Smart Polymers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

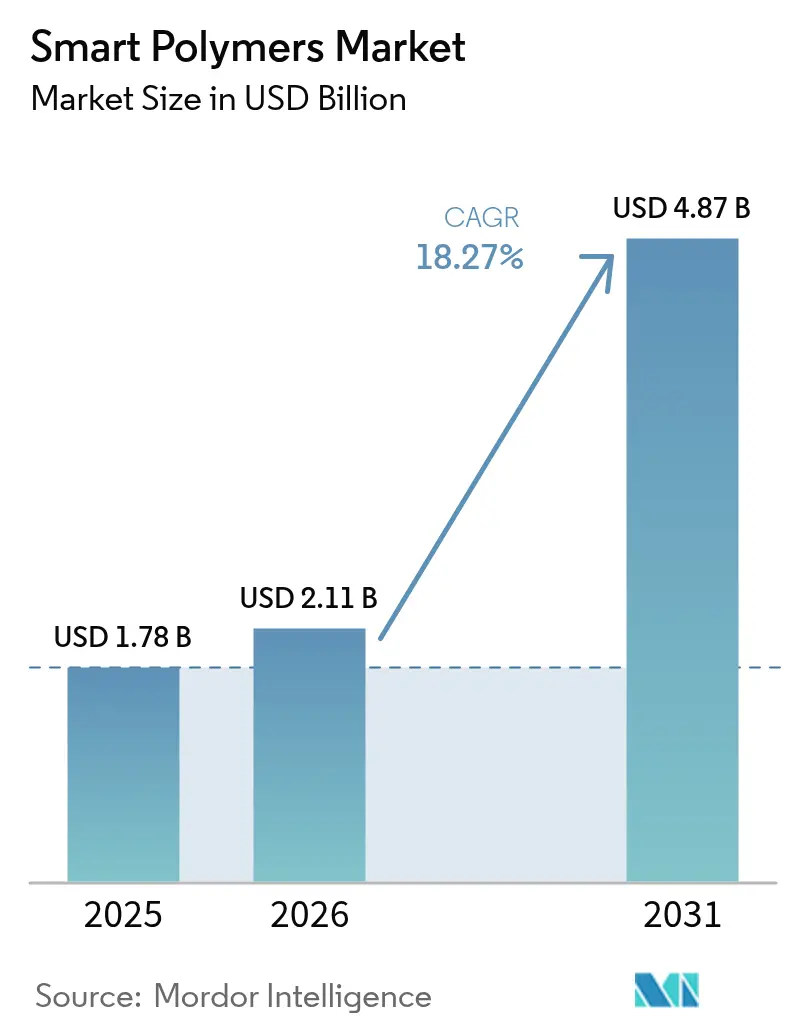

| Market Size (2026) | USD 2.11 Billion |

| Market Size (2031) | USD 4.87 Billion |

| Growth Rate (2026 - 2031) | 18.27% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Polymers Market Analysis by Mordor Intelligence

The Smart Polymers market size is expected to grow from USD 1.78 billion in 2025 to USD 2.11 billion in 2026 and is forecast to reach USD 4.87 billion by 2031 at 18.27% CAGR over 2026-2031. Momentum comes from rapid breakthroughs in materials chemistry, surging demand for minimally invasive healthcare solutions, and the accelerating replacement of passive plastics with responsive polymers in consumer electronics, textiles, and mobility. Asia-Pacific’s strong manufacturing base and government-backed research and development spending in China, Japan, and South Korea position the region as the primary production and consumption hub. Suppliers are diversifying product portfolios from single-trigger to multi-trigger systems to meet industry calls for tunable stiffness, autonomous healing, and embedded conductivity. Concurrently, capital-efficient scale-up technologies—continuous flow reactors, precision extrusion, and AI-guided formulation are narrowing the cost gap with conventional engineering plastics, widening adoption prospects in value-conscious sectors such as packaging and apparel.

Key Report Takeaways

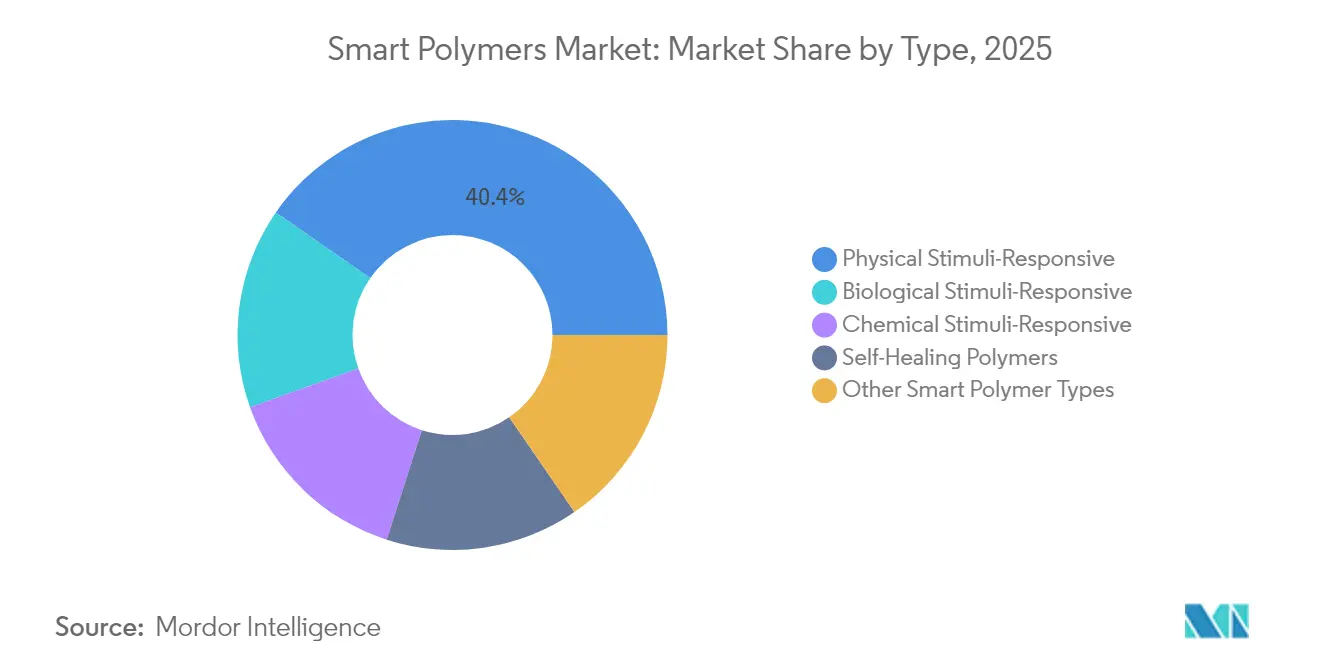

- By type, physical stimuli-responsive polymers held 40.35% of the Smart Polymers market share in 2025, while biological stimuli-responsive polymers are projected to grow at a 21.55% CAGR to 2031.

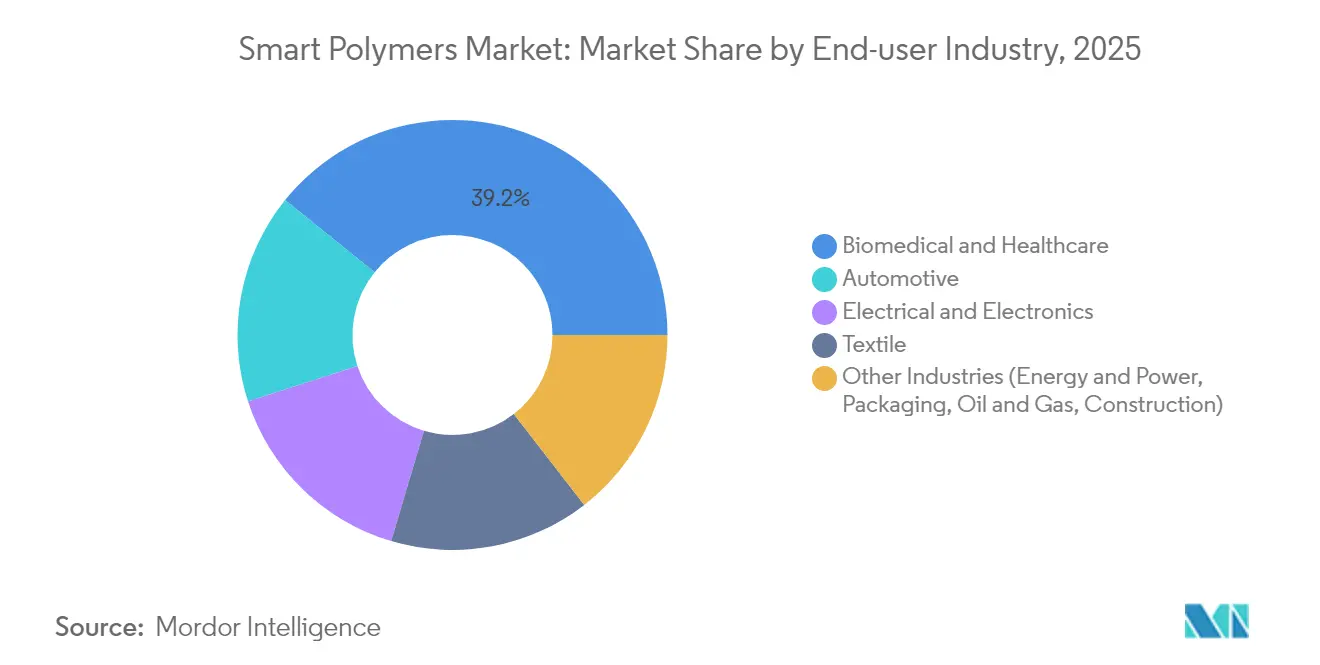

- By end-user industry, biomedical and healthcare accounted for 39.20% of the Smart Polymers market size in 2025 and is advancing at a 20.35% CAGR through 2031.

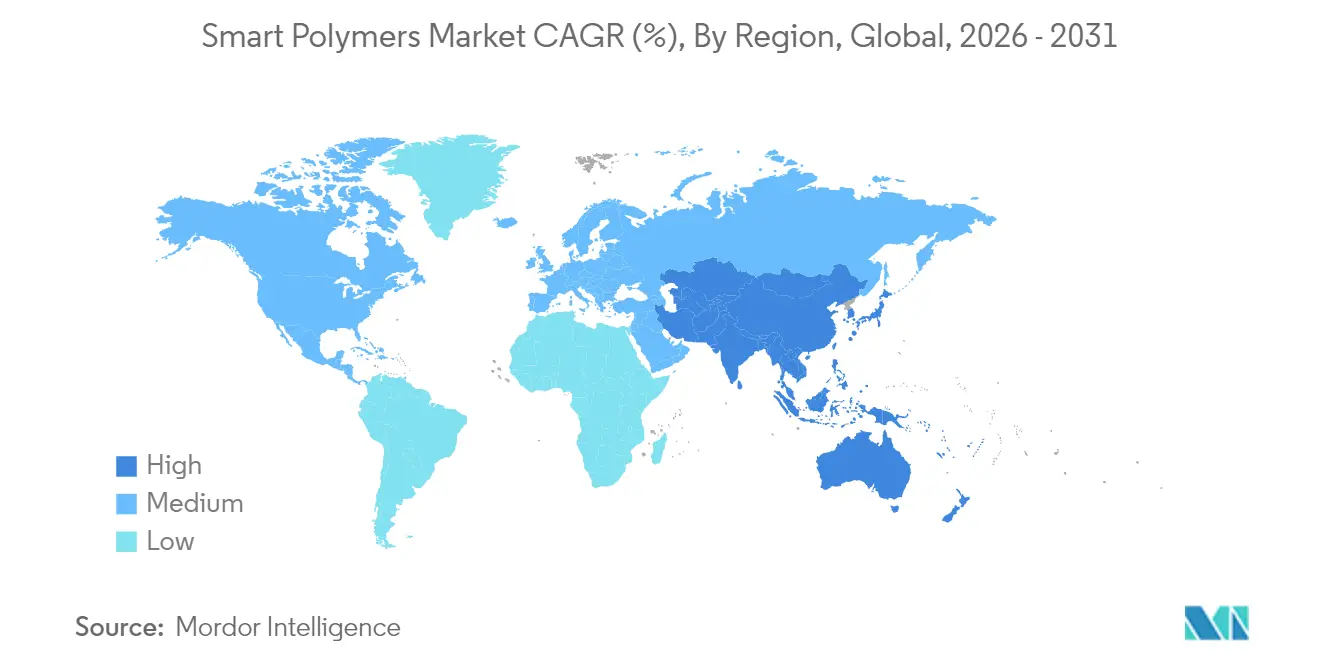

- By geography, Asia-Pacific commanded 35.30% revenue share of the Smart Polymers market in 2025 and is forecast to post the fastest regional CAGR at 19.05% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Polymers Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shape-memory polymers in textiles | +2.1% | Asia-Pacific, North America | Medium term (2–4 years) |

| Self-healing coatings demand | +3.4% | North America, Europe | Medium term (2–4 years) |

| Wearable-electronics boom | +4.2% | Asia-Pacific | Short term (≤2 years) |

| EU lightweight-composites mandates | +2.8% | Europe | Medium term (2–4 years) |

| 4-D printing in aerospace | +1.9% | North America, Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Increasing Application of Shape-Memory Polymers in the Textile Industry

Textile producers are embedding shape-memory polymers (SMPs) into fibers that actively regulate comfort by contracting or relaxing with temperature changes. Athleisure brands now specify SMP-blended yarns that wick moisture in high-heat conditions and tighten weave density when ambient temperatures fall, maintaining a stable microclimate around the wearer. SRTX Labs demonstrated ballistic-grade SMPs re-engineered for knits that are 10 times stronger than steel and lighter than water, integrating antimicrobial functionality without topical coatings. Universities are coupling SMP substrates with flexible sensor threads; a University of British Columbia team printed low-cost piezoresistive arrays that capture gait dynamics and vital signs, turning hoodies and compression sleeves into medical devices.

Self-Healing Coatings Demand

Electronics, automotive, and industrial OEMs are shifting from manual repainting and over-engineering toward coatings that autonomously repair scratches, micro-cracks, and pinholes. A landmark study by Cicoira produced PEDOT: PSS films doped with ethylene glycol and tannic acid that recover electrical integrity after 90% tensile strain, sustaining conductivity near 17 S cm-1 even after repeated cuts[1]Cicoira et al., “Self-Healable, Conductive Polymer Films,” rsc.org. The formulation adheres to metals, polyolefins, and thermoplastic polyurethanes, opening pathways in conformal sensors, flexible batteries, and corrosion-resistant architectural panels.

Wearable-Electronics Boom in Asia

In 2025, the Smart Polymers market benefits from Asia-Pacific’s surge in health-centric wearables, from glucose-tracking patches to exoskeletal sleeves. The University of Hong Kong’s in-sensor computing platform uses organic electrochemical transistors embedded in stretchable substrates, processing physiological data onboard while matching skin softness. Regional consumer-electronics brands integrate these conductive smart polymers into next-generation earbuds and smartwatches to eliminate rigid circuit boards, creating lighter form factors and always-on analytics.

EU Lightweight-Composites Mandates in Automotive

Stricter EU fleet-average emission limits have accelerated OEM substitution of steel with carbon-fiber-reinforced polymer (CFRP) structures that embed vibration-damping resins and shape-memory epoxy joints. CarbonTT’s CFRP chassis for the Fiat Ducato cut 185 kg, raising payload 36% without compromising torsional stiffness. Automobile interior Tier-1s are applying thermoplastic polyurethane (TPU) skins that self-heal seat scuffs under cabin temperatures, trimming warranty claims.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost and scale-up complexity | −3.5% | Global | Short term (≤2 years) |

| Regulatory uncertainty for clinical approvals | −2.7% | North America, Europe | Medium term (2–4 years) |

| Lack of recycling pathways | −1.8% | Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Production Cost and Scale-up Complexity

Laboratory batches rely on precision catalysts, cryogenic feeds, and multi-step purification. When scaled to tonne-level reactors, viscosity changes and side reactions hamper reproducibility, inflating unit costs beyond engineering polymers. Continuous-flow synthesis and reactive-extrusion lines promise cost compression, yet capital intensity remains high for SMEs, slowing entry into low-margin packaging and footwear markets.

Regulatory Uncertainty for Clinical Approvals

Medical smart polymers face divergent pathways under the FDA’s combination-product rules and the EU Medical Device Regulation. Developers must validate leachables, degradation by-products, and AI-assisted dosing algorithms, extending timelines and raising compliance spend. ISO 10993 biocompatibility testing demands cytotoxicity, genotoxicity, and systemic toxicity panels for any formulation tweak, deterring rapid iteration.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type

Though smaller in revenue today, the biological stimuli-responsive category is accelerating with a 21.55% CAGR as drug-delivery specialists exploit enzyme, glucose, and antigen triggers for targeted release. Physical stimuli-responsive grades still dominate 40.35% of the Smart Polymers market share, anchored by shape-memory alloys and thermochromic coatings specified in aerospace fairings and smart windows.

Researchers are merging pH and redox sensitivity into a single polymer backbone, enabling localized chemotherapeutic release only in the tumor micro-environment, reducing systemic toxicity. Hybrid platforms employ imprinted recognition sites that emulate antibodies yet withstand sterilization cycles. Such customizability is attracting diagnostics firms that embed these polymers into point-of-care biosensors.

By End-User Industry: Healthcare Extends Leadership

Biomedical and Healthcare applications capture 39.20% of the Smart Polymers market size today and sustain a 20.35% CAGR as minimally invasive therapies proliferate. Injectable nanocomposite hydrogels now orchestrate macrophage behavior, stimulating vascularized bone regeneration in complex fractures. Concurrently, pharma companies are reformulating depot injections with thermoresponsive carriers that gel at body temperature, enabling monthly dosing for chronic conditions.

Consumer health and military procurement intersect in fiber computers woven into base-layer garments that log core temperature, heart rate, and dehydration indicators during extreme-environment missions. Automotive OEMs and tier suppliers form the next demand wave, molding self-healing bumper skins and adaptive grilles that alter airflow for battery-electric vehicles.

Geography Analysis

Asia-Pacific leads with 35.30% of Smart Polymers market revenue and exhibits the fastest regional growth at 19.05% CAGR. China’s “Made in China 2025” program earmarks responsive materials as a strategic pillar, granting tax rebates for domestic production lines. Japanese conglomerates scale ionomer-based SEBS blends for haptic feedback actuators in gaming suits, while South Korean electronics giants co-develop stretchable circuit inks for foldable displays.

North America is backed by NIH and DARPA grants, funding bioresorbable stents and smart sutures. Collaborative clusters around Boston and the San Francisco Bay Area pair medical-device start-ups with contract manufacturing organizations that specialize in GMP-grade smart polymer extrusion.

Europe enforces stringent sustainability directives, catalyzing demand for recyclable and biodegradable grades. Horizon Europe projects sponsor bio-based thermoplastic elastomers designed for closed-loop recovery, aligning with automotive OEM decarbonization targets.

South America and MEA markets remain nascent, yet Brazil’s orthopedic-implant makers and the UAE’s smart-city initiatives are early adopters of moisture-responsive sealants and temperature-modulating facade panels.

Competitive Landscape

The Smart Polymers market displays moderate fragmentation. BASF, Covestro AG, and Evonik Industries, AG headline tier-one players, capitalizing on multipurpose pilot plants and global distribution. Mid-tier firms differentiate through application-specific chemistries. Start-ups concentrate on sustainability niches. Companies advancing polyhydroxyalkanoate-based smart polymers target compostable packaging.

Smart Polymers Industry Leaders

Covestro AG

BASF

Evonik Industries, AG

Huntsman International LLC

DuPont

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Covestro AG and Linxens have teamed up to create medical electronic skin patches to tackle challenges in material selection, manufacturing processes, and ensuring regulatory compliance for wearable devices designed for continuous health monitoring.

- August 2024: SABIC and Lubrizol have teamed up to create eco-friendly materials tailored for consumer electronics and mobility. This collaboration merges SABIC's LNP specialty compounds with Lubrizol's ESTANE ECO TPU.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the smart polymers market as the global sales value of engineered, stimuli-responsive polymer resins and formulated compounds that undergo a reversible, measurable change in physicochemical properties when exposed to triggers such as temperature, pH, electric or magnetic fields, or specific biomolecules. These materials are tracked at the point they leave the polymer manufacturer or compounder, before any further conversion into films, coatings, parts, or devices.

The study purposely omits conventional specialty plastics that only offer static high performance and also excludes smart composites where the active component is not the polymer itself.

Segmentation Overview

- By Type

- Physical Stimuli-Responsive

- Chemical Stimuli-Responsive

- Biological Stimuli-Responsive

- Self-Healing Polymers

- Other Smart Polymer Types

- By End-User Industry

- Biomedical and Healthcare

- Electrical and Electronics

- Textile

- Automotive

- Other Industries (Energy and Power, Packaging, Oil and Gas, Construction)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

We conducted structured interviews with polymer chemists at university spin-offs, sourcing managers at med-tech OEMs, and R&D directors at electronics molders across North America, Europe, and Asia-Pacific. These conversations validated functional loadings per device, realistic ASP corridors, and adoption pacing assumptions, filling gaps that desk work alone could not resolve.

Desk Research

Our analysts began with publicly available tier-1 data sets such as United States FDA 510(k) device clearances, Eurostat Prodcom output for HS3909 codes, global patent families from Questel, and polymer trade flows reported by UN Comtrade. Open-access journals (Advanced Functional Materials, Polymer Chemistry) and association papers from the International Federation of Robotics clarified emerging use cases, while company 10-Ks and investor decks revealed capacity shifts and average selling price (ASP) trajectories. Subscription sources, including D&B Hoovers for producer financials and Dow Jones Factiva for deal flow, helped us benchmark revenue baselines. The sources listed are illustrative; many additional publications and databases were reviewed during verification.

Market-Sizing & Forecasting

A combined bottom-up and top-down approach underpins the model. Top-down reconstruction uses medical implant procedure volumes, high-value plastics trade data, and average compound pricing to size demand pools, which are then pressure-tested against sampled supplier roll-ups and channel checks.

1. Annual orthopedic and cardiovascular implant counts. 2. Average kg of shape-memory polymer per implant. 3. Printed-electronics substrate square-meter output. 4. Smart-textile production meters. 5. Global polymer price index movements. 6. R&D spend by leading producers as a share of sales.

Multivariate regression, supplemented by scenario analysis for regulatory or price shocks, drives the 2025-2030 forecast curve. Where bottom-up estimates lacked country granularity, regional import data were prorated using device manufacturing footprints before final reconciliation.

Data Validation & Update Cycle

Model outputs pass variance checks versus historical trade, patent, and capacity data, followed by peer review among senior analysts. Reports refresh annually, and material market events trigger interim updates; a final validation sweep occurs immediately before client delivery.

Why Mordor's Smart Polymers Baseline Remains Dependable

Published figures often diverge because firms differ in scope choices, stimulus categories, and refresh timing. By anchoring the count strictly to resin-level sales and aligning triggers with ISO-recognized stimuli definitions, we minimize gray areas.

Key gap drivers include broader specialty-polymer inclusion by some publishers, unvetted ASP heuristics, and legacy base years that ignore recent capacity additions in Asia.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.78 B (2025) | Mordor Intelligence | |

| USD 12.84 B (2023) | Regional Consultancy A | Bundles smart polymers with smart materials; uses producer revenue gross of downstream conversion |

| USD 20.4 B (2022) | Global Consultancy B | Combines stimuli plastics with composites, relies on patent counts to extrapolate demand |

| USD 3.41 B (2023) | Trade Journal C | Applies single regional ASP globally; omits pH-responsive segment |

In short, our disciplined scope selection, variable transparency, and yearly refresh cadence give decision-makers a balanced baseline they can trace back to clear assumptions and publicly verifiable inputs.

Key Questions Answered in the Report

What is the current size of the Smart Polymers market?

The Smart Polymers market size is USD 2.11 billion in 2026, with forecasts pointing to USD 4.87 billion by 2031.

Which segment is growing the fastest?

Biological stimuli-responsive polymers are expanding at a 21.55% CAGR, outpacing other categories thanks to rising demand in targeted drug delivery.

Why is Asia-Pacific the largest regional market?

The region benefits from integrated electronics and textile supply chains, supportive government research and development funding, and a large consumer base adopting health-monitoring wearables.

How are self-healing polymer coatings used in industry?

They autonomously repair scratches and micro-cracks, extending product life in automotive body panels, consumer electronics casings and infrastructure coatings.

What are the main barriers to commercialization?

High production costs during scale-up and regulatory complexity, especially for medical applications, represent the primary restraints affecting market adoption.

Page last updated on: