High-Barrier Packaging Film Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.77 Billion |

| Market Size (2031) | USD 2.52 Billion |

| Growth Rate (2026 - 2031) | 7.34% CAGR |

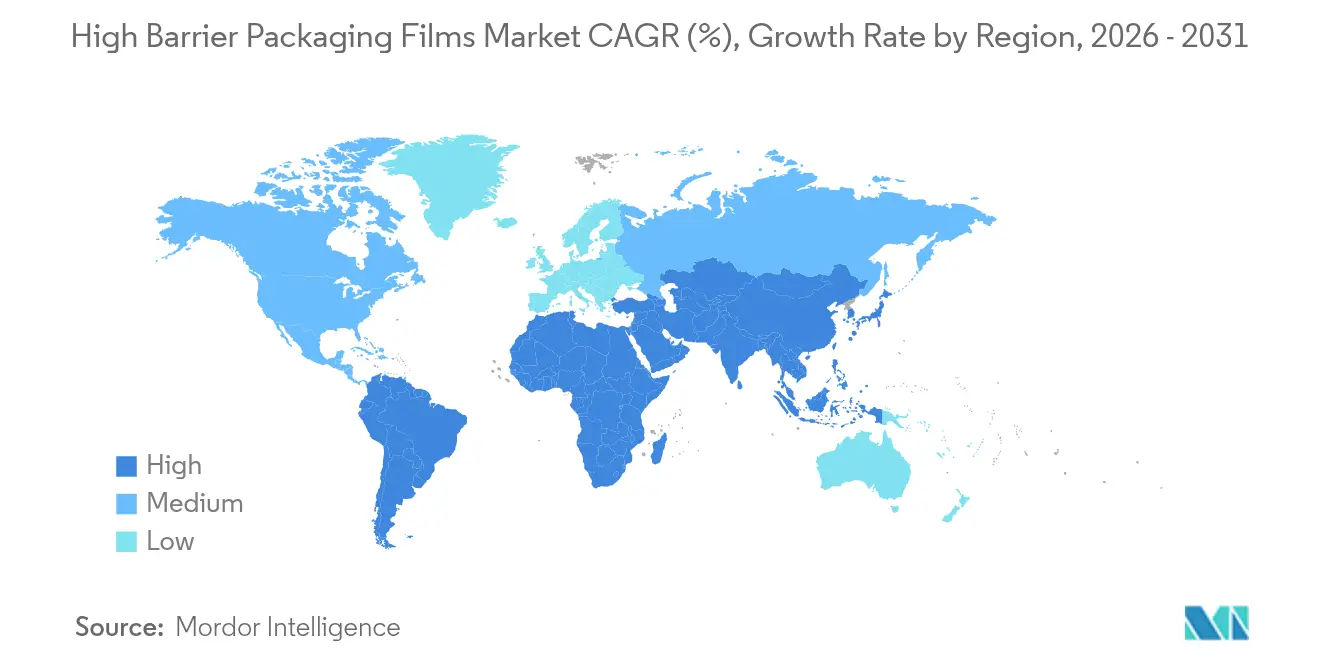

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

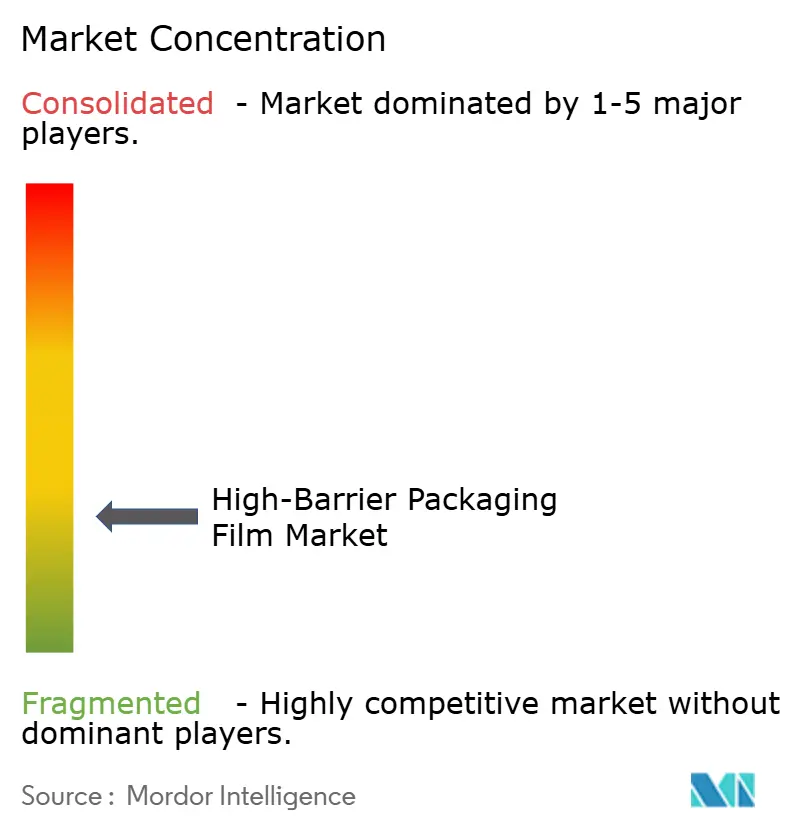

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

High-Barrier Packaging Film Market Analysis by Mordor Intelligence

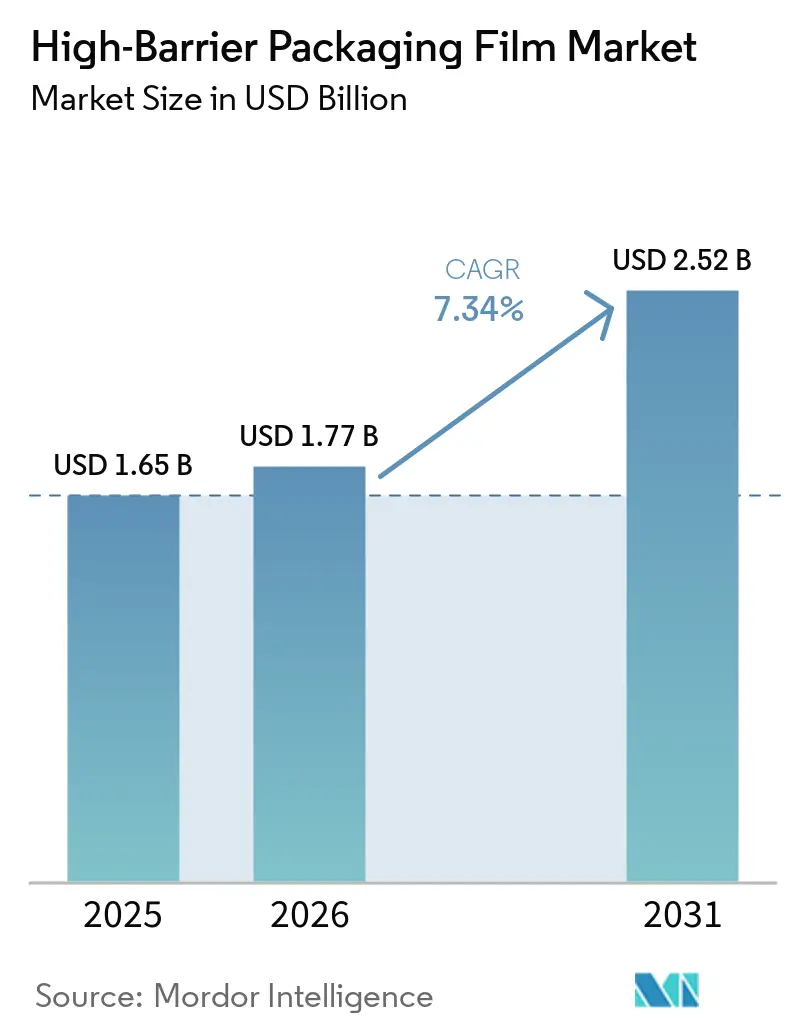

The high barrier packaging films market size in 2026 is estimated at USD 1.77 billion, growing from 2025 value of USD 1.65 billion with 2031 projections showing USD 2.52 billion, growing at 7.34% CAGR over 2026-2031. Rapid adoption of recyclable mono-material films, stronger demand for biologics cold-chain solutions, and surging e-grocery volumes underpin this expansion. The industry is also reacting to tougher Extended Producer Responsibility (EPR) rules that tie fees to recyclability, prompting converters to pivot toward machine-direction-oriented polyethylene (MDO-PE) and solvent-free organic coatings. Resin price volatility, supply pressure for key barrier resins such as PVDC and EVOH, and the capital intensity of new orientation lines are creating a cost pass-through race that rewards integrated players able to hedge raw-material swings.

Key Report Takeaways

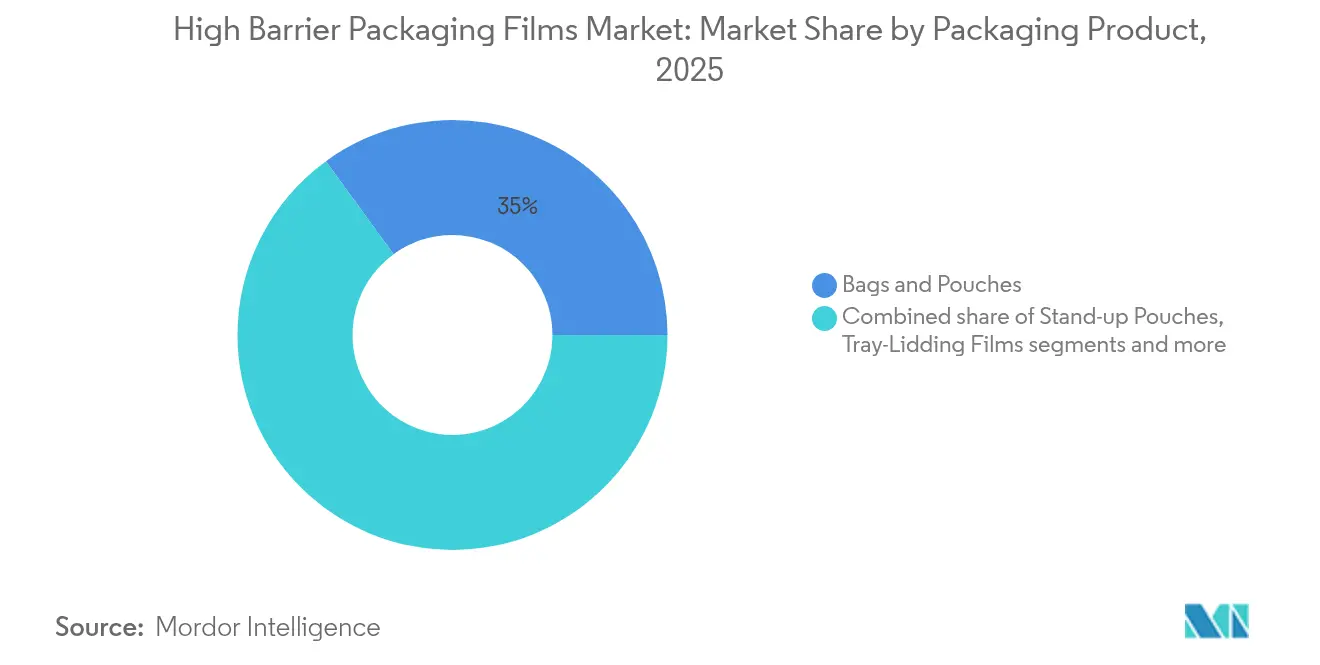

- By packaging product, bags and pouches held 35.02% revenue share in 2025; vacuum skin packs are forecast to post the fastest 9.43% CAGR through 2031.

- By material, polyethylene accounted for 32.21% of 2025 revenue, while biopolymers are expected to expand at a 10.02% CAGR to 2031.

- By end-user industry, food and pet food captured 65.12% revenue share in 2025; pharmaceutical and medical applications are projected to grow at an 8.21% CAGR.

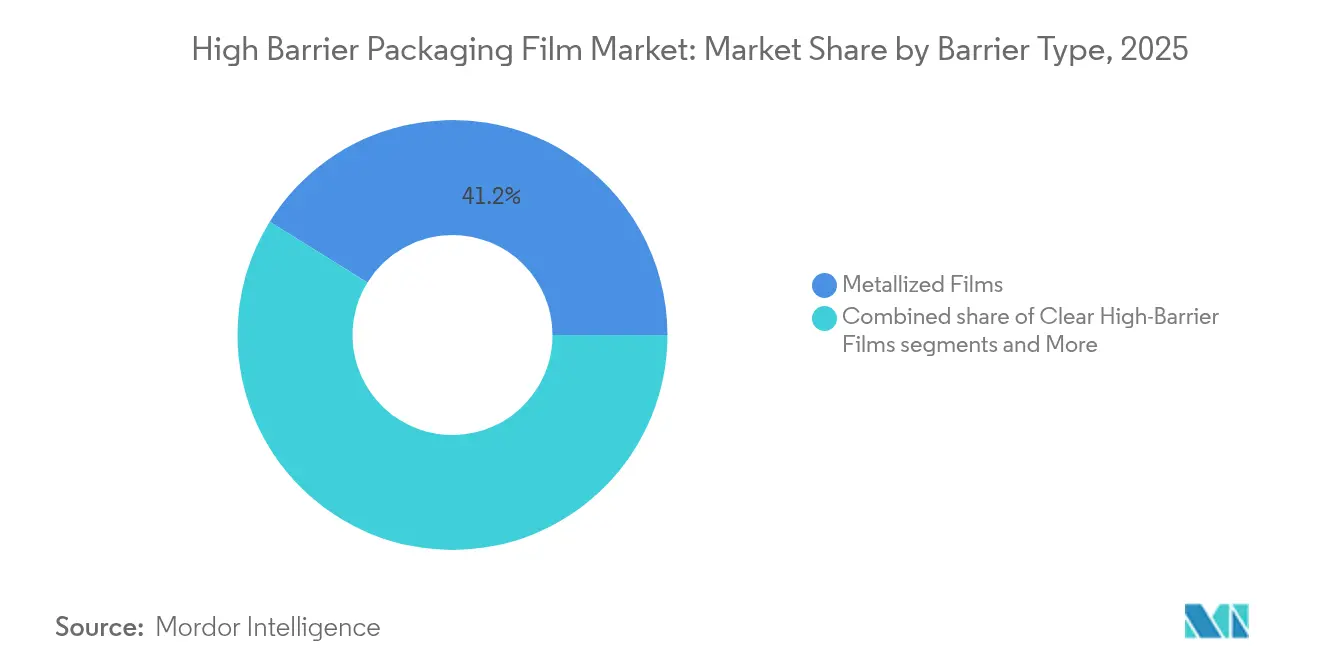

- By barrier type, metallized films led with 41.18% revenue share in 2025, whereas organic-coated films are set to advance at an 8.33% CAGR through 2031.

- By technology, multilayer co-extrusion (≤7 layers) commanded 60.05% revenue share in 2025; mono-material barrier films are projected to grow at a 8.89% CAGR to 2031.

- By geography, Asia-Pacific dominated with 42.31% revenue share in 2025; the Middle East and Africa is expected to climb at a 9.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global High-Barrier Packaging Film Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pharma blister boom in biologics and cold-chain logistics | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| E-grocery surge driving pouch and film demand | +0.9% | APAC core, spill-over to North America and Europe | Short term (≤ 2 years) |

| Shift from rigid to lightweight stand-up pouches in APAC | +0.8% | APAC, with early adoption in China, India, and ASEAN | Medium term (2-4 years) |

| High-protein pet-food formats relying on barrier pouches | +0.6% | North America and Europe, expanding to APAC | Long term (≥ 4 years) |

| Mono-material MDO-PE/BOPE adoption for recyclability | +1.1% | Europe leading, followed by North America | Long term (≥ 4 years) |

| NIR-detectable nano-coatings reducing EPR fees | +0.7% | Europe and select North American states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Pharma blister Boom in Biologics and Cold-chain Logistics

Global biologics therapies require oxygen transmission rates below 0.1 cc/m²/day and temperature stability from –20 °C to +25 °C, pushing converters to specify multilayer films containing EVOH and novel coatings that meet these strict thresholds. DS Smith’s TailorTemp fiber pack keeps chilled conditions for 36 hours, illustrating a switch to recyclable formats acceptable to regulators and hospitals. Oncology drugs valued at more than USD 10,000 per dose tolerate packaging cost premiums, allowing suppliers to command margins that offset higher-performance resin prices. Investment in regional cold warehouses in the United States and Germany is also lifting demand for heat-stable, puncture-resistant films compatible with dry-ice shipping.

E-grocery Surge Driving Pouch and Film Demand

Online retailers handle each grocery order three to five times before delivery, making puncture resistance and flawless seals mandatory. Converters respond by thickening sealing layers and adding higher-density tie resins that retain flexibility over a wider temperature range. Vietnam’s packaging sector, racing toward USD 3.5 billion by 2026, exemplifies how e-commerce economies jump directly to lightweight flexible formats. Sauces, condiments, and baby food moving into large stand-up pouches show 12% fewer breakages than glass jars during last-mile transit, underpinning brand conversions announced by multinational food manufacturers in 2025.

Shift from Rigid to Lightweight Stand-up Pouches in Asia-Pacific

Asian brand owners are trading rigid HDPE canisters for MDO-PE stand-up pouches because transport costs fall 30%, enabling lower shelf prices while improving sustainability metrics. Volpak reports that Chinese condiment fillers retooled four complete lines in 2024 to accommodate 350 ppm rotary fill-seal machines optimized for pouches.[1] Volpak, “Seasoning the Future: How Doypack Is Transforming Sauce Packaging,” volpak.com Lightweighting also aligns with cross-border export packaging rules, where South Korean food exporters must meet Japan’s new positive list for synthetic resins starting June 2025.[2]Food Packaging Forum, “Japan Preparing Food Contact Material Regulation,” foodpackagingforum.org

Mono-material MDO-PE/BOPE Adoption for Recyclability

Full-PE barrier pouch holds more than 95% polyethylene yet meets oxygen barrier targets of 0.2 cc/m²/day, proving that mono-material structures can displace traditional PET/PE laminates. Klöckner Pentaplast’s kp FlexiFlow flow-wrap films achieve 93% polypropylene content and run at 120 packs per minute on horizontal FFS lines, illustrating production speed parity with conventional solutions. European EPR systems levy up to EUR 800 per ton on non-recyclable multilayers, prompting pack owners to fund new orientation lines and converting know-how.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile PE/PP resin prices | -0.8% | Global, with acute impact in Asia-Pacific | Short term (≤ 2 years) |

| Plastic-waste regulations vs multilayer films | -0.6% | Europe leading, expanding to North America | Medium term (2-4 years) |

| Limited recycling for SiOx/AlOx BOPE | -0.4% | Europe and North America | Long term (≥ 4 years) |

| PVDC and EVOH supply crunch post-2027 | -1.0% | Global, with severe impact in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile PE/PP Resin Prices

North American polypropylene rose 4–5 cents per pound in early 2025 after refinery shutdowns tightened polymer-grade propylene supply, squeezing converters’ margins. Asian film makers also face competition from China’s planned 2.6 million-tonne PP export push in 2024, creating a price whipsaw and deterring long-term supply contracts. Smaller converters pass through costs more slowly, prompting some to scale back high barrier packaging films production until hedging tools become affordable.

PVDC and EVOH Supply Crunch Post-2027

PVDC still controls more than half of dry-food high barrier applications, yet new chlorinated-polymer rules in Europe and North America cap capacity additions, signaling a tight market beyond 2027. EVOH faces similar pressure because only a few global producers, led by Kuraray, plan incremental debottlenecking, leaving demand exposed to unplanned outages. Brand owners are consequently validating organic coatings and SiOx-coated BOPE well ahead of anticipated supply gaps, lengthening qualification timelines for new SKUs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Product: Vacuum Skin Packs Edge Forward

The segment led by bags and pouches banked 35.02% of 2025 revenue, while vacuum skin packs are projected to record a 9.43% CAGR through 2031, reflecting premium fresh meat and seafood brands’ need for up to 13-day shelf life in chilled supply chains. This portion of the high barrier packaging films market also benefits from attractive product visibility that drives higher cart values in e-grocery channels. Stand-up pouches continue to replace glass jars in sauces and infant food, aided by shipping-cost savings that run to USD 100 per pallet. Meal kit suppliers favor tray lidding films with peelable options compatible with microwave reheating, supporting moderate growth.

Vacuum skin packs require deeper forming and stronger puncture resistance, prompting film formulators to add linear low-density polyethylene seal webs and EVOH tie layers. Such packs often preserve 97% of modified-atmosphere oxygen at day eight, extending the sell-by date and shrinking food waste. Thermoforming films, mostly PET or PP-based, remain essential for blister packs in pharma, but growth lags as mono-material PE replacements pass regulatory audits. Sachets and flow wraps face consumer backlash in Southeast Asia, notably Indonesia’s 30% reduction target for sachet waste by 2029, pushing converters toward recyclable alternatives. Blister base films, despite regulatory headwinds, preserve share for high-value tablets that demand near-zero moisture ingress; converters hedge risk by offering bio-based PET versions.

By Material: Biopolymers Gain Momentum

Polyethylene retains the lion’s share at 32.21%, anchored by broad processing compatibility, although price volatility triggers quarterly reforms in sealing-layer blends to protect margin. Biopolymers such as PLA and PHA, while accounting for a single-digit slice, are clocking a brisk 10.02% CAGR, buoyed by retailer commitments to compost-ready packaging. The high barrier packaging films market size for biopolymers is still limited, but becomes meaningful when a large confectionery brand rolls out pouch lines across Europe, scaling annual demand to 12,000 tons.

Polypropylene follows as the solution for hot-fill applications and transparency, whereas BOPET retains importance for dimensional stability. EVOH’s sub-0.1 cc/m²/day oxygen barrier secures its premium price point even during raw-material shortfalls because no drop-in substitute matches performance at similar thickness. PVDC, though under scrutiny, remains the workhorse in coffee and seasoning sachets. Aluminum foil use recedes in flexible laminates due to sustainability claims, yet still prevails in retort pouches for ready-to-eat meals where 121 °C sterilization cycles demand metal performance. Organic coatings based on micro-fibrillated cellulose or chitosan draw interest because they add less than 1 µm of deposit yet cut overall weight, integrating well within existing gravure-coated production lines.

By End-User Industry: Pharmaceuticals Gather Pace

Food and pet food end uses dominate, absorbing 65.12% of 2025 industry turnover. Market leaders extend product shelf life to slash shrink in global supply chains; for example, dairy processors in India report 18% waste reduction after switching to five-layer EVOH pouches. Pharmaceutical and medical applications expand 8.21% CAGR as biologic injectables require validated cold-chain packaging that holds oxygen levels below stringent thresholds. High barrier packaging films market share for pharmaceuticals will rise further when large-scale fill-finish lines in North Carolina come online in 2026, demanding 1.2 billion unit-dose blisters annually.

Pet food premiumization fuels pouch demand with zip closures and aroma barriers that retain palatability for high-protein recipes. Beverage applications, though stable, see incremental growth from ready-to-drink coffee and sports nutrition powders adopting gusseted pouches. Cosmetics select laminated tubes with aluminum-free high-barrier melt-coated layers that resist essential-oil migration. Chemical and agricultural inputs make niche use of multi-wall barrier sacks but witness limited growth due to bulk IBC alternatives.

By Barrier Type: Organic Coatings Challenge Metallized Films

Metallized PET and OPP films still hold 41.18% share, delivering robust barrier at attractive economics, yet end-of-life constraints motivate CPG brands to explore clear barrier options. Organic-coated films capture an 8.33% CAGR by employing water-based dispersions that create liquid, grease, and vapor shields without hindering post-consumer sorting. The high barrier packaging films market size for organic coatings is small but strategic, as eco-labels pour resources into transparent, monomaterial packs that maintain product visibility on digital shelves.

Inorganic oxide-coated BOPE films grant near-glass barrier while offering recyclability advantages over aluminum foil, though their higher cost slows mass adoption. Hybrid solutions appear, combining thin metallization with compostable sealants, achieving balance between barrier and compostability. Metallized structures still lead in coffee, snack, and powdered beverage segments where light and oxygen sensitivity demand <0.3 cc/m²/day OTR at low incremental cost. Paper-based laminates with dispersion coatings make inroads into confectionery wraps, showing 45% weight reduction and improved tear strength, yet require machinery retrofits.

By Technology: Mono-Material Films Disrupt Multilayer Norm

Traditional 7-layer-or-less co-extrusion comprised 60.05% of 2025 sales because converters mastered the process and capital is fully amortized. Mono-material barrier films, however, post a 8.89% CAGR, driven by retailer mandates that all store-brand packaging be recycle-ready by 2028. The high barrier packaging films market is witnessing quick uptake of blown-film MDO lines capable of creating down-gauged BOPE, improving clarity and stiffness, and hitting OTR targets when paired with EVOH or nano-silica coatings.

High-layer (9- to 11-layer) co-extrusion continues for cook-in applications and deep-draw thermoforming, retaining share where precise layer interfaces modulate moisture and oxygen gradients. Cast film processes dominate for retort pouch lidding because they offer uniform gauge and glossy optics. Blown film retains strength advantages for heavy-duty sachets and bulk liners. Equipment vendors race to supply orientation modules that retrofit onto existing blown-film towers, giving converters flexibility to toggle between standard and MDO modes as order books shift.

Geography Analysis

Asia-Pacific retained 42.31% of 2025 revenue, sustained by rising middle-class consumption and a shift from rigid jars to flexible pouches that pare logistics costs. The Chinese government’s push to export 2.6 million tons of polypropylene in 2024 dampened resin prices, allowing regional converters to quote aggressive bids in export tenders yet exposing them to price whiplash. Japan’s positive list for food contact materials, effective June 2025, obliges film suppliers to qualify 21 polymer classes and 827 additives, lengthening time-to-market for new structures. Southeast Asia’s sachet dilemma sparks innovation in refillable pouches, aligning with Indonesia’s 30% waste-cut target by 2029.

Middle East and Africa expands at 9.35% CAGR, fueled by investment in pharmaceutical blister capacity and improved refrigerated transport corridors linking the Gulf to North and East Africa. Governments funnel health budgets into local vaccine plant start-ups that specify multilayer cold-chain pouches, propelling demand for EVOH-rich structures. Energy subsidies in Saudi Arabia reduce ethylene costs, giving regional integrated producers margin to support downstream barrier film investments.

North America, though mature, gains from biologics fill-finish expansions and premium pet food formats that rely on multi-layer pouches. EPR laws in California and Oregon levy fees by recyclability index, steering retailers toward mono-material solutions. Canada’s single-use plastics ban accelerates moves from thermoform clamshells to resealable PE pouches. Mexico leverages USMCA to attract co-extrusion investments, positioning itself as a near-shoring hub.

Europe remains a bellwether for circular economy mandates. EPR charges of up to EUR 0.80 per kilogram drive adoption of mono-material BOPE and barrier-coated papers. Amcor’s AmFiber paper received an EU patent for high barrier recyclable performance, validating movement away from foil amcor.com. Eastern Europe’s lower operating costs entice western brand owners to shift volume, yet cold winters test film toughness, spurring higher-impact resins.

South America records stable growth, hinged on processed foods and agricultural exports. Argentina and Brazil see currency swings that challenge import resin parity pricing, causing periodic substitution of barrier layers with cheaper blends. Regional recyclers lack capacity for metallized scrap, but new chemical recycling plants in Brazil promise to close loops by 2027.

Competitive Landscape

Market structure is fragmented. The USD 8.4 billion Amcor-Berry Global merger in April 2025 combines 400 plants, creating scale for recyclable film R&D and procurement leverage that tempers resin price spikes.[3]Amcor, “Amcor Completes Combination with Berry Global,” amcor.com Toppan’s USD 1.8 billion pickup of Sonoco’s thermoformed and flexibles arm delivers ready access to North American food and healthcare customers, shortening commercialisation times for high barrier packaging films Roche lines. Novolex and Pactiv Evergreen’s merger consolidates food-service flexible packaging, providing integrated sheet extrusion, bag making, and compostable film assets.

Strategic focus has moved from sheer capacity to recyclability credentials. Leaders invest in MDO kit, solvent-free coating stations, and near-infrared detectable inks that reduce EPR fees. Mid-tier players chase niche advantages: European start-ups commercialize chitosan-coated BOPE for premium chocolate bars; Asian specialists roll out high-oxygen-barrier heat-shrink sleeves for dairy PET bottles. Patent filings cluster around NIR-detectable coatings and bio-based tie resins, as documented by recent luminescent-varnish work aimed at digital anti-counterfeiting.

Raw-material access dictates competitive positioning. Integrated resin producers such as ExxonMobil and Dow leverage internal ethylene production to smooth price spikes. Convertors without backward integration partner through long-term offtake contracts or vertical deals; for example, Middle Eastern polymer giants supply EVOH blends to European co-extruders under five-year cost-plus formulas. Sustainability credentials now influence procurement, with global CPGs awarding multi-year LTA contracts to film makers that can prove ≥95% mono-material content and confirmed curbside recyclability.

High-Barrier Packaging Film Industry Leaders

-

Amcor plc

-

Cosmo Films Limited

-

Celplast Metallized Products Limited

-

Glenroy, Inc.

-

Huhtamaki Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Toppan agreed to acquire Sonoco’s thermoformed and flexibles business for USD 1.8 billion to boost high barrier film capability.

- October 2024: Klöckner Pentaplast released kp FlexiFlow recyclable PE and PP barrier wraps that cut package weight by 75% and hit 120 ppm line speed.

- May 2024: Plastchim-T bought Manucor S.p.A., raising BOPP capacity to 200,000 tons and expanding EMEA reach.

- January 2024: Mold-Tek Packaging opened three Indian plants adding 5,500 MTA capacity for pharma barrier tubs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the high-barrier packaging film market as flexible mono- or multilayer polymer sheets engineered to hold oxygen, water vapor, aromas, and light below documented limits, which keeps food, beverage, pharmaceutical, and personal-care packs stable for longer.

Scope exclusion: rigid laminates, stand-alone aluminum foils, and commodity stretch or shrink wraps are outside our universe.

Segmentation Overview

-

By Packaging Product

- Bags and Pouches

- Stand-up Pouches

- Tray-Lidding Films

- Thermoforming Films

- Stretch and Shrink Wrap

- Blister Base Film

- Flow-wrap and Sachets

- Vacuum Skin Packs

-

By Material

- Polyethylene (LDPE, HDPE, MDO-PE)

- Polypropylene (BOPP, CPP)

- Biaxially Oriented Polyethylene Terephthalate (BOPET)

- Ethylene Vinyl Alcohol Copolymer (EVOH)

- Polyamide

- Aluminium Foil

- Polyvinylidene Chloride (PVDC)

- Biopolymers (PLA, PHA)

- Other Material

-

By End-user Industry

-

Food and Pet Food

- Meat and Seafood

- Dairy and Cheese

- Snacks and Confectionery

- Beverages

- Pharmaceutical and Medical

- Personal Care and Cosmetics

- Electronics

- Agriculture and Chemicals

-

Food and Pet Food

-

By Barrier Type

- Metallized Films

- Clear High-Barrier Films

- Organic-coated Films

- Inorganic Oxide Films

-

By Technology

- Multilayer Co-extrusion (?7 layers)

- High-layer (>7) Co-extrusion

- Mono-material Barrier Films

- Other Technology

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- ASEAN

- Australia and New Zealand

- Rest of Asia-Pacific

-

Middle East and Africa

-

Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

-

Africa

- South Africa

- Kenya

- Rest of Africa

-

Middle East

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

We spoke with converters, resin makers, and large brand owners across North America, Europe, and Asia. Their input on average selling prices, line utilization, and the pace of the shift toward recyclable mono-material designs filled gaps left by secondary work.

Desk Research

We linked United Nations Comtrade trade codes for multilayer PE and PP films with Eurostat output indices and USDA cold-chain statistics, then matched those signals with insights from the Flexible Packaging Association, PlasticsEurope, and the Institute of Packaging Professionals. Company 10-Ks, D&B Hoovers financial snapshots, Questel patent timelines, and pricing alerts from Dow Jones Factiva helped Mordor analysts map fresh capacity starts and resin swings. The sources named are illustrative; many additional public datasets informed cross-checks.

Next, we overlaid government water-vapor transmission norms and recycled content mandates across ten economies to trim non-addressable demand, while Volza shipment data showed the share of MDO-PE exports already carrying barrier coatings.

Market-Sizing & Forecasting

A top-down model reconstructs global demand from HS-392062 and HS-392190 flows and values them with region-specific ASPs gathered during calls. Sampled converter revenue roll-ups and pouch output serve as bottom-up sense checks. Key drivers include retort pouch penetration, cold-chain lane expansion, new co-extrusion lines, resin price curves, evolving EPR timelines, and mono-material uptake. We project them to 2030 with multivariate regression plus ARIMA, followed by scenario analysis for resin volatility.

Data Validation & Update Cycle

Analysts run variance sweeps against converter utilization and export data, route anomalies for senior review, and only then sign off. Reports refresh annually; material shocks trigger interim passes, and a final review happens before delivery.

Why Mordor's High-Barrier Packaging Films Baseline commands reliability

Published values often differ because each publisher applies its own scope, price ladder, and refresh rhythm.

According to Mordor Intelligence, our disciplined scoping and dual-path validation keep figures reproducible and balanced. Key gap drivers elsewhere include adding mid-barrier grades, folding foils into totals, using flat global ASPs, or relying on outdated tonnage factors.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.65 Bn (2025) | Mordor Intelligence | - |

| USD 35.80 Bn (2024) | Regional Consultancy A | Adds mid-barrier films and foils, scant primary checks |

| USD 34.10 Bn (2023) | Global Consultancy B | Shipment tonnage × flat ASP, no recycled content adjust |

| USD 22.16 Bn (2024) | Industry Journal C | Mixes rigid laminates, vague scope |

In short, we expose every assumption, refresh data yearly, and tie numbers back to public codes or first-hand interviews, giving decision-makers a dependable baseline for strategic moves.

Key Questions Answered in the Report

What is the current size of the high barrier packaging films market?

The high barrier packaging films market reached USD 1.77 billion in 2026 and is projected to climb to USD 2.52 billion by 2031 at a 7.34% CAGR.

Which region leads the high barrier packaging films market?

Asia-Pacific dominates with 42.31% of 2025 revenue thanks to rapid conversion from rigid containers to flexible pouches.

Why are mono-material films gaining ground?

Retailers and regulators impose EPR fees on non-recyclable packs, so brands adopt mono-material MDO-PE or BOPE structures that meet curbside recycling guidelines while retaining barrier performance.

Which packaging product segment is growing fastest?

Vacuum skin packs show a 9.43% CAGR through 2031 because they extend chilled shelf life and improve product visibility, benefitting fresh meat and seafood suppliers.

What restrains market growth?

Volatile polyethylene and polypropylene prices and a looming supply squeeze for PVDC and EVOH resins after 2027 create cost and sourcing challenges for converters.

How are leading companies responding to sustainability pressures?

Firms invest in MDO lines, solvent-free organic coatings, and NIR-detectable inks, while mergers such as Amcor-Berry Global create scale to fund recyclable barrier technology rollouts.

Page last updated on: