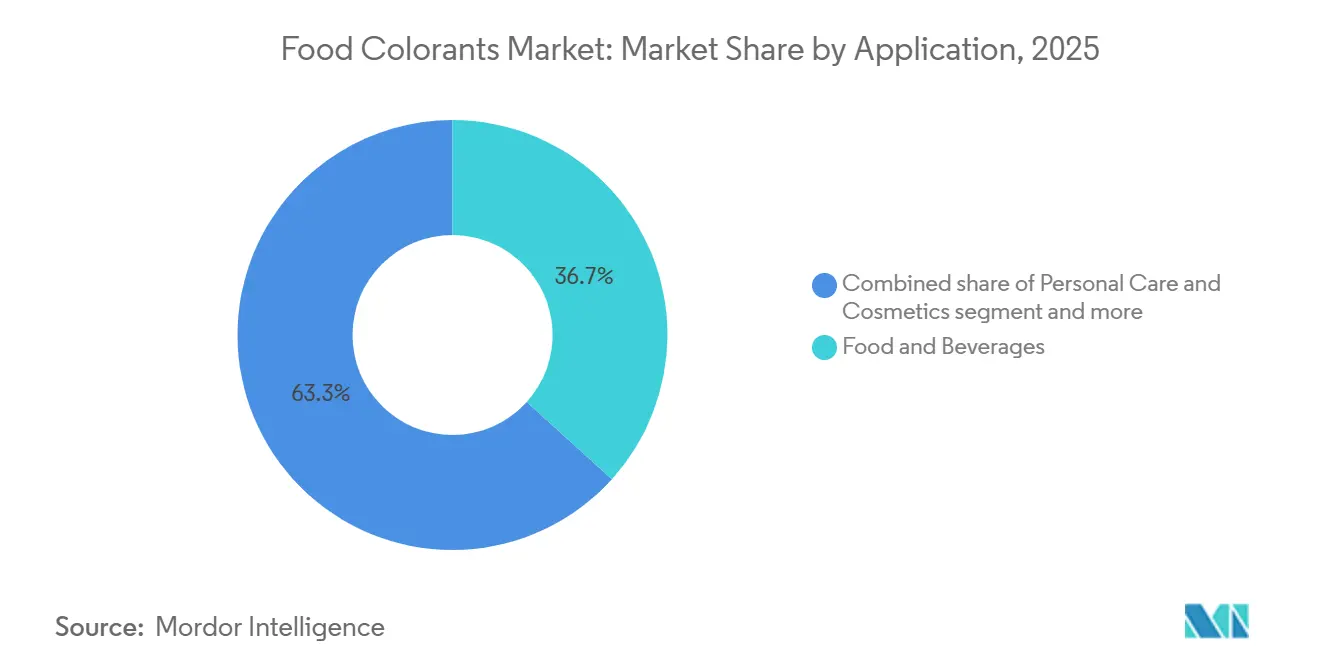

- By application, food and beverages held a 36.71% share of the food colorants market size in 2025, while the personal care and cosmetics segment is advancing at a 10.42% CAGR to 2031.

- By geography, Europe accounted for 33.43% revenue in 2025; Asia-Pacific is projected to post an 11.52% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Food Colorants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in processed foods and beverage industry | +2.3% | Global, with strongest impact in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Natural colorants take center stage in cosmetics | +1.8% | North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Rising demand for organic and clean-label ingredients | +2.1% | Global, led by North America and Western Europe | Short term (≤ 2 years) |

| Regulatory tailwinds expanding natural color approvals | +1.9% | North America primary, Europe secondary impact | Short term (≤ 2 years) |

| Advanced extraction methods improving yield, purity, and sustainability | +1.2% | Global, with research and development centers in North America and Europe | Long term (≥ 4 years) |

| Rising adoption of spirulina-derived blue shades | +0.7% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth in processed foods and beverage industry

The growth in processed food manufacturing drives consistent demand for colorants across various product categories, particularly in emerging markets where urbanization increases convenience food consumption. The expansion of the Asia-Pacific's processed food sector directly influences colorant usage, as manufacturers aim to enhance product appearance while catering to regional taste preferences. According to the Centers for Disease Control and Prevention (CDC) National Health and Nutrition Examination Survey released in August 2025, ultra-processed foods constitute 55.0% of total daily calories consumed by Americans aged 1 and older, with youth aged 1–18 consuming 61.9%[1]Source: National Center for Health Statistics, "Ultra-processed Food Consumption in Youth and Adults: United States, August 2021–August 2023," cdc.gov. This significant consumption of processed and packaged foods maintains a steady demand for food additives, especially colorants, which enhance visual appeal and product differentiation. According to Ayana Bio, 67.0% of consumers in 2023/24 demonstrated willingness to pay premium prices for ultra-processed foods that offer convenience and quality. Natural colorants, including spirulina, beetroot, turmeric, and carotenoids, have increased in popularity as manufacturers respond to clean-label preferences while providing stable coloring solutions for confectionery, beverages, snacks, and ready-to-eat meals. The FDA's 2024 approval of spirulina extract for beverage applications demonstrates regulatory adaptation to support natural colorant use in processed foods[2]Source: Federal Register, "GNT USA, LLC; Filing of Color Additive Petition," federalregister.gov. This trend shows medium-term impact as food processing infrastructure develops gradually, supported by consistent demographic and economic growth across developing regions.

Natural colorants take center stage in cosmetics

The global natural colorants market is experiencing robust growth, driven by increasing demand for ethical and vegan beauty products. Consumer preferences have fundamentally shifted toward cruelty-free, vegan, and ethically sourced cosmetics. This change extends beyond traditional clean-label or organic preferences, emphasizing ethical consumption, sustainability, and transparency in ingredient sourcing. Companies are actively transitioning from synthetic and animal-based pigments to plant-based and mineral-derived colorants in response to consumer awareness about product formulations. Consumer focus on ingredient transparency has intensified, particularly regarding vegan and cruelty-free products. A June 2024 Naris Cosmetics survey found that 46% of Japanese consumers thoroughly review ingredient labels before making purchasing decisions[3]Source: Naris Cosmetics, naris.co.jp. The cosmetics market is experiencing a substantial transformation through the rapid expansion of vegan beauty products, which eliminate all animal-derived ingredients, including carmine (E120) from cochineal insects. This development has accelerated the adoption of alternative pigments sourced from plants, fruits, and algae. As ethical beauty transitions from a niche segment to mainstream, natural colorants are becoming essential components for future cosmetic product development and innovation.

Rising demand for organic and clean-label ingredients

The global demand for organic and clean-label products drives growth in the natural colorants market. Consumer preference for transparent ingredient lists influences product reformulation across food categories. This trend reflects shifting consumer preferences across various industries, including packaged goods and healthcare, with an emphasis on transparency, minimal processing, ethical sourcing, and the elimination of synthetic chemicals. As consumers examine product labels more closely, manufacturers are replacing synthetic dyes with natural alternatives derived from vegetables, minerals, fruits, and microbial sources. According to data from the International Federation of Organic Agriculture Movements and the Research Institute for Organic Agriculture (FiBL), the United States accounted for approximately 43% of global organic retail sales in 2023, while China contributed around 9%. The clean-label movement emphasizes ingredient transparency, establishing colorants as indicators of product purity and quality rather than mere aesthetic elements. This shift from synthetic to natural colorants reflects the industry's commitment to creating transparent, ethical, and health-conscious products.

Regulatory tailwinds expanding natural color approvals

Regulatory momentum is increasingly favoring the adoption of natural colorants in the food industry, creating significant growth opportunities for manufacturers. Government agencies and food safety authorities worldwide are prioritizing the reduction of synthetic, petroleum-based dyes due to health and sustainability concerns. The U.S. Food and Drug Administration approved three new color additive petitions in 2025, supporting efforts to phase out petroleum-based dyes. The approved additives include Galdieria extract blue from red algae, butterfly pea flower extract for blue-purple colors, and calcium phosphate for white applications. FDA confirmed the agency's commitment to accelerating the transition away from synthetic dyes, with U.S. food manufacturers pledging to eliminate petroleum-based colorants by the end of 2026. These regulatory developments reflect global momentum toward the approval of natural colorants, with the FDA's expedited review process providing manufacturers with viable alternatives to synthetic dyes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulations on synthetic colorants | -1.4% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Stability and performance limitations for natural colorants | -1.8% | Global, particularly challenging in tropical climates | Medium term (2-4 years) |

| High cost of natural pigments | -1.2% | Global, most pronounced in price-sensitive markets | Short term (≤ 2 years) |

| Climate-driven crop supply volatility | -0.9% | Global, concentrated in agricultural regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent regulations on synthetic colorants

Growing consumer awareness of health and environmental issues has led regulatory bodies to tighten controls on synthetic dyes and colorants due to their health risks and environmental impact. These regulations are driving manufacturers in the food, beverage, cosmetic, and pharmaceutical industries to adopt natural colorants. Natural alternatives offer safety benefits and environmental advantages while meeting consumer demands for clean-label products. This shift in regulatory landscape and consumer preferences continues to create substantial demand for natural and sustainable colorants across various sectors. The U.S. Food and Drug Administration (FDA) requires batch certification for artificial colorants to verify their identity and specifications. However, colorants derived from natural sources, including vegetables, minerals, and animals, are exempt from this certification requirement. These certification-exempt natural colorants include annatto extract (yellow), dehydrated beets (bluish-red to brown), caramel (yellow to tan), beta-carotene (yellow to orange), and grape skin extract (red or purple). This regulatory leniency has significantly strengthened the market for natural food colorants in the region. In October 2023, consumer advocacy groups intensified pressure on the FDA to ban synthetic red No. 3 food coloring, following California's legislative action that prohibited the dye's use due to its established connection with hyperactivity reactions in children.

Stability and performance limitations for natural colorants

Natural colorants have significant stability limitations when exposed to various environmental factors such as heat, light, and pH variations, which substantially restricts their applications compared to synthetic alternatives. These inherent limitations frequently require extensive product reformulation processes and can significantly affect the overall shelf life of products. For example, phycocyanin's stability can be enhanced through the incorporation of specific food preservatives like sorbitol and sucrose, though this approach increases both formulation complexity and associated production costs. Research and development teams across the industry continue to address these fundamental challenges through advanced technologies, including sophisticated encapsulation methods and innovative stabilizing agents. Companies such as Oterra have made substantial progress in this area by developing specialized ultrafine milled powders that provide more intense color shades at lower dosages, effectively minimizing stability risks while maintaining the desired color intensity in final applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Natural Colors Drive Market Transformation

Natural color commands 59.62% market share in 2025, reflecting consumer preference shifts and regulatory momentum toward plant-based alternatives, while synthetic color segments paradoxically exhibit the fastest growth at 10.10% CAGR through 2031 as manufacturers stockpile supplies before regulatory phase-outs. In the natural color segment, spirulina has shown significant growth following FDA approvals for use in beverage applications, while carotenoids continue to benefit from established supply chains and reliable stability profiles. Anthocyanins face formulation challenges in high-pH applications but maintain strong demand in dairy and confectionery products. Curcumin benefits from dual functionality as both a colorant and a functional ingredient, while carmine faces ethical concerns from vegan consumers despite superior performance characteristics.

Food manufacturers are stockpiling supplies of azo dyes and brilliant blue FCF ahead of impending regulatory restrictions, driving an acceleration in the synthetic segment's growth. This stockpiling behavior, aimed at mitigating potential supply chain disruptions and ensuring production continuity, creates temporary market distortions that obscure a more profound, long-term shift towards natural alternatives. Meanwhile, the FDA's expedited approval process for natural colors offers a competitive edge to companies boasting strong regulatory expertise, efficient compliance mechanisms, and a diverse product lineup, enabling them to adapt swiftly to evolving market demands.

By Color: Red Dominance Faces Purple Innovation

In 2025, red colorants command a leading 31.74% market share, thanks to their widespread use in various food categories and strong consumer acceptance. These colorants are extensively utilized in products such as sauces, beverages, and confectionery, where their vibrant hue and stability make them a preferred choice among manufacturers. Purple colorants, especially in premium beverages and confectionery, are on the rise, boasting the highest growth rate at a 10.71% CAGR projected through 2031. Their increasing adoption is driven by their ability to provide unique shades and functional benefits, aligning with the growing demand for premium and visually appealing products. Blue colorants are gaining popularity, driven by spirulina-based innovations and FDA-approved algae-derived alternatives, which offer natural and sustainable options for manufacturers. Green colorants are thriving, leveraging chlorophyll-based solutions that cater to the growing demand for clean labels, particularly in health-focused food and beverage products. Meanwhile, yellow colorants grapple with regulatory hurdles, particularly synthetic variants like Tartrazine, paving the way for natural alternatives such as turmeric to seize market opportunities. Turmeric-based yellow colorants are increasingly favored for their natural origin and additional health benefits, such as anti-inflammatory properties.

The surge in purple colorants is largely attributed to their rising prominence in premium beverages. Here, anthocyanin-based colors stand out, offering pH-responsive traits that meld visual allure with functional advantages. These properties allow manufacturers to create products that not only look appealing but also provide added value, such as antioxidant benefits. This trend resonates with consumers' growing preference for natural ingredients that don't compromise on functionality. Moreover, strides in betacyanin stabilization via emulsion technologies not only enhance color retention but also expand application horizons, enabling their use in a wider range of products, including dairy and plant-based alternatives. Today's manufacturers are prioritizing colors based on stability, regulatory adherence, and functional benefits tailored to specific product positioning, rather than solely on aesthetics. This shift reflects a more strategic approach to colorant selection, ensuring that products meet both consumer expectations and regulatory standards.

By Application: Food Dominance with Cosmetics Acceleration

Food and beverages applications hold a 36.71% market share in 2025, supported by well-established supply chains and regulatory frameworks, while the personal care and cosmetics segment exhibits the highest growth rate at 10.42% CAGR through 2031, propelled by the clean beauty movement and consumer willingness to pay premium prices. In food and beverages, bakery and confectionery applications require heat-stable colorants to preserve vibrancy during processing, while dairy products need pH-stable solutions for protein-rich environments. The beverages category benefits from FDA approvals for spirulina and algae-based blue colorants, expanding natural options. Snacks and cereals manufacturers face immediate reformulation requirements due to the synthetic dyes.

Pharmaceuticals and dietary supplements offer new market opportunities as regulatory focus expands from food to medicinal applications, including European Union reform proposals for color additives in medicines. The pharmaceutical segment shows growth potential due to increased examination of synthetic additives in children's medications and rising consumer demand for natural alternatives in supplements. The application segmentation now encompasses requirements beyond basic coloration, as manufacturers seek colorants that deliver additional benefits such as antioxidant properties or enhanced stability. The pharmaceutical segment's expansion reflects the broader industry shift toward natural ingredients and functional benefits in medical and supplement formulations.

Geography Analysis

Europe holds a 33.43% market share in 2025, driven by established natural colorant regulations and robust supply chains for plant-based alternatives, maintaining its position as the global market leader. Germany and France demonstrate leadership in regulatory compliance and premium positioning, while the United Kingdom maintains strong demand despite Brexit-related supply chain adjustments. Italy emphasizes traditional food authenticity in line with natural colorant adoption, and Spain leverages its agricultural production capabilities for colorant extraction, further strengthening the regional market dynamics.

Asia-Pacific demonstrates the highest growth rate at 11.52% CAGR through 2031, supported by China's new standards for plant-based coloring foods introduced in May 2025 and India's comprehensive public awareness campaign on synthetic-dye health effects. The region's substantial processed-food industry requires extensive sourcing of curcumin, spirulina, and vegetable-juice concentrates to meet growing demand. Japanese confectionery manufacturers are transitioning from carmine to purple-sweet-potato extracts to accommodate vegan preferences, while Southeast Asian fruit exporters are incorporating color-extraction facilities to reduce waste and enhance export value in the global market.

North America shows significant market development as the FDA's timeline to remove petroleum-based dyes drives major food brands to secure alternatives, creating substantial market opportunities. U.S. beverage manufacturers initiated production trials of Galdieria extract blue shortly after approval, demonstrating the immediate impact of regulatory changes on market adoption. Under the Canada-United States-Mexico Agreement, Canada is expected to align with U.S. colorant restrictions, facilitating cross-border certification processes and enhancing regional market integration.

Competitive Landscape

The food colorants market is moderately fragmented, allowing both established multinationals and startups to carve out market share through unique offerings and tech innovations. Sensient Technologies, a market leader, boasts an 11.8% revenue growth in its Color Group for 2024, driven by its integrated supply chains, regulatory expertise, and a focus on delivering high-quality, innovative solutions to meet evolving consumer demands. As companies double down on innovation and strategic positioning, the competitive landscape is in flux, with players striving to differentiate themselves through advanced technologies and sustainable practices.

Givaudan's acquisition of DDW underscores the ongoing industry consolidation, bolstering Givaudan's natural color portfolio and market foothold. This acquisition highlights the growing importance of natural colorants in the market, as consumers increasingly prefer clean-label and plant-based products. Meanwhile, up-and-coming firms like Phytolon are attracting significant venture capital to pioneer precision fermentation technologies, challenging the norms of traditional extraction methods. These technologies not only enhance production efficiency but also align with sustainability goals, addressing the rising demand for environmentally friendly solutions. Firms that clinch FDA approval for novel natural colorants can solidify their market stance ahead of larger rivals, gaining a pronounced edge in this ever-evolving arena.

Fermentation-based production is at the forefront of technological progress, boasting benefits like consistent quality, scalable output, and a smaller environmental footprint than traditional agricultural methods. Michroma and Chromologics are at the helm, crafting fermentation-derived colorants with superior stability and performance. These advancements are reshaping the industry by enabling manufacturers to meet stringent quality standards while reducing reliance on resource-intensive agricultural processes. Such breakthroughs are not only redefining production standards but also elevating industry benchmarks for quality, sustainability, and innovation.

Food Colorants Industry Leaders

-

Sensient Technologies Corporation

-

Novonesis (Chr. Hansen Holding A/S)

-

Givaudan (Naturex)

-

Archer-Daniels-Midland (ADM)

-

DSM Firmenich

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: GNT Group B.V. introduced EXBERRY Shade Vivid Orange, a clean-label offering derived from non-GMO paprika. This innovative product imparts an orange hue without resorting to traditional paprika oleoresins or extracts. Its versatility spans confectionery, dairy, bakery, and plant-based meat sectors, facilitating clean-label declarations.

- July 2024: Givaudan Sense Color launched Amaize orange-red. Amaize line of corn-based anthocyanin colors has a bright orange-red shade that closely matches Red 40 in acidic applications. It is available in powder and liquid forms and is suitable for low-pH applications, including beverages, confections, fruit preps, ice lollies, sorbets, and snack seasonings.

- January 2024: Phytolon and Ginkgo Bioworks achieved a milestone in their collaboration by developing fermentation-based natural food colorants. The companies created two strains that produce betalains, which are natural pigments that generate red, pink, and yellow colors. This development enables beverage manufacturers to access sustainable and scalable natural food colorant solutions.

Global Food Colorants Market Report Scope

Food colorants are substances used to impart, restore, or enhance the color of food and beverages. The food colorants market is segmented by product type, color, application, and geography. By product type, the market is segmented into natural color and synthetic color. By color, the market is segmented into blue, green, red, yellow, purple, orange, pink, and others. By application, the market is segmented into food and beverages, personal care and cosmetics, pharmaceuticals, dietary supplements, and other applications. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. The report offers market size and forecast in value terms in USD million and volume terms in tons for all the above segments.

Product Type

| Natural Color | Anthocyanins |

| Carotenoids | |

| Curcumin | |

| Carmine | |

| Spirulina | |

| Other Types | |

| Synthetic Color | Azo Dyes (Tartrazine, Sunset Yellow, etc.) |

| Brilliant Blue FCF | |

| Others |

Color

| Blue | Green |

| Red | |

| Yellow | |

| Purple | |

| Orange | |

| Pink | |

| Others |

Application

| Food and Beverages | Bakery and Confectionery |

| Dairy Products | |

| Snacks and Cereals | |

| Beverages | |

| Others | |

| Personal Care and Cosmetics | |

| Pharmaceuticals | |

| Dietary Supplements | |

| Other Applications |

Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Qatar | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Rest of Middle East and Africa |

| Product Type | Natural Color | Anthocyanins |

| Carotenoids | ||

| Curcumin | ||

| Carmine | ||

| Spirulina | ||

| Other Types | ||

| Synthetic Color | Azo Dyes (Tartrazine, Sunset Yellow, etc.) | |

| Brilliant Blue FCF | ||

| Others | ||

| Color | Blue | Green |

| Red | ||

| Yellow | ||

| Purple | ||

| Orange | ||

| Pink | ||

| Others | ||

| Application | Food and Beverages | Bakery and Confectionery |

| Dairy Products | ||

| Snacks and Cereals | ||

| Beverages | ||

| Others | ||

| Personal Care and Cosmetics | ||

| Pharmaceuticals | ||

| Dietary Supplements | ||

| Other Applications | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Qatar | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the food colorants market?

The market is valued at USD 4.08 billion in 2026 and is projected to reach USD 6.51 billion by 2031.

Which region grows fastest for food colorants?

Asia-Pacific shows the highest momentum with an 11.52% forecast CAGR, fueled by China and India’s processed-food expansion.

Which color segment leads sales today?

Red shades remain dominant, holding 31.74% of 2025 revenue, but purple hues grow fastest.

How will FDA regulations influence future demand?

The scheduled 2026 phase-out of petroleum-based dyes forces all U.S. manufacturers to adopt natural alternatives, sharply lifting demand during 2026-2028.

Page last updated on: