Solar Photovoltaic Glass Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

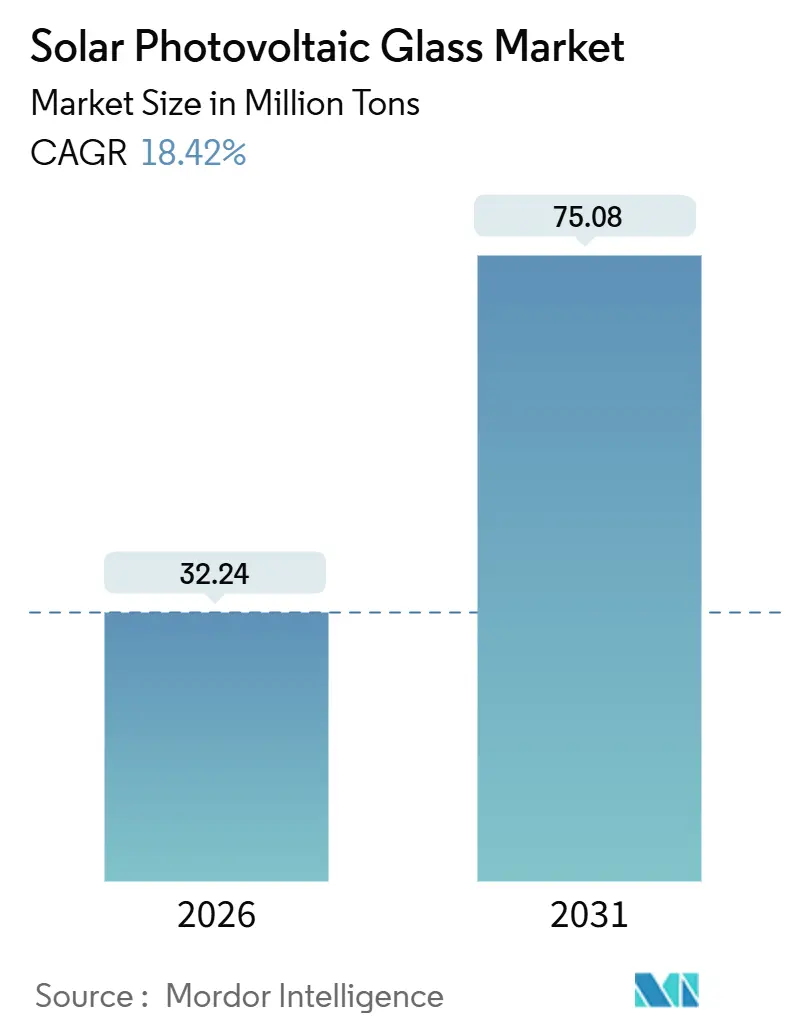

| Market Volume (2026) | 32.24 Million tons |

| Market Volume (2031) | 75.08 Million tons |

| Growth Rate (2026 - 2031) | 18.42% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Solar Photovoltaic Glass Market Analysis by Mordor Intelligence

The Solar Photovoltaic Glass Market size is estimated at 32.24 Million tons in 2026, and is expected to reach 75.08 Million tons by 2031, at a CAGR of 18.42% during the forecast period (2026-2031). Government-mandated local-content rules, anti-dumping measures, and targeted tax credits are catalyzing regional capacity additions, even as global module oversupply intermittently depresses prices. Trade barriers in India and incentive packages in the United States have reshaped procurement economics, pushing float-line investments onshore and fracturing a once-global supply chain. Technology shifts toward bifacial, glass-glass, and thin-film modules are doubling per-watt glass intensity in certain projects, while recycled-cullet mandates in Europe add a parallel source of volume growth. Competitive dynamics are intensifying as module makers backward-integrate to secure margin and supply certainty, widening the strategic gap between scale-driven Asian leaders and policy-sheltered North American entrants.

Key Report Takeaways

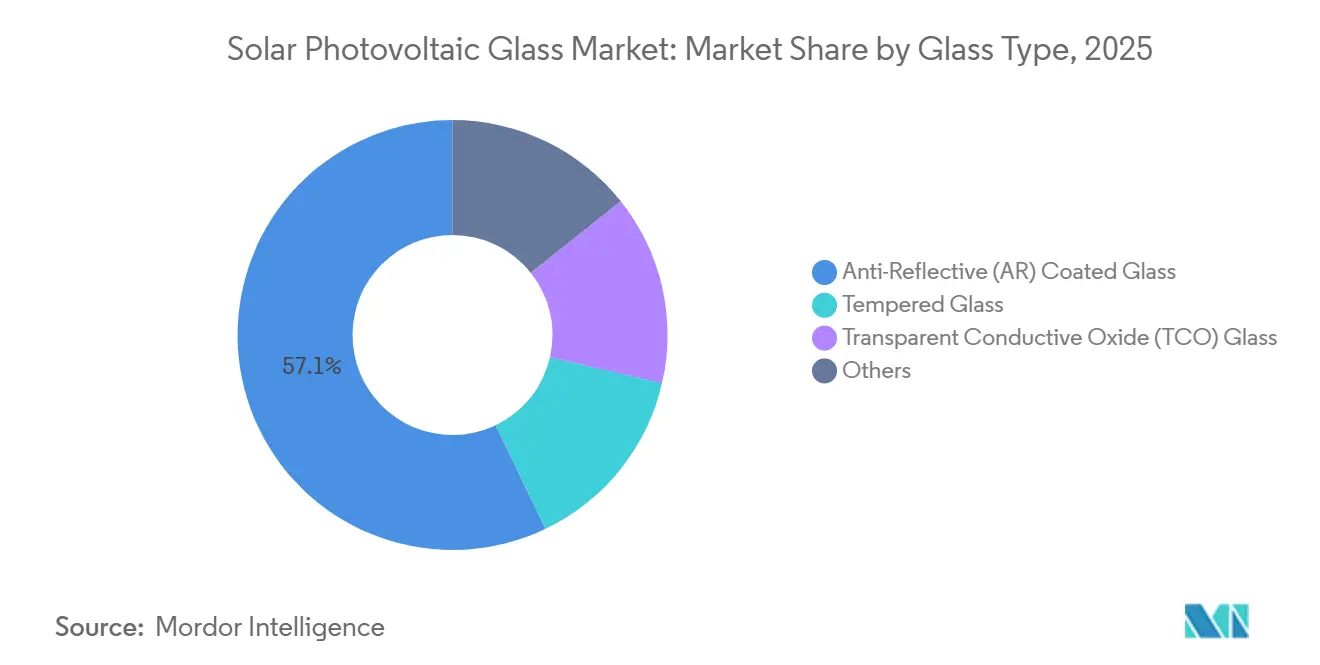

- By glass type, anti-reflective coated glass led with 57.12% of the solar photovoltaic glass market share in 2025, while transparent conductive oxide glass is projected to grow at a 22.43% CAGR to 2031.

- By manufacturing process, float-line production accounted for 67.78% of the solar photovoltaic glass market size in 2025, and rolled glass is set to advance at a 19.56% CAGR through 2031.

- By solar technology, crystalline silicon captured 90.90% of demand in 2025, whereas CIGS is forecast to post the fastest 23.42% CAGR by 2031.

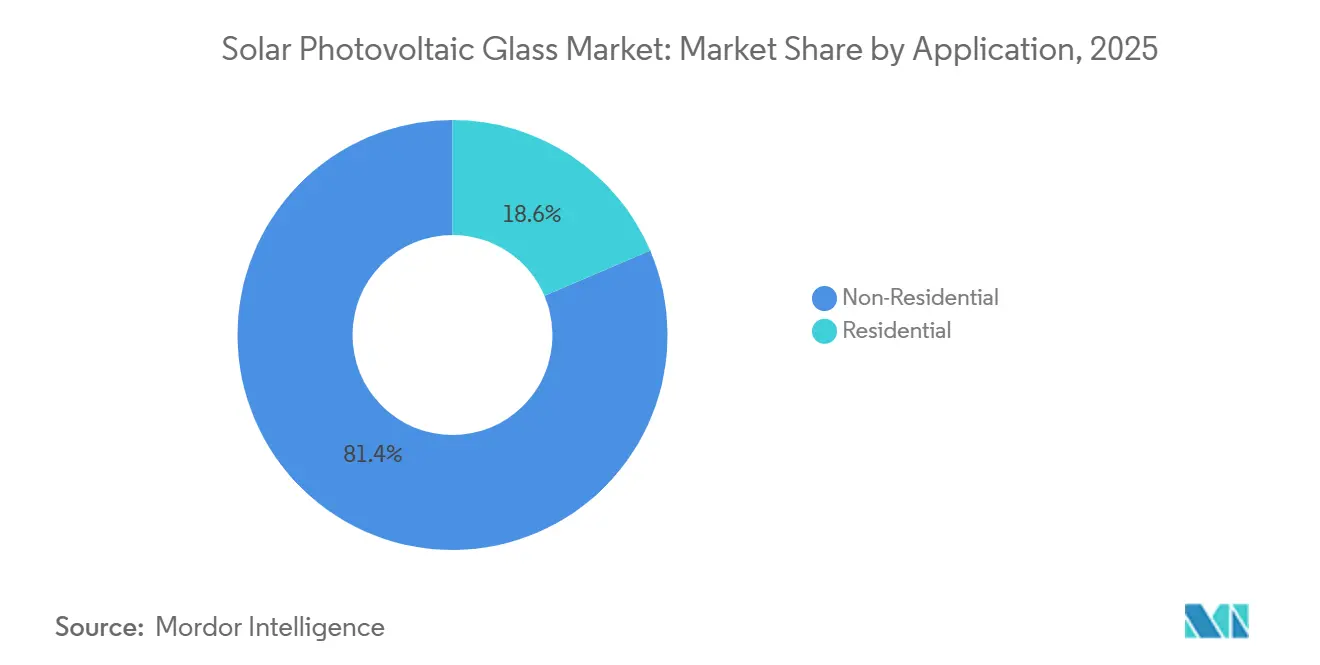

- By application, non-residential installations commanded 81.43% of volume in 2025 and are expected to maintain an 18.78% CAGR over the forecast period.

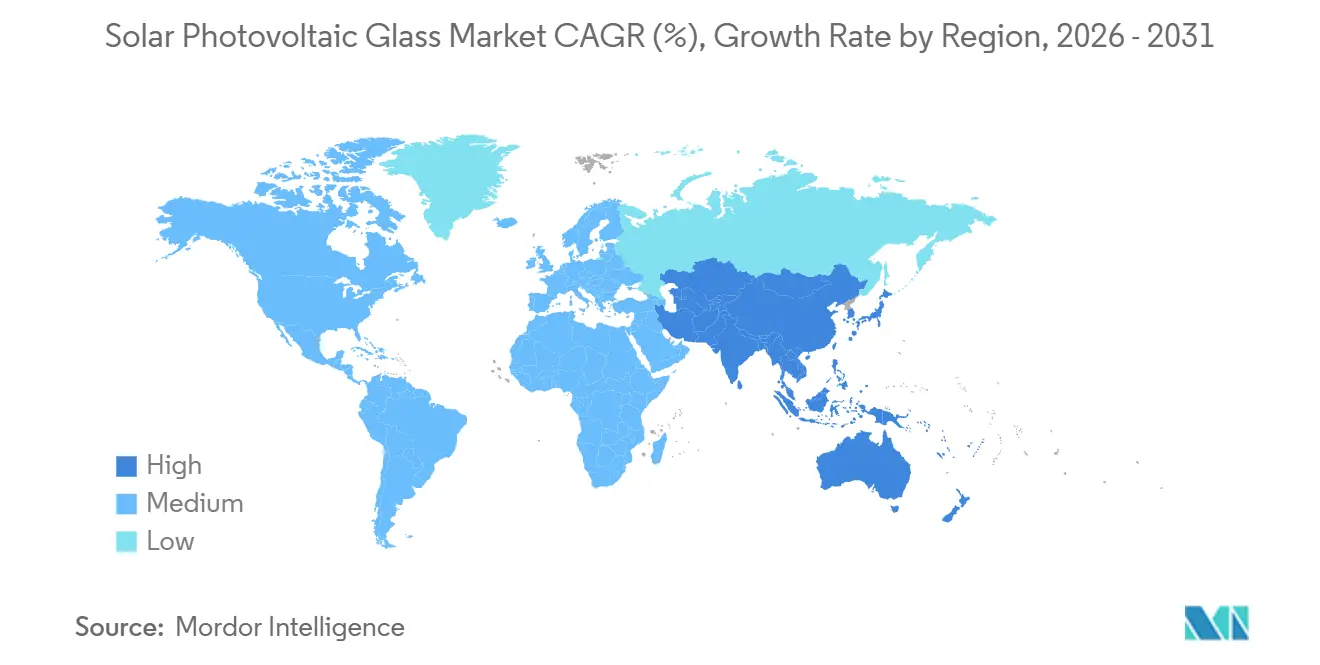

- By geography, Asia-Pacific dominated with 61.14% of the 2025 volume and is poised to expand at a 19.34% CAGR, the highest regional growth rate.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Solar Photovoltaic Glass Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-mandated solar-glass quotas in Asia | +4.2% | China, India, ASEAN spill-over | Medium term (2-4 years) |

| Rapid build-out of ultra-low-iron float lines in MENA | +3.1% | Saudi Arabia, UAE, Egypt | Long term (≥4 years) |

| Rising adoption of bifacial and glass-glass modules | +3.8% | Global, led by APAC and North America | Short term (≤2 years) |

| Inflation Reduction Act-fuelled U.S. reshoring | +2.7% | United States | Medium term (2-4 years) |

| Circular-economy demand for recycled glass | +1.9% | EU core, Japan pilots | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Government-Mandated Solar-Glass Quotas in Asia

Local-content quotas in China and India are pulling furnace capacity back onshore after a decade of offshoring that favored lower-cost Southeast Asian hubs. India’s Directorate General of Trade Remedies imposed anti-dumping duties of USD 570–664 per ton on Chinese and Vietnamese imports in December 2024, instantly reversing landed-cost advantages for overseas suppliers. Simultaneously, China’s Ministry of Industry and Information Technology issued draft rules in mid-2025 requiring that at least 60% of a module’s glass be sourced within provincial borders, supporting employment in traditional glass-producing provinces[1]Ministry of Industry and Information Technology, “Draft Local-Content Guidance,” scmp.com. These measures shorten logistics chains, shelter domestic producers from import competition, and accelerate furnace-build decisions even during periods of soft module demand. Capacity growth decoupled from end-market fundamentals in late 2025, creating periodic regional oversupply but sustaining the overall solar photovoltaic glass market growth curve. Although logistics costs have risen, local players benefit from secure off-take and policy-driven margins.

Rapid Build-Out of Ultra-Low-Iron Float Lines in Middle-East and North Africa

Saudi Arabia, the United Arab Emirates, and Egypt are exploiting low-cost gas and strong solar resources to establish export-ready float-line clusters. ACWA Power’s 2 GW Al Dhafra project in Abu Dhabi demonstrated regional self-sufficiency by sourcing tempered glass from nearby furnaces in 2025. Riyadh’s Public Investment Fund earmarked USD 500 million for a 1,000-ton-per-day plant at Jubail, with commissioning set for 2026. Egypt’s New and Renewable Energy Authority signed an MoU with Şişecam in 2025 to study a Suez-adjacent line aimed at European offtakers. These investments promise a structurally lower cash cost due to feedstock energy economics but face execution risks tied to equipment lead times and offtake agreements. If schedules slip, capital may be stranded in a market already contending with module oversupply, underscoring the importance of synchronized downstream demand.

Rising Adoption of Bifacial and Glass-Glass Modules

Utility-scale developers are flocking to bifacial and glass-glass architectures that boost yield and extend module life. Bifacial penetration reached 35% of 2025 installations, particularly in high-albedo deserts and snow-covered regions, effectively doubling glass demand per watt[2]International Energy Agency, “Renewables 2025,” iea.org. First Solar’s Series 7 dual-glass CdTe module logged a degradation rate below 0.4% per year, reinforcing investor appetite for long-dated cash flows. The shift is asymmetric; residential installers still favor lighter polymer backsheets, creating planning complexity for glass suppliers. Nevertheless, expanded bifacial uptake is set to add incremental volume even if overall module growth moderates, bolstering solar photovoltaic glass market momentum.

Inflation Reduction Act-Fuelled United States PV-Glass Reshoring

Section 45X of the Inflation Reduction Act delivers a USD 0.40 per m² production tax credit for domestic solar glass, flipping the investment calculus for U.S. float lines. First Solar’s USD 1.1 billion expansion across Ohio and Alabama in 2024 added 3.3 GW of modules and integrated TCO glass lines. Guardian Industries followed in early 2025, committing to retrofit its Kingsburg, California furnace for ultra-low-iron output. While incentives bridge the cost gap, the United States faces skills shortages in furnace operations and an 18-month lead time for critical refractories, delaying ramp-ups. Treasury guidance issued in mid-2025 further clarifies that only glass melted and tempered domestically qualifies, ensuring new capacity rather than partial finishing.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soda-ash and energy-price volatility | -1.8% | Global, acute in Europe and Turkey | Short term (≤2 years) |

| Capital-intensive furnace conversion to low-carbon fuels | -1.4% | EU, North America, Japan | Long term (≥4 years) |

| Hail-damage risk to thin heat-strengthened glass | -0.9% | North America, Australia, Brazil | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Soda-Ash and Energy-Price Volatility

Soda ash made up 12-15% of raw-material costs in 2025 and spiked 38% Y/Y when natural-gas curtailments shuttered Turkish and Chinese plants. Glass furnaces themselves rely heavily on gas; European operators saw TTF prices average EUR 45/MWh in H1 2025, triple the long-term norm. Spanish and Italian lines opted for maintenance shutdowns over operating at negative margins, while Chinese mills, sheltered by state-controlled pricing, widened their cost advantage. Volatility compresses cash flows and delays investment decisions, tempering but not derailing the solar photovoltaic glass market expansion.

Capital-Intensive Furnace Conversion to Low-Carbon Fuels

Hydrogen-fueled or electric furnaces cost USD 80–120 million per 600-TPD line, a hurdle that only the largest players can cross ahead of Europe’s 2027 Carbon Border Adjustment Mechanism. Schott’s pilot hydrogen furnace cut Scope 1 emissions by 70% but reduced campaign life from 12 to 8 years due to refractory wear. NSG’s electric pilot in Japan ran at a 15% cost premium when grid prices topped JPY 20/kWh (USD 0.13/kWh). The technology pathway is proven but capital-heavy, making timing contingent on regulatory clarity and green hydrogen availability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Glass Type: Coatings Enhance Yield, TCO Accelerates

Anti-reflective coated glass held 57.12% of 2025 volume, cementing its role as the performance baseline for crystalline-silicon modules. Transparent conductive oxide glass, though a smaller slice of the solar photovoltaic glass market size, is set for a rapid 22.43% CAGR as thin-film demand scales. Tempered substrates continue in rooftop markets because building codes emphasize impact resistance, but growth is slower as utility projects shift to lighter heat-strengthened variants. First Solar’s inline-TCO float process trims production time by 15%, making vertically integrated CdTe lines less exposed to spot glass pricing.

Premium dual-layer AR coatings from AGC cut reflectance below 1%, translating into module-level efficiency gains of up to 0.5 percentage points. The coating space is bifurcating: tier-one manufacturers pay USD 2-3/m² extra for anti-soiling layers, while price-sensitive developers opt for uncoated glass. Specialty products for agrivoltaics and building-integrated photovoltaics, including semi-transparent options, form niche avenues that lift overall value per ton, reinforcing the solar photovoltaic glass market growth narrative.

By Manufacturing Process: Float Leads, Rolled Rebounds

Float-line technology controlled 67.78% of 2025 output owing to superior flatness (<0.1 mm/m) critical for high-efficiency cells. Rolled glass, historically confined to thin film, is forecast to rise at a 19.56% CAGR as CdTe and CIGS lines multiply. A solar photovoltaic glass market size advantage stems from float’s scale economics - Xinyi operates 14 lines with cash costs below USD 180/ton - but its 24/7 nature locks in high fixed energy demand. Rolled production offers demand-responsive flexibility and textured surfaces that aid light trapping, narrowing the quality gap through automated thickness control systems.

Guardian’s retrofitted Kingsburg float line aims to tap domestic-content premiums in the United States, showing policy can offset float operating rigors. Meanwhile, Taiwan Glass is tightening rolled-glass tolerance to ±0.15 mm, making it suitable for bifacial modules. Incremental process shifts could redistribute share but leave float structurally dominant through 2031.

By Solar Technology: Crystalline Dominates, CIGS Surges

Crystalline silicon absorbed 90.90% of glass tonnage in 2025, supported by wafer cost deflation and entrenched supply chains. CIGS, off a low base, is projected at a 23.42% CAGR as flexible form factors open portable and building-integrated avenues. Cadmium-telluride modules require proprietary TCO glass, providing First Solar with captive demand and pricing insulation. Emerging perovskite-silicon tandems, such as Hanwha Q CELLS’ 28%-efficient pilot, may shift specifications toward alternative substrates, but commercialization remains post-2027. For now, crystalline expansion anchors the solar photovoltaic glass market share, while niche thin-film gains diversify the product mix.

By Application: Utility-Scale Non-Residential Drives Volume

Non-residential projects represented 81.43% of 2025 demand and are forecast to maintain an 18.78% CAGR through 2031. Utility-scale farms favor 2.0 mm bifacial glass to cut material usage, reinforcing volume leadership. Commercial rooftops and industrial facilities add steady but smaller demand streams under corporate decarbonization mandates. Residential uptake grows from a lower base yet is tempered by higher financing costs. Specialized segments such as agrivoltaics require semi-transparent coatings, and floating solar relies on moisture-resistant glass, both adding differentiated demand pockets that keep overall solar photovoltaic glass market growth broad-based.

Geography Analysis

Asia-Pacific held 61.14% of global volume in 2025 and is on pace for a 19.34% CAGR, the fastest regional climb. China’s Xinyi and CSG operated more than 32,000 TPD of capacity but paused new furnace ignitions in early 2026 as glass prices dipped below cash cost. India’s December 2024 anti-dumping duties triggered domestic expansions by Borosil Renewables and HNG Float Glass, insulating the local solar photovoltaic glass market from import pressure. Japan and South Korea remain smaller in tonnage yet focus on high-efficiency TCO lines linked to tandem-cell research and development. Southeast Asian exporters, once cost leaders, now face margin pressure from rising protectionism in end-markets.

North America records a lower absolute share but commands the steepest percentage capacity growth because of Section 45X credits. First Solar’s Ohio and Alabama complexes, plus Guardian’s California retrofit, anchor a reshoring wave that rewards integrated players with bonus tax incentives. Canada’s upcoming 5 GW module plant by Canadian Solar will source glass domestically, while Mexico positions itself for nearshore supply into the United States under USMCA rules. Lead-time advantages and content bonuses collectively underpin a differentiated solar photovoltaic glass market strategy versus import-heavy models.

Europe’s share was relatively low in 2025 as high gas prices shuttered several legacy lines; TTF futures averaged EUR 45/MWh in the first half, triple historical norms. Innovation persists, however: Saint-Gobain-Veolia’s Lyon recycling facility and Schott’s hydrogen-fired pilot furnish technology leadership and align with the EU’s 2027 Carbon Border Adjustment Mechanism. Central European rolled-glass makers struggle against Asian imports even after tariffs, pointing to consolidation ahead. South America and Middle East and Africa remain growth frontiers, with Saudi Arabia’s 1,000-TPD Jubail line and Brazil’s BNDES-backed São Paulo project underscoring policy-driven localization pushes that extend the global solar photovoltaic glass market footprint.

Competitive Landscape

The global solar photovoltaic glass market is moderately fragmented. Backward integration by module makers intensifies rivalry, as illustrated by Hanwha Solutions’ 1,200-TPD Korean float line commissioned in 2024. Asian incumbents chase economies of scale, squeezing cash costs below USD 180/ton, while U.S. entrants monetize policy premiums and reduced freight. European producers differentiate through decarbonization credentials and recycled-content compliance, preserving margin in a high-cost energy environment. Technology is an emerging moat. First Solar’s inline fluorine-doped tin-oxide deposition eliminates a sputter step and trims cycle time 15%, securing IP-driven margins. AGC’s dozen dual-layer AR patents filed since 2024 spotlight a pivot to coating innovation. Disruptors like Onyx Solar and Interfloat exploit specialty niches (semi-transparent façades and low-cost rolled thin-film substrates) that sit outside volume-centric battles yet expand overall solar photovoltaic glass market diversity. Capital intensity remains a hurdle; new 600-TPD lines need USD 80–120 million, limiting entrants to players with balance-sheet strength or policy support. Consolidation talk heightened in 2025 after soda-ash price spikes compressed margins for second-tier independents, indicating room for mergers.

Solar Photovoltaic Glass Industry Leaders

Xinyi Solar Holdings Limited

Flat Glass Group Co. Ltd.

AGC Inc.

CSG Holding Co. Ltd.

Saint-Gobain

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: First Solar completed its USD 1.1 billion Ohio and Alabama expansion, adding 3.3 GW of CdTe modules and integrated TCO glass lines.

- September 2024: Guardian Industries announced a retrofit of its Kingsburg, California, float line to ultra-low-iron production, tapping U.S. tax credits.

- August 2024: Hanwha Solutions commissioned a 1,200-TPD float line in South Korea, achieving full vertical integration.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the solar photovoltaic glass market as low-iron glass sheets that encapsulate or replace conventional module covers and simultaneously function as the light-harvesting surface in crystalline-silicon, CdTe, CIGS, or other PV modules. According to Mordor Intelligence, sizing is expressed in metric tons of new PV-grade glass shipped to module makers or directly integrated in building façades.

Scope exclusion: patterned solar control glass without integrated photovoltaic functionality, automotive smart glass, and any post-consumer recycled volume are outside this study.

Segmentation Overview

- By Glass Type

- Tempered Glass

- Anti-Reflective (AR) Coated Glass

- Transparent Conductive Oxide (TCO) Glass

- Others

- By Manufacturing Process

- Float Glass

- Rolled Glass

- By Solar Technology

- Crystalline Silicon

- Cadmium-Telluride (CdTe) Thin Film

- Amorphous Silicon (a-Si)

- Copper-Indium-Gallium-Diselenide (CIGS)

- Other Technologies

- By Application

- Residential

- Non-Residential

- Commercial

- Industrial/Institutional

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Netherlands

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- South Africa

- Egypt

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed manufacturing engineers from float-line operators, procurement managers at module assemblers across Asia, Europe, and North America, and EPC contractors active in utility-scale projects. These conversations confirmed average melt-tank utilizations, real-world wastage, and anticipated AR-coating adoption, allowing us to close data gaps flagged during desk research and to triangulate cost progression assumptions.

Desk Research

We began with structured pulls from public bodies such as the International Renewable Energy Agency, the International Energy Agency PVPS database, China's National Energy Administration, and Eurostat trade codes for HS-700719. These sources outlined installed PV capacity additions and cross-border flows of low-iron rolled glass, which anchored regional supply-demand balances. Our team then layered insights from company 10-Ks, investor decks, SolarPower Europe installation trackers, and customs-level shipment analytics retrieved through Volza and D&B Hoovers to refine conversion factors for glass per watt ratios. The indicative sources listed are not exhaustive; many additional open datasets and press releases were referenced for validation.

Market-Sizing & Forecasting

A top-down production and trade reconstruction established 2025 demand, after which regional supplier roll-ups and sampled average selling price multiplied by weight served as cross-checks. Key variables fed into the model include national installation targets, square meters of module glass per watt, float-line capacity pipelines, glass conversion yield, and quarterly ASP shifts. Multivariate regression paired with scenario analysis projects volume to 2030, while an ARIMA overlay smooths cyclical fluctuations in module build rates. Where bottom-up estimates diverged, we recalibrated coefficients through iterative back-testing against historical shipments.

Data Validation & Update Cycle

Outputs pass a two-level analyst review that flags anomalies versus independent indicators such as polysilicon drawdowns and EVA sheet sales. Reports refresh annually, with mid-cycle updates triggered by capacity announcements, trade policy shifts, or greater than 5 percent variance in quarterly installations.

Why Mordor's Solar Photovoltaic Glass Baseline Earns Trust

Published numbers often differ because firms mix solar control glass with PV grades, apply disparate ASP progressions, or convert currencies at outdated rates.

Key gap drivers lie in scope breadth, unit of account, and refresh cadence. We report physical tons tied to module production schedules, whereas many publishers release blended dollar values or include non-PV architectural glass, which inflates totals. Others project aggressive CAGR paths without reconciling them against float-line construction lead times or ethylene-vinyl-acetate supply constraints.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| 32.10 Mn tons (2025) | Mordor Intelligence | - |

| USD 53.5 Bn (2024) | Global Consultancy A | Mixes PV and solar control glass, value basis, broader product scope |

| USD 17.3 Bn (2024) | Industry Journal B | Excludes China's captive glass output, relies on installation-led revenue multiples |

| USD 10.08 Bn (2024) | Regional Consultancy C | Uses static ASP, limited primary checks, last update greater than 18 months ago |

Taken together, the comparison shows that Mordor's disciplined, annually refreshed tonnage model grounded in verified production and trade data offers clients the most reproducible baseline for strategic planning.

Key Questions Answered in the Report

What is the projected size of the solar photovoltaic glass market by 2031?

The market is expected to reach 75.08 million tons by 2031, expanding from 32.24 million tons in 2026.

How fast is demand for transparent conductive oxide glass growing?

TCO glass is forecast to register a 22.43% CAGR between 2026 and 2031, the fastest among glass types.

Which region will add capacity most quickly over the forecast period?

Asia-Pacific will maintain the highest absolute volume, while North America posts the steepest percentage growth due to U.S. tax incentives.

How are policy measures influencing glass manufacturing locations?

Anti-dumping duties in India, local-content quotas in China, and U.S. Section 45X tax credits are driving a shift toward regionalized, onshore float-line investments.

What technology trends are changing glass demand intensity?

Wider adoption of bifacial and glass-glass modules is roughly doubling glass usage per watt in many utility-scale projects, boosting overall volume growth.

What is the biggest cost challenge facing producers today?

Volatility in soda-ash and natural-gas prices compresses margins, especially in Europe, where energy costs remain elevated.

Page last updated on: