Solar Control Glass Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

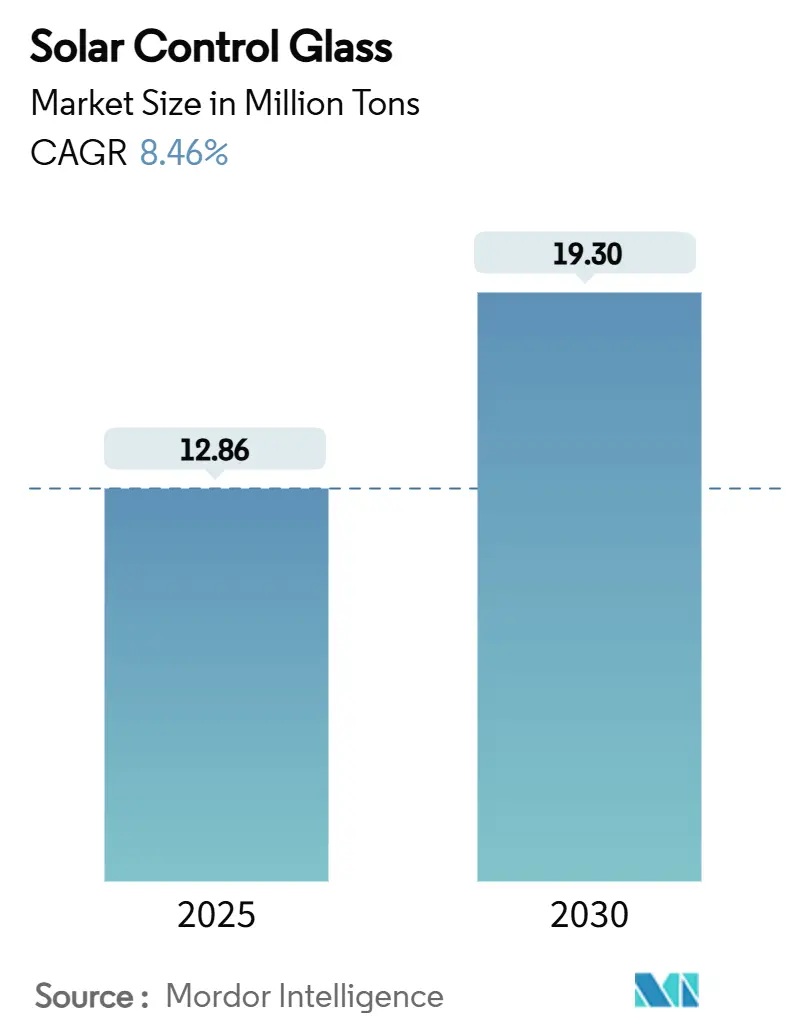

| Market Volume (2025) | 12.86 Million tons |

| Market Volume (2030) | 19.30 Million tons |

| Growth Rate (2025 - 2030) | 8.46% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Solar Control Glass Market Analysis by Mordor Intelligence

The Solar Control Glass Market size is estimated at 12.86 million tons in 2025, and is expected to reach 19.30 million tons by 2030, at a CAGR of 8.46% during the forecast period (2025-2030). Policy-driven demand, architectural moves toward high-performance façades, and technology upgrades in sputter-coating lines continue to pull this specialty glazing from optional to default specification. Rapid urban growth across Asia and rising retrofit activity in Europe and North America deepen the addressable base, while vehicle electrification opens an additional, fast-scaling outlet for low-emissivity and infrared-reflective glass. Incumbent producers defend share through vertical integration and line-level automation that curtail defect rates, even as electrochromic entrants carve premium niches. Supply risk is mitigated by fresh capacity in Malaysia and India, balancing the regional tilt that once favored a handful of Chinese float plants.

Key Report Takeaways

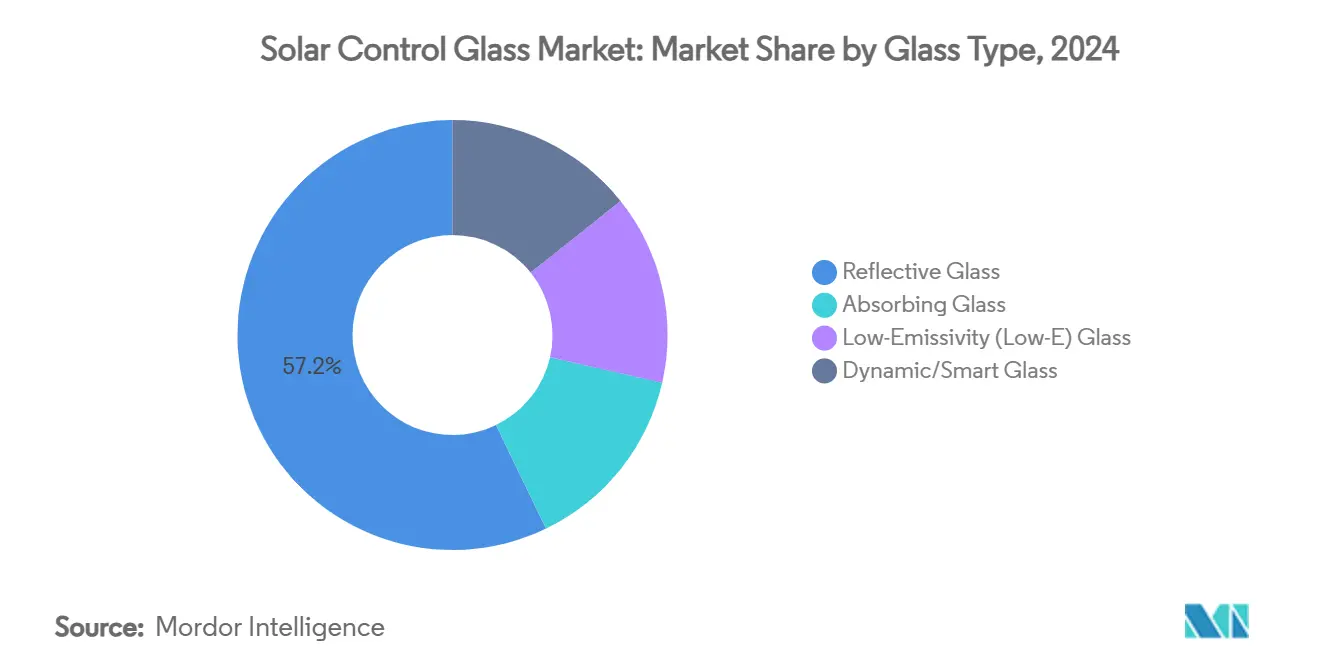

- By glass type, Reflective Glass led with 57.16% of the solar control glass market share in 2024; the segment is also expanding at a 9.45% CAGR through 2030.

- By coating type, Soft-Coat technology commanded 68.37% share of the solar control glass market size in 2024 while outpacing Hard-Coat at a 9.59% CAGR.

- By application, Building Façades and Curtain Walls captured 46.18% revenue in 2024 and are set to grow at 9.81% CAGR to 2030.

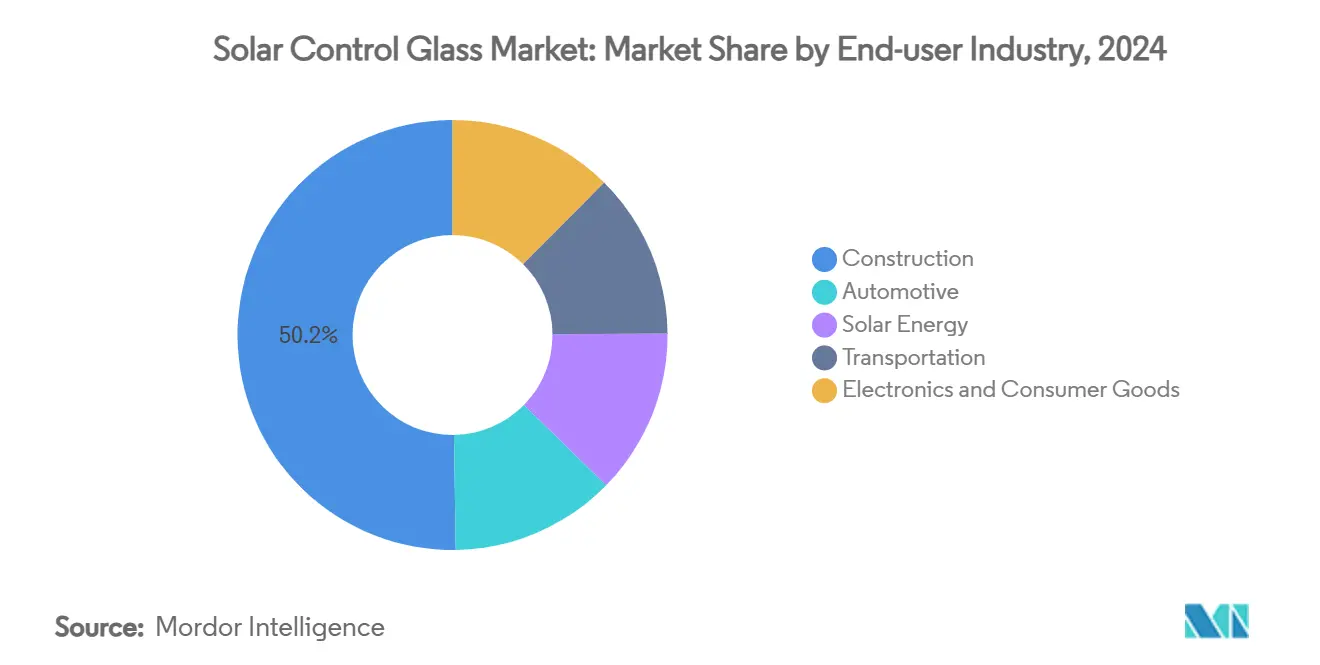

- By end-user industry, the Construction sector accounted for 50.24% of the solar control glass market size in 2024 and is progressing at a 9.86% CAGR.

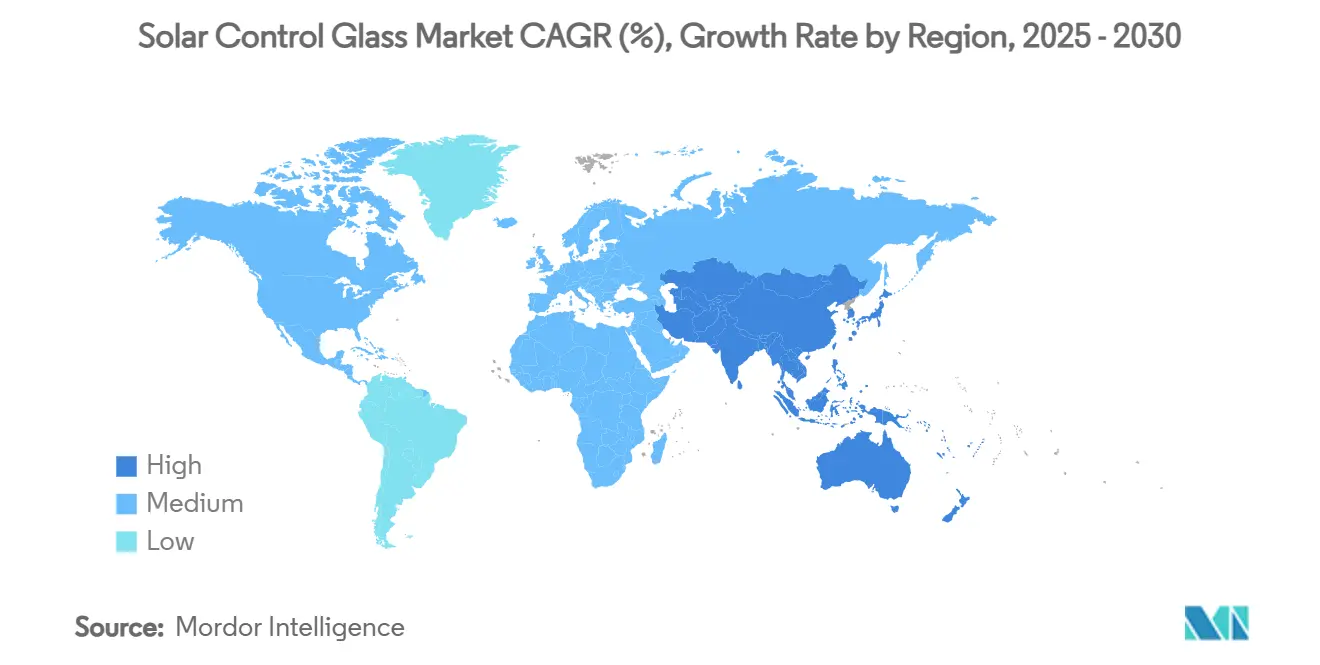

- By geography, Asia-Pacific held a 40.43% share in 2024; the region is forecast to accelerate at a 9.72% CAGR through 2030.

Global Solar Control Glass Market Trends and Insights

Driver Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Automotive glazing for cabin thermal management | +2.1% | Global focus on Asia-Pacific and North America | Medium term (2-4 years) |

| Stricter energy-efficiency regulations for building envelopes | +2.8% | North America and EU, emerging Asia-Pacific | Short term (≤ 2 years) |

| Rising construction in emerging economies | +1.9% | Asia-Pacific core, MEA, and Latin America spill-over | Long term (≥ 4 years) |

| Integration with BIPV systems | +1.2% | Europe and North America, early Asia-Pacific uptake | Long term (≥ 4 years) |

| Advances in dynamic tinting and electrochromic coatings | +0.8% | Global premium projects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption in Automotive Glazing for Cabin Thermal Management

Glass area in electric vehicles increases every model year as OEMs pursue visibility and design freedom. Low-e, IR-reflective panes now substitute roof sheet-metal, cutting HVAC draw and extending range, with Hyundai’s nano-film showing a 12.5 °C interior drop without sacrificing 70% visible light. Fleet operators validate the benefit: a 15-20% HVAC energy cut translates to notable fuel or battery savings across trucks and buses. Heated, metal-coated windshields combine defrost and solar control, commanding premium option pricing that buyers of luxury and battery-electric cars readily absorb. Autonomous-ready sensor pods embedded in laminate layers add further value and align with regulatory visibility rules. With Asia assembling more than half of global EVs, the solar control glass market gains a dependable automotive growth engine.

Stricter Energy-Efficiency Regulations for Building Envelopes

The 2024 IECC trimmed allowable U-factors for vertical fenestration by up to 17% versus the prior cycle, forcing builders to switch from clear float to coated units in virtually all U.S. climate zones. California’s Title 24 goes further, recognizing chromogenic glazing as a compliance credit, a shift echoed by EU Directive 2024/1275 that cites zero-emission building targets by 2050[1]European Parliament, “Directive 2024/1275,” eur-lex.europa.eu . These codes embed backstops that prevent trade-offs with mechanical systems, turning high-performance glass into a non-negotiable line item. Manufacturers capable of delivering consistent optical and thermal metrics across climate bands gain specification preference, while legacy hard-coat lines face obsolescence. Short regulatory cycles cement an accelerated replacement pull, supporting the solar control glass market even during construction slowdowns.

Rising Construction Activities in Emerging Economies

Urbanization keeps Asia-Pacific at the center of new-build demand. India alone forecasts tripling glass revenue for one leading producer by 2035 as domestic float and coat capability scales. Thailand, Vietnam, and Indonesia earmark infrastructure budgets that drive high-rise starts where the glazing fraction reaches 70% of the envelope area. Middle East landmarks such as the Mohammed Bin Rashid Library deploy electrochromic façades to safeguard interiors while meeting LEED targets.

Integration with Building-Integrated Photovoltaics (BIPV) Systems

Luminophore-based concentrators and bifacial thin films lift electrical yield by 25-30% while preserving clear views. A Swiss study records up to 122% energy-positive renovation outcomes with colored BIPV façades, returning 5.3-5.9% IRR over 18 years. Architects insist on neutral aesthetics; coating stacks are now tuned to mask PV busbars, widening acceptance for curtain-wall integration. Intelligent controls juggle heat-gain suppression with energy harvest, turning façades into dynamic generating skins that expand the solar control glass market scope.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost versus conventional float glass | -1.8% | Global, stronger in emerging markets | Short term (≤ 2 years) |

| Limited awareness in under-developed regions | -1.1% | Sub-Saharan Africa, parts of Asia and Latin America | Medium term (2-4 years) |

| Recycling and end-of-life regulatory challenges | -0.7% | Europe and North America, spreading worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Versus Conventional Float Glass

Solarban-grade coated units add 5-7% to installed façade budgets, a delta that balloons on megaprojects despite lifecycle savings. Electrochromic glass multiplies that premium, deterring first-cost-driven bids, especially in public builds where lowest price wins. Sputter lines cost hundreds of millions and run slimmer campaign mixes than generic float tanks, constraining amortization headroom. Until scale drops module cost, the solar control glass market will bifurcate between performance-led developed economies and value-driven emerging regions.

Limited Awareness in Under-Developed Regions

Specification often rests with contractors lacking energy-model literacy, keeping clear float entrenched. Few local labs in Africa or smaller Asian economies can certify coatings under hot-humid protocols, increasing import risk and deterring uptake. Training programs cluster in Europe and the U.S., creating knowledge gaps exactly where solar gain is harshest. Historical vernacular that favors masonry over glazing further slows adoption. Government procurement rules that ignore lifecycle cost reinforce the status quo, delaying full diffusion of the solar control glass market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Glass Type: Reflective Dominance Drives Market Evolution

Reflective panes held a 57.16% stake in 2024 and still clock the quickest 9.45% CAGR because engineers continue layering silver stacks that push visible neutrality yet reflect over 50% near-infrared. This traction anchors the solar control glass market even as low-e multiplies in triple-silver forms that drop emissivity to 0.02. Absorbing tints stay relevant for transport cabins that prioritize glare control. Dynamic glass is leveraged by color-neutral electrochromic cells shrug off earlier haze issues.

Second-generation quantum-optimized coatings trialed at university labs signal future displacements should production shift to roll-to-roll polymer substrates. Reflective stalwarts counter by embedding IR-reflective layers into laminated constructs that survive the temper cycle, keeping them specified for façades in tropical markets. With vehicle roof apertures widening, reflective and low-e share will blur as OEMs choose hybrid stacks that mix absorptive pigments with low-E layers.

By Coating Type: Soft-Coat Supremacy Endures

Soft-coat lines delivered 68.37% of 2024 volume, their 9.59% CAGR propelled by magnetron sputtering upgrades that guarantee ±1 nm layer accuracy and boost yield. Hard-coat pyrolytic glass holds niche share in residential remodeling, where easy tempering offsets lower performance. Yet new hard-coat recipes aiming for 0.12 emissivity show progress. The solar control glass market size linked to soft-coat expansion reflects downstream unitized curtain-wall modules that need color uniformity across batches.

Investment is migrating to low-carbon variants; AGC’s low-carbon float halves embedded CO₂ from 10.3 kg to 5.5 kg CO₂e /m², a decisive lever for architects chasing EPD credits. Fault-tolerant automation packages co-developed with Schneider Electric avert molten-tin contamination downtime, trimming scrap and stabilizing supply. As green mandates tighten, suppliers that certify both thermal and embodied-carbon metrics will fortify their footprint in the solar control glass market.

By Application: Building Façades Lead Architectural Integration

Façades and curtain walls represented 46.18% of 2024 shipments and will expand at 9.81% CAGR, hinging on code-driven envelope upgrades and the aesthetic pull of daylight-rich interiors. The solar control glass market share in façade-specific units is backed by triple-glazed spandrel panels combining low-e and ceramic frits for pattern variety. Window and door retrofits fuel steady underlying volume, particularly in Europe, where subsidy programs tie grants to verified U-factor drops.

Automotive glazing logs the steepest incremental tonnage as EV makers convert steel roofs to laminated glass for head-room perception and solar gain control. Smart roofs with SPD or PDLC films that tint within seconds debut in high-end models, hinting at trickle-down in mass segments.

By End-User Industry: The Construction Sector Drives Expansion

Construction absorbed 50.24% of 2024 tonnage and maintains a 9.86% growth clip, amplified by renovation inflows in developed economies and greenfield megacities in Asia. BIPV that now scores utility rebates, inflating end-use diversity within the solar control glass market size.

Transportation segments such as rail and marine specify laminated, heated, and fire-rated panes, broadening technical variety and sustaining mid-cycle orders even when building cycles pause. Consumer electronics adds a nascent but intriguing off-take for anti-reflection panels in high-brightness displays, signaling how cross-industry convergence will continue to stretch the boundaries of the solar control glass market.

Geography Analysis

Asia-Pacific booked 40.43% of 2024 volume and is set to widen its lead with a 9.72% CAGR as China’s public-works pipeline and India’s PLI-backed float lines scale rapidly. Thailand and Vietnam channel infrastructure spend into airport and metro expansions, each specifying unitized façades exceeding 60% glazing ratios, thereby deepening regional heft in the solar control glass market.

North America secures resilient demand through retrofit incentives. Canada’s Zero Carbon Building Standard echoes the trajectory, securing a stable upgrade pipeline for schools and healthcare facilities. Europe continues its green-deal momentum; Directive 2024/1275 obliges zero-emission new builds by 2030, triggering early replacement of post-2000 façades to meet net-zero envelopes[2]European Parliament, “Directive 2024/1275,” eur-lex.europa.eu .

Middle East and Africa ride megaprojects such as NEOM, where 75% of façade area specifies low-e and dynamic glazing under searing desert loads. South America edges forward with corporate headquarters that pilot smart-glass façades in Quito and São Paulo, helped by lower coastal humidity that favors sputter-line durability. Collectively, divergent regional drivers converge to reinforce the upward trajectory of the solar control glass market.

Competitive Landscape

The market is consolidated in nature. Top players defend share through captive silica mines, energy-efficient furnaces, and trenchless logistic chains that anchor cost competitiveness in the solar control glass market. Guardian’s SNX 70+ coating delivers 70% visible light with a sub-0.25 solar-heat-gain coefficient, sustaining specifier preference in daylight-centric designs. Innovation from SageGlass and other electrochromic pioneers forces incumbents to diversify, either via acquisitions or JV licenses. Regional players in China and India mature quickly; their second-generation coaters achieve 2 m wide glass at cycle times rivalling Japanese benchmarks.

Solar Control Glass Industry Leaders

AGC Inc.

Guardian Industries Holdings Site

Nippon Sheet Glass Co., Ltd

Saint-Gobain

Şişecam

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Nippon Sheet Glass launched HeatComfort, a heated insulating glass that maintains indoor temperature stability without altering U-value, adding comfort-plus sustainability in cold regions.

- September 2024: Guardian Glass North America began full-scale sales of SunGuard SNX 70+ high-VLT, low-SHGC coated glass for daylight-rich façades.

Global Solar Control Glass Market Report Scope

| Absorbing Glass |

| Reflective Glass |

| Low-Emissivity (Low-E) Glass |

| Dynamic / Smart Glass |

| Hard-Coat (Online Pyrolytic) |

| Soft-Coat (Offline Sputter) |

| Building Facades and Curtain Walls |

| Windows and Doors |

| Automotive Glazing |

| Other Appplications (Skylights and Roof Glazing, Solar Panels and BIPV Modules, etc.) |

| Construction |

| Automotive |

| Solar Energy |

| Transportation |

| Electronics and Consumer Goods |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Glass Type | Absorbing Glass | |

| Reflective Glass | ||

| Low-Emissivity (Low-E) Glass | ||

| Dynamic / Smart Glass | ||

| By Coating Type | Hard-Coat (Online Pyrolytic) | |

| Soft-Coat (Offline Sputter) | ||

| By Application | Building Facades and Curtain Walls | |

| Windows and Doors | ||

| Automotive Glazing | ||

| Other Appplications (Skylights and Roof Glazing, Solar Panels and BIPV Modules, etc.) | ||

| By End-User Industry | Construction | |

| Automotive | ||

| Solar Energy | ||

| Transportation | ||

| Electronics and Consumer Goods | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the solar control glass market in 2025?

The solar control glass market size is 12.86 million tons in 2025 and is projected to reach 19.30 million tons by 2030.

Which glass type holds the leading share?

Reflective Glass commands 57.16% of 2024 volume and continues to grow faster than the overall market at 9.45% CAGR.

What region leads demand?

Asia-Pacific accounts for 40.43% of 2024 shipments and is on track for a 9.72% CAGR through 2030.

Why is soft-coat technology preferred?

Soft-coat delivers lower emissivity (0.03-0.12) than hard-coat, providing superior thermal performance demanded by modern energy codes.

How do regulations influence market growth?

Revised codes such as the 2024 IECC and EU zero-emission directives mandate lower U-factors, driving adoption of coated and dynamic glazing.

Page last updated on: