Flexible Solar Cell Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

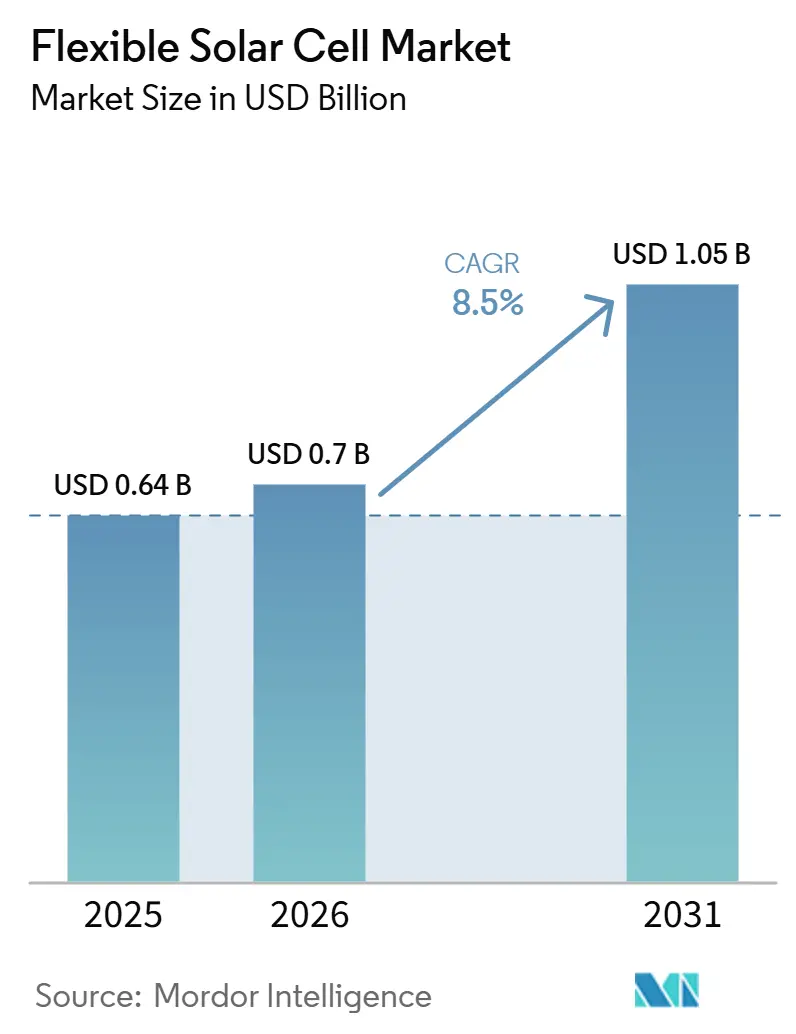

| Market Size (2026) | USD 0.7 Billion |

| Market Size (2031) | USD 1.05 Billion |

| Growth Rate (2026 - 2031) | 8.50% CAGR |

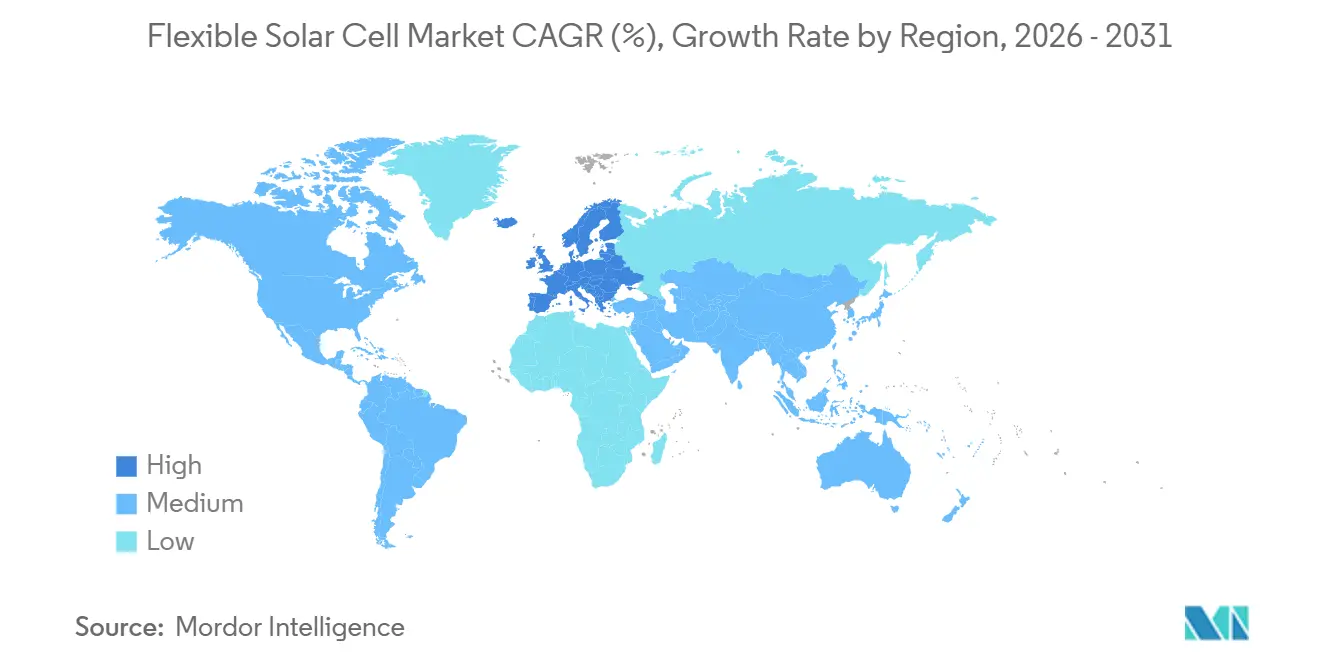

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

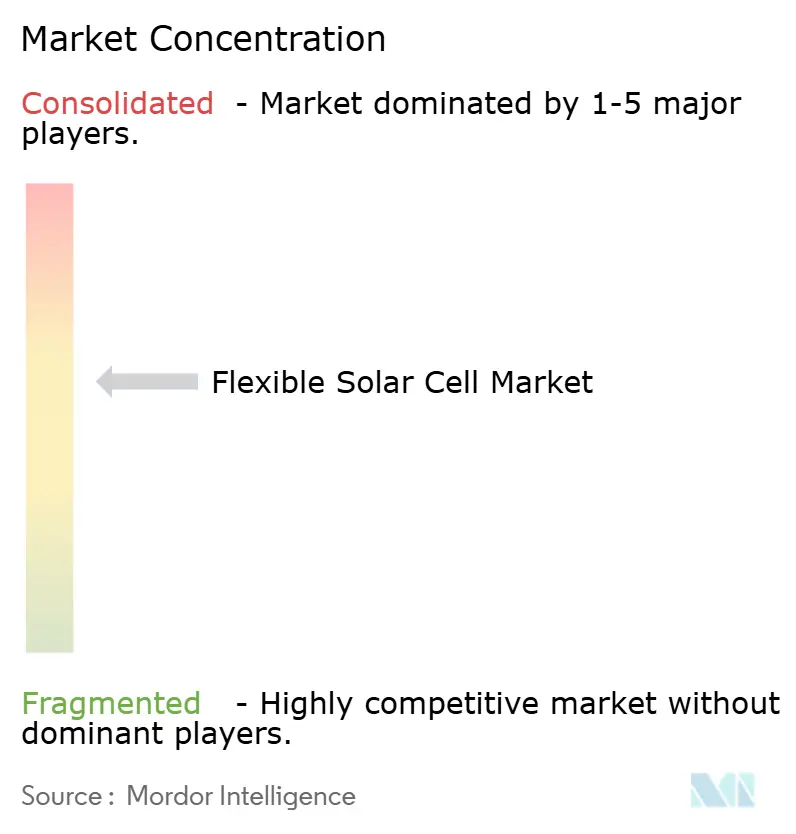

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flexible Solar Cell Market Analysis by Mordor Intelligence

The Flexible Solar Cell Market size is expected to grow from USD 0.64 billion in 2025 to USD 0.70 billion in 2026 and is forecast to reach USD 1.05 billion by 2031 at 8.5% CAGR over 2026-2031. Strong policy support in Europe, declining roll-to-roll production costs in Asia-Pacific, and demand for lightweight power solutions in wearables and aerospace are driving the flexible solar cell market toward double-digit annual shipments. Technology substitution is accelerating: perovskite-polymer tandems have already achieved over 33% cell efficiency in certified tests, while CIGS modules benefit from proven 20-year field data that supports project financing. Substrate innovation is also a contributing factor, as ultra-thin glass meets stringent moisture-barrier requirements at bending radii below 5 millimeters, enabling 30-year warranties for building-integrated photovoltaics (BIPV). Commodity price volatility, particularly indium's 3.4-fold price spike in 2024, is driving investment in recycling and indium-free absorber chemistries, while also increasing near-term margin risk for CIGS incumbents.

Key Report Takeaways

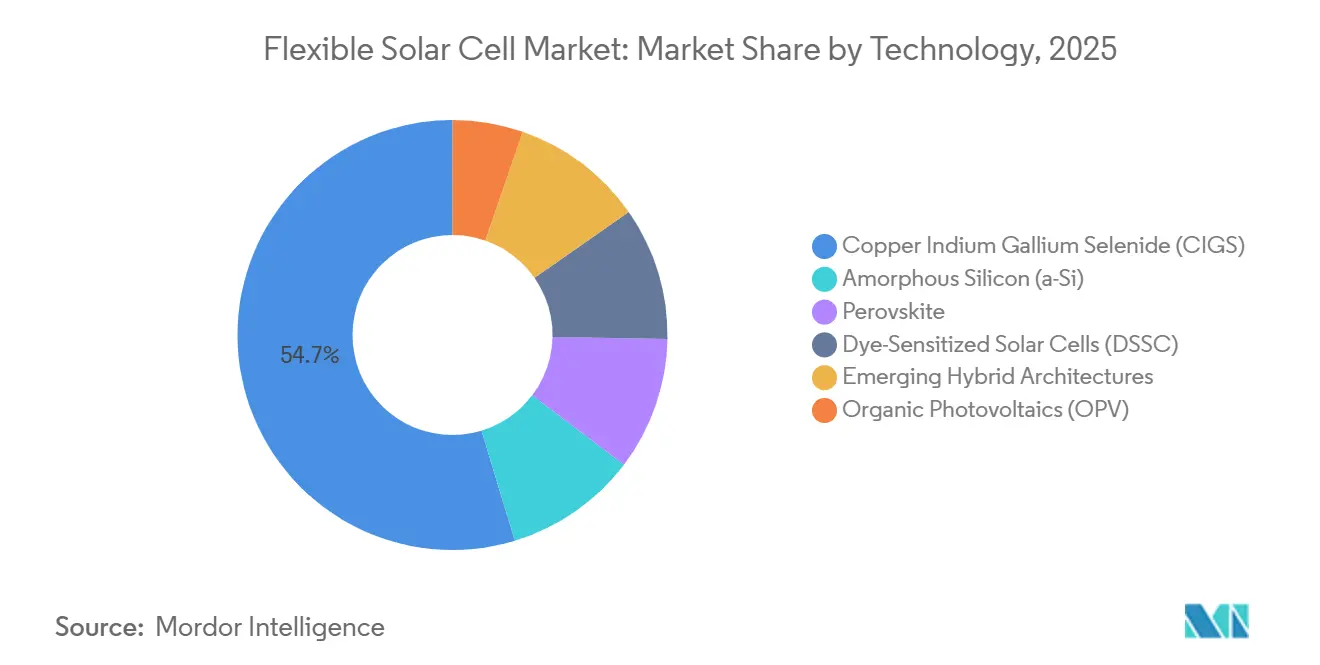

- By technology, CIGS held a 54.7% share of the flexible solar cell market in 2025, while perovskite architectures are forecast to grow at a CAGR of 28.1% through 2031.

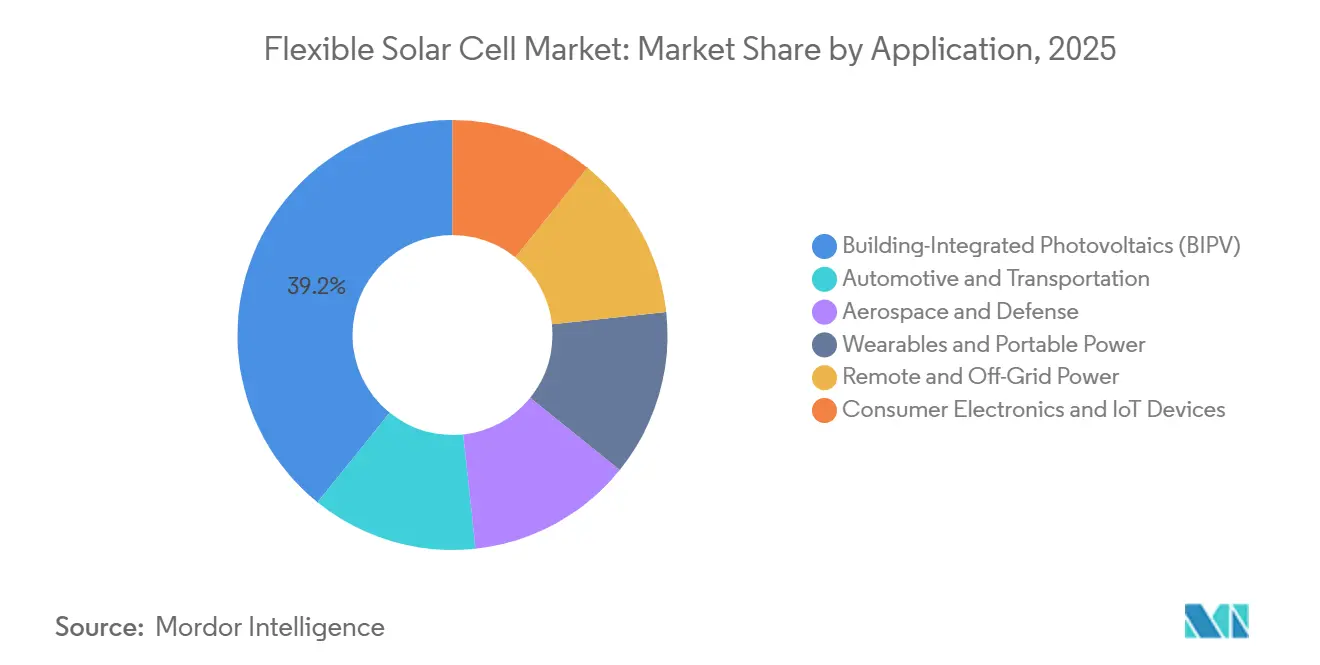

- By application, BIPV accounted for 39.2% of revenue in 2025, while consumer electronics and IoT devices are projected to grow at a CAGR of 15.9% through 2031.

- By substrate, plastics accounted for 64.0% of demand in 2025, while ultra-thin glass is projected to grow at a CAGR of 14.4%, driven by superior recyclability.

- By geography, Asia-Pacific accounted for 49.9% of revenue in 2025, while Europe is the fastest-growing region at a CAGR of 12.3% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Flexible Solar Cell Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Roll-to-roll cost reductions in CIGS & a-Si production | +2.1% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Net-zero building codes boosting BIPV demand | +2.8% | Europe & North America, early adoption in China tier-1 cities | Short term (≤ 2 years) |

| Wearables & IoT need ultra-light power sources | +1.6% | Global, led by North America and Asia-Pacific consumer hubs | Medium term (2-4 years) |

| Tandem perovskite-polymer breakthroughs for HAPS & drones | +1.3% | North America & Europe defense, Asia-Pacific commercial UAV | Long term (≥ 4 years) |

| Military procurement of foldable solar-battery hybrids | +1% | North America, Europe, Israel, South Korea & Japan | Medium to Long term (3–5 years) |

| Recyclable substrate mandates (PET-free architectures) | +0.8% | Europe (highest), followed by Japan and South Korea | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Roll-to-roll Cost Reductions in CIGS & a-Si Production

Capital outlays per gigawatt for new CIGS lines fell to USD 120 million in 2025, 33% below batch-processed rigid plants, trimming the levelized cost of electricity under high-irradiance conditions to USD 0.05 per kWh.[1]National Renewable Energy Laboratory, “Cost and Performance Analysis of Roll-to-Roll CIGS Lines,” nrel.gov A Poland-based 100 MW facility validated an 18-month tooling payback period after integrating in-line laser scribing, which removed 12% of legacy labor costs. EU-funded trials maintained 17.2% stabilized efficiency at 10 m/min web speed, confirming that throughput gains do not necessarily compromise performance. Slot-die coating with non-halogenated solvents reduced hazardous waste fees by 40%, which is significant as REACH restrictions continue to tighten. Amorphous silicon lines, operating below 200 °C, can now coat directly onto technical textiles, opening opportunities in wearable markets where rigid wafers are unsuitable.

Net-zero Building Codes Boosting BIPV Demand

The EU Energy Performance of Buildings Directive requires near-zero energy status for all new structures by 2030, pulling photovoltaic purchasing decisions into the construction supply chain.[2]European Commission, “Energy Performance of Buildings Directive 2026 Update,” ec.europa.eu Germany's Gebäudeenergiegesetz requires a 65% on-site renewable share for heating, and France's RE2020 regulation caps embodied carbon, prompting architects to adopt lightweight, low-carbon flexible laminates. Spain and Nordic countries have extended mandates to warehouses and glazed façades, respectively, expanding the available roof and wall surface area significantly. Flexible laminates weigh 2-3 kg/m² compared to 12-15 kg/m² for framed glass, making them suitable for high-rise retrofits where costly structural modifications would otherwise be required. As a result, sales cycles are shifting from energy managers to façade engineers, increasing demand visibility while extending specification timelines.

Wearables & IoT Need Ultra-light Power Sources

Ultraflexible organic photovoltaics (OPV) at 90 µm thickness deliver 16.1% efficiency and survive 10,000 bends at 1 mm radius, enabling perpetual Bluetooth sensors under 200 lux indoor light.[3]RIKEN Center for Emergent Matter Science, “Ultraflexible OPV for IoT Sensors,” riken.jp A 5 cm² cell on a smartwatch strap generates 15.88 mW, sufficient for heart-rate monitoring without nightly charging. Industrial IoT pilots in logistics have reduced battery-swap labor by 60%, and a soil-moisture probe with a 5 cm² flexible cell now offers a 10-year maintenance-free life. Commercial electronics OEMs value the sub-100 µm form factor, which fits under molded silicone cases without requiring housing redesigns. With 41 billion connected devices projected by 2027, the flexible solar cell market stands to gain a sustained, volume-driven channel beyond construction and mobility applications.

Tandem Perovskite-polymer Breakthroughs for HAPS & Drones

A March 2026 record of 33.4% efficiency on a flexible perovskite-organic tandem sets the bar for high-altitude pseudo-satellites (HAPS) where every gram matters.[4]LONGi Green Energy, “Record Efficiency Flexible Tandem Cell Press Release,” longi.com Germany's HAP-alpha, with a 27-meter wingspan, integrates these cells to maintain an altitude of 20 km for several months, providing telecommunications coverage across 400 km diameters. Airbus' Zephyr program has already validated 26-day stratospheric endurance using GaAs cells, and tandem perovskites are expected to enable further weight reductions. For commercial drones, mounting 0.5 m² flexible arrays on wings extends flight range from 30 km to 85 km, a key threshold for rural medical delivery. Defense procurement pays USD 5/W, six times the price of terrestrial modules, as mission endurance takes priority over capital expenditure, reinforcing a premium sub-segment within the flexible solar cell market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lower efficiency versus c-Si panels | -1.8% | Global, most acute on constrained North American & European rooftops | Short term (≤ 2 years) |

| Indium supply bottlenecks for CIGS scaling | -0.9% | Global, concentrated risk in Asia-Pacific CIGS fabs | Long term (≥ 4 years) |

| Accelerated UV / moisture degradation | -1.4% | Global, particularly tropical and high-humidity Asia-Pacific, Middle East & coastal regions | Short to Medium term (1–4 years) |

| Lack of global certification protocols for ultra-thin modules | -0.7% | Global, particularly Europe & North America where certification is critical for commercialization | Short to Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Lower Efficiency Versus c-Si Panels

Field data show flexible CIGS efficiency at 15-20% compared to 22-24% for mono-silicon. On a Munich rooftop, this 22% energy shortfall extends payback from 8 years to 10.2 years under EUR 0.30/kWh tariffs. Perovskite tandems offer potential parity, but flexible variants remain below 20% due to low-temperature processing constraints. Organic cells are commercialized at approximately 12% efficiency, which is acceptable for indoor applications but limits outdoor use unless transparency premiums offset the reduction in kilowatt-hours generated. Bifacial coatings recover 8-12% through roof-albedo gains, but add USD 0.18/W in specialized backsheet costs. The efficiency gap is therefore narrowing slowly, which is tempering near-term rooftop penetration in the flexible solar cell market.

Indium Supply Bottlenecks for CIGS Scaling

CIGS technology consumes 30 g of indium per kW, meaning the 920 t global annual output limits supply capacity to approximately 31 GW. China controls 57% of indium refining, and 2024 export quotas drove spot prices from USD 170/kg to USD 580/kg. The United States imports 100% of its indium supply and classifies it as a critical material. Recycling pilots have achieved 99.999% purity recovery, but these operations remain regionally limited. Substitution with kesterite eliminates the need for indium but reduces efficiency by 6-7 percentage points, a trade-off most financiers are unwilling to accept. Without large-scale closed-loop recovery, indium supply constraints are expected to limit CIGS to approximately 15-18% of the flexible solar cell market capacity by 2031.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Perovskite Tandems Redefine Efficiency Ceiling

CIGS held a 54.7% share of the flexible solar cell market in 2025, supported by established roll-to-roll production lines and IEC-61646 certification. Perovskites are projected to grow at a 28.1% CAGR through 2031, driven by tandem efficiencies exceeding 33% that surpass single-junction silicon. Organic photovoltaics remain the preferred option for building façades due to their transparency, with module-level efficiency of 10–13% that prioritizes aesthetics over power output. Amorphous silicon continues to be used in rugged chargers where deposition onto textiles at 200°C is required, despite first-year degradation now exceeding 20%.

Perovskite-CIGS tandem cells on 30 µm glass weigh 200 g/m², a specification that supports pricing of USD 5/W in aerospace applications. However, bankability remains a challenge, as investors continue to favor CIGS due to its 20-year field record, despite risks associated with indium costs. Organic photovoltaic manufacturers are addressing area-scaling limitations through silver-nanowire electrodes that reduce series resistance by 15%, moving toward 15% commercial efficiency. Dye-sensitized cells are being removed from commercial roadmaps, as they lack the durability and efficiency required to remain competitive in the flexible solar cell market.

By Substrate Material: Plastic Flexibility Meets Glass Durability

Plastics, including PET, PEN, and polyimide, accounted for 64.0% of demand in 2025, driven by sub-USD 2/m² pricing. Ultra-thin glass is projected to grow at a 14.4% CAGR, supported by its ability to reduce water-vapor ingress by 100-fold and its compatibility with existing float-glass recycling processes. Metal foils remain a niche segment at 8% share, primarily used in space applications, while polypropylene naphthalate serves outdoor BIPV applications due to its UV resilience and mid-range cost.

Polyimide's USD 8/m² cost faces increasing pressure as 30 µm glass prices decline to USD 6/m², reducing its cost advantage. Stainless-steel substrates remain in use for satellite fleets at USD 50/m², where radiation hardness and thermal conductivity justify the higher capital expenditure. Ultra-thin glass supports long-life perovskite modules, while PET enables cost-sensitive portable electronics to remain within USD 1/W retail price targets.

By Application: Consumer Electronics Surge Ahead

Building-integrated photovoltaics held 39.2% of the flexible solar cell market in 2025, while the consumer electronics and IoT segment is expected to outpace all other segments with a 15.9% CAGR through 2031.

Riken's wristband prototype demonstrates that 5 cm² cells can power wearables continuously, with the potential to remove 41 billion coin-cell batteries from supply chains by 2027. Tesla's 400 W Cybertruck kit extends daily driving range by 15 km in sunny states, though it still faces a five-year payback period. Stratospheric drones have demonstrated that high-altitude telecom operations can be conducted at one-tenth the cost of satellites, reinforcing aerospace as a prominent application that supports broader visibility for the flexible solar cell market.

Geography Analysis

Asia-Pacific accounted for 49.9% of 2025 revenue, driven by Chinese roll-to-roll CIGS lines and dominance in indium refining. Japan's Solar Frontier shipped 900 MW of CIGS in 2024, and South Korea's KRW 800 billion perovskite pilot is expected to begin production in 2027. India's 500 MW flexible line supports rural electrification, while ASEAN contract manufacturers are adding 400 MW of capacity, keeping regional module costs below USD 0.70/W.

Europe is the fastest-growing region at a 12.3% CAGR, supported by directives mandating near-zero-energy buildings by 2030. Germany installed 180 MW of flexible laminates in 2024, with KfW subsidies covering 30% of BIPV capital expenditure. France's lifecycle carbon regulations favor lightweight films, and Spain is adopting curved-roof warehouse installations that require no structural reinforcement. Nordic pilots are integrating transparent OPV into triple-glazed units to meet passive-house compliance standards.

In North America, U.S. Inflation Reduction Act tax credits support 250 MW of annual installations, concentrated in California and Texas. Canada is targeting off-grid indigenous communities, while Mexico remains a small market as utility-scale rigid installations continue to dominate. In the Middle East and Africa, notable projects include the UAE's 12 MW Masdar City façade and Saudi Arabia's 50 MW NEOM specification, though project execution remains delayed. In South America, the market is largely driven by off-grid kits deployed in Brazil's Amazon basin.

Competitive Landscape

The global flexible solar cell market is moderately fragmented. First Solar invested USD 1.1 billion in a 3.5 GW Louisiana CdTe plant, though flexible modules account for less than 5% of its shipments. Hanergy's restructuring allowed Risen and JA Solar to gain ground, with both companies entering the CIGS segment through joint ventures that utilize existing furnace assets.

European specialists focus on premium BIPV applications. Heliatek raised EUR 80 million in 2025 to scale 13%-efficient films with 30-year warranties, while Flisom is piloting aerospace-grade 14.6% CIGS on 25 µm substrates. Oxford PV holds 47 patents in perovskite-silicon tandems, and LONGi's 33.4% efficiency record has intensified competition in innovation. HyET Solaris' EUR 60 million Series B is funding a 50 MW perovskite line targeting USD 0.80/W module costs, which could undercut CIGS pricing before 2028.

Strategic alliances are deepening vertical integration across the market. Flexell Space is partnering with Kongsberg on satellite arrays, Atomic-6 supplies foldable mil-spec kits, and Armor's ASCA line targets indoor IoT energy harvesting at 12% efficiency. Standards activity under IEC 63163 is expected to raise certification barriers, likely increasing market concentration among firms with strong balance sheets and broad patent portfolios. Niche specialists, however, are expected to remain where application-specific requirements outweigh the benefits of scale.

Flexible Solar Cell Industry Leaders

Hanergy

First Solar Inc.

Heliatek GmbH

PowerFilm Solar Inc.

Flisom AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Active Surfaces, a startup harnessing solar-energy technologies from MIT research, has unveiled lightweight, flexible, and high-efficiency solar energy films. These innovative films are crafted for application on roofs, walls, and even curved surfaces.

- July 2025: Researchers at the Korea Institute of Materials Science (KIMS) have crafted a novel material and fabrication method for flexible perovskite solar cells, allowing production under ambient air conditions. This advancement tackles the material's pronounced sensitivity to moisture, a persistent hurdle in its broader commercial adoption.

- June 2025: Researchers at Singapore's Solar Energy Research Institute (SERIS) have developed an ultra-thin, flexible solar cell with a record power conversion efficiency of 26.4%, verified independently. This advancement highlights potential for integrated electronics.

- April 2025: Chinese scientists have advanced flexible solar technology by solving the challenge of bonding smooth perovskite layers to rough CIGS substrates. Their approach uses solvent manipulation and a seeded layer to improve adhesion, efficiency, and durability. The result is a flexible tandem solar cell with power output matching rigid models and minimal performance loss after extensive bending.

Global Flexible Solar Cell Market Report Scope

Flexible solar cells are lightweight and bendable photovoltaic modules crafted by depositing thin-film materials, like CIGS, amorphous silicon, or perovskite, onto flexible substrates, including plastics or metal foils. These cells excel in applications demanding portability and low weight, especially when installed on curved or unconventional surfaces. This makes them perfect for use in vehicles, tents, and small electronic devices, where traditional rigid panels fall short.

The flexible solar cell market is segmented by technology (organic photovoltaics, copper indium gallium selenide, amorphous silicon, perovskite, and more), substrate material (plastic, metal foils, and ultra-thin glass), application (building-integrated photovoltaics, consumer electronics and IoT devices, automotive and transportation, and more), and geography. By technology, the market is segmented into organic photovoltaics, copper indium gallium selenide, amorphous silicon, perovskite, and more. By substrate material, the market is segmented into plastic, metal foils, and ultra-thin glass. By application, the market is segmented into building-integrated photovoltaics, consumer electronics and IoT devices, automotive and transportation, and more. The report also covers the market size and forecasts for the flexible solar cell market in 19 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Organic Photovoltaics (OPV) |

| Copper Indium Gallium Selenide (CIGS) |

| Amorphous Silicon (a-Si) |

| Perovskite |

| Dye-Sensitized Solar Cells (DSSC) |

| Emerging Hybrid Architectures |

| Plastic (PET, PEN, PI) |

| Metal Foils (Stainless Steel, Titanium) |

| Ultra-Thin Glass |

| Building-Integrated Photovoltaics (BIPV) |

| Consumer Electronics and IoT Devices |

| Automotive and Transportation |

| Aerospace and Defense |

| Wearables and Portable Power |

| Remote and Off-Grid Power |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Technology | Organic Photovoltaics (OPV) | |

| Copper Indium Gallium Selenide (CIGS) | ||

| Amorphous Silicon (a-Si) | ||

| Perovskite | ||

| Dye-Sensitized Solar Cells (DSSC) | ||

| Emerging Hybrid Architectures | ||

| By Substrate Material | Plastic (PET, PEN, PI) | |

| Metal Foils (Stainless Steel, Titanium) | ||

| Ultra-Thin Glass | ||

| By Application | Building-Integrated Photovoltaics (BIPV) | |

| Consumer Electronics and IoT Devices | ||

| Automotive and Transportation | ||

| Aerospace and Defense | ||

| Wearables and Portable Power | ||

| Remote and Off-Grid Power | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the expected revenue for the flexible solar cell market by 2031?

The sector is projected to reach USD 1.05 billion by 2031, reflecting an 8.5% CAGR over 2026-2031.

Which technology will grow fastest through 2031?

Perovskite architectures are forecast to expand at a 28.1% CAGR, outpacing CIGS and organic counterparts.

Why are flexible modules appealing for consumer electronics?

Sub-100 µm OPV films deliver sufficient milliwatts for Bluetooth sensors, eliminating battery swaps and meeting durability under 10,000 bend cycles.

Which region will register the highest growth rate?

Europe leads with a 12.3% CAGR through 2031, propelled by stringent net-zero building codes.

How does indium supply affect CIGS expansion?

Indium's limited 920 t annual output and China's 57% refining share cap CIGS capacity near 31 GW unless recycling scales rapidly.

What is the main barrier to rooftop adoption in dense cities?

Flexible modules' 15-20% efficiency trails silicon's 22-24%, extending project payback and challenging returns where roof space is scarce.

Page last updated on: