Smart Stadium Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

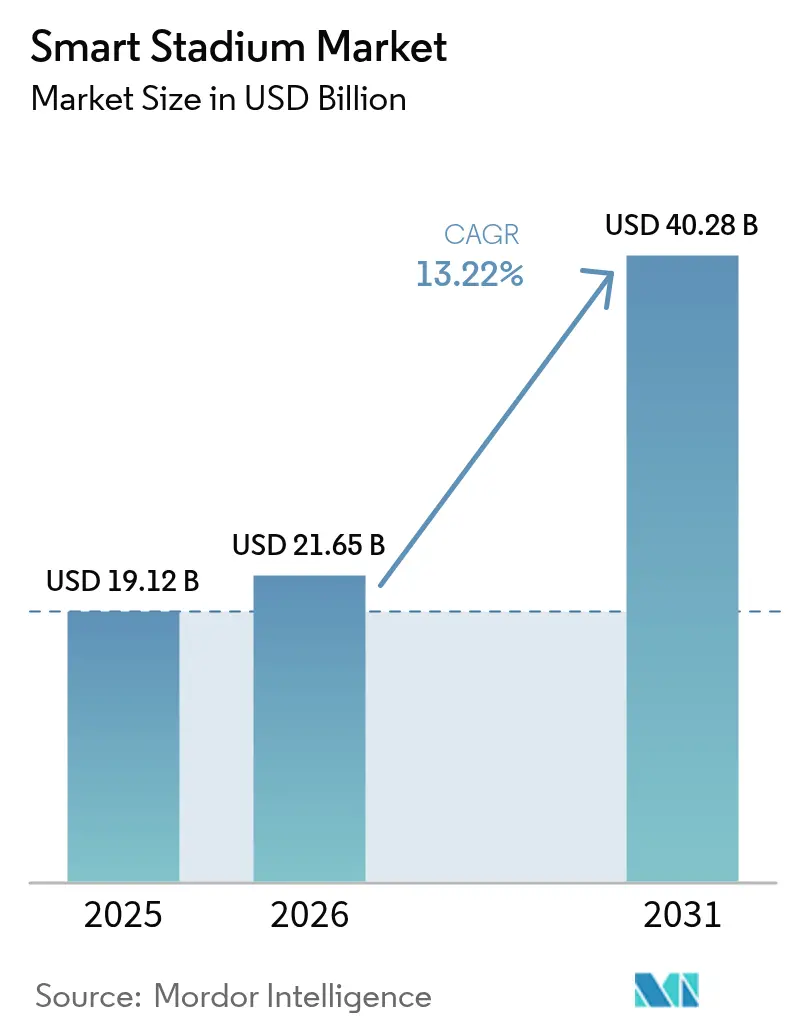

| Market Size (2026) | USD 21.65 Billion |

| Market Size (2031) | USD 40.28 Billion |

| Growth Rate (2026 - 2031) | 13.22% CAGR |

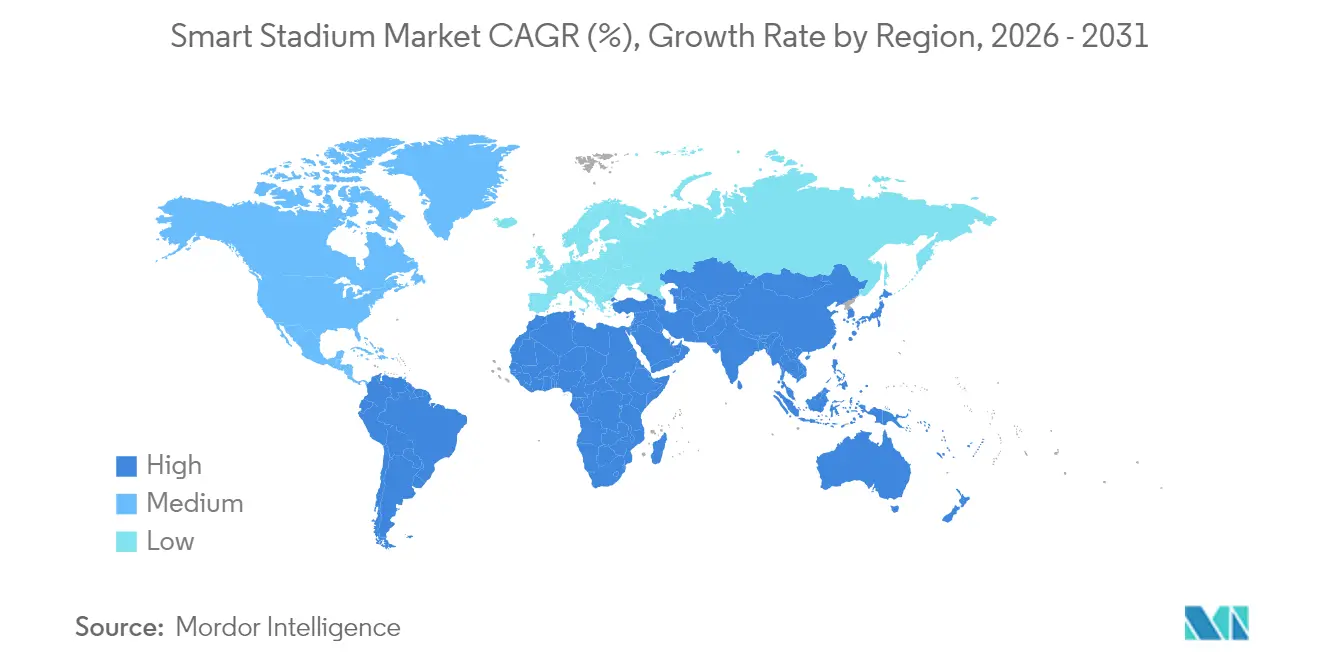

| Fastest Growing Market | Middle East |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Smart Stadium Market Analysis by Mordor Intelligence

Smart stadium market size in 2026 is estimated at USD 21.65 billion, growing from 2025 value of USD 19.12 billion with 2031 projections showing USD 40.28 billion, growing at 13.22% CAGR over 2026-2031. Venue owners see the network as a profit engine rather than a cost center, driving investment in private 5G cores, edge-compute nodes, and cloud analytics that unlock real-time betting, dynamic sponsorship assets, and data-driven crowd services. Mega-events such as the 2026 FIFA World Cup and the 2028 Los Angeles Olympics are compressing upgrade cycles into 24-month windows, while European zero-trust mandates are raising integration standards and creating defensible positions for certified platforms. U.S. legalization of mobile wagering is generating new licensing revenues, and Asia’s smart-city grants are subsidizing IoT roll-outs across tier-2 venues. Competitive intensity is rising as full-stack vendors integrate radio, edge, and software bundles, forcing smaller specialists to focus on niche layers like AI video analytics and distributed antenna systems.

Key Report Takeaways

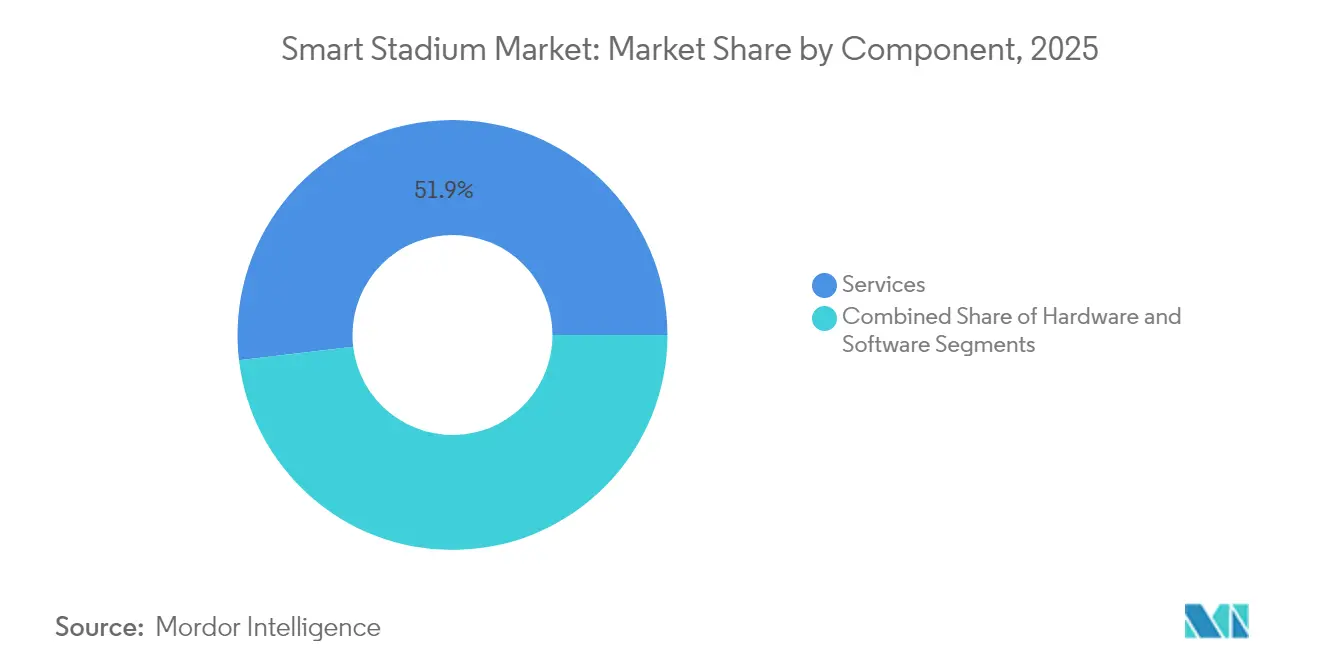

- By component, Services led with 51.88% revenue share in 2025, while Software is projected to expand at a 15.02% CAGR through 2031.

- By software solution, Digital Content and Fan Engagement commanded 28.10% of revenue in 2025; Smart Ticketing and Parking is forecast to grow at a 13.95% CAGR to 2031.

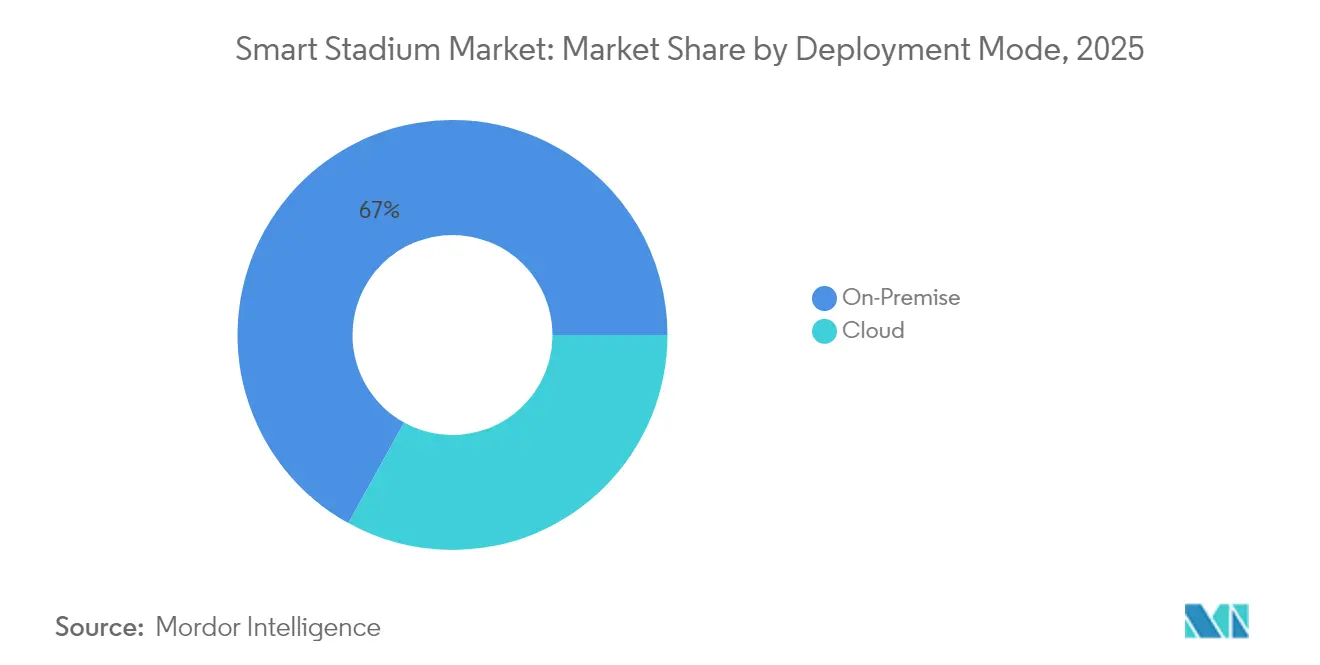

- By deployment mode, On-Premise installations held 66.95% in 2025, whereas Cloud is expected to accelerate at a 14.72% CAGR through 2031.

- By connectivity technology, Wi-Fi 6/7 captured 44.05% in 2025, and 5G and Private LTE is advancing at a 14.05% CAGR to 2031.

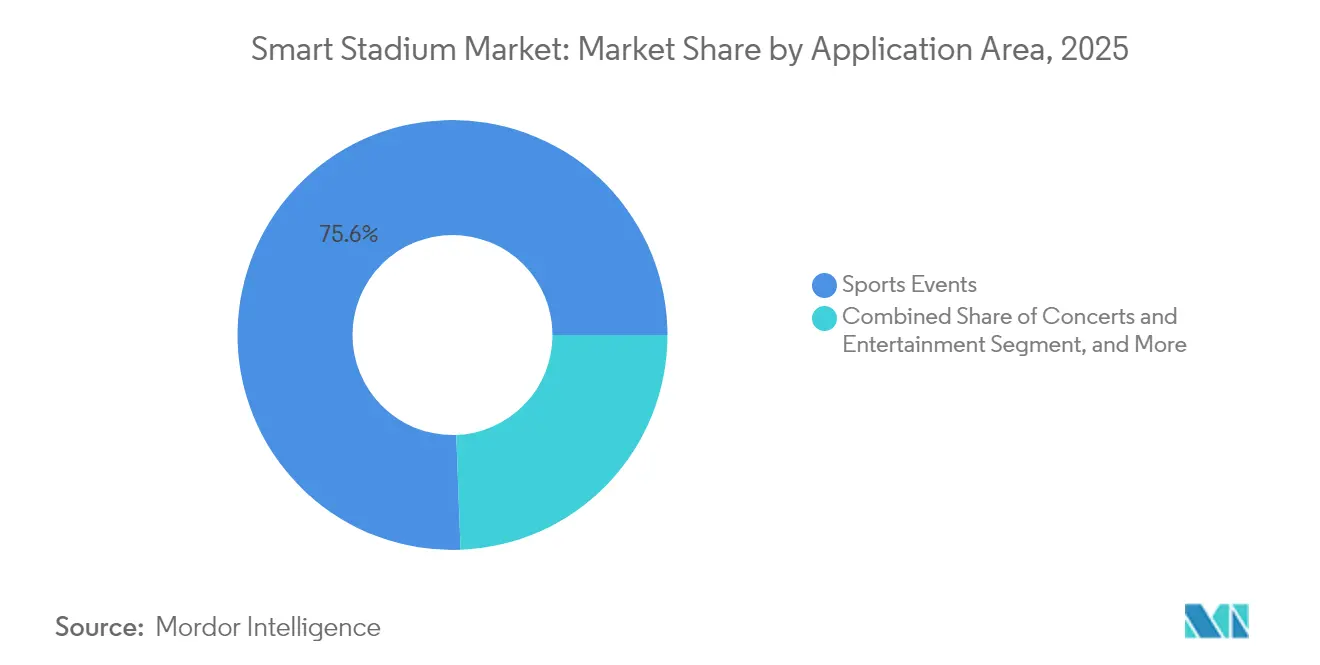

- By application, Sports Events accounted for 75.60% of 2025 revenue and Esports Tournaments are poised for a 13.40% CAGR through 2031.

- By revenue stream, Ticketing and Merchandise held 35.30% in 2025, while Data Monetization and Betting is projected to rise at a 14.25% CAGR to 2031.

- By geography, North America led with 37.10% share in 2025; the Middle East is expected to log the fastest regional growth at 14.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Stadium Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G network roll-outs catalyzing high-density connectivity | +2.8% | North America and Europe, early APAC metros | Medium term (2-4 years) |

| Mega-event pipeline (2026 FIFA World Cup, 2028 LA Olympics) accelerating digitization budgets | +3.1% | United States, Mexico, Canada | Short term (≤ 2 years) |

| EU crowd-safety mandates (NIS2 and Cyber Resilience Act) requiring real-time analytics | +1.9% | European Union, UK, Switzerland | Medium term (2-4 years) |

| In-venue sports betting and data licensing opening new revenue streams | +2.4% | United States, expanding to Canada and LATAM | Medium term (2-4 years) |

| Smart-city grants in APAC (e.g., India’s Khelo India 2.0) funding stadium IoT upgrades | +1.7% | India, China, Southeast Asia | Long term (≥ 4 years) |

| Green-Deal targets driving energy-efficient building automation in EU arenas | +1.5% | European Union and candidate countries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

5G Network Roll-outs Catalyzing High-Density Connectivity

Carrier investment in millimeter-wave and C-band spectrum is enabling stadiums to serve tens of thousands of concurrent users at multi-gigabit speeds, a feat that legacy distributed-antenna systems could not economically achieve. Verizon completed 5G Ultra Wideband builds across 28 NFL venues in 2024, supporting augmented-reality replays and in-seat betting that demand sub-20-millisecond latency.[1]Verizon Communications, “5G Ultra Wideband Deployment Across NFL Stadiums,” verizon.com Notre Dame Stadium’s 2024 Wi-Fi 6E overlay achieved an aggregate of 26 Gbps during a single game and is being paired with a private LTE core for deterministic IoT telemetry. European operators such as Vodafone and Deutsche Telekom are positioning stadium densification as anchor tenants for standalone 5G cores that also showcase slicing to municipal buyers. Dedicated small-cell grids reduce interference during peak ingress when device density exceeds 1,500 connections per access point. The resulting bandwidth is underpinning next-generation services that raise per-capita spending and sponsorship yield.

Mega-Event Pipeline Accelerating Digitization Budgets

The 2026 FIFA World Cup and 2028 Los Angeles Olympics are compressing decade-long refresh cycles into two-year sprints. Lenovo’s 2024 global deal with FIFA supplies edge servers and AI appliances to 16 venues across the United States, Mexico, and Canada. Mexico’s Estadio Azteca began a USD 150 million renovation in 2024, installing fiber-to-the-seat connectivity for 4K on-demand video. The LA28 organizing committee is utilizing Autodesk BIM workflows to integrate predictive maintenance that will continue beyond the games. These flagship builds create a demonstration effect that pushes secondary markets to upgrade to Olympic-grade standards, expanding the smart stadium market well beyond host cities.

EU Crowd-Safety Mandates Requiring Real-time Analytics

The Network and Information Security Directive 2, adopted in 2024, classifies large venues as essential entities and obliges them to deploy real-time anomaly detection for systems serving more than 10,000 attendees. The 2024 Cyber Resilience Act extends liability to hardware and software vendors, incentivizing operators to source integrated, certified platforms.[2]European Parliament, “Network and Information Security Directive 2,” europarl.europa.eu UEFA’s 2024 safety code now requires AI crowd-density analytics for Category 4 stadiums. As a result, clubs are consolidating supplier lists, favoring solutions from Cisco, Schneider Electric, and Siemens that arrive pre-certified and reduce audit scope. Compliance increases upfront costs but builds long-term barriers to entry, solidifying the incumbent's advantage within the smart stadium market.

In-Venue Sports Betting and Data Licensing Opening New Revenue Streams

U.S. legalization of mobile wagering is turning stadiums into real-time data generators. Sportradar’s live-odds engine processed more than 1.2 million betting events per day during the 2024 NFL season, aided by venue geofencing that enables enhanced odds offers for on-site fans. Genius Sports holds exclusive rights to distribute NFL player-tracking statistics through 2030, and venues typically earn multi-million-dollar annual fees for granting access to their data. Betting kiosks and mobile top-ups extend concession dwell time, boosting secondary spend on food and merchandise. The incremental revenue offsets sensor and edge-compute capital costs, making the economics of the smart stadium market more attractive to private operators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy system fragmentation elevating retrofit integration costs | -1.6% | Europe, venues built < 2010 | Medium term (2-4 years) |

| Rising cyber-liability under GDPR and CCPA slowing fan-data platforms | -1.3% | European Union and California | Medium term (2-4 years) |

| Prolonged municipal lease approvals delaying capital deployment | -1.2% | South America | Medium term (2-4 years) |

| Under-utilization rates below 40 event-days compressing ROI | -1.0% | Middle East private venues | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy System Fragmentation Elevating Retrofit Costs

European arenas built between 1990 and 2010 often run proprietary HVAC, access control, and surveillance platforms on disparate protocols such as BACnet, Modbus, and ONVIF. Converging these silos demands custom middleware and lengthy on-site commissioning, which can double the per-seat cost of a greenfield build. A 2024 Stadium Business Summit survey found that 63% of operators identified integration complexity as their top barrier to adoption, with retrofit timelines reaching 18 months for large venues. Operators must sometimes maintain parallel systems during migration, eroding ROI. Although the EU’s Energy Performance of Buildings Directive accelerates decommissioning of obsolete equipment, capital constraints and municipal lease restrictions slow wholesale replacement, weighing on smart stadium market growth.

Rising Cyber-Liability Under GDPR and CCPA

The GDPR allows fines of up to 4% of a company's global turnover for personal-data breaches, and the California Consumer Privacy Act extends deletion rights to biometric and location records. A 2024 Irish regulator ruling fined a football club EUR 2.8 million (USD 3.28 million) for inadequate mobile app consent, prompting peer venues to pause fan engagement pilots. Compliance now requires data-protection impact assessments, encryption at rest, and appointed data-protection officers, adding 15-25% to platform operating costs. California’s 2024 enforcement of geolocation rules further complicates wayfinding and crowd analytics deployments. These liabilities prompt operators to adopt anonymized edge processing, which limits cloud egress; however, the added complexity can slow rollouts and temper near-term smart stadium market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Momentum Builds on Service Foundations

Services anchored 51.88% of 2025 revenue as system integrators mapped legacy electrical, mechanical, and IT assets into a single IoT fabric. Software, however, is forecast to grow at a 15.02% CAGR, making it the fastest driver of smart stadium market growth. Operators prefer subscription licenses for building-automation and crowd-analytics modules that avoid forklift upgrades. Cisco’s 2024 Private 5G bundle illustrates the shift, combining radios, core software, and professional services into a single SKU. As commodity x86 servers replace proprietary appliances, venues cut the total cost of ownership and accelerate feature roll-outs. The smart stadium industry is increasingly treating software as the principal lever for new revenue streams, with hardware refreshes timed to coincide with carrier 5G roadmaps and Wi-Fi generational shifts.

Hardware occupies an essential middle ground. Edge gateways, access points, and sensor arrays must still meet broadcast-quality latency thresholds, particularly for real-time betting integrations. Replacement cycles align with the adoption of Wi-Fi 7 and the introduction of 6 GHz spectrum in major markets. Vendors that bundle firmware updates and AI inference capabilities into existing devices are best positioned to capture replacement demand. The evolving component mix underscores how the smart stadium market is migrating from capital-intensive builds toward recurring-revenue service models.

By Software Solution: Engagement Leads, Ticketing Accelerates

Digital Content and Fan Engagement software accounted for 28.10% of 2025 solution revenue, reflecting demand for mobile apps, in-seat ordering, and augmented-reality overlays that increase per-capita spending. Smart Ticketing and Parking, projected to post a 13.95% CAGR, is emerging as the breakout. Liverpool FC’s NFC roll-out cut average ingress times from 12 to 7 minutes and produced timestamped mobility data for advertisers. SKIDATA’s 2024 cloud parking solution, already live in Germany and Austria, integrates with city traffic systems to enable dynamic pricing.

Building Automation and Energy Management are converging around sustainability mandates; Schneider Electric’s EcoStruxure platform claims 20-30% energy savings, a compelling metric for EU operators facing near-zero-energy targets. Security software remains compliance-driven as UEFA and FIFA push AI crowd analytics into venue licensure. Across categories, modular, cloud-native design is expanding the addressable market for smart stadiums.

By Deployment Mode: Hybrid Architectures Dominate Roadmaps

On-Premise infrastructure represented 66.95% of installations in 2025, still critical where data sovereignty and sub-10-millisecond latency are non-negotiable. Yet, cloud deployments are forecast to expand at a 14.72% CAGR, as Amazon Web Services, Microsoft Azure, and Google Cloud offer hybrid blueprints that keep sensitive data on-site while scaling analytics in the cloud.

Riot Games’ “Project Stryker” demonstrates a model where on-premise SMPTE 2110 workflows feed AWS global production centers, delivering esports events with sub-5-millisecond switching. Europe’s 2024 Data Act, mandating IoT data portability, is further reducing lock-in fears. The emerging default is a split stack where deterministic applications live at the edge, and elastic workloads burst to the cloud, expanding the smart stadium market size without compromising compliance.

By Connectivity Technology: Wi-Fi Holds Core, 5G Gains Pace

Wi-Fi 6/7 secured 44.05% of 2025 deployments, leveraging incumbent access-point footprints and IEEE 802.11be’s deterministic latency. 5G and Private LTE, scaling at 14.05% CAGR, supply licensed-spectrum reliability for safety-critical functions like automated alerts and dynamic wayfinding.

JMA Wireless shipped distributed antenna systems to 15 NFL stadiums in 2024, supporting carrier aggregation and mmWave backhaul. Bluetooth Low Energy beacons add inexpensive proximity marketing, operating for up to five years on coin-cell batteries. Fiber backbones and containerized edge servers anchor all wireless layers, creating a converged fabric where Wi-Fi 7’s multi-link operation and 5G network slicing dynamically allocate bandwidth by application priority. The interplay of licensed and unlicensed spectrum is a defining feature of the smart stadium market.

By Application Area: Sports Events Prevail, Esports Climbs

Sports Events dominated with 75.60% of 2025 revenue, thanks to professional leagues and college athletics that mandate high reliability and monetize premium seating. Esports arenas, however, are slated for a 13.40% CAGR through 2031 as gaming audiences demand sub-5-millisecond latency and SMPTE 2110 video workflows. Riot Games built its own broadcast-class network stack to meet these requirements, then monetized the IP by licensing it to third-party venues.

Concerts and entertainment bookings generate high per-event revenue but face routing and rigging constraints that limit the number of available dates. Corporate events fill off-season calendars yet yield lower per-capita spend. Hybrid formats, which combine on-site and virtual attendance, are further expanding the smart stadium market by monetizing the same content twice, once at the gate and again on the stream.

By Revenue Stream: Traditional Anchors Meet Data Upside

Ticketing and Merchandise produced 35.30% of 2025 venue revenue and remains the economic anchor. Data Monetization and Betting, however, is projected to grow at 14.25% CAGR as operators license play-by-play feeds and biometric telemetry to sportsbook and media partners. Sportradar’s rights portfolio surpassed 750,000 events in 2024, underscoring the significant demand for real-time data.

Concessions benefit from mobile ordering, which lifts the average spend by 15-20%. Dynamic digital signage shifts advertising from static boards to per-impression pricing informed by real-time demographics. Unified digital wallets that integrate ticketing, concessions, and betting into a single account simplify settlement and open up cross-sell opportunities, deepening the revenue well for the smart stadium market.

Geography Analysis

North America led the smart stadium market with 37.10% share in 2025, lifted by mature betting regulations and aggressive 5G densification. Verizon’s dedicated small-cell grids and edge-compute nodes across 28 NFL venues enable augmented-reality replays and real-time wagering. Canada and Mexico are renovating ahead of the 2026 World Cup, with Estadio Azteca’s USD 150 million fiber-to-seat upgrade setting a regional benchmark. California’s privacy rules, however, compel venues to anonymize location data at the edge, which slows biometric rollouts.

The Middle East is projected to post the fastest regional CAGR at 14.45% thanks to sovereign-funded mega-venues aligned with Vision 2030. Riyadh’s King Salman Stadium is targeting net-zero energy through integrated solar arrays and AI crowd analytics, while Dubai Arena operates cashless concessions and dynamic parking. Underutilization below 40 event days per year threatens ROI, yet government backstops are mitigating refinancing risk to ensure showcase projects land on time, a dynamic that broadens the smart stadium market reach.

The Asia Pacific and Europe follow diverse adoption curves, shaped by public funding programs and regulations. India’s Khelo India 2.0 earmarked INR 30 billion (USD 360 million) in 2024-2025 for IoT upgrades in tier-2 stadiums. China’s 14th Five-Year Plan bundles stadium IoT into municipal bond packages, accelerating deployment in Guangdong and Zhejiang. Europe’s zero-trust and energy directives lift baseline costs but protect incumbents that can certify supply-chain security. Japan and South Korea leverage 5G penetration for cashless payments and AR fan experiences, yet seismic-code retrofits raise capital needs. Across regions, policy drivers and mega-event timetables dictate timing, but the underlying demand for connected fan experiences keeps the smart stadium market on a steady growth path.

Regulatory Landscape

Smart stadium deployments increasingly operate within telecom, cybersecurity, and data-governance regimes, not only building and venue rules. In the European Union, Directive (EU) 2018/1972 (European Electronic Communications Code, consolidated through October 2024) supports permitting and access obligations for high-capacity connectivity, while Regulation (EU) 2024/1309 targets faster roll-out of Very High Capacity Networks, shaping how venues procure fiber backbones, in-building wireless, and 5G-equivalent infrastructure.

Standards are also influencing procurement requirements for IoT, digital twins, and interoperability. WTSA-24 Resolution 98 (New Delhi, 2024) formalizes ITU standardization workstreams around IoT and smart sustainable cities, and ITU-T recommendations such as Y.4600 provide reference architectures for smart city digital twin systems that can be extended to large venues. In combination with data-governance anchors referenced in industry frameworks (for example, IEEE P7000 series and ISO/IEC TR 24030 for AI and data governance), these touchpoints raise expectations for cross-vendor integration, auditability, and secure-by-design deployments in connected venues.

Value Chain Analysis

The smart stadium value chain begins with semiconductor and device inputs (chipsets, cameras, sensors, access points, switching) and moves through connectivity layers (Wi-Fi 6/7, DAS, private LTE/5G), edge compute, and cloud platforms, before transitioning into application software for security, crowd management, ticketing/parking, digital content, and venue operations. System integrators and managed-service partners translate venue requirements into multi-domain designs, mapping legacy building systems and public safety operations into a unified network and data plane, while vendors increasingly package radios, core software, edge appliances, and professional services into bundled offerings to reduce integration time and operational handoffs.

Commercialization and delivery are anchored in multi-year venue partnerships and league-level programs that standardize deployments at scale. Examples include NWN being named the Official Technology Infrastructure Partner for the Kraft Group (covering Gillette Stadium and adjacent facilities), Cisco partnering with Monumental Sports and Entertainment for a new high-tech arena build-out, HPE becoming an exclusive network infrastructure and hybrid cloud partner for Miami Freedom Park and Inter Miami CF, and Extreme Networks extending its NFL partnership through 2028. These arrangements push demand into commissioning, cybersecurity operations, and lifecycle services, and they tighten interoperability needs across ticketing, payments, identity, and video workflows.

Competitive Landscape

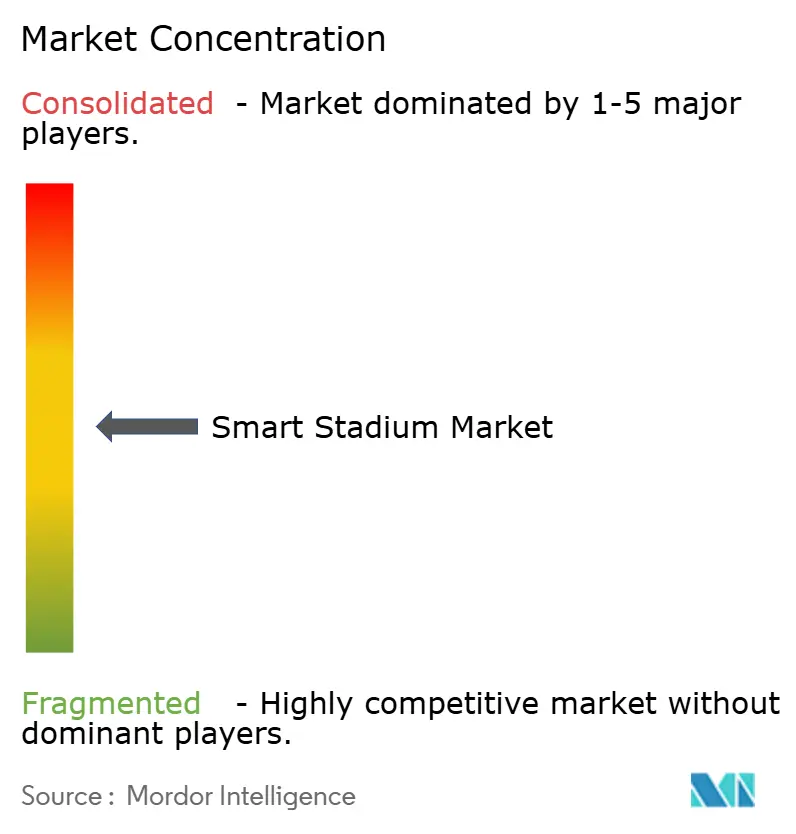

The smart stadium market is moderately fragmented. Global integrators such as Cisco, IBM, Huawei, and Johnson Controls compete on turnkey portfolios that bundle radio, edge computing, and analytics, locking in contracts for five to seven years. Cisco’s 2025 Private 5G update folds video-analytics edge appliances into a single SKU, halving deployment timelines for mid-sized venues. Hyperscalers partner with rights holders Riot Games’ Project Stryker funnels live esports feeds through AWS to secure high-margin workloads and deepen integration with venue data stacks.

Niche players thrive by filling gaps the giants overlook. JMA Wireless focuses on distributed antenna systems that aggregate carrier spectrum, while AllGoVision delivers AI-powered crowd analytics tuned for safety compliance. SKIDATA specializes in cloud-based ticketing and parking solutions that integrate with city traffic management platforms. Participation in IEEE 802.11be and SMPTE IP-video task forces signals the credibility of a long-term roadmap, an attribute operators weigh as they invest capital in twenty-year assets.

Regulation is quietly reshaping competitive dynamics. The EU Cyber Resilience Act’s CE-mark requirement is pushing uncertified devices out of tender lists and consolidating share among suppliers with audited supply chains.[4] European Commission, “Cyber Resilience Act,” digital-strategy.ec.europa.eu Vendors boasting end-to-end portfolios are better positioned to shoulder liability and deliver single-throat-to-choke assurances. Meanwhile, white-space opportunities persist in 10,000- to 30,000-seat venues that cannot afford bespoke builds, creating demand for managed-service models and keeping the door open for agile disruptors within the smart stadium market.

Smart Stadium Industry Leaders

-

Cisco Systems Inc.

-

IBM Corporation

-

Huawei Technologies Co. Ltd.

-

Johnson Controls International plc

-

Intel Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key opportunity is in converged connectivity and operations stacks that reduce the number of parallel networks and point tools inside venues. Recent projects reflect a shift from discrete upgrades to end-to-end platforms: HPE publicized a phased self-driving network program at Atletico de Madrid's Riyadh Air Metropolitano featuring Wi-Fi 7 access points, and Boldyn Networks described a converged connectivity deployment (Wi-Fi 7 plus neutral-host cellular/DAS) for Nu Stadium, Miami Freedom Park ahead of its April 2026 debut. These builds support repeatable templates for 10,000- to 30,000-seat venues that want enterprise-grade performance without bespoke integration, which in turn underpins managed-service models covering design, deployment, and ongoing assurance.

Mega-event and multi-operator complexity also creates whitespace for cross-border device provisioning, roaming, and data governance across heterogeneous infrastructure. Deutsche Telekom used the 2026 FIFA World Cup scenario to map an integrated IoT stack spanning 5G connectivity and real-time data for parking, logistics, and crowd management, reinforcing demand for interoperable digital-twin-ready architectures and standardized data interfaces. As stadium owners adopt Wi-Fi 7 for high-density seating while retaining private cellular for mobility-heavy operations, vendors that can certify security, orchestrate hybrid edge-cloud analytics, and integrate ticketing, identity, and video into a single command layer have a clearer expansion path beyond flagship venues.

Recent Industry Developments

- July 2026: Cisco was named Founding Partner for connectivity and cybersecurity for Valencia CF's Nou Mestalla, covering network infrastructure, Wi-Fi technology, and security capabilities. The deal positions Cisco deeper into greenfield stadium programs where the network, security, and operations tooling are designed together from the start.

- May 2026: Cisco and the United States Golf Association renewed their technology partnership for five years, extending joint work across venue and event technology initiatives. The renewal reinforces multi-year contracting in large public venues, supporting longer lifecycle roadmaps for networking, observability, and AI-enabled operations.

- November 2024: Riot Games and Cisco launched Project Stryker, combining on-premise SMPTE 2110 workflows with AWS remote production for sub-5-millisecond esports broadcasts. The architecture shows how hybrid edge-to-cloud media stacks are becoming a reference pattern for latency-sensitive events hosted in arenas and stadiums.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the smart stadium market is defined as revenue earned from technology solutions and related services that help venues run safer, more connected, and more efficient live events, and also improve fan experience through digital systems.

Scope exclusions: Construction and major civil renovation work, along with general event staffing that is not tied to a smart stadium technology contract, are excluded.

Segmentation Overview

-

By Component

- Hardware

- Software

- Services

-

By Software Solution

- Building Automation Management

- Stadium and Public Security

- Event and Crowd Management

- Digital Content and Fan Engagement

- Network Management

- Energy Management

- Smart Ticketing and Parking

-

By Deployment Mode

- On-Premise

- Cloud

-

By Connectivity Technology

- Wi-Fi 6/7

- 5G and Private LTE

- Distributed Antenna Systems (DAS)

- Bluetooth Low Energy / BLE Beacons

- Fiber and Edge Compute Infrastructure

-

By Application Area

- Sports Events

- Concerts and Entertainment

- Esports Tournaments

- Corporate and Other Events

-

By Revenue Stream

- Ticketing and Merchandise

- Concessions and Hospitality

- Advertising and Sponsorship

- Venue Rental and Non-Sport Events

- Data Monetization and Betting

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

South America

- Brazil

- Argentina

- Rest of South America

-

Asia Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia Pacific

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

-

Africa

- South Africa

- Egypt

- Rest of Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the base structure of the model and to sanity check the direction of the estimates. We referred to public sources such as ITU and FCC spectrum and connectivity references, IEEE and IETF publications for network standards, NIST guidance for cybersecurity, and government trade statistics portals for electronics and ICT-related import and export signals. We also reviewed stadium and sports venue updates shared by city authorities and venue operators, plus relevant filings and investor presentations from listed technology suppliers to understand solution mix and typical deal motions.

On top of this, we used paid subscriptions for company financials and intelligence, patent database scans, and import and export shipment-level signals where they helped validate pricing and shipment cadence for connectivity and venue hardware. The sources mentioned here are illustrative, and many other public and proprietary references were also used for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with solution providers, system integrators, venue and event operations teams, and connectivity specialists, so the model inputs were grounded in how deployments get budgeted and delivered. Because this is a global market, respondent input was balanced across APAC, EMEA, and the Americas to confirm regional adoption pace, typical project scope, and how software and services are bundled in contracts.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 16% | APAC: 47% |

| Mid tier: 56% | Functional/Unit leaders: 37% | EMEA: 30% |

| Smaller Players: 17% | Managers: 47% | Americas: 23% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where the demand pool is reconstructed from the installed base of large venues and their digital upgrade cycles, and then converted into annual spending using typical solution bundles and rollout intensity. To keep the totals realistic, we then corroborated the outputs with selective bottom-up approximations, including sampled project values for connectivity upgrades, software platform subscriptions, and integration services, and then adjusted for gaps where deal scope is not fully disclosed.

Key inputs that shaped the model included the pace of Wi-Fi 6/7 and private 5G adoption in venues, the share of on-premise versus cloud deployments, services attach rates in large integration projects, average refresh cycles for security and surveillance systems, and the penetration of fan engagement and digital content platforms. For forecasting, scenario analysis was used, and the scenarios were anchored to expert views on venue capex cycles, event calendar normalization, and tightening expectations on safety and data security. Where the bottom-up checks were thin, conservative assumptions were applied and then revisited through follow-up calls until the ranges tightened.

Data Validation & Update Cycle

Validation was done in steps so that obvious overcounts and missing pieces were caught early. Analysts compared the modeled totals with independent signals, such as venue upgrade announcements, connectivity build-out activity, and shifts in software and services mix reported by suppliers, and then investigated exceptions before sign-off. If a large variance showed up by region or offering type, respondents were re-contacted to confirm whether the change came from pricing, deployment delays, or scope differences.

The report is refreshed annually, and interim updates are made when material events occur that can shift adoption or pricing. Before delivery, a final analyst pass is completed to incorporate the latest public disclosures and newly validated primary inputs, so clients receive an updated view that aligns with current market conditions.

Mordor Intelligence's Smart Stadium Market Estimate Compared With Other Published Estimates

Published numbers for smart stadiums often differ because firms do not count the same set of revenues, and they also use different assumptions on what a venue upgrade includes. Differences in base year, currency timing, and how fast cloud and connectivity spending scales can further widen the spread.

Some external estimates lean toward a narrower definition that focuses mainly on software and services tied to event management and crowd operations, then treats connected infrastructure as a supporting mention. For Mordor Intelligence, the market total is counted only when the solution is deployed for stadium operations or fan engagement and is booked across hardware, software, and services, with construction-only work and generic staffing left out.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 19.12 B (2025) | |

| Global Consultancy A | USD 20.22 B (2025) | Uses a broader spend interpretation for venue digitalization that can pull in adjacent arena technology budgets and assumes faster year-one adoption of premium connectivity upgrades. |

| Trade Journal B | USD 16.59 B (2025) | Tracks a narrower revenue pool centered on software and services categories, which can undercount hardware-heavy connectivity and security refresh projects in large venues. |

The comparison shows that the spread is mostly explained by what gets counted as smart stadium spend and how quickly large venue upgrades are assumed to ramp in the base year. Our approach stays traceable to venue upgrade activity, offering mix, and realistic attach rates, which makes the estimate easier to reproduce and validate over time.

Key Questions Answered in the Report

How large is the smart stadium market in 2026?

The smart stadium market size reached USD 21.65 billion in 2026 and is projected to climb to USD 40.28 billion by 2031.

What CAGR is anticipated for smart stadium investments through 2031?

Aggregate spending is forecast to rise at a 13.22% CAGR over the 2026-2031 period.

Which region leads adoption of connected-venue technology?

North America held 37.10% share in 2025, supported by 5G densification and sports-betting legislation.

What is the fastest growing revenue stream inside connected venues?

Data monetization and betting is projected to expand at a 14.25% CAGR as leagues license real-time feeds to sportsbook and media partners.

Which connectivity technologies dominate new stadium builds?

Wi-Fi 6/7 remains the primary access layer but private 5G is advancing quickly, especially for latency-sensitive and mission-critical applications.

How are mega-events influencing upgrade cycles?

The 2026 FIFA World Cup and 2028 Los Angeles Olympics are compressing refresh timelines into two-year sprints, forcing operators to adopt edge-compute and private-network architectures sooner than planned.

Page last updated on: