Organic Solar Cell Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

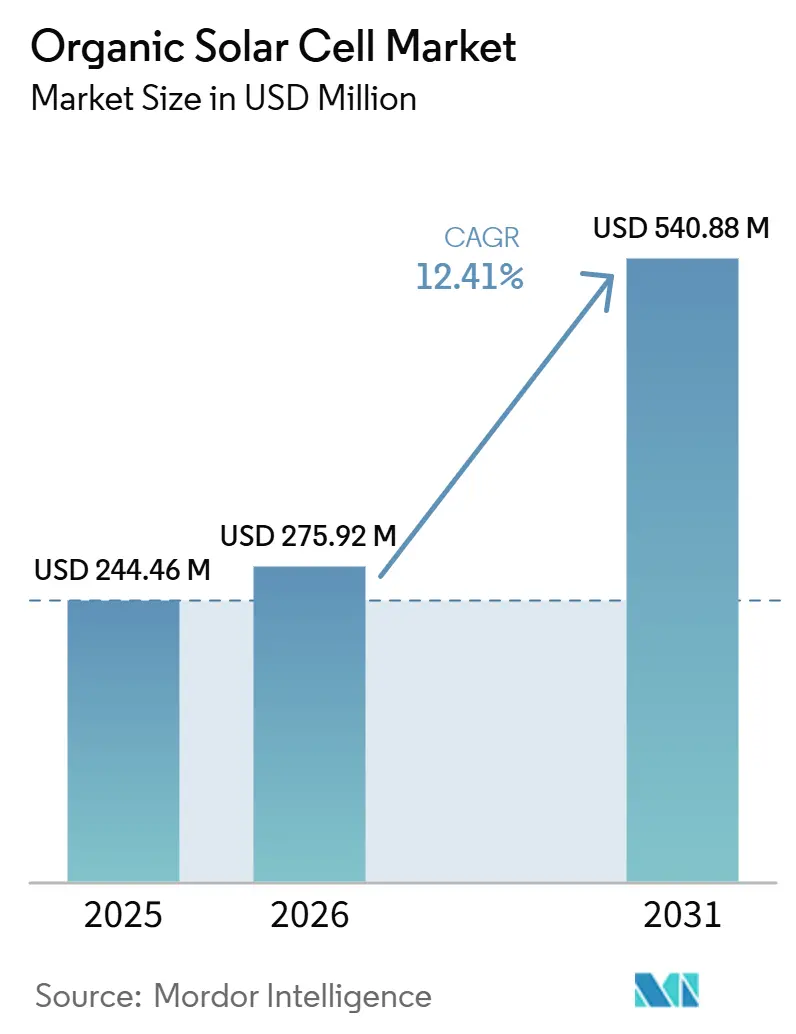

| Market Size (2026) | USD 275.92 Million |

| Market Size (2031) | USD 540.88 Million |

| Growth Rate (2026 - 2031) | 14.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Organic Solar Cell Market Analysis by Mordor Intelligence

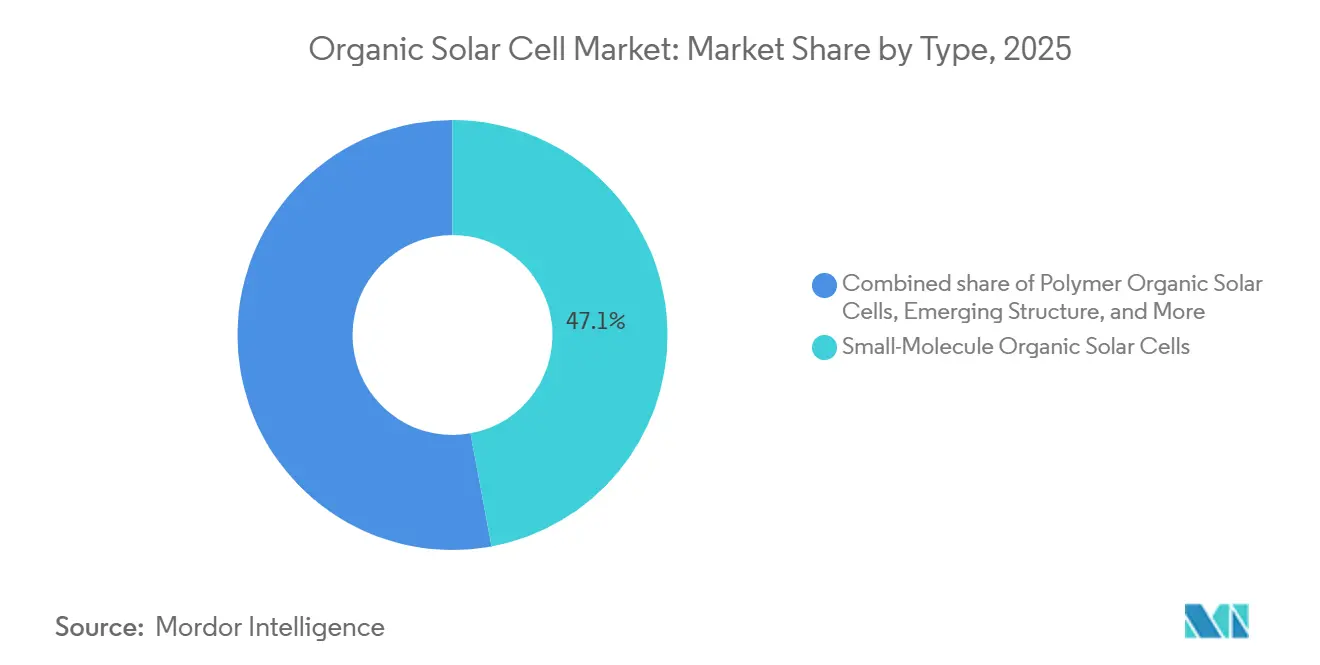

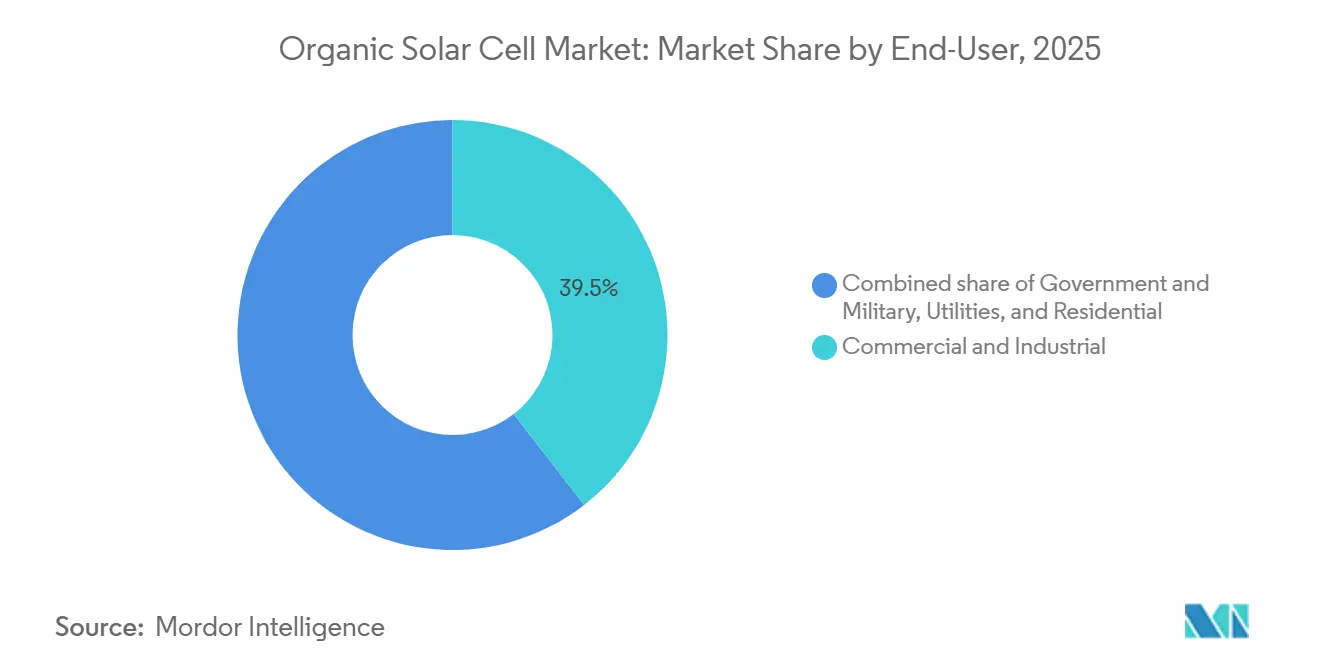

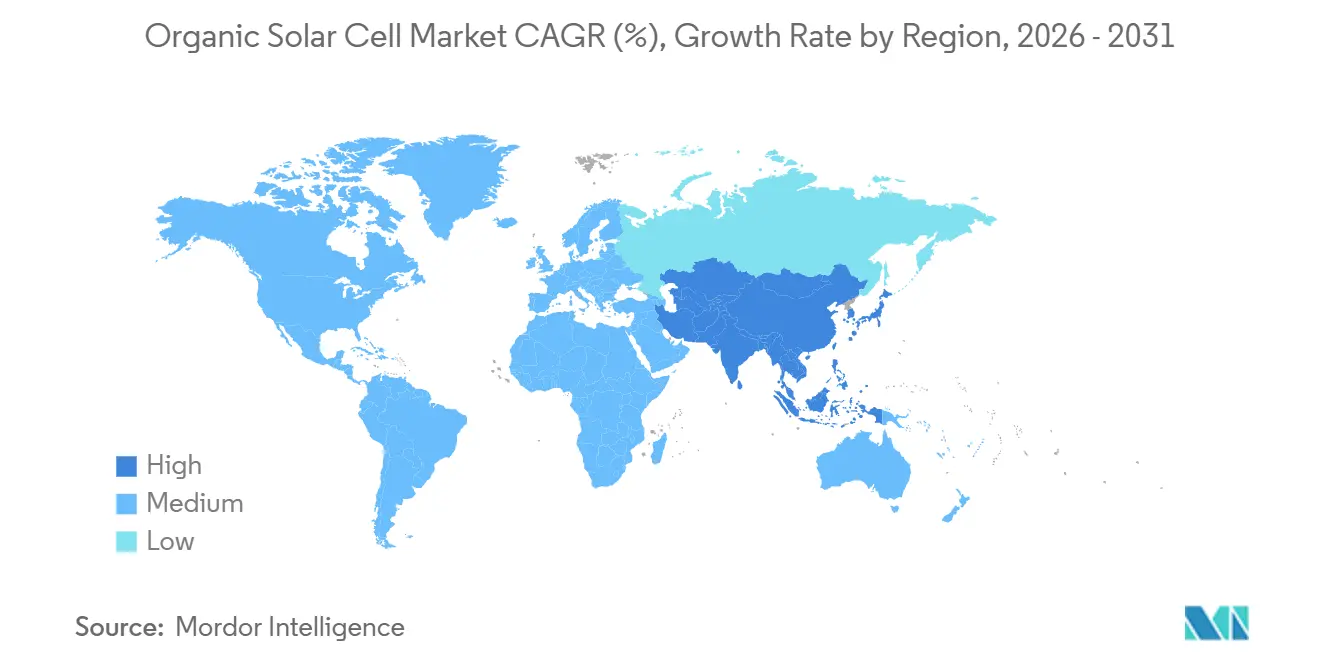

The Organic Solar Cell Market size is expected to increase from USD 244.46 million in 2025 to USD 275.92 million in 2026 and reach USD 540.88 million by 2031, growing at a CAGR of 14.41% over 2026-2031. Certified power-conversion efficiencies surpassed the 20% threshold in 2025, driven by advancements in non-fullerene acceptors. These developments reduced the performance gap with existing thin-film technologies and enabled applications in weight-sensitive, semi-transparent, and curved-surface designs. Europe accounted for 38.6% of revenue in 2025, primarily due to early adoption of building-integrated photovoltaics (BIPV) retrofits aligned with stringent carbon regulations. Meanwhile, the Asia-Pacific region experienced the fastest growth, with a compound annual growth rate (CAGR) of 13.8%, as Chinese and Indian companies expanded roll-to-roll production lines under local-content requirements. Small-molecule architectures maintained a 47.1% market share, supported by the maturity of vacuum-deposited processes. However, polymer devices are scaling rapidly, with a CAGR of 14.4%, as slot-die printing reduces capital expenditure. Among applications, BIPV accounted for 37.8% of demand in 2025, while indoor energy harvesting is growing at a CAGR of 16.1%, driven by superior performance under low-lux conditions. Commercial and industrial users represented 39.5% of installed capacity. Competitive intensity remains moderate, as the top five suppliers control approximately 35% of capacity, leaving opportunities for niche players specializing in transparent glazing, ultra-flexible wearables, and indoor Internet-of-Things (IoT) power solutions.

Key Report Takeaways

- By type, small-molecule devices led with 47.1% of the organic solar cell market share in 2025. By type, polymer organic solar cells are forecast to grow at a 14.4% CAGR through 2031.

- By application, building-integrated photovoltaics accounted for 37.8% of the organic solar cell market size in 2025, and indoor energy harvesting is expected to grow at a 16.1% CAGR to 2031.

- By end-user, commercial and industrial facilities commanded 39.5% of 2025 deployments, while government and military users are expected to advance at a 15.3% CAGR.

- By geography, Europe dominated with 38.6% 2025 revenue, whereas Asia-Pacific is projected to grow at a 13.8% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Organic Solar Cell Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid efficiency gains via non-fullerene acceptors | +3.20% | Global, with R&D concentration in China, Germany, Japan | Medium term (2-4 years) |

| Demand for ultra-light BIPV retrofits | +2.80% | Europe & North America, early adoption in Gulf Cooperation Council | Short term (≤ 2 years) |

| EU carbon-footprint-linked subsidies | +2.10% | European Union, potential spillover to UK and EFTA | Short term (≤ 2 years) |

| Corporate net-zero demand for transparent PV | +1.90% | Global, led by Fortune 500 headquarters in North America and Europe | Medium term (2-4 years) |

| Roll-to-roll printing cost parity by 2028 | +1.60% | Global manufacturing hubs in Germany, China, South Korea | Long term (≥ 4 years) |

| Defense need for foldable power | +1.00% | North America, Europe, Asia-Pacific (South Korea, Japan, Australia) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Efficiency Gains via Non-Fullerene Acceptors

Certified single-junction efficiencies reached 20.82% in 2025, significantly reducing the gap with cadmium-telluride thin film technologies and establishing organic cells as viable for mainstream commercial applications. The Y6-family acceptors enhanced absorption into the near-infrared spectrum, reduced voltage losses to below 0.5 V, and improved thermal-cycle stability. Over 200 patent filings were recorded between 2024 and early 2026, highlighting China, Germany, and Japan as key centers of innovation. However, the higher synthesis complexity of non-fullerene acceptors (NFAs) continues to drive up raw material costs, making long-term competitiveness dependent on scaling roll-to-roll production beyond pilot-scale operations. Flagship initiatives, such as Heliatek’s Flex16 line, aim to achieve module efficiencies exceeding 16% for building-integrated applications.

Demand for Ultra-Light BIPV Retrofits

Municipal near-zero-energy regulations and corporate LEED targets have driven an increase in BIPV retrofits, as organic modules weigh approximately 2 kg/m², which is only one-fifth the weight of framed silicon panels. In July 2025, NEXT Energy Technologies installed a six-panel 40 × 60-inch façade, achieving 3.5% efficiency and 32% visible-light transmittance. This installation offset 20–25% of building plug loads without significantly reducing interior light levels. The EU Solar Standard, effective from 2026, mandates solar-ready roofs for large non-residential buildings. Additionally, France’s VAT reduction to 5.5% for low-carbon modules in October 2025 created a 14.5-percentage-point price advantage for organic PV. Lightweight organic sheets also address structural-load limitations on heritage façades, enabling retrofit opportunities that silicon-based solutions often cannot meet.

EU Carbon-Footprint-Linked Subsidies

The European Commission's EUR 21 billion solar allocation prioritizes technologies with embedded carbon footprints below 400 kg CO₂e per kW, a threshold easily achieved by organic films, which record less than 10 g CO₂e per kWh over their lifetime generation. Funding from the Innovation Fund and Horizon Europe is directed toward pilot capacity in Italy and Germany, accelerating the transition from pilot lines to gigawatt-scale factories. While the reduction in feed-in tariffs reflects the improving economics of renewables, carbon-weighted incentives remain in place, supporting short-term demand. Compliance audits promote vertically integrated production within the region, encouraging suppliers to localize processes such as solvent recovery, substrate sourcing, and recycling. Companies that demonstrate comprehensive environmental benefits throughout the product lifecycle are likely to gain a competitive edge as procurement guidelines become increasingly stringent through 2030.

Corporate Net-Zero Demand for Transparent PV

Global enterprises aiming for net-zero targets by 2040 are increasingly adopting onsite energy generation solutions that do not alter existing corporate architecture. Transparent organic solar modules integrated into curtain walls can offset up to 25% of the annual electricity consumption of high-rise office buildings while maintaining daylight requirements. Installations at Fortune 500 company headquarters serve as case studies, reducing the perceived risks associated with adopting this technology for mainstream real estate developers. Since transparent panels replace existing facade elements rather than adding new ones, project payback is driven by savings on materials and revenue from power generation. As the organic solar cell market transitions to applications within building envelopes, sales processes are shifting from utility PPA negotiations to construction-specification bidding, thereby expanding the potential customer base.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sub-10-year module lifetime | -2.40% | Global, acute in high-humidity tropics and desert climates | Short term (≤ 2 years) |

| Non-fullerene acceptor feedstock bottlenecks | -1.80% | Global supply chain, production concentrated in China | Medium term (2-4 years) |

| Lack of bankability standards | -1.50% | Global, most severe in project-finance markets (North America, Europe) | Medium term (2-4 years) |

| Perovskite-silicon tandem competition | -1.20% | Utility-scale projects in China, Middle East, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sub-10-Year Module Lifetime

Outdoor tests in 2025 showed 91% efficiency retention after seven months, but investors still require 25-year performance projections.(1)“Organic Photovoltaics Reach 20% Efficiency Milestone,” Nature, nature.com The damp-heat IEC 61215 protocols demonstrated a 94% retention rate after 1,032 hours, equivalent to approximately three to five years in field conditions. However, issues such as moisture ingress and photodegradation continue to limit warranty durations. According to VDE's 2025 bankability review, lenders require at least two years of field data, a benchmark achieved by only a few suppliers, with Heliatek being a notable example. The lack of consensus on aging multipliers leads insurers to adopt conservative degradation rates, increasing the levelized cost of energy compared to silicon-based systems. Advances in encapsulation technologies, such as atomic-layer-deposited barriers, are targeting 15-year lifespans to align with commercial lease durations.

Perovskite-Silicon Tandem Competition

Laboratory tandem efficiencies reached 34.9% in 2024, and early commercial shipments started the same year. (2)Oxford PV, “First Solar Licensing Agreement,” oxfordpv.com Utility-scale buyers prioritizing cost per watt may consider tandem modules if they offer comparable weight characteristics. Organic cells maintain an advantage in flexibility and indoor performance; however, price competition could reduce margins in BIPV if tandem module prices drop below USD 0.20 per watt.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Small-Molecule Strength Faces Polymer Upsurge

Small-molecule devices accounted for 47.1% of the organic solar cell market share in 2025, driven by the high-layer uniformity achieved through vacuum evaporation and the utilization of OLED toolsets. Hybrid structures, which combine polymer donors with small-molecule acceptors, address niche customer requirements by balancing absorption bandwidth and thermal resilience. Polymer variants are projected to grow at a compound annual growth rate (CAGR) of 14.4%, supported by slot-die and gravure printing technologies that offer 40% lower capital expenditure and faster scale-up potential.

Process reproducibility continues to favor small-molecule formats in automotive and defense applications. However, advancements in polymer chains have improved batch consistency, reducing previous reliability concerns. The market size for polymer-based organic solar cell modules is expected to grow significantly as encapsulation improvements address thermal-cycle instability. Certification pathways, such as Heliatek’s IEC 61215 precedent, are being followed, with several polymer product lines anticipated to receive similar endorsements by 2027. Manufacturers focusing on polymer bulk supply are also pursuing backward integration into monomer synthesis to achieve cost efficiencies.

By Application: BIPV Dominates, Indoor Harvesting Accelerates

Building-integrated photovoltaics captured 37.8% of 2025 demand, reflecting Europe’s near-zero-energy codes and transparent façade retrofits. (3)NEXT Energy Technologies, “Transparent Façade Field Trial,” nextenergytech.com Indoor energy harvesting, driven by the growth of IoT sensors, is projected to achieve the highest compound annual growth rate (CAGR) of 16.1% and is expected to account for an increasing share of the organic solar cell market by 2031. In consumer electronics, thin and curved organic laminates are utilized to extend device runtime without increasing battery weight. In the automotive sector, prototypes from companies such as Sono Motors and Aptera have demonstrated solar range extensions of 64-245 km per day.

Agrivoltaic pilot projects in Italy and Spain are evaluating the use of semi-transparent organic sheets over crops. This emerging application could gain broader adoption once module lifetimes exceed 10 years. In defense applications, foldable modules are preferred due to their superior packability and durability compared to silicon, allowing for higher profit margins. Niche applications, including greenhouse glazing and marine canopies, remain limited in scale but highlight the adaptability of the technology's form factor.

By End-User: Commercial Leads, State Buyers Gain Speed

Commercial and industrial facilities accounted for 39.5% of the 2025 installations, as corporate real estate owners adopted transparent façades to meet net-zero commitments while maintaining natural light. Government and military demand is projected to grow at a CAGR of 15.3%, driven by defense agencies requiring lightweight mobile power solutions and public-building solar mandates set to take effect in India from 2026.

Utilities have initiated trials of semi-transparent canopy projects and dual-land-use agrivoltaic installations to diversify their asset portfolios. Residential adoption remains slower but is increasing within premium smart-home segments that prioritize aesthetics and integration with home automation systems. Throughout the forecast period, state procurement frameworks are expected to protect domestic suppliers from foreign competition, encouraging local plant investments despite their sub-gigawatt production capacities.

Geography Analysis

Europe accounted for 38.6% of the projected 2025 revenue, driven by the implementation of Energiewende policies, France's carbon-linked VAT rebates, and the EU Solar Standard, which together created a supportive regulatory framework. Germany's KfW green-loan incentives reduced financing costs for solar-plus-storage hybrids, which also benefited from the lower balance-of-system costs associated with organic modules. France’s tax advantage for low-carbon modules redirected retrofit budgets toward organic sheets, and Nordic countries are piloting transparent façades in new zero-carbon schools. (4)Source: European Commission, “EU Solar Standard Directive,” ec.europa.eu

The Asia-Pacific region is projected to exhibit the fastest growth, with a CAGR of 13.8%, driven by China's dominance in the specialty-chemical base for non-fullerene acceptor supply and India's planned 32% budget increase to INR 305.39 billion (USD 3.65 billion) by 2026, which mandates the use of locally manufactured cells for government projects. Japan's ALCA-Next consortium is focused on achieving efficiencies exceeding 20%, while South Korea's defense spending supports the development of early anchor customers. Although intellectual property disputes and export-control uncertainties present minor challenges, local roll-to-roll equipment manufacturers are accelerating factory ramp-ups.

North America accounts for a mid-teens market share, supported by California's Title 24 solar regulations and lightweight power tenders from the U.S. Department of Defense. Additional demand is generated by Canada's net-zero building code and Mexico's electronics near-shoring initiatives. In the Middle East, there is growing interest in transparent photovoltaic (PV) technology for iconic towers and shaded walkways. Meanwhile, Brazil is conducting agrivoltaic trials that integrate organic panels with shade-tolerant crops.

Competitive Landscape

The organic solar cell market is expected to exhibit moderate concentration. Heliatek's achievement of the 2024 IEC 61215 certification enabled bank-financed pilot projects with European utilities, establishing a benchmark for durability standards. Armor SA's ASCA division emphasizes printed modules for indoor electronics, while Mitsubishi Chemical leverages its expertise in polymer chemistry to advance ternary-blend scale-up efforts.

Strategic initiatives in the market focus on vertical integration into non-fullerene acceptor synthesis to address feedstock shortages, as well as partnerships with façade-glass suppliers, defense contractors, and automotive OEMs. Dracula Technologies secured EUR 40 million in funding in 2024, scaling its LAYER indoor modules, which were showcased at CES 2026 with a 30% performance improvement and a 10-year lifespan. Ubiquitous Energy is developing transparent windows for WELL-certified office spaces, while InfinityPV targets low-capex slot-die production lines for mass retail packaging applications.

Patent filings during 2025-2026 focus on advancements in edge sealing, ternary-blend formulations, and inline optical inspection technologies. These trends suggest that intellectual property will play a critical role in differentiation as production volumes increase. In the absence of widely accepted aging standards specific to organic solar cells, early adopters achieving third-party certifications are positioned to establish de facto industry norms, creating higher entry barriers for new competitors.

The organic solar cell industry prioritizes process control and supply chain resilience over sheer production scale, at least until roll-to-roll mega-factories achieve gigawatt-scale production, anticipated after 2028.

Organic Solar Cell Industry Leaders

Heliatek GmbH

Armor SA (ASCA)

Mitsubishi Chemical Group

InfinityPV ApS

Solarmer Energy Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Maxwell Technologies announced a USD 506 million investment to establish a perovskite-tandem equipment manufacturing facility in China. The facility aims to achieve an annual production capacity of 1 GW by 2028, increasing competitive pressure on organic solar cells in utility-scale applications, where cost-per-watt is a critical factor.

- March 2026: First Solar and Oxford PV have signed a patent license agreement to enable perovskite-on-cadmium-telluride tandem cells. This strategic move aligns with Oxford PV's planned commercial shipment milestone in September 2024 and poses a potential challenge to the niche market of organic cells in semi-transparent and lightweight applications.

- February 2026: India's Union Budget increased solar allocations by 32% year-over-year to INR 305.39 billion (approximately USD 3.65 billion). Additionally, mandates will require the use of locally manufactured cells in government projects starting June 2026, fostering a protected market for domestic organic-PV startups.

- June 2024: Heliatek has developed lightweight organic photovoltaic modules tailored for low load-bearing roofs and facades, enabling the expansion of building-integrated photovoltaic applications to older buildings with structural constraints.

Global Organic Solar Cell Market Report Scope

Organic solar cells (OSCs), also known as organic photovoltaics (OPVs), are lightweight, flexible, and often transparent solar cells manufactured using carbon-based materials, such as conductive polymers or small molecules, instead of silicon. These thin-film cells absorb sunlight to generate electricity, providing a flexible and, in many cases, more cost-effective alternative to conventional solar technologies.

The Global Organic Solar Cell Market is segmented into type, application, end-user, and geography. By type, the market is segmented into small-molecule, polymer, hybrid, and emerging structures. By application, the market is segmented into building-integrated photovoltaics (BIPV), consumer electronics, automotive, indoor energy harvesting, defense and aerospace, and others. By end-user, the market is segmented into residential, commercial and industrial, utilities, and government and military sectors. The report also covers the market size and forecasts for the organic solar cell market in 18 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Small-Molecule Organic Solar Cells |

| Polymer Organic Solar Cells |

| Hybrid Organic Solar Cells |

| Emerging Structures |

| Building-Integrated Photovoltaics (BIPV) |

| Consumer Electronics |

| Automotive |

| Indoor Energy Harvesting |

| Defense & Aerospace |

| Others |

| Residential |

| Commercial and Industrial |

| Utilities |

| Government and Military |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Small-Molecule Organic Solar Cells | |

| Polymer Organic Solar Cells | ||

| Hybrid Organic Solar Cells | ||

| Emerging Structures | ||

| By Application | Building-Integrated Photovoltaics (BIPV) | |

| Consumer Electronics | ||

| Automotive | ||

| Indoor Energy Harvesting | ||

| Defense & Aerospace | ||

| Others | ||

| By End-user | Residential | |

| Commercial and Industrial | ||

| Utilities | ||

| Government and Military | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the organic solar cell market be by 2031?

It is projected to reach USD 540.88 million, rising at a 12.41% CAGR from 2026 to 2031.

Which application is growing fastest for organic photovoltaics?

Indoor energy harvesting leads with a 16.1% CAGR as IoT devices proliferate.

Why are non-fullerene acceptors important?

They pushed certified efficiencies past 20% in 2025 and add about 3.2 percentage points to forecast CAGR.

Which region leads adoption today?

Europe commanded 38.6% of 2025 revenue due to strict carbon mandates and BIPV retrofits.

What limits broader utility-scale deployment?

Module lifetimes under 10 years and limited bankability standards keep financiers cautious.

Who holds the main market share among suppliers?

Heliatek, Armor SA, Mitsubishi Chemical, InfinityPV, and NEXT Energy Technologies together account for roughly 35% of global capacity.

Page last updated on: