South America Cross Border Road Freight Transport Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

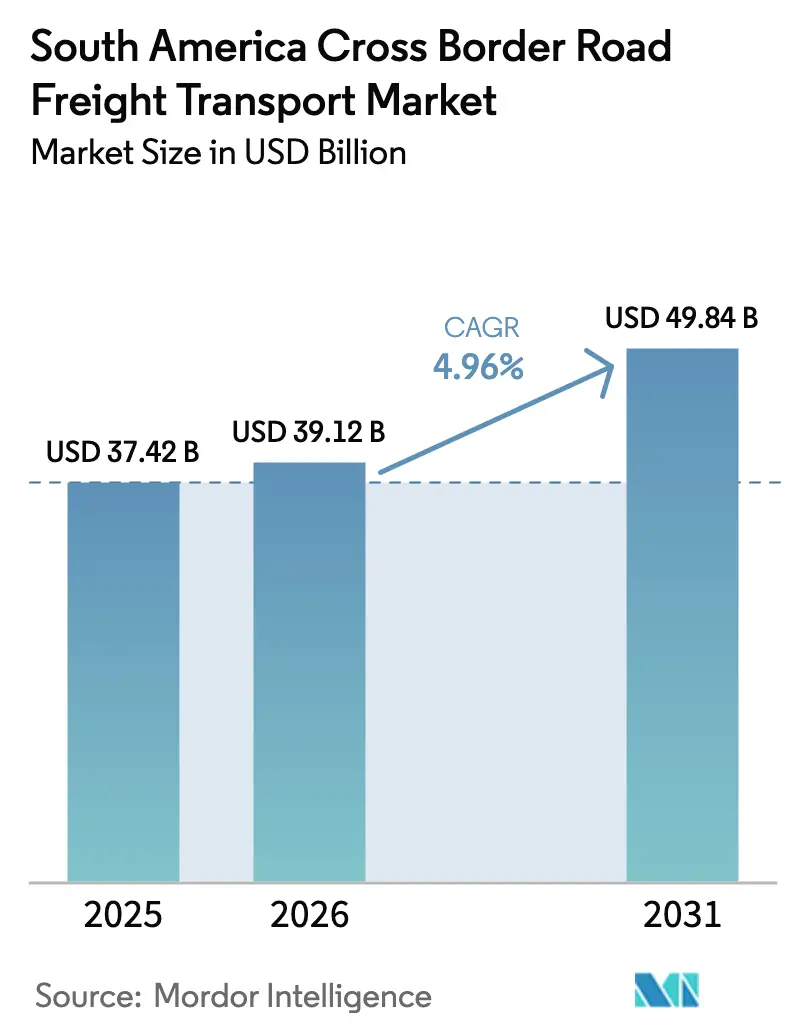

| Base Year Market Size (2025) | USD 37.42 Billion |

| Market Size (2026) | USD 39.12 Billion |

| Market Size (2031) | USD 49.84 Billion |

| Growth Rate (2026 - 2031) | 4.96% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Cross Border Road Freight Transport Market Analysis by Mordor Intelligence

The South America Cross Border Road Freight Transport Market size is expected to increase from USD 37.42 billion in 2025 to USD 39.12 billion in 2026 and reach USD 49.84 billion by 2031, growing at a CAGR of 4.96% over 2026-2031.

Robust intra-MERCOSUR merchandise flows, rising e-commerce parcel density, and lithium-corridor buildouts are accelerating demand for bonded trucking corridors across the continent. Highway concessions worth BRL 180 billion (USD 34.5 billion) are duplicating lanes on critical federal routes, trimming Sao Paulo-Buenos Aires transit times, and enhancing asset utilization for long-haul carriers. Digital single-window customs pilots are already cutting border-clearance delays by 40%, encouraging shippers to move time-sensitive goods by road rather than by slower coastal alternatives. Meanwhile, freight-matching platforms are aggregating smaller loads, shrinking empty-mile ratios, and spurring adoption of less-than-truckload services that broaden access to the South America cross border road freight transport market.

Key Report Takeaways

- By end-user industry, manufacturing led with 28.92% of the South America cross border road freight transport market share in 2025, while wholesale and retail trade is advancing at the fastest 5.61% CAGR through 2031.

- By truckload specification, full truckload held 81.27% share of the South America cross border road freight transport market size in 2025; less-than-truckload is forecast to expand at a 5.73% CAGR to 2031.

- By containerization, non-containerized freight commanded 84.41% of the South America cross border road freight transport market size in 2025, while containerized movements are set to grow at a 5.49% CAGR.

- By distance, long-haul services captured 64.83% of the South America cross border road freight transport market share in 2025, yet short-haul corridors are projected to rise at a 5.78% CAGR as nearshoring of assembly operations gains momentum.

- By goods configuration, solid cargo dominated with a 75.85% share in 2025, whereas fluid goods are climbing at a 5.44% CAGR on the back of biodiesel and petroleum-derivative swaps.

- By temperature control, non-refrigerated loads represented 94.39% of 2025 volumes, but temperature-controlled freight is growing at a 5.57% CAGR due to pharmaceutical and fresh-produce traffic.

- By country, Brazil accounted for 45.26% of the South America cross border road freight transport market size in 2025, and Peru is projected to be the fastest-growing national market at a 6.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Cross Border Road Freight Transport Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of intra-MERCOSUR trade flows | +1.2% | Argentina, Brazil, Paraguay, Uruguay; spillover to Chile | Medium term (2-4 years) |

| E-commerce boom boosts parcel trucking | +1.0% | Global, with the highest intensity in Brazil, Chile, and Colombia | Short term (≤ 2 years) |

| Highway & corridor megaprojects (e.g., Brazil BRL 180 bn plan) | +1.3% | Brazil core; secondary benefits in Argentina, Paraguay border zones | Long term (≥ 4 years) |

| Lithium-triangle mining surge creating new corridors | +0.8% | Chile, Argentina, Bolivia tri-border; export routes to Pacific ports | Medium term (2-4 years) |

| Digital customs single-window interoperability | +0.7% | MERCOSUR member states; pilot expansions in Colombia, Peru | Medium term (2-4 years) |

| Freight-matching platforms cutting empty miles | +0.6% | Brazil, Argentina urban clusters; expanding to Chile, Colombia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Intra-MERCOSUR Trade Flows

The EU-MERCOSUR pact, provisionally active since late 2024, eliminates 91% of industrial tariffs, which immediately spurred an 8.3% jump in intra-bloc trade to USD 47 billion during 2025. Weekly cross border shipments of automotive components now bridge Argentine suppliers and Brazilian assembly lines, compressing inventory costs by 15%. Paraguay’s biodiesel feedstock exports fill backhaul capacity that had previously gone empty, lifting fleet utilization rates. Uruguay’s pulp producers route containerized cargo through Argentine ports, forming triangular circuits that reduce deadhead. Harmonized inspection protocols under the pact shave 12 hours off clearance at Paso de los Libres-Uruguaiana, the bloc’s busiest land crossing.

E-Commerce Boom Boosting Parcel Trucking

Latin American e-commerce expanded 12.2% in 2025, with cross border orders making up 18% of gross merchandise value. MercadoLibre’s logistics arm moved 1.2 million cross border parcels monthly and guarantees 48-hour delivery between São Paulo and major southern capitals, enabled by 23 fulfillment sites dedicated to the South America cross border road freight transport market. Chile’s Falabella and Colombia’s Exito pooled less-than-truckload cargo, lowering per-parcel freight costs by 22%. The MERCOSUR Digital Single Market, live since 2025, cut customs documentation windows to four hours, reinforcing time-definite parcel movements. Autonomous sorting hubs piloted at Foz do Iguacu process parcels in 90 minutes, unlocking late-cutoff dispatches and improving delivery-promise adherence.

Highway & Corridor Megaprojects

Brazil auctioned BRL 180 billion (USD 34.5 billion) in highway concessions across 12,000 kilometers, mandating lane duplication and electronic tolling that are forecast to trim Sao Paulo Buenos Aires truck transit by 18% by 2028[1]Ana Mano, “Brazil Auctions BRL 180 Billion in Highway Concessions,” Reuters, reuters.com. CCR and Ecorodovias are paving 2,400 kilometers in Mato Grosso do Sul and Parana, removing seasonal detours for grain haulers. Argentina upgraded the Neuquen-Temuco corridor for 60-tonne rigs serving Vaca Muerta shale projects. Chile widened Route 5, boosting truck flow by 35% and shortening port-gate queues. Colombia’s Bogota-Buenaventura dual carriageway now completes the Andean-Pacific run in eight hours, opening Ecuadorian and Peruvian lanes to Colombian exporters.

Lithium-Triangle Mining Surge Creating New Corridors

Chile, Argentina, and Bolivia controlled 58% of global lithium reserves and lifted extraction volumes 27% in 2025[2]U.S. Geological Survey, “Mineral Commodity Summaries 2026 – Lithium,” usgs.gov . Haul roads from Chile’s Salar de Atacama to Salta cross the Andes at 4,000 meters, requiring specialized heavy-haul fleets with auxiliary braking and GPS-linked descent controls. Argentina issued 14 new extraction permits and is paving RN 40 spurs to Rosario port, integrating the route into the South America cross border road freight transport market. Bolivia’s USD 1 billion joint venture with CATL already tendered contracts for 300,000 tonnes per year of feedstock haulage. A tri-national working group is unifying axle-load standards, preventing pavement damage, and ensuring uninterrupted year-round service.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infrastructure deficits & high share of unpaved roads | -0.9% | Paraguay, Bolivia, rural Argentina, northern Brazil | Long term (≥ 4 years) |

| Bureaucratic border procedures & NTMs | -0.7% | All MERCOSUR crossings; acute at Paso de los Libres, Foz do Iguaçu | Medium term (2-4 years) |

| Cabotage laws blocking coastal shipping alternatives | -0.5% | Brazil, Argentina, Chile coastal zones; affects long-haul corridors | Long term (≥ 4 years) |

| Diesel-price volatility from biofuel mandates | -0.6% | Brazil, Argentina (biodiesel mandates); spillover to Paraguay, Uruguay | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Infrastructure Deficits & High Share of Unpaved Roads

Unpaved segments account for 62% of Paraguay’s network and 48% of Bolivia’s, compelling detours that tack on up to 400 kilometers and lift fuel burn by 25%[3]World Bank Staff, “Logistics Performance Index 2025,” World Bank, worldbank.org. Paraguay’s gravel Transchaco corridor limits speeds to 40 km/h and closes during rainy spells, stranding export soy and inflating transit risk. Bolivia’s sole paved soy route is prone to landslides, immobilizing trucks for up to 5 days during the wet season. Northern Brazil’s partially paved BR-163 forces grain haulers to queue for days, driving logistics costs to USD 85 per ton versus USD 45 on all-weather routes. IDB estimates place the capex need for all-weather upgrades at USD 22 billion, triple the current infrastructure budgets.

Bureaucratic Border Procedures & NTMs

A typical MERCOSUR crossing involves 11 document checks, adding 28 hours of total dwell time at Paso de los Libres-Uruguaiana compared with six hours at the United States-Canada bridge. Argentina’s import-licensing regime and Brazil’s red-channel inspections create a 48-hour schedule padding. Chile mandates fumigation of all wooden pallets from Argentina, adding USD 150 and 24 hours per load. Pharmaceutical checks at Colombia’s INVIMA can take 72 hours, forcing reefer rigs to idle on grid power and risk cold-chain breaks. The World Bank’s 2025 Logistics Performance Index scored South American border administration at 2.6/5, underscoring process redundancies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User Industry: Manufacturing Leads While Retail Trade Accelerates

Manufacturing generated 28.92% of the South America cross border road freight transport market share in 2025 as just-in-time components flowed between Brazilian auto plants and Argentine part suppliers[4].JSL Investor Relations, “Annual Report 2025,” jsl.com.br Wholesale and retail trade is projected to post a 5.61% CAGR through 2031, driven by cross border e-commerce parcels increasingly relying on bonded LTL consolidation hubs. The South America cross border road freight transport market size attributable to retail consignments is forecast to expand from USD 11.4 billion in 2026 to USD 15.0 billion in 2031, underscoring the strategic importance of omnichannel warehouse placement. Meanwhile, agriculture maintains a steady tonnage baseline during harvest peaks, demanding surge capacity of grain hoppers and reefers for seafood bound from Chile to Peru. Mining, oil, and gas hinge on lithium-triangle and Vaca Muerta projects that require ADR-certified fleets. Construction materials ride Brazil’s highway concessions pipeline, while pharmaceuticals, electronics, and FMCG volumes climb as manufacturers nearshore to neutralize tariff uncertainties.

Price sensitivity differs: manufacturing and mining tend to award long-term contracts that anchor fleet utilization, whereas retail and pharmaceuticals exhibit higher velocity but tighter delivery windows. Shippers in fast fashion and consumer electronics are shifting to less-than-truckload platforms to flex capacity without committing to full loads. The agriculture and construction segments skew toward non-containerized formats, resisting intermodal options due to limitations in loading infrastructure. Across categories, real-time visibility and milestone compliance are becoming procurement criteria, forcing carriers to integrate telematics and APIs with shipper TMS platforms to remain in preferred-carrier pools.

By Truckload Specification: FTL Dominates, LTL Gains with Digital Aggregation

Full truckload contributed 81.27% of the South America cross border road freight transport market in 2025. Commodity shippers rely on dedicated trailers for biofuel, grain, and copper concentrate that travel direct point-to-point. Less-than-truckload, however, is projected to exhibit the highest CAGR of 5.73% as digital freight-matching platforms consolidate small consignments. The South America cross border road freight transport market size generated by LTL is set to jump to more than USD 9 billion by 2031. Digital apps preload customs data, enabling a single manifest for multiple shippers that cuts administrative overhead 30% and accelerates gate releases.

FTL operators are introducing semi-automated capacity-planning tools that allocate drop-and-hook kits at border yards, shrinking detention times. LTL networks are investing in cross-docks at Ciudad del Este, Foz do Iguaçu, and Salta, which linehaul loads overnight and break them into last-mile routes by dawn. MercadoLibre’s 92% trailer-fill benchmark illustrates the density achievable when data transparency persuades shippers to pool freight. FTL remains dominant for hazardous goods and perishable cargo requiring single-shipper traceability. Nevertheless, the profitability gap between FTL and high-density LTL is narrowing as fuel and toll savings from reduced empty kilometers accrue to carriers that embrace collaborative, platform-based dispatching.

By Containerization: Non-Containerized Prevails but Intermodal Picks Up

Non-containerized traffic controlled 84.41% of the South America cross border road freight transport market in 2025, moving bulk grain, fuel, and oversize machinery. Containerized flows, though smaller, are riding a 5.49% CAGR tailwind as rail-road intermodal corridors mature. Door-to-door services combining double-stack trains with truck first- and last-mile legs cut emissions 40% per ton-kilometer and reduce Sao Paulo-Buenos Aires transit to 72 hours, 24 hours faster than pure-road routes. Customs e-seals on ISO boxes earn 82% green-lane clearance, slashing inspection frequency. Grain shippers remain wedded to hopper trailers that feed port silos by gravity, while tank operators avoid container leasing costs and cleaning constraints. Yet electronics, apparel, and pharmaceuticals are shifting to containers to mitigate theft risk and improve humidity control, signaling further intermodal potential inside the South America cross border road freight industry.

Non-containerized operators defend their share through specialized assets, such as tanker fleets with vapor-recovery systems and flatbeds fitted for irregularly shaped mining cargo. Infrastructure upgrades that extend heavyweight access roads to new lithium fields favor open-deck rigs. Intermodal players bank on concessioned rail lines from Mato Grosso to Santos and from Antofagasta to Mendoza that will add hauling slots by 2027. Container repositioning costs remain a concern, but bilateral equipment-sharing agreements between Brazilian and Argentine carriers are reducing deadhead repositioning legs. Over the forecast horizon, container uptake will likely concentrate on high-value, theft-sensitive commodities, while non-containerized freight will continue to dominate bulk agricultural and energy supply chains.

By Distance: Long Haul Leads, Short Haul Accelerates With Nearshoring

Long-haul journeys accounted for 64.83% of South America cross border road freight transport market share in 2025. Nearshoring, however, is pushing assembly plants and fulfillment centers closer to borders, causing short-haul lanes to register the fastest 5.78% CAGR through 2031. Near-border cities such as Ciudad del Este and Tacna now function as manufacturing-adjacent hubs, dispatching electronics and apparel to Brazilian and Peruvian retailers within a single driver shift. Short-haul trips benefit from minimal accommodation costs and smoother compliance with 2024 hours-of-service rules that cap continuous driving at 10 hours.

Long-haul carriers are retrofitting tractors with sleeper cabs and adding driver swap stations to remain compliant while preserving service windows. Toll differentiation that favors multi-axle rigs on new concession roads makes long-haul per-kilometer charges steeper, but economies of scale persist for full-load grain and mining cargo. Short-haul fleets are pivoting toward smaller, more maneuverable trucks capable of handling urban delivery constraints and rapid border turnarounds. Technology platforms are democratizing access to short-haul capacity, showing real-time spot rates that entice owner-operators to accept intra-day assignments. Both distance segments will coexist, yet capital formation is tilting toward agile short-haul fleets that can plug seamlessly into e-commerce fulfillment networks.

By Goods Configuration: Solid Goods Dominate While Fluid Goods Gain With Biofuels

Solid goods accounted for 75.85% of 2025 revenue, reflecting the prevalence of grain, minerals, and manufactured products in South America cross border road freight transport routes. Fluid cargo, mainly biodiesel, fuel condensate, and sulfuric acid, is on a 5.44% CAGR path through 2031, driven by evolving biofuel mandates and lithium-processing chains. Brazil’s 14% biodiesel blend compels 1.2 million tons of Argentine imports annually, filling tanker trailers that meet ADR standards. Sulfuric-acid tankers run northbound from Peruvian smelters to Chilean refineries, closing the directional-imbalance gap that once plagued carriers.

Solid-cargo shippers prize high-cube utilization and embrace drop-deck systems for mining equipment, while fluid-goods operators grapple with stricter recertification intervals and ullage-safety rules that reduce net payload. Profit margins for fluid cargo are compensated via surcharge mechanisms tied to hazmat compliance. Solid-cargo carriers integrate weigh-in-motion sensors to avoid roadside penalties that lengthen dwell time. Overall, advancing energy transition policies will gradually increase the share of fluid goods, but solid freight will retain primacy due to the continent’s agriculture- and mining-heavy export profile.

By Temperature Control: Ambient Loads Rule, Cold Chain Expands Fast

Ambient freight outweighed cold chain with a 94.39% share in 2025. Yet temperature-controlled lanes forecast a 5.57% CAGR, riding on mutual recognition of pharmaceutical GDP certifications and on fresh-produce exports from Chile’s Central Valley to Brazilian supermarkets. JSL invested BRL 1.2 billion in Euro VI tractors and 2,400 refrigerated trailers to capture this growth. Chilean berry exporters leverage telematics-controlled reefers that flag 2°C deviations, reducing spoilage claims.

Cold-chain operators charge 40-60% premiums to defray reefer fuel, equipment depreciation, and annual validation audits. Fleet scarcity pushes reefer utilization near 95% during peak harvest, prompting double-brokered spot charters that drive rates higher. Nevertheless, regulatory convergence under the 2025 GDP agreement lowers multistate licensing hurdles, reducing entry barriers for new cold-chain entrants. Ambient freight will stay dominant, but pharma, beef, and high-value fruit will ensure a structurally higher growth curve for cold-chain services within the South America cross border road freight transport industry.

Geography Analysis

Brazil captured 45.26% of South America cross border road freight transport market size in 2025, anchored by dense manufacturing clusters in Sao Paulo, Minas Gerais, and Rio Grande do Sul. Highway concessions duplicating lanes on BR-050 and BR-116 will further elevate Brazil’s share by lowering transit costs into Argentina, Uruguay, and Paraguay. Brazil’s Siscomex platform already processes 95% of import declarations electronically, collapsing clearance time to four hours. Real-time data interchange means Brazilian shippers can pre-clear long-haul cargo before rigs leave origin docks.

Peru is the fastest-growing national segment, with a projected 6.18% CAGR, enabled by USD 1.8 billion in expansions at the Callao and Paita ports that attract Andean copper and consumer-goods flows. Copper-concentrate hauls from Cerro Verde and Las Bambas mines link to Pacific gateways and onward ocean services to Asia, elevating Peru’s relevance to the South America cross-border road freight transport market. Peru’s VUCE single window interoperates with Chile’s, lowering Tacna-Arica dwell times to six hours.

Colombia’s 4G program shaved Bogota-Buenaventura time to eight hours, opening Ecuadorian and Peruvian lanes to Colombian agro-industry exporters. Political frictions still limit flows with Venezuela, yet the Lima-Bogota express service launched by Ransa and Grupo TASA targets 72-hour door-to-door cycles that could unlock new cross border e-commerce lanes. The rest of South America, including Paraguay, Uruguay, and Bolivia, provided 18% of regional tonnage in 2025, benefiting from free-trade zones like Ciudad del Este that act as parcel aggregation points for Brazilian retailers.

Competitive Landscape

The South America cross border road freight transport market is moderately fragmented, leaving ample space for a corridor specialist. Global integrators DHL, DSV, Kuehne+Nagel, CEVA, and GEODIS secure automotive and high-tech contracts that demand integrated air-sea-road solutions but often cede low-margin bulk lanes to regional outfits.

Regional champions such as Tegma, Andreani, SAAM, Agunsa, and Ransa run asset-light models that subcontract owner-operators during peak seasons yet keep dedicated ADR- or GDP-compliant fleets for hazardous or temperature-controlled moves. Digital disruptors CargoX and Cargamos undercut traditional brokers by up to 18% through algorithmic pricing and instant carrier payments, forcing incumbents to upgrade their tech stacks. Technology penetration diverges sharply: JSL equips 78% of its cross border tractors with predictive-maintenance telematics, whereas fleets under 50 trucks average 34%, a service gap multinationals flag on quarterly carrier scorecards.

MERCOSUR cabotage restrictions shield domestic carriers from foreign competition but also limit scalability. The inability of a Brazilian-flag tractor to haul domestic freight inside Argentina reduces round-trip utilization. Consequently, consolidation across borders remains contractual rather than asset-based, with integrators leveraging joint ventures and drop-yard sharing to approximate pan-regional coverage. White-space opportunities abound in reverse logistics for e-commerce returns, refrigerated final-mile delivery, and real-time visibility dashboards tailored for SME shippers without proprietary TMS platforms.

South America Cross Border Road Freight Transport Industry Leaders

DHL Group

Ceva Logistics

DSV

JSL S.A.

Kuehne + Nagel

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: C.H. Robinson expanded cross-border operations in November 2025 with over 450,000 sq ft added in El Paso, Texas, boosting United States-Mexico border logistics for automotive and high-tech freight.

- April 2025: CEVA Logistics (CMA CGM) signed a deal to acquire Borusan Tedarik, expanding warehousing and ground transport, though primarily in Turkey with network effects for Europe connections.

- April 2025: Log-In Intermodal (Brazil) announced expansion of its Manaus cabotage route in April 2025, adding a fourth vessel and increasing North Brazil capacity by 30%, integrating road transport via subsidiary Tecmar.

- April 2025: DSV A/S completed its acquisition of DB Schenker in April 2025, forming a major global transport player with enhanced network capabilities potentially benefiting South American operations through scale.

South America Cross Border Road Freight Transport Market Report Scope

| Agriculture, Fishing, and Forestry |

| Construction |

| Manufacturing |

| Oil and Gas, Mining and Quarrying |

| Wholesale and Retail Trade |

| Others |

| Full-Truck-Load (FTL) |

| Less than-Truck-Load (LTL) |

| Containerized |

| Non-Containerized |

| Long Haul |

| Short Haul |

| Fluid Goods |

| Solid Goods |

| Non-Temperature Controlled |

| Temperature Controlled |

| Argentina |

| Brazil |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By End User Industry | Agriculture, Fishing, and Forestry |

| Construction | |

| Manufacturing | |

| Oil and Gas, Mining and Quarrying | |

| Wholesale and Retail Trade | |

| Others | |

| By Truckload Specification | Full-Truck-Load (FTL) |

| Less than-Truck-Load (LTL) | |

| By Containerization | Containerized |

| Non-Containerized | |

| By Distance | Long Haul |

| Short Haul | |

| By Goods Configuration | Fluid Goods |

| Solid Goods | |

| By Temperature Control | Non-Temperature Controlled |

| Temperature Controlled | |

| By Country | Argentina |

| Brazil | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

What is the forecast value of the South America cross-border road freight market by 2031?

It is expected to reach USD 49.84 billion by 2031.

Which end-user segment is expanding fastest in cross-border trucking across South America?

Wholesale and retail trade is growing at a 5.61% CAGR, driven by e-commerce parcels and omnichannel fulfillment.

How fast will containerized road freight grow compared with non-containerized cargo?

Containerized movements are projected to rise at a 5.49% CAGR, outpacing the still-dominant non-containerized segment.

Which country is the fastest-growing market for cross-border road freight in South America?

Peru is forecast to expand at a 6.18% CAGR through 2031, supported by port upgrades and copper-export logistics.

What share of the market did full truckload hold in 2025?

Full truckload services captured 81.27% of market revenue in 2025.

How are digital freight-matching platforms influencing market dynamics?

Platforms like CargoX and Cargamos lower empty-mile ratios and reduce per-kilogram rates, accelerating LTL adoption across key regional corridors.

Page last updated on: