Ultra-Thin Glass Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 15.71 Billion |

| Market Size (2031) | USD 26.87 Billion |

| Growth Rate (2026 - 2031) | 11.34% CAGR |

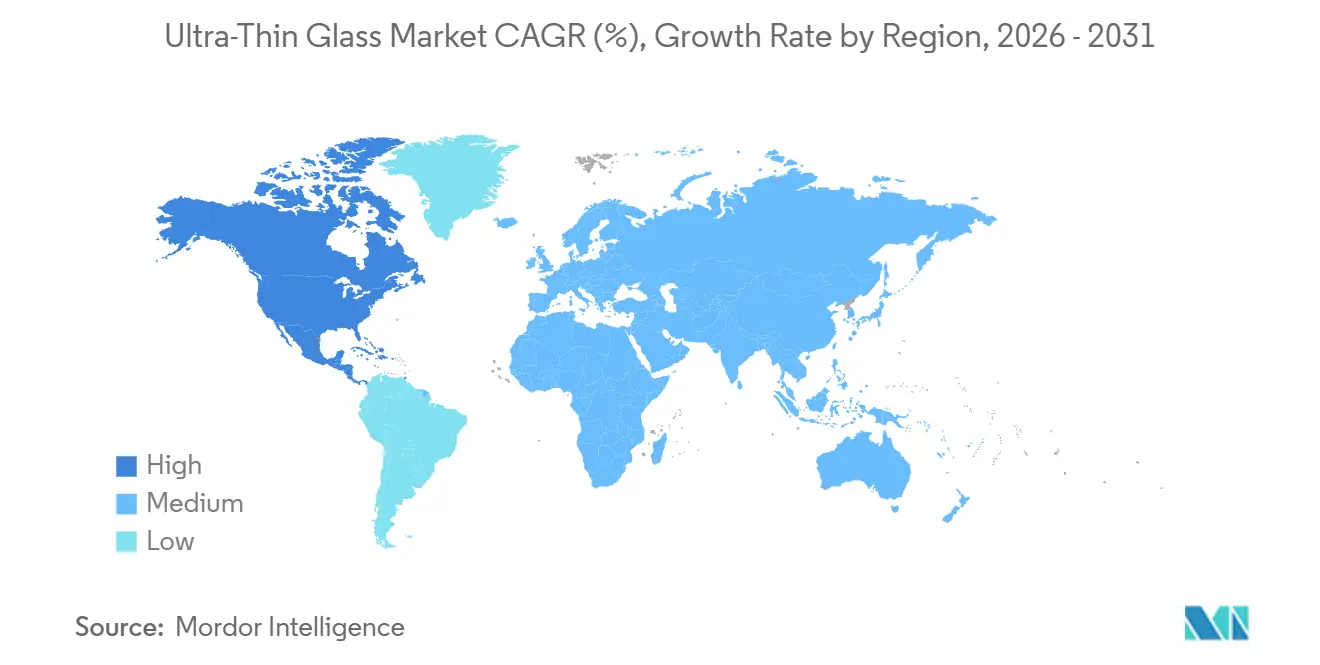

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ultra-Thin Glass Market Analysis by Mordor Intelligence

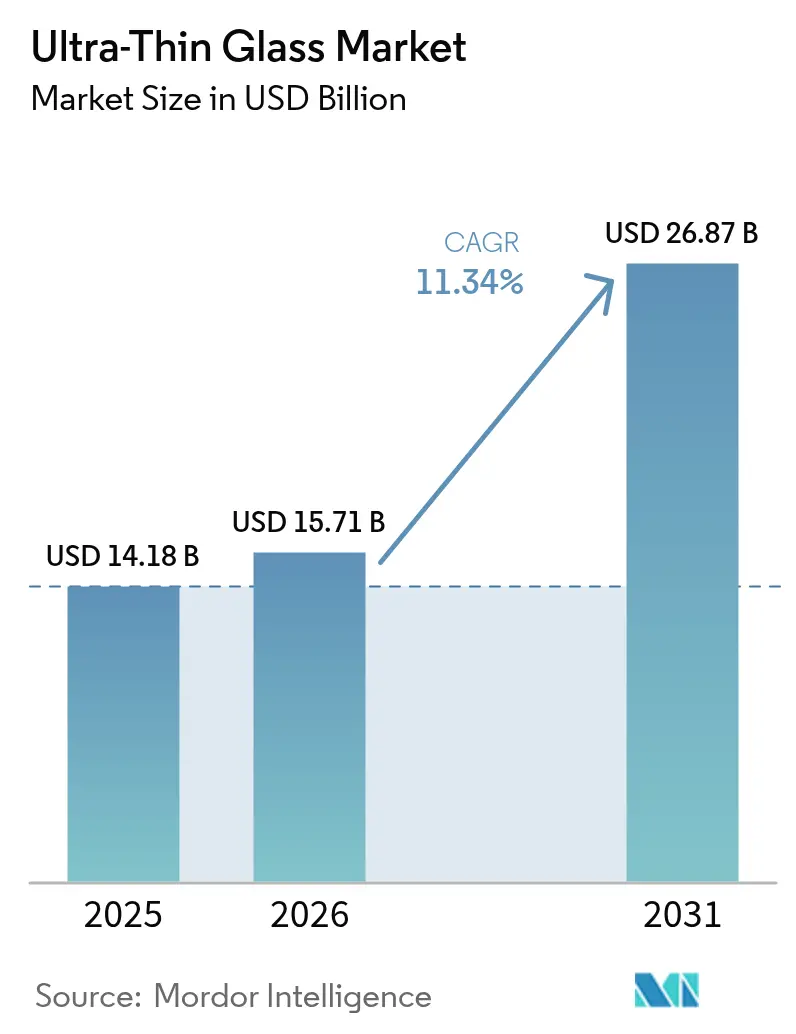

The Ultra-Thin Glass Market size is projected to be USD 14.18 billion in 2025, USD 15.71 billion in 2026, and reach USD 26.87 billion by 2031, growing at a CAGR of 11.34% from 2026 to 2031. Demand is accelerating as foldable smartphones, chiplet-based semiconductors, and weight-sensitive automotive glazing converge on substrates thinner than 0.5 millimeters. Touch-panel displays continue to anchor volume, yet next-generation glass interposers for advanced packaging and curved head-up displays (HUDs) are unlocking higher-margin outlets. Material selection is also widening: soda-lime variants dominate cost-focused devices, while aluminosilicate, borosilicate, and lithium-aluminosilicate chemistries secure premium niches that mandate low thermal expansion or extreme surface compression. Regionally, Asia-Pacific retains a scale advantage on the back of Chinese microfloat retrofits and Korean OLED investments, but North America is emerging as the fastest-growing node as the CHIPS Act localizes semiconductor supply chains.

Key Report Takeaways

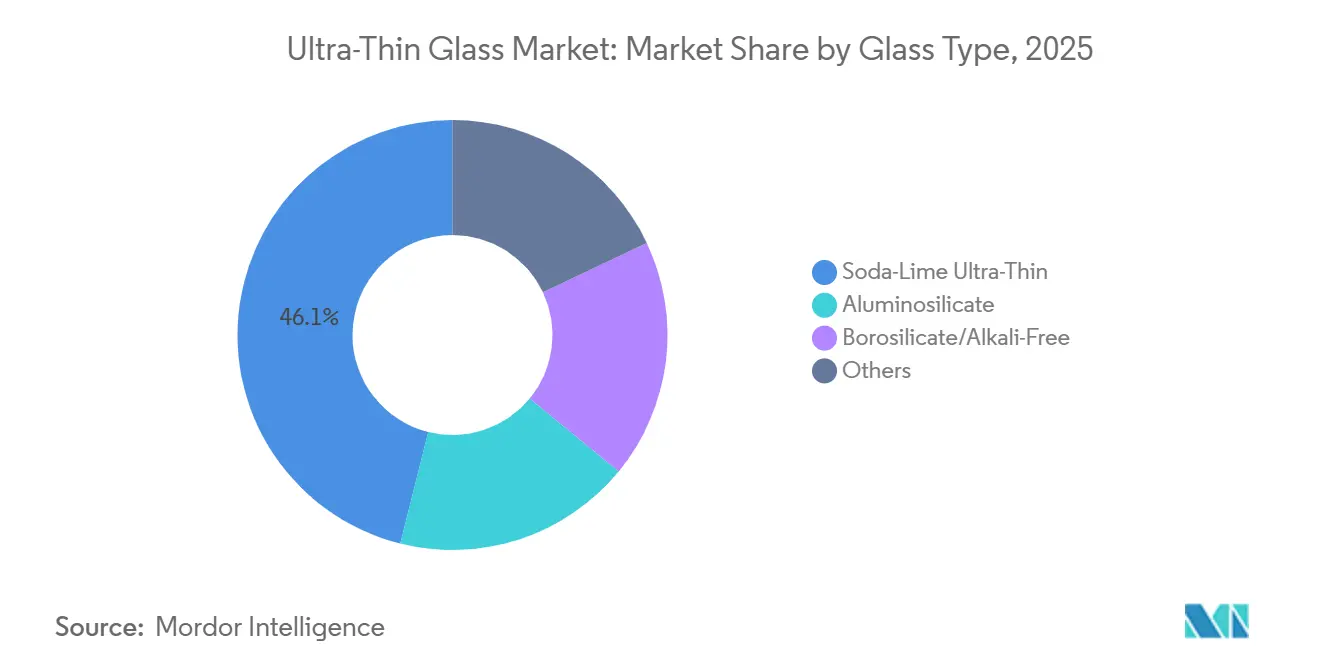

- By glass type, soda-lime commanded 46.09% of the ultra-thin glass market share in 2025, and the segment is projected to post a 12.10% CAGR to 2031.

- By manufacturing process, float and microfloat lines held 50.68% share of the ultra-thin glass market size in 2025 and are forecast to expand at a 12.89% CAGR between 2026-2031.

- By application, touch-panel displays led with 29.50% of the ultra-thin glass market share in 2025, while semiconductor substrates are projected to register the fastest 12.20% CAGR through 2031.

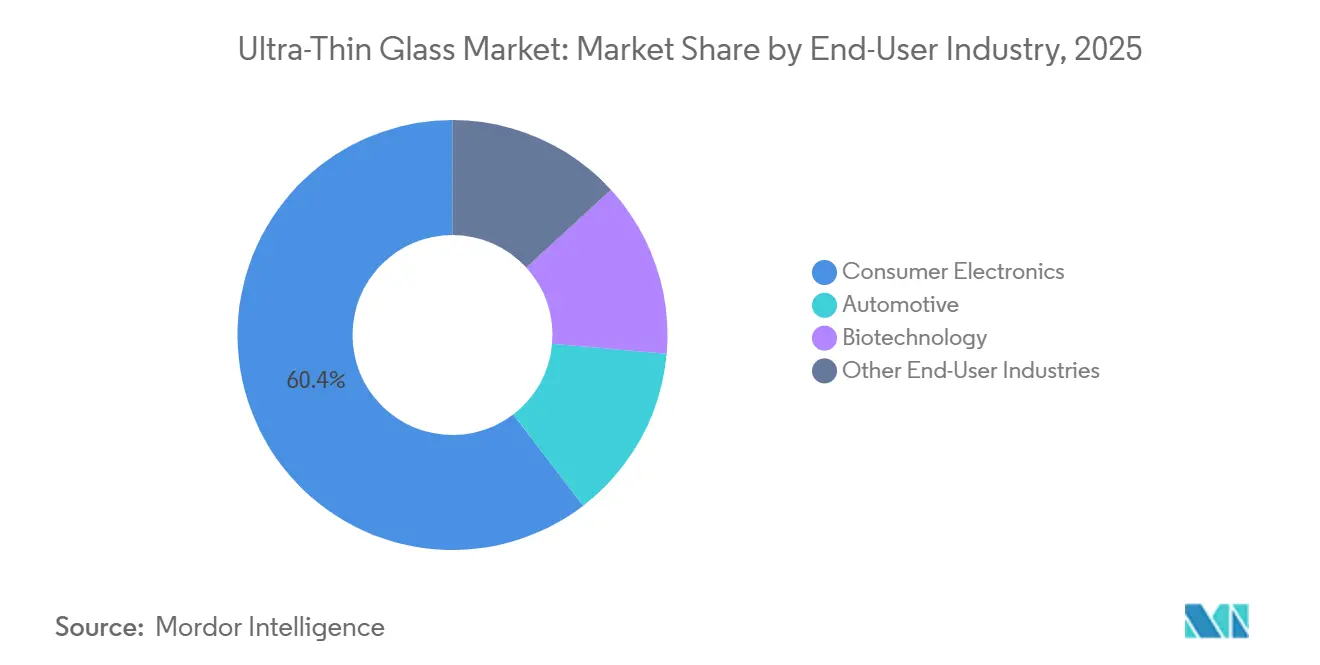

- By end-user industry, consumer electronics represented 60.41% of 2025 revenue, but automotive glazing is expected to grow at an 11.99% CAGR to 2031.

- By geography, Asia-Pacific contributed 49.59% of the 2025 value, whereas North America will record the highest regional CAGR of 11.91% over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ultra-Thin Glass Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from consumer electronics | +2.8% | Global, with APAC core accounting for 49.59% share | Medium term (2-4 years) |

| Rapid adoption in foldable smartphones and notebooks | +2.5% | APAC (South Korea, China), North America (Apple supply chain) | Short term (≤ 2 years) |

| Advancements in flexible OLED and micro-LED display lines | +2.1% | South Korea, China, Taiwan (display-panel hubs) | Medium term (2-4 years) |

| Weight-reduction needs in automotive glazing and HUDs | +1.6% | North America, Europe (automotive OEM clusters) | Long term (≥ 4 years) |

| Glass interposers for chiplet packaging | +1.4% | North America, Japan, South Korea (advanced-packaging nodes) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand from Consumer Electronics

In 2025, consumer electronics accounted for a significant portion of the market volume, driven by a robust upgrade cycle towards under-display sensors and edge-to-edge touch modules, fueling double-digit growth. Samsung's Galaxy S25 Ultra, featuring the new Corning Gorilla Armor 2, achieved a notable reduction in surface reflectance[1]Corning Incorporated, “Corning Gorilla Armor 2,” corning.com. This innovation has led rival OEMs to pursue similar 0.4-millimeter substrates. Following suit, notebook vendors are now adopting ultra-thin glass panels, moving away from the previously used yellow-prone polyimide films. However, the segment's dynamics are evolving, with semiconductor substrates for AI accelerators beginning to capture a larger market share. These advanced packaging applications not only command higher average selling prices but also utilize alkali-free chemistries. This ensures the protection of 112 Gbps SerDes lanes, subtly shifting the revenue focus towards these performance-critical grades.

Rapid Adoption in Foldable Smartphones and Notebooks

Ultra-thin glass economics have been revolutionized by the advent of foldable form factors. Samsung Display is rolling out its 8.6-generation OLED line, set to deliver crease-free panels tailored for Apple's anticipated foldable iPhone debuting in 2026. In a bid to mitigate risks, Chinese panel manufacturers are collaborating on microfloat soda-lime covers. These innovative covers boast impressive endurance and come at a significant cost advantage. Meanwhile, Corning has struck a deal, licensing its Willow roll-to-roll borosilicate, specifically designed for 180-degree notebook hinges. As a result, the industry's spotlight has shifted from merely ensuring hinge durability to mastering yield management. Notably, both float and microfloat lines are nearing the pivotal threshold, a sweet spot that harmonizes price and reliability for the mass-market foldable segment.

Advancements in Flexible OLED and Micro-LED Display Lines

Display fabs are now embedding ultra-thin glass directly into their backplane stacks. LG Display's CoE program is depositing RGB filters onto glass encapsulation layers, achieving a reduction in panel thickness and a cut in power consumption. Additionally, as micro-LED initiatives gain momentum, there's a demand for glass with a thermal expansion below 3.5 ppm/°C. SCHOTT's newly released low-loss glass in 2024 not only meets this requirement but also boasts high blue-light transmittance. As a result, while soda-lime continues to serve as the budget-friendly choice for OLED smartphones, borosilicate and lithium-aluminosilicate are stepping up for thermally sensitive micro-LED and automotive applications.

Weight-Reduction Needs in Automotive Glazing and HUDs

Electric-vehicle platforms are relentlessly chasing every kilogram of weight savings. Laminated ultra-thin windshields can reduce a car's weight, translating to an increase in range for a vehicle powered by a 75 kWh battery. AGC's Leoflex glass, set to be qualified in 2025, not only adheres to ISO-mandated thermal-shock durability standards but also boasts a significant weight reduction for curved HUD combiners. Procurement data reveals a significant uptick: European Tier-1s issued multiple RFQs for ultra-thin panoramic roofs in 2025, a notable increase from 2023, indicating a surge in design wins. Furthermore, EU recyclability regulations are amplifying this trend, incentivizing the use of lighter materials that are easier to document.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of high-purity raw materials and precision processing | -1.8% | Global, acute in North America and Europe due to energy costs | Medium term (2-4 years) |

| Brittleness and yield loss during large-area handling | -1.5% | APAC manufacturing hubs (China, South Korea, Japan) | Short term (≤ 2 years) |

| Limited recycling streams for greater than 0.3 mm glass waste | -0.9% | Europe (End-of-Life Vehicles Directive), North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of High-Purity Raw Materials and Precision Processing

Costs rise as electronic-grade silica, with iron content less than 50 ppm, high-purity alumina powder, and platinum-rhodium furnace hardware see price hikes. In 2025, spot silica prices surged, impacting float-line margins, especially for those without hedged contracts. Fusion-draw furnaces, operating at high temperatures, necessitate crucible replacements periodically. Additionally, ion-exchange and laser patterning techniques command a significant premium for aluminosilicate covers compared to soda-lime. European manufacturers grapple with heightened pressures from soaring natural-gas tariffs. While SCHOTT's electric-melting retrofit in Mainz offers some relief, it doesn't fully shield against energy price fluctuations.

Brittleness and Yield Loss During Large-Area Handling

Substrates thinner than 0.3 mm fracture under a stress of 20 MPa, a threshold frequently exceeded during vacuum-chuck transfers. In 2025, Chinese float operators reported a scrap rate for Gen 8-plus panels, diminishing their cost advantage[2]CSG Holding, “Display Glass Production,” csgglass.com. While Corning’s ion-levitation handlers boost yields, their high price tag per tool limits their use to semiconductor lines. However, roll-to-roll coating shows potential at Fraunhofer’s Glass4Flex pilot; its inability to accommodate ion-exchange confines its applications to non-structural sensors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Glass Type: Soda-Lime Dominates Cost-Sensitive Volume

Soda-lime ultra-thin products captured 46.09% of 2025 revenue and are forecast to grow at a 12.10% CAGR, underpinned by microfloat lines that hit sub-100 μm thickness at high yield. Aluminosilicate commands foldable-device covers where surface compression above 800 MPa secures 200,000 folds without cracks. Borosilicate and alkali-free glass underpin semiconductor substrates; their sub-3.5 ppm/°C expansion protects high-speed interconnects. Lithium-aluminosilicate remains a niche in HUD optics for its near-zero expansion. ISO 12543-4 durability tests favor borosilicate in automotive laminates, nudging premium OEMs upscale despite higher costs. Chinese float operators are therefore scaling soda-lime to significant production levels for mid-tier electronics, while patent-rich incumbents retain high-margin aluminosilicate and borosilicate tiers.

By Manufacturing Process: Float Lines Scale, Fusion Draw Safeguards Quality

Float and microfloat technologies delivered 50.68% of 2025 production, and capacity expansions point to a 12.89% CAGR through 2031. The cost of a microfloat line is significantly lower than that of a fusion draw, allowing for a shorter payback period, assuming an optimal utilization rate. However, certain zero-defect applications, such as glass interposers and foldable covers, remain reliant on fusion and down-draw methods. This preference is due to the fact that in these methods, the melt never comes into contact with refractory surfaces. For instance, SCHOTT’s down-draw borosilicate achieves a thickness of 20 μm with a roughness of less than 0.5 nm. These metrics are beyond reach in the tin-bath float method, where contact results in asperities of approximately 2 nm. Meanwhile, slit-draw and roll-to-roll processes are catering to the burgeoning flexible electronics market. Notably, Corning Willow is pioneering curved OLED lighting, and Fraunhofer is coating reels for photovoltaic modules. Consequently, the choice of process has evolved into a balancing act between acceptable inclusion density and capital expenditure, leading to a segmentation in the supply base.

By Application: Semiconductor Substrates Accelerate

Touch panels represented 29.50% of 2025 revenue, but semiconductor substrates will clock a 12.20% CAGR to 2031, driven by the shift of chiplet packaging to glass. Intel's borosilicate interposers, capable of supporting TSVs and an impressive I/O density, are now replacing organic laminates, which were limited to much lower densities. With alkali-free compositions, sodium migration is effectively prevented at specific voltage biases. Additionally, SCHOTT's low-loss glass boasts a dielectric loss at high frequencies. In the automotive sector, glazing plays a pivotal role in both weight reduction and augmented reality heads-up display (AR-HUD) optics. For instance, laminated ultra-thin windshields can reduce vehicle weight, and optical combiners can enhance the field of view by doubling it. While flexible OLED lighting, microfluidics, and solar cover sheets currently represent a small portion of the market, they are poised for significant growth as roll-to-roll techniques advance.

By End-User Industry: Automotive Gains Momentum

Consumer electronics contributed 60.41% of the 2025 value, driven by the sale of smartphones and notebooks, both featuring cutting-edge ultra-thin covers, touch panels, and innovative under-display sensors. Automotive glazing is the up-and-comer, growing at an 11.99% CAGR as EV range targets push lightweight materials and EU recyclability mandates favor traceable substrates. Additionally, HUD combiners, utilizing 0.3 mm glass, not only minimize ghost images but also facilitate AR overlays. This innovation has led to orders projected to surpass millions of units annually by 2028. On a more niche front, biomedical cartridges and energy modules, though smaller in scale, are strategically significant. They harness the unique properties of glass—its impermeability and biocompatibility—to meet stringent FDA and IEC standards.

Geography Analysis

Asia-Pacific delivered 49.59% of 2025 revenue, buoyed by Korean OLED investments and Chinese float retrofits that bolster economies of scale. North America’s 11.91% CAGR through 2031, fueled by the CHIPS Act's fabs and mandates for vehicle lightweighting. Major players are driving the demand for advanced packaging, while AGC’s Tlaxcala plant in Mexico supplies U.S. OEMs. Europe, holding a notable market share, is influenced by automotive glazing needs and stringent ecodesign regulations. SCHOTT’s retrofit of electric melting not only mitigates energy volatility but also reduces CO₂ emissions. Meanwhile, OEMs like BMW are adopting ultra-thin roofs to achieve a fleet target by 2027. Although South America and the MEA regions are still emerging, they stand to benefit from solar-energy initiatives, especially with a focus on 100 μm borosilicate covers post-2028.

Competitive Landscape

The ultra-thin glass market is consolidated. Corning’s Gorilla Armor 2 underpins an annual contract with Samsung’s flagship phones, blocking rivals from the high-visibility Android segment. Chinese firms scale microfloat capacity for cost-driven smartphones and side glazing. Compliance adds a new barrier; ISO 12543-4 durability tests and EU digital-passport rules threaten the disqualification of suppliers lacking traceability or accelerated-aging data.

Ultra-Thin Glass Industry Leaders

Corning Incorporated

AGC Inc.

SCHOTT AG

Nippon Electric Glass Co., Ltd.

CSG Holding Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Corning Incorporated has revealed an ultra-thin, durable glass designed to transform heat retention in buildings, potentially generating substantial annual energy cost savings. Inspired by materials utilized in smartphone screens, this innovation is anticipated to play a critical role in addressing the estimated USD 25 billion annual energy loss in the United States caused by inefficient windows.

- January 2025: AGC Glass Europe has announced plans to invest in a new insulating vacuum glass production line at its Lodelinsart site in Belgium. The production line, expected to begin operations in mid-2026, aims to significantly enhance AGC's production capacity for FINEO ultra-thin insulating vacuum glass in Europe, strategically positioning the facility closer to its key customers.

Global Ultra-Thin Glass Market Report Scope

Ultra-thin glass (UTG) is defined as a material with a thickness typically ranging from 0.1mm to 1mm, offering exceptional mechanical strength, optical clarity, and flexibility. It distinguishes itself from conventional glass by combining the rigidity of glass with the adaptability of polymers, enabling groundbreaking applications across diverse sectors.

The ultra-thin glass market is segmented by glass type, manufacturing process, application, end-user industry, and geography. By glass type, the market is segmented into aluminosilicate (e.g., Gorilla, Dragontrail), borosilicate/alkali-free, soda-lime ultra-thin, and others (e.g., lithium-aluminosilicate). By manufacturing process, the market is segmented into fusion draw, down-draw/overflow, float and microfloat, and slit draw/roll-to-roll. By application, the market is segmented into semiconductor substrate, touch panel displays, fingerprint sensors, automotive glazing, and other applications (e.g., automotive displays and glazing). By end-user industry, the market is segmented into consumer electronics, automotive, biotechnology, and other end-user industries (e.g., energy and power). The report also covers the market size and forecasts for the aerosol paints market in 15 countries across major regions. For each segment, the market sizing and forecasts are done based on value (USD).

| Aluminosilicate (e.g., Gorilla, Dragontrail) |

| Borosilicate/Alkali-Free |

| Soda-Lime Ultra-Thin |

| Others (Lithium-Aluminosilicate, etc.) |

| Fusion Draw |

| Down-Draw/Overflow |

| Float and Microfloat |

| Slit Draw/Roll-to-Roll |

| Semiconductor Substrate |

| Touch Panel Displays |

| Fingerprint Sensors |

| Automotive Glazing |

| Other Applications (Automotive Displays and Glazing, etc.) |

| Consumer Electronics |

| Automotive |

| Biotechnology |

| Other End-User Industries (Energy and Power, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Glass Type | Aluminosilicate (e.g., Gorilla, Dragontrail) | |

| Borosilicate/Alkali-Free | ||

| Soda-Lime Ultra-Thin | ||

| Others (Lithium-Aluminosilicate, etc.) | ||

| By Manufacturing Process | Fusion Draw | |

| Down-Draw/Overflow | ||

| Float and Microfloat | ||

| Slit Draw/Roll-to-Roll | ||

| By Application | Semiconductor Substrate | |

| Touch Panel Displays | ||

| Fingerprint Sensors | ||

| Automotive Glazing | ||

| Other Applications (Automotive Displays and Glazing, etc.) | ||

| By End-User Industry | Consumer Electronics | |

| Automotive | ||

| Biotechnology | ||

| Other End-User Industries (Energy and Power, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the forecast revenue for ultra-thin glass by 2031?

Global consumption is USD 15.71 billion in 2026 and is projected to reach USD 26.87 billion by 2031, reflecting a 11.34% CAGR.

Which region will expand the fastest by 2031?

North America is expected to post the highest regional CAGR of 11.91% on the back of CHIPS Act semiconductor fabs and lightweight automotive glazing demand.

Which application segment is growing quickest?

Semiconductor substrates are forecast to grow at a 12.20% CAGR as chiplet packaging migrates to glass interposers.

Why is soda-lime glass still dominant despite premium chemistries?

Soda-lime maintains a 46.09% revenue share because microfloat retrofits achieve sub-100 μm thickness at lower capital intensity, keeping unit costs attractive for high-volume consumer devices.

How are recyclability rules influencing supplier choices?

EU digital-passport and end-of-life mandates are pushing OEMs toward traceable ultra-thin glass grades and suppliers that can document take-back pathways.

Page last updated on: