Float Glass Market Size and Share

Market Overview

| Study Period | 2025 - 2031 |

|---|---|

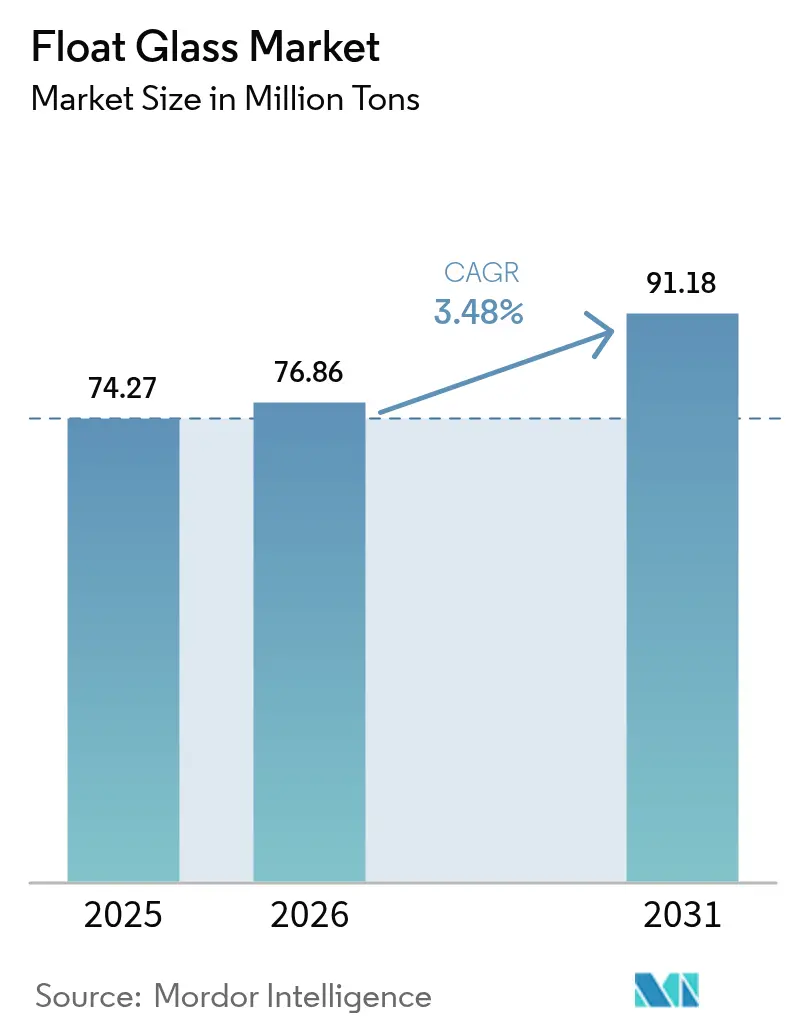

| Market Volume (2026) | 76.86 Million tons |

| Market Volume (2031) | 91.18 Million tons |

| Growth Rate (2026 - 2031) | 3.48% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Float Glass Market Analysis by Mordor Intelligence

Float Glass Market size in 2026 is estimated at 76.86 million tons, growing from 2025 value of 74.27 million tons with 2031 projections showing 91.18 million tons, growing at 3.48% CAGR over 2026-2031. Surging demand for high-performance substrates in solar, automotive, and energy-efficient façades supports steady volume gains even as traditional construction end-uses mature. Manufacturers leverage process automation and furnace upgrades to curb the volatility stemming from soda-ash and natural-gas input costs, while decarbonization investments safeguard access to export markets facing carbon-based trade barriers. Competitive differentiation now rests less on throughput and more on precision, reliability, and the capacity to deliver ultra-clear, thin, or multi-functional sheets that command premium margins. Rapid installations of utility-scale solar arrays in North America and the shift toward low-carbon building envelopes in Europe are reshaping global procurement models, forcing Asian suppliers to accelerate emission-reduction roadmaps to maintain share. With multibillion-dollar capacity additions scheduled in both China and the United States, the float glass market continues to rebalance toward regionalized supply chains that prioritize resilience and carbon efficiency.

Key Report Takeaways

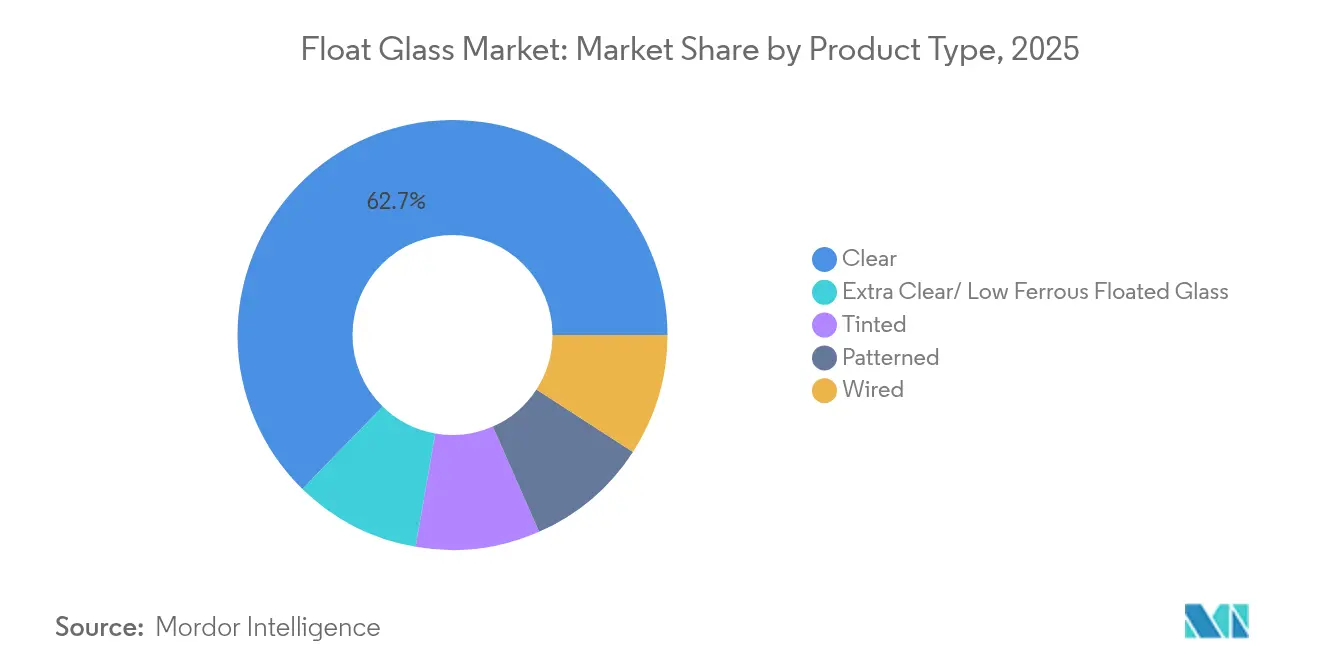

- By product type, clear glass led with 62.70% of the float glass market share in 2025, growing at a CAGR of 3.79% through 2031.

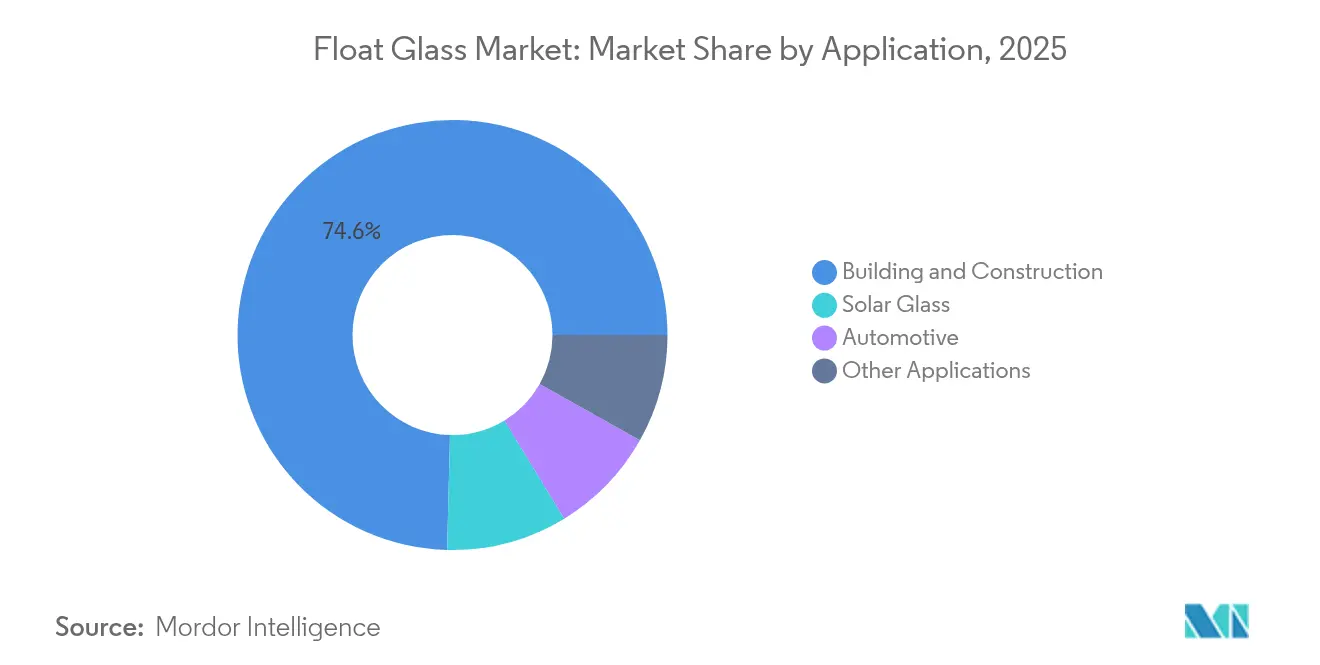

- By application, building and construction led with a share of 74.60% in 2025, while solar glass advanced at an 8.01% CAGR through 2031, the highest rate among all segments.

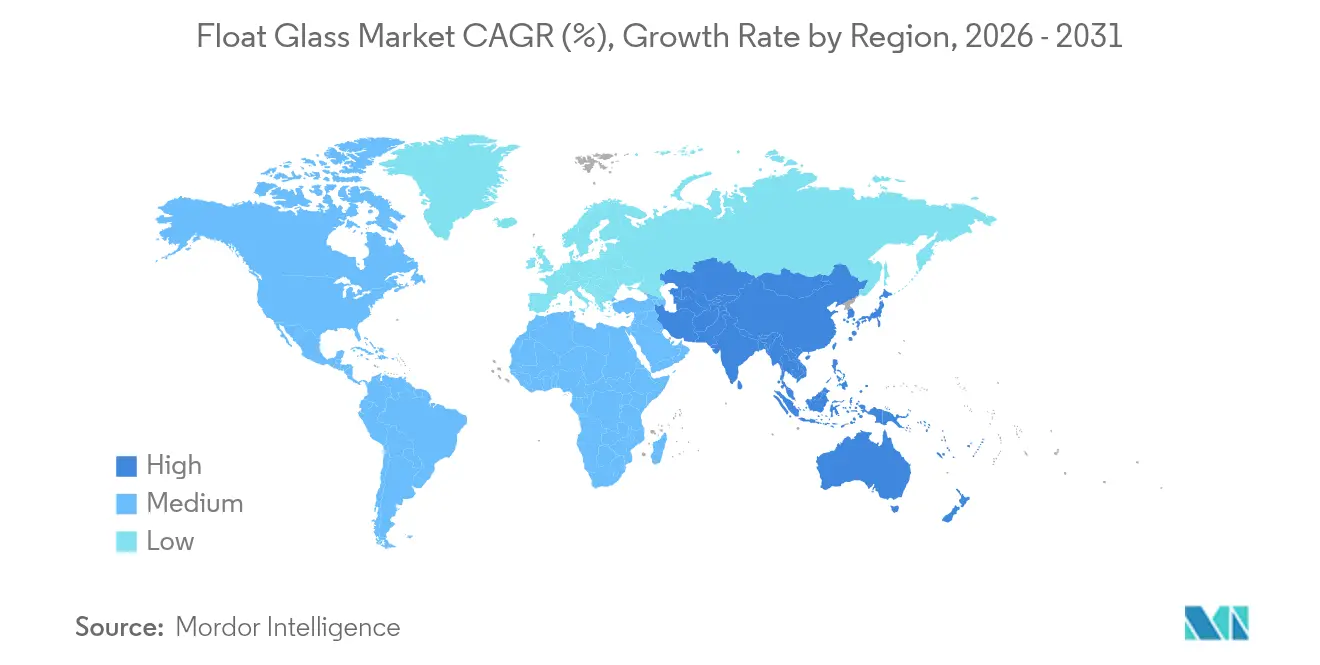

- By geography, Asia-Pacific accounted for 62.65% of the float glass market size in 2025 and is projected to expand at 3.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Float Glass Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction-sector expansion in emerging economies | +0.8% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| Automotive lightweighting raises glazing m² per vehicle | +1.2% | Global, with concentration in APAC and North America | Long term (≥4 years) |

| Utility-scale solar buildouts boost demand for low-iron float glass | +0.9% | Global, led by North America and APAC | Short term (≤2 years) |

| Urban regeneration mandates energy-efficient façades | +0.4% | Europe and North America, expanding to APAC urban centers | Medium term (2-4 years) |

| BIPV façade regulations spur ultra-clear low-iron substrates | +0.3% | Europe core, early adoption in North America and APAC | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Construction-Sector Expansion in Emerging Economies

Decisive public-sector outlays on transport, housing, and industrial corridors are fueling sustained purchases of architectural glass across South and Southeast Asia. India’s construction pipeline equals 3.5 times the sector’s annual operating revenue. Thailand’s Eastern Economic Corridor continues to absorb large sheet volumes even as labor shortages slow project execution. With regional float lines already running at utilization rates below 80%, producers situated near these demand hubs can ramp shipments swiftly without green-field investments. As a result, the float glass market will rely on fast-growing emerging economies to offset plateauing consumption in mature Western countries.

Automotive Lightweighting Raises Glazing M² Per Vehicle

Electrification mandates have made weight a premium KPI for automakers, yet advanced driver-assistance systems, panoramic roofs, and immersive infotainment screens are simultaneously expanding the glass surface area per car. This paradox underpins a structural upswing for the float glass market, as OEMs specify thinner yet larger laminated or tempered panes that integrate antennas, heaters, and head-up-display coatings. Fuyao’s decision to inject CNY 5.8 billion (USD 804 million) into new float lines dedicated to electrified vehicle platforms illustrates the scale of the opportunity. The resulting requirement for optical clarity and electromagnetic transparency supports premium pricing, ensuring that volume growth feeds directly into revenue and margin expansion for technologically capable suppliers.

Utility-Scale Solar Build-Outs Boost Demand for Low-Iron Float Glass

Record-low levelized costs of USD 31/MWh for U.S. utility solar installations have removed subsidy dependencies, setting off a multi-gigawatt development wave that leans heavily on 2.0 mm ultra-clear sheets to maximize cell efficiency[1]Joachim Seel, “Utility-Scale Solar, 2024 Edition,” Lawrence Berkeley National Laboratory, lbl.gov. China’s acceleration in N-type module output has raised silica purity requirements and pushed specialized sand prices to USD 55 per ton, underscoring how the float glass market derives fresh value from tailored mineral supply chains. Although thinner substrates use less glass per pane, higher rejection rates and tighter tolerances mean volume shipped per installed megawatt actually climbs, magnifying tonnage demand despite the down-gauging trend.

BIPV Façade Regulations Spur Ultra-Clear Low-Iron Substrates

The European Union’s industrial carbon plan positions building-integrated photovoltaics as an instrument for meeting net-zero targets, mandating ultra-clear substrates that optimize electrical output. Yet only 1-3% of PV systems in Sweden today are integrated into envelopes, highlighting significant headroom for adoption. As architects in hot climates refine climate-responsive façade designs that reduce thermal loads without sacrificing aesthetics, demand tilts toward float sheets with both high solar transmission and selective infrared control. Each regulatory ratchet effectively cements high-clarity float glass as an indispensable input for distributed renewable generation.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile soda-ash and natural-gas prices | -0.6% | Global, with acute impact in Europe and North America | Short term (≤2 years) |

| Polymer and polycarbonate substitutes in safety glazing | -0.4% | North America and Europe core, expanding to APAC | Medium term (2-4 years) |

| EU Carbon Border Adjustment Mechanism compliance costs | -0.3% | Asia-Pacific exporters to EU, secondary impact on global pricing | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Polymer and Polycarbonate Substitutes in Safety Glazing

Automotive and architectural standards permit polycarbonate solutions that weigh 40-50% less than laminated glass while matching impact resistance. Weight-sensitive OEMs therefore experiment with polymer roofs and rear windows; however, scratch performance, UV stability, and optical distortion issues still confine usage to niche placements. Glass makers answer with thinner, lighter laminates using advanced PVB interlayers, as evidenced by Eastman’s European capacity expansion. The resulting material joust moderates the float glass market CAGR but also catalyzes innovation, widening the product envelope and raising entry barriers.

EU Carbon Border Adjustment Mechanism Compliance Costs

Beginning in 2026, importers must remit certificates reflecting embedded CO₂, eroding the historic cost edge enjoyed by Asian float lines fired by coal or fuel oil. Analyses show U.S. suppliers will pay markedly less under CBAM, improving their price parity in Europe[2]Daniel Hoenig, “Projecting CBAM Impacts,” Climate Leadership Council, clcouncil.org . Saint-Gobain and AGC have responded with a hybrid oxy-fuel/electric furnace prototype targeting 75% emission cuts. The policy reframes decarbonization as a market access fee rather than a voluntary ESG pursuit, accelerating capital rotation into low-carbon plants across the float glass market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Clear Glass Sustains Leadership Through Premium Applications

Clear sheet controlled 62.70% of the float glass market share in 2025 and will register the highest 3.79% CAGR through 2031. This dominance reflects unrivaled versatility: façade glazing, automotive windscreens, and low-iron solar covers all demand transparency levels unattainable by tinted or patterned variants. Manufacturers channel research and development budgets into purification and melt-homogeneity technologies that suppress bubble content and iron residue, securing margins that offset commodity headwinds. Tinted and patterned sheets persist as design-driven niches, yet their uptake follows cyclical architectural trends rather than structural technology shifts.

Extra-clear low-ferrous grades sit at the premium apex, powered by solar boom economics and luxury façade aesthetics. NSG’s Pilkington Mirai™ and Xinyi’s 2.0 mm glass lines exemplify the emphasis on both embodied-carbon cuts and extreme thinness. As N-type solar modules cascade through production lines, sheet rejection rates rise, paradoxically lifting clear-glass tonnage per installed gigawatt. Integrated sand quarries and real-time impurity scanners thus become critical competitive assets across the float glass market.

By Application: Solar Glass Disrupts Building-Construction Dominance

Building and construction accounted for 74.60% of float glass market size in 2025, supported by emerging-economy housing programs and Western retrofit mandates. Yet the solar glass sub-segment, propelled by an 8.01% CAGR. Grid-parity economics place ultra-clear float sheets at the core of megawatt-class PV arrays, enabling suppliers to lock in multiyear offtake contracts with module makers eager for quality consistency. Automotive demand delivers incremental tonnage via expanded glass-to-metal ratios in EV cabins, while electronic and industrial niches contribute high-margin but low-volume revenues.

Circularity initiatives further tighten application linkages. AGC’s tie-up with ROSI recycles end-of-life solar cover glass back into the float batch, trimming virgin silica usage and easing CBAM risk. As downstream users embed scope-3 scrutiny into supplier scorecards, product passports confirming recycled content and energy provenance become decisive bid factors, steering the float glass market toward vertically integrated ecosystems.

Geography Analysis

Asia-Pacific dominates the float glass market, supplying 62.65% of global output in 2025 and advancing at a 3.92% CAGR to 2031. China anchors the base with mega-scale kiln clusters, while India rides an unprecedented USD 1.5 trillion construction upcycle that absorbs large sheets for residential towers and logistics parks. Thailand’s infrastructure spend around the Eastern Economic Corridor cushions regional demand dips tied to residential slowdowns. Yet Asian exporters must navigate rising freight charges and looming CBAM levies, prompting pilot investments in hybrid furnaces and rooftop solar to reduce shipped-ton CO₂.

Europe, historically the cradle of float innovation, is now the crucible for low-carbon manufacturing. Saint-Gobain’s ORAÉ series combines high recycled content with cradle-to-cradle certification, while AGC Interpane’s upgrades in Germany and Austria elevate line efficiencies despite weak housing starts.

North America capitalizes on nearshoring dynamics and clean-energy incentives. Fuyao’s USD 400 million boost to its Illinois float facility ensures just-in-time supply for Midwest EV plants. Combined with the Inflation Reduction Act’s manufacturing tax credits, these moves shift import reliance toward domestically melted sheets, narrowing latency and carbon footprints. South America and the Middle East and Africa deliver incremental tonnage via stadium builds, desalination projects, and smart-city launches, but limited local capacity keeps per-capita consumption below mature-market norms.

Regulatory Landscape

Trade and carbon-linked compliance measures are increasingly determinative for float glass flows and pricing. In the United States, trade enforcement tightened in 2026 when the US Department of Commerce issued antidumping and countervailing duty orders covering float glass products from the Peoples Republic of China and Malaysia, effective April 6, 2026, following an affirmative material injury outcome at the US International Trade Commission. This was preceded by a February 2026 final less-than-fair-value determination for China (investigation period April 1, 2024, to September 30, 2024) and a July 2025 preliminary affirmative finding. Together, these actions raise the cost and risk of import-dependent sourcing strategies, while increasing the importance of regional capacity and qualifying domestic supply.

In Europe, environmental and product-declaration requirements are tightening around industrial emissions and building-product transparency. Flat glass manufacturing is governed by the Industrial Emissions Directive (Directive 2010/75/EU) and its best available techniques framework, and procurement is increasingly shaped by Environmental Product Declarations aligned with ISO 14025 and EN 15804 as sustainability documentation becomes a recurring bid requirement for construction products. The report scope also reflects the start of EU Carbon Border Adjustment Mechanism compliance from 2026, which shifts competitiveness toward producers that can document lower embedded CO2 and operate more efficient, lower-carbon furnace configurations.

Value Chain Analysis

The float glass value chain starts with upstream extraction and beneficiation of silica sand and carbonates, alongside procurement of soda ash, followed by batch preparation and melting in energy-intensive float furnaces, then forming on the tin bath and annealing to produce standard sheets. Downstream steps include cutting and logistics, plus secondary processing such as tempering, laminating, and applying functional coatings for automotive, building envelopes, and solar cover glass.

Because bulk density and transport costs are material constraints, silica sand and other minerals are often sourced close to float lines, while soda ash typically requires broader sourcing and remains a key cost and availability variable alongside natural gas and electricity. Midstream manufacturing is concentrated among multinational and large regional producers (including AGC, Saint-Gobain, Guardian Industries, NSG Group/Pilkington, and Sisecam). Differentiation increasingly depends on low-iron quality control, thin-gauge capability, and yield management. Distribution runs through fabricators, glazing contractors, OEM supply programs, and module/IGU value chains, where certification and documentation (for example, EPDs for construction and supplier scorecards for automotive) affect vendor qualification. Recycling stays structurally constrained versus container glass due to stringent purity requirements, but initiatives to bring qualified cullet back into the batch are gaining relevance as they reduce energy demand and support decarbonization and market-access compliance needs.

Competitive Landscape

The market is moderately fragmented. Competitive positioning hinges on process automation, sustainability roadmaps, and access to captive silica or soda-ash assets rather than sheer furnace count. Sustainability is now a price-of-entry metric. NSG’s 100% biofuel trial in the U.K. and AGC’s hydrogen-assisted melts in Belgium cut kiln CO₂ by up to 50%, winning OEM procurement points in Europe’s decarbonizing automotive supply chain. Smaller regional specialists survive by tailoring colors, patterns, or service bundles, often under OEM contract manufacturing models. As CBAM and other carbon tariffs proliferate, the premium attached to verifiable low-emission sheets will likely widen, conferring first-mover advantage to innovators and reinforcing a technology-centric pecking order within the float glass market.

Float Glass Industry Leaders

AGC Inc.

Nippon Sheet Glass Co., Ltd.

Saint-Gobain

Guardian Industries Holdings

Xinyi Glass Holdings Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is widening in low-carbon and high-transparency float products that can be verified for embodied emissions and recycled content, as carbon-linked procurement moves from voluntary to mandatory documentation across several end-use channels. The 2026 start of EU Carbon Border Adjustment Mechanism compliance turns embedded CO2 reporting into a commercial factor for exporters serving Europe, reinforcing opportunities for hybrid or electric-boosted furnace upgrades and for differentiated low-embodied-CO2 product lines such as AGC Glass Europe expanded production of Low-Carbon Planibel Clearlite at Seingbouse, France. In parallel, Environmental Product Declarations aligned with ISO 14025 and EN 15804 are increasingly used to qualify construction products, creating an opening for producers that can provide standardized product data packages across regions and applications.

Capacity and capability investments in growth geographies also point to opportunity in local-for-local supply, especially where downstream customers require consistency and fast lead times. In India, Saint-Gobain began construction in August 2025 of a new float glass line (1,000 tonnes per day) at Oragadam, Chennai, and Gujarat Guardian Limited began construction in May 2026 on a second float line and wet coating facility at Ankleshwar (adding 1,000 metric tons per day), reflecting demand for architectural and coated products that reduce building energy loads. In Turkey, Sisecam completed its TR9 flat glass line in Tarsus in March 2026 (1,200 metric tonnes per day; EUR 315 million), expanding regional supply for construction and value-added processing. For solar and automotive, opportunities concentrate on ultra-clear, thin substrates and integrated coating and lamination ecosystems, supported by ongoing moves such as NSG Groups progression of advanced coating investments in Japan and Poland and recycling linkages such as AGC's tie-up with ROSI for end-of-life solar glass feedstock.

Recent Industry Developments

- April 2026: The US Department of Commerce issued antidumping and countervailing duty orders on float glass products from the Peoples Republic of China and Malaysia, effective April 6, 2026, following an affirmative material injury determination by the US International Trade Commission. The orders reshape landed-cost economics for importers and encourage buyers to qualify alternative regional supply and domestic melting capacity. They also raise the premium on traceable cost and origin compliance across distributor and fabricator networks.

- August 2025: Saint-Gobain began construction of its 7th float glass line (1,000 tonnes per day) and a 5th mineral wool insulation line at its Oragadam, Chennai facility in India. Adding float capacity alongside insulation supports a more integrated building-envelope offering, which strengthens specification-driven sales into energy-efficient construction programs. The move also reinforces Indias role as a manufacturing hub for architectural and value-added glass.

- January 2024: Fuyao Glass approved a CNY 5.8 billion (USD 804 million) investment for two float lines in Hefei, China focused on next-generation vehicle platforms. The investment targets automotive-grade substrates where optical quality and downstream processing compatibility are critical to OEM supply. It also signals continued capital commitment toward thinner, larger-area glazing that aligns with EV design trends.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the float glass market covers standard flat glass made using the float process and supplied as clear or specialty sheets that are later cut and processed for construction, automotive glazing, and solar-related uses across major regions.

Scope exclusions: We exclude downstream fabricated glass value added, such as tempering, laminating, insulating glass unit assembly, and installed facade system labor.

Segmentation Overview

- By Product Type

- Clear

- Tinted

- Patterned

- Wired

- Extra Clear/Low Ferrous Floated Glass

- By Application

- Building and Construction

- Automotive

- Solar Glass

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Vietnam

- Thailand

- Indonesia

- Malaysia

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Nordic Countries

- Rest of Europe

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- Nigeria

- Qatar

- United Arab Emirates

- Egypt

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the initial demand map and to set practical boundaries for what should count as float glass versus later-stage processing. We relied on public sources that describe construction output, auto production, and energy build-outs, then linked those signals to glass use intensity and typical thickness mixes.

Key inputs were taken from sources such as national statistical offices and customs agencies for trade flows, the International Energy Agency for solar deployment context, the World Bank for macro indicators, and building or glazing association publications for code-driven adoption and renovation activity. We also reviewed company annual reports, investor presentations, and reputable press coverage to understand capacity announcements, furnace rebuild cycles, and pricing commentary. For cross-checking supplier footprints and patent activity (coatings and low-iron formulations), paid database subscriptions were used selectively where public disclosures were thin. The sources listed here are illustrative, and many other public and paid references were also used to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work focused on checking how volume shifts by end use and how pricing is typically quoted, converted, and adjusted for thickness, coatings, and contract terms. We spoke with a mix of manufacturers, processors, distributors, and large buyers so the model reflects real ordering patterns, not just published capacity claims. Because this is a global market, feedback was balanced across the main producing and consuming regions to confirm assumptions and close gaps left by public data.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 12% | APAC: 48% |

| Mid tier: 51% | Functional/Unit leaders: 43% | EMEA: 33% |

| Smaller Players: 17% | Managers: 45% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where construction activity, vehicle production, and solar installation trends are converted into a float-glass demand pool using practical intensity factors, then split by region using trade flows and local supply patterns. Those regional totals are checked against selective bottom-up approximations, including sampled shipment discussions with channel participants and a sanity check of capacity utilization implied by furnace nameplate output.

A few market fingerprints are treated as key inputs because they explain most of the movement year to year. These include new floor space starts and renovation share (to reflect glazing demand timing), vehicle builds by major producing countries, solar module and glass adoption momentum, import-export direction for flat glass, and average selling price logic that varies by thickness, low-iron content, and coating mix. Where direct volume or price points were missing, we filled gaps using nearest-neighbor country proxies and then revalidated the assumptions through interviews.

Forecasts were developed using scenario analysis, since energy costs, construction cycles, and solar policy can shift demand quickly and differently across regions. In each scenario, expected changes in construction pipeline, automotive output, furnace rebuild schedules, and pricing pass-through were applied before the final growth path was confirmed through expert feedback.

Data Validation & Update Cycle

Validation was done through multiple passes that compare model outputs with independent signals, including trade balances, capacity change announcements, and end-use activity trends. When a country result looked inconsistent with these signals, the drivers were revisited and, where needed, follow-up calls were made to recheck the assumption.

Before sign-off, a second analyst reviews the logic, unit conversions, and currency handling so pricing and volume do not get mixed across years. The report is refreshed annually, and interim updates are triggered when material events occur, such as major furnace shutdowns, new capacity start-ups, or sudden energy price shocks. Right before delivery, we run a final review pass so the client receives the most current view available.

Mordor Intelligence's Float Glass Market Size Compared With Other Published Estimates

Published market sizes for float glass can look far apart because different authors choose different units, pricing bases, and timing for currency conversion, then update those inputs at different speeds. Some estimates are also built around broad flat-glass boundaries, which can pull in more downstream value than a buyer expects.

In our work, the biggest drivers are how average selling prices are normalized across regions (spot versus contract indications), how volume is converted into value in the same year as the base inputs, and whether reprocessed products are counted again. The refresh cadence also matters because construction, energy, and freight shocks can change realized prices quickly, and that is why the currency timing and variance checks used in Mordor Intelligence are treated as a first-step control before totals are finalized.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 53.98 B (2026) | |

| Trade Publisher A | USD 43.00 B (2025) | Often reported as a single global value with limited detail on how volume-to-value is converted, which can understate pricing dispersion by thickness, coatings, and low-iron mix, and it may use earlier-year currency rates. |

| Industry Publisher B | USD 42.70 B (2025) | May rely on broad demand narratives without explicitly separating raw float output from downstream processed glass value add, and assumptions on ASP progression can differ when energy and soda-ash costs shift. |

The comparison mainly shows that timing and boundaries create most of the spread, rather than a single right or wrong number. By keeping the model tied to end-use demand signals, checking implied utilization, and applying a consistent price and currency year, we keep the estimate traceable to repeatable inputs that can be revisited as the market changes.

Key Questions Answered in the Report

What is the projected global demand for float glass in 2031?

The float glass market size will reach 91.18 million tons by 2031, rising from 76.86 million tons in 2026.

How fast is solar-grade float sheet demand growing?

Solar glass is expanding at an 8.01% CAGR to 2031 on the back of utility-scale installations.

Which region drives most float glass production today?

Asia-Pacific supplies 62.65% of global volume, with China and India as primary hubs.

How does CBAM affect Asian float exporters?

Starting 2026, shipments into the EU will carry carbon fees, reducing prior cost advantages and incentivizing low-carbon furnaces.

Why are automakers important for glass makers’ future orders?

Electrification and larger glazing areas lift per-vehicle glass use, while thinner, high-clarity sheets fetch premium prices.

Page last updated on: