Solar Charger Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

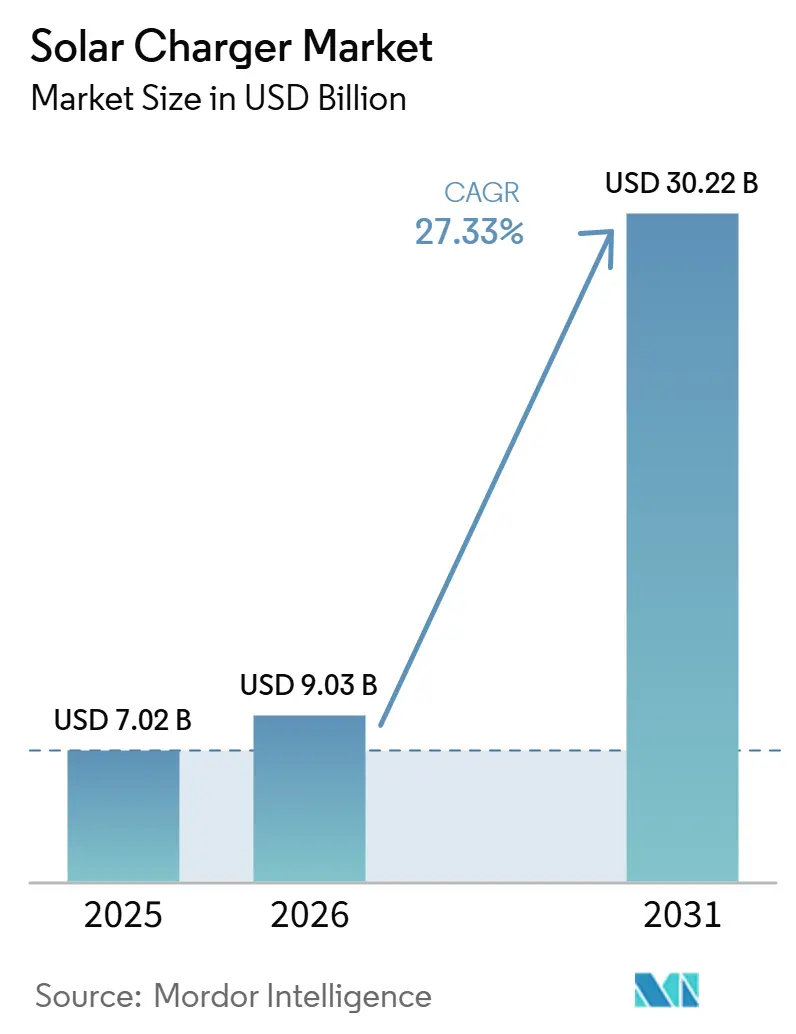

| Market Size (2026) | USD 9.03 Billion |

| Market Size (2031) | USD 30.22 Billion |

| Growth Rate (2026 - 2031) | 27.33% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Solar Charger Market Analysis by Mordor Intelligence

The Solar Charger Market size is expected to increase from USD 7.02 billion in 2025 to USD 9.03 billion in 2026 and reach USD 30.22 billion by 2031, growing at a CAGR of 27.33% over 2026-2031. Falling module prices below USD 0.10 per watt, surging outdoor-recreation spending, and the first vehicle-integrated photovoltaic (VIPV) programs from global automakers are expanding the addressable solar charger market well beyond leisure users. Automotive OEMs are embedding 3-4 m² solar arrays into roofs and hoods, cutting charging visits for commuter EV drivers by as much as 65% [1]Nissan Motor Co., “Nissan-Lightyear Solar Technology Partnership,” nissan-global.com. Certification mandates in Southeast Asia and disaster-relief deployments by NGOs are further driving adoption. High-efficiency tandem cells are reducing surface-area requirements, enabling lighter and foldable form factors. Competitive intensity remains high across a fragmented landscape of established portable power brands, specialist solar firms, and new automotive-tier suppliers, each competing for early-mover advantage as the solar charger market shifts from aftermarket panels to factory-installed energy harvesting.

Key Report Takeaways

- By product type, conventional rigid solar panel chargers held 37.9% of the solar charger market share in 2025; foldable and flexible variants are projected to grow at a 31.8% CAGR through 2031.

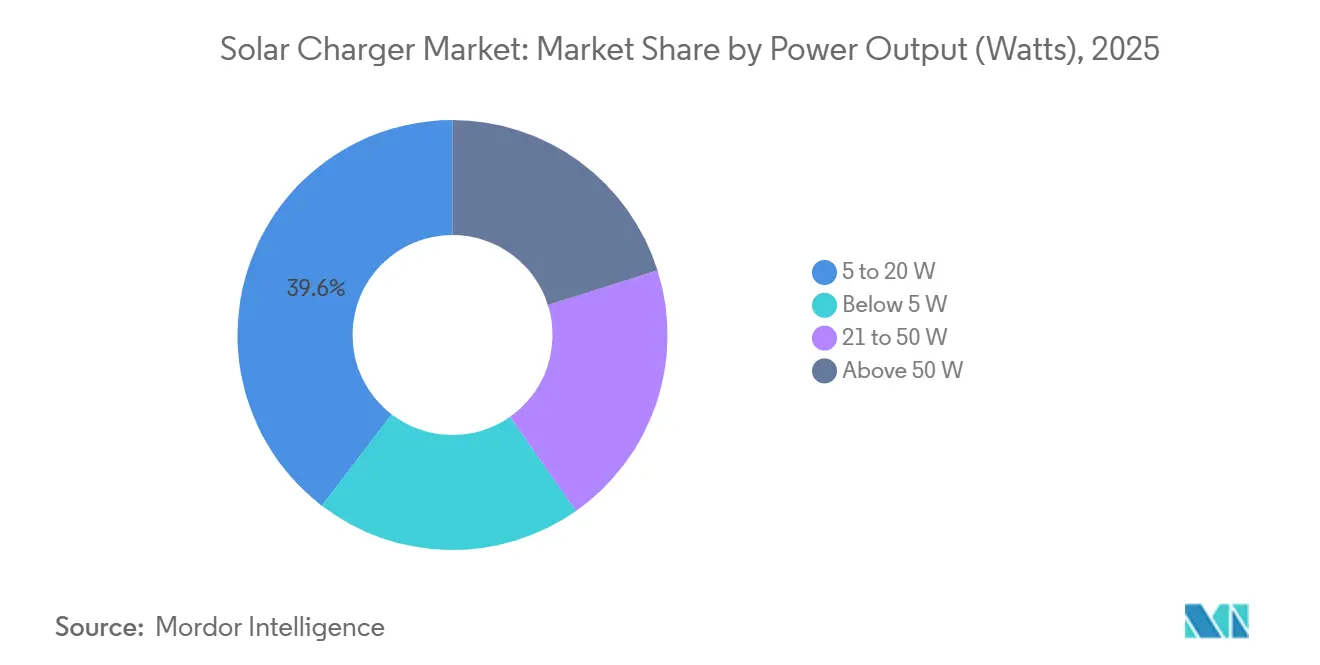

- By power output, 5-20 watt units accounted for 39.6% of the solar charger market size in 2025, whereas 21-50 watt systems are projected to grow at a 30.2% CAGR through 2031.

- By application, consumer electronics led with 49.8% revenue share in 2025, while the military and defense segment is projected to grow at a 29.5% CAGR through 2031.

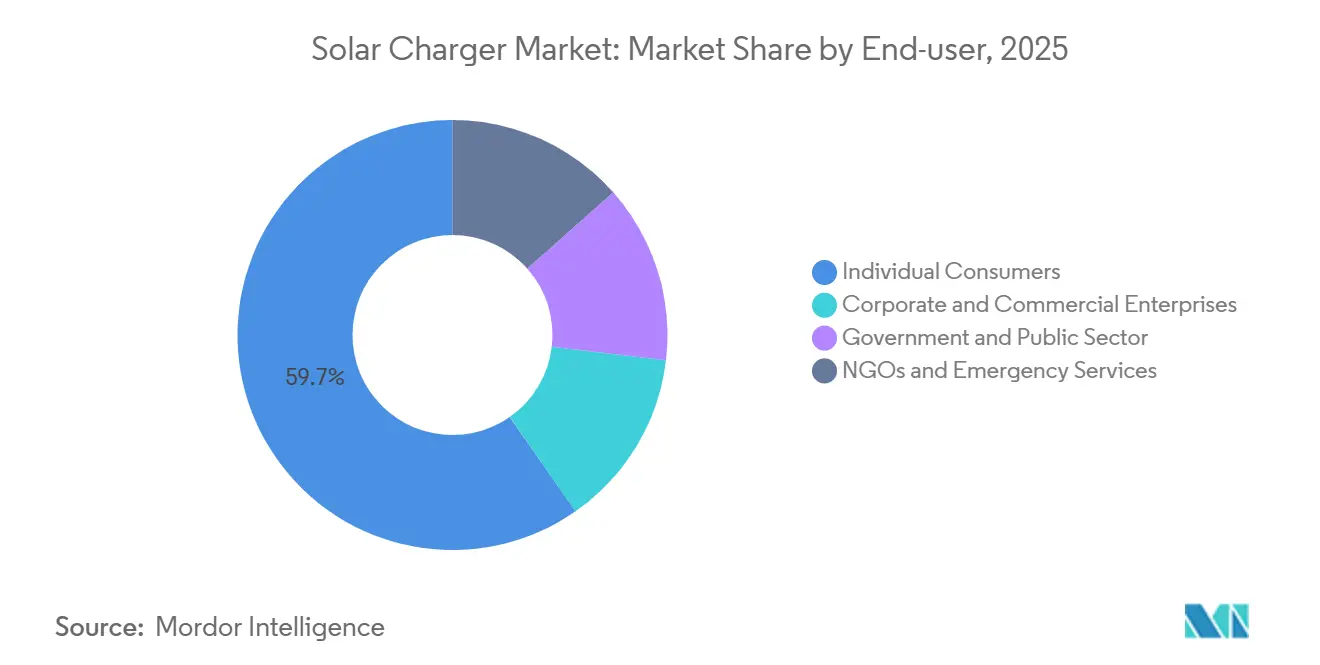

- By end-user, individual consumers accounted for 59.7% of demand in 2025; NGOs and emergency services are projected to record the fastest growth at a 31.0% CAGR through 2031.

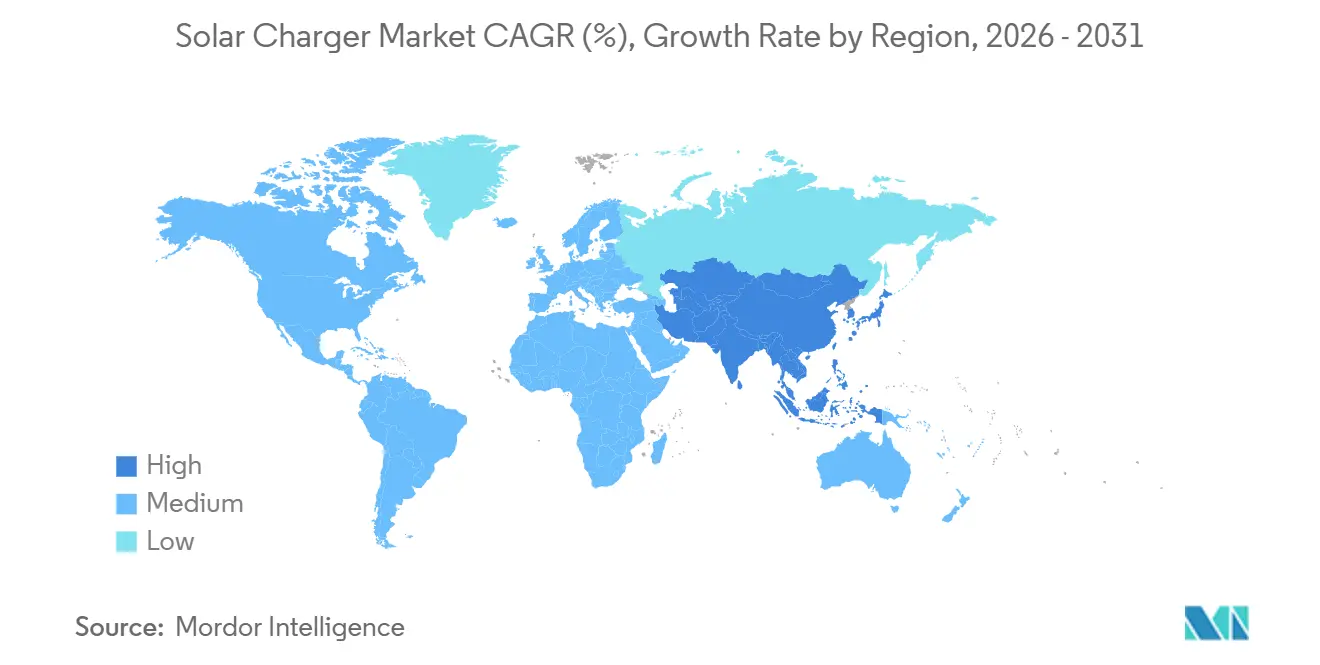

- By region, Asia-Pacific dominated with 35.5% revenue share in 2025, and the region is expected to grow at a 29.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Solar Charger Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising outdoor recreation and off-grid power demand | +4.5% | Global, led by North America and ASEAN | Medium term (2–4 years) |

| Declining solar-PV cost and efficiency gains | +6.2% | Global, with China and Europe at the core | Short term (≤ 2 years) |

| Growth in portable consumer-electronics ownership | +3.8% | China, India, ASEAN, MEA | Medium term (2–4 years) |

| Clean-energy incentives and e-waste reduction policies | +4.1% | EU, California, selected ASEAN states | Long term (≥ 4 years) |

| Adoption of solar-integrated fabrics in defense | +2.80% | North America, Europe, select APAC | Long term (≥ 4 years) |

| ESG-funded micromobility solar charging | +1.90% | Urban centers worldwide | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Outdoor Recreation & Off-Grid Power Demand

Outdoor recreation spending continues to climb and now directly shapes purchasing patterns for 20-50 watt foldable panels that keep phones, drones, and laptops running for multi-day trips [2] International Energy Agency, “Renewables 2025,” iea.org. Distributed photovoltaics supplied 42% of new global solar capacity in 2025, underscoring the structural shift toward small-scale systems. Defense validation reinforces the civilian narrative: 300-watt roof arrays on tactical vehicles trimmed diesel use by 10%, a proof point that resonates with overlanders and expedition outfitters [3]U.S. Army, “Operational Energy Strategy 2025,” army.mil. Disaster preparedness is another demand driver, as NGOs deploy containerized microgrids in cyclone- and wildfire-prone regions, positioning solar chargers as low-cost resilience assets. Together, these factors expand the solar charger market from a camping accessory niche into a broader off-grid power category.

Declining Solar-PV Cost and Efficiency Gains

Sub-USD 0.10 per-watt pricing reached the portable segment in 2025, cutting bill-of-materials costs by 30-40% compared with 2020. Flexible perovskite-silicon tandem cells achieved 33.89% efficiency in laboratory-validated prototypes, shrinking footprint and weight.[4] LONGi Solar, “Record Flexible Perovskite-Silicon Tandem Cell,” longisolar.com Automakers are already capitalizing on cost efficiencies, with AGC Automotive's back-contact solar roof set to enter mass production at greater than 25% efficiency. This development will provide range extension without plug-in charging and eliminate the need for roller-blind mechanisms. As unit economics improve, aggressive retail pricing is making solar power banks cheaper on a per-watt-hour basis than conventional fast-charge packs, a trend expected to materialize within three years. These factors are driving a 27.3% CAGR in the solar charger market.

Growth in Portable Consumer-Electronics Ownership

Smartphone and tablet penetration continues to rise in APAC and MEA, supporting sustained demand for solar chargers. Households in off-grid and poorly electrified regions bundle solar kits with feature-phone purchases, while urban gig-economy workers adopt 30-50 watt panels for in-vehicle device charging. Anker's 3,840 Wh SOLIX F3800 represents a modular system that functions as both a residential backup unit and a mobile power station. This convergence is reducing the distinction between consumer electronics and home energy management, expanding the solar charger market toward hybrid AC/DC ecosystems.

Clean-Energy Incentives and E-Waste Reduction Policies

Germany registered 426,269 balcony solar systems in 2025, demonstrating how streamlined permitting accelerates plug-and-play adoption. The United Kingdom followed in March 2026, approving sub-800 watt plug-in panels that require no electrician, opening the market to tenants and flat dwellers as first-time buyers. In contrast, the expiry of the 30% US federal tax credit in December 2025 extended payback periods from seven to ten years and reduced installer payrolls by 20%, illustrating the impact of subsidy discontinuation. Parallel e-waste directives mandate replaceable batteries, pushing OEMs toward circular-design architectures that extend product life but increase near-term costs.

Restraints Impact Analysis*

| Restraint | (~) (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Variable irradiance and intermittency of solar resource | –3.2% | High-latitude Europe, Canada, Northern U.S. | Short term (≤ 2 years) |

| Competition from fast-charge power banks and adapters | –2.8% | Urban Asia-Pacific and North America | Medium term (2–4 years) |

| Import tariffs on PV components | -2.10% | North America | Medium term (2–4 years) |

| Lithium-ion supply-chain tightness | -1.90% | Battery hubs worldwide | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Variable Irradiance and Intermittency of Solar Resource

Longitudinal monitoring across 1 million km of road trials revealed that vehicle-roof panels in Central Europe harvest only 2.8 kWh per m² annually, versus 4.6 kWh in equatorial regions. This variability means a wintertime smartphone charge in Oslo can take three times longer than in Bangkok. Portable power brands address intermittency with MPPT controllers and oversized batteries, but the added cost and weight slow adoption in cloudier geographies, making the solar charger market inherently regional.

Competition from Fast-Charge Power Banks/Adapters

USB-C PD and SuperVOOC devices deliver 65–100 watts from grid-charged 20,000 mAh packs retailing at USD 50, undercutting comparable solar solutions priced above USD 120. Solid-state batteries expected after 2028 may widen this performance gap further. OEMs have responded by bundling solar panels with AC input and emphasizing sustainability and grid independence. However, convenience-driven urban buyers largely prefer faster, lower-cost plug-in options, reducing the urban total addressable market for solar chargers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Flexible Formats Lead Consumer Uptake

Foldable and flexible models grew at a 31.8% CAGR through 2031, well above the overall solar charger market, driven by perovskite-silicon tandem cells with 33.89% efficiency that bend without cracking. Rigid panel chargers retained a 37.9% market share in 2025, as RV, marine, and cabin owners continue to prioritize durability over portability.

Automotive vehicle-integrated photovoltaics (VIPV) is raising performance benchmarks: Hyundai spin-off Solarstic's injection-molded polymer modules output 500 watts and integrate directly into body panels. As costs decline, aftermarket car-battery trickle chargers may lose relevance, while flexible consumer panels benefit from vehicle-driven scale effects. This technological convergence is reshaping value distribution across the solar charger market.

By Power Output: Mid-Range Units Drive Future Growth

The 5-20 watt segment accounted for 39.6% of revenue in 2025, reflecting its dominance in smartphone charging applications. The 21-50 watt segment is growing at the fastest rate, with a CAGR of 30.2%, driven by expanding use in laptops, drones, and micromobility devices.

High-wattage (100 watt+) foldable panels increasingly overlap with semi-permanent array applications. A notable example is Nissan's 500-watt Ao-Solar Extender prototype, which can add 3,000 km of annual EV range. Growing consumer expectations for 100-watt panels to match rooftop efficiency levels are pushing suppliers to use premium cell bins and hardened laminates to maintain product reliability in the solar charger market.

By Application: Defense Overtakes Leisure on Growth Metrics

Consumer electronics accounted for 49.8% of 2025 revenue, while military contracts are emerging as the fastest-growing segment, with a 29.5% CAGR driven by 100-660 watt soldier-portable kits that reduce diesel and battery resupply requirements.

Micromobility fleets represent an adjacent niche with notable growth potential. Barcelona and Liverpool deployments of Bolt's solar e-bikes reduce battery swaps by six annually, lowering labor, transport, and grid energy costs. NGO disaster response also contributes to demand; more than 300 kW of mobile solar deployed across 250 resilience hubs highlights humanitarian demand for portable solar charging solutions.

By End-User: NGOs and Emergency Services Accelerate Procurement

Individuals account for the largest share of the market at 59.7%. However, NGOs and emergency services are expanding at the fastest rate, with a CAGR of 31.0%, as blackout-prone regions prioritize portable power solutions. Their procurement ranges from pilot kits to megawatt-class containerized fleets, reshaping channel dynamics within the solar charger market.

Corporate buyers, including construction and telecom firms, are increasingly seeking service-level agreements that bundle hardware with monitoring capabilities, prompting OEMs to offer hybrid CAPEX/OPEX models. Government incentives targeting renters, such as the UK's 800-watt plug-in rule change, are bringing new urban demographics into the solar charger market.

Geography Analysis

Asia-Pacific accounted for 35.5% of global revenue in 2025 and is projected to grow at a CAGR of 29.1% through 2031. This growth is supported by certification frameworks such as TISI, ICC, and CR, which restrict sub-standard imports and strengthen consumer confidence. China's vertically integrated supply chain enables landed costs 20-30% below those of Western competitors, while import duties in India are redirecting assembly investment toward domestic production. Rising smartphone adoption in Indonesia and the Philippines sustains baseline unit demand, and typhoon-prone island nations are adopting solar chargers to improve energy resilience.

North America presents a mixed outlook. Demand from outdoor recreation and RV users supports sales in the 50-200 watt segment, while the expiry of the federal Investment Tax Credit (ITC) has extended residential payback periods to 10 years, reducing momentum in the rooftop segment. The U.S. Army's multiyear procurement pipeline and Massachusetts' solar e-bike hub in Somerville demonstrate how defense and municipal programs offset volatility in the civilian market. Canada's cabin market and Mexico's off-grid rural regions maintain steady mid-power demand, supporting North America's overall market share.

Europe benefits from consistent policy support. Germany's balcony solar installations and the UK's authorization of plug-in panels in March 2026 reduce the need for professional installation, making adoption more accessible for renters. France's feed-in tariff (FiT) schemes support residential uptake, while the Nordic countries utilize extended summer daylight for marine and cabin applications. In other regions, Brazil's Amazonia, the UAE's desert environments, and South Africa's ongoing load-shedding challenges represent high-growth but high-risk markets that depend on financing mechanisms such as green bonds and multilateral aid. These emerging regions broaden the global solar charger market and reduce reliance on demand from mature Western markets.

Competitive Landscape

The solar charger market is expected to be moderately consolidated. Major portable power brands (Anker, Jackery, EcoFlow) leverage global retail footprints and integrated storage ecosystems, while outdoor specialists (Goal Zero, Renogy) focus on ruggedness and DC compatibility. BioLite's April 2025 acquisition of Goal Zero combines two premium outdoor product lines and consolidates lithium iron phosphate procurement. Automotive-tier entrants such as AGC Automotive and Solarstic compete with aftermarket panels through factory-installed VIPV roofs integrated at the assembly line.

Technology investment is a key differentiator: LONGi's 27.09% rigid-cell and 33.89% flexible-cell efficiency breakthroughs reduce weight and area, enabling lighter consumer products. Companies embedding bi-directional inverters and smart-grid APIs are positioning for vehicle-to-home applications, a likely next growth area for the solar charger market. Regional supply chain diversification, such as Renogy's shift to Latin American assembly, reduces exposure to tariff changes and logistics disruptions. Market fragmentation persists, but the capability gap between high-volume consumer brands and niche defense-oriented vendors is narrowing as both pursue flexible-cell performance improvements and VIPV economies of scale.

Solar Charger Industry Leaders

Anker Innovations

Goal Zero (NRG Energy)

Renogy

Jackery Inc.

EcoFlow

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: SolarEdge Introduces Wallbox for Direct Solar EV Charging. The manufacturer has announced the launch and initial installations of its One EV Charger Pro, a residential charging station designed for the European market. This product integrates with SolarEdge systems to enable direct solar-powered electric vehicle (EV) charging.

- May 2025: SolarEdge Technologies, Inc. introduced a solar-powered EV charging solution for businesses. The solution includes a new EV charger, managed by an energy management system developed after SolarEdge's acquisition of Wevo Energy the previous year.

- January 2025: Jackery launched Solar Roof tiles with more than 25% cell efficiency, priced USD 7,000-20,000, alongside Explorer 3000 v2 generator and a new DC-to-DC charger.

- January 2025: Anker debuted the Solix Solar Beach Umbrella, producing up to 100 W from perovskite cells, doubling low-light efficiency versus silicon.

Global Solar Charger Market Report Scope

Solar chargers harness sunlight through solar panels, converting it directly into electricity. This electricity can charge batteries or power electronic devices. In contrast to conventional chargers that rely on wall outlets, solar chargers tap into the sun's renewable energy, enabling off-grid power solutions.

The global solar charger market report is segmented by type, power output, application, end-user, and geography. By type, the market is segmented into solar panel chargers, solar car-battery chargers, foldable/flexible solar chargers, solar backpack chargers, and integrated solar-device chargers. By power output, the market is segmented into below 5W, 5-20W, 21-50W, and above 50W. By application, the market is segmented into consumer electronics, automotive and mobility, military and defense, industrial and commercial, and remote and off-grid locations. By end-user, the market is segmented into individual consumers, corporate and commercial enterprises, government and public sector, NGOs and emergency services. The report also covers the market size and forecasts for the global solar charger market in 18 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Solar Panel Chargers |

| Solar Power Banks |

| Solar Car-Battery Chargers |

| Foldable/Flexible Solar Chargers |

| Solar Backpack Chargers |

| Integrated Solar-Device Chargers |

| Below 5 W |

| 5 to 20 W |

| 21 to 50 W |

| Above 50 W |

| Consumer Electronics | Smartphones and Tablets |

| Laptops and Wearables | |

| Cameras and Drones | |

| Automotive and Mobility | Passenger Vehicles |

| Micromobility (e-bikes, scooters) | |

| Military and Defense | |

| Industrial and Commercial | |

| Remote and Off-grid Locations |

| Individual Consumers |

| Corporate and Commercial Enterprises |

| Government and Public Sector |

| NGOs and Emergency Services |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Type | Solar Panel Chargers | |

| Solar Power Banks | ||

| Solar Car-Battery Chargers | ||

| Foldable/Flexible Solar Chargers | ||

| Solar Backpack Chargers | ||

| Integrated Solar-Device Chargers | ||

| By Power Output (Watts) | Below 5 W | |

| 5 to 20 W | ||

| 21 to 50 W | ||

| Above 50 W | ||

| By Application | Consumer Electronics | Smartphones and Tablets |

| Laptops and Wearables | ||

| Cameras and Drones | ||

| Automotive and Mobility | Passenger Vehicles | |

| Micromobility (e-bikes, scooters) | ||

| Military and Defense | ||

| Industrial and Commercial | ||

| Remote and Off-grid Locations | ||

| By End-user | Individual Consumers | |

| Corporate and Commercial Enterprises | ||

| Government and Public Sector | ||

| NGOs and Emergency Services | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast will global demand for solar chargers grow to 2031?

The solar charger market is projected to expand at a 27.3% CAGR from 2026 to 2031, taking revenue from USD 9.03 billion to USD 30.22 billion.

Which region contributes the most revenue today?

Asia-Pacific led with 35.5% of global revenue in 2025, driven by certification mandates and smartphone proliferation.

What product formats are gaining share the quickest?

Foldable and flexible chargers are rising at 31.8% CAGR thanks to high-efficiency tandem cells and growing demand for lightweight gear.

Why are NGOs becoming major buyers?

Disaster-relief agencies deploy portable solar to power clinics, shelters, and communications during grid outages, pushing NGO and emergency-service demand up 31.0% CAGR.

How does automotive solar integration affect the charger business?

Vehicle-integrated photovoltaics from Nissan, Hyundai, and others reduce demand for aftermarket car chargers yet create scale economies that lower flexible-cell costs for consumer products.

What is the main technological frontier after 2026?

Perovskite-silicon tandem cells exceeding 33% efficiency and injection-molded polymer VIPV modules are set to redefine performance and integration possibilities for next-generation solar chargers.

Page last updated on: