Size and Share of Mergers And Acquisitions Of Diabetes Drugs And Device Companies

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

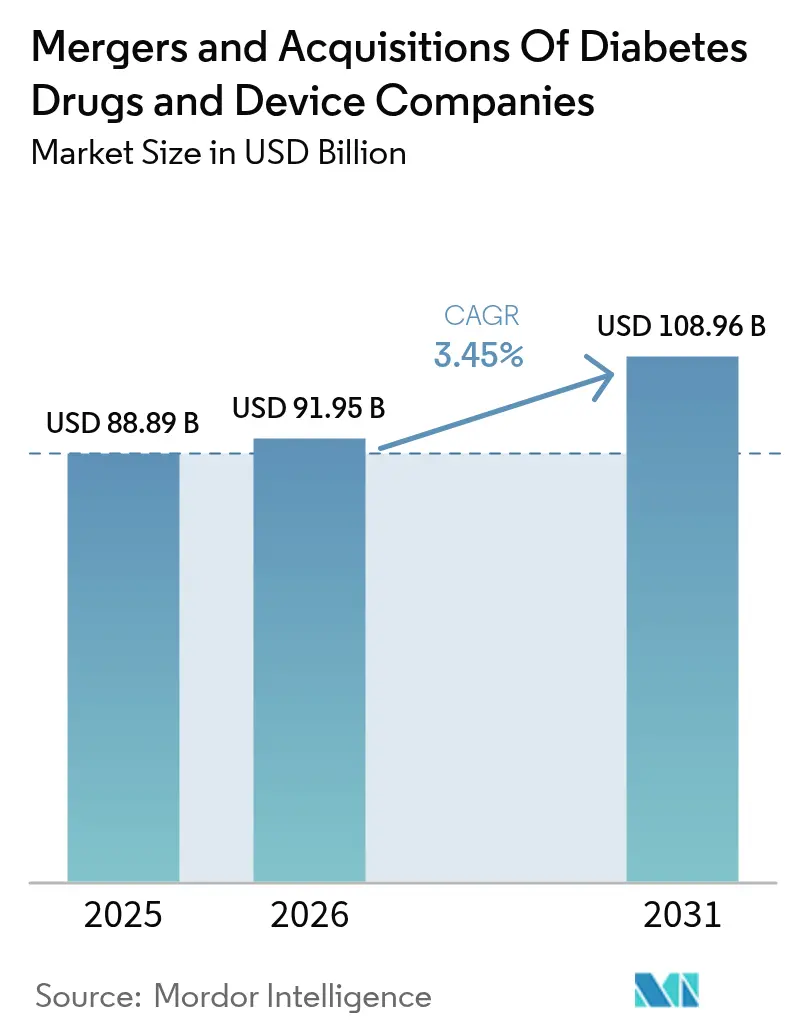

| Market Size (2026) | USD 91.95 Billion |

| Market Size (2031) | USD 108.96 Billion |

| Growth Rate (2026 - 2031) | 3.45% CAGR |

| Fastest Growing Market | North America |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Mergers And Acquisitions Of Diabetes Drugs And Device Companies by Mordor Intelligence

The Mergers And Acquisitions Of Diabetes Drugs And Device Companies Market size in 2026 is estimated at USD 91.95 billion, growing from 2025 value of USD 88.89 billion with 2031 projections showing USD 108.96 billion, growing at 3.45% CAGR over 2026-2031.

Diabetes is a chronic condition characterized by high blood glucose levels caused by the inability to produce or use insulin effectively. Diabetes treatment aims to maintain healthy blood glucose levels to prevent short- and long-term complications, such as cardiovascular disease, kidney disease, blindness, and lower limb amputation. Furthermore, patients attempting to tightly control their blood glucose levels to prevent long-term complications associated with fluctuations in blood glucose levels are at a greater risk for overcorrection and the resultant hypoglycemia. Achieving nominal results can be very difficult without diabetes care devices and medications.

Mergers and acquisitions help manufacturers achieve exponential, rather than linear, growth, thereby continuing to capture the interest of investors. Mergers and acquisitions are critical tools for strategy implementation. Deal-making is crucial for implementing game-changing strategic actions and building organizations that are ready to face future challenges. However, diabetic businesses use mergers and acquisitions as a routine part of their business model to gain access to innovation, as well as to optimize manufacturing operations and prune business portfolios.

The key factors driving mergers and acquisitions are strategic changes to achieve the segment's critical size requirement and large mergers that allow the bundling of subcritical businesses to build new platforms. The other driving force behind mergers and acquisitions is efficient capital allocation across the industry, which applies to R&D and manufacturing. The originators' large, complex organizations are unsuitable for fostering innovation. An ecosystem of venture capital and entrepreneurs has proven far more effective in identifying and allocating funds to early-stage biomedical research opportunities. Essentially, venture capitalists pre-fund diabetes drug companies' early-stage development.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Insights and Trends of Mergers And Acquisitions Of Diabetes Drugs And Device Companies

Rising Diabetes Prevalence encouraging players to focus on enhancing growth and market presence through Mergers and Acquisitions, Partnerships, and Collaborations

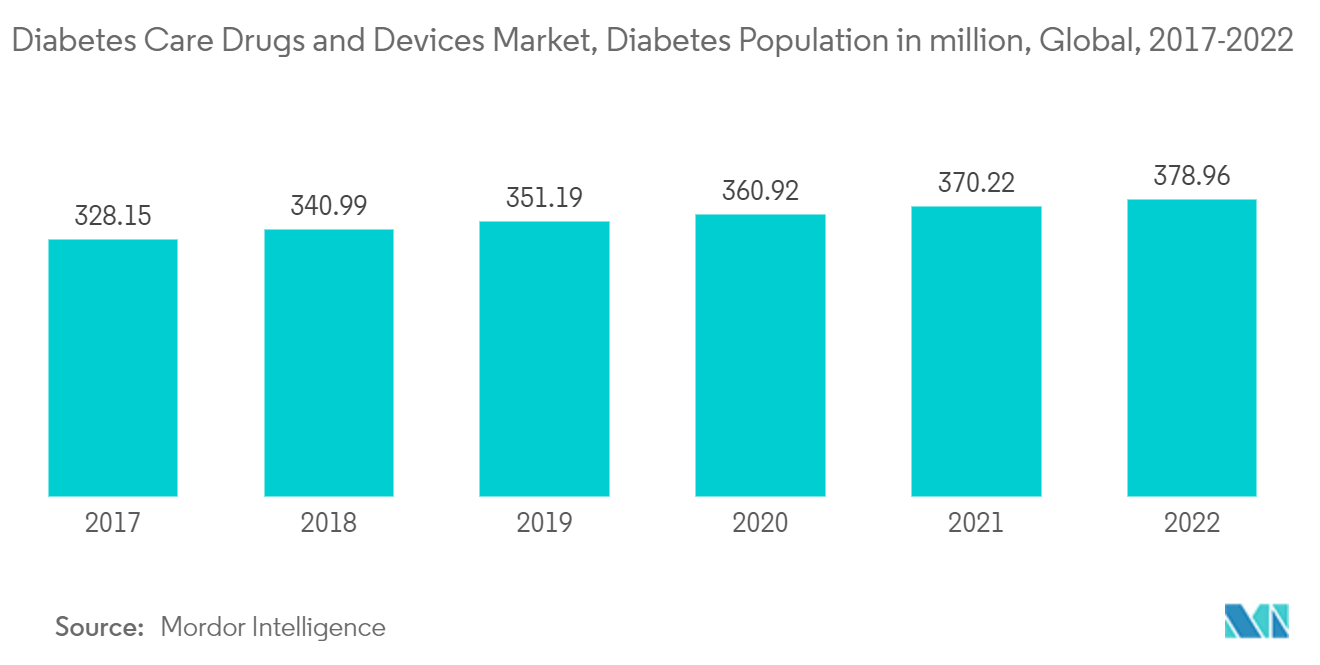

The diabetes population is expected to rise by 1.92% globally over the forecast period.

According to IDF, the adult diabetes population in 2021 was approximately 537 million, likely increasing by 643 million in 2030. The rate of newly diagnosed Type-1 and Type-2 diabetes cases is seen to increase, mainly due to obesity, unhealthy diet, and physical inactivity. An increased number of people are at risk of prediabetes, which can further lead to Type-2, causing risk factors for complications, acute and long-term complications, and deaths. The increased prevalence of diabetic patients and healthcare expenditure worldwide are indications of the increased inclination toward diabetic products.

WHO launched a Global Diabetes Compact, a global initiative aiming for sustained improvements in diabetes prevention and care, focusing on supporting low and middle-income countries. The compact is bringing together national governments, UN organizations, nongovernmental organizations, private sector entities, academic institutions, philanthropic foundations, people living with diabetes, and international donors to work on a shared vision of reducing the risk of diabetes and ensuring that all people who are diagnosed with diabetes have access to equitable, comprehensive, affordable, and quality treatment and care.

Mergers and acquisitions have increased significantly, with buyers and sellers looking to create more strategic, operational, and financial values. The key factors driving the diabetes market's mergers and acquisitions are strategic changes to achieve the critical size required in the segment and large mergers that allow the bundling of subcritical businesses to build new platforms. Efficient capital allocation across the industry is the other driving force behind mergers and acquisitions. Through Mergers and acquisitions activity, players in the diabetes market are expanding their product offerings. Also, players focus on expanding their geographical reach through Mergers, acquisitions, and partnerships with other established players. In August 2021, United Kingdom digital health startup Gendius signed a contract with AstraZeneca to confirm its strategic partnership to develop remote diabetes management and support patients in Gulf Cooperation Council (GCC) countries. Such partnerships will help the market players' growth over the forecast period.

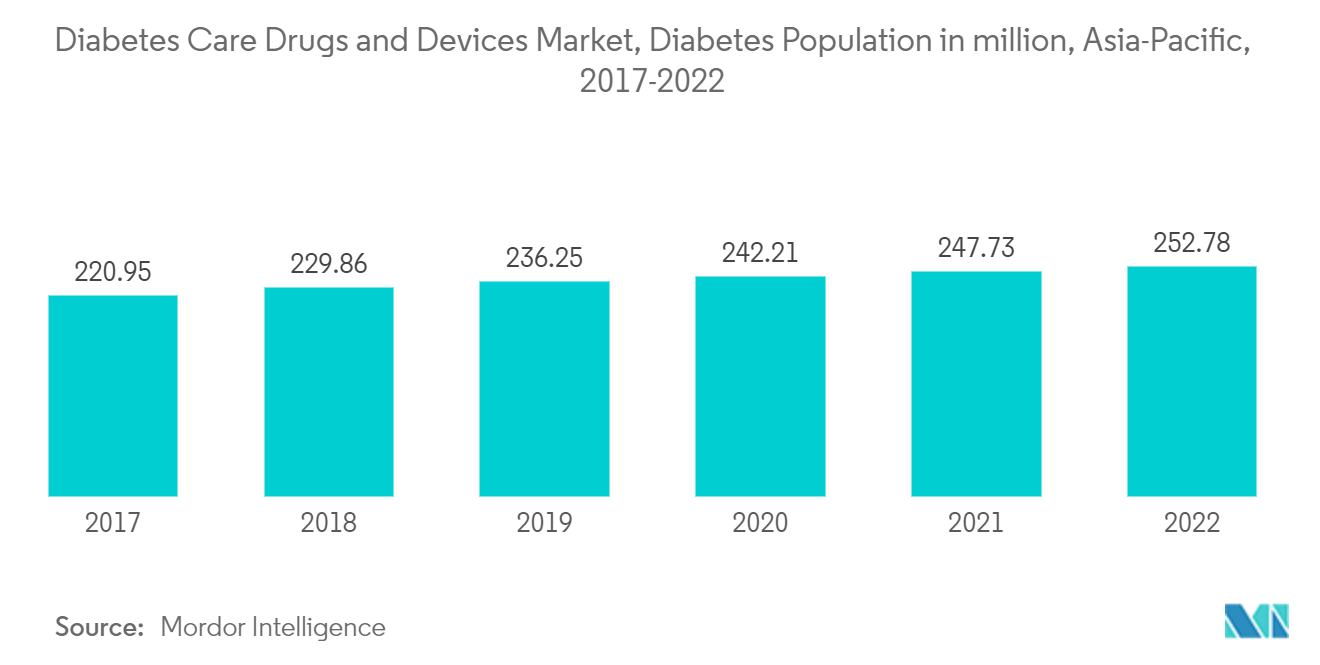

Companies Focusing on Growth Opportunities in Asia-Pacific Region

According to the International Diabetes Federation's latest estimates, the diabetes population in Southeast Asia and the Western Pacific region are projected to increase to 68% and 26% respectively, by 2045. Asia-Pacific, with the largest diabetic population worldwide, offers significant growth opportunities for players in the market. Hence, players focus on growing in the key markets of the region through collaborations and strategic partnerships. Players are entering strategic collaborations to jointly explore integrated solutions aimed at advancing intelligent healthcare in the region.

Companies also focus on expanding their product offerings in key growth markets in the region through partnerships. For instance, in March 2023, Astellas Pharma Inc. entered into an agreement with Roche Diabetes Care Japan Co., Ltd. for the development and commercialization of Roche Diabetes Care's Accu-Chek Guide Me blood glucose monitoring system with advanced accuracy as a combined medical product with BlueStar. BlueStar is an FDA-cleared digital health solution for diabetes patients, developed by Welldoc, Inc., and is currently marketed in the United States and Canada. Astellas and Welldoc are jointly developing BlueStar in Japan. In the future, Astellas will aim to obtain regulatory approval and reimbursement as a combined medical product.

Such strategies are expected to drive the growth of the players in the region during the forecast period.

Competitive Landscape

Some prominent players are Medtronic, Eli Lily, Sanofi, Dexcom, and Novo Nordisk, among others. Mergers and acquisitions between players in the recent past helped companies strengthen their market presence and develop capabilities that are novel to the companies. For instance, in July 2021, Eli Lily and Company announced the acquisition of Protomer Technologies Inc. to focus on advancing glucose-responsive insulins and accelerate the development of next-generation protein therapeutics.

Leaders of Mergers And Acquisitions Of Diabetes Drugs And Device Companies

Eli Lily and Company

Sanofi Aventis

Dexcom

Novo Nordisk

Medtronic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2023: Sanofi announced that it will pay USD 25 per share in cash or about USD 2.9 billion for Provention Bio; the deal is expected to close in the second quarter of 2023. The deal gives Sanofi access to Provention's approved immunotherapy Tzield, designed to stall the progression of type 1 diabetes.

- February 2023: Insulet acquired assets related to Bigfoot Biomedical's pump-based automated insulin delivery (AID) technologies for USD 25 million. Insulet and Bigfoot offer two distinct forms of diabetes-management care: Insulet's Omnipod system that delivers insulin via a wearable, tubeless pump dubbed the Pod and a remote controller called the Personal Diabetes Manager (PDM). Bigfoot's Unity provides injection support technologies that leverage smartpen caps and provide dose suggestions to patients based on continuous glucose monitoring data and provider recommendations.

Scope of Report on Mergers And Acquisitions Of Diabetes Drugs And Device Companies

Mergers and acquisitions are business transactions in which the ownership of companies, business organizations, or their operating units are transferred to or consolidated with another company or business organization. The Mergers and Acquisitions of Diabetes Drugs and Device Companies includes analysis by Geography, Mergers and Acquisitions, Partnerships, and Collaborations among primary drug and device companies. The report provides detailed company profiles of companies that provide diabetes care drugs and devices, including business overviews, products and services, financial information, contracts, mergers and acquisitions, joint ventures, collaborations, and other business agreements and strategies adopted by leading players in the market. The report covers all significant mergers and acquisitions, partnerships, and collaborations related to diabetes care drugs and devices.

Key Questions Answered in the Report

How big is the Mergers and Acquisitions of Diabetes Drugs and Device Companies?

The Mergers and Acquisitions of Diabetes Drugs and Device Companies analysis is expected to reach USD 91.95 billion in 2026 and grow at a CAGR of 3.45% to reach USD 108.96 billion by 2031.

What are the current Mergers and Acquisitions of Diabetes Drugs and Device Companies size?

In 2026, it is expected to reach USD 91.95 billion.

Who are the key players in Mergers and Acquisitions of Diabetes Drugs and Device Companies?

Eli Lily and Company, Sanofi Aventis, Dexcom, Novo Nordisk and Medtronic are the major companies operating in the Mergers and Acquisitions of Diabetes Drugs and Device Companies

Which is the fastest growing region in Mergers and Acquisitions of Diabetes Drugs and Device Companies?

North America is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Mergers and Acquisitions of Diabetes Drugs and Device Companies??

In 2025, the North America accounts for the largest market share in Mergers and Acquisitions of Diabetes Drugs and Device Companies.

Page last updated on: