Solar Sunlight Control System Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

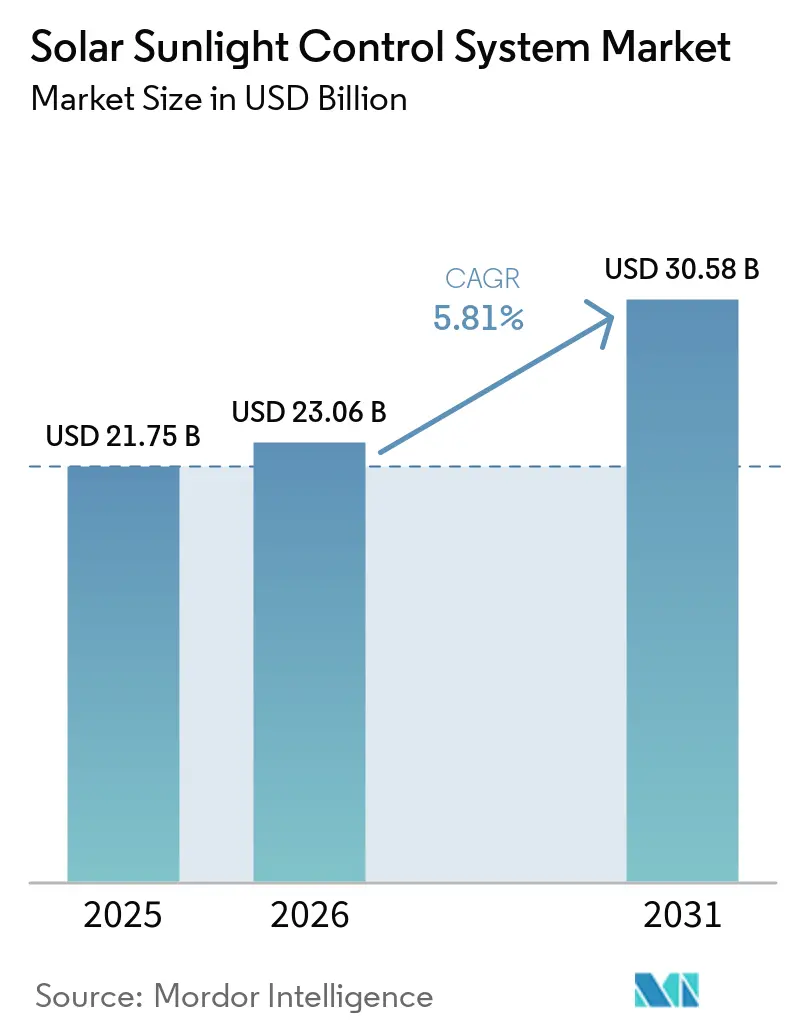

| Market Size (2026) | USD 23.06 Billion |

| Market Size (2031) | USD 30.58 Billion |

| Growth Rate (2026 - 2031) | 5.81% CAGR |

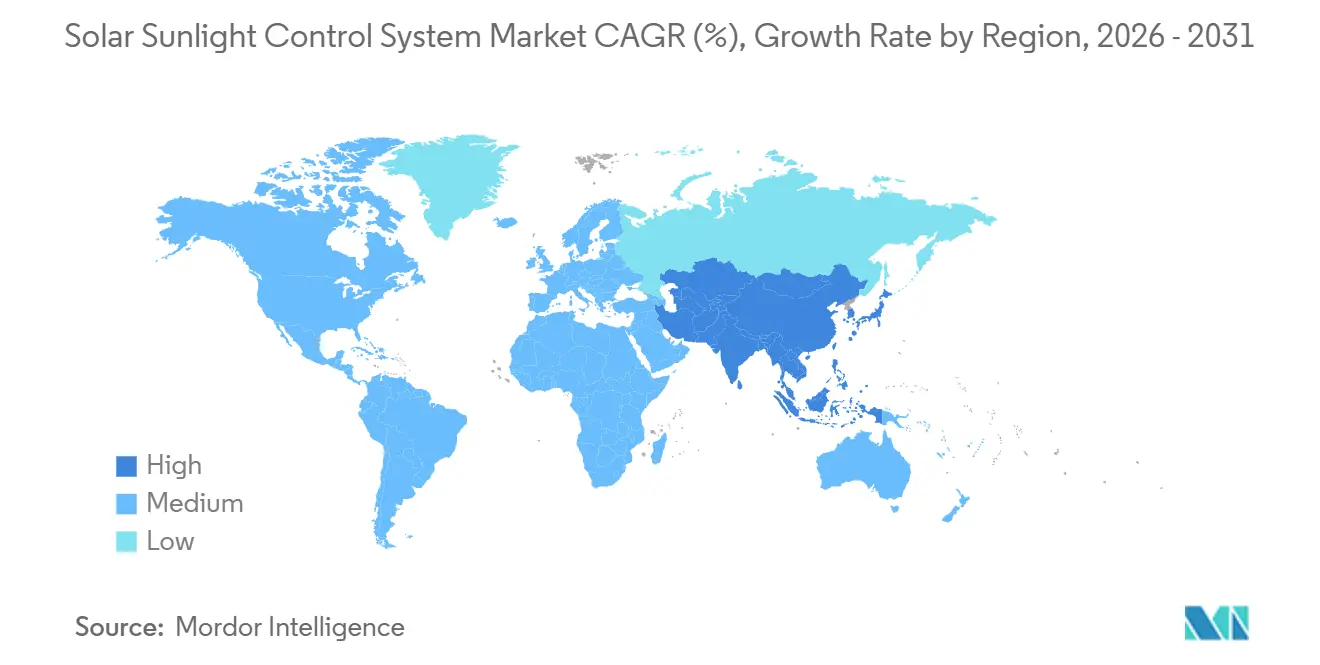

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

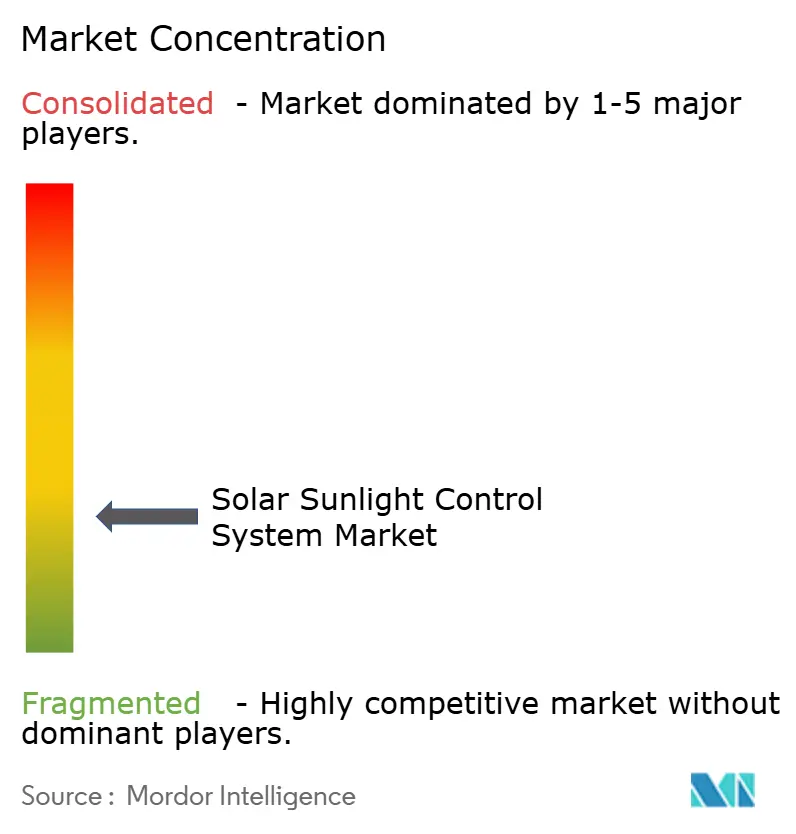

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Solar Sunlight Control System Market Analysis by Mordor Intelligence

The Solar Sunlight Control System Market size was valued at USD 21.75 billion in 2025 and is estimated to grow from USD 23.06 billion in 2026 to reach USD 30.58 billion by 2031, at a CAGR of 5.81% during the forecast period (2026-2031). Automated and smart control systems already account for 45.3% of 2025 installations, reflecting a rapid pivot toward AI-driven platforms that deliver 6- to 18-month paybacks.[1]BrainBox AI, “AI-Driven HVAC and Shading Optimization,” brainboxai.com Federal tax incentives, such as the U.S. Inflation Reduction Act’s 30%-50% investment tax credit for electrochromic windows and the residential 30% credit (capped at USD 600) for ENERGY STAR-certified motorized shades, compress payback periods and accelerate retrofit activity.[2]Internal Revenue Service, “Energy Efficient Home Improvement Credit,” IRS.gov Commercial landlords embrace dynamic glazing for wellness certifications and energy savings, while homeowners prioritize energy-efficient window coverings to offset utility costs. As differentiation shifts from hardware to predictive software, recurring SaaS revenue models now shape vendor strategy.

Key Report Takeaways

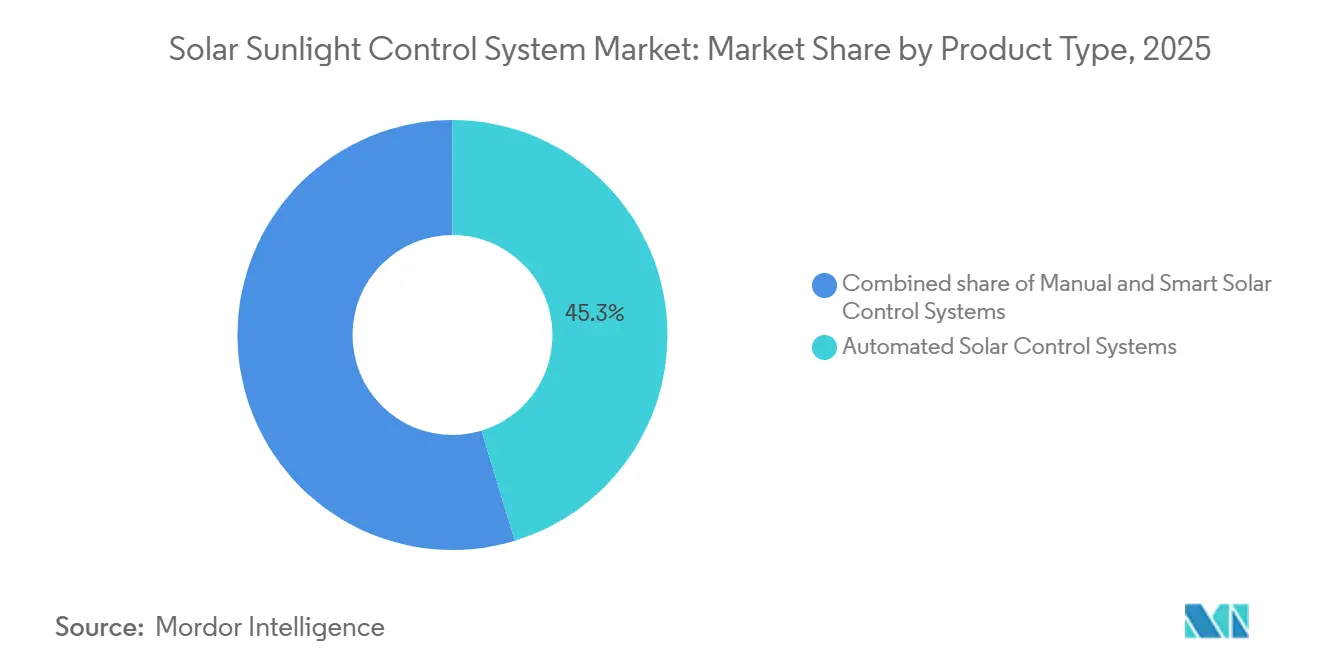

- By product type, automated shading led with 45.3% of the Solar sunlight control system market share in 2025; smart control systems are projected to expand at a 12.0% CAGR through 2031.

- By technology, photoelectric sensors led with 40% of the Solar sunlight control system market share in 2025; infrared sensors are projected to expand at a 11.1% CAGR through 2031.

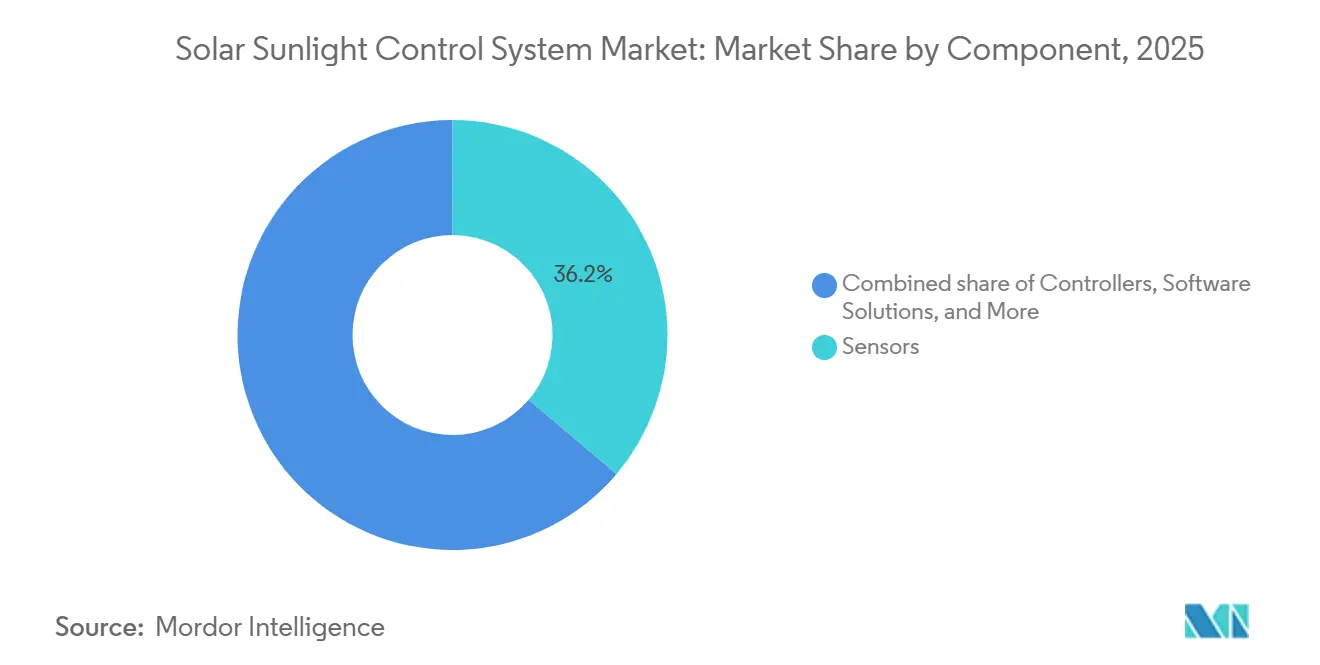

- By component, sensors accounted for 36.2% share of the Solar sunlight control system market size in 2025, but software solutions are expected to advance at a 13.4% CAGR to 2031.

- By installation type, new installations accounted for 64.6% share of the Solar sunlight control system market size in 2025, but retrofit installations are advancing at a 6.4% CAGR to 2031.

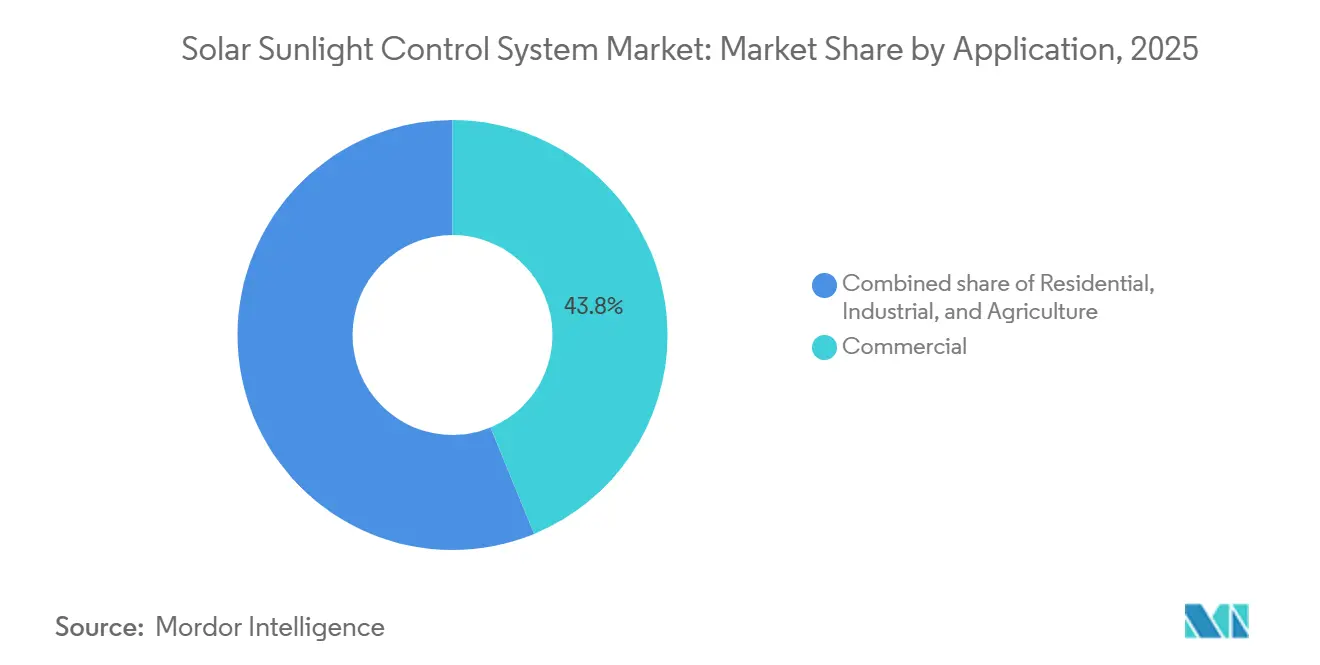

- By application, commercial real estate commanded 43.8% of revenue in 2025, while the residential segment is forecast to grow at a 7.2% CAGR to 2031.

- By geography, North America held 33.4% revenue share in 2025; Asia-Pacific is slated for the fastest regional growth at a 6.7% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Solar Sunlight Control System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter green-building energy codes elevating daylight & façade performance requirements | +1.20% | Global; North America & EU leadership, APAC accelerating | Long term (≥ 4 years) |

| Commercial real-estate shift toward dynamic glazing for wellness & energy savings | +0.90% | North America, EU, tier-1 APAC cities | Medium term (2-4 years) |

| Surge in residential retrofits seeking energy-efficient window coverings | +0.80% | North America, EU; emerging APAC | Medium term (2-4 years) |

| U.S. Inflation Reduction Act 30%-50% ITC for electrochromic smart windows | +0.70% | United States | Short term (≤ 2 years) |

| AI-driven predictive shading software delivering <3-year payback | +0.60% | Global smart-building hubs | Short term (≤ 2 years) |

| Health-centric certifications rewarding circadian-light management | +0.50% | North America & EU; APAC rising | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Green-Building Energy Codes Elevating Daylight & Façade Performance Requirements

Building regulations worldwide now embed daylight metrics and solar-heat-gain caps, effectively mandating dynamic shading or electrochromic glazing. ASHRAE 90.1-2022 raises visible-transmittance thresholds, while the EU’s Energy Performance of Buildings Directive recast doubles renovation targets and pushes automated shading into national codes.[3]Envigilance, “ASHRAE 90.1-2022 Addenda,” envigilance.com China’s GB/T 50378-2019 awards higher ratings to projects with intelligent sunlight control, locking the Solar sunlight control system market into core design considerations rather than optional upgrades.

Commercial Real-Estate Shift Toward Dynamic Glazing for Wellness & Energy Savings

Landlords report rent premiums and faster lease-ups when dynamic glazing replaces blinds. GREYSTAR’s Exo Apartments reached full occupancy 80% faster after installing View Smart Windows, linking glare-free daylight to tenant appeal.[4]View Inc., “Smart Glass for Smart Buildings,” view.com Kilroy Realty cut annual energy spend by USD 1 million across properties using View’s networked platform. Saint-Gobain’s 2025 launch of SageGlass RealTone with four tint zones satisfies occupant preference for view clarity, further boosting adoption.

Surge in Residential Retrofits Seeking Energy-Efficient Window Coverings

Motorized shades have moved from luxury to mainstream. IRS Section 25C credits shave hundreds of dollars off installation costs, and Lutron’s 2026 luxury-residential survey shows 56% of designers now specify automated shades by default. Hunter Douglas’ May 2025 PowerView upgrade adds Matter-over-Thread support, erasing smart-home interoperability barriers.

U.S. Inflation Reduction Act’s 30%-50% ITC for Electrochromic Smart Windows

The IRA extends Section 48 credits to electrochromic glazing, improving project IRRs and driving specification in states with stringent energy codes such as California and New York. Retrofit inquiries for switchable-film provider Smart Tint spiked as owners realized tax benefits apply beyond new builds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of smart glass & motorized shading | -0.8% | Global, most acute in price-sensitive APAC and South America markets | Medium term (2-4 years) |

| Skilled-labour shortage for complex retrofit installations | -0.5% | North America & EU; emerging in APAC urban centers | Short term (≤ 2 years) |

| Limited recyclability of multi-layer smart films creating EoL liabilities | -0.3% | EU (stringent circular-economy mandates); North America (voluntary ESG commitments); emerging in APAC | Long term (≥ 4 years) |

| Cyber-security threats to IoT-connected shading networks | -0.2% | Global, concentrated in North America & EU where IoT penetration is highest; rising concern in APAC smart cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Smart Glass & Motorized Shading

Electrochromic glazing commands a 15%-25% premium over static low-E glass, adding USD 50-USD 150 per ft² to façade budgets and deterring mid-market projects. Motorized shades cost USD 300-USD 800 per window versus USD 50-USD 150 for manual blinds, prompting developers in Southeast Asia and South America to value-engineer them out. Although total-cost-of-ownership models yield 5- to 10-year paybacks, first-cost sensitivity remains a hurdle.

Skilled-Labour Shortage for Complex Retrofit Installations

Low-voltage technicians capable of integrating shading with BMS platforms command wage premiums of 20%-30%. CEDIA offers residential certifications, but no equivalent exists for commercial façade retrofits, stretching project timelines. Somfy’s March 2026 Glydea ULTRA 50 WireFree motor simplifies installation yet still requires wireless-network fluency, underscoring the talent gap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type : Smart Control Systems Widen the Performance Gap

Automated shading captured 45.3% of 2025 revenue, illustrating the early mainstreaming of motorization, yet smart control systems are forecast to expand at a 12.0% CAGR to 2031, more than twice the overall Solar sunlight control system market pace. Buyers now judge value on predictive intelligence rather than motion alone, and the smart tier embeds cloud analytics, AI algorithms, and open APIs that unlock SaaS billing. Consequently, legacy manual products remain relevant only in price-sensitive retrofits and regions with unreliable power.

Smart platforms also reshape gross-margin profiles because annual software fees rise faster than hardware costs fall. Lutron’s Athena cloud service, for example, charges per-square-foot subscriptions that exceed the amortized cost of its motors, underscoring how analytics rather than mechanics anchor future profits. As project specifications increasingly require BACnet, Matter, or Bluetooth mesh compatibility, smart control vendors win on interoperability and cybersecurity assurances.

By Technology : Infrared Sensors Challenge Photoelectric Dominance

Photoelectric sensors held 40.0% of 2025 revenue because of familiarity and low BOM costs, but infrared sensing will climb at an 11.1% CAGR through 2031 as building owners demand thermal-load and occupancy data in one device. A 2025 IEEE field trial showed LoRa-based infrared nodes sustaining 99.2% network uptime while extending battery life by 80%, directly addressing maintenance concerns that once limited wireless adoption.

Infrared arrays also feed real-time heat-map data to AI engines, enabling shading adjustments seconds before occupants perceive discomfort. Thermal-sensor bundles therefore reduce HVAC spikes, which is why life-science laboratories and data centers specify them despite the 10% unit premium. As wireless protocols such as Matter and Zigbee 3.0 embed security keys at the silicon level, buyers accept wireless reliability, further tipping the share away from wired photoelectric loops.

By Component : Software Solutions Outpace Hardware Growth

Sensors retained 36.2% of 2025 component revenue, yet software solutions will accelerate at a 13.4% CAGR to 2031, the fastest of any component line. Platform vendors monetize predictive maintenance dashboards, multi-facility orchestration, and RESTful integration endpoints that embed shading logic into broader smart-building stacks. Because Chinese motor makers now offer DC drives at 40%-60% discounts, hardware gross margins compress, forcing incumbents to chase analytics-led differentiation.

BrainBox AI’s reinforcement-learning engine, sold at USD 0.10-0.25 per ft² annually, already delivers recurring revenue that surpasses hardware attachment in mature accounts. Edge chips baked into next-generation sensors further shift capability upstream, as local inference keeps blinds functional during internet outages an emerging spec requirement for mission-critical hospitals.

By Installation Type : Retrofits Gain Momentum on Wire-Free Solutions

New-build projects accounted for 64.6% of 2025 activity, sustained by commercial towers that embed solar control during design. Even so, retrofit deployments will post a 6.4% CAGR to 2031, outstripping new construction as energy audits and disclosure rules pressure owners of aging stock. Wire-free motors such as Somfy’s Glydea ULTRA 50 trim per-window installation time to under an hour and cut labor costs 60%-70%, closing capital gaps that once stalled upgrades.

Glas Trösch’s 2026 pilot proved that 2.6 tonnes of laminated glazing can be recycled with 1.33 tonnes of CO₂ savings, easing owners’ end-of-life liability concerns. Financing models that bundle SaaS shading with energy-performance contracts shift expense lines from CapEx to OpEx, further propelling retrofit penetration.

By Application : Residential Segment Accelerates on Incentives and Wellness

Commercial facilities still generated 43.8% of 2025 revenue, benefiting from class-A offices and life-science campuses that prize wellness and energy savings. Yet residential installations will grow at a 7.2% CAGR because homeowners now combine IRS Section 25C tax credits with utility rebates to compress payback windows. Lutron’s 2026 designer survey found that 56% of interior professionals specify automated shades as standard, highlighting the segment’s shift from luxury to baseline expectation.

Hunter Douglas’ Matter-enabled PowerView platform resolves interoperability friction, letting devices slot seamlessly into Apple Home, Google Home, and Alexa environments. Meanwhile, agrivoltaic pilots that blend solar panels with dynamic shading in greenhouses lifted lettuce yields 12%-18%, hinting at upside in controlled-environment farming. The Solar sunlight control system industry, therefore, spans everything from penthouse apartments to tomato greenhouses, reinforcing the segment’s rising strategic weight.

Geography Analysis

North America retained 33.4% of 2025 revenue as the IRA’s 30%-50% investment tax credit pushed electrochromic glazing into mainstream specifications. State-level stretch codes in California and New York tighten solar-heat-gain caps annually, ensuring the Solar sunlight control system market continues to grow on mandated performance thresholds. Tax certainty through 2032 encourages longer development pipelines, and abundant smart-building expertise accelerates retrofit conversions.

Asia-Pacific will record a 6.7% CAGR to 2031, the fastest regional trajectory, because China, India, and ASEAN economies embed daylight metrics into occupancy permits. China’s GB/T 50378-2019 standard awards premium ratings to projects with intelligent shading, and tier-1 developers chase that label to secure higher lease rates. India’s 2024 update of the Energy Conservation Building Code forces new offices in hot-dry zones to achieve solar-heat-gain coefficients below 0.25, effectively mandating dynamic glazing. As urbanization pushes skyscraper counts higher, automated façade solutions become indispensable.

Europe benefits from the Renovation Wave initiative, which aims to double deep retrofit rates by 2030. Projects such as Saint-Gobain’s Smart Campus Bordeaux showcase electrochromic scalability, while high labor costs make automation more cost-effective than manual blinds. Latin America and the Middle East trail global averages yet still log mid-single-digit growth; cooling-energy premiums in Saudi Arabia and the UAE motivate shade automation, whereas economic volatility tempers large-scale adoption in Brazil and Argentina. Collectively, regional policy convergence places the Solar sunlight control system market on a worldwide upswing that aligns climate targets with financial incentives.

Competitive Landscape

Competitive intensity is moderately low, with the top five suppliers, Lutron, Somfy, Hunter Douglas, View Inc., and Saint-Gobain SageGlass, collectively holding a significant share of 2025 revenue. Hardware specialists guard dealer networks and proprietary protocols, yet margin pressure from low-cost Asian motors forces moves into software. Springs Window Fashions’ 2025 acquisition of PowerShades adds SaaS IP and a CEDIA installer base, mirroring industry appetite for analytics revenue.

Open-protocol disruptors chip away at incumbents’ lock-in. Warema’s Xeenos Go actuators ship with Matter certification, letting devices pair natively with Apple Home and SmartThings, a challenge to vendor-specific hubs. Lutron countered by unveiling fixture-level wireless intelligence that slashes rack space and permits hassle-free re-zoning, strengths valued by fit-out contractors on compressed schedules. Cybersecurity lags; none of the majors yet carry IEC 62443 certification, exposing a gap ripe for specialists who can proof-point encryption and threat-detection at the edge.

Materials innovation also shifts the its share. A 2025 Nature Communications study introduced dual-cathode electrochromic cells that double tint speed while storing energy, a patent now licensed by two Chinese glass giants. If recyclable copper-zinc films demonstrated in 2026 reach commercial yield, circular-economy credentials could become a new battleground. Against that backdrop, the Solar sunlight control system market will likely move toward ecosystems in which hardware, analytics, and recycling logistics merge, rewarding vendors that control the full life cycle.

Solar Sunlight Control System Industry Leaders

-

Hunter Douglas

-

Somfy Systems

-

Lutron Electronics

-

View Inc.

-

Warema Renkhoff SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Somfy launched the Glydea ULTRA 50 WireFree Zigbee drapery motor, cutting retrofit installation time by 40%

- March 2026: Glas Trösch completed a pilot recycling project reclaiming 2.6 tonnes of glazing.

- February 2026: Lutron introduced its Intelligent Lighting portfolio with fixture-level wireless intelligence.

- March 2025: Saint-Gobain finished the Paris Research extension featuring 105 m² of SageGlass.

Global Solar Sunlight Control System Market Report Scope

In renewable energy, solar sunlight control systems refer to a mechanical and electronic system designed to align solar panels with the sun to optimize energy capture.

The Solar Sunlight Control System Market is segmented into product type, technology, component, installation type, application, and geography. By product type, the market is segmented into manual, automated, and smart control systems. By technology, the market is segmented into photoelectric, thermal, infrared sensors, and wireless technology. By component, the market is segmented into actuators, controllers, sensors, software solutions, and other components. By installation type, the market is segmented into new installations and retrofit installations. By application, the market is segmented into residential, commercial, industrial, and agriculture applications. The report also covers the market size and forecasts for the solar sunlight control system market across major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Manual Solar Control Systems |

| Automated Solar Control Systems |

| Smart Control Systems |

| Photoelectric Sensors |

| Thermal Sensors |

| Infrared Sensors |

| Wireless Technology |

| Actuators |

| Controllers |

| Sensors |

| Software Solutions |

| Others |

| New Installations |

| Retrofit Installations |

| Residential |

| Commercial |

| Industrial |

| Agriculture |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Product Type | Manual Solar Control Systems | |

| Automated Solar Control Systems | ||

| Smart Control Systems | ||

| By Technology | Photoelectric Sensors | |

| Thermal Sensors | ||

| Infrared Sensors | ||

| Wireless Technology | ||

| By Component | Actuators | |

| Controllers | ||

| Sensors | ||

| Software Solutions | ||

| Others | ||

| By Installation Type | New Installations | |

| Retrofit Installations | ||

| By Application | Residential | |

| Commercial | ||

| Industrial | ||

| Agriculture | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the Solar sunlight control system market be by 2031?

It is projected to reach USD 30.58 billion by 2031, reflecting a 5.81% CAGR from 2026.

Which segment is forecast to grow fastest through 2031?

Smart control systems are expected to register a 12.0% CAGR, outpacing every other product type.

Why is Asia-Pacific the fastest-growing region?

Mandatory green-building codes in China, India, and ASEAN countries drive a 6.7% regional CAGR as developers must meet daylight and façade-performance targets.

How do U.S. tax credits influence adoption?

The Inflation Reduction Act grants a 30%-50% investment tax credit for electrochromic windows, compressing payback periods and accelerating commercial retrofits.

What limits wider deployment of smart glass today?

First-cost premiums of 15%-25% over static glazing and shortages of skilled low-voltage installers extend project timelines and deter budget-sensitive developers.

Page last updated on: