Sodium-ion Battery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

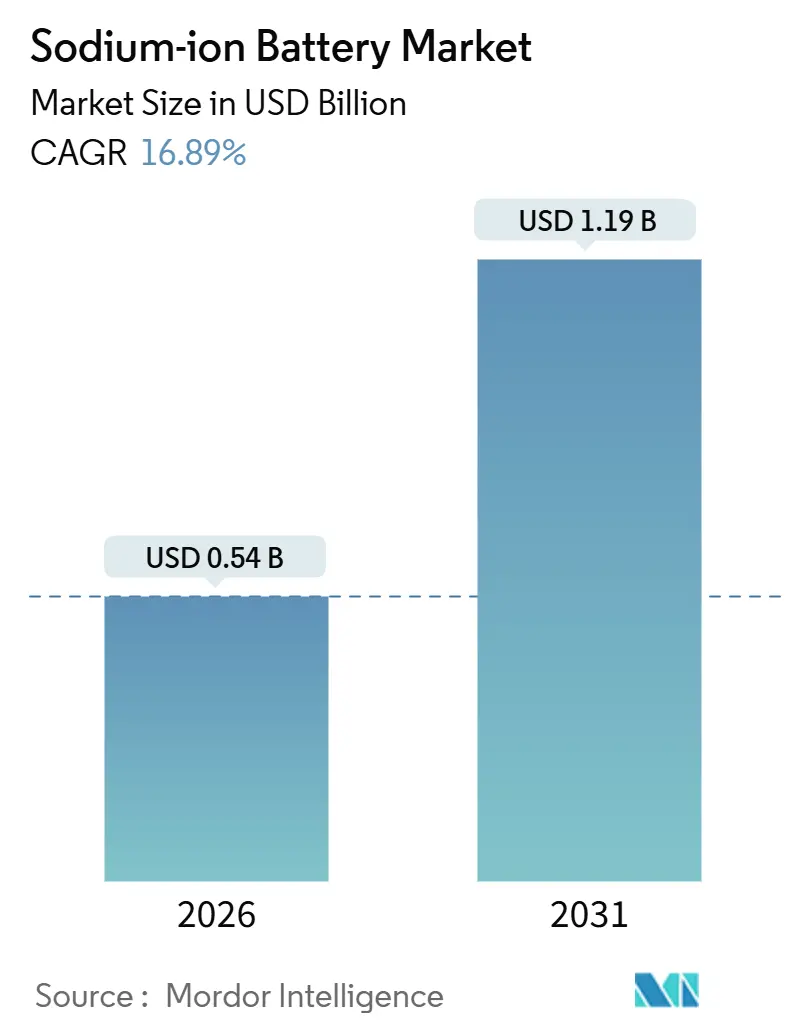

| Market Size (2026) | USD 0.54 Billion |

| Market Size (2031) | USD 1.19 Billion |

| Growth Rate (2026 - 2031) | 16.89% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sodium-ion Battery Market Analysis by Mordor Intelligence

The Sodium-ion Battery Market size is estimated at USD 0.54 billion in 2026, and is expected to reach USD 1.19 billion by 2031, at a CAGR of 16.89% during the forecast period (2026-2031).

Broad-based cost pressure on lithium, stringent European sustainability rules, and China’s industrial policy are steering cell makers toward sodium chemistries that promise cheaper raw materials, shorter supply chains, and lower embedded carbon. Rapid policy-backed grid tenders in China, coupled with Europe’s battery passport mandate, have accelerated pilot deployments by almost two years, compressing the learning curve normally associated with new chemistries. Automakers are hedging lithium exposure by earmarking low-range city cars for sodium packs, while utilities view four-hour discharge systems as a hedge against lithium carbonate price swings. Meanwhile, breakthroughs in Prussian-blue cathodes are closing the performance gap with lithium iron phosphate, particularly for two-wheelers and urban delivery fleets.

Key Report Takeaways

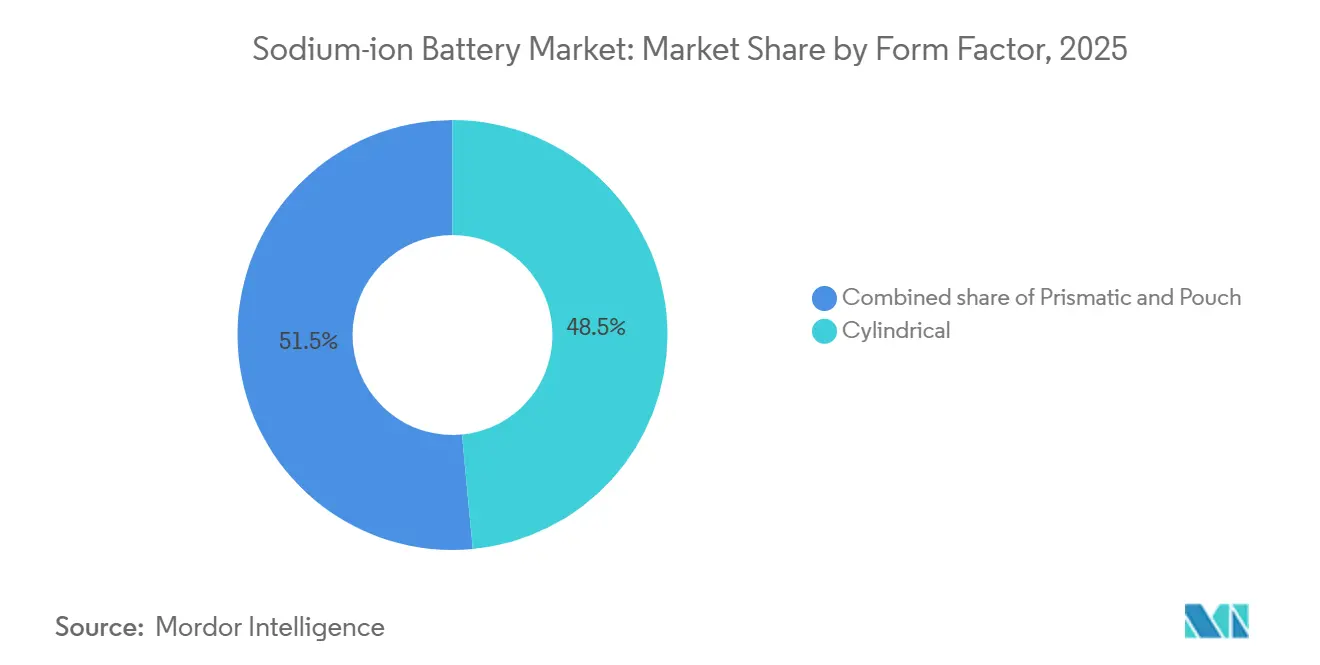

- By form factor, cylindrical cells captured 48.5% of the sodium-ion battery market size in 2025, whereas pouch formats are advancing at a 22.0% CAGR to 2031.

- By application, stationary energy storage held 71.8% of the sodium-ion battery market share in 2025, while transportation is projected to post a 19.8% CAGR through 2031.

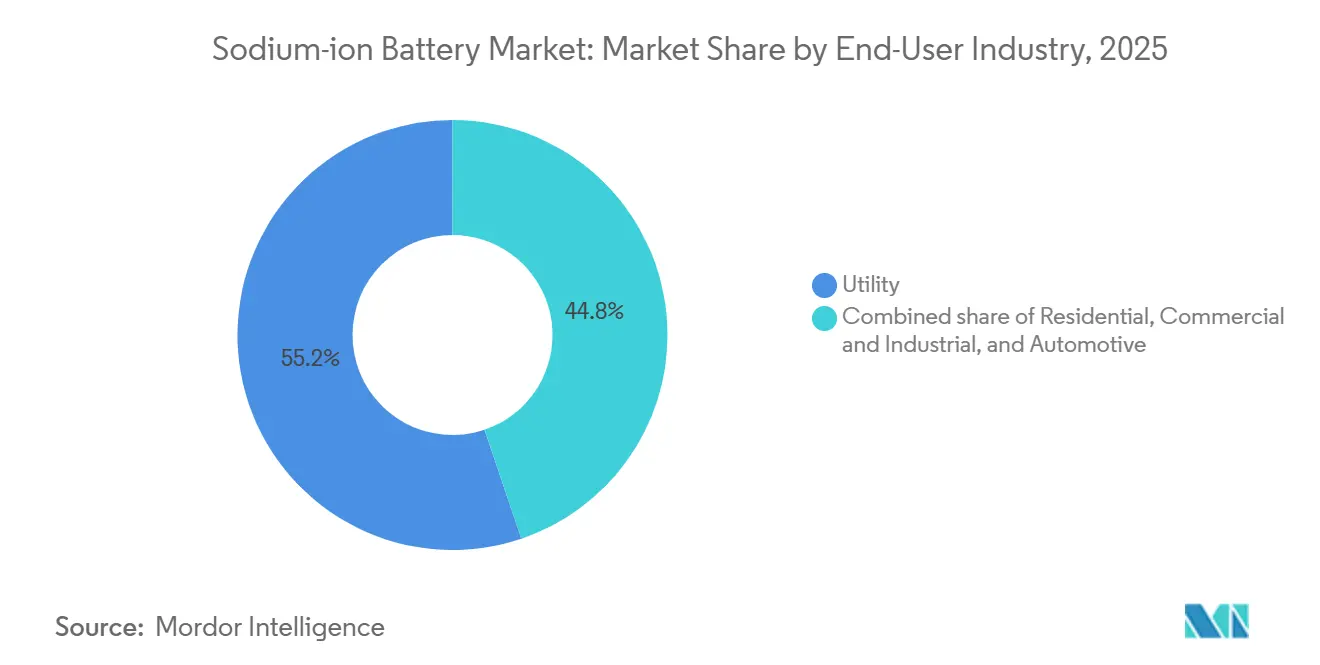

- By end-user industry, utilities commanded 55.2% of the sodium-ion battery market share in 2025, yet automotive demand is forecast to expand at a 23.3% CAGR through 2031.

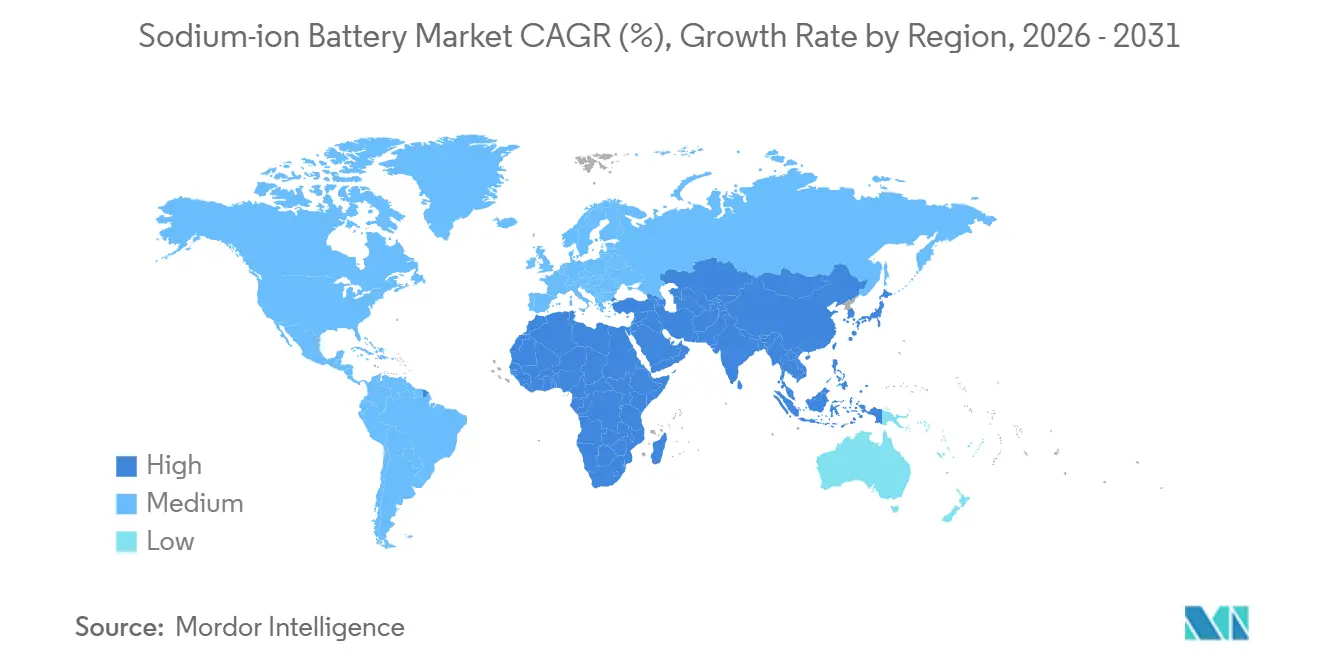

- By geography, Asia-Pacific led with 45.6% of the sodium-ion battery market size in 2025 and is expected to grow at a 19.5% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sodium-ion Battery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| China’s policy-backed 100+ MWh grid tenders | +3.5% | China, ASEAN | Medium term (2-4 years) |

| European EV OEMs pivot to sodium-ion for low-range cars | +2.8% | Germany, France, Nordics | Medium term (2-4 years) |

| LFP cathode cost inflation pushes packs below USD 70/kWh | +4.2% | Global | Short term (≤ 2 years) |

| Prussian-blue cathodes enable 15-minute charge for India two-wheelers | +2.5% | India, Southeast Asia | Medium term (2-4 years) |

| Cold-climate resilience drives Nordic storage subsidies | +1.8% | Sweden, Norway, Finland | Long term (≥ 4 years) |

| CATL-utility joint-venture plants secure vertical supply | +3.0% | China, Europe, North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

China’s Policy-Backed 100 + MWh Grid Tenders Accelerate Domestic Demand

Provincial grid operators in Guangxi and Jiangsu awarded more than 100 MWh of sodium-ion contracts during 2025 after Beijing labeled the chemistry “strategic” for energy storage.[1]CATL, “Naxtra Product Launch Press Release,” catl.com A 100 MWh system installed by HiNa Battery in Nanning delivered 92% round-trip efficiency across 5,000 cycles and met a levelized cost of storage below USD 0.10 per kWh. Tenders were fast-tracked to cushion utilities from lithium carbonate volatility that spiked to USD 80,000 per tonne in 2022. Domestic soda-ash reserves at USD 300 per tonne underpin price stability, while China Development Bank offers preferential loans that shave project financing costs. By anchoring multi-gigawatt-hour demand, policymakers have shortened commercial ramp-up timelines by close to two years.

European EV OEMs Switching Low-Range Models to Sodium-Ion to Meet EU Battery Regulation

The European Union’s Battery Regulation requires carbon-footprint declarations and recycled-content thresholds from 2027, nudging OEMs toward cobalt- and nickel-free sodium recipes.[2]European Commission, “Regulation (EU) 2023/1542 on Batteries,” europa.eu Stellantis and Volkswagen are piloting sodium packs for A- and B-segment cars, citing a 35% to 40% drop in embedded carbon compared with NMC811 cells. Northvolt built a 160 Wh/kg prototype with Altris and is adapting prismatic formats at Skellefteå for Volvo’s next city car line. Simpler supply chains reduce digital-passport compliance costs, and OEMs view sodium chemistry as a hedge should lithium exports tighten in Chile or Australia.

LFP Cathode Cost Inflation Narrows Pack-Level Cost Gap Below USD 70/kWh

Lithium iron phosphate prices rose from USD 12/kg in early 2024 to USD 18/kg by mid-2025 amid mining limits in Sichuan, slashing LFP’s cost advantage. CATL’s 2025 Naxtra cell reached a bill-of-materials of USD 55 per kWh at pack level, roughly 20% below comparable LFP systems once leaner thermal management is counted. Utilities in Spain and California model parity with LFP at four-hour durations, a sweet spot for solar load-shifting. Lower voltage also permits lighter busbars, trimming pack weight and balance-of-plant costs.

Prussian-Blue Breakthrough Enables 15-Minute Charge for India Two-Wheelers

A 2024 study at Jawaharlal Nehru Centre showed Prussian-blue cathodes holding 15-minute charge cycles across 3,000 cycles. Altris commercialized a Prussian-white variant in 2025, supplying Indian assemblers serving the 12 million-unit annual electric-rickshaw market.[3]Altris AB, “Prussian-White Commercialization Announcement,” altris.se Fast recharge dovetails with India’s battery-swapping model, cutting spare-pack requirements by 40% per station. Government production incentives worth USD 2.4 billion list sodium-ion as eligible, accelerating joint ventures between local OEMs and Chinese cell suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 30% energy-density penalty vs. LFP in long-range EVs | -2.5% | North America, Europe premium EVs | Medium term (2-4 years) |

| Absence of standardized BMS protocols adds integration cost | -1.8% | Global | Short term (≤ 2 years) |

| Nascent recycling ecosystem complicates EU battery passport | -1.2% | Europe | Medium term (2-4 years) |

| Metallic-sodium deposition risk above 3.7 V | -0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

-30% Energy-Density Penalty vs. LFP in Long-Range EVs

Sodium cells reach 140–160 Wh/kg, roughly 30% short of LFP’s 180–200 Wh/kg, forcing heavier packs and limiting the chemistry to city cars, vans, and stationary roles. Tesla targets 300 Wh/kg by 2027 for its 4680 cell, highlighting the gulf that sodium must close. Heavier racks inflate cabling and fire-suppression needs by about 15% in grid storage. European automakers confine sodium packs to A-segment models that formed just 12% of 2025 EV sales. Antimony-doped anodes show promise in labs but remain cost-prohibitive, keeping density ceilings static through 2031.

Absence of Standardized BMS Protocols Raises Integration Costs

IEC 62619 still lacks sodium-ion guidelines, forcing bespoke safety tests for every pack.[4]International Electrotechnical Commission, “IEC 62619 Battery Safety Standard,” iec.ch Custom firmware adds USD 0.5–1 million in non-recurring engineering per product line, deterring Tier-2 assemblers. Sodium’s 3.1 V nominal voltage demands re-worked bus architecture in vehicles, extending platform integration by up to 18 months. Natron’s attempt to launch a cross-chemistry BMS ended with its 2025 pause, removing a key standardization advocate. Until SAE issues a J2464 variant, redundant validation will persist.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form Factor: Pouch Gains Ground in Automotive

Cylindrical formats held 48.5% of the sodium-ion battery market size in 2025, benefiting from repurposed lithium winding lines. Pouch cells are set for a 22.0% CAGR, propelled by automakers chasing volumetric efficiency under vehicle floors. Prismatic modules, roughly 30%, dominate megawatt-scale projects where standardized 280 Ah blocks simplify racking. CATL’s Naxtra range offers both 18650 cylinders for home storage and pouches for scooters, proving chemistry flexibility.

Stacked pouch cells let designers exploit irregular chassis spaces in A-segment cars, a decisive edge where every cubic centimeter counts. Prismatic dominance in China’s grid market owes to hot-swappable modules that slash field servicing downtime. Cylindrical cost leadership is fading as automated stacking lines mature; by 2031, market preference may converge on pouch and prismatic as automotive volume overtakes stationary installations.

By Application: Stationary Storage Anchors Revenue, Transportation Surges

Stationary energy storage accounted for 71.8% of the sodium-ion battery market share in 2025, anchored by Chinese grid tenders and Spanish solar-plus-storage contracts. Transportation, though smaller at 18%, is projected to grow 19.8% annually, narrowing the gap by 2031. CATL’s TENER Stack, a 9 MWh container launched in 2025, validated utility economics with 92% round-trip efficiency across a 15-year warranty. Two-wheeler electrification in India, backed by USD 2.4 billion in incentives, will bring sodium packs into 12 million vehicles per year by 2030. Consumer electronics remain niche because 350 Wh/L volumetric density trails lithium-ion’s 450 Wh/L, thickening handset chassis. Industrial backup power claims 7% of revenue, leveraging Natron cells certified for 50,000 cycles before the company’s 2025 pause. Marine auxiliaries in Norway and South Korea form a 3% niche, trading weight for inherent fire safety in port equipment.

Transportation’s climb will recalibrate the sodium-ion battery market size distribution by 2031 as battery-swapping ecosystems monetize 15-minute recharge capability. Utilities are already stretching power-purchase agreements to 15 years to smooth higher capital outlays. Residential demand, concentrated in Scandinavia, is rising due to fire-safety and cold-weather performance but lacks broad installer networks. Over time, the segment mix will tilt toward transportation and home storage, trimming utilities’ share below 45%, yet retaining a cost-sensitive base that stabilizes manufacturing plant utilization.

By End-User Industry: Automotive Outpaces Utility Growth

Utility buyers commanded 55.2% of the sodium-ion battery market share in 2025, fueled by multi-gigawatt-hour Chinese and Spanish procurement. Automotive users, 22% in 2025, will grow at 23.3% CAGR on the back of two-wheeler fleets in India and European city cars. Residential users held a 12% share, largely in cold Nordic regions, subsidizing fire-safe chemistries. Commercial and industrial backup applications made up 11%, favoring cycle life over energy density.

Automotive demand will draw parity with utilities around 2031 as Prussian-blue cathodes mature, while residential uptake depends on turnkey products from established inverter brands. Utilities are stretching contract terms, improving project IRRs, and absorbing the 15% upfront premium over LFP. Commercial buyers prize 50,000-cycle cells for peak shaving, a segment that may revive if Natron or successors restart high-cycle factories. The end-user mosaic will remain dynamic, but automotive and residential slices will expand fastest.

Geography Analysis

Asia-Pacific controlled 45.6% of the sodium-ion battery market share in 2025 and is forecast to rise at a 19.5% CAGR to 2031. China’s gigawatt-hour factories and India’s two-wheeler boom underpin demand. HiNa’s 100 MWh project in Nanning showcased grid-scale viability, and CATL sealed multi-year offtake deals with Jiangsu and Shandong grids that together host 18% of China’s renewables. India’s USD 2.4 billion incentive scheme accelerates partnerships between domestic OEMs and Faradion’s Jamnagar plant, scheduled for 2026 start-up. Japan and South Korea explore sodium for marine auxiliaries, while Thailand and Indonesia emerge as assembly hubs for regional scooter markets.

Europe captured around 28% share in 2025, led by Nordic cold-climate adoption and residential-storage subsidies. Sweden’s SEK 80 million grant to Altris and Norway’s NOK 5,000 per kWh rebate highlight policy pull. Germany and France are piloting sodium for solar firming ahead of 2027 carbon footprint rules. Northvolt works on prismatic cells for Volvo’s city cars, adding domestic capacity. Southern markets like Spain and Italy depend on imports, limiting early penetration.

North America held a roughly 18% share in 2025, concentrated in utility storage and data-center backup. Peak Energy’s 2 GWh Colorado plant aims for 2027 output with Southern Company and Duke Energy offtake. Natron’s North Carolina gigafactory plan stalled after its 2025 shutdown, leaving supply gaps. Eligibility for Inflation Reduction Act credits remains pending Department of Energy guidance. Canada pilots mini-grids in Alberta’s oil sands, and Mexico assesses rural electrification schemes. South America and the Middle East & Africa combined for under 9%, with Brazil and South Africa testing mini-grids where lithium logistics prove costly.

Competitive Landscape

Moderate concentration characterizes the sodium-ion battery market: CATL, BYD, and HiNa Battery controlled an estimated 55–60% of global capacity in 2025. Incumbent lithium players repurpose existing lines, slashing capex per GWh and squeezing standalone startups. CATL’s USD 500 million supplier-financing program secures sodium-carbonate and hard-carbon inputs, imitating its lithium strategy.

Faradion, purchased by Reliance in 2024, is building a Jamnagar gigafactory that integrates electrode coatings with petrochemical feedstocks, targeting a 10–12% bill-of-materials cut. Peak Energy de-risked its Colorado plant by locking 500 MWh of utility offtakes before groundbreaking. Altris and Polarium target white-space in cold-climate home storage, leveraging Prussian-white cathodes that tolerate −30 °C without heaters.

Technology differentiation centers on cathode innovation: Prussian-blue offers fast charge and long life, yet scaling synthesis remains a hurdle. Altris patented a low-temperature route that trims powder costs 30%, potentially unlocking mass scooter markets. Competitive pressure is set to climb after 2028 if LG Energy Solution and Samsung SDI execute sodium hedging strategies. Smaller firms may consolidate, license IP, or exit under margin compression.

Sodium-ion Battery Industry Leaders

Faradion Limited

HiNa Battery Technology Co. Ltd.

Contemporary Amperex Technology Co. Limited

Altris AB

Natron Energy Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: CATL unveiled its new sodium-ion battery brand “Naxtra” with an energy density of 175 Wh/kg, set to enter mass production in December 2025.

- February 2025: Trentar Energy Solutions partnered with KPIT Technologies to commercialise sodium-ion batteries in India through a 3 GWh manufacturing commitment targeting electric two-wheelers.

- November 2024: BYD launched a sodium-ion grid-scale BESS with 2.3 MWh capacity per 20-foot container, aimed at stationary projects that prioritise cost and longevity.

- August 2024: Natron Energy secured a USD 1.4 billion investment to construct a sodium-ion factory in North Carolina focused on Prussian-Blue cells for data centres and renewable storage.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, we define the sodium-ion battery market as all room-temperature rechargeable cells in which sodium ions shuttle between layered oxide or Prussian-blue cathodes and hard-carbon or similar anodes, delivered in cylindrical, prismatic, or pouch form and sold for stationary energy storage, transportation, industrial backup, and consumer devices. Our study tracks factory shipments, revenues, and average selling prices from 2020 through 2030.

Scope Exclusion: We exclude high-temperature molten-salt sodium-sulfur systems and early-stage hybrid chemistries that are not yet commercially shipped.

Segmentation Overview

- By Form Factor

- Cylindrical

- Prismatic

- Pouch

- By Application

- Stationary Energy Storage

- Transportation

- Consumer Electronics

- Industrial Backup Power

- Marine and Others

- By End-User Industry

- Utility

- Residential

- Commercial and Industrial

- Automotive

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Spain

- Nordic Countries

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview sodium-ion cell makers, ESS integrators, EV drivetrain engineers, and regional energy-policy officials across Asia-Pacific, Europe, and North America. These conversations validate capacity utilization, emerging demand pools, and price road maps that secondary data alone cannot capture.

Desk Research

We start with public datasets from bodies such as the International Energy Agency, U.S. Energy Information Administration, EUROBAT, China's MIIT, and Eurostat, which give production, trade, and deployment signals. Company 10-Ks, investor decks, patent filings screened through Questel, and grid-storage tenders pulled via Tenders Info help us benchmark cost curves and project pipelines. D&B Hoovers, Dow Jones Factiva, and peer-reviewed journals then anchor supplier revenues, cathode breakthroughs, and policy timelines. This list is illustrative; many other sources are consulted to cross-check figures and fill smaller gaps.

Market-Sizing & Forecasting

Our model begins with a top-down reconstruction of global sodium-ion demand by mapping installed stationary storage (MWh) and entry-level EV production, then applying chemistry-specific penetration rates. Select bottom-up roll-ups of major suppliers' shipment disclosures and sampled ASP x volume checks test and adjust totals. Key variables include sodium carbonate feedstock cost trends, average cell energy density, policy-linked storage targets, sub-1 MWh community microgrid tenders, and EV battery-pack size migration. Multivariate regression projects each variable to 2030. Gaps where supplier data are missing are bridged with region-weighted industry averages reviewed during expert calls.

Data Validation & Update Cycle

Before release, our analysts rerun anomaly checks, reconcile currency conversions, and obtain a second sign-off from a senior reviewer. The model refreshes annually, with interim updates if policy shifts or capacity announcements move the baseline.

Why Mordor's Sodium ion Battery Baseline Is Highly Credible

Published estimates often differ, and we acknowledge that methodology, scope, and update cadence drive these gaps. Some outlets mix molten-salt NaS units with room-temperature cells, others roll announced capacity into revenue too early, and a few freeze exchange rates for the whole horizon; such choices shift totals materially.

Key gap drivers include inclusion of high-temperature chemistries, counting contracted but undelivered projects, and assuming aggressive price erosion without supplier confirmation, whereas Mordor keeps to shipped volumes, validated ASP paths, and yearly currency re-baselining.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.47 B (2025) | Mordor Intelligence | - |

| USD 0.67 B (2025) | Global Consultancy A | Includes NaS cells and pipeline capacities |

| USD 1.47 B (2024) | Industry Journal B | Applies blanket ASP decline and mixed chemistry scope |

| USD 0.37 B (2024) | Trade Journal C | Uses export value only, omits domestic deployments |

The comparison shows that when scope is tightened to commercial room-temperature cells and prices are grounded in supplier disclosures, Mordor delivers a balanced, transparent baseline that decision-makers can confidently trace back to explicit variables and repeatable steps.

Key Questions Answered in the Report

How large is the sodium-ion battery market in 2026?

It reached USD 545.64 million and is projected to expand at a 16.89% CAGR through 2031.

Which segment uses the most sodium-ion batteries today?

Stationary energy storage commanded 71.8% revenue in 2025 thanks to Chinese and Spanish grid projects.

What limits sodium-ion adoption in long-range electric cars?

A 30% lower energy density versus lithium iron phosphate makes packs heavier, restricting the chemistry to sub-300 km duty cycles.

Why are Nordic countries early adopters of sodium-ion home storage?

Cells retain over 80% capacity at −20 °C and reduce fire risk in wooden homes, qualifying for generous subsidies.

Which companies dominate global sodium-ion capacity?

CATL, BYD, and HiNa Battery together controlled about 55–60% of worldwide capacity in 2025.

Page last updated on: