Market Overview

| Study Period | 2021 - 2031 |

|---|---|

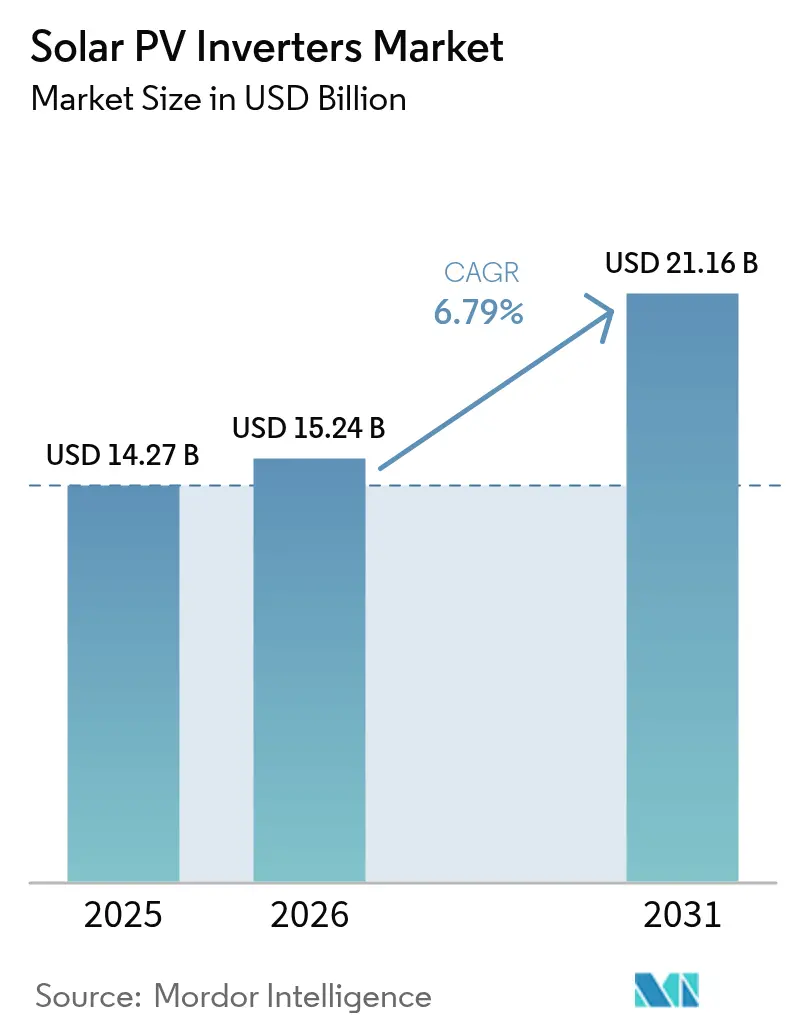

| Market Size (2026) | USD 15.24 Billion |

| Market Size (2031) | USD 21.16 Billion |

| Growth Rate (2026 - 2031) | 6.79% CAGR |

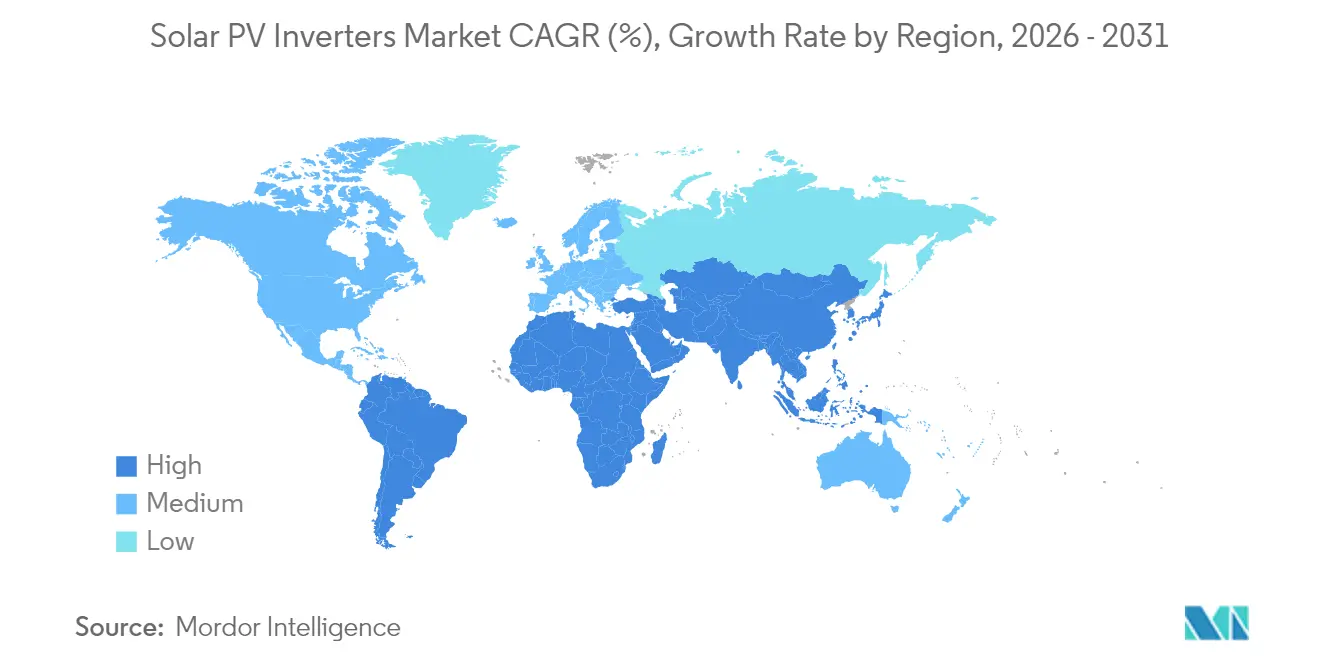

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Solar PV Inverters Market Analysis by Mordor Intelligence

The Solar PV Inverters market size is expected to grow from USD 14.27 billion in 2025 to USD 15.24 billion in 2026 and is forecast to reach USD 21.16 billion by 2031 at 6.79% CAGR over 2026-2031.

The market’s expansion is underpinned by a move from simple DC-to-AC conversion toward smart, grid-forming solutions that safeguard power quality and unlock new revenue streams for owners. Asia-Pacific anchors global demand, yet the Middle East is now the fastest-growing territory as large utility projects intersect with grid-modernization agendas. Robust replacement cycles in Japan, rooftop mandates in India, and higher-voltage designs across the United States and Europe amplify near-term unit volumes, while persistent SiC/IGBT shortages and rising curtailment in China temper the pace of expansion. Despite those headwinds, premium pricing for advanced grid-support functions keeps aggregate revenue upward in the solar PV inverter market [1]GE Vernova, “Introducing 2,000 V Solar Inverter Platform,” gevernova.com.

Key Report Takeaways

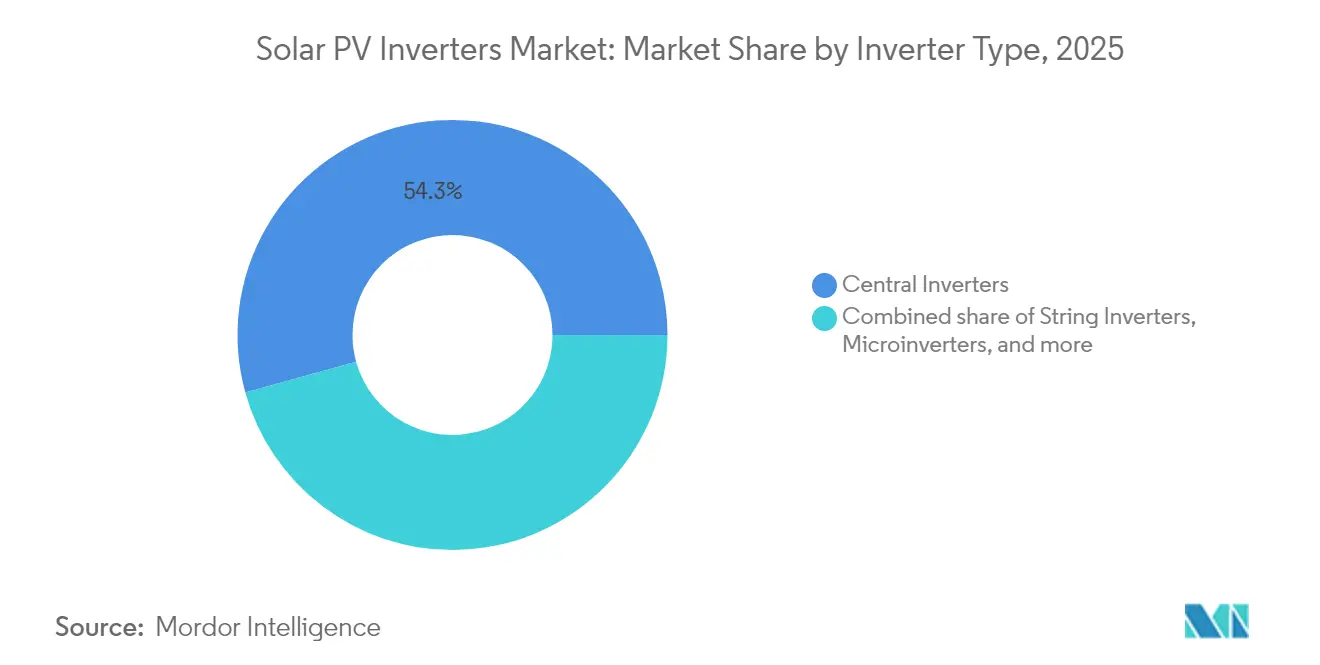

- By inverter type, central systems commanded 54.30% revenue share in 2025, while microinverters are projected to register the fastest 7.96% CAGR by 2031.

- By application, utility-scale installations accounted for 62.25% of the solar PV inverter market size in 2025, while residential is set to grow at a 7.45% CAGR through 2031.

- By phase, three-phase units led with 71.20% of the solar PV inverter market share in 2025; Single-phase is forecasted to post a 7.05% CAGR between 2026 and 2031.

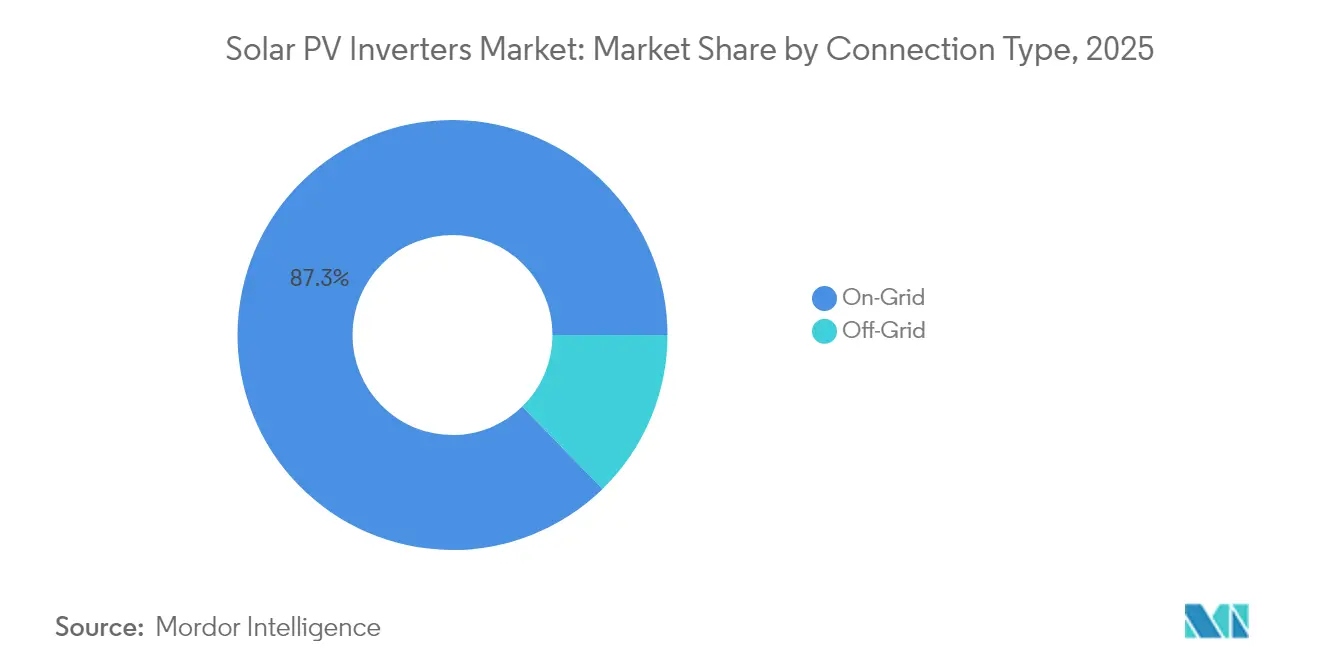

- By connection type, on-grid designs captured 87.30% of revenue in 2025, while off-grid solutions should expand at an 8.32% CAGR to 2031.

- By geography, Asia-Pacific held 54.40% of global shipments in 2025; the Middle East and Africa is the fastest-growing region with a 9.31% CAGR to 2031.

- Company level: the ten largest suppliers collectively controlled a major share of 2024 revenue, reflecting a highly concentrated landscape that raises barriers for new entrants.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Solar PV Inverters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of high-voltage 1 500 V string inverters in utility-scale projects (US, Spain) | +1.2% | Global, with concentration in US and Spain | Medium term (2-4 years) |

| Mandatory rooftop-solar mandates in India's commercial buildings boosting ≤100 kW inverter demand | +0.8% | India, with spillover to Southeast Asia | Short term (≤ 2 years) |

| Aggressive replacement cycle of inverters installed during Japan's 2012-2016 FIT boom | +0.6% | Japan, with lessons for early-adopter markets | Medium term (2-4 years) |

| Integration of advanced grid-support functions lifting ASPs in Europe | +0.9% | Europe, expanding to North America | Long term (≥ 4 years) |

| Growth of hybrid PV-storage solutions driving bidirectional inverters in Australia | +0.7% | Australia, with replication in battery-incentive markets | Medium term (2-4 years) |

| Localization incentives in Brazil encouraging domestic manufacture of central inverters | +0.4% | Brazil, with potential expansion to Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid adoption of high-voltage 1 500 V string inverters in utility-scale projects (US, Spain)

Utility developers increasingly specify 1,500 V—and pilot 2,000 V—DC architectures to lower balance-of-system costs and boost power density. GE Vernova’s 2,000 V platform showcases a 30% output gain that decreases levelized energy costs. This voltage migration renders 1,000 V arrays economically obsolete on new-build sites and spurs retrofit projects, especially where land and grid headroom allow bigger block sizes. Heightened semiconductor demand follows, tightening the supply of SiC devices and elevating the strategic importance of thermal design expertise among leading brands.

Mandatory rooftop-solar mandates in India’s commercial buildings boosting ≤100 kW inverter demand

India’s policy obliges new and existing commercial structures to install rooftop arrays, driving the sustained need for ≤100 kW inverters. Record additions of 4 GW in fiscal 2024 signal the scale of the opportunity [2]Institute for Energy Economics and Financial Analysis, “India Rooftop Solar Update 2024,” ieefa.org. Domestic manufacturers benefit from import-substitution targets embedded in the country’s 110 GW cell-and-module build-out by 2026, reinforcing the local value chain. While implementation gaps remain across several states, standardized installation practices create a template for broader residential uptake.

Aggressive replacement cycle of inverters installed during Japan’s 2012-2016 FIT boom

Feed-in premium rules push Japanese system owners to swap decade-old inverters for units that supply reactive power and follow real-time price signals. Tokyo’s 2025 solar mandate for new buildings accelerates demand for devices capable of voltage regulation, driving premium revenue opportunities. The Japanese cycle offers a blueprint for other mature PV territories where early installations face synchronous aging and stricter grid codes.

Integration of advanced grid-support functions lifting ASPs in Europe

Europe now mandates remote-controlled, smart inverters on new projects. Germany’s Solarspitzen-Gesetz, in force since March 2025, limits feed-in to 60% unless advanced control capability is deployed. SMA’s adoption of 2 kV SiC MOSFETs in its flagship central platform underscores the performance leap required to satisfy those codes. Similar rules in Spain, Italy, and the United Kingdom elevate average selling prices (ASPs) across the regional solar PV inverter market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent shortages & price volatility of high-current SiC/IGBT power modules | -1.4% | Global, with acute impact in premium segments | Short term (≤ 2 years) |

| Rising curtailment in China's northwest dampening central-inverter orders | -0.9% | China, with spillover effects to global pricing | Medium term (2-4 years) |

| Fragmented US interconnection codes inflating certification costs | -0.6% | United States, with indirect impact on global standards | Medium term (2-4 years) |

| Fire-safety concerns on rooftop DC circuits slowing microinverter uptake in Germany | -0.4% | Germany and EU, with potential spread to other markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent shortages & price volatility of high-current SiC / IGBT power modules

SiC wafer supply tightness continues to constrain high-efficiency inverters and amplify bill-of-material costs. Wolfspeed’s financial distress heightens risk perceptions, whereas Infineon’s switch to cost-effective 200 mm SiC wafers signals relief from 2026 onward [3]Infineon Technologies AG, “200 mm SiC Rollout Begins,” infineon.com. European and North American producers, dependent on advanced semiconductors for grid-forming functionality, experience sharper margin compression than vertically integrated Chinese peers able to fall back on silicon alternatives.

Rising curtailment in China’s northwest dampening central-inverter orders

Curtailment in China’s northwest could rise from 2.4% in 2023 to 10% by 2030. Large utility assets face revenue erosion, compelling developers to postpone or resize projects and trim orders for central units. Market-based pricing for renewable electricity, effective June 2025, intensifies competition for grid capacity. A nationwide storage build-out may offset long-range risks, but near-term order books remain vulnerable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Inverter Type: Microinverters Gather Momentum

Central units retained a 54.30% revenue lead in 2025, yet microinverters are forecast to grow at an 7.96% CAGR as module-level electronics move beyond the early-adopter niche. Enphase shipped more than 6.5 million domestic microinverters in 2025, satisfying US localization criteria and underlining the segment’s commercial scale . The solar PV inverter market rewards firms that combine ASIC design, wireless data, and thermal engineering in a miniature footprint. Central architectures now confront flattish demand in China due to curtailment but remain anchored in utility projects elsewhere, especially where plant-level controls and competitive capex remain priorities.

Competitive intensity is pronounced in microelectronics; barriers arise from firmware sophistication and safety certifications rather than raw hardware cost. Consequently, low-price entrants struggle to keep pace with rapid feature rollouts such as rapid shutdown and battery interface modes. Despite robust volume growth, microinverters are not likely to eclipse string platforms before the next decade, keeping the solar PV inverter market diversified by architecture.

By Application: Prosumer Demand Narrows the Gap

Utility plants captured 62.25% of 2025 shipments, reflecting large project pipelines locked under long-term PPAs. Even so, residential systems should expand by 7.45% annually as grid services and net-billing frameworks enhance household economics. India’s Pradhan Mantri Surya Ghar program targets 30 GW of rooftop arrays by March 2027, while Australia’s battery add-on trend lifts attachment rates. Commercial rooftops ride India’s rooftop mandate wave but face cautious finance terms in other regions that stretch payback timelines.

Prosumers increasingly value bidirectional capability and island-mode resilience, prompting inverter OEMs to integrate battery control logic. The resulting ASP uplift compensates for slower macro installation growth, supporting aggregate revenue progression inside the solar PV inverter market. Utility developers, meanwhile, focus on 1,500 V and 2,000 V platforms, coupling them with STATCOM-like functionalities to meet stricter grid-code compliance.

By Phase: Residential Scale Fuels Single-Phase Uptake

Three-phase machines accounted for 71.20% of 2025 revenue, anchored in commercial rooftops and utility installations. Single-phase units, however, track a 7.05% CAGR as household volumes climb in Europe, India, and Australia. Government approval of balcony solar kits up to 800 W in Germany illustrates how plug-and-play designs create grassroots capacity growth. Looking ahead, larger US homes and Japanese complexes may warrant quasi-three-phase solutions, blurring historical boundaries between the two categories.

Cost-downs in digital control boards and power stages allow single-phase products to incorporate advanced grid-forming algorithms. This capability reduces voltage flicker, boosting acceptance among distribution network operators. OEMs that standardize modular platforms across both phase variants should capture cross-segment synergies while keeping the bill of materials in check.

By Connection Type: Hybrid Flexibility Expands Off-Grid Niches

On-grid architectures maintained an 87.30% share in 2025, enabled by net metering and feed-in frameworks. Off-grid solutions, projected to grow 8.32% annually, see traction in Sub-Saharan electrification and remote mining camps that demand autonomy from weak grids. Falling lithium-ion costs and ruggedized inverter-charger combos simplify deployment, although maintenance and upfront capex still hinder widespread uptake.

Hybrid systems that switch seamlessly between grid-tied and islanded modes straddle both segments. They satisfy backup power expectations in outage-prone regions such as California while capturing demand-response revenue when grid-connected. Consequently, inverter firmware roadmaps prioritize multi-mode capability as a baseline rather than an optional upgrade, reinforcing value capture inside the solar PV inverter market.

Geography Analysis

Asia-Pacific generated 54.40% of 2025 shipments, underpinned by China’s vertically integrated supply chain and India’s policy-driven rooftop push. While China’s new market-based tariff regime may slow greenfield installations, volume resilience stems from retrofits that embed storage and higher-voltage strings. India’s manufacturing capacity, set to reach 110 GW by 2026, tightens domestic procurement loops and shields the local solar PV inverter market from import volatility, although regional disparities in regulatory execution temper immediate gains.

The Middle East, clocking the quickest 9.31% CAGR through 2031, aligns gigawatt-scale projects with economic diversification blueprints. Harsh desert conditions drive demand for high-derating-temperature designs, opening niches for European OEMs specializing in sealed cubicle solutions. Grid-reinforcement efforts in Saudi Arabia and the United Arab Emirates elevate low-voltage ride-through and reactive-power management specifications, pressing vendors to certify products against stricter utility benchmarks. North America and Europe operate in a mature install base where replacement and retrofit cycles dominate incremental demand. The US Inflation Reduction Act’s domestic content credits accelerate localized production, with Texas, South Carolina, and Arizona facilities targeting annual output well above 30 GW by 2026. Europe’s renewable penetration surpassing 50% in markets such as Germany and Spain raises the value of grid-forming features, allowing vendors to pass through higher ASPs even as new-build volumes plateau.

Competitive Landscape

Market concentration is moderately consolidated: the ten largest suppliers commanded a major global revenue share in 2024. Chinese firms capitalize on material cost advantages and end-to-end vertical integration to dominate high-volume, price-sensitive segments. Conversely, European and American brands differentiate in firmware sophistication and compliance with domestic content stipulations. SolarEdge, for instance, produced its 250,000th unit at its Austin site in June 2025, underscoring localized scale-up momentum.

Technology rivalry centers on grid-forming control loops, bidirectional interfacing, and cybersecure remote-update capability. SMA’s integration of 2 kV SiC MOSFETs displays a leap toward ultra-high voltage solutions, while GE Vernova’s 2,000 V range targets balance-of-system savings for large developers. Enphase’s microelectronics pedigree delivers competitive moats in firmware, ASICs, and proprietary communication protocols, complicating fast-follower strategies from low-cost entrants.

M&A activity continues as inverter specialists seek portfolio breadth. Generac’s acquisition of Chilicon Power in 2024 provided an immediate pathway into microinverter hardware and monitoring. Hoymiles’ decision to open a Mexican plant the same year illustrates strategic hedging against United States trade uncertainties. Prospective newcomers confront a dual hurdle of steep certification expenses and a global value chain in which established vendors already occupy the lion’s share of utility pre-qualification lists, reinforcing the solar PV inverter market’s high entry barriers.

Solar PV Inverters Industry Leaders

Huawei Technologies Co., Ltd.

Sungrow Power Supply Co., Ltd.

SMA Solar Technology AG

SolarEdge Technologies Inc.

Enphase Energy Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: SolarEdge reached 250,000 inverters produced at its Austin plant, creating over 1,000 jobs and strengthening United States supply resilience.

- May 2025: Enphase shipped 6.5 million US-made IQ microinverters and 50 MWh of batteries from domestic factories, covering 80% of its total 2025 shipments.

- April 2025: ROHM announced SMA Solar’s use of 2 kV SiC MOSFETs in the Sunny Central FLEX platform, boosting large-scale array efficiency

- September 2024: GE Vernova introduced a 2,000 V utility inverter; the pilot system in North America raised plant output by 30%.

Global Solar PV Inverters Market Report Scope

A solar PV inverter is a power inverter that converts electricity in direct current (DC) output from a photovoltaic (PV) solar panel into alternating current (AC) at utility frequency. This can be used for residential and commercial electrical grids or by a local off-grid electrical network, such as microgrids.

The solar PV inverters market is segmented by inverter type, application, and geography. By inverter type, the market is segmented into central inverters, string inverters, and micro-inverters. By application, the market is segmented into residential, commercial and industrial, and utility-scale. The report also covers the market size and forecasts for solar PV inverters across major regions. For each segment, the market sizing and forecasts have been done based on revenue (value in USD billion).

By Inverter Type

| Central Inverters |

| String Inverters |

| Microinverters |

| Hybrid/Battery-Ready Inverters |

By Phase

| Single-Phase |

| Three-Phase |

By Connection Type

| On-Grid |

| Off-Grid |

By Application

| Residential |

| Commercial and Industrial |

| Utility-Scale |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Inverter Type | Central Inverters | |

| String Inverters | ||

| Microinverters | ||

| Hybrid/Battery-Ready Inverters | ||

| By Phase | Single-Phase | |

| Three-Phase | ||

| By Connection Type | On-Grid | |

| Off-Grid | ||

| By Application | Residential | |

| Commercial and Industrial | ||

| Utility-Scale | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Thailand | ||

| Indonesia | ||

| Vietnam | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the solar PV inverter market in 2026?

The solar PV inverter market stands at USD 15.24 billion in 2026.

How fast will the market grow over the next five years?

It is projected to expand at a 6.79% CAGR, reaching USD 21.16 billion by 2031.

Which region leads global demand?

Asia-Pacific holds 54.40% of shipments due to China’s manufacturing scale and India’s rooftop mandates.

What inverter topology is gaining share fastest?

Microinverters exhibit the quickest growth at a 7.96% CAGR, propelled by residential and distributed generation uptake.

How concentrated is the industry?

The ten largest suppliers account for 60% of 2024 revenue, indicating high concentration with significant entry barriers.

What is the main technological trend shaping product design?

Grid-forming and bidirectional capabilities that support energy storage and ancillary services dominate current R&D roadmaps.

Page last updated on: