Solar Tree Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

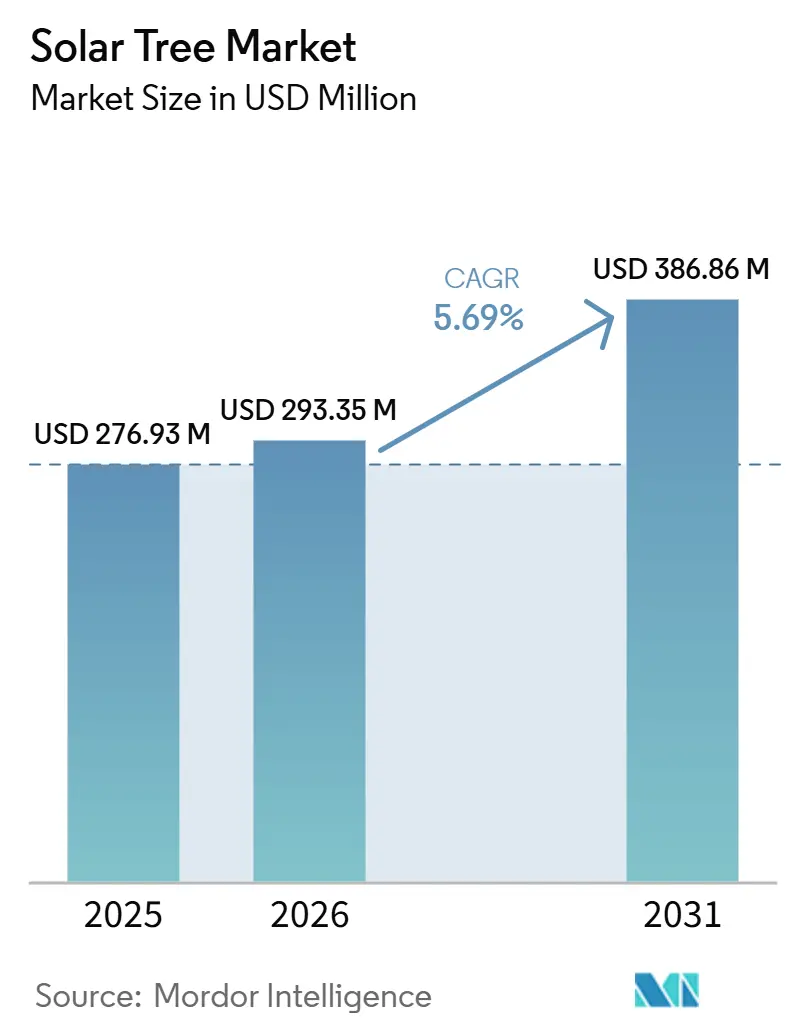

| Market Size (2026) | USD 293.35 Million |

| Market Size (2031) | USD 386.86 Million |

| Growth Rate (2026 - 2031) | 5.69% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

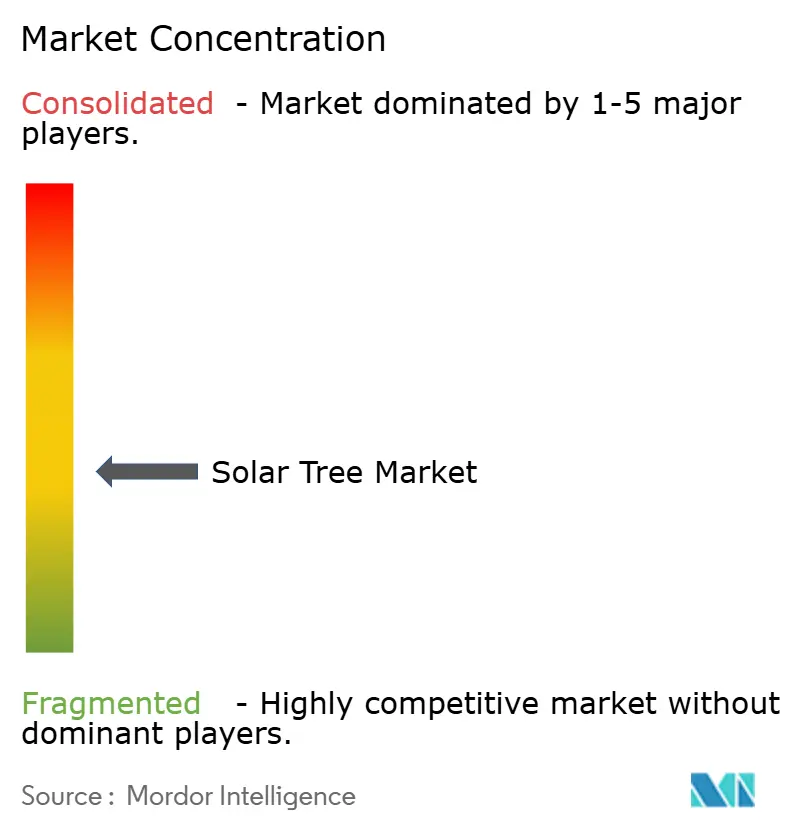

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Solar Tree Market Analysis by Mordor Intelligence

The Solar Tree Market size is projected to be USD 276.93 million in 2025, USD 293.35 million in 2026, and reach USD 386.86 million by 2031, growing at a CAGR of 5.69% from 2026 to 2031. Rapid urbanization is reducing available roof space, pushing city planners toward vertical solutions that also serve as public amenities. Off-grid configurations are dominant because they avoid lengthy interconnection queues and provide power resilience during disasters. Hybrid units are growing rapidly as municipalities combine batteries with grid-tied electronics to meet resiliency codes and peak-shaving targets. Material innovation, particularly bio-resin composites, reduces structural weight, easing permitting in seismic zones. The competitive landscape is intense but fragmented; no vendor holds more than a 15% revenue share, which keeps pricing pressure high while also driving product differentiation.

Key Report Takeaways

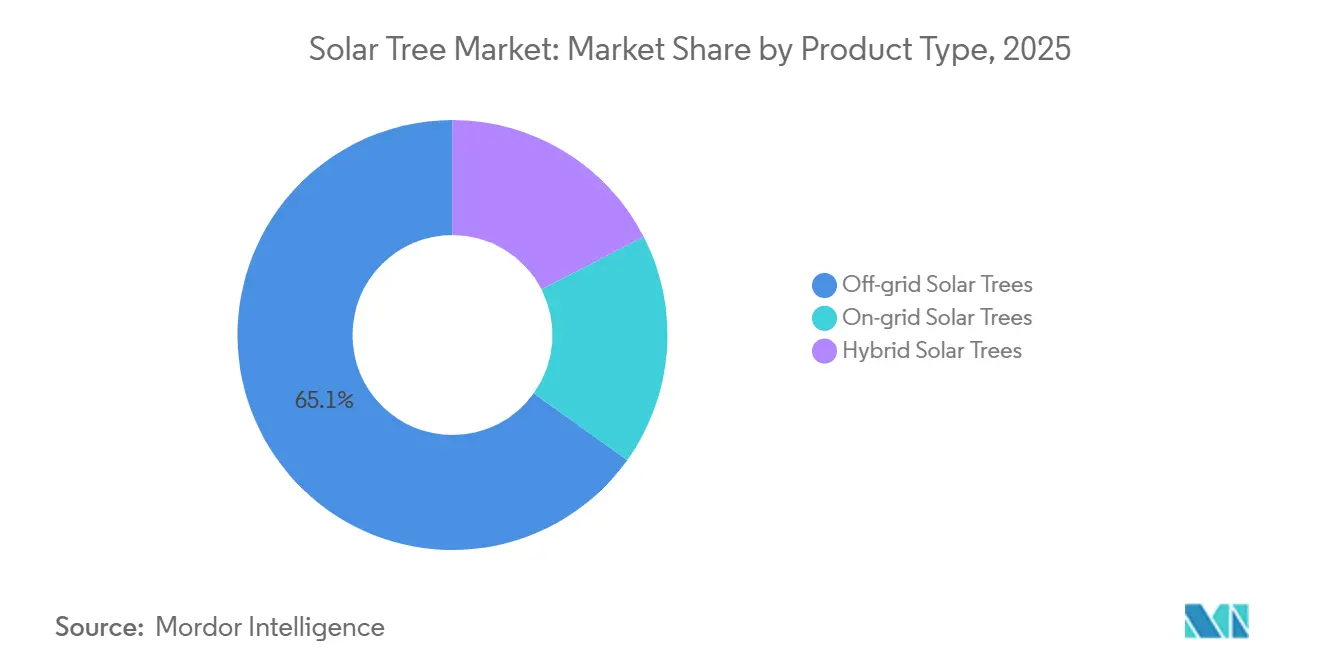

- By product type, off-grid systems held the largest share at 65.1% of the solar tree market in 2025. Hybrid systems are forecast to grow at a 7.4% CAGR through 2031.

- By solar panel technology, monocrystalline held the largest share at 74.7% of the solar tree market in 2025. Thin-film and BIPV are forecast to grow at an 8.4% CAGR through 2031.

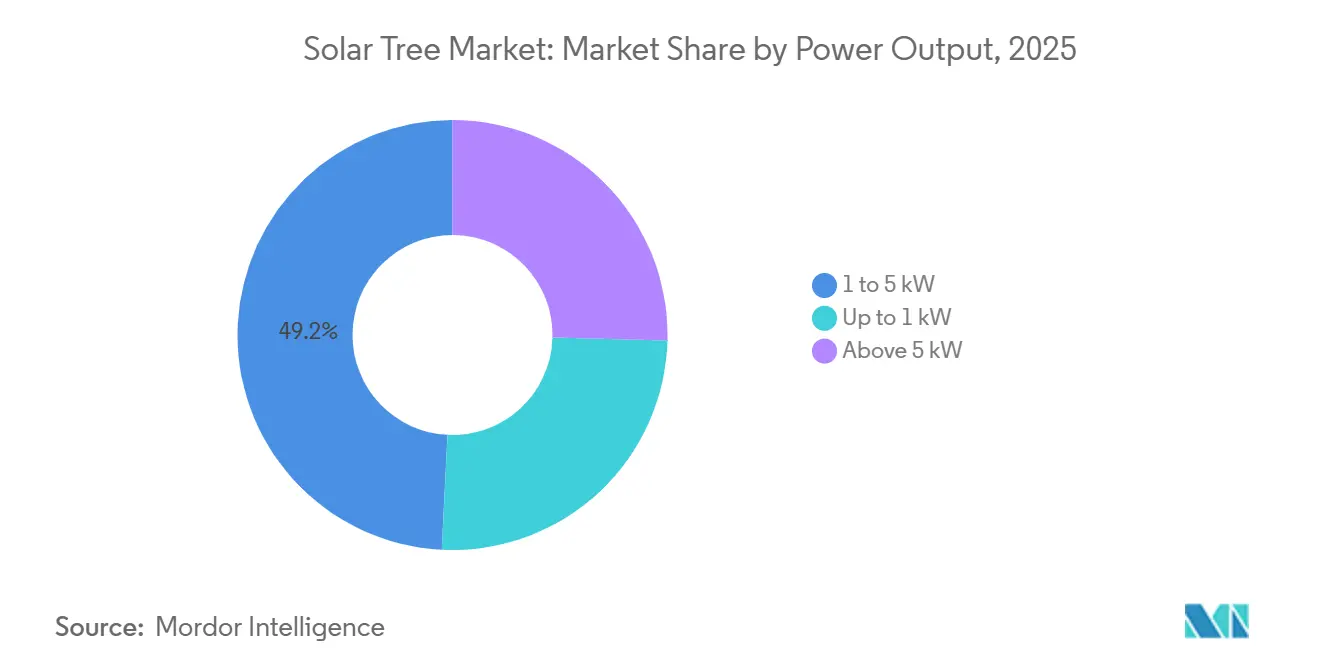

- By power output, the 1 to 5 kW segment held the largest share at 49.2% of the solar tree market in 2025. The above 5 kW segment is forecast to grow at a 6.8% CAGR through 2031.

- By installation mode, free-standing/foundation installations held the largest share at 89.8% of the solar tree market in 2025. Modular/mobile units are forecast to grow at a 10.1% CAGR through 2031.

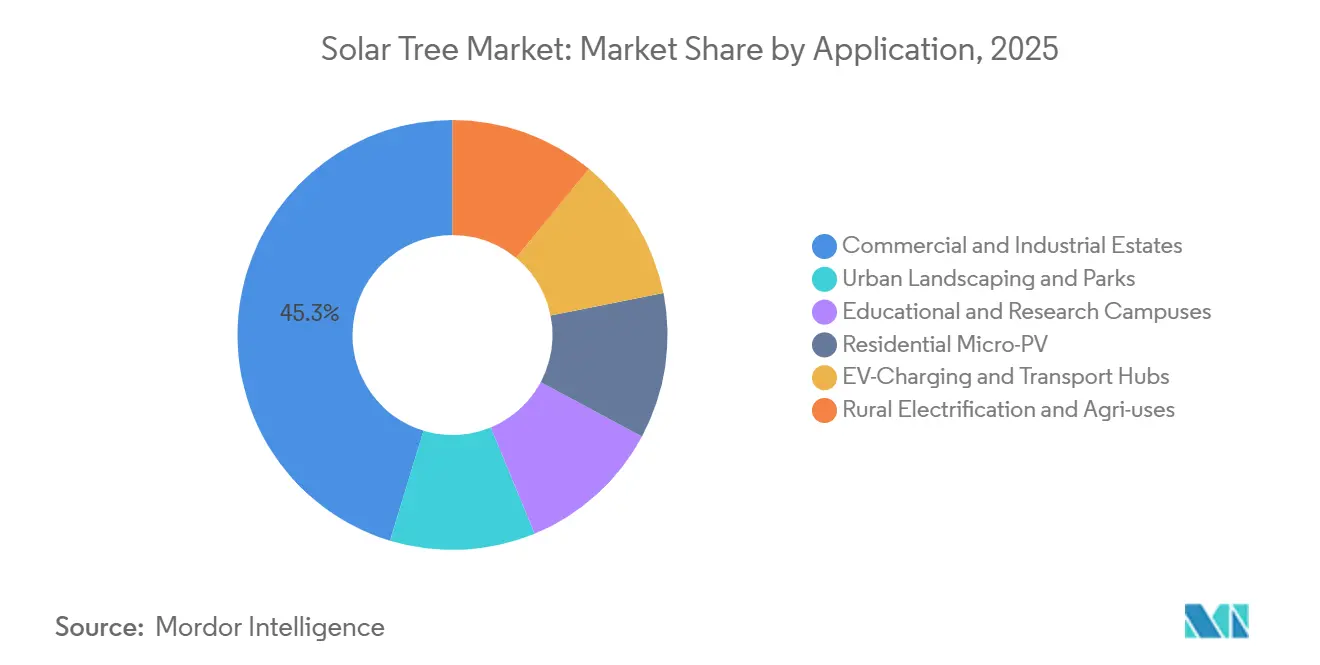

- By application, commercial and industrial held the largest share at 45.3% of the solar tree market in 2025. EV charging and transport applications are forecast to grow at a 7% CAGR through 2031.

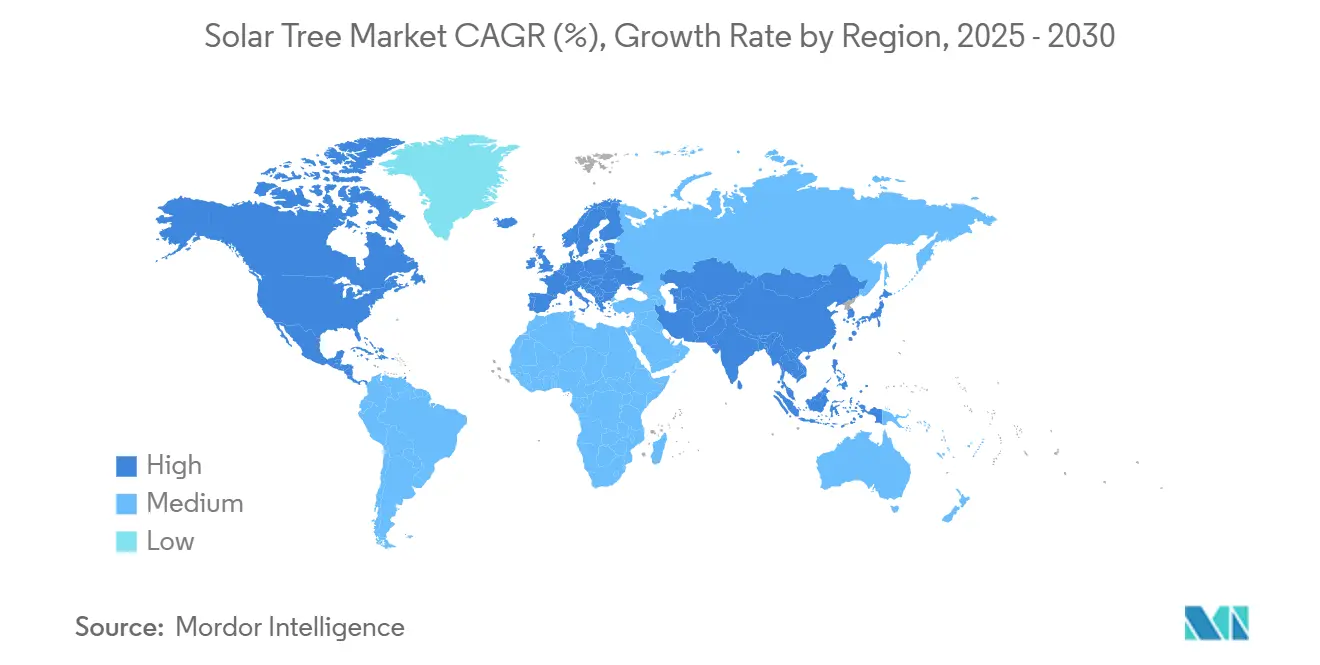

- By geography, Asia-Pacific accounted for 45.9% of revenue in 2025 and is forecast to grow at a 6.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Solar Tree Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewable-energy mandates from >70 countries | +1.8% | Global, with EU, California, and India leading enforcement | Medium term (2-4 years) |

| Urban greening & smart-city furniture demand | +1.2% | APAC core (China, India, ASEAN), spill-over to Middle East | Medium term (2-4 years) |

| Space-efficient power for land-scarce metros | +0.9% | North America & EU metro cores, Japan, South Korea | Long term (≥4 years) |

| Surge in EV-charging nodes needing solar trees | +1.4% | North America, EU, China coastal cities | Short term (≤2 years) |

| Lightweight bio-resin mast reduces install time | +0.4% | Global, early adoption in EU and North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Renewable-Energy Mandates From Over 70 Countries

Policy targets are steering procurement toward distributed generation, and the solar tree market benefits when land or roof constraints rule out flat panels. The European Union’s revised Renewable Energy Directive compels member states to hit 42.5% renewable electricity by 2030.[1]European Commission, “REPowerEU Plan,” europa.eu California’s SB 100 and Title 24 codes now require solar-ready infrastructure on new parking structures, nudging owners toward canopy-style solar trees.[2]California Energy Commission, “Title 24, 2026 Building Standards,” energy.ca.gov Maryland’s HB 1036 demands solar on 50% of state-agency parking space by 2030, instantly creating a 200-megawatt opportunity. India’s National Solar Mission seeks 500 gigawatts of renewables by 2030 and channels Smart Cities Mission funds into energy-generating street furniture.[3]Ministry of New and Renewable Energy, “National Solar Mission Update,” mnre.gov.in Although few rules explicitly name solar trees, municipal planners increasingly select them where rooftops are saturated or architecturally protected.

Urban Greening and Smart-City Furniture Demand

City councils are combining carbon-neutrality goals with placemaking by adopting energy-producing amenities. Dubai Municipality installed 103 Smart Palm units that generate 7.2 kWh per day while offering Wi-Fi and device charging, establishing these as tourist landmarks. Similar strategies are emerging across ASEAN mega-cities, where solar trees shade walkways, reduce lighting costs, and collect data via embedded sensors. Public interest and social media visibility are accelerating budget approvals, giving suppliers an entry point into otherwise conservative procurement channels. Integrated designs are also increasing land value around deployment sites, which developers use to recoup capital costs.

Space-Efficient Power for Land-Scarce Metros

Downtown parcels in Tokyo or Manhattan are valued at over USD 10,000 per square meter, making vertical arrays, which occupy a tenth of the footprint, financially attractive. In 2025, Japan's Tottori City installed 178.5 kW of bifacial panels over a parking area, preserving revenue from vehicle stalls while meeting 25% of civic power needs. Bifacial orientation increases production during morning and evening peaks, aligning with time-of-use tariffs. Studies in Seoul report 18% higher annual energy output per square meter compared to horizontal panels, supporting the case for vertical high-density installations.

Surge in EV-Charging Nodes Needing Solar Trees

Grid upgrade queues and demand charges are making off-grid charging increasingly attractive for fleet operators. Beam Global's EV ARC system deploys in four hours and requires no trenching, a key differentiator for government customers that helped secure statewide contracts in New Jersey in 2026. The University of Washington funded a 20-charger solar canopy through a USD 1.2 million grant, demonstrating that blended finance can accelerate campus adoption. When utility demand charges exceed USD 15 per kW monthly, a condition present in 60% of U.S. commercial tariffs, solar-augmented chargers achieve a lower lifetime cost than grid-only solutions.

Restraints Impact Analysis of Solar Tree Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial CAPEX vs. rooftop PV | -1.1% | Global, most acute in price-sensitive emerging markets | Medium term (2-4 years) |

| Low consumer / EPC familiarity outside EU | -0.7% | North America, APAC (excluding Japan), Middle East & Africa | Short term (≤2 years) |

| Height & aesthetic by-laws in heritage districts | -0.6% | EU historic centers, North America urban cores, select APAC cities | Long term (≥ 4 years) |

| Complex O&M for articulated petal designs | -0.4% | Global, with higher impact in regions lacking technical expertise | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial CAPEX vs. Rooftop PV

Installed costs of USD 4.50-6.00 per W remain 30-50% above flat roof installations, according to DOE benchmarks. This gap narrows where parking shade or branding generates additional revenue; however, municipal budgets often default to lower-cost carport arrays. Brazil's distributed-generation outlays are declining for 2026, putting pressure on premium products. Financing options are evolving, with Connecticut Green Bank's February 2026 RFP explicitly permitting solar trees on constrained sites, but such structures remain uncommon, maintaining friction in the sales cycle.

Low Consumer / EPC Familiarity Outside EU

Only 15% of US commercial solar installers have completed a solar tree project, and most operations and maintenance (O&M) vendors are unfamiliar with routine upkeep tasks such as actuator lubrication. Bidder counts on US municipal tenders average 2.3, approximately half the level seen for rooftop projects, which drives up prices. Europe benefits from a decade of standardized guidelines developed by SolarPower Europe, which also provides installer training. US vendors such as Beam Global now offer three-day certification programs; however, scaling remains a challenge, particularly as rooftop installations continue to occupy most installer capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Solar Tree Market Segment Analysis

By Product Type:

Off-Grid Dominance Meets Hybrid AccelerationOff-grid systems accounted for 65.1% of 2025 revenue, primarily because rural programs and disaster response agencies prioritize plug-and-play reliability. ECOSUN's containerized Mobil-Grid replaces diesel at remote mines, with payback periods of under four years when fuel costs exceed USD 0.40 /kWh.[4]ECOSUN Innovations, “Mobil-Grid Datasheet,” ecosun.eu Hybrid systems are growing at a 7.4% CAGR as battery costs decline toward USD 75/kWh, enabling cities to capture feed-in credits while maintaining power during outages through on-site storage. On-grid-only designs remain present in European feed-in-tariff markets but are losing share elsewhere.

Municipal pilots demonstrate functional convergence across applications. Florida Power & Light's SolarNow program deployed more than 100 hybrid units across 70 venues before the program ended in 2025, showing that visitor centers benefit from backup power during hurricanes. Engineering institutions such as Dayananda Sagar College are integrating small wind rotors onto solar trees, attracting research funding despite a 25% higher capital expenditure. Installations in dusty Sahel environments show 15–20% annual energy losses without regular cleaning, prompting manufacturers to adopt hydrophobic coatings.

By Solar-Panel Technology:

Monocrystalline Incumbency Faces Aesthetic DisruptorsMonocrystalline silicon held a 74.7% market share in 2025, driven by cost advantages from mass production. JinkoSolar's TOPCon cells exceed 23% efficiency, enabling fewer panels per installation and lighter mast structures. The market share of thin-film and building-integrated variants is expected to rise, as heritage sites reject reflective glass. Dubai's ASCA organic-photovoltaic palms demonstrate how flexible modules meet design requirements that conventional hardware cannot fulfill.

Perovskite tandem research indicates potential efficiency of 25% alongside 70% weight savings; however, warranties remain under ten years, limiting adoption in municipal contracts that require 20-year coverage. Bifacial modules capture 10-18% additional yield from ground albedo, with Japan's east-west rack installations monetizing this through peak-price arbitrage. Growing diversification is prompting panel suppliers to specialize, lightweight film for mobile kits and TOPCon monocrystalline for grid-tied installations, reshaping procurement alliances across the market.

By Power Output:

Mid-Range Dominance, High-Output SurgeSystems rated 1–5 kW accounted for 49.2% of 2025 installations, driven by applications such as park lighting and USB charging. The CSIR-CMERI 53.6 kW installation demonstrates scalability at the higher end; however, systems above 5 kW often require additional structural review, adding months to the permitting process. Above-5 kW units are growing at a 6.8% CAGR, supported by EV charging hub deployments. Walmart's 980 kW canopy installation in Arizona, which integrates 150 chargers, achieved a two-year payback period following demand-charge reductions.

Micro-tree units under 1 kW serve bus shelters and temporary festival installations but face cost challenges at USD 8/W. Storage integration is blurring capacity boundaries: a 3 kW solar tree paired with a 10 kWh battery can deliver 24-hour lighting at USD 0.104/kWh under Las Vegas irradiance conditions, making it more cost-effective than diesel for health clinic applications. As EV fleets expand, high-output dual-purpose canopies are expected to capture a larger share of the market.

By Installation Mode:

Foundation Lock-In, Modular MobilityConcrete-anchored installations accounted for 89.8% of 2025 deployments, as 20-year asset lifespans justify the associated civil works. Japan's patented UP-Stand piles reduce excavation requirements, allowing owners to utilize boundary spaces that were previously unusable. The modular kits segment is smaller but growing at 10.1% annually, driven by demand from NGOs and military organizations for containerized energy solutions that can be deployed quickly. Africa GreenTec's Solartainer delivers 50-100 kW with 200 kWh of storage in a single unit, making it suitable for humanitarian missions.

Chinese low-cost container kits are priced up to 50% below Western alternatives; however, donors continue to select premium vendors due to after-sales support and financing arrangements. Rooftop installations remain uncommon because of structural load limits above 50 kg/m², though bio-resin masts may ease these constraints, potentially opening hotels and high-rise terraces as a niche opportunity.

By Application:

Commercial Anchor, EV-Charging CatalystCommercial and industrial estates accounted for 45.3% of 2025 revenue, driven by applications in shade provision, branding, and peak-demand reduction. A retail campus in Quanzhou reduced energy consumption by 30%, saving approximately USD 69,000 annually through solar parking roofs. EV-charging hubs represent the fastest-growing application segment at a 7.0% CAGR; Beam Global's state contract demonstrates how agencies avoid substation upgrades by adopting solar trees with integrated storage.

Education campuses and urban parks represent the next largest applications, with demand driven by visibility and curriculum integration. The University of Washington's February 2026 installation offsets 25% of facility load and supports 20 Level 2 chargers, illustrating the multi-benefit economics of solar tree deployments. Agrivoltaic pilots in Kenya provide cattle shade and power water pumps, indicating potential future diversification as capital expenditure declines.

Geography Analysis

APAC Solar Tree Market

Asia-Pacific retained 45.5% of 2024 revenue and is on track for a 6.2% CAGR to 2030, supported by dense urbanization, aggressive renewable-portfolio standards, and regional supply-chain depth that lowers hardware costs. China’s build-out of an 8 GW desert complex demonstrates the scale benefits that spill into component pricing for regional municipal projects. Singapore and Thailand layer policy incentives on imported electricity and regional grid links, ensuring continuous demand for compact, high-yield solutions in land-scarce metros.

North America and Europe Solar Tree Market

North America and Europe form a mature, policy-driven corridor where zero-carbon building codes and corporate ESG targets sustain steady orders despite higher labor costs. California’s commercial solar mandate and New York City’s Local Laws 92/94 set compliance floors that favor vertical arrays when roofs are fully utilized. In Europe, differential tax credits—from Germany’s 30% write-off to Italy’s Superbonus—shape country-level growth trajectories, yet shared land-scarcity issues in historic cores tilt buyers toward sculptural solar options. The 93.1 GW annual solar-addition outlook through 2027 deepens the pipeline for specialty formats that coexist with strict urban-design codes.

South America and MEA Solar Tree Market

South America, the Middle East, and Africa collectively account for a smaller revenue slice but exhibit outsized long-run potential. Falling module prices doubled panel sales in Niger and seeded demand for vertical arrays that can bypass fragile grids. Ghana’s 16.8 MW rooftop showcase illustrates how donor-backed programs accelerate first-mover projects that validate performance under tropical conditions. As financing tools mature, these regions are expected to leapfrog directly to modular, off-grid trees for irrigation, healthcare, and telecom towers.

Competitive Landscape

The solar tree market is moderately fragmented. Beam Global leverages patents for rapid-deploy solar chargers and recorded a 50% revenue increase in Q4 2025. Tata Power Solar combines upstream wafer output with EPC services, positioning itself for India's domestic-content pipeline, and unveiled a 10-GW ingot plant in November 2025. Paired Power secured a U.S. patent in August 2025 covering 42 kWh storage integrated beneath its PairTree canopy, adding resilience appeal.

Smaller players are establishing niches. LightLeaf Solar's carbon-fiber modules weigh one-quarter of glass panels, reducing crane rental costs by 30% for remote installations. ENGO Planet embeds kinetic tiles to harvest pedestrian energy, broadening revenue streams in high-foot-traffic plazas. Cofly Energy pursues wind-solar hybrids for coastal resorts and has secured early pilots in Oman.

Key strategic themes include vertical integration to buffer supply disruptions, geographic diversification to capitalize on subsidy differences across markets, and multi-function amenities, Wi-Fi, sensors, and advertising screens that improve payback beyond simple kWh sales. With no dominant market leader, municipalities face high search costs and often default to established vendors with proven maintenance records.

Solar Tree Industry Leaders

Beam Global (ex-Envision Solar)

Smartflower Solar

Tata Power Solar – Solar-Tree Division

SolarBotanic Trees Ltd.

Spotlight Solar

- *Disclaimer: Major Players sorted in no particular order

Solar Tree Market Companies Covered in this Report

- Arka Energy

- Beam Global

- Big Sun Energy Technology Inc.

- Cofly Energy

- CSIR - Central Mechanical Engineering Research Institute (CSIR-CMERI)

- ENGO Planet

- Envision Solar International, Inc.

- Heliatronics, Inc.

- Ideematec Deutschland GmbH

- JinkoSolar Holding Co., Ltd.

- NXTGEN NanoTree

- Smartflower Solar GmbH

- Solar Vertical SAS

- SolarBotanic Trees Ltd.

- Solarix B.V.

- Spotlight Solar LLC

- Su-Kam Power Systems Limited

- SunRobotics Technologies Private Limited

- Tata Power Solar Systems Limited (Solar-Tree Division)

- Tree Power Co., Ltd.

Recent Industry Developments in Solar Tree Market

- March 2025: Tata Power Renewable Energy Limited signed an MoU with the Government of Andhra Pradesh to develop up to 7,000 MW of renewable projects, including hybrid solar-tree clusters.

- February 2025: Beam Global reported a 200% surge in energy-storage sales, driven by bespoke battery packs for solar-tree deployments.

- January 2025: Hanwha Qcells achieved 28.6% efficiency in a perovskite-silicon tandem cell, with pilot production slated for 2026.

- December 2024: RMC Switchgears allocated USD 12 million to build a 1 GWp solar-products plant in Jaipur, India.

Global Solar Tree Market Report Scope

A solar tree is an innovative renewable energy structure. Engineers have designed this structure to mimic a natural tree, featuring a central vertical "trunk" that supports multiple photovoltaic (PV) panels, arranged to resemble "leaves".

The global solar tree market report is segmented by product type, solar-panel technology, power output, installation mode, application, and geography. By product type, the market is segmented into on-grid, off-grid, and hybrid. By solar-panel technology, the market is segmented by monocrystalline, polycrystalline, thin-film and BIPV. By power output, the market is segmented into up to 1 kW, 1-5 kW, and above 5 kW. By installation mode, the market is segmented into free-standing, rooftop/terrace, modular kit and mobile. By application, the market is segmented into urban landscaping, commercial and industrial, educational campuses, residential, EV-charging hubs, and rural electrification and agri-uses. The report also covers the market size and forecasts for the global solar tree market in 18 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

Segmentation Overview

| On-grid Solar Trees |

| Off-grid Solar Trees |

| Hybrid Solar Trees |

| Monocrystalline Silicon |

| Polycrystalline Silicon |

| Thin-film and BIPV |

| Up to 1 kW |

| 1 to 5 kW |

| Above 5 kW |

| Free-standing Foundation |

| Rooftop / Terrace Mounted |

| Modular Kit and Mobile Units |

| Urban Landscaping and Parks |

| Commercial and Industrial Estates |

| Educational and Research Campuses |

| Residential Micro-PV |

| EV-Charging and Transport Hubs |

| Rural Electrification and Agri-uses |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Product Type | On-grid Solar Trees | |

| Off-grid Solar Trees | ||

| Hybrid Solar Trees | ||

| By Solar-Panel Technology | Monocrystalline Silicon | |

| Polycrystalline Silicon | ||

| Thin-film and BIPV | ||

| By Power Output | Up to 1 kW | |

| 1 to 5 kW | ||

| Above 5 kW | ||

| By Installation Mode | Free-standing Foundation | |

| Rooftop / Terrace Mounted | ||

| Modular Kit and Mobile Units | ||

| By Application | Urban Landscaping and Parks | |

| Commercial and Industrial Estates | ||

| Educational and Research Campuses | ||

| Residential Micro-PV | ||

| EV-Charging and Transport Hubs | ||

| Rural Electrification and Agri-uses | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the solar tree market in 2026?

The solar tree market size is estimated at USD 293.35 million in 2026, on track to reach USD 386.86 million by 2031.

What is the expected growth rate for solar trees?

From 2026-2031 the market is projected to expand at a 5.69% CAGR, driven by urban greening, EV charging, and policy mandates.

Which product type leads adoption?

Off-grid solar trees held 65.1% share in 2025 thanks to resilience needs in remote and disaster-prone areas.

Why are hybrid systems gaining traction?

Falling battery prices and resiliency codes push cities toward hybrids, which are forecast to grow at 7.4% CAGR through 2031.

Which region is the fastest-growing?

Asia-Pacific leads with a 6.1% CAGR to 2031, propelled by India's Smart Cities Mission and dense metro areas in China and Japan.

Who are notable players in the market?

Beam Global, Tata Power Solar, Paired Power, Smartflower Solar, and SolarBotanic Trees hold prominent positions, though no firm tops 15% share.

Page last updated on: