Smokeless Tobacco Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 13.21 Billion |

| Market Size (2031) | USD 18.45 Billion |

| Growth Rate (2026 - 2031) | 4.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

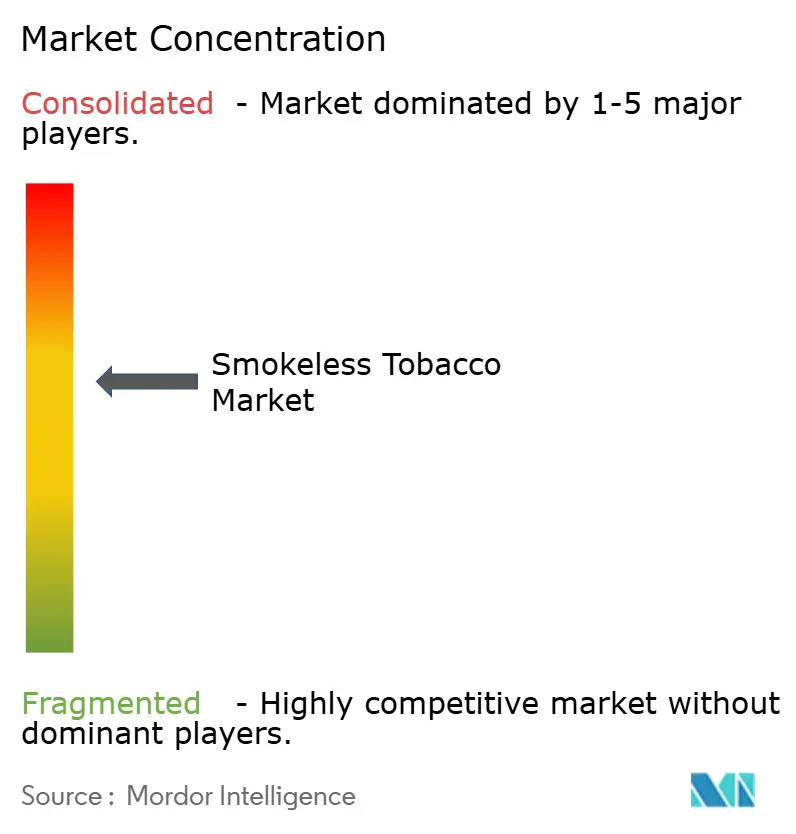

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Smokeless Tobacco Market Analysis by Mordor Intelligence

The smokeless tobacco market size was valued at USD 11.58 billion in 2025 and estimated to grow from USD 13.21 billion in 2026 to reach USD 18.45 billion by 2031, at a CAGR of 4.31% during the forecast period (2026-2031). The sector balances regulatory tightening in high-income nations against deep-rooted cultural acceptance in South Asia and the Nordics. Product innovation in tobacco-free nicotine pouches broadens appeal among smokers facing indoor-smoking bans, yet mounting scientific scrutiny of oral-tobacco health risks tempers expansion. North American incumbents leverage FDA marketing authorizations and capacity investments to defend dominant shares, while Asian producers exploit cost advantages and rising urban incomes. Direct-to-consumer subscription models are eroding dependence on the brick-and-mortar channel and reshaping promotional strategies.

Key Report Takeaways

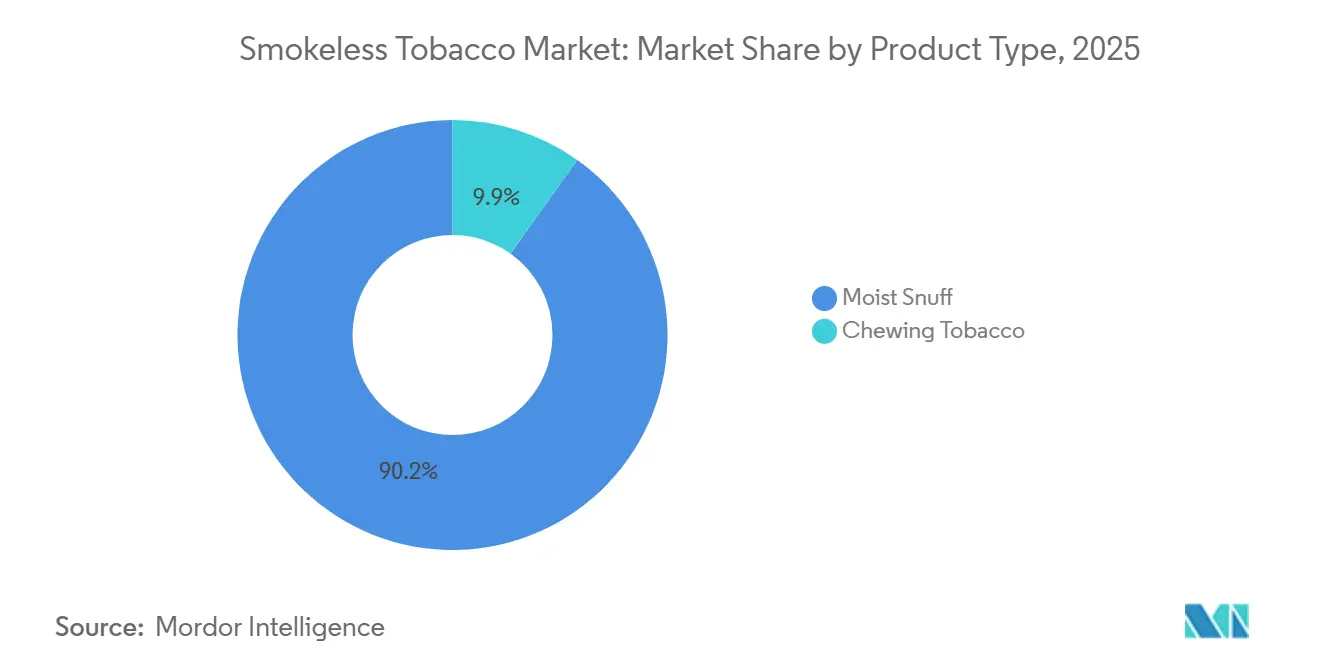

- By product type, moist snuff held 90.15% of the smokeless tobacco market share in 2025, while chewing tobacco is forecast to grow at a 5.85% CAGR through 2031.

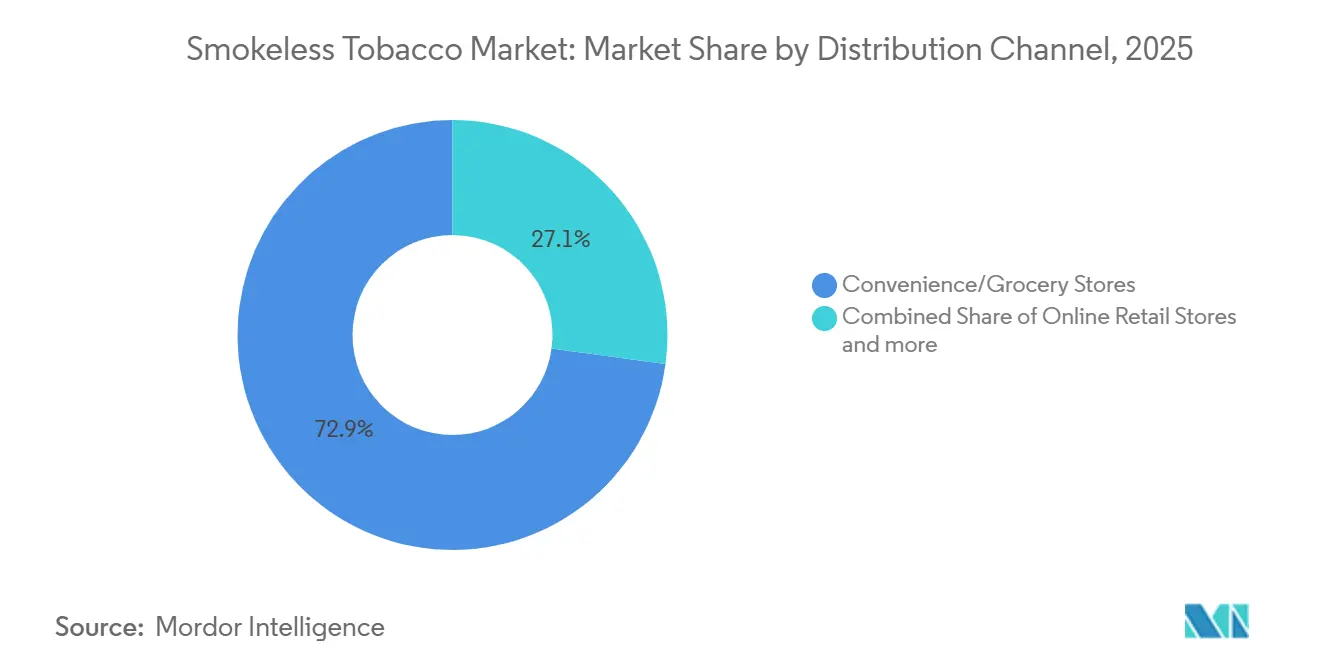

- By distribution channel, convenience and grocery stores captured 72.85% revenue in 2025; online retail is projected to advance at a 6.73% CAGR to 2031.

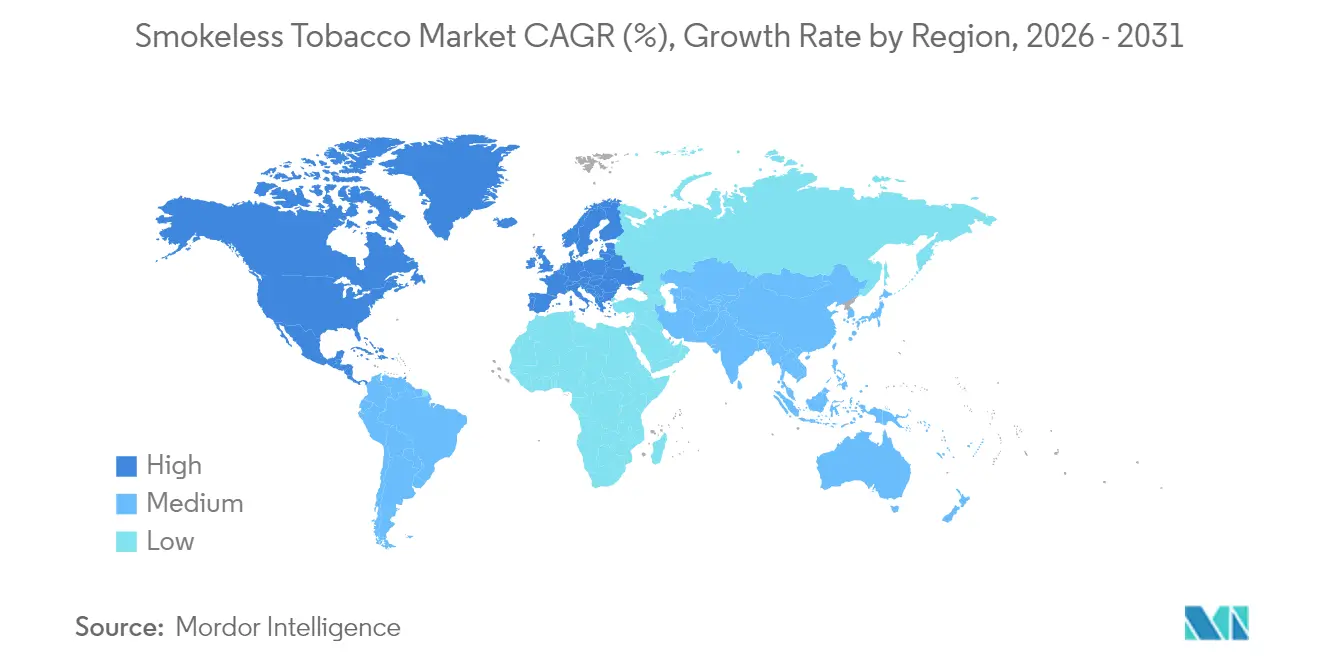

- By geography, North America commanded 72.63% revenue share in 2025, whereas Asia-Pacific is expected to post the fastest 6.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smokeless Tobacco Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Public Smoking Bans Fueling Shift To Smokeless Options | +0.8% | Global, with strongest effect in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Innovations In Nicotine Pouch Products And Flavors | +1.1% | North America, Nordic Europe, emerging adoption in UK and Poland | Short term (≤ 2 years) |

| Strategic Marketing Targeting Youth Demographics | +0.5% | North America, Europe (regulatory scrutiny rising) | Short term (≤ 2 years) |

| Cultural And Traditional Acceptance In Key Regions | +0.9% | Asia-Pacific (India, Bangladesh), Nordic Europe (Sweden, Norway), North Africa (Algeria) | Long term (≥ 4 years) |

| High-Potency Nicotine Delivery Satisfying Addictive Needs | +0.7% | Global, particularly North America and Nordic markets with established oral-tobacco use | Medium term (2-4 years) |

| Rise Of Synthetic-Nicotine And Herbal Alternatives In Restricted Areas | +0.6% | North America (regulatory arbitrage), select Asia-Pacific markets with tobacco bans | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Public Smoking Bans Fueling Shift To Smokeless Options

Since 2020, over 60 countries have enacted comprehensive indoor smoking bans, limiting opportunities for combustible tobacco use. As a result, adult nicotine consumers are increasingly turning to discreet oral formats that comply with workplace and hospitality venue regulations. Sweden's long-standing snus tradition highlights this shift: in 2024, daily snus usage among Swedish men reached 20%, coinciding with one of Europe's lowest smoking rates, as reported by the Swedish Public Health Agency[1]Source: Swedish Public Health Agency, “Tobacco Habits in Sweden 2024,” folkhalsomyndigheten.se. The FDA's marketing authorization for ZYN nicotine pouches in January 2025 underscores the rationale behind these bans, with regulators drawing clearer distinctions between combustion-based and noncombustion nicotine methods. This distinction opens doors for manufacturers adept at navigating premarket reviews and obtaining modified risk labels. In January 2026, Philip Morris International presented to the FDA's Tobacco Products Scientific Advisory Committee, advocating for a claim that switching entirely to ZYN could lower the risk of six smoking-related diseases. If granted, this endorsement could revolutionize marketing strategies and hasten the adoption of such products.

Innovations In Nicotine Pouch Products And Flavors

Flavor diversification and nicotine strength segmentation have propelled pouches from a niche market in the Nordic region to a global powerhouse. Manufacturers are now introducing 3 milligram and 6 milligram variants, alongside exotic flavors like citrus, coffee, and cinnamon, aligning with consumer preferences highlighted in sensory research. In June 2024, Altria filed premarket tobacco product applications for its on! PLUS line. This line boasts a proprietary soft feel material and seamless construction, setting it apart from leading tobacco derived nicotine brands. Additionally, integrated disposal compartments tackle littering concerns highlighted in municipal ordinances. In late 2024, British American Tobacco launched Velo Plus across the U.S., broadening flavor and nicotine choices to directly challenge ZYN, which holds a dominant 50.7% value share in tracked U.S. channels. The strategy hinges on portfolio segmentation: the entry level 3 milligram pouches aim to attract cigarette smokers wary of high nicotine doses, while the 6 milligram and stronger variants cater to heavy users familiar with the quick absorption of moist snuff. Furthermore, flavor innovation acts as a safeguard against potential menthol cigarette bans, given that adult menthol smokers show a greater inclination to try mint and wintergreen pouches over unflavored ones.

Strategic Marketing Targeting Youth Demographics

In 2024, the FDA issued warning letters to manufacturers for using youthful imagery in campaigns or neglecting robust age gating on branded websites. This highlights the agency's increasing scrutiny on digital advertising and influencer partnerships on social media. Altria's decision to voluntarily halt online sales on ZYN.com in June 2024 came after a subpoena from the District of Columbia. The subpoena was linked to compliance with the city's 2022 flavored tobacco ban, underscoring the reputational and legal challenges of direct to consumer channels that sidestep traditional age verification methods. Yet, despite these enforcement actions, the category continues to grow, suggesting that marketing to legal age adults is proving more effective than concerns over youth uptake. In January 2026, Philip Morris International presented findings to the FDA, highlighting that youth prevalence of nicotine pouch use remains low. Their data also indicated that exposure to modified risk claims did not boost usage intentions among young adults, bolstering their argument for adult targeted messaging. As more brands pursue modified risk authorizations, the balancing act between commercial speech and public health will become even more pronounced. Compliance with the FDA's stringent labeling and promotional guidelines will be crucial for brands to avoid market withdrawal.

Cultural And Traditional Acceptance In Key Regions

India stands as the world's largest market for oral tobacco, which includes products like gutka and khaini. These products are deeply woven into the social fabric, especially among agricultural and blue collar workers. ITC Limited, a leading player in India's tobacco landscape, has set its sights on significantly boosting its raw tobacco exports to British American Tobacco. By the fiscal year 2025 26, ITC aims to secure supply contracts worth INR 2,350 crore (around USD 282 million). This ambition not only highlights India's stature as a major consumption hub but also as a pivotal global sourcing center. Meanwhile, in Nordic Europe, the snus tradition, enjoying a unique EU exemption for Sweden, boasts per capita consumption rates that are unparalleled. Notably, even with domestic sales restrictions, consumers in Norway and Denmark are gravitating towards Swedish style snus products. Such deep rooted cultural ties ensure a consistent demand, resilient to price hikes and anti tobacco campaigns. This is evident as snus volumes in Sweden remain stable or even grow, contrasting with the decline in cigarette sales. For multinational companies, the hurdle is clear: they must cultivate a similar cultural acceptance in regions where oral tobacco is a novel concept. Achieving this will demand years of consumer education and navigating regulatory landscapes.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion Of Safer Nicotine Alternatives | -0.6% | Global, strongest in North America and Western Europe where heated-tobacco and e-vapor penetration is high | Medium term (2-4 years) |

| Intensified Anti-Tobacco Public Campaigns | -0.4% | Global, with concentrated efforts in OECD countries and WHO FCTC signatories | Long term (≥ 4 years) |

| Stricter Government Regulations And Prohibitions | -0.7% | North America (FDA premarket review), EU (flavor bans, plain packaging), select Asia-Pacific markets (India state-level bans) | Short term (≤ 2 years) |

| Mounting Scientific Evidence of Health Risks | -0.5% | Global, influencing policy in evidence-based regulatory regimes (FDA, EU, Australia) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion Of Safer Nicotine Alternatives

Heated-tobacco products and closed-system e-vapor devices are drawing users away from both combustible and smokeless formats. These innovations offer adult smokers a tech-savvy experience, appealing especially to early adopters who are less inclined towards traditional oral tobacco. In 2024, Japan Tobacco's Ploom brand boasted a volume growth of around 40%. The company, eyeing a mid-teens market share in pivotal regions like Japan and Italy by 2028, backed its ambitions with a hefty JPY 135 billion capital expenditure in 2024. Meanwhile, British American Tobacco's Vuse secured a 40.3% global value share in closed-system consumables in 2024. Notably, its share in U.S. tracked channels hit 50.7%, underscoring vapor's potential to overshadow both cigarettes and smokeless products. For smokeless manufacturers, the landscape is mixed: while nicotine pouches can thrive alongside vapor for users seeking discretion, traditional moist snuff and chewing tobacco are witnessing a decline as younger generations pivot to modern alternatives. Philip Morris International is pushing for a modified-risk authorization for ZYN, aiming to rebrand pouches as a scientifically-backed harm-reduction tool, a crucial move to rival heated tobacco's regulatory wins in various markets.

Intensified Anti-Tobacco Public Campaigns

WHO Framework Convention on Tobacco Control signatories have extended mass-media campaigns beyond combustibles to encompass all tobacco and nicotine products, deploying graphic health warnings and testimonial advertising that emphasize oral cancer, gum disease, and cardiovascular risks associated with smokeless use. These campaigns resonate particularly in markets where smokeless tobacco lacks the cultural normalization seen in Sweden or India, creating headwinds for category expansion in Western Europe and Oceania. The FDA's January 2026 review of ZYN's modified-risk application included explicit consideration of youth exposure to reduced-risk messaging, with the agency noting that claim exposure did not increase use intentions among young adults but requiring ongoing post-market surveillance to detect unintended uptake[2]Source: Food and Drug Administration, "Meeting of the Tobacco Products Scientific Advisory Committee (TPSAC)", fda.gov. This regulatory caution reflects public-health advocates' concerns that harm-reduction claims, even when scientifically accurate, may renormalize nicotine use and undermine decades of denormalization efforts. The net effect is a constrained marketing environment where manufacturers must balance commercial imperatives against reputational risks, often resulting in conservative messaging that fails to communicate product benefits to adult smokers who might otherwise switch.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Moist Snuff Dominance Anchors North American Revenue

In 2025, Moist Snuff dominated the global product type revenue, capturing a significant 90.15% share. This dominance underscores the format's deep-rooted presence in the U.S., where both dip and snus have longstanding traditions, and in Nordic Europe, where the Swedish-style snus not only enjoys cultural acceptance but also benefits from a regulatory exemption, sidestepping the EU's oral tobacco ban. Within the realm of Moist Snuff, U.S. style dip, characterized by loose or pouched tobacco placed between the cheek and gum, and Swedish-style snus, which comes as pasteurized tobacco in portion bags, cater to distinct consumer preferences. Dip enthusiasts prioritize a robust nicotine delivery and the ritual of spitting, whereas snus aficionados appreciate discretion and the convenience of not having to expectorate. In a clear nod to the industry's evolving dynamics, Philip Morris International made headlines in 2024 with a USD 232 million expansion in Kentucky and a separate investment in a Colorado facility. These moves, centered on boosting ZYN nicotine pouch capacity rather than traditional snus, highlight a strategic shift towards tobacco-free oral nicotine, even as the company continues to benefit from the cash flow generated by legacy moist snuff volumes.

Chewing Tobacco, accounting for the remaining product-type share in 2025, is poised for growth, projected to grow at a 5.85% CAGR through 2031, the fastest among its peers. This surge is largely attributed to India's expansive consumption base and the rising incomes in Sub-Saharan Africa, where loose-leaf and plug tobacco serve as accessible nicotine sources. ITC Limited's ambitious strategy to more than double its raw tobacco exports to British American Tobacco by the fiscal year 2025-26 highlights India's dual significance: as a major consumption market and a pivotal global supply hub. Leveraging its agricultural integration, ITC ensures its offerings meet the stringent quality specifications demanded by international buyers. However, the growth of Chewing Tobacco isn't without challenges. State-level gutka bans in India have disrupted distribution, nudging consumption towards unregulated avenues. Additionally, flavor restrictions in Western markets curtail product differentiation. Yet, the segment's allure lies in its relatively straightforward manufacturing process and lower capital intensity compared to pouches. This advantage empowers regional players to engage in price competition, especially in markets where brand loyalty is tenuous, and consumers lean towards nicotine content over nuanced sensory experiences.

By Distribution Channel: E-commerce Disrupts Traditional Retail

In 2025, convenience and grocery stores dominated smokeless-tobacco distribution, claiming a substantial 72.85% share. This dominance can be attributed to factors like impulse buying, widespread geographic presence, and the capability to enforce age verification at the point of sale, thanks to trained personnel and ID-scanning technology. While North America and Europe showcase a mature market, the Asia-Pacific region presents a different picture. Here, oral-tobacco sales are largely led by independent kirana stores and paan shops, with modern retail only making inroads in major cities. Online retail, despite its modest share in 2025, is set to surge at a 6.73% CAGR through 2031, outpacing all other channels. This growth is fueled by direct-to-consumer subscription models that ensure repeat purchases and a regulatory edge in areas where e-commerce age-verification lags behind traditional retail. Highlighting the challenges of the online realm, Altria's June 2024 halt of ZYN.com sales came in the wake of a District of Columbia subpoena, underscoring the heightened legal and reputational stakes tied to online channels and their scrutiny over youth access.

Distribution channels like supermarkets, hypermarkets, tobacco specialty shops, military commissaries, and duty-free outlets play distinct roles based on geography. For instance, in Nordic Europe, supermarkets are normalizing snus by placing it alongside confectionery items, while U.S. military commissaries leverage tax-advantaged pricing to boost sales among service members. The competition is fierce, especially for backbar visibility and promotional allowances. Manufacturers vie for prime spots behind checkout counters, where decisions are made in mere seconds. British American Tobacco's December 2024 trading update highlighted the success of Velo's revamped brand and Grizzly Modern Oral in U.S. retail. The nationwide rollout of Velo Plus aims to diversify flavor and nicotine offerings. However, this surge in product variety is tightening retail shelf space, leading to the delisting of slower-moving SKUs and favoring brands with rapid sales and robust trade ties. Online platforms, with their boundless virtual shelf space, sidestep these limitations. They empower niche brands to connect with scattered consumer segments without needing a national distribution network. This evolving landscape is poised to gradually diminish the share of convenience stores in the market.

Geography Analysis

In 2025, North America contributed 72.63% of global revenue, with the U.S. dominating most snuff and pouch consumption. In contrast, Canada faced restrictions due to flavored-tobacco bans. The FDA's 2025 approval of ZYN legitimized this product category, triggering a wave of pre-market applications. Investments exceeding USD 800 million by 2025 ensured an adequate supply. Although litigation risks remain high, clearer regulations provide a strategic framework for marketing teams.

Europe exhibits a divided landscape: the Nordic exemption zone allows legal snus sales, while the rest of the EU permits only tobacco-free pouches in retail. Consumers in Sweden, Norway, and Denmark lead globally in per-capita usage. British American Tobacco reported strong performance for Velo in newer launch markets, including the United Kingdom and Poland, during 2024, with the brand achieving 11.2% volume share of total oral products and 28.2% of modern oral in top markets[3]Source: British American Tobacco, “2024 Full-Year Pre-Close Trading Update,” bat.com. The brand's future growth depends on potential EU reforms or broader acceptance of nicotine pouches under separate regulatory frameworks.

The Asia-Pacific region is experiencing rapid growth, with a projected 6.28% CAGR by 2031. India's entrenched chewing-tobacco culture drives significant volume, while urbanization supports a shift toward premium products. State-level gutka bans in India have fueled informal sales but have not reduced overall demand. Pakistan and Bangladesh reflect India's consumption patterns but lack scalable branded supply chains. Entering this market requires navigating fragmented retail structures and diverse excise policies. The Rest of the World, including South Africa and Algeria, offers modest yet strategic opportunities. South Africa's regulated oral-tobacco market provides a testing ground for branded products. Conversely, Algeria's rural loose-leaf market delivers high volume but operates on low margins. Due to currency volatility and sudden policy changes, a phased approach to capital investment is recommended.

Competitive Landscape

In the global smokeless tobacco market, where concentration is moderate, established giants are adopting acquisitions and product innovations to maintain their competitive edge. While these market leaders diversify and integrate vertically to capitalize on the broader nicotine ecosystem, newer entrants are focusing on niche areas, such as tobacco-free options and synthetic nicotine. For example, Philip Morris International's USD 16 billion acquisition of Swedish Match highlights the industry's shift toward smokeless alternatives. Similarly, Japan Tobacco International's USD 2.4 billion purchase of Vector Group in October 2024 reflects the ongoing drive to expand market share through mergers and acquisitions.

Amid advertising restrictions, companies are leveraging technology to improve product formulations, enhance manufacturing efficiency, and strengthen digital marketing efforts, ensuring direct consumer engagement. A clear trend is evident: firms are making significant R&D investments to develop synthetic nicotine and tobacco-free products. They are skillfully navigating regulatory challenges while aligning with consumer preferences. In 2024, Imperial Brands allocated USD 329 million to next-generation product development, focusing on oral nicotine pouches, heated tobacco, and vaping alternatives.

Emerging opportunities are arising from regulatory differences between tobacco-derived and synthetic products, geographic expansion into regions with lenient harm reduction policies, and targeting health-conscious consumers seeking cigarette alternatives. The FDA's regulatory framework not only provides competitive advantages for authorized products but also creates barriers for new entrants, particularly those lacking regulatory expertise or the financial resources for extensive approval processes.

Smokeless Tobacco Industry Leaders

-

Altria Group, Inc.

-

British American Tobacco Plc

-

Philip Morris International, Inc.

-

Imperial Brands Plc

-

Japan Tobacco Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: 22nd Century Group, Inc. launched new Pinnacle VLN and moist snuff products in over 1,700 convenience stores across 27 states in the USA, following an update to its manufacturing and marketing agreement with a major c-store chain. This includes two new low-nicotine Pinnacle VLN cigarette products alongside two moist snuff flavors, rolled out in late summer and fall 2025, pending state approvals.

- March 2025: Reynolds American expanded its Tobaccoville, North Carolina, manufacturing facility to expand its oral nicotine pouch production, specifically for the Velo Plus brand, which added 300 jobs. The company, a subsidiary of British American Tobacco, is increasing its workforce by combining local manufacturing and national trade marketing roles to meet demand for its smokeless products. This expansion follows a similar addition of over 500 jobs in 2024, primarily for the Velo Plus line and sales alignment.

- August 2024: Philip Morris International Inc. invested USD 232 million through one of its Swedish Match affiliates to expand production capacity of its manufacturing facility in Owensboro, Kentucky. The facility was asserted to produce ZYN nicotine pouches to help meet the growing demand from legal-age consumers switching from cigarettes or other traditional tobacco products.

Global Smokeless Tobacco Market Report Scope

Smokeless tobacco is a tobacco product that is neither burned nor inhaled but orally consumed through chewing or snusing. The smokeless tobacco market is segmented into product type, distribution channel, and geography. Based on product type, the market is segmented into chewing tobacco and moist snuff. Moist snuff is further bifurcated into US-style moist snuff (dip) and Swedish-style snus. Based on distribution channels, the market is segmented into convenience/traditional grocers, supermarkets/hypermarkets, online retail stores, and other distribution channels. Also, the study provides an analysis of the smokeless tobacco market in emerging and established markets across the globe, including North America, Europe, Asia-Pacific, and the Rest of the World. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Chewing Tobacco |

| Moist Snuff |

| US-Style Moist Snuff (Dip) |

| Swedish Style Snus |

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Europe | Czech Republic |

| Denmark | |

| Norway | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | India |

| Rest of Asia-Pacific | |

| Rest of the World | South Africa |

| Algeria | |

| Other Countries |

| By Product Type | Chewing Tobacco | |

| Moist Snuff | ||

| US-Style Moist Snuff (Dip) | ||

| Swedish Style Snus | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Europe | Czech Republic | |

| Denmark | ||

| Norway | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| Rest of Asia-Pacific | ||

| Rest of the World | South Africa | |

| Algeria | ||

| Other Countries | ||

Key Questions Answered in the Report

How large will the smokeless tobacco market be in 2031?

It is projected to reach USD 18.45 billion by 2031, expanding at a 4.31% CAGR between 2026 and 2031.

Which region dominates value sales?

North America held 72.63% of global revenue in 2025, driven by entrenched moist-snuff and pouch consumption.

What is the fastest-growing region?

Asia-Pacific is forecast to post a 6.28% CAGR through 2031, led by India’s chewing-tobacco base and rising urban income.

Which product type leads share?

Moist snuff commanded 90.15% revenue share in 2025, anchored by U.S. dip and Swedish snus demand.

Page last updated on: