South Africa Cross Border Road Freight Transport Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

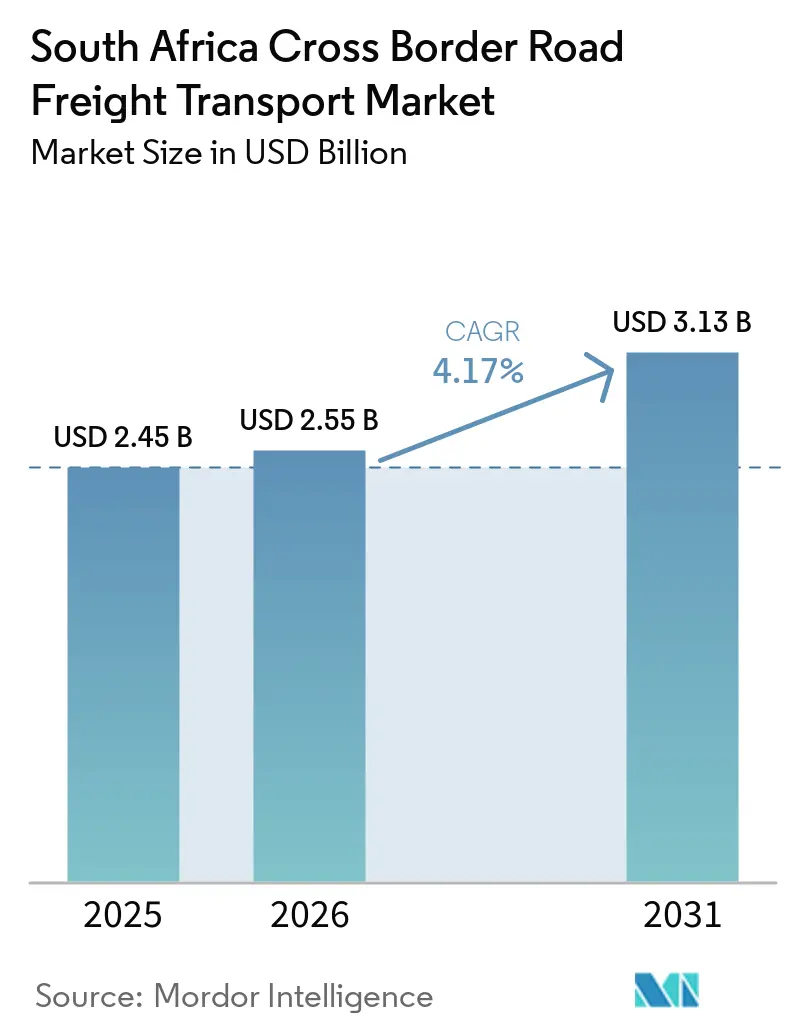

| Base Year Market Size (2025) | USD 2.45 Billion |

| Market Size (2026) | USD 2.55 Billion |

| Market Size (2031) | USD 3.13 Billion |

| Growth Rate (2026 - 2031) | 4.17% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Cross Border Road Freight Transport Market Analysis by Mordor Intelligence

The South Africa cross-border road freight transport market size is expected to increase from USD 2.45 billion in 2025 to USD 2.55 billion in 2026, and reach USD 3.13 billion by 2031, growing at a CAGR of 4.17% over 2026-2031.

Structural shifts in regional trade corridors, persistent rail underperformance, and faster digital customs clearance under the AfCFTA framework underpin the growth outlook. Miners continue to divert chrome, copper, and platinum-group metal traffic to trucks as Transnet struggles with cable theft and locomotive shortages. Parallel demand expansion comes from e-commerce and FMCG distributors that now embed next-day cross-border delivery promises into their service offerings. Infrastructure upgrades to the Kazungula Bridge and the Beitbridge public-private partnership compress border dwell time, lift fleet productivity, and open the door to higher-frequency short-haul runs. Rounding out the positive forces, one-stop border posts and automated AfCFTA certificates trim compliance costs for small and medium-sized carriers.

Key Report Takeaways

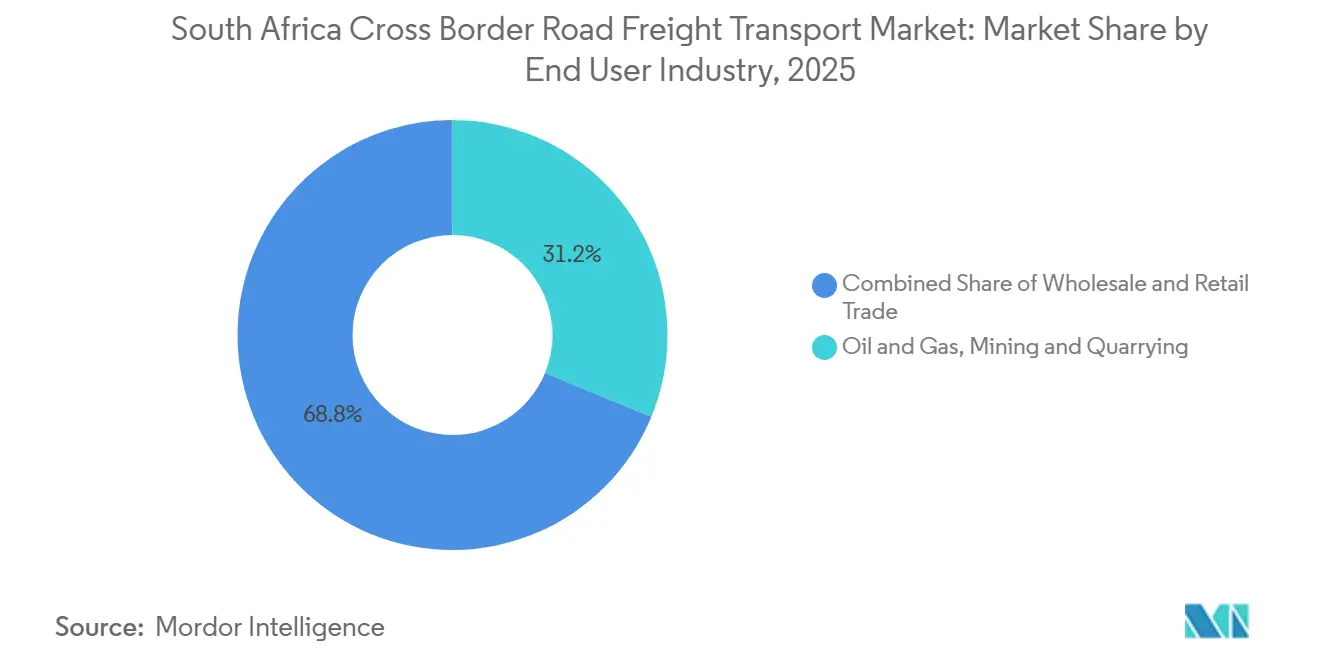

- By end-user industry, oil and gas, mining, and quarrying accounted for 31.25% of the South Africa cross border road freight transport market share in 2025; wholesale and retail trade is projected to expand at a 4.82% CAGR through 2031.

- By truckload specification, full-truckload accounted for 80.7% of the South Africa cross border road freight transport market size in 2025; less-than-truckload is forecast to grow at a 4.94% CAGR over 2026-2031.

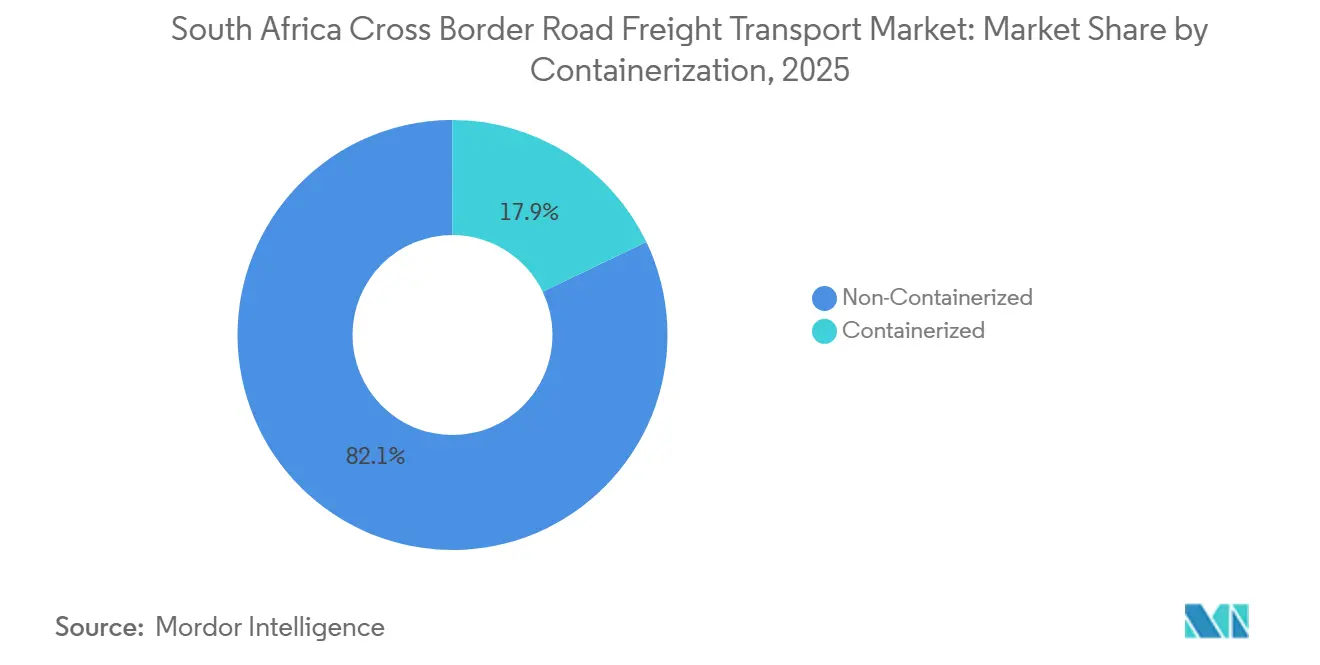

- By containerization, non-containerized freight accounted for 82.11% of the South Africa cross border road freight transport market share in 2025; containerized traffic is expected to rise at a 4.70% CAGR to 2031.

- By distance, long-haul moves captured 67.34% of the South Africa cross border road freight transport market size in 2025; short-haul lanes are poised to accelerate at a 4.99% CAGR through 2031.

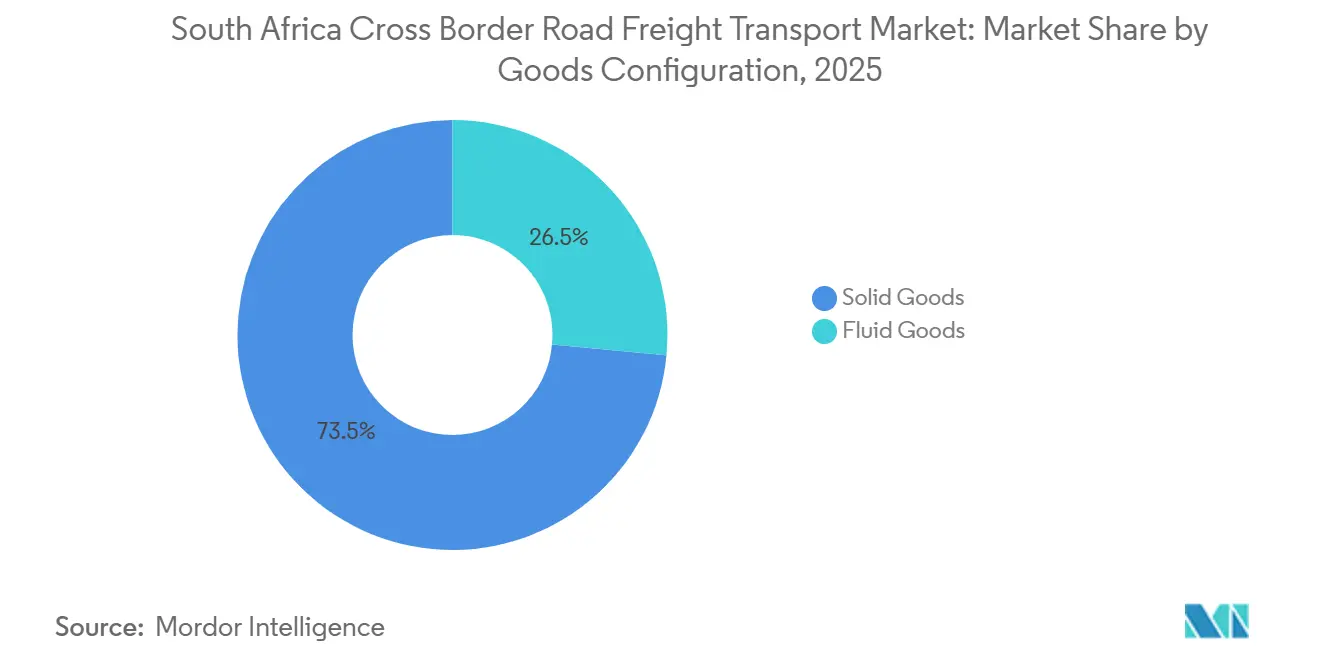

- By goods configuration, solid goods commanded 73.5% of the South Africa cross border road freight transport market share in 2025; fluid goods are set to expand at a 4.65% CAGR over the forecast period.

- By temperature control, non-refrigerated freight accounted for 95.03% of the South Africa cross border road freight transport market size in 2025; temperature-controlled consignments are projected to grow at a 4.78% CAGR through 2031.

- By trade region, South Africa accounted for 55.61% of the South Africa cross border road freight transport market size in 2025 from landlocked SADC countries. Coastal countries are expected to drive future growth with a CAGR of 5.39%, indicating a shift toward diversified regional trade corridors.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Africa Cross Border Road Freight Transport Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Regional Mining Exports via Road | 1.2% | SADC Landlocked (Zambia, Zimbabwe, Botswana); spillover to Mozambique corridors | Medium term (2-4 years) |

| E-Commerce and FMCG Demand for Parcel-Grade Cross-Border Delivery | 0.8% | Gauteng-SADC trade lanes; KwaZulu-Natal to Maputo corridor | Short term (≤ 2 years) |

| Modal Shift from Rail to Road Amid Rail-System Failures | 1.0% | National (South Africa), with acute impact on coal/manganese export routes | Short term (≤ 2 years) |

| Corridor Infrastructure Upgrades (Kazungula Bridge, Beitbridge OSBP) | 0.6% | Zambia-Botswana-Namibia corridor; Zimbabwe-South Africa Beitbridge crossing | Medium term (2-4 years) |

| Telematics-Driven Productivity Gains for Medium/Heavy Fleets | 0.4% | National fleet operators; cross-border long-haul segments | Long term (≥ 4 years) |

| AFCFTA-Driven Harmonization of Customs and Permits | 0.5% | SADC region; early gains in SACU member states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Regional Mining Exports via Road

After outages at Transnet reduced the utilization of the manganese line, chrome and copper shipments have increasingly turned to road transport. This shift comes at a cost, with miners paying a 15-20% premium for road transport to avoid demurrage fees on vessels. In 2024, a record 14.3 million tons of chrome were exported via truck, underscoring the road's pivotal role in the transport landscape. Thanks to the Kazungula one-stop post, Zambians can now reach Gauteng smelters in just three days, bolstering the cross-border road freight market with South Africa. Additionally, the rising use of ISO tanks for mineral slurry further cements the road's significance, even as funding for rail rehabilitation struggles to meet its execution targets[1]“Trade Statistics Release, December 2024.” 2024, South African Revenue Service, sars.gov.z.

South Africa's road freight market has also seen a surge in demand for specialized vehicles, including side-tippers and flatbeds, to accommodate the growing volume of mineral exports. The increased reliance on road transport has led to higher wear and tear on infrastructure, prompting calls for improved road maintenance and investment. Furthermore, the shift to road transport has created opportunities for logistics companies to expand their fleet sizes and optimize supply chain operations. Despite these developments, the rail sector continues to face challenges, with delays in infrastructure upgrades and limited capacity hindering its competitiveness against road transport.

E-Commerce and FMCG Demand for Parcel-Grade Cross-Border Delivery

By 2025, South Africa's retail trade momentum remained strong, building on the 7.7% year-on-year growth recorded in late 2024. E-commerce penetration continued to expand across urban and peri-urban markets, driving sustained growth in parcelized cross-border shipments, particularly along high-frequency corridors such as those linking Durban and Gauteng to Maputo and Mbabane. Leading integrators, including DHL Group, have enhanced parcel-sorting and distribution capabilities across the SADC region, solidifying their position in time-sensitive logistics segments. Simultaneously, the ongoing digitalization of customs processes under the African Continental Free Trade Area has improved clearance efficiency at key land borders, enabling faster turnaround times and supporting next-day or near-next-day delivery models for cross-border parcels. As a result, less-than-truckload (LTL) and parcel logistics are growing faster than traditional bulk freight, emerging as a significant structural driver of South Africa's cross-border road freight transport market.

The regional cross-border e-commerce market is projected to grow at an estimated ~8–9% CAGR during the forecast period, driven by increasing internet penetration and rising consumer demand. Logistics providers are adopting advanced technologies such as real-time tracking, route optimization, and fleet telematics to enhance delivery reliability and asset utilization. Government investments in road infrastructure and corridor upgrades are expected to reduce transit times and improve freight capacity along major SADC trade routes. Additionally, demand for temperature-controlled logistics is increasing, particularly for pharmaceuticals, vaccines, and perishable goods, creating high-margin opportunities for operators with compliant cold-chain capabilities. Collectively, these developments are accelerating the shift toward higher-frequency, smaller-volume shipments, reinforcing the long-term growth trajectory of cross-border road freight in Southern Africa[2]“Budget Review.” 2024, South African National Treasury, treasury.gov.za.

Modal Shift from Rail to Road Amid Rail-System Failures

Despite a ZAR 127 billion (USD 7.75 billion) recovery plan, Transnet's volumes lag 30-40% behind historic peaks, forcing shippers to turn to trucking. While private rail entrant Traxtion placed an order for 46 locomotives, it still awaits regulatory clarity on network access. South Africa's rail infrastructure challenges have led to increased logistics costs, with trucking now accounting for over 80% of freight movement in certain corridors. In a move underscoring confidence in the road's continued prominence in South Africa's cross-border road freight transport market, Super Group channeled ZAR 7.47 billion (USD 0.45 billion) from a leasing divestiture straight into its cross-border fleets.

Additionally, the cross-border road freight market is projected to grow steadily over the forecast period, driven by rising demand for efficient, flexible logistics solutions. The South African government has also announced plans to attract private investment in rail infrastructure, aiming to improve network efficiency and reduce dependency on road freight. Furthermore, the increasing adoption of digital freight platforms is expected to enhance operational efficiency and transparency in the logistics sector.

Corridor Infrastructure Upgrades (Kazungula Bridge, Beitbridge OSBP)

Thanks to the Kazungula upgrade, average dwell time plummeted from 12 hours to under 4, boosting round-trip asset turns on the Johannesburg-Lusaka lanes by 40%. The National Treasury's ZAR 12.5 billion (USD 0.76 billion) PPP allocates ZAR 4.2 billion (USD 0.25 billion) to Beitbridge, focusing on scanner redundancy and the establishment of new holding yards. These expedited border processes not only bolster short-haul frequencies but also enhance e-commerce parcel strategies, driving up utilization in South Africa's cross-border road freight transport market.

The upgrade has enhanced supply chain efficiency, lowered transit costs, and reduced delays, which are essential for time-sensitive goods. The improved infrastructure is anticipated to significantly contribute to the consistent growth of the cross-border road freight transport market during the forecast period. Additionally, upgraded border facilities have improved the reliability of freight schedules, decreased congestion at critical checkpoints, and enabled smoother trade flows, all of which are crucial for sustaining competitiveness in regional and international markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic Port and Border Congestion Raising Transit Uncertainty | -0.9% | Beitbridge (South Africa-Zimbabwe); Lebombo (South Africa-Mozambique); Durban port | Short term (≤ 2 years) |

| Security Risks: Hijacking, Cargo Theft, Driver Shortages | -0.7% | Gauteng (56% of incidents); Eastern Cape; Mpumalanga; KwaZulu-Natal | Short term (≤ 2 years) |

| Emerging Carbon-Pricing and ESG Pressure on Road Haulage | -0.3% | National (South Africa); potential spillover to SACU member states | Long term (≥ 4 years) |

| Diversion of Copperbelt Cargo to Lobito/Beira Corridors | -0.6% | Zambia-DRC Copperbelt; Angola Lobito route; Mozambique Beira/Maputo routes | Medium term (2- 4 years) |

| Source: Mordor Intelligence | |||

Chronic Port and Border Congestion Raising Transit Uncertainty

In 2024, Beitbridge, which typically handles over 15,000 trucks per month, experienced a 30-40% spike in dwell times due to diversions. This surge compelled reroutes through Lebombo, leading to inflated costs. Meanwhile, trucks at Durban berths occasionally wait up to 72 hours, causing cascading delays further inland. The South African cross-border road freight transport market also faces challenges, including inconsistent infrastructure quality, regulatory bottlenecks, and fluctuating fuel prices, which further strain operational efficiency.

Additionally, the market is grappling with driver shortages and rising labor costs, which are impacting delivery timelines and increasing operational expenses. While a 2026 border-post PPP hints at a 40% boost in processing speed by 2028, the current unpredictability casts a shadow on service reliability in South Africa's cross-border road freight transport market[3]“Quarterly Bulletin, September 2024.” 2024, South African Reserve Bank, sarb.co.za.

Security Risks: Hijacking, Cargo Theft, Driver Shortages

Security risks, labor availability challenges, border crossing inefficiencies, and cost pressures collectively constrain South Africa’s cross-border road freight market. Security concerns, particularly along high-density corridors connecting Gauteng to neighboring countries, remain a significant issue. Truck hijackings and cargo theft undermine operator confidence, especially for smaller fleets that lack the resources for advanced security systems. To mitigate these risks, companies increasingly deploy escorts, tracking technologies, and stricter route controls, which elevate operational complexity and compress margins, particularly in the less-than-truckload segment. Labor shortages further exacerbate these challenges, as cross-border driving roles are difficult to fill due to safety concerns, extended transit durations, and regulatory requirements across multiple jurisdictions. This reliance on experienced drivers limits operators' ability to scale capacity efficiently.

Operational inefficiencies at border crossings and cost pressures from fuel price volatility and fleet maintenance add to the market's difficulties. Despite modernization efforts, congestion, documentation delays, and inconsistent enforcement practices disrupt transit schedules, reducing asset utilization and complicating the maintenance of reliable delivery timelines, particularly for time-sensitive cargo. Additionally, the operational burden of maintaining aging fleets, which are prone to breakdowns and inefficiencies, increases downtime and maintenance costs. These combined factors continue to challenge profitability and service reliability, reinforcing barriers to entry and slowing innovation within the cross-border road freight market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User Industry: Mining Anchors Volume, Retail Drives Growth

The oil and gas, mining, and quarrying sectors accounted for 31.25% of the South Africa cross border road freight transport market size in 2025. However, the wholesale and retail trade sector is projected to grow at the fastest rate of 4.82% through 2031, driven by the expansion of e-commerce platforms facilitating parcelized shipments to SADC neighbors. While mining will retain its position as the leader in absolute tonnage, its growth rate is expected to decelerate as rail reliability improves. Retailers leveraging AfCFTA duty relief and automated customs clearance processes are redefining service expectations in the South African cross border road freight transport market.

In 2024, sustained chrome flows, totaling 14.3 million tons transported by road, will keep dedicated tippers fully utilized. Simultaneously, facilities such as the Takealot Durban hub and DHL’s parcel-sorting centers underscore a structural shift toward smaller, high-frequency consignments. Over the forecast period, retail and FMCG volumes are anticipated to increase their share of the South Africa Cross Border Road Freight Transport Market, utilizing spare capacity made available by the stabilization of mining export volumes[4]“Industrial Policy Action Plan / Trade Reports.” 2024, Department of Trade, Industry and Competition, thedtic.gov.za.

By Truckload Specification: LTL Gains as Shipments Fragment

In 2025, full-truckload (FTL) accounted for 80.7% of the South Africa cross border road freight transport market size in 2025. Meanwhile, less-than-truckload (LTL) services grew at a 4.94% CAGR, driven by surges in online retail and pharmaceutical distribution. The automation of AfCFTA certificates, coupled with DHL's 2026 acquisition of Vital, has fostered tighter consolidation networks, enhancing the feasibility of LTL services even at secondary borders. Additionally, the adoption of digital freight platforms has streamlined operations, reducing transit times and improving cost efficiency for LTL shipments.

FTL services remain dominant for transporting copper concentrate and ferrochrome, as the risk of contamination necessitates dedicated trailers. However, with the growth in parcel deliveries, the market is diversifying, leading to a gradual reduction in FTL's share in South Africa's cross-border road freight transport sector. Furthermore, the increasing demand for temperature-controlled logistics, particularly for perishable goods, is expected to further drive the adoption of LTL services in the region.

By Containerization: ISO Boxes Gain in Mining and Retail

In 2025, non-containerized cargo accounted for 82.11% the South Africa cross border road freight transport market size in 2025. However, containerized traffic is set to grow at an annual rate of 4.70%. This growth is driven by miners increasingly adopting ISO tanks for safer, more efficient material transport, and by retailers leveraging refrigerated shipments to meet the rising demand for perishable goods. Grindrod’s Cape Town depot, with a 5,000-TEU capacity and 240 reefer plugs, serves as a prime example of how cross docking synergies can reduce diesel dependency and enhance operational efficiency. Such developments are expected to play a pivotal role in reshaping market dynamics. While bulk chrome and fuel continue to underpin the dominance of non-containerized cargo, the growing emphasis on intermodal efficiencies is likely to shift the balance.

The integration of containerized solutions into the South African cross-border road freight transport market is anticipated to improve cost-effectiveness and streamline logistics. This trend underscores the growing importance of containerized traffic in meeting evolving market demands and enhancing overall supply chain performance.

By Distance: Short Haul Accelerates on Border Efficiency

In 2025, long-haul accounted for 67.34% of the South Africa cross border road freight transport market size in 2025. However, as border dwell times decrease, short-haul is witnessing the fastest growth at 4.99%. The reduction in border delays has enabled fleets to optimize operations, allowing for more frequent rotations between key routes such as Gauteng-Maputo and Cape Town-Windhoek. This shift is significantly boosting asset productivity and operational efficiency for transport providers in the region.

While long-haul continues to dominate the market, primarily due to the importance of Copperbelt-Durban routes, it is gradually losing incremental market share to short-haul sectors. The growing preference for high-frequency short-haul routes highlights the evolving dynamics of South Africa's cross-border road freight transport market, driven by improved border processes and the need for faster delivery cycles.

By Goods Configuration: Solid Dominates, Fluid Steadily Expands

Chrome and maize spearheaded the delivery of solid goods, accounting for 73.55% of the South Africa cross border road freight transport market size in 2025. Solid goods continue to dominate the South Africa cross-border road freight transport market, driven by consistent demand for these commodities. The segment's performance highlights its critical role in supporting regional trade and economic activities.

Meanwhile, fluid goods, predominantly diesel and chemicals, are projected to grow by 4.65%, driven by heightened fuel demand at remote mines. In this market, price volatility has spurred the adoption of telematics-aided routing, helping to mitigate fuel costs and bolster momentum in the fluid segment. This technological integration is expected to enhance operational efficiency and sustain growth in the fluid goods category.

By Temperature Control: Cold Chain Emerges as Premium Segment

In 2025, non-temperature-controlled freight accounted for 95.03% of the South Africa cross border road freight transport market size in 2025, driven by mining, construction materials, and ambient general cargo, while temperature-controlled freight is forecast to grow at 4.78% during 2026-2031, supported by expanding pharmaceutical, biologic, and perishable food distribution networks across SADC borders. Investments like DHL's EUR 500 million (USD 550 million) healthcare logistics infrastructure and Grindrod's 5,000-TEU container depot with 240 reefer plugs in Cape Town highlight the growing focus on cold-chain logistics. Infrastructure upgrades, such as the Kazungula one-stop border post reducing dwell times to under four hours, enable South African exporters to reach Lusaka and Harare within 48 hours of harvest, supporting premium pricing. The South African Revenue Service's November 2025 automation of AfCFTA certificate-of-origin processing further reduced customs clearance times for qualifying parcels to under 12 hours, minimizing cold-chain risks. While non-temperature-controlled freight will remain dominant through 2031 due to its role in transporting mining and construction cargo, its growth will slow as demand for temperature-controlled logistics rises to meet regulatory standards and ensure product integrity.

Geography Analysis

SADC landlocked nations dominate volumes with 55.61% of market size in 2025, largely due to Zambian copper and Zimbabwean chrome trucked via Beitbridge. Botswana gains from the efficiencies of the Kazungula corridor, while Lesotho and Eswatini ride on proximity to Gauteng distribution hubs. Malawi’s reliance on Beira keeps it vulnerable to Mozambican unrest.

SADC coastal states headline forecast expansion by 5.39%. Maputo’s USD 2 billion terminal doubling and Lobito’s rail upgrade unlock alternative routes that shorten cycle times for South African exporters. Namibia’s Walvis Bay and the Trans-Kalahari Corridor position the country as a west-coast pivot for Botswana and Zambian flows, adding diversity to the South Africa cross-border road freight transport market.

Rest-of-Africa lanes remain niche but are gathering pace as the AfCFTA removes tariff friction. DHL’s Johannesburg and Cape Town hubs aim to stitch Nigeria and Kenya into parcel networks, yet infrastructure and customs gaps still temper scaling beyond SADC neighbors. Over time, harmonized transit bonds are expected to expand the geographic footprint of the South African cross-border road freight transport industry.

Competitive Landscape

The South African cross-border road freight transport market exhibits moderate concentration. DHL, DSV, and Kuehne+Nagel utilize global capital to establish parcel-sorting hubs, collectively holding approximately 37% of the market share. Regional operators such as Grindrod, Imperial Logistics, and Super Group focus on corridor-specific infrastructure, including reefer depots and border-side yards, to maintain contracts in bulk mining and perishables. DHL’s acquisition of Vital in April 2026 enhances its last-mile delivery capabilities, while Grindrod’s Salt River depot strengthens its position in the reefer segment. Emerging players like JSL are expanding their fleets through telematics-driven strategies, gradually eroding the market share of established competitors.

Regional players are leveraging their localized expertise to compete with global giants. Grindrod’s investments in reefer depots and border-side yards are aimed at securing long-term contracts in the mining and perishable goods sectors. Similarly, Imperial Logistics and Super Group are focusing on corridor-specific assets to cater to niche demands. These strategies help regional operators maintain their foothold in a market increasingly influenced by global players. Meanwhile, DHL’s acquisition of Vital highlights the growing importance of last-mile delivery capabilities in the competitive landscape.

Environmental, Social, and Governance (ESG) compliance and carbon-tax reporting are becoming key differentiators in the market. Carriers equipped with real-time fuel monitoring systems and fleet-renewal budgets are better positioned to secure tenders from multinational clients, intensifying competition. However, entry barriers remain moderate, with the top five operators accounting for approximately 60% of confirmed revenue. As ESG regulations tighten, operators with advanced telematics and sustainability-focused investments are likely to gain a competitive edge, further shaping the dynamics of the market.

South Africa Cross Border Road Freight Transport Industry Leaders

DHL Group

DSV A/S

Kuehne+Nagel

GEODIS

CMA CGM Group (Including CEVA Logistics)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: National Treasury unveils ZAR 12.5 billion PPP to modernize six land borders, targeting 40% faster truck clearance.

- April 2026: DHL closes Vital Group buyout after Competition Tribunal approval, integrating 900 vehicles into its Gauteng and KZN fleets.

- February 2026: The Kazungula Bridge Authority established a one-stop border post at the Botswana-Zambia crossing, reducing the average border dwell time for compliant trucks from 12 hours to under 4 hours.

- October 2025: Transnet announced a ZAR 127 billion (USD 7.3 billion) five-year plan for Richards Bay terminal upgrades and Durban Pier 2 crane installations, reflecting government commitment to port-capacity expansion through 2031.

South Africa Cross Border Road Freight Transport Market Report Scope

| Agriculture, Fishing, and Forestry |

| Construction |

| Manufacturing |

| Oil and Gas, Mining and Quarrying |

| Wholesale and Retail Trade |

| Others |

| Full-Truck-Load (FTL) |

| Less than-Truck-Load (LTL) |

| Containerized |

| Non-Containerized |

| Long Haul |

| Short Haul |

| Fluid Goods |

| Solid Goods |

| Non-Temperature Controlled |

| Temperature Controlled |

| SADC Landlocked Countries | Botswana |

| Eswatini | |

| Lesotho | |

| Malawi | |

| Zambia | |

| Zimbabwe | |

| SADC Coastal Countries | Angola |

| Democratic Republic of the Congo (DRC) | |

| Mozambique | |

| Namibia | |

| Tanzania | |

| Rest of Africa |

| By End User Industry | Agriculture, Fishing, and Forestry | |

| Construction | ||

| Manufacturing | ||

| Oil and Gas, Mining and Quarrying | ||

| Wholesale and Retail Trade | ||

| Others | ||

| By Truckload Specification | Full-Truck-Load (FTL) | |

| Less than-Truck-Load (LTL) | ||

| By Containerization | Containerized | |

| Non-Containerized | ||

| By Distance | Long Haul | |

| Short Haul | ||

| By Goods Configuration | Fluid Goods | |

| Solid Goods | ||

| By Temperature Control | Non-Temperature Controlled | |

| Temperature Controlled | ||

| By Trade Region | SADC Landlocked Countries | Botswana |

| Eswatini | ||

| Lesotho | ||

| Malawi | ||

| Zambia | ||

| Zimbabwe | ||

| SADC Coastal Countries | Angola | |

| Democratic Republic of the Congo (DRC) | ||

| Mozambique | ||

| Namibia | ||

| Tanzania | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the South Africa cross-border road freight transport market?

The market stood at USD 2.55 billion in 2026 and is projected to reach USD 3.13 billion by 2031.

Which end-user segment is growing fastest?

Wholesale and retail trade is forecast to post a 4.82% CAGR to 2031, driven by e-commerce parcel flows.

Which regions dominate cross-border freight flows?

SADC landlocked countries such as Zambia and Zimbabwe dominate volumes, driven by mineral exports through South African corridors.

Which corridor improvements matter most?

Kazungula’s one-stop border post and the Beitbridge PPP are expected to cut border dwell by up to 40%, boosting short-haul frequency.

How will carbon taxation affect carriers?

Effective carbon tax rises from ZAR 46 /t CO₂e in 2026 to ZAR 116 /t by 2030, encouraging telematics-driven fuel efficiency among fleet operators.

Page last updated on: