Smart Kitchen Appliances Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

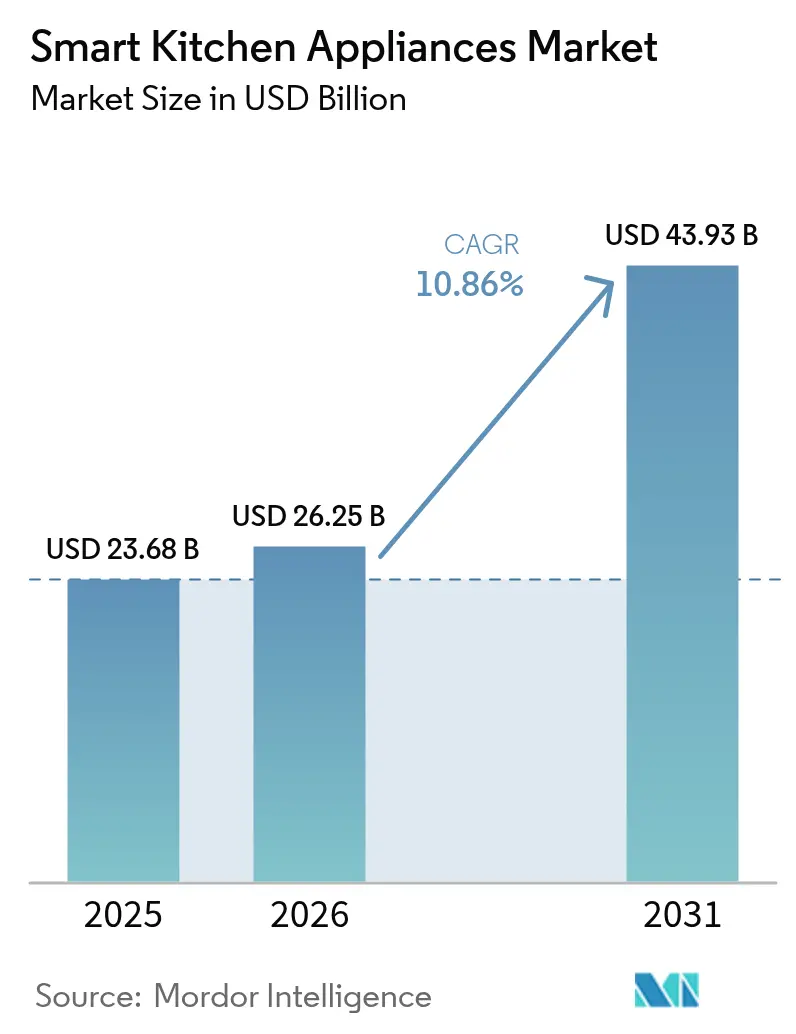

| Market Size (2026) | USD 26.25 Billion |

| Market Size (2031) | USD 43.93 Billion |

| Growth Rate (2026 - 2031) | 10.86% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

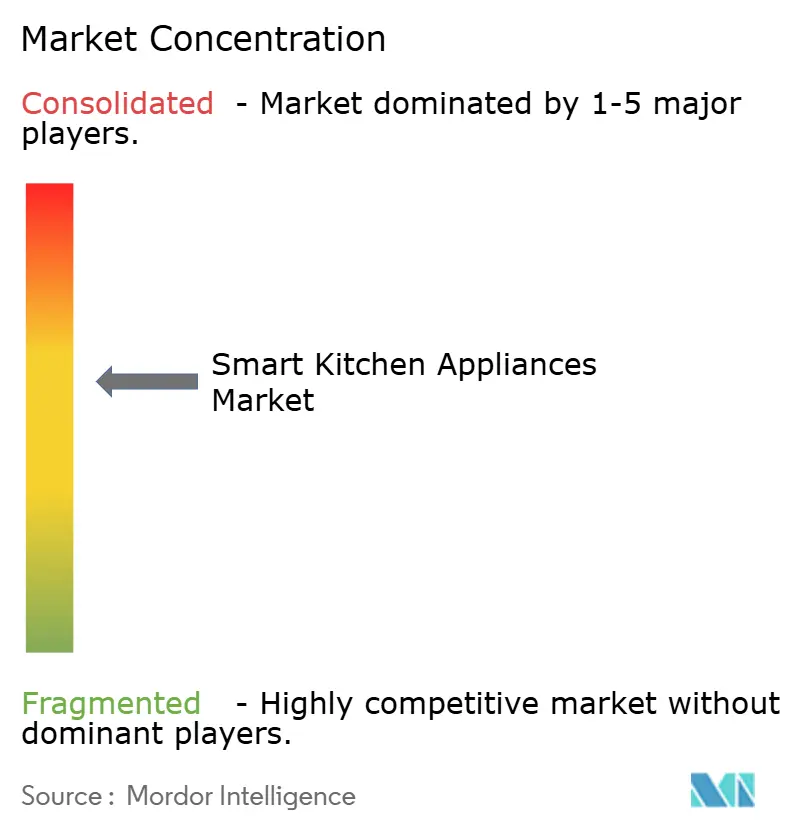

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Kitchen Appliances Market Analysis by Mordor Intelligence

The smart kitchen appliances market size is expected to grow from USD 23.68 billion in 2025 to USD 26.25 billion in 2026 and is forecast to reach USD 43.93 billion by 2031 at 10.86% CAGR over 2026-2031. Heightened household connectivity, tightening energy-efficiency mandates, and rapid AI infusion collectively underpin the upward revenue trajectory. Manufacturers are competing on ecosystem breadth, embedding voice control, in-appliance vision, and predictive maintenance features that raise perceived value and drive replacement demand. Semiconductor shortages remain the primary supply-side risk, yet most tier-one vendors have diversified sourcing strategies that partially insulate production schedules. Platform partnerships between appliance brands and tech giants further amplify consumer switching costs and unlock ancillary revenue through digital services.

Key Report Takeaways

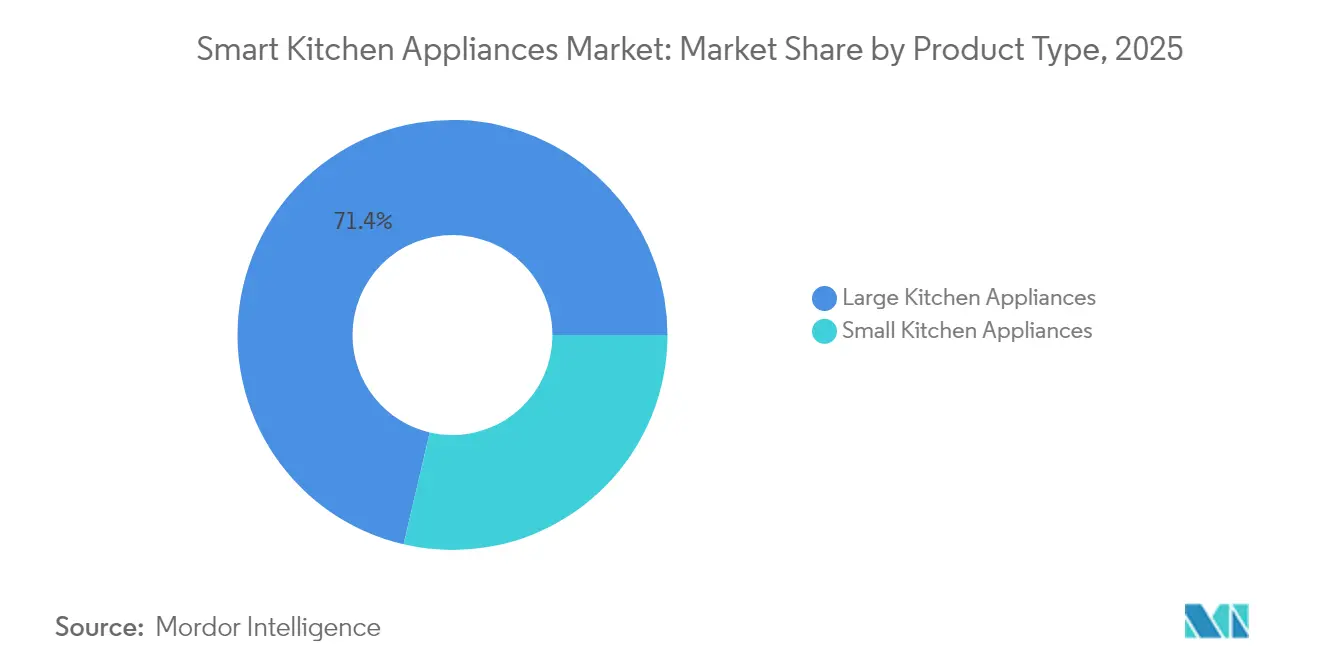

- By product category, large appliances held 71.35% of the smart kitchen appliances market share in 2025, while small appliances are forecast to post a 14.36% CAGR through 2031.

- By end user, the residential segment commanded 80.25% share of the smart kitchen appliances market size in 2025; commercial applications are projected to expand at an 11.42% CAGR to 2031.

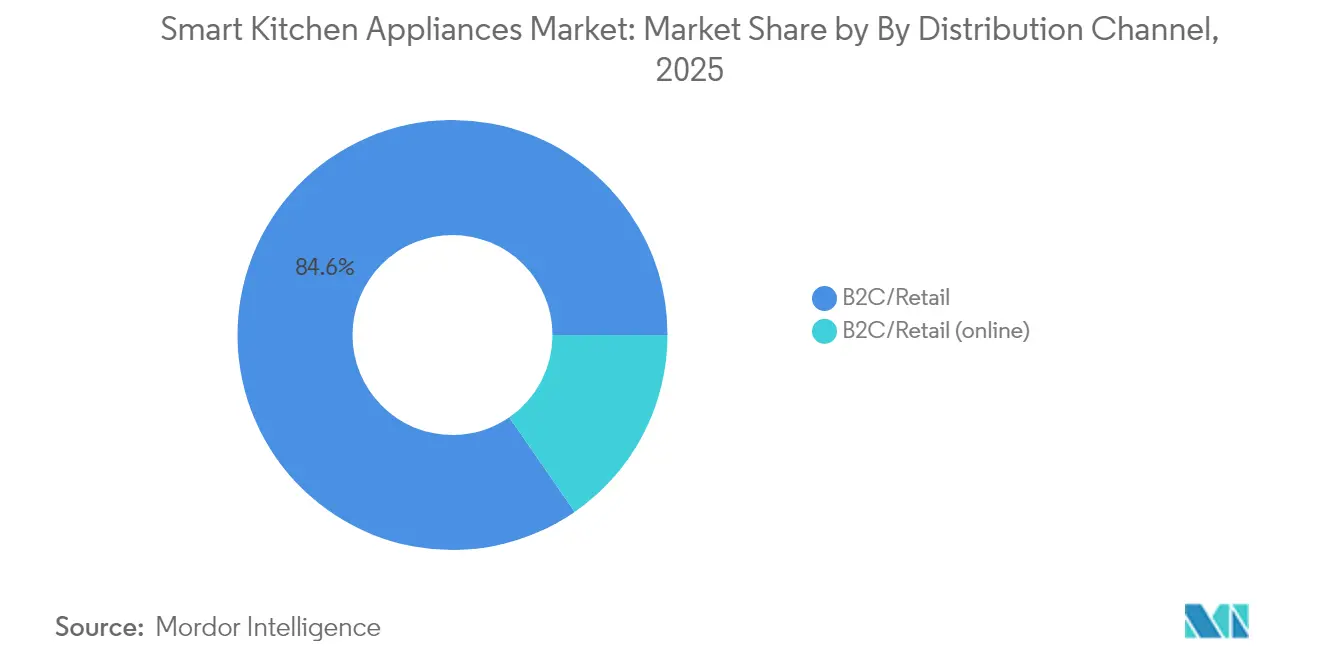

- By distribution channel, B2C retail controlled 84.62% revenue share in 2025, whereas online sub-channels within B2C are advancing at a 14.52% CAGR through 2031.

- By geography, North America led with 33.78% smart kitchen appliances market share in 2025; Europe is expected to record the quickest regional CAGR at 11.98% by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Kitchen Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising household adoption of IoT-enabled appliances | +2.1% | Global (North America & Europe lead) | Medium term (2-4 years) |

| Energy-efficiency regulations & incentives | +1.8% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Growing e-commerce penetration for appliance sales | +1.5% | Global, strongest in urban markets | Short term (≤ 2 years) |

| Premiumisation in residential renovations | +1.2% | North America & Europe | Medium term (2-4 years) |

| Edge-AI embedded cooking-assist features | +0.9% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Food-waste-tracking subscriptions bundled with fridges | +0.7% | North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Household Adoption of IoT-Enabled Appliances

High-speed internet ubiquity and affordable sensor modules lower adoption barriers, letting brands embed connectivity as a default rather than a premium add-on. Samsung’s 2024 Bespoke AI launch illustrates how natural-language voice assistants turn complex tasks into casual commands, boosting daily engagement with smart features. Younger demographics treat remote monitoring and recipe automation as baseline expectations, changing the purchase criteria that once revolved solely around capacity and finish. Network effects inside multi-device ecosystems foster repeat purchases and reinforce brand loyalty when expansion or replacement cycles arise.

Energy-Efficiency Regulations & Incentives

The U.S. Department of Energy finalized new cooking-product standards in 2024, with compliance mandated by 2028; connected appliances can algorithmically meet these stringent thresholds more easily than analog counterparts[1]Source: U.S. Department of Energy, “Energy Conservation Program: Cooking Products; Energy Conservation Standards,” energy.gov. New York State’s appliance rules and Canada’s Amendment 18 further widen the regulatory net, compelling manufacturers to prioritize smart controls that fine-tune electricity draw while maintaining performance. Across the Atlantic, Europe’s Eco-design directives tighten minimum efficiency levels, nudging consumers toward products that quantify savings in real time. Because energy bills remain elevated, AI-powered optimization functions resonate financially as well as environmentally, improving willingness to pay premium prices. Vendors that certify early enjoy multi-year first-mover advantages before lagging rivals complete re-tooling.

Growing E-Commerce Penetration for Appliance Sales

Digital storefronts streamline comparison shopping, facilitate user-generated content, and support virtual demonstrations that replicate showroom interactions without high overhead. Pandemic-era comfort with ordering big-ticket items online has persisted, and top brands now allocate disproportionate launch budgets to direct-to-consumer channels. Rich product pages explain connectivity benefits in depth, often bundling extended warranties and installation services that historically required in-store consultants. Data collected post-sale enables appliance makers to upsell subscription features such as recipe libraries or predictive maintenance alerts, diversifying revenue beyond one-time hardware margins. Urban consumers embrace doorstep delivery combined with haul-away of legacy units, removing a key logistical barrier that once favored brick-and-mortar outlets.

Premiumisation in Residential Renovations

The National Kitchen & Bath Association lists connected cooking suites as a leading remodeling priority for 2025, reflecting homeowner desire for future-proof investments[2]Source: National Kitchen & Bath Association, “2025 Design Trends Report,” nkba.org. Built-in smart ranges, refrigerators, and dishwashers integrate seamlessly with cabinetry and raise property resale value, justifying their higher price tags. Brands like BSH and Samsung respond by expanding bespoke finish options while keeping connectivity uniform across the range, ensuring aesthetic cohesion without sacrificing functionality. Renovation cycles span well over a decade, so appliances installed today will anchor brand ecosystems until at least the late 2030s. This lock-in effect encourages vendors to bundle extended service plans and software updates, reinforcing customer retention over multiple product generations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost versus conventional appliances | -2.3% | Global (strongest in emerging economies) | Short term (≤ 2 years) |

| Consumer data-privacy & cyber-risk concerns | -1.7% | North America & Europe | Medium term (2-4 years) |

| Inter-brand interoperability gaps | -1.1% | Global, accentuated in mixed-brand homes | Medium term (2-4 years) |

| Supply-chain exposure to SiC/GaN chip shortages | -0.8% | Global, concentrated in high-end segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Versus Conventional Appliances

Smart models command 20-40% premiums, stretching household budgets in regions where discretionary income remains tight. Installation of induction-based cooking appliances may also necessitate electrical upgrades, amplifying the initial cash outlay. To overcome sticker shock, vendors experiment with low-interest financing, trade-in credits, and modular upgrade paths that spread expenditure over time. Government rebate schemes tied to energy efficiency help but vary widely by jurisdiction, creating uneven global adoption curves. As component costs fall and economies of scale deepen, price gaps are likely to narrow, yet affordability will stay a gating factor in many emerging markets.

Consumer Data-Privacy & Cyber-Risk Concerns

Academic assessments of IoT firmware frequently uncover weak encryption and default credentials that hackers can exploit, heightening anxiety around connected kitchens. Privacy-sensitive shoppers fear that usage patterns and voice recordings could be harvested for targeted advertising or fall into malicious hands. Incidents involving camera-equipped devices intensify scrutiny and prompt calls for mandatory security labeling similar to energy ratings. Industry alliances now promote secure-boot processes, over-the-air patching, and end-to-end encryption as baseline requirements, yet consumer education remains inconsistent. Manufacturers that certify to robust frameworks such as Matter and implement transparent data policies will gain trust advantages over less proactive rivals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Large Appliances Sustain Volume While Compact Devices Spark Innovation

Large appliances commanded 71.35% of the smart kitchen appliances market in 2025, anchored by refrigerators, dishwashers, and cooking ranges that integrate deeply with household routines. Samsung’s AI Vision refrigerator, capable of recognizing 37 food items and generating automatic grocery lists, illustrates how core appliances have become digital hubs. Regulatory headwinds accelerate dishwasher replacement, as upcoming efficiency rules in 2027 favor models with adaptive wash algorithms that trim water and electricity usage. Oven innovation centers on embedded cameras such as GE Appliances’ CookCam, which, paired with edge-AI, predicts doneness and prevents over-cooking, reinforcing premium positioning. Because these items carry multi-year warranties and longer lifecycles, brand lock-in is strong, encouraging manufacturers to expand adjacent services like recipe subscriptions.

Small kitchen appliances, although holding a smaller revenue base, are forecast to grow at a 14.36% CAGR through 2031 due to urbanization and demand for multifunctionality. Connected air fryers, smart coffee makers, and countertop ovens introduce features, remote start, automatic ingredient detection, nutritional tracking, that once appeared only in flagship ranges. Lower average selling prices shorten replacement cycles, letting brands iterate software features quickly and test consumer appetite for paid upgrades. Voice-assistant compatibility has become table stakes, while smartphone apps push firmware updates that unlock new cooking modes post-purchase, enhancing perceived value. As a result, compact devices act as entry points, onboarding first-time buyers who may later upgrade to full smart suites.

Segment 2

Residential applications capture 80.25% market share in 2025, reflecting widespread consumer adoption of smart home technologies and increasing comfort with connected appliances that enhance daily cooking and food management experiences. Home kitchens serve as primary testing environments for smart appliance innovations, with consumers driving demand for features like voice control, remote monitoring, recipe assistance, and energy management capabilities that improve convenience and efficiency. The residential segment benefits from declining smart home technology costs, improved internet infrastructure, and growing consumer familiarity with IoT devices that reduce adoption barriers and accelerate market penetration. Smart refrigerators in residential applications increasingly incorporate food waste tracking capabilities, with systems like Enhanced Refrigerator with Quality and Quantity Monitoring (ERQQM) using RFID and sensors to monitor food conditions and alert users about spoilage.

Commercial applications demonstrate faster growth at 11.42% CAGR through 2031, driven by hospitality operators recognizing operational efficiency gains, food safety improvements, and cost reduction opportunities from connected kitchen systems. The hospitality sector leads commercial adoption with smart kitchen implementations projected to grow from USD 18.75 billion in 2023 to USD 60.19 billion by 2030, reflecting industry recognition of technology's role in addressing labor shortages and operational challenges. Restaurant chains leverage smart appliances for standardized cooking processes, inventory management, and quality control across multiple locations, creating operational consistency and reducing training requirements. Commercial smart refrigeration systems provide real-time temperature monitoring, automated alerts for maintenance issues, and energy optimization capabilities that reduce operational costs while ensuring food safety compliance.

By Distribution Channel: Digital Commerce Reshapes Traditional Retail Models

B2C retail channels maintain 84.62% market share in 2025, encompassing multi-brand stores, exclusive brand outlets, and online platforms that serve diverse consumer preferences for smart appliance research, evaluation, and purchase experiences. Online channels within B2C retail demonstrate exceptional growth at 14.52% CAGR, reflecting fundamental shifts in consumer purchasing behavior toward digital-first appliance acquisition and manufacturers' direct-to-consumer strategies. Multi-brand stores provide comparative shopping environments where consumers evaluate smart appliance features across manufacturers, though digital integration increasingly supplements physical showrooms with augmented reality demonstrations and connected product experiences. Exclusive brand outlets enable manufacturers to showcase smart appliance ecosystems comprehensively, demonstrating integration capabilities and providing specialized sales support that justifies premium pricing for connected devices.

B2B distribution directly from manufacturers represents smaller market share but provides essential channels for commercial customers requiring specialized smart appliance configurations, bulk purchasing arrangements, and integrated system solutions. Commercial customers increasingly prefer direct manufacturer relationships for smart appliances due to complex integration requirements, customization needs, and ongoing service support that traditional distributors cannot provide effectively. B2B channels enable manufacturers to capture higher margins while building direct customer relationships that inform product development and create opportunities for comprehensive smart kitchen system sales. The B2B segment benefits from commercial customers' willingness to invest in smart appliances for operational efficiency gains, regulatory compliance benefits, and competitive differentiation in food service markets.

Geography Analysis

North America held 33.78% of the smart kitchen appliances market in 2025, reflecting consumers’ readiness to pay for premium connected suites and the region’s mature smart-home backbone. The U.S. Department of Energy’s 2024 cooking-product standards strengthen replacement demand as households shift to compliant models that surpass the new thresholds. Retailers blend in-store demos with virtual consultations, while subscription add-ons such as recipe libraries gain traction among tech-savvy households. Canada follows a parallel path: Amendment 18 to its Energy Efficiency Regulations broadens the appliance categories under mandatory limits beginning in 2026, rewarding suppliers that already ship AI-optimized unit. Mexico’s urban middle class gravitates toward mid-range smart ranges and refrigerators as cross-border e-commerce raises product visibility, propelling vendors to tailor bilingual apps for broader appeal.

Europe is forecast to advance at a 11.98% CAGR through 2031, the fastest among major regions, driven by stringent eco-design directives and elevated energy costs that highlight the payback of intelligent load-management features. Germany and the Nordic countries spearhead adoption of A-rated smart ovens and dishwashers that display real-time consumption dashboards, reinforcing the region’s sustainability ethos. BSH’s EUR 15.3 billion turnover in 2024 underscores manufacturer success in aligning AI cooking assistance with eco-labels. Southern Europe, historically price-sensitive, now receives lower-capacity smart refrigerators tailored for compact apartments, widening addressable demand. Retailers increasingly bundle extended service plans that guarantee software updates for at least five years, boosting buyer confidence and long-run satisfaction.

Asia-Pacific presents sizable upside as rising disposable incomes intersect with government smart-city programs. Chinese brands such as Haier leverage scale advantages to export AI-equipped refrigerators under aggressive pricing, challenging incumbents in Southeast Asia. Japan and South Korea maintain high per-capita penetration yet still upgrade to edge-AI cooking solutions that integrate with home-energy management panels. India shows early momentum in metros, where developers of premium condominiums pre-install smart ranges and app-linked hoods as value-adds. Regional heterogeneity persists: while urban consumers prioritize multifunctionality due to space constraints, rural adoption hinges on improved broadband and financing options.

Competitive Landscape

The competitive field is moderately fragmented, with a cohort of global majors, Samsung, LG, BSH, Whirlpool, and GE Appliances, commanding significant revenue but leaving ample room for regional specialists and software-centric entrants. Leadership increasingly rests on ecosystem depth rather than isolated hardware innovation. Samsung’s Instacart-enabled refrigerator bridges appliances with grocery e-commerce, expanding revenue beyond the initial sale. Whirlpool and Samsung’s early certification on Matter 1.3 underscores a strategic pivot toward open-standard interoperability that reassures multi-brand households. GE Appliances, meanwhile, differentiates through CookCam AI and the EcoBalance platform that pairs devices with ABB’s smart panel for unified energy orchestration.

Chinese challengers, notably Haier and Midea, capitalize on cost leadership and rapid feature rollouts to penetrate emerging markets and value tiers in developed economies. Their cloud-based service layers, such as Haier’s Smart Home Experiential Cloud, collect usage data that informs agile firmware updates and personalized promotions. European premium labels focus on design aesthetics paired with resource-saving credentials, exploiting consumer willingness to invest in long-lasting, eco-certified goods. Start-ups targeting single categories—smart cooktops, AI sous-vide sticks—employ software-as-a-service pricing to monetize continuous algorithm improvements, pressuring incumbent margin structures.

Strategic alliances blur industry boundaries. Appliance makers court semiconductor suppliers to secure SiC and GaN allocations, while partnering with voice-assistant providers to streamline UX. Cross-industry deals, such as Samsung’s integration with Instacart, suggest that future differentiation will stem from data partnerships and commerce tie-ins more than from incremental thermal-efficiency gains. As platforms mature, industry watchers anticipate selective M&A that consolidates firmware stacks, ensuring consistent user journeys across the full kitchen suite.

Smart Kitchen Appliances Industry Leaders

Samsung Electronics Co. Ltd

Whirlpool Corporation

LG Electronics Inc.

BSH Hausgeräte

Haier Smart Home

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: GE Appliances launched AI-powered recipe suggestions via SmartHQ visual recognition and introduced a wireless Smart Probe for precision cooking.

- February 2025: GE Appliances partnered with ABB to fold the ReliaHome Smart Panel into its EcoBalance ecosystem, enhancing whole-home energy optimization.

- January 2025: Samsung Electronics and Instacart unveiled shoppable refrigerators that employ AI Vision to identify stored items and trigger one-click restocking.

- January 2024: Panasonic deepened its collaboration with Fresco by rolling out an AI cooking assistant for the HomeCHEF 4-in-1 multi-oven.

Global Smart Kitchen Appliances Market Report Scope

Smart kitchen appliances are crafted with enhanced user-friendliness, aiming to eliminate the necessity for manual labor. The market for smart kitchen appliances exhibits a high level of fragmentation.

The smart kitchen appliances are segmented into by product type (smart ovens, smart dishwashers, smart refrigerators, smart cookware and cooktops, smart scale and thermometers, and other product types), distribution channel (multi-branded stores, exclusive stores, online, and other distribution channels), end users (residential and commercial), and by geography (North America, Europe, Asia-Pacific, South America, and Middle East & Africa). The report offers market size and forecasts for the smart kitchen appliances market in value (USD) for all the above segments.

| Large Kitchen Appliances | Refrigerators & Freezers |

| Dishwashers | |

| Range Hoods | |

| Cooktops | |

| Ovens | |

| Other Large Kitchen Appliances | |

| Small Kitchen Appliances | Food Processors |

| Juicers and Blenders | |

| Grills and Roasters | |

| Air Fryers | |

| Coffee Makers | |

| Electric Cookers | |

| Toasters | |

| Electric Kettles | |

| Countertop Ovens | |

| Other Small Kitchen Appliances |

| Residential |

| Commercial |

| B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B (directly from the manufacturers) |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Product | Large Kitchen Appliances | Refrigerators & Freezers |

| Dishwashers | ||

| Range Hoods | ||

| Cooktops | ||

| Ovens | ||

| Other Large Kitchen Appliances | ||

| Small Kitchen Appliances | Food Processors | |

| Juicers and Blenders | ||

| Grills and Roasters | ||

| Air Fryers | ||

| Coffee Makers | ||

| Electric Cookers | ||

| Toasters | ||

| Electric Kettles | ||

| Countertop Ovens | ||

| Other Small Kitchen Appliances | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B (directly from the manufacturers) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of smart kitchen appliances worldwide by 2031?

The category is poised to reach USD 43.93 billion by 2031, expanding at an 10.86% CAGR from its 2026 baseline.

Which region shows the fastest revenue growth for connected cooking devices?

Europe is expected to record a 11.98% CAGR through 2031, outperforming other major regions due to strict energy rules and eco-conscious consumers.

How large is the connected refrigerator segment relative to other large appliances?

Refrigerators dominate large-appliance revenue due to features such as AI Vision item recognition, making them the anchor of many smart-kitchen ecosystems.

What factors restrain adoption of AI-enabled ovens in emerging economies?

High upfront pricing and concerns over cyber-security deter buyers, even though long-term energy savings are significant.

How are brands addressing interoperability anxieties among multi-brand households?

Leading manufacturers are adopting the open Matter 1.3 standard, enabling cross-brand control from a single app or voice assistant.

Why are commercial kitchens investing in connected dishwashers and ranges?

Restaurants pursue smart units to cut labor time, standardize cooking quality, and use predictive maintenance data to curb unplanned downtime.

Page last updated on: