SNP Genotyping Market Size and Share

Market Overview

| Study Period | 2023 - 2031 |

|---|---|

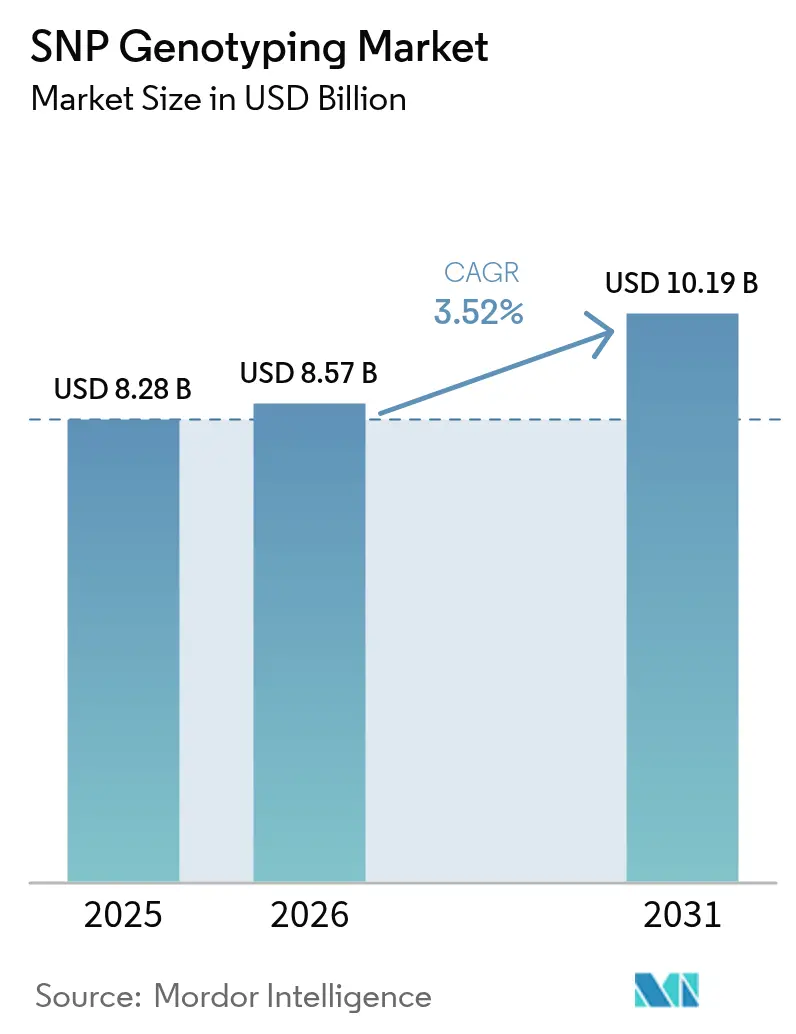

| Market Size (2026) | USD 8.57 Billion |

| Market Size (2031) | USD 10.19 Billion |

| Growth Rate (2026 - 2031) | 3.52% CAGR |

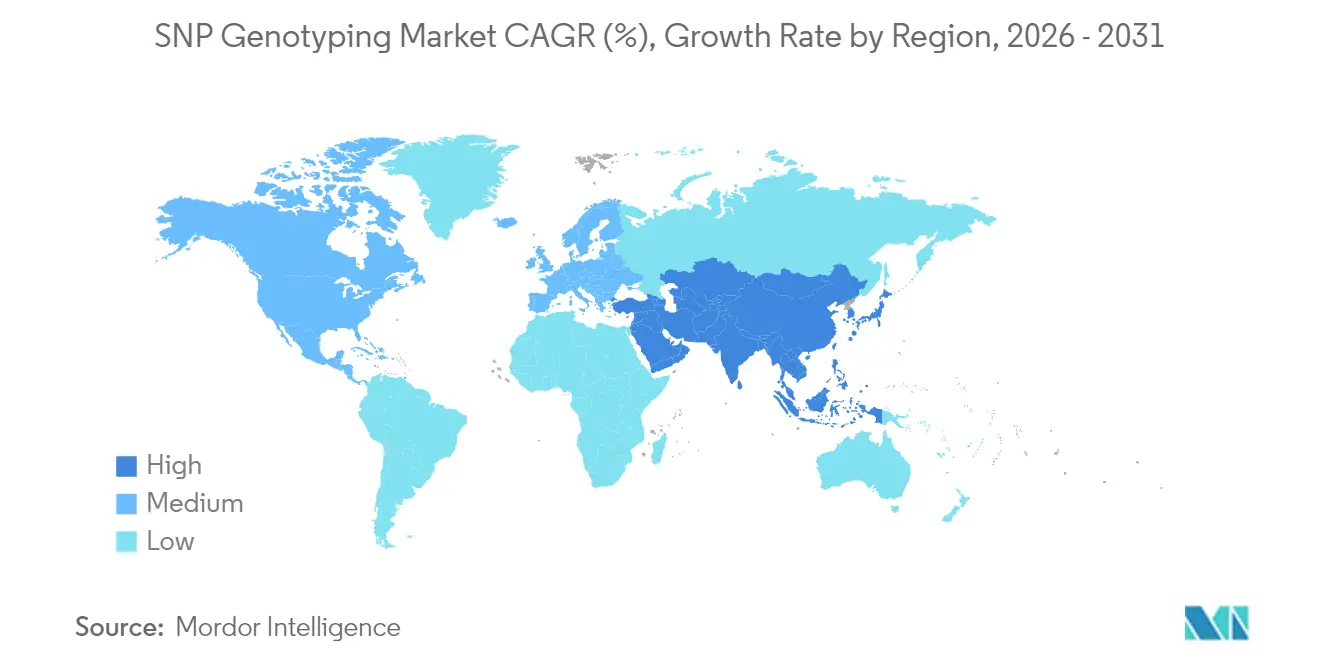

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

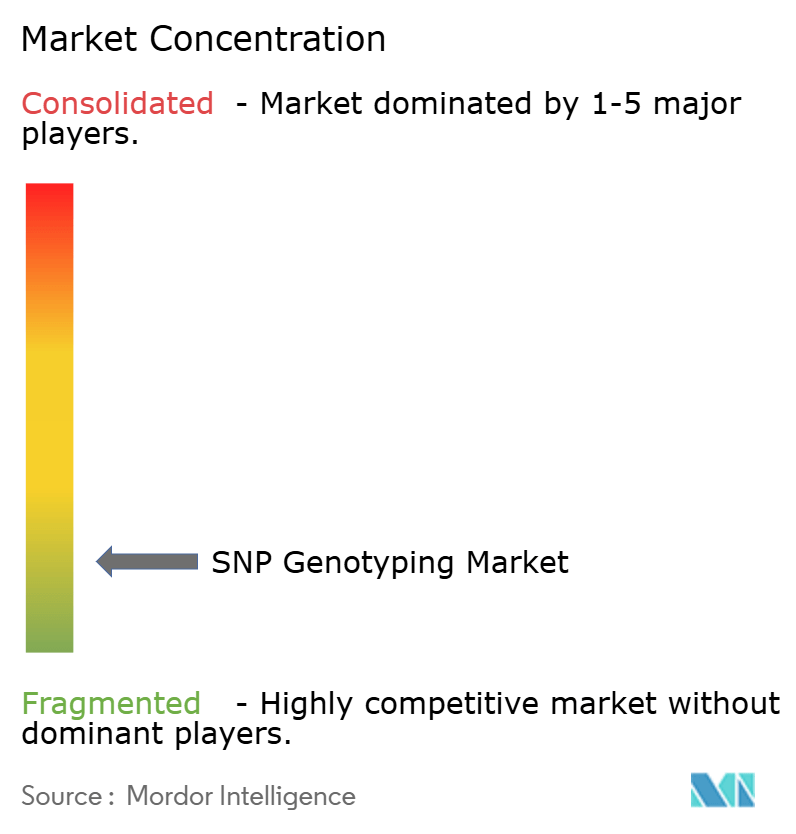

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

SNP Genotyping Market Analysis by Mordor Intelligence

The SNP genotyping market size in 2026 is estimated at USD 8.57 billion, growing from 2025 value of USD 8.28 billion with 2031 projections showing USD 10.19 billion, growing at 3.52% CAGR over 2026-2031. Falling next-generation sequencing (NGS) costs, wider adoption of companion diagnostics, and government-backed population genomics projects underpin this measured expansion. The steady growth signals a maturing competitive environment in which platform innovation, cloud analytics, and AI-enabled automation provide differentiation levers. Pharma demand is rising as more than 30 active collaborations link drug pipelines to high-throughput SNP panels, while agrigenomics and direct-to-consumer (DTC) wellness tests diversify revenue streams. However, persistent bioinformatics talent shortages and evolving privacy regulations temper short-term upside.

Key Report Takeaways

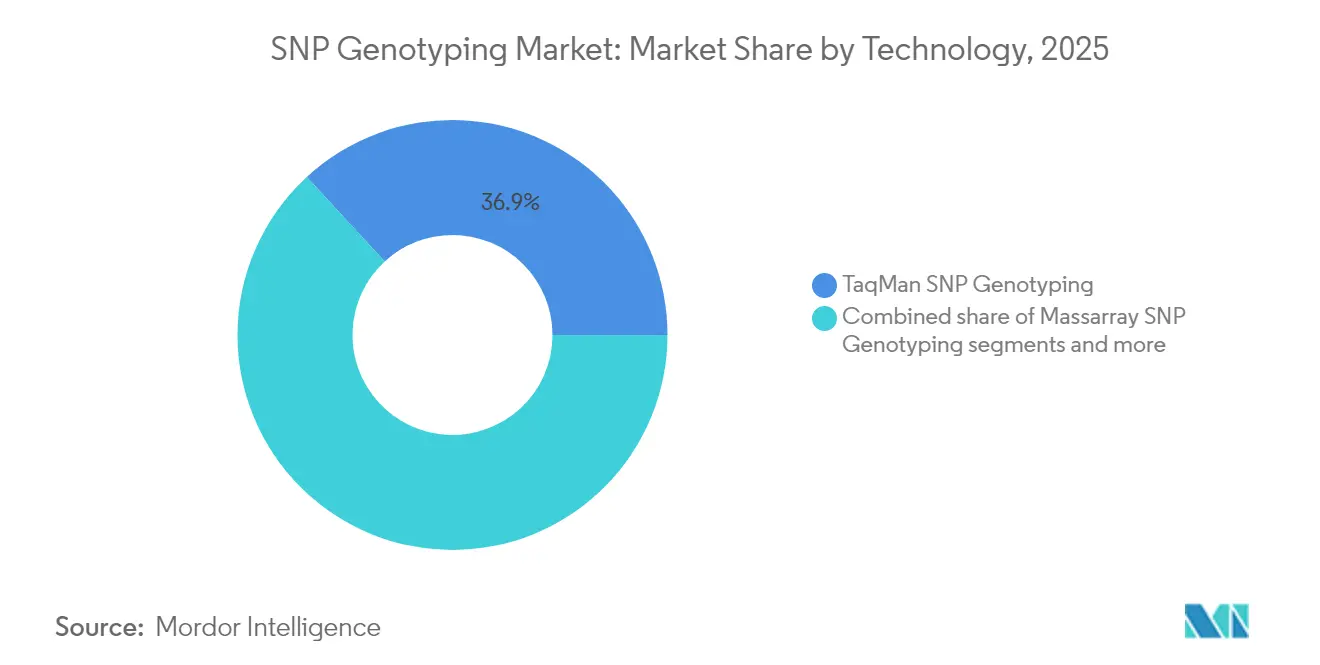

- By technology, TaqMan captured 36.85% of SNP genotyping market share in 2025, whereas other technologies are advancing at a 4.08% CAGR through 2031.

- By product type, reagents & kits commanded 32.78% share of the SNP genotyping market size in 2025, while software & services are projected to expand at a 3.74% CAGR between 2026-2031.

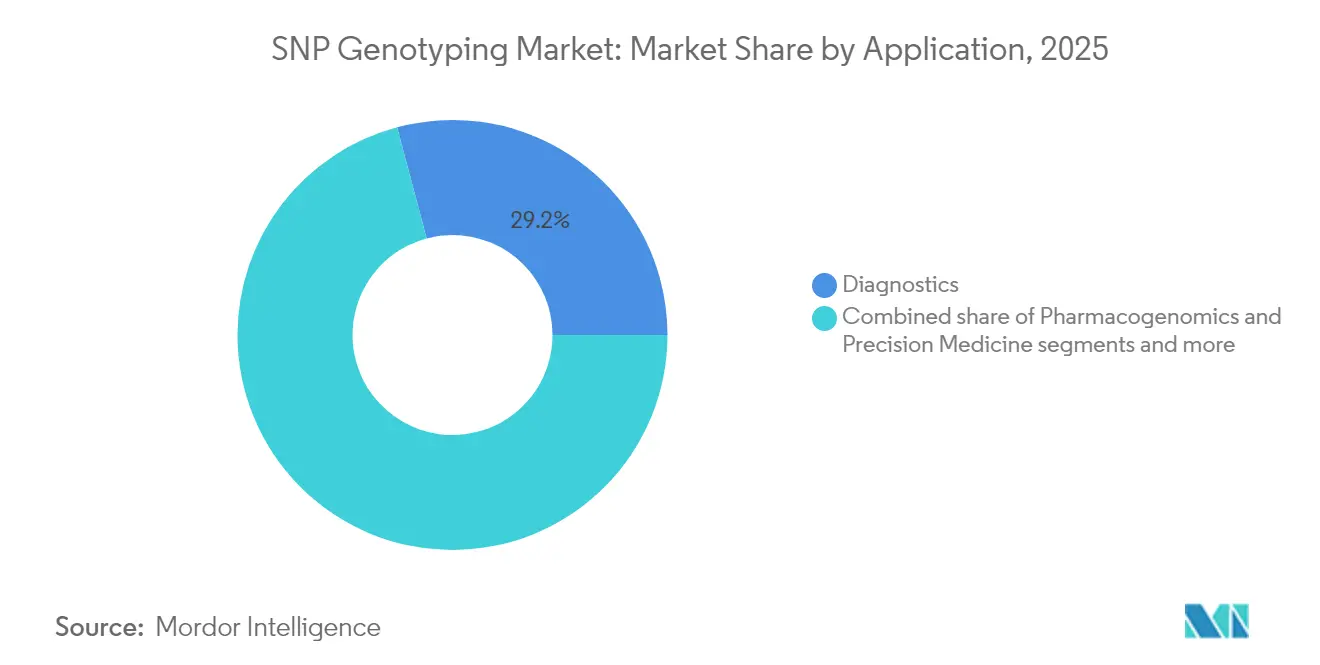

- By application, diagnostics yielded a 29.15% share of the SNP genotyping market size in 2025 and pharmacogenomics & precision medicine is progressing at a 3.79% CAGR through 2031.

- By end user, pharmaceutical & biotechnology companies held 35.10% of SNP genotyping market share in 2025; contract research organizations are set to grow fastest at 4.43% CAGR to 2031.

- By geography, North America led with 38.74% revenue share in 2025, whereas Asia-Pacific is poised for the quickest 3.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global SNP Genotyping Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Falling NGS Costs & Throughput Explosion | +0.8% | Global, with strongest impact in APAC and emerging markets | Short term (≤ 2 years) |

| Pharmaceutical Pivot to Companion Diagnostics | +0.7% | North America & EU primary, expanding to APAC | Medium term (2-4 years) |

| Agrigenomics Demand for Climate-Resilient Crops | +0.4% | Global, concentrated in agricultural regions | Long term (≥ 4 years) |

| Growing DTC Wellness Genotyping Kits | +0.3% | North America & EU, emerging in APAC | Medium term (2-4 years) |

| AI-enabled Ultra-High-Throughput Microfluidics | +0.2% | Global, led by technology hubs | Long term (≥ 4 years) |

| Cloud-based Secure Genomic Data Marketplaces | +0.2% | Global, regulatory compliance dependent | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Falling NGS Costs & Throughput Explosion

Surface-coating and roll-to-roll fluidics now deliver whole-genome reads for USD 15, a drop of 98% from 2020 levels, broadening access for population studies and low-resource clinics. Illumina’s NovaSeq X exemplifies the trend by pushing per-sample economics below array prices and forecasting high single-digit revenue growth through 2027. Higher lane density allows millions of SNPs to be screened in parallel, while miniaturized library prep cuts consumable spend and sample input requirements. Academic centers formerly constrained by capital budgets can now run large cohorts, accelerating discovery timelines. The cost curve therefore tilts adoption toward sequencing-based SNP genotyping and away from fixed arrays.

Pharmaceutical Pivot to Companion Diagnostics

More than 30 companion-diagnostic alliances now channel pharma investment into high-accuracy SNP panels that guide dosing and therapy selection. FDA backing for broad assays such as FoundationOne CDx, which covers 324 genes, validates multi-biomarker strategies reliant on SNP calls. Real-time platforms integrated into clinical workflows shorten eligibility decisions from days to hours, supporting same-visit prescriptions in oncology and chronic disease care. Successful precedents like Herceptin and Gleevec reinforce the commercial logic and encourage pipeline drugs to embed genotyping from Phase II onward. As pharmacogenomics shifts from research to routine, laboratory throughput, regulatory compliance, and turnaround time become decisive purchase criteria.

Agrigenomics Demand for Climate-Resilient Crops

Extreme weather raises the premium on drought-, heat-, and pest-tolerant cultivars; SNP genotyping underpins marker-assisted selection and genomic prediction in breeding pipelines. CRISPR editing coupled with SNP-identified loci accelerates trait introgression in maize, wheat, and rice, cutting variety-development cycles by two years. Recent wheat studies mapped 12 loci governing pre-harvest sprouting resistance and explained up to 10% of phenotypic variance, illustrating tangible breeding gains. Multiplex KASP assays further lower cost per data point, driving small-holder adoption in Asia and Africa. Long-term funding through initiatives such as the Agricultural Genome to Phenome program locks in sustained reagent demand.

Growing DTC Wellness Genotyping Kits

Consumer interest in nutrition, fitness, and preventive health pushes the global DTC segment past USD 4 billion by 2025. South Korea expanded permissible wellness loci from 12 to 70, showing how regulation can unlock consumer markets while reserving clinical claims for physicians. Pharma also values the data; Regeneron’s USD 256 million buyout of 23andMe’s assets underscores the monetization of large-scale SNP databases for target discovery. Employer-sponsored wellness programs add a B2B channel, though privacy concerns require stringent consent and encryption protocols. Higher sample volumes feed the consumables cycle and introduce new user segments to precision medicine concepts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Qualified Bioinformaticians | -0.6% | Global, most acute in emerging markets | Medium term (2-4 years) |

| Regulatory Patchwork on Genetic Data Privacy | -0.4% | EU & North America primary, expanding globally | Long term (≥ 4 years) |

| Patent Thickets around Probe Chemistries | -0.3% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Supply-chain Risk for Rare Earth Fluorophores | -0.2% | Global, Asia-Pacific supply concentration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of Qualified Bioinformaticians

Eighty-two percent of genomics firms report difficulty hiring data scientists who can unify AI, statistics, and molecular biology skills. Rapid output from high-throughput platforms overwhelms existing analysis pipelines, forcing labs to outsource or delay projects. Limited academic seats in computational genomics prolong the gap, while salary inflation hits smaller firms hardest. Emerging markets feel the pinch most acutely, restricting local uptake even where instrument costs fall. Over the medium term, reskilling programs and cloud automation will ease but not eliminate the constraint.

Regulatory Patchwork on Genetic Data Privacy

GDPR classifies genetic data as sensitive, requiring explicit consent and limiting secondary uses; member-state add-ons further complicate compliance. In the U.S., HIPAA’s minimum-necessary rule plus state-level statutes like CCPA raise additional hurdles for cross-border cloud storage. NIST’s evolving cybersecurity frameworks reflect persistent re-identification risks with fewer than 100 SNPs, mandating continuous risk assessment. Fragmentation inflates legal costs, slows multinational studies, and favors vendors with robust compliance toolkits. Long-term harmonization remains uncertain, dampening the SNP genotyping market’s expansion into fully global data exchanges.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: TaqMan Holds Ground while AI Platforms Accelerate

TaqMan captured 36.85% of SNP genotyping market share in 2025 through established real-time PCR accuracy and validated probe chemistries suited for regulated diagnostics. AI-enabled microfluidic systems now challenge that dominance, posting 4.08% CAGR as they automate single-cell handling at 98% identification precision. MassARRAY sustains usage in high-sample academic screens, though its growth plateaus as sequencing costs compress.

Early adopters exploit machine-learning-guided PCR conditions to improve forensic results from degraded DNA, expanding utility beyond pristine samples. Patent barriers around probe designs insulate incumbents, yet novel multivalent binding chemistries hint at future breakthroughs. As AI integration deepens, purchasing decisions pivot on throughput gains and workflow automation rather than raw chemistry alone.

By Product Type: Consumables Lead; Software & Services Climb

Reagents & kits represented 32.78% of revenue in 2025, underscoring a consumables-driven model that delivers 88% of top vendors’ sales and anchors recurring cash flows. Software & services are the fastest-growing slice at 3.74% CAGR as cloud-native analytics platforms unlock multi-omics integration and regulatory-grade audit trails.

Instrument upgrades proceed on five-year cycles, keeping hardware sales steady but subdued. Meanwhile, automated library prep stations mitigate contamination risk and standardize results, adding pull-through for consumables. Compliance features such as ISO 27001 alignment within Connected Analytics strengthen vendor lock-in for enterprise users.

By Application: Diagnostics Dominate; Pharmacogenomics Gains Pace

Diagnostics commanded 29.15% of SNP genotyping market size in 2025, driven by reimbursed tests for oncology, cardiology, and rare disease risk. Pharmacogenomics & precision medicine is rising fastest at 3.79% CAGR as payers recognize value in genotype-guided dosing that reduces adverse events.

Agrigenomics remains a stable niche benefiting from food-security funding, while forensics adopts high-sensitivity panels to solve cold cases. Drug discovery workflows ingest population-scale SNP datasets to stratify clinical trials and predict responder subgroups, sustaining service revenues for contract labs.

By End User: Pharma Leads; CROs Expand Rapidly

Pharmaceutical & biotechnology companies held 35.10% revenue share in 2025, reflecting internal pipeline needs and regulatory submission requirements. Yet contract research organizations (CROs) are set for the swiftest 4.43% CAGR as outsourcing accelerates post-pandemic and U.S. restrictions redirect work away from Chinese providers toward India and Europe.

Academic centers pursue population studies funded by regional genomics initiatives, while clinical labs adapt to FDA’s phased oversight of laboratory-developed tests, investing in compliance upgrades that favor platform standardization.

Geography Analysis

North America’s 38.74% share stems from entrenched R&D spending, reimbursement pathways, and regulatory clarity exemplified by the 2024 LDT rule that phases in premarket reviews over four years. Illumina and Thermo Fisher collectively reported more than USD 15 billion in 2024 genetics-related revenue, reinforcing a deep domestic supply chain.

Asia-Pacific posts the fastest 3.98% CAGR through 2031 as China’s USD 9 billion precision-medicine program and India’s Genome India Project seed vast cohort studies. Cost advantages and skilled talent pools attract outsourced sequencing workloads amid U.S.-China tensions, giving regional CROs a tailwind.

Europe grows steadily on the back of academic consortia and national health service pilots, though GDPR compliance overhead tempers momentum. Oxford Nanopore’s emergence and a 142-company genomic startup base demonstrate a vibrant, if regulation-heavy, ecosystem.

Regulatory Landscape

Regulation for SNP genotyping covers in vitro diagnostics oversight, pharmacogenomics guidance tied to drug development and labeling, and genetic data privacy rules that influence how genotype results are collected, stored, and reused. In the United States, FDA activity has been a key anchor for test developers, including a November 2025 proposal to reclassify oncology nucleic acid-based companion diagnostics (CDx) from Class III to Class II via the 510(k) pathway (comment period closing in January 2026). The agency also codified setmelanotide eligibility gene variant detection as a Class II device with special controls in April 2026 under 21 CFR 862.1164. FDA clearances such as K241456 (January 2025) for a Class II genetic health risk test illustrate continued use of the 510(k) route for certain variant-detection systems.

Pharmacogenomics requirements are also reaching routine practice through labeling and related practice guidance. FDA labeling activity referenced for DPYD testing ahead of capecitabine therapy (November 2025) frames genotyping as a risk-mitigation step, increasing the weight of analytical validation, traceability, and quality systems in clinical laboratories. In Europe, EMA scientific guidelines on good pharmacogenomic practice and pharmacogenomics methodologies across the product lifecycle shape expectations for biomarker strategy, assay performance, and post-market monitoring. Privacy compliance remains fragmented, particularly for DTC and consumer-facing genotyping, as US state-level genetic privacy laws expand, including South Dakota SB 49 effective July 2026, which pushes vendors toward stronger consent and disclosure controls and data-governance tooling.

Value Chain Analysis

The SNP genotyping value chain runs from assay and instrument design (probe chemistries, enzymes, microarrays, microfluidics, and sequencing-based workflows) through instrument and consumables manufacturing, distribution via direct sales and channel partners, and downstream execution in pharmaceutical and biotechnology labs, CROs, academic centers, and clinical and diagnostic laboratories. Recurring value is concentrated in consumables (reagents and kits) and in software and services that support workflow integration, QC, traceability, and auditability for regulated and multi-site studies.

Upstream constraints center on specialized components and suppliers for optical modules, microfluidic chips, and semiconductor-based detectors, which can extend delivery timelines for automated platforms and increase qualification effort when alternates are introduced. These bottlenecks show up downstream in procurement behavior, including multi-year reagent contracts for population-scale cohort studies and dual-sourcing for critical consumables to reduce disruption risk. After-sale support also matters for installed instruments, with service networks and regional repair centers using multi-year spare-parts coverage to sustain uptime, particularly where genotyping throughput and turnaround time affect clinical reporting and large outsourced study schedules.

Competitive Landscape

Moderate consolidation prevails: the top five vendors account for an estimated half of revenue, led by Illumina’s USD 4.33 billion sequencing franchise. Incumbents protect share through end-to-end platforms, broad intellectual-property estates, and companion-diagnostic alliances with big pharma.

AI-enabled microfluidic startups target workflow automation and cost disruption, while cloud marketplaces for de-identified genomic data open alternative revenue models. Regulatory rigor becomes a strategic moat; FDA’s 2024 warning to Agena Bioscience illustrates the compliance stakes. The U.S. Biosecure Act shifts demand toward non-Chinese vendors, reshaping global supply dynamics.

IP filings around multivalent probes and enzymatic chemistries hint at future leapfrogs. Meanwhile, ecosystem partnerships such as Labcorp-Ultima Genomics tighten integration between diagnostics providers and platform innovators.

SNP Genotyping Industry Leaders

Thermo Fisher Scientific Inc.

Agilent Technologies

Bio-Rad Laboratories Inc.

Illumina Inc.

LGC Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Clinical and research workflows indicate whitespace around software-led performance gains and broader consolidation of SNP genotyping into NGS pipelines. Illumina introduced TruPath Genome (February 2026) and later expanded DRAGEN v4.5 support (April 2026) to improve interpretation in difficult genomic regions, including resolution of highly homologous medically relevant genes used in rare-disease research. These releases reinforce buying criteria beyond raw throughput, including phasing, reproducibility, and bioinformatics traceability. In prenatal and reproductive health, Natera extended SNP-informed approaches through the launch of a 21-gene Fetal Focus sgNIPT (January 2026), then announced an enhanced Panorama NIPT using SNP-informed deep sequencing (May 2026). This sequence points to an opportunity for vendors supplying high-fidelity SNP calling, library prep, and analysis in low-input, low-fetal-fraction settings.

Point-of-care and field-deployable SNP/SNV detection remains under-penetrated relative to central-lab platforms, supported by emerging evidence for rapid, one-pot workflows. Academic publications in 2026 described isothermal and CRISPR-based approaches for rapid SNP/SNV discrimination, including a microfluidic CRISPR platform reported in Nature Communications in 2026, which aligns with demand for faster time-to-result and reduced instrumentation burden in decentralized testing. Separately, genetic data privacy fragmentation, including GDPR in Europe and expanding US state-level DTC genetic testing rules, creates product whitespace for consent management, de-identification, and compliant data-sharing architectures embedded into genotyping software and services, particularly for DTC and population genomics programs where secondary data use underpins the business case.

Recent Industry Developments

- July 2026: Researchers reported a microfluidic CRISPR-based platform in Nature Communications for sequencing-concordant SNP genotyping using one-pot workflow concepts. The publication highlights technical progress toward faster, more portable SNP discrimination formats that can reduce reliance on centralized lab infrastructure and extend SNP testing into decentralized settings.

- October 2025: Thermo Fisher Scientific launched the Applied Biosystems SwiftArrayStudio Microarray Analyzer with integrated genotyping capabilities targeting GWAS and pharmacogenomics workflows. The release strengthens microarray-based options for high-throughput SNP studies where standardized processing and throughput are prioritized, alongside instrument-software integration.

- October 2024: LGC Biosearch Technologies launched Amp-Seq One, a one-step targeted amplicon sequencing workflow positioned for accelerated breeding programs. This product move expands genotyping-by-sequencing toolkits for agrigenomics users and increases pull-through demand for targeted panels, library prep reagents, and downstream analysis services.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market tracks revenues generated from SNP genotyping workflows used to detect single nucleotide variants, including the related instruments, consumables, and supporting software that directly enable SNP calls across human and non-human samples.

Scope exclusions: We exclude broader sequencing-only revenue that does not result in a defined SNP genotyping assay output, and general lab services that are not specific to SNP genotyping.

Segmentation Overview

- By Technology (Value)

- TaqMan SNP Genotyping

- Massarray SNP Genotyping

- SNP GeneChip Arrays

- Other Technologies

- By Product Type (Value)

- Instruments & Workstations

- Reagents & Kits

- Software & Services

- By Application (Value)

- Diagnostics

- Pharmacogenomics & Precision Medicine

- Agriculture & Animal Genetics

- Forensics

- Drug Discovery & Development

- By End User (Value)

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutes

- Contract Research Organizations

- Clinical & Diagnostic Laboratories

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base around testing activity, funding, and technology adoption, before assumptions were carried into the model. We relied on public sources such as the US NIH and other national grant portals, the US FDA for companion diagnostics context, CDC publications when relevant for screening and surveillance, and OECD and World Bank indicators to anchor health and R&D spend trends.

To keep inputs realistic, we also reviewed peer-reviewed genetics journals, clinical trial registries, and patent databases to confirm platform direction, along with trade and customs statistics for instruments and reagents movement in key hubs. Company annual reports, investor presentations, and press releases were used to understand product focus, geographic mix, and pricing language. We also referenced paid subscriptions for company financials and intelligence, patent searching, and import-export shipment-level signals to cross-check what is visible in public. These desk sources are illustrative, and many other public documents were reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what portion of genetic testing activity is truly SNP genotyping, and how fast different use cases are expanding over the next five years. We spoke with assay developers, lab managers, procurement roles, and research users across APAC, EMEA, and the Americas, so pricing, utilization, and replacement cycles could be checked against real buying behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 12% | APAC: 43% |

| Mid tier: 51% | Functional/Unit leaders: 29% | EMEA: 34% |

| Smaller Players: 16% | Managers: 59% | Americas: 23% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand pool build where testing and research activity are reconstructed using indicators that can be defended in public data, then refined with interview feedback. In SNP genotyping, the key inputs include the mix shift across common platforms (PCR-based assays, array-based workflows, and mass spectrometry approaches), average reagent and kit spend per sample, instrument installed base behavior, and the pace of adoption in pharmacogenomics and diagnostic research.

Once the demand pool is framed, selective bottom-up checks are done so totals remain practical, including sampled price points for assays and consumables, channel feedback on shipment trends, and limited supplier roll-ups where disclosure is clear enough. Where smaller labs or fragmented research users are not fully visible, the gap is handled through utilization ranges tied to funding cycles and published sample volumes, then narrowed through primary feedback. For forecasting, scenario analysis is applied around variables such as funding stability, regulated diagnostic adoption, and technology substitution, and the final trajectory is accepted only after the assumptions align with what experts consider achievable in the 2026 to 2031 window.

Data Validation & Update Cycle

Outputs are validated through cross-checks against independent signals, including instrument shipment patterns, public funding direction, and the observed split between research and clinical demand. If any region or technology shows an unusual jump, the drivers are re-tested, and follow-up calls are triggered to confirm whether it is a real market shift or a modeling artifact.

Before sign-off, the numbers go through multi-step analyst review, including variance checks versus prior-year trends and sanity checks on implied pricing and volume. Reports are refreshed annually, and interim updates are added when material events occur, such as major regulatory changes or step-changes in platform pricing. Right before delivery, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's Snp Genotyping Market Estimate Compared With Other Published Estimates

Published market sizes for SNP genotyping can look far apart because the counted revenue pool is not always the same, and because some models lean heavily on aggressive growth curves without enough checks on volumes and pricing. Differences also show up when firms pick different base years, convert currencies at different points in time, or include adjacent genomics activities that sit close to SNP genotyping.

The table points to a wide spread in 2024 to 2026 values and the implied growth rates. Under Mordor Intelligence's model, the 2026 value of USD 8.57 B is built around SNP genotyping technologies like TaqMan, MassARRAY, and SNP GeneChip arrays, and it avoids folding in broader genetic testing revenue that is not tied to a SNP genotyping assay output.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 8.57 B (2026) | |

| Trade Journal A | USD 6.48 B (2024) | Uses an earlier base year and a broader segmentation lens, and the bridge from 2024 to later years is not clearly tied to platform-level price and utilization checks. |

| Regional Consultancy B | USD 7.52 B (2025) | Applies a high-growth forecast path that can overstate uptake if diagnostic conversion and funding-led research volumes are assumed to rise in parallel across all regions. |

In practice, the gap is largely explained by scope boundaries and how pricing and sample volumes are projected, especially when adjacent genomics revenue is bundled into the total. By keeping the model traceable to platform mix, sample-based spend, and geography-level adoption checks, the final number stays easier to reproduce and to audit in client discussions.

Key Questions Answered in the Report

How big is the SNP Genotyping Market?

The SNP Genotyping Market size is expected to reach USD 8.57 billion in 2026 and grow at a CAGR of 3.52% to reach USD 10.19 billion by 2031.

What is the current SNP Genotyping Market size?

In 2026, the SNP Genotyping Market size is expected to reach USD 8.57 billion.

Who are the key players in SNP Genotyping Market?

Thermo Fisher Scientific Inc., Agilent Technologies, Bio-Rad Laboratories Inc., Illumina Inc. and LGC Group are the major companies operating in the SNP Genotyping Market.

Which is the fastest growing region in SNP Genotyping Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in SNP Genotyping Market?

In 2025, the North America accounts for the largest market share in SNP Genotyping Market.

What years does this SNP Genotyping Market cover, and what was the market size in 2025?

In 2025, the SNP Genotyping Market size was estimated at USD 8.57 billion. The report covers the SNP Genotyping Market historical market size for years: 2022, 2023 and 2024. The report also forecasts the SNP Genotyping Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: