Low Iron Glass Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

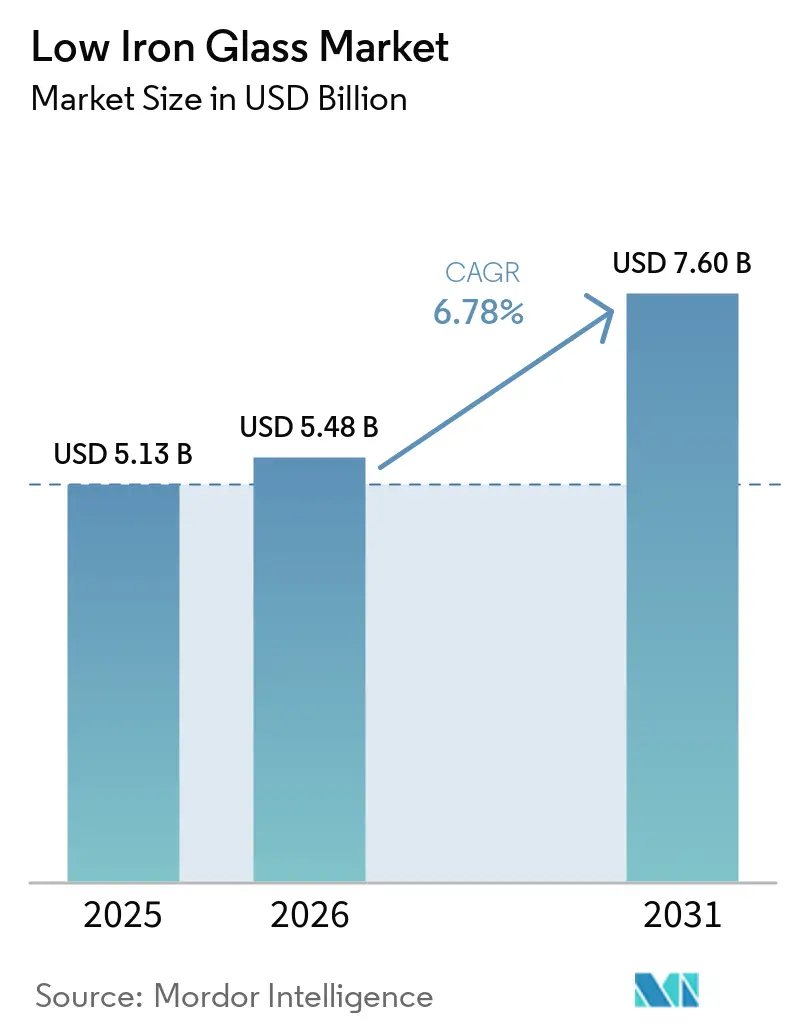

| Market Size (2026) | USD 5.48 Billion |

| Market Size (2031) | USD 7.60 Billion |

| Growth Rate (2026 - 2031) | 6.78% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Low Iron Glass Market Analysis by Mordor Intelligence

The low iron glass market size is projected to be USD 5.13 billion in 2025, USD 5.48 billion in 2026, and reach USD 7.60 billion by 2031, growing at a CAGR of 6.78% from 2026 to 2031. Demand is shifting toward precision substrates that support next-generation photovoltaic modules, electrochromic facades, and high-resolution display optics, as specifiers move beyond standard float glass. Clear low-iron glass formulations with coated variants, such as anti-reflective, low-emissivity (Low-E), and transparent conductive oxide (TCO), are driving the low-iron glass market, fueled by the expansion of building-integrated photovoltaics (BIPV) and smart-building platforms. The Asia-Pacific region leads the market, supported by China’s significant share of global photovoltaic-glass production capacity. Meanwhile, North America is increasing capacity additions, supported by the United States Inflation Reduction Act. However, challenges such as tight silica-sand supply, carbon-pricing exposure, and the cost premium compared to standard float glass are tempering growth. Vertical integration and recycling initiatives are helping to reduce cost disparities and support decarbonization efforts.

Key Report Takeaways

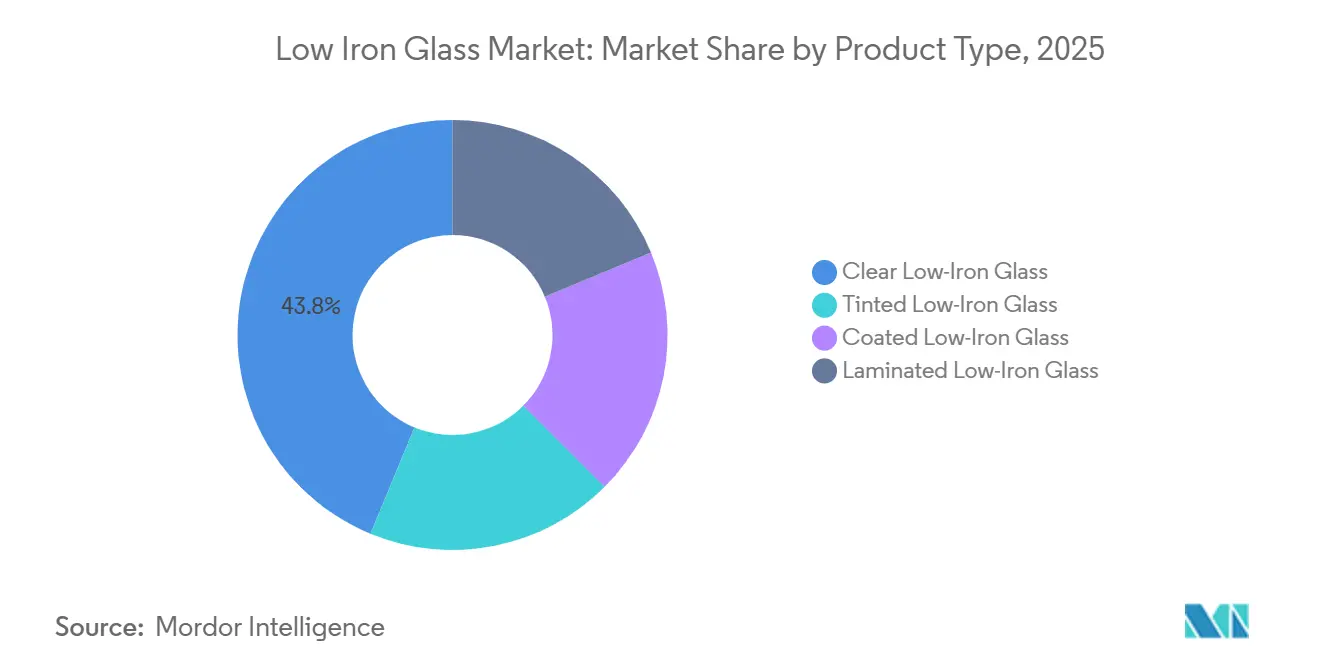

- By product type, clear low-iron glass led with 43.78% of 2025 revenue, while coated variants are projected to expand at a 7.38% CAGR through 2031.

- By application, architectural and building facades held 35.83% of the 2025 value and are advancing at a 7.39% CAGR through 2031.

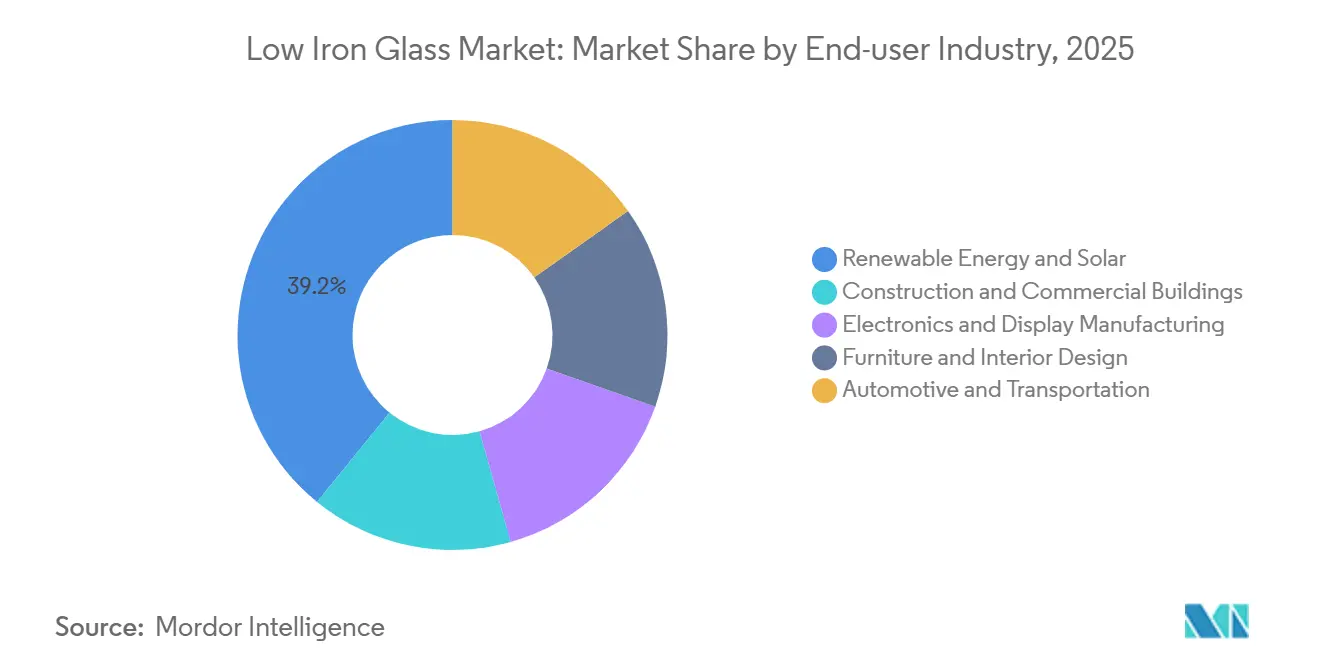

- By end-user industry, renewable energy and solar commanded 39.15% of 2025 demand and will maintain the fastest 7.51% CAGR to 2031.

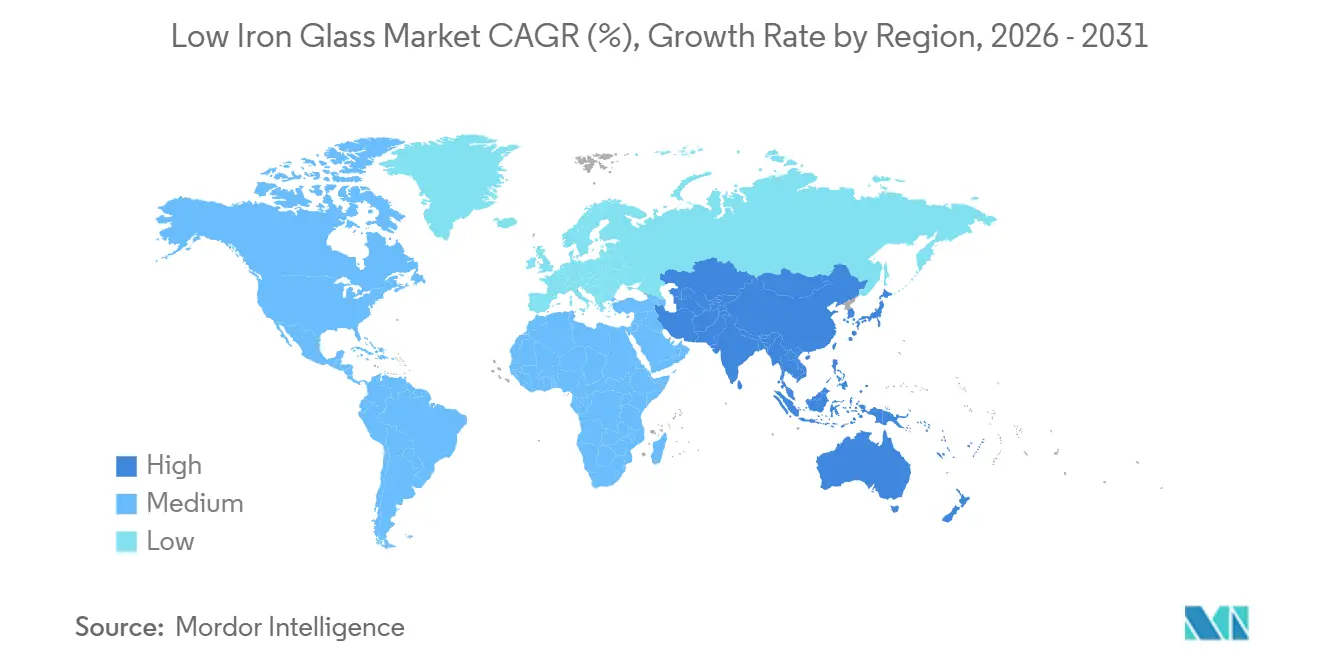

- By geography, Asia-Pacific captured the highest low-iron glass market share at 48.02% in 2025 and is forecast to expand at a 7.32% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Low Iron Glass Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Superior clarity and light-transmission in architectural glazing | +1.8% | Global, with early adoption in North America, Western Europe, and Gulf Cooperation Council markets | Medium term (2–4 years) |

| Growing adoption in solar PV and BIPV modules | +2.1% | APAC core (China, India, Southeast Asia), spillover to the Middle East and North Africa | Long term (≥4 years) |

| Integration with electrochromic and smart-facade systems | +0.9% | North America and the EU, pilot deployments in Singapore and the UAE | Long term (≥4 years) |

| Emerging demand from high-resolution display and AR/VR cover glass | +0.7% | Global, concentrated in South Korea, Japan, Taiwan, and California | Medium term (2–4 years) |

| Domestic content mandates fueling regional solar-glass manufacturing | +1.5% | United States, India, and select Middle Eastern economies with local-content policies | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Superior Clarity and Light Transmission in Architectural Glazing

Developers are specifying visible-light transmission above 91% to meet Leadership in Energy and Environmental Design (LEED) version 5 and Building Research Establishment Environmental Assessment Method (BREEAM) 2024 daylighting standards, driving demand in the low-iron glass market. For example, the 62-story 8 Bishopsgate tower in London utilized Sedak isopure low-iron glass units, achieving 72% light transmission and a U-value of 0.7 W/m²-K, which reduced annual heating, ventilation, and air conditioning (HVAC) costs by 18%[1]Sedak GmbH, “8 Bishopsgate,” sedak.com. Similarly, mid-rise retrofits are adopting low-iron glass; Vitro’s Solarban Acuity line offers 73% transmission and a 0.23 solar heat-gain coefficient, qualifying projects in North America for utility rebates. AGC Inc. Clearvision glazing, used in The Jack building in Seattle, achieved 68% transmission and a 0.28 heat-gain coefficient, demonstrating how ultra-clear substrates enhance occupant comfort. As green building codes become stricter, architects are increasingly incorporating low-iron glass in curtain walls, skylights, and atria, further driving global demand.

Growing Adoption in Solar PV and BIPV Modules

Bifacial and tandem perovskite-silicon solar cells require front-glass transmittance of greater than or equal to 91.5%, which standard soda-lime float glass cannot achieve, solidifying the role of low-iron glass in renewable energy applications. PURE Solar’s 25% efficient BIPV panel, launched in 2024, demonstrated a 3-4 percentage-point yield improvement using low-iron substrates. Fraunhofer Institute for Solar Energy Systems (ISE)’s MorphoColor coatings maintain 90-96% of black-cell efficiency on colored low-iron glass, proving that aesthetics do not compromise performance. In 2025, China produced 32.741 million tons of photovoltaic glass and has since imposed restrictions on new kilns unless they upgrade to low-iron formulations. Meanwhile, India’s five-year anti-dumping duties on solar glass have accelerated Borosil Renewables’ expansion to 600 tons per day, highlighting how policy measures are bolstering domestic production capacity.

Integration with Electrochromic and Smart-Facade Systems

Electrochromic glazing combines tungsten-trioxide or polymer-dispersed liquid-crystal films with low-iron glass substrates to optimize dynamic range. The European Union (EU)-funded Switch2save project achieved 5-70% transmission tunability and reduced cooling loads by 32% in Mediterranean pilot projects. Researchers in Barcelona demonstrated that tungsten trioxide (WO₃) nanosheet devices on low-iron glass retained 92% of their performance after 10,000 cycles[2]Institute of Materials Science of Barcelona, “WO₃ Nanosheet Electrochromics,” icmab.es. Guardian’s planned expansion in Saudi Arabia will supply UltraClear low-iron glass for electrochromic units by 2028. However, adhesion challenges remain, as sputtered films require interfacial layers to endure thermal cycling in façades. Manufacturers are investing in surface-energy engineering to meet the 20-year warranty requirements.

Emerging Demand from High-Resolution Display and AR/VR Cover Glass

High-resolution displays and AR/VR applications, such as waveguides and holographic heads-up displays (HUDs), demand refractive indices of greater than or equal to 1.7, thickness tolerances of ±0.05 mm, and light transmission of greater than or equal to 92%, all of which are met by low-iron glass. Corning’s high-index glass, launched in 2024, achieves 93% transmission and enables 50° diagonal fields of view. Ohara’s S-LAH99W optical glass, introduced in 2025, offers low birefringence, addressing chromatic aberration in compact AR optics. AGC Automotive’s P-polarized HUD windshield, which entered production in 2025, reduces ghosting to below 0.3 mm using low-iron substrates. Additionally, a 2025 alliance between Hyundai Mobis, ZEISS, tesa, and Saint-Gobain Sekurit aims to standardize haze levels below 0.8% on low-iron laminates for 10,000-nit holographic windshield displays by 2029.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher production cost vs. standard float glass | -0.9% | Global, most acute in price-sensitive residential and automotive segments | Short term (≤2 years) |

| Volatile high-purity silica-sand supply and pricing | -0.6% | Global, concentrated risk in Asia-Pacific and North America sourcing from Vietnam, Australia, and U.S. deposits | Medium term (2–4 years) |

| Limited specialty-glass recycling infrastructure | -0.4% | Europe and North America have minimal impact in the Asia-Pacific, where virgin feedstock dominates | Long term (≥4 years) |

| Energy-intensity exposure to carbon pricing schemes | -0.7% | EU27, UK, and jurisdictions with active carbon markets; emerging risk in California and select Canadian provinces | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Higher Production Cost Versus Standard Float Glass

Low-iron glass units are priced 25-40% higher than standard float glass due to the use of sub-60 parts per million (ppm) iron silica, extended melting cycles, and stricter composition controls. This price premium limits the adoption of low-iron glass in cost-sensitive fenestration applications. For example, Taiwan Glass reported a TWD 960 million (USD 30.21 million) loss in 2025 and shifted its focus to electronic-grade fiberglass cloth to address declining flat-glass margins. Pilkington Optiwhite, used in applications such as museum cases and aquariums, is priced at USD 120 per square meter (m²) in small quantities, compared to USD 50 per m² for standard float glass, restricting its use to projects requiring high clarity. Additionally, tempering and laminating processes for low-iron glass require recalibrated furnace schedules due to reduced solar absorption, which increases processing costs by 10-15%.

Volatile High-Purity Silica-Sand Supply and Pricing

High-purity silica reserves are concentrated in regions such as Vietnam, Western Australia, and select areas in the United States, making producers vulnerable to supply disruptions. Hue Premium Silica plans to increase its output to 880,000 tons per year by 2025, but it depends on imported European equipment, which is subject to export-control risks. To address feedstock uncertainties, Xinyi Glass Holdings Limited has invested USD 700 million in an integrated silica processing complex in Egypt with a capacity of 1.1 million tons per year. Meanwhile, Canadian Premium Sands suspended its twin projects in Canada and the United States in 2025, citing silica sand price fluctuations of 30-50% over an 18-month period. Manufacturers in the low-iron glass industry now maintain 90-120 days of inventory, which places additional strain on the working capital of smaller fabricators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Coated Variants Gain Momentum

Coated low-iron glass is expected to grow at a CAGR of 7.38% through 2031, surpassing the growth of clear formulations, which accounted for 43.78% of revenue in 2025. Anti-reflective (AR) and transparent conductive oxide (TCO) coatings improve module output by 2-3 percentage points. The Institute of Photonic Sciences (ICFO) and Corning's lithography-free AR process achieved transmittance levels below 99% and entered pilot production in 2024. Laminated products are used in heads-up displays (HUDs) and augmented reality (AR) waveguides, with Eastman's Saflex Horizon Vision interlayer achieving ghost-image separations of less than 0.3 millimeters when combined with low-iron substrates. Tinted glass has limited adoption due to reduced transmission with deeper colors. However, MorphoColor films on low-iron glass maintained 90-96% of black-cell efficiency, offering aesthetic options for façade applications. Clear glass continues to dominate cost-sensitive fenestration applications but is losing market share as coated glass narrows price gaps, encouraging substitution within the low-iron glass market.

Research and development efforts are focused on nanostructured coatings. Chinese manufacturers have commercialized silicon dioxide (SiO₂) sol-gel films that deliver 94-96% transmission at premiums of less than 15% compared to uncoated substrates, driving adoption in utility-scale solar applications. Roll-to-roll ultraviolet (UV) nanoimprint moth-eye structures, which promise 0.1% reflectance and 94% transmission, could gain adoption if production yields exceed 95% by 2028. These technological advancements enhance value propositions for end-users and support manufacturers in maintaining profit margins.

By Application: Architectural Facades Drive Upside

Architectural and building facades accounted for 35.83% of projected 2025 revenue and are expected to sustain a 7.39% CAGR through 2031, driven by the adoption of mid-rise retrofits alongside trophy-tower projects. Developments such as The Jack and 8 Bishopsgate demonstrate the energy-saving benefits, boosting the adoption of low iron glass in curtain walls, double-skin systems, and skylights. Leadership in Energy and Environmental Design (LEED) version 5 credits encourage visible light transmission exceeding 91%, while city-level daylighting mandates in locations like New York and London further drive demand.

Solar photovoltaic (PV) and building-integrated photovoltaics (BIPV) represent the second-largest application segment, supported by the increasing use of bifacial modules and perovskite-silicon tandem technologies. Display glass is gaining traction due to advancements in augmented reality/virtual reality (AR/VR) and automotive head-up displays (HUDs), with Corning’s high-index product pipeline addressing evolving specifications. The furniture and interior segments utilize ultra-clear tempered glass for premium showcases, though price sensitivity limits broader adoption. Additional demand comes from aquarium viewing panels and horticulture lighting enclosures, which benefit from superior color fidelity and high solar transmission.

By End-User Industry: Renewable Energy Sets the Pace

Renewable energy accounted for 39.15% of the total tons in 2025 and is expected to drive future growth with a projected CAGR of 7.51%, supported by advancements in light-sensitive module architectures. In 2025, China operated 102 kilns and 457 solar-glass production lines, achieving a scale unmatched globally. The market share of low-iron glass in renewable energy is anticipated to increase as tandem-cell technologies are rolled out more widely. The construction industry also contributes to demand, sourcing premium glazing materials to comply with net-zero mandates. In the electronics sector, Original Equipment Manufacturers (OEMs) purchase low-iron substrates for augmented reality (AR) optics and high-density monitors, although aluminosilicate cover glass remains a competitor in the smartphone market. Automotive Original Equipment Manufacturers (OEMs) use low-iron glass for windshields to enhance head-up display (HUD) clarity, with prototype holographic displays potentially driving higher volumes after commercialization post-2029. Meanwhile, furniture and retail fixtures represent a niche market, benefiting from the growing trend of luxury renovations.

Geography Analysis

Asia-Pacific is expected to hold 48.02% market value in 2025, with a CAGR of 7.32%, maintaining its position in the low iron glass market. China is upgrading kilns to low-iron formulations under capacity-swap regulations, while India’s anti-dumping duties are driving expansions by Borosil and Vishakha. Indonesia’s Batang free-trade zone has attracted investments from Xinyi and KCC, exceeding USD 11.8 billion, establishing a regional export hub. Japan and South Korea are focusing on coated and display-grade innovations to support augmented reality (AR) and organic light-emitting diode (OLED) optics applications.

North America is advancing reshoring efforts. NSG’s Ohio plant and Corning’s USD 315 million Canton extension are supporting First Solar and extreme ultraviolet (EUV) lithography supply chains. Fuyao’s USD 400 million Illinois project and Solarcycle’s recycling facility in Georgia are strengthening circular supply chains. Mexico is leveraging the United States-Mexico-Canada Agreement (USMCA) access, with Vitro’s partnership program encouraging the co-development of functional glazing. However, data from commercial research firms has been excluded to maintain source integrity.

Europe is addressing high energy tariffs and European Union Emissions Trading System (ETS) Phase 4 carbon costs, prompting glassmakers to explore hybrid furnace technologies. AGC and Saint-Gobain’s Volta pilot project in the Czech Republic aims to test a 50% electric and 50% oxyfuel melting process by 2028. Şişecam has invested USD 389 million across Turkey, Italy, and Bulgaria, while NSG’s new coating line in Poland, set to launch in 2027, will cater to automotive and architectural markets. Recycling remains a challenge, with only 5% of construction flat glass being returned as furnace-ready cullet. However, the Netherlands achieves a 75% collection rate, highlighting a significant disparity and a strategic gap in the low-iron glass industry. The Middle East is increasing primary production capacity. Xinyi’s USD 386 million Saudi Arabia line and Guardian’s coater-plus-float expansion are expected to supply Gulf electrochromic and building-integrated photovoltaic (BIPV) projects by 2028. In South America, while the market remains smaller, opportunities are emerging as Brazil and Chile introduce solar-content requirements.

Competitive Landscape

The low-iron glass market is moderately fragmented. European and North American processors focus on coated, laminated, and small-batch architectural glass, benefiting from their proximity to designers. Examples of vertical integration strategies include Xinyi Glass Holdings Limited’s complex in Egypt and Hue Premium Silica’s upgraded facility in Vietnam, both aimed at securing high-purity sand supplies. Additionally, the 2025 alliance between Hyundai Mobis, Carl Zeiss AG (ZEISS), tesa SE, and Saint-Gobain Sekurit highlights cross-value-chain collaborations targeting holographic displays with brightness exceeding 10,000 nits.

Technological differentiation is becoming more evident. The Institute of Photonic Sciences (ICFO) and Corning Incorporated have introduced 99%-transmittance augmented reality (AR) glass, currently in pilot production; successful scaling could impact existing AR-film providers. AGC Inc. and Saint-Gobain are working on low-carbon furnaces to meet European Union Emissions Trading System (EU ETS) requirements, while smaller firms face challenges due to high capital expenditure demands. Market consolidation is also underway, with Apollo Global Management’s proposed USD 3.7 billion acquisition of NSG Group expected to create a vertically integrated western leader, contrasting with AGC’s divestiture of its North American operations to Cardinal Glass Industries for USD 450 million. Meanwhile, start-ups developing sol-gel coatings with sub-15% price premiums are expanding cost-competitive supply options.

Low Iron Glass Industry Leaders

Saint-Gobain Glass

Flat Glass Group Co., Ltd.

Xinyi Glass Holdings Limited

AGC Inc.

borosilrenewables

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Corning Incorporated and Meta Platforms, Inc. commenced a USD 6 billion multiyear initiative to enhance optical cable production capacity in Hickory, North Carolina. This expansion is expected to support the growing demand for advanced materials, including low-iron glass, which is critical for high-performance optical applications. The project aligns with the increasing need for a reliable and efficient communication infrastructure.

- January 2025: Corning has committed up to USD 315 million to expand its high-purity fused silica production capacity in Canton, New York. High-purity fused silica is a critical material used in the manufacturing of low-iron glass, which is essential for applications requiring high optical clarity and minimal impurities. This investment aims to meet the growing demand for low-iron glass in industries such as solar energy and advanced optics.

Global Low Iron Glass Market Report Scope

Low-iron glass is a type of glass with high transparency, achieved by reducing the iron content in the silica mixture. Unlike standard glass, which has a green tint, particularly on edges or thicker panes, low-iron glass minimizes this coloration, providing enhanced light transmittance and a clear, neutral appearance.

The low-iron glass market is segmented by product type, application, end-user industry, and geography. By product type, the market is segmented into clear low-iron glass, tinted low-iron glass, coated low-iron glass, and laminated low-iron glass. By application, the market is segmented into architectural and building façades, solar PV modules and BIPV, display glass (TV, monitor, smartphone, AR/VR), furniture and interior decoration, automotive optical glass, and aquarium and horticulture lighting. By end-user industry, the market is segmented into renewable energy and solar, construction and commercial buildings, electronics and display manufacturing, furniture and interior design, and automotive and transportation. The report also covers the market size and forecasts for low-iron glass in 18 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Clear Low-Iron Glass |

| Tinted Low-Iron Glass |

| Coated Low-Iron Glass |

| Laminated Low-Iron Glass |

| Architectural and Building Façades |

| Solar PV Modules and BIPV |

| Display Glass (TV, Monitor, Smartphone, AR/VR) |

| Furniture and Interior Decoration |

| Automotive Optical Glass |

| Aquarium and Horticulture Lighting |

| Renewable Energy and Solar |

| Construction and Commercial Buildings |

| Electronics and Display Manufacturing |

| Furniture and Interior Design |

| Automotive and Transportation |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordic Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Clear Low-Iron Glass | |

| Tinted Low-Iron Glass | ||

| Coated Low-Iron Glass | ||

| Laminated Low-Iron Glass | ||

| By Application | Architectural and Building Façades | |

| Solar PV Modules and BIPV | ||

| Display Glass (TV, Monitor, Smartphone, AR/VR) | ||

| Furniture and Interior Decoration | ||

| Automotive Optical Glass | ||

| Aquarium and Horticulture Lighting | ||

| By End-user Industry | Renewable Energy and Solar | |

| Construction and Commercial Buildings | ||

| Electronics and Display Manufacturing | ||

| Furniture and Interior Design | ||

| Automotive and Transportation | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Nordic Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is current market size of Low Iron Glass Market?

The low iron glass market size is projected to be USD 5.13 billion in 2025, USD 5.48 billion in 2026, and reach USD 7.60 billion by 2031, growing at a CAGR of 6.78% from 2026 to 2031.

Which segment is expanding fastest within Low-iron glass applications?

Architectural facades are growing at a 7.39% CAGR as daylighting codes drive ultra-clear curtain-wall demand.

Why is low-iron glass critical for next-generation solar modules?

Bifacial and tandem perovskite-silicon cells need front-glass transmittance above 91.5%, a threshold that low-iron substrates meet while standard float glass does not.

How are domestic-content rules influencing supply chains?

U.S. and Indian content mandates have spurred new float-glass and coating lines, reshoring capacity, and shortening logistics for module assemblers.

Page last updated on: