Glass Substrate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 7.42 Billion |

| Market Size (2031) | USD 9.01 Billion |

| Growth Rate (2026 - 2031) | 3.96% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Glass Substrate Market Analysis by Mordor Intelligence

The Glass Substrate Market size was valued at USD 7.14 billion in 2025 and is estimated to grow from USD 7.42 billion in 2026 to reach USD 9.01 billion by 2031, at a CAGR of 3.96% during the forecast period (2026-2031). This healthy growth is underpinned by rising semiconductor packaging demand, accelerating adoption of glass-core interposers, and sustained volumes in display manufacturing even as legacy LCD capacity migrates to automotive and industrial panels. Glass-core technology championed by Intel and Absolics is expected to solve warpage and signal-integrity bottlenecks in next-generation AI accelerators, while ultra-thin glass gains momentum in foldable smartphones and rollable OLED televisions. At the same time, quartz substrates are carving out a premium niche in extreme-ultraviolet (EUV) photomask blanks, and plasma-assisted chemical-vapor deposition (CVD) lines are coming online to meet sub-nanometer surface demands in semiconductor fabs. Competitive dynamics, therefore, hinge on a dual strategy of cost leadership in commodity borosilicate and deep R&D in specialty grades, forcing producers to balance volume commitments with margin-rich innovation streams.

Key Report Takeaways

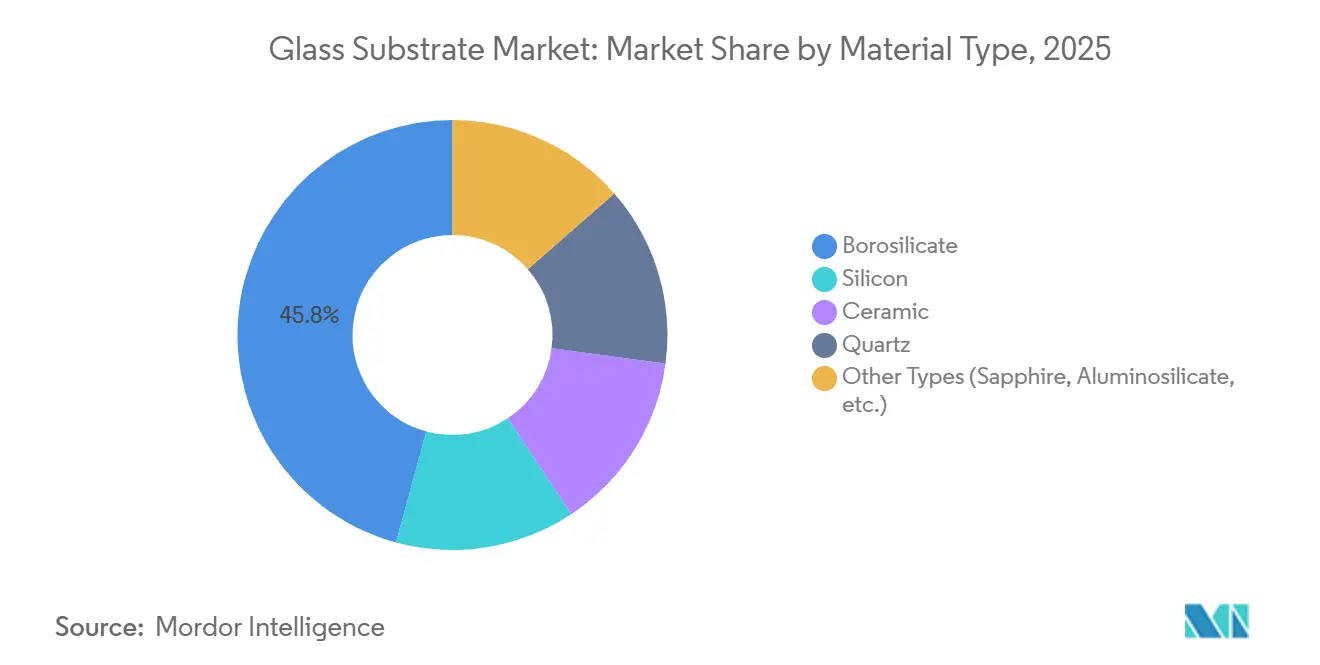

- Borosilicate glass captured 45.76% glass substrates market share in 2025, while quartz substrates are forecast to advance at a 4.41% CAGR through 2031.

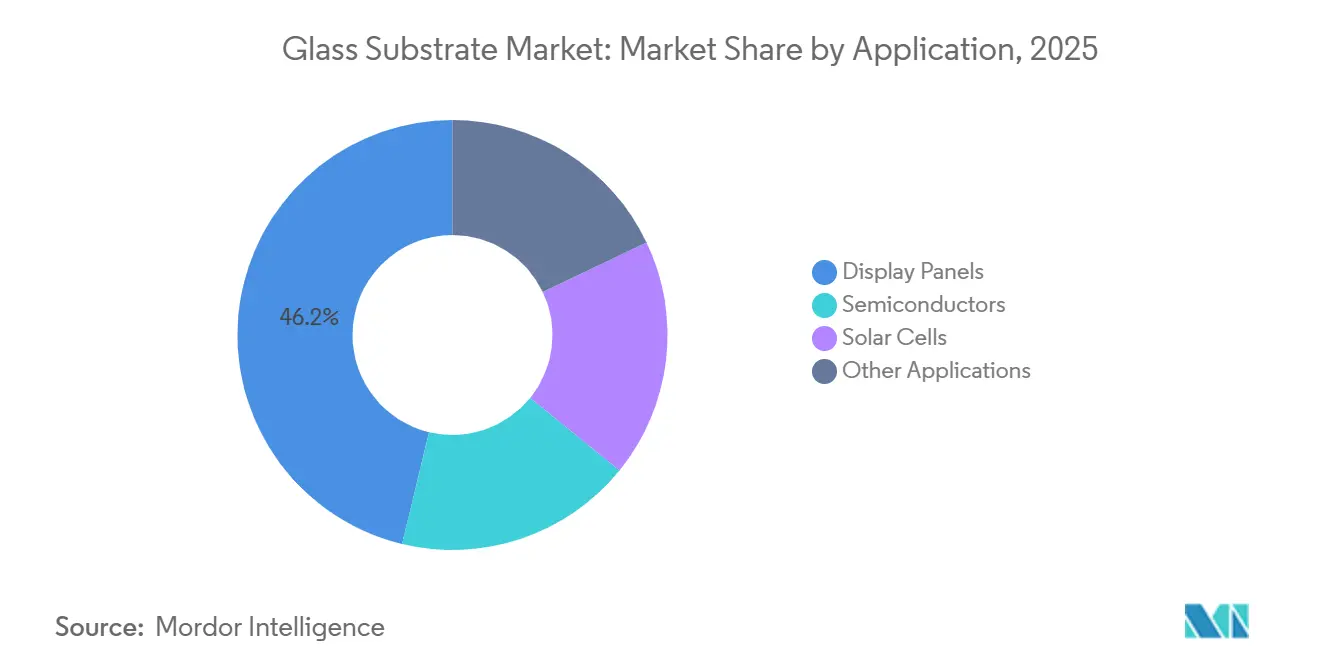

- Display Panels accounted for 46.22% of 2025 application revenue; the segment is projected to progress at a 4.44% CAGR over the forecast period.

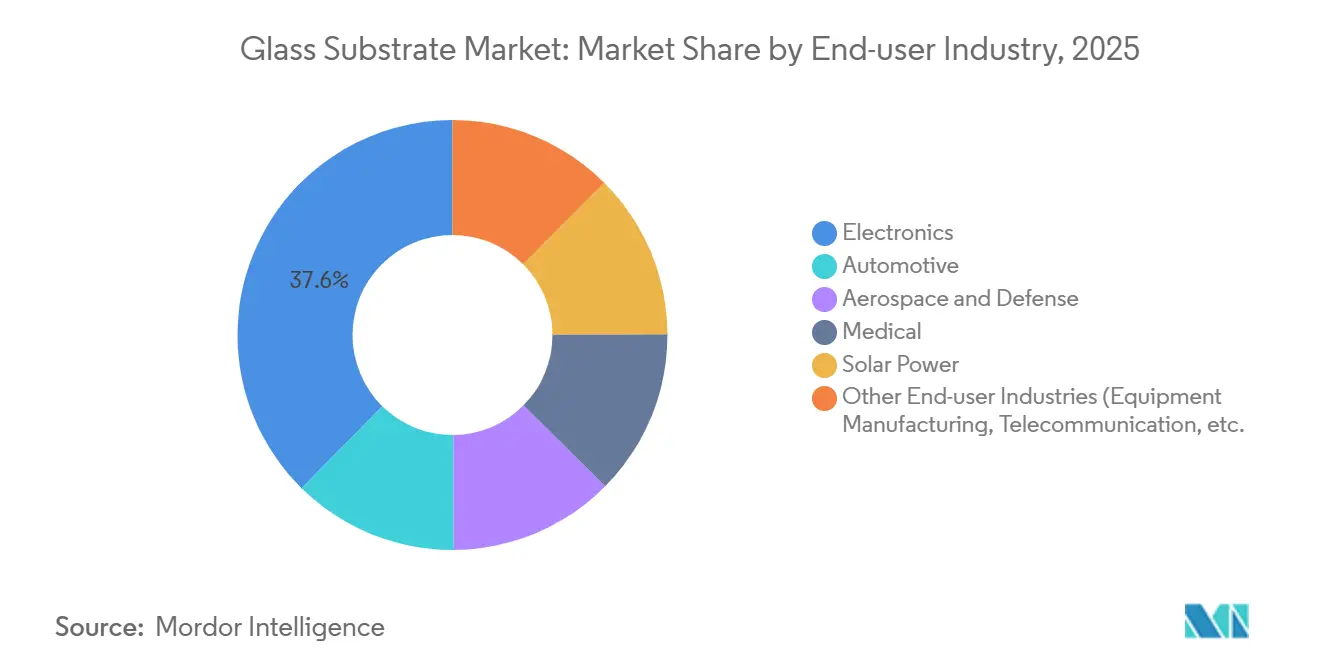

- Electronics led end-user demand with 37.62% revenue share in 2025 and is poised to expand at a 4.23% CAGR to 2031.

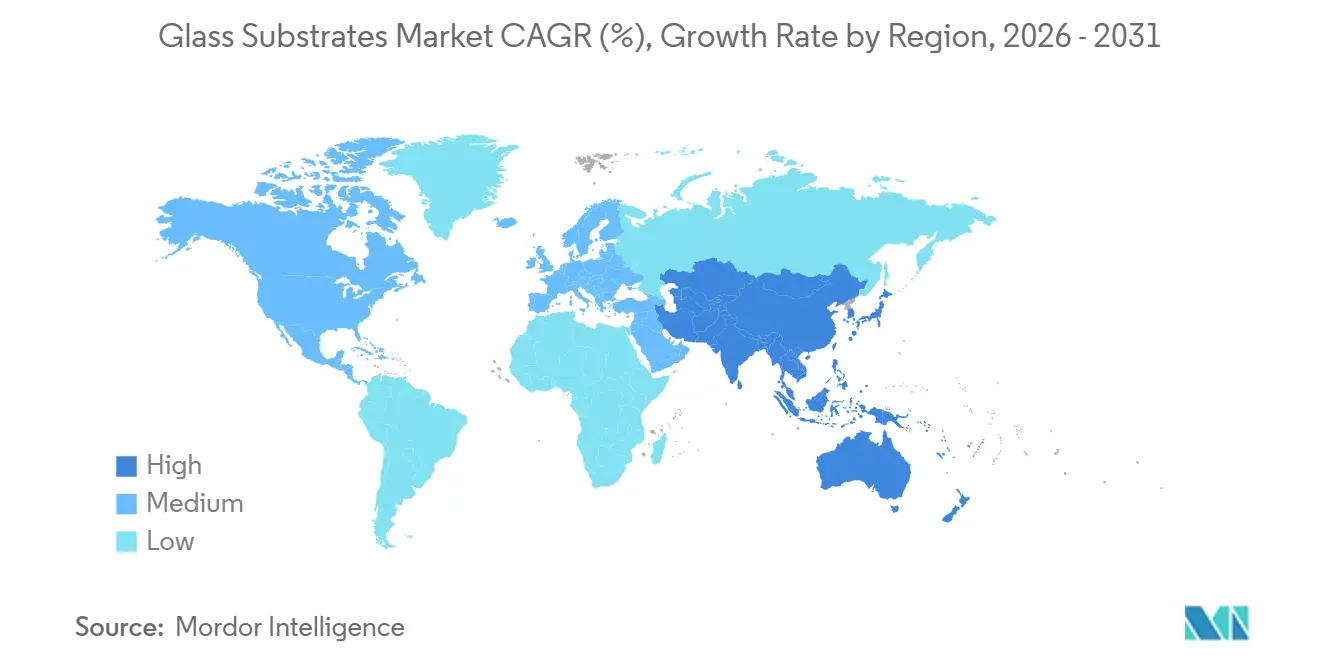

- Asia-Pacific dominated geography with a 48.82% share in 2025, whereas the region is also expected to register the highest 4.19% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Glass Substrate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing usage of LCDs in consumer electronics | +0.8% | China, South Korea, Taiwan, spill-over to North America, Europe | Medium term (2-4 years) |

| Expansion of semiconductor fabrication lines | +1.2% | Taiwan, South Korea, United States, Japan | Long term (≥ 4 years) |

| Rising demand for automotive and AR/VR displays | +0.7% | North America, Europe, China, Japan, South Korea | Medium term (2-4 years) |

| Growth of high-efficiency photovoltaic cells | +0.5% | China, India, United States, Germany | Long term (≥ 4 years) |

| Emergence of glass-core substrates in advanced packaging | +1.0% | United States, Japan, South Korea, Taiwan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Usage of LCDs in Consumer Electronics

Persistent LCD volumes in mid-range smartphones, tablets, and monitors keep the glass substrates market firmly anchored in Asia-Pacific manufacturing hubs. Large-format gaming and professional monitors are now adopting thinner, lighter substrates to enable borderless designs that cut shipping weight and curb panel breakage. The mix shift toward higher value LCD panels favors suppliers capable of precision thinning and surface treatments alongside commodity-scale output. These dual capabilities strengthen incumbent positions for vertically integrated producers that can amortize R&D across multiple applications. Display OEM roadmaps also signal incremental glass demand from automotive infotainment retrofits, where existing LCD fabs redeploy capacity toward curved cockpit clusters[1]Corning Incorporated, “Curved Mirror Solutions for HUD Systems,” corning.com.

Expansion of Semiconductor Fabrication Lines

The USD 150 billion wave of new fabs announced by Intel, Samsung, and TSMC through 2030 is reshaping the glass substrates market. Demand is ramping across three vectors: quartz photomask blanks for EUV patterning, glass-core substrates for 2.5D and 3D packages, and chemically inert inspection windows used in extreme-clean-room environments. Rapidus’s demonstration of a 600 mm × 600 mm glass panel promises 10-fold chip yield relative to silicon interposers, highlighting the area-economy edge of rectangular glass panels over round wafers. Early design wins in this ecosystem lock suppliers into long qualification cycles, rewarding those who scale capacity in tandem with foundry outputs.

Rising Demand for Automotive and AR/VR Displays

Head-up displays (HUDs) and augmented-reality (AR) headsets require glass substrates that deliver high optical clarity, scratch resistance, and thermal stability. Corning’s curved windshield mirror enables windshield-spanning AR overlays scheduled for 2026 mass-production vehicles, while glass waveguides lighten headset form factors for Meta and Apple devices. Although automotive and AR/VR volumes lag smartphone shipments, their stringent qualification requirements lengthen revenue tail lifecycles and justify premium pricing. Producers able to customize stress-relief, anti-glare coatings, and freeform geometries gain a defensible edge.

Emergence of Glass Core Substrates in Advanced Packaging

Intel’s public roadmap aligns glass cores with next-generation Xeon and AI processors, citing lower dielectric constants and superior rigidity versus silicon interposers. Absolics’ CHIPS Act grant supports the first U.S. panel-scale glass-core line, while Nippon Electric Glass’s CO2-laser-drillable vias address throughput bottlenecks. Advantages include larger panel formats, better coefficient-of-thermal-expansion (CTE) matching, and finer wiring pitch. However, tool reconfiguration from round-wafer to panel handling and metallization of through-glass vias remains an adoption speed bump, suggesting commercialization beyond pilot scale after 2027.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High manufacturing and capital costs | -0.9% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Persistent supply-chain volatility and energy price spikes | -0.6% | Europe, North America, secondary effects in APAC | Short term (≤ 2 years) |

| Stringent environmental regulations on boron emissions | -0.3% | European Union, California | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Manufacturing and Capital Costs

Greenfield float or fusion-draw lines cost USD 200 million-USD 500 million, with melting furnaces consuming up to 40% of initial outlays. SCHOTT’s EUR 40 million electric-melting retrofit at Mainz highlights the capex premium of decarbonization, yet integrated players deem it essential to hedge energy volatility. Specialty paths—ultra-thin glass, quartz blanks—stack extra investments in chemical strengthening, polishing, and Class 1 clean rooms, pushing fully loaded project costs above USD 300 million. This barrier consolidates the glass substrates market around incumbents capable of cross-subsidizing long paybacks with broad product portfolios.

Persistent Supply-Chain Volatility and Energy Price Spikes

Natural-gas and electricity costs tripled in parts of Europe during 2024-2025. Glass melting’s energy intensity, at 4-6 MJ per kilogram, squeezed margins when supply contracts fixed selling prices. High-purity quartz sand used in EUV mask blanks and bifacial PV modules also tightened as semiconductor and solar demand outpaced mine expansions. Route diversions around the Red Sea lengthened transit times, forcing OEMs to raise buffer stocks. Large suppliers responded by hedging power, diversifying melting fuels to hydrogen and electricity, and locking in multiyear feedstock contracts, yet smaller firms remain exposed to spot-price swings that can erase quarterly profits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Borosilicate Retains Volume Lead, Quartz Accelerates in EUV

Borosilicate glass accounted for 45.76% of the glass substrates market size in 2025 and continues to underpin TFT-LCD production due to its thermal stability and cost advantage. Its share growth is slowing as legacy LCD capacity pivots toward automotive and industrial displays, yet the sheer throughput of Gen 8.5 and Gen 10.5 fabs keeps borosilicate volumes high[2]AGC Inc., “Borosilicate Glass Substrates for TFT-LCD,” agc.com. Suppliers are adding precision thinning and surface-treatment lines to command better margins, particularly for curved infotainment and larger gaming monitors. Meanwhile, quartz substrates are projected to post a 4.41% CAGR through 2031 on the back of EUV lithography’s relentless scaling below 3 nm. Near-zero CTE and sub-ppb metallic purity push quartz unit pricing multiples higher than borosilicate, insulating margins from commodity swings.

Quartz’s rising demand transforms supply chains: HOYA and Shin-Etsu’s synthetic-quartz duopoly now invests in additional CVD reactors, while semiconductor OEMs co-fund capacity to avoid EUV blank shortages. The glass substrates market, therefore, bifurcates into high-volume borosilicate workshops chasing cost efficiencies and low-volume quartz operations emphasizing defect-free quality. Both materials remain indispensable, but profit pools skew toward quartz and emerging glass-ceramic hybrids for foldables that blend flexibility with scratch resistance.

By Application: Flat Panels Remain Revenue Core, Packaging Substrates Disrupt Status Quo

Display Panels secured 46.22% of 2025 application revenue in the glass substrates market and are forecast to rise at a 4.44% CAGR on the strength of OLED and micro-LED adoption. While LCD panel prices face cyclical erosion, OLED substrates command 2-3× premiums for sub-nanometer surfaces and alkali-free compositions that prevent pixel degradation. The delta in unit pricing partially offsets slowing square-meter growth in traditional LCD lines.

Semiconductor packaging and interposers are the disruptive frontier. Glass-core substrates enable larger package areas and thinner wiring than silicon or organic laminates, positioning the technology for AI accelerators and data-center chiplets. Early pilot lines in the United States and Japan suggest a commercial ramp after 2027. Photomask blanks for EUV remain a niche yet strategic application: every sub-3 nm node requires thousands of defect-free quartz blanks that cost more than USD 30,000 each. Solar cells, MEMS, and biosensor platforms round out demand, benefiting from glass’s chemical durability, optical clarity, and dimensional stability.

By End-User Industry: Electronics Dominates Yet Specialty Verticals Gain Traction

Electronics represented a commanding 37.62% share of the glass substrates market size in 2025 and is set to advance at a 4.23% CAGR to 2031. Mid-range smartphones, tablets, and TVs still require vast TFT-LCD glass tonnage, but premium tiers migrate to OLED and ultra-thin glass that fetch higher per-square-meter prices. Foldable handsets rely on 30-50 µm glass strengthened for 200,000-plus bend cycles, expanding revenue per unit despite lower area consumption.

Automotive and medical are also the fastest-expanding verticals, each demanding specialty formulations. Curved head-up-display mirrors and augmented-reality windshields use chemically tempered borosilicate or aluminosilicate for impact resistance. Semiconductor customers transition from silicon interposers to glass cores, accelerating long-lead substrate design-ins. Biosensors and microfluidics deploy optically clear, chemically inert glass wafers for diagnostic consumables, while solar manufacturers specify low-iron sheets for bifacial photovoltaic panels. A balanced portfolio spanning commodity and specialty verticals is increasingly critical to meet divergent performance and cost expectations.

Geography Analysis

Asia-Pacific dominated the glass substrates market with a 48.82% share in 2025 and is projected to post the highest 4.19% CAGR through 2031. China’s BOE, CSOT, and HKC run the bulk of global TFT-LCD capacity, generating massive demand for borosilicate glass. Japan maintains control of the synthetic-quartz supply for EUV mask blanks, while South Korea spearheads ultra-thin glass and foldable OLED innovations. Taiwan’s foundry cluster consumes quartz blanks and glass carriers, with TSMC’s expansion in Arizona and Kumamoto creating secondary hubs outside the region. India’s Vedanta-AvanStrate investment signals an emerging domestic substrate base aimed at local smartphone and TV assembly.

North America market growth is buoyed by semiconductor packaging and automotive display projects rather than commodity LCD output. Intel’s Ohio and Arizona fabs will validate panel-scale glass-core substrates, and Absolics’ CHIPS Act-supported plant anchors the first U.S. manufacturing footprint in this field. Corning’s New York and North Carolina sites supply Gorilla Glass, UTG, and precision optics to regional electronics and vehicle OEMs. Automotive makers in the United States, Canada, and Mexico are integrating windshield-wide HUDs into 2026-2027 models, intensifying demand for curved glass mirrors and holographic laminates.

The European glass substrates demand is anchored by significant consumption in Germany, France, and the United Kingdom. SCHOTT’s electric-melting retrofit showcases Europe’s decarbonization push, while its 2024 acquisition of quartz-glass specialist QSIL strengthens strategic exposure to EUV lithography. Automotive OEMs such as BMW and Mercedes-Benz deploy AR windshields that rely on ZEISS and Panasonic optics laminated in high-clarity glass. Elevated energy costs and tighter emission norms pressure commodity borosilicate margins, driving European producers toward high-margin specialty segments and energy-efficient melting technologies.

South America and the Middle East & Africa are witnessing a rising demand for glass substrates, mostly float-glass for construction and autoglass, with limited exposure to semiconductor or advanced display markets.

Competitive Landscape

The glass substrates market is moderately consolidated, with the top five suppliers, including Corning and SCHOTT, holding significant market share. Commodity TFT-LCD glass is fragmenting as Chinese panel makers vertically integrate, illustrated by Vedanta’s USD 500 million capacity build-out in India. White-space opportunities cluster around glass-core substrates for AI accelerators. Intel’s roadmap and Absolics’ CHIPS Act funding validate demand but leave metallization and panel-handling challenges unresolved. Technology leadership, rather than scale alone, is emerging as the decisive competitive weapon as applications pivot from commodity displays to high-performance computing and foldable form factors.

Glass Substrate Industry Leaders

Corning Incorporated

AGC Inc.

Nippon Electric Glass Co., Ltd.

SCHOTT AG

HOYA Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: SCHOTT completed the acquisition of QSIL, expanding its high-purity quartz glass portfolio for EUV lithography and fiber optics.

- June 2024: Nippon Electric Glass introduced GC Core, a CO₂-laser-drillable glass-ceramic substrate tailored for advanced semiconductor packages.

- May 2024: Corning secured a USD 32 million CHIPS Act grant to enlarge U.S. capacity for semiconductor packaging substrates and EUV photomask blanks.

Global Glass Substrate Market Report Scope

Glass substrates, known for their ultra-smooth and thin structure, are vital for technologies like LCD displays, semiconductors, and solar panels. They offer superior flatness, thermal stability, and electrical properties, enabling high-performance electronics and advancements in next-generation devices.

The glass substrate market is segmented by material type, application, end-user industry, and geography. By material type, the market is segmented into borosilicate, silicon, ceramic, quartz, and other types (sapphire, aluminosilicate, etc.). By application, the market is segmented into display panels, semiconductors, and other Applications (MEMS devices, etc.). By end-user industry, the market is segmented into electronics, automotive, aerospace and defense, medical, solar power, and other end-user industries (telecommunication, etc.). The report also covers the market size and forecasts for glass substrates in 20 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Borosilicate |

| Silicon |

| Ceramic |

| Quartz |

| Other Types (Sapphire, Aluminosilicate, etc.) |

| Display Panels |

| Semiconductors |

| Solar Cells |

| Other Applications |

| Electronics |

| Automotive |

| Aerospace and Defense |

| Medical |

| Solar Power |

| Other End-user Industries (Equipment Manufacturing, Telecommunication, etc.) |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle-East and Africa |

| By Material Type | Borosilicate | |

| Silicon | ||

| Ceramic | ||

| Quartz | ||

| Other Types (Sapphire, Aluminosilicate, etc.) | ||

| By Application | Display Panels | |

| Semiconductors | ||

| Solar Cells | ||

| Other Applications | ||

| By End-user Industry | Electronics | |

| Automotive | ||

| Aerospace and Defense | ||

| Medical | ||

| Solar Power | ||

| Other End-user Industries (Equipment Manufacturing, Telecommunication, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| South Korea | ||

| India | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the glass substrates market by 2031?

The glass substrates market is forecast to reach USD 9.01 billion by 2031, reflecting a 3.96% CAGR over 2026-2031.

Which material type currently leads in market share?

Borosilicate glass held a 45.76% share in 2025, driven by its cost-effective use in TFT-LCD panels.

Why are glass-core substrates gaining attention in semiconductor packaging?

Glass cores offer lower dielectric constants, better CTE matching, and larger panel formats than silicon interposers, enabling higher-performance AI accelerators.

Which region commands the largest share of glass substrate demand?

Asia-Pacific dominated with 48.82% share in 2025 and is projected to grow fastest to 2031.

How do energy costs affect glass substrate producers?

Melting furnaces are energy-intensive, and recent natural-gas price spikes in Europe have squeezed margins, prompting investments in electric and hydrogen melting technologies.

Page last updated on: