Turkey Cross-Border Road Freight Transport Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

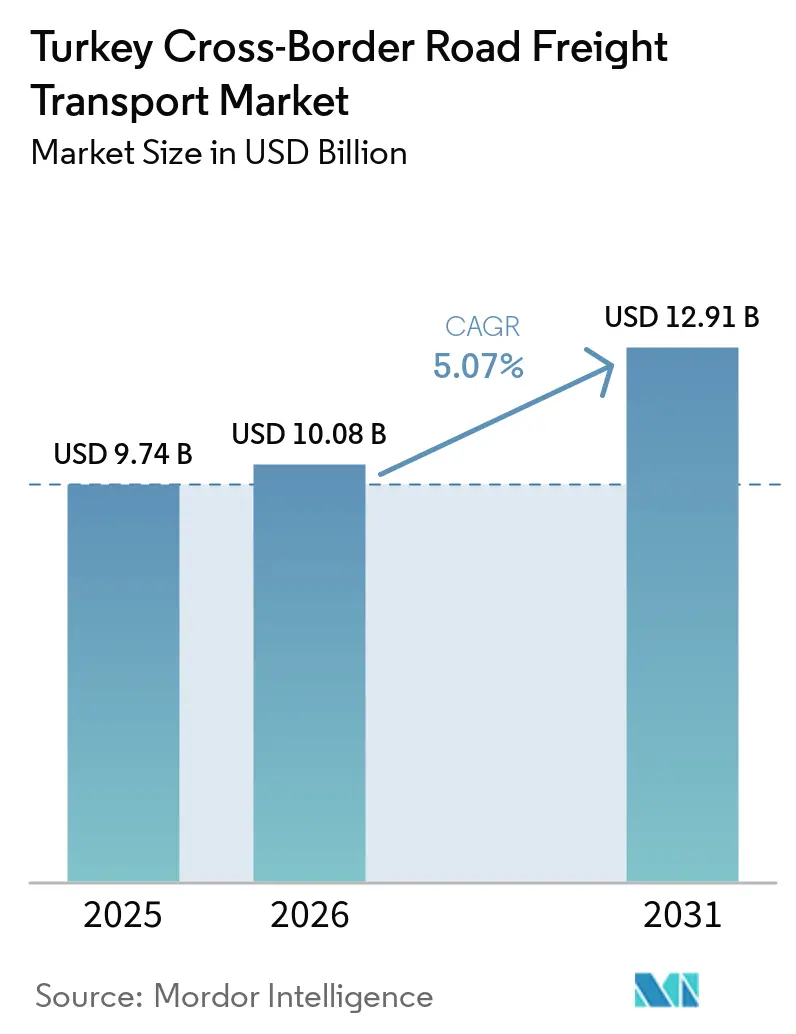

| Base Year Market Size (2025) | USD 9.74 Billion |

| Market Size (2026) | USD 10.08 Billion |

| Market Size (2031) | USD 12.91 Billion |

| Growth Rate (2026 - 2031) | 5.07% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turkey Cross-Border Road Freight Transport Market Analysis by Mordor Intelligence

The Turkey cross-border road freight transport market size is expected to increase from USD 9.74 billion in 2025 to USD 10.08 billion in 2026 and reach USD 12.91 billion by 2031, growing at a CAGR of 5.07% over 2026-2031.

Robust export momentum to the European Union (EU) and the Middle East and North Africa (MENA) bloc, continued integration of Turkish production clusters into EU supply chains, and the USD 17 billion Development Road Project are the primary tailwinds. Record outbound trade USD 273.4 billion in 2025, combined with the Middle Corridor’s 68% year-on-year tonnage jump, is widening lane density toward both Bulgaria and Iraq[1]Republic of Turkey Ministry of Transport and Infrastructure, “Transport Infrastructure Statistics,” uab.gov.tr. Simultaneously, highway upgrades at Kapıkule and Habur are compressing dwell times, while technology investments such as heavy-vehicle navigation and real-time reefer monitoring are trimming operating costs and boosting compliance. Larger global integrators are exploiting scale following the DSV–DB Schenker merger, whereas Turkish incumbents are expanding warehousing footprints and rail assets to preserve margins amid permit fees and driver shortages.

Key Report Takeaways

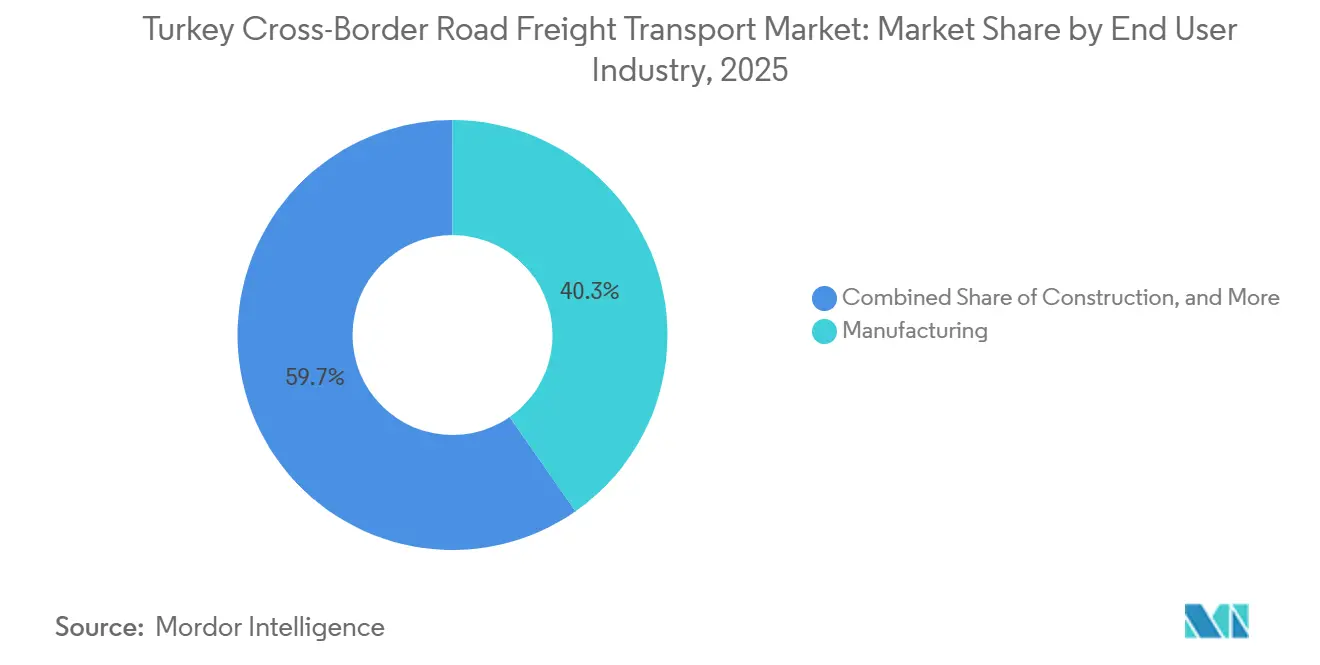

- By end-user industry, manufacturing accounted for 40.31% of the Turkey cross-border road freight transport market share in 2025, while agriculture, fishing, and forestry is projected to grow at a 6.72% CAGR to 2031.

- By truckload specification, full truckload (FTL) accounted for 71.1% of the Turkey cross-border road freight transport market size in 2025; less-than-truckload (LTL) is expanding at a 6.84% CAGR on the back of cross-border e-commerce.

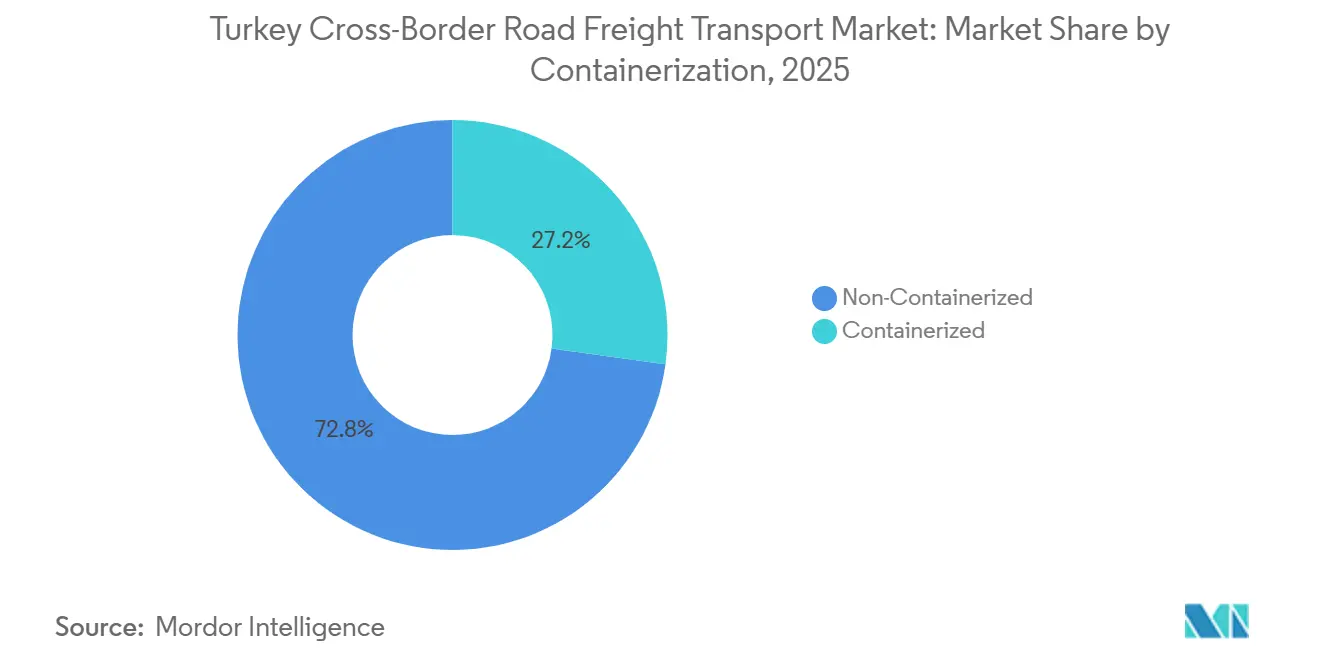

- By containerization, non-containerized cargo held 72.83% of the Turkey cross-border road freight transport market share in 2025, but containerized lanes are forecast to grow at a 7.00% CAGR as rail-road intermodal services scale.

- By distance, long haul held 64.56% of the Turkey cross-border road freight transport market size in 2025, but short haul is forecast to rise at a 5.55% CAGR.

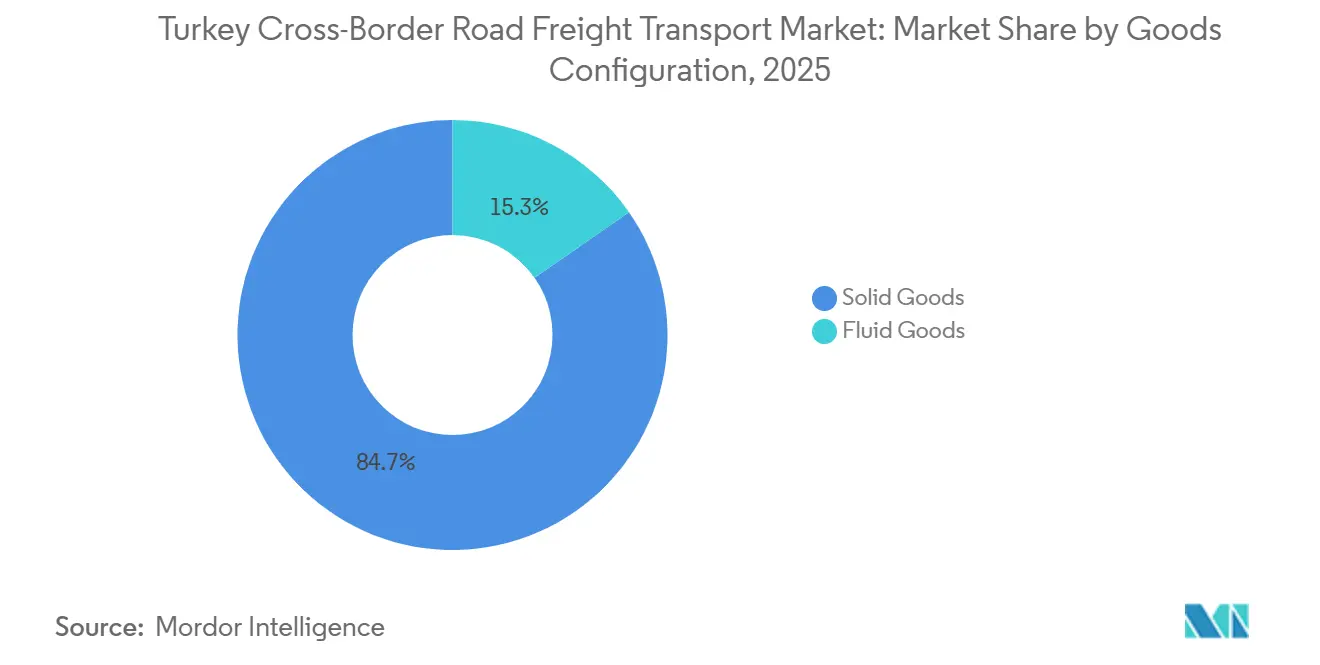

- By goods configuration, solid goods held 84.68% of the Turkey cross-border road freight transport market share in 2025, but fluid goods is forecast to rise at a 5.89% CAGR.

- By temperature control, non-refrigerated freight accounted for 84.77% of the Turkey cross-border road freight transport market size in 2025, yet temperature-controlled movements are increasing at an 8.68% CAGR thanks to pharmaceutical and fresh-produce flows.

- By country, Bulgaria led with 36.91% of the Turkey cross-border road freight transport market share in 2025, whereas Iraq is poised to advance at a 7.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Turkey Cross-Border Road Freight Transport Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Turkish exports to the EU and MENA | +1.8% | EU gateways (Bulgaria, Greece), MENA lanes (Iraq, Syria) | Medium term (2-4 years) |

| Near-shoring of European manufacturing to Turkey | +1.2% | Core EU (Germany, France, UK) and Balkan spillovers | Long term (≥ 4 years) |

| Highway and border-gate modernization projects | +0.9% | Kapıkule, Habur, Gürbulak | Short term (≤ 2 years) |

| E-commerce-led surge in cross-border LTL demand | +0.7% | Romania, Poland, UAE, Saudi Arabia | Medium term (2-4 years) |

| Middle-Corridor diversion of Central-Asian freight | +0.5% | Georgia, Armenia, Kazakhstan, Uzbekistan | Long term (≥ 4 years) |

| GCC fast-track transit-visa reforms for Turkish drivers | +0.3% | Saudi Arabia, UAE, Kuwait | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Turkish Exports to the EU and MENA

EU-bound shipments climbed to USD 117 billion in 2025, equal to 50.3% of Turkey’s trade with the bloc, while Iraq alone absorbed USD 10.3 billion worth of goods. These flows translated into dense truck volumes through Kapıkule and Habur, with the latter processing 1.75 million crossings in 2024 as shippers skirted new Syrian tariffs. The geographic proximity of Bursa’s auto plants, Denizli’s textile mills, and Iskenderun’s steelworks, each within a 500-kilometer truck haul of key border gates, keeps road the lowest-cost mode for loads under 1,500 kilometers. Rerouting via Iraq and Jordan extends the distance by about 350 kilometers but still reduces landed cost because it avoids 25-30% Syrian ad valorem charges. Completion of Phase 1 of the Development Road corridor by 2028 is set to cut Basra–Turkey transit to under 16 hours, sustaining Iraq’s outsized growth contribution to the road freight sector.

Near-Shoring of European Manufacturing to Turkey

Renault’s EUR 400 million (USD 465.5 million) upgrade of its Bursa plant and Hyundai’s launch of Ioniq 3 production in İzmit for 2026 delivery anchor a massive wave of OEM investments. Each new model spawns daily inbound component shuttles from Spain, France, and Germany and outbound vehicle hauls back into the EU, adding roughly 150-200 truck moves per day on Bulgaria and Greece corridors. Lower wages, zero industrial tariffs under the EU–Turkey Customs Union, and immediate access to MENA buyers give automakers a dual-market hedge. Smaller, more frequent just-in-time consignments are shifting volume toward the Turkey cross-border road freight transport market’s LTL segment, underpinning its 6.84% CAGR. Mars Logistics responded in 2026 with a EUR 70 million (USD 81.4 million) fleet and wagon purchase, aimed at pushing total corporate turnover beyond EUR 700 million (USD 814.6 million), heavily supported by these automotive-lane expansions.

Highway and Border-Gate Modernization Projects

Substantial capital investment in Turkey’s 2026 budget targets critical choke points, including Kapıkule-North, Gürbulak, and İpsala. Historically severe wait times, which have periodically peaked into multi-day delays, are forecast to drop significantly once expanded automation and increased parking capacity go live at Kapıkule-North. Every hour saved materially reduces costs related to driver pay, idle fuel burn, and cargo spoilage, equating to vast potential annual savings across heavy cross-border traffic volumes.[2]International Road Transport Union, “IRU Driver Shortage Report 2024,” iru.org Efficiency asymmetry persists, however, with rigorous EU border checks under the current Official Controls Regulations still lengthening inbound dwell, acting as a structural drag on backhaul pricing competitiveness.

E-Commerce–Led Surge in Cross-Border LTL Demand

Cross-border parcel volumes originating from Turkey expanded significantly year-on-year in 2024-2025 on the back of Trendyol’s and Hepsiburada’s European rollouts. Consignments under 30 kg require 24- to 48-hour delivery and show return ratios of 15-20%, favoring LTL networks that can consolidate multiple shippers and maximize route density. Horoz Logistics responded with new direct lines to Romania, Spain, Portugal, Morocco, and the Turkic republics, though experiencing profitability contractions in 1H 2025 versus 1H 2024 due to expansion and integration costs. Asset-heavy FTL carriers without real-time tracking now confront margin compression as shippers gravitate toward tech-enabled LTL offerings that post empty-mile ratios below 15%.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU transit-permit quotas and fees | –0.8% | Austria, Italy, Slovenia, and Czechia | Medium term (2-4 years) |

| Domestic truck-driver shortage and aging workforce | –0.6% | National hubs: Istanbul, Ankara, İzmir | Long term (≥ 4 years) |

| Turkish lira volatility inflating diesel costs | –0.5% | Nationwide, spillover to Bulgaria and Greece fuel stops | Short term (≤ 2 years) |

| Emerging EU carbon rules (ETS, CBAM) | –0.4% | All EU member states, indirect on Turkey–EU corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU Transit-Permit Quotas And Fees

Turkey holds only 7,688 multilateral ECMT permits, leaving a 15-20% gap relative to actual trip demand and forcing carriers to buy secondary-market documents for EUR 500-1,000 (USD 581.9-1,163.7) per movement. Greek, Bulgarian, and Hungarian tolls add another EUR 600-800 (USD 698.0 -930.7) to a standard Istanbul–Rotterdam leg, raising end-to-end cost by almost 15%. Because permit rules cap empty backhauls, many operators drive an extra 200-300 km through low-control Balkan corridors, burning more diesel and losing booking slots at EU cross-docks. EU roadside inspections target Turkish plates two to three times more often than EU vehicles under Regulation 1071/2009, heightening the risk of delays and insurance premiums. Higher compliance costs narrow the price gap with rail and short-sea routes, prompting some shippers to divert loads of more than 1,500 km from trucks.[3]European Commission, “Regulation 882/2004 on Official Controls,” eur-lex.europa.eu

Domestic Truck-Driver Shortage And Aging Workforce

The sector is short about 93,000 qualified drivers, or 17% of positions, leaving trucks idle for 2 or 3 days each week while loads wait at depots. Demographics amplify the squeeze: the Turkish driver pool is increasingly aging with a shrinking pipeline of younger entrants, and women account for just 1.4% of the workforce. Long cross-border rotations keep drivers away from home 250-280 nights a year, yet annual pay averages only USD 18,000-22,000, around 35% below EU levels, so few young candidates apply. Fleets cope by doubling crew on EU lanes, but that adds substantial daily wage burdens and still falls short of meeting growth in e-commerce and temperature-controlled loads. Persistent gaps are steering carriers toward rail links and intermodal swaps, even though these require fresh capital and new scheduling software.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: Manufacturing Dominates While Agriculture Accelerates

Manufacturing drives substantial outbound revenue and secured 40.31% of the Turkey cross-border road freight transport market share. This slice is anchored in the country’s USD 41 billion automotive export base and USD 15 billion of annual textile shipments, most of which leave Bursa, İzmit, Denizli, and Gaziantep in full truckload convoys bound for Bulgaria and Greece. Automotive parts travel on fixed-day schedules toward German, French, and British assembly plants, creating predictable weekly lane density and encouraging carriers to commit dedicated drop-and-hook assets. Textile pallets, by contrast, move in mixed consignments that favor less-than-truckload consolidation and direct store delivery to Spanish and Italian retailers. Chemical and metals traffic remains sizeable as steel coils from Iskenderun and flat-rolled aluminum from Kocaeli feed EU construction and appliance demand.

Agriculture, fishing, and forestry is expected to grow at 6.72% CAGR, well above the Turkey cross-border road freight transport market growth rate, as Iraq’s heavy reliance on food imports and Syria’s reopened borders are lifting refrigerated truck demand. Reefer loads with tomatoes, peppers, table grapes, and dairy now exit Hatay and Şırnak seven days a week, and backhaul lanes often carry Iraqi dates or Syrian cotton for Turkish processors. Construction freight stands out as a cyclical but high-yield niche; post-earthquake rebuilding in Hatay and Kahramanmaraş is sending daily cement, rebar, and prefabricated-panel convoys to southern districts, then across Habur into Kurdistan infrastructure sites. Wholesale and retail trade, heavily influenced by e-commerce replenishment, is adding new daily parcel runs to Romanian and Bulgarian fulfillment centers operated by LC Waikiki and Defacto. Pharmaceutical loads small in tonnage but rich in revenue are leaping ahead under GDP guidelines, supported by advanced temperature-controlled infrastructure like Sanofi’s 11,000 m² Tuzla hub.

By Truckload Specification: FTL Leads But LTL Gains Momentum

Full truckload kept 71.1% of the Turkey cross-border road freight transport market size in 2025, because auto, steel, and bulk-textile shippers still book dedicated 20- to 25-tonne moves for transit under 1,500 km at competitive rates of EUR 0.90–1.00 (USD 1.05-1.16) per kilometer. The FTL model delivers high trailer utilization and predictable scheduling, yet it is increasingly constrained by a 17% driver deficit and tight EU transit-permit quotas that make Bulgarian and Romanian backhauls more expensive. Large fleets have started mitigating shortages by implementing two-driver crew rotations on the Istanbul–Rotterdam lanes and by using dual-mode road-rail swaps in Sofia, which cut average rest-time losses by 11 hours per trip. Asset-heavy carriers are also fitting aerodynamic skirts and digital tire-pressure sensors to trim diesel burn by two or three liters per 100 km on the Kapıkule corridor.

LTL is expanding at a 6.84% CAGR through 2031 as e-commerce, spare-parts replenishment, and high-frequency just-in-time manufacturing inflows fragment shipment sizes. Dynamic routing software now pools multiple shippers into single night-haul vans headed for Sofia or Bucharest, pushing empty-mile ratios below 15% and shaving one day off Balkan delivery windows. Turkish SMEs are partnering with German digital forwarders to auction spare pallet spaces on the approaches to the Kapıkule gate, earning EUR 120-140 (USD 139.64-162.91) in incremental revenue per trip and smoothing capacity swings. Hybrid chains are also emerging: Mars Logistics uses its 100 new rail wagons to shuttle containerized auto parts from Bursa to Sofia, then breaks down loads into palletized LTL for last-mile drops across Central Europe, capturing both volume and yield uplift.

By Containerization: Non-Containerized Dominates While Box Traffic Surges

Non-containerized tonnage held 72.83% of 2025 flows because steel coils, cement, wind-turbine blades, and fresh produce favor open-deck, bulk, or reefer trailers that permit side or top loading and fast quay-side turnaround. Curtain-siders remain the default for apparel and electronics, giving operators flexibility to back-haul return loads without weight-distribution penalties. Many Turkish carriers retrofit double-stack garment rails inside 13.6 m trailers, allowing load factors above 95 m³ on the Bursa–Lyon fast-fashion shuttle. Oversized renewable-energy components, rotor hubs, tower sections, and nacelles require convoy escorts and route surveys that only specialized heavy-haul fleets can deliver, but they command pricing of EUR 3.50–4.00 (USD 4.07-4.66) per kilometer.

Containerized freight is expanding at a 7.00% CAGR. Two drivers underpin the surge: first, Arkas Logistics’ five dual-mode locomotives and 700 wagons enable Istanbul–Sofia container block trains that cut road running hours while keeping last-mile trucking intact; second, the Middle Corridor now discharges 40-foot high-cube boxes in Poti and Batumi, creating steady drayage demand toward Kapıkule. Sealed containers reduce cargo theft claims and speed cross-docking restowing at the Kocaeli and Tekirdağ depots. Box traffic also unlocks digital customs pre-clearance because QR-coded seals allow Bulgarian and Romanian officials to scan manifests curb-side, trimming onsite inspections.

By Distance: Long-Haul Prevails But Short-Haul Expands

Long-haul trips over 500 km accounted for 64.56% of the Turkey cross-border road freight transport market share in 2025, as Istanbul–Rotterdam, Bursa–Munich, and Gaziantep–Paris legs underpin weekly milk-run schedules for auto, textile, and white-goods makers. These lanes average EUR 12,000–15,000 (USD 13,963.6-17,454.6) per truck per month, even after empty backhauls are factored in, because operators bundle spot charters with contract cargo to reach 78% asset utilization. Two-driver teams and automated tachograph downloads help fleets remain compliant with EU working-time rules while shaving a full calendar day from the classic three-and-a-half-day Istanbul–Vienna leg.

Short-haul cross-border runs under 500 km are rising 5.55% annually. Romanian OEMs source Turkish plastic granulates on a 380 km Kapıkule–Pitești shuttle that completes in 10 hours, enabling same-day molding. Daily e-commerce sorties move 3,000–4,000 parcels from Çorlu warehouses to Sofia, Bucharest, and Thessaloniki, often in high-roof Sprinters that cross Kapitan Andreevo at off-peak midnight slots. Carriers prefer short distances to train rookie or female drivers because night-at-home rosters improve recruitment and retention, partially easing the 93,000-driver shortfall.

By Goods Configuration: Solid Goods Rule While Fluid Goods Hold Their Niche

Solid cargo held an 84.68% slice of the Turkey cross-border road freight transport market size in 2025, mirroring Turkey’s manufacturing export mix of body panels, tires, knitwear, and rolled steel. Palletized automotive parts depart Bursa at cube-max capacity and are reloaded with German powertrains or French electronics for inbound assembly lines, keeping bidirectional lanes profitable even after EU vignette hikes. Retail fashion, shipping in hanging-garment trailers, uses radio-frequency identification tags to sync with store planograms and lower inventory shrinkage. Polished-marble slabs from Afyonkarahisar transit 2,400 km to Italian stone mills on extendable decks that integrate GPS-linked vibration sensors to cut breakage claims.

The fluid goods segment is growing at a 5.89% CAGR, ride ADR-rated tankers that earn premium EUR 1.60–2.00 (USD 1.86-2.33) per km rates. Azeri crude and Iraqi distillates move north through Hakkâri and Van for Turkish refinery feedstocks, while ISO 22000-certified milk tankers haul UHT exports to Iraq and Saudi Arabia. Fluid-cargo specialists are upgrading to super-insulated cryogenic trailers with remote pressure telemetry, actively reducing boil-off and product loss. EU Green Deal regulations are already nudging some petrochemical shippers to transfer long legs onto rail tank containers, yet road remains indispensable for the first and final 100 km drays.

By Temperature Control: Non-Reefer Dominates Yet Reefer Climbs Quickly

Non-refrigerated units accounted for 84.77% of 2025 traffic because autos, textiles, metals, and construction materials withstand ambient temperatures ranging from –20 °C to +50 °C. Dry-van fleets have responded to fuel inflation by adopting low-rolling-resistance tires and predictive-maintenance telematics, which have cut unscheduled roadside events by 18%, supporting on-time delivery scores near 97%. Spot dry-freight rates on Istanbul–Sofia lanes, however, fell 5–8% in real terms during 2024-2025 as an oversupply of Bulgarian and Romanian rigs pressured margins.

Temperature-controlled freight is expected to reach almost a fifth of the Turkey cross-border road freight transport market size by 2031, as it compounds at 8.68% annually. Pharmaceutical hubs increasingly use reefer boxes fitted with GSM/Bluetooth sensors to ship 2–8 °C biologics, meeting rigorous EMA GDP validation requirements. Fresh fruit exporters in Mersin now deploy vent-door reefers that maintain 90% humidity and 4–8 °C, extending tomato shelf life by four days and unlocking premium shelf-ready prices in Vienna supermarkets. Logistics providers are deploying advanced reefer telemetry suites to actively push down spoilage claims and negotiate more favorable contracts based on lower waste. Diesel-powered cooling contributes 7–10 l extra burn per 100 km, yet clients accept a 30–50% price premium versus dry vans because cold-chain breaks can void entire loads valued above USD 100,000.

Geography Analysis

Bulgaria absorbed 36.91% of outbound volume in 2025, the largest share of the Turkey cross-border road freight transport market, because Kapıkule and İpsala channels nearly all TEN-T east–west flows into the EU. Stable industrial ties, USD 4.7 billion in Turkish exports, and ongoing border upgrades sustain a dense long-haul corridor linking to Romania, Hungary, and Germany. Border-crossing dwellers at Kapıkule remain a focal point for modernization works aimed at significantly reducing waiting-time costs.

Iraq is the fastest-growing lane, advancing at a 7.87% CAGR through 2031, on the back of USD 10.3 billion in Turkish exports and reconstruction outlays exceeding USD 88 billion for housing, roads, and power assets. Habur processed 1.75 million crossings in 2024 and will gain further throughput once the Development Road corridor significantly cuts Basra-to-border transit, accelerating Istanbul–Basra roundtrips.

Greece, Armenia, and Georgia collectively handle roughly one-quarter of Turkey’s cross-border truck count. Greek lines serve Italian and Spanish buyers via ferries from Patras and Thessaloniki, while Georgia and Armenia anchor the Middle Corridor, which lifted tonnage by 68% year-on-year in 2024 after Russia sanctions diverted freight. Short-haul e-commerce has added daily van routes into Bulgaria and Romania, and recent Saudi visa reforms are opening a nascent Gulf leg for early adopters.[4]Turkish Statistical Institute, “Foreign Trade Statistics 2024-25,” tuik.gov.tr

Competitive Landscape

Market structure remains moderately fragmented: the ten largest carriers hold about 35-40% of the Turkey cross-border road freight transport market, leaving a long tail of 500-plus SMEs that each operate fewer than 50 trucks. Fragmentation is starting to ease after DSV closed its USD 16 billion DB Schenker takeover in April 2025, creating a massive global giant that has begun bundling sea-air-road to aggressively undercut single-mode competitors on key European lanes.

Turkish incumbents are scaling through M&A and fleet renewal. CEVA’s strategic purchase of Borusan Lojistik significantly expanded its domestic warehousing and annual load-handling capacity, allowing a tighter grip on drayage and customs brokerage. Mars Logistics plowed EUR 70 million (USD 81.47 million) into trailers, tractors, and 100 rail wagons in 2026 to service just-in-time auto contracts, while Arkas Logistics bought five dual-mode locomotives and rolled out heavy-vehicle navigation to successfully trim fleet fuel burn and optimize routing.

Technology is now the main differentiator. Horoz Logistics’ IoT-led LTL platform optimizes routing to push empty-mile ratios below 15%, though network expansion costs have pressured short-term profitability, whereas OMSAN Logistics is exploring triangular EU–Saudi legs made possible by transit visa reforms, aiming to maximize asset utilization on complex roundtrips. White-space upside lies in pharmaceutical GDP-grade reefer lanes and intermodal road-rail shuttles that tap the Development Road corridor for mid-distance container flows.

Turkey Cross-Border Road Freight Transport Industry Leaders

Ekol Logistics

Netlog Logistics

Mars Logistics

CEVA Logistics (CMA CGM)

DHL Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Saudi Arabia began issuing 15-day transit visas to Turkish drivers, cutting approval times from up to 50 days to roughly three.

- February 2026: OMSAN Logistics unveiled a growth plan, including a Rotterdam–Istanbul alumina lane for ALMATIS and a Turkey–Romania raw-material shuttle for PLADIS.

- January 2026: Gebrüder Weiss bought 51% of Sienzi Lojistik, adding a 6,000 m² bonded terminal near Muratbey Customs to its Turkish network.

- April 2025: DSV finalized its USD 16 billion acquisition of DB Schenker, elevating capacity on EU–Turkey corridors and adding 50,000 trucks worldwide.

Turkey Cross-Border Road Freight Transport Market Report Scope

| Agriculture, Fishing, and Forestry |

| Construction |

| Manufacturing |

| Oil and Gas, Mining and Quarrying |

| Wholesale and Retail Trade |

| Others |

| Full-Truck-Load (FTL) |

| Less than-Truck-Load (LTL) |

| Containerized |

| Non-Containerized |

| Long Haul |

| Short Haul |

| Fluid Goods |

| Solid Goods |

| Non-Temperature Controlled |

| Temperature Controlled |

| Greece |

| Armenia |

| Bulgaria |

| Georgia |

| Iraq |

| Rest of Countries |

| By End User Industry | Agriculture, Fishing, and Forestry |

| Construction | |

| Manufacturing | |

| Oil and Gas, Mining and Quarrying | |

| Wholesale and Retail Trade | |

| Others | |

| By Truckload Specification | Full-Truck-Load (FTL) |

| Less than-Truck-Load (LTL) | |

| By Containerization | Containerized |

| Non-Containerized | |

| By Distance | Long Haul |

| Short Haul | |

| By Goods Configuration | Fluid Goods |

| Solid Goods | |

| By Temperature Control | Non-Temperature Controlled |

| Temperature Controlled | |

| By Country | Greece |

| Armenia | |

| Bulgaria | |

| Georgia | |

| Iraq | |

| Rest of Countries |

Key Questions Answered in the Report

What is the current size of the Turkey cross-border road freight market?

The market was valued at USD 10.08 billion in 2026 and is forecast to reach USD 12.91 billion by 2031, expanding at a 5.07% CAGR.

Which destination country handles the most Turkish trucks?

Bulgaria leads with 36.91% of total outbound volume because Kapıkule and İpsala feed directly into the EU TEN-T network.

Which segment is growing fastest?

Temperature-controlled cargo is set to climb at an 8.68% CAGR thanks to pharmaceutical cold-chain and fresh-produce demand.

How are visa reforms influencing Gulf lanes?

Saudi Arabia’s new 15-day transit visa, active since March 2026, is expected to boost Turkey–GCC trips from under 5,000 in 2024 to about 7,000 by 2028.

What is the biggest operational bottleneck for Turkish carriers?

A 17% domestic driver shortage about 93,000 vacancies reduces fleet utilization and pushes operators toward rail or intermodal options.

How will EU carbon rules affect Turkish hauliers?

The Carbon Border Adjustment Mechanism subjects roughly EUR 19 billion (USD 22 billion) of Turkish exports to carbon pricing from 2026, adding compliance overhead for backhaul trips into the EU.

Page last updated on: