Pneumatic Nebulizer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

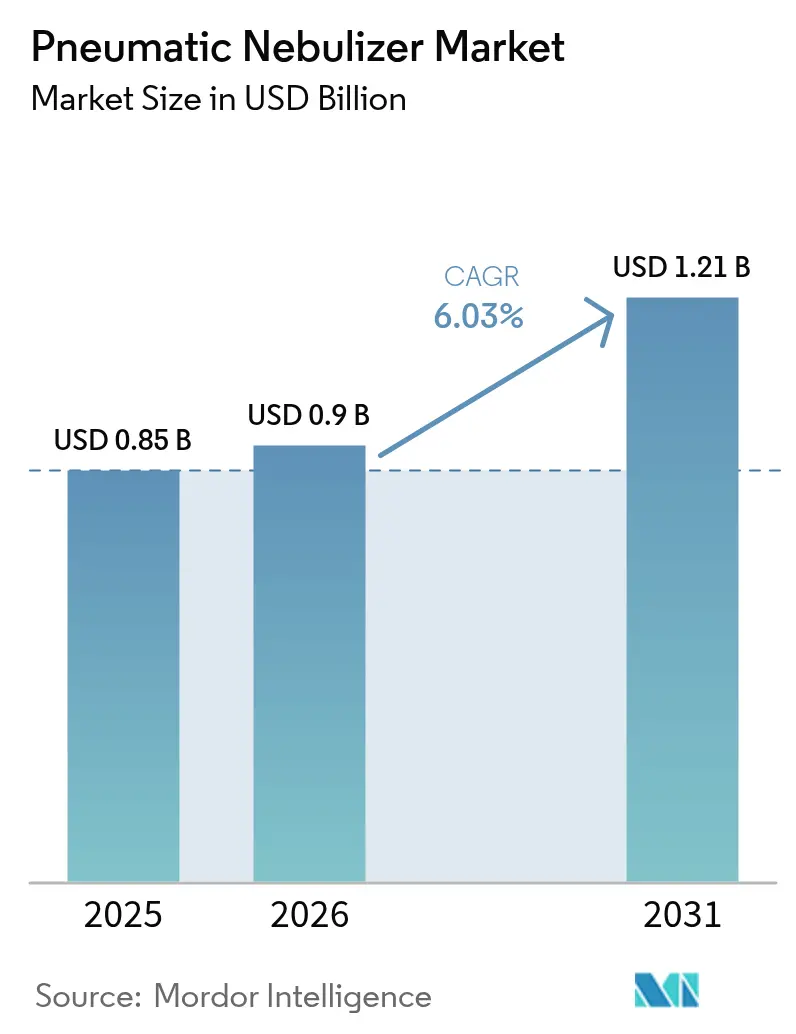

| Market Size (2026) | USD 0.9 Billion |

| Market Size (2031) | USD 1.21 Billion |

| Growth Rate (2026 - 2031) | 6.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pneumatic Nebulizer Market Analysis by Mordor Intelligence

The pneumatic nebulizer market size is expected to grow from USD 0.85 billion in 2025 to USD 0.90 billion in 2026 and is forecast to reach USD 1.21 billion by 2031 at 6.03% CAGR over 2026-2031. Demand holds firm as chronic obstructive pulmonary disease (COPD) affects 213 million people worldwide, while 26% of seniors aged 85 and older already live with COPD. Adoption accelerates because health systems promote home-based respiratory therapy to reduce hospitalization costs, and new reimbursement codes A7021 and E0469 in the United States clarify payment for nebulizers CGS Administrators. Europe and China add tailwinds by broadening device coverage under public insurance plans European Commission. Technology upgrades such as low-noise smart compressors boost patient compliance, while e-commerce expands access to replacement kits. Competitive activity stays moderate but active, with Philips settling USD 1.1 billion litigation to refocus on product innovation and OMRON integrating 3A Health Care for aerosol expertise[1]Source: OMRON Healthcare, “OMRON announces acquisition of 3A Health Care,” omron-healthcare.co.uk .

Key Report Takeaways

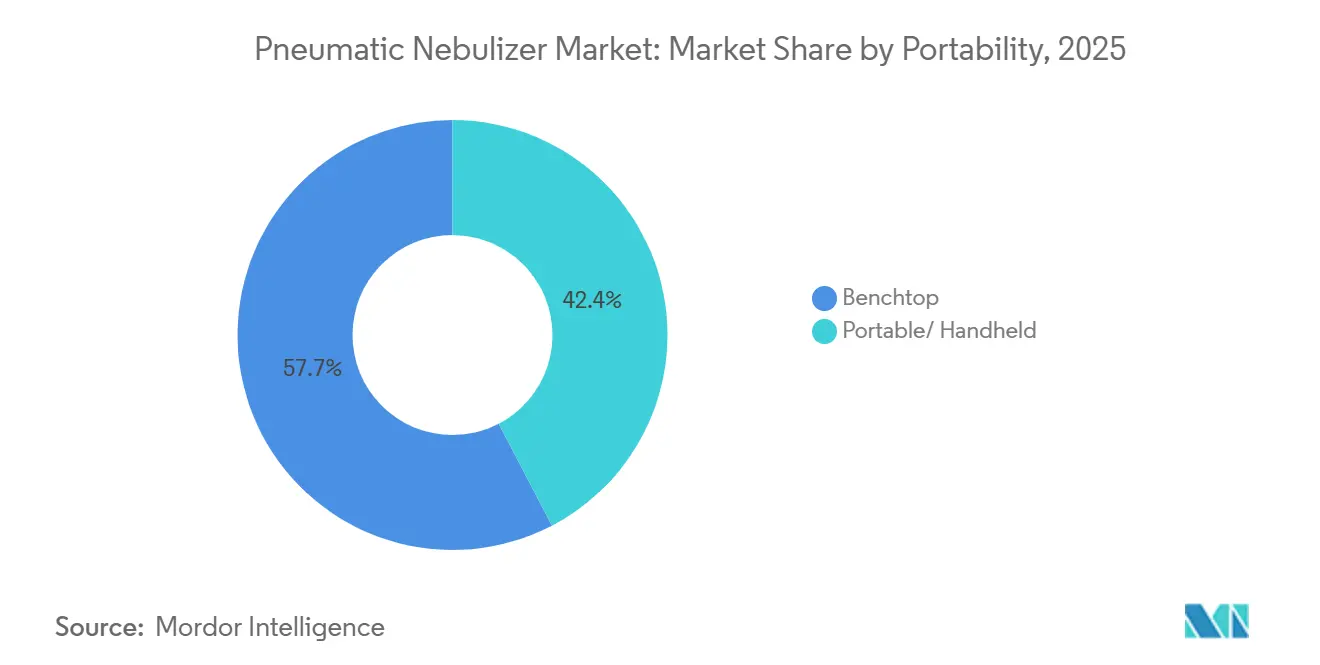

- By portability, benchtop/tabletop held 57.65% of the market share in 2025, while the portable/handheld segment is projected to register the fastest growth at a 7.06% CAGR through 2031.

- By technology, the conventional compressor segment accounted for 68.72% of the market share in 2025, whereas the smart/digital-integrated compressor segment is anticipated to expand at the fastest 7.42% CAGR through 2031.

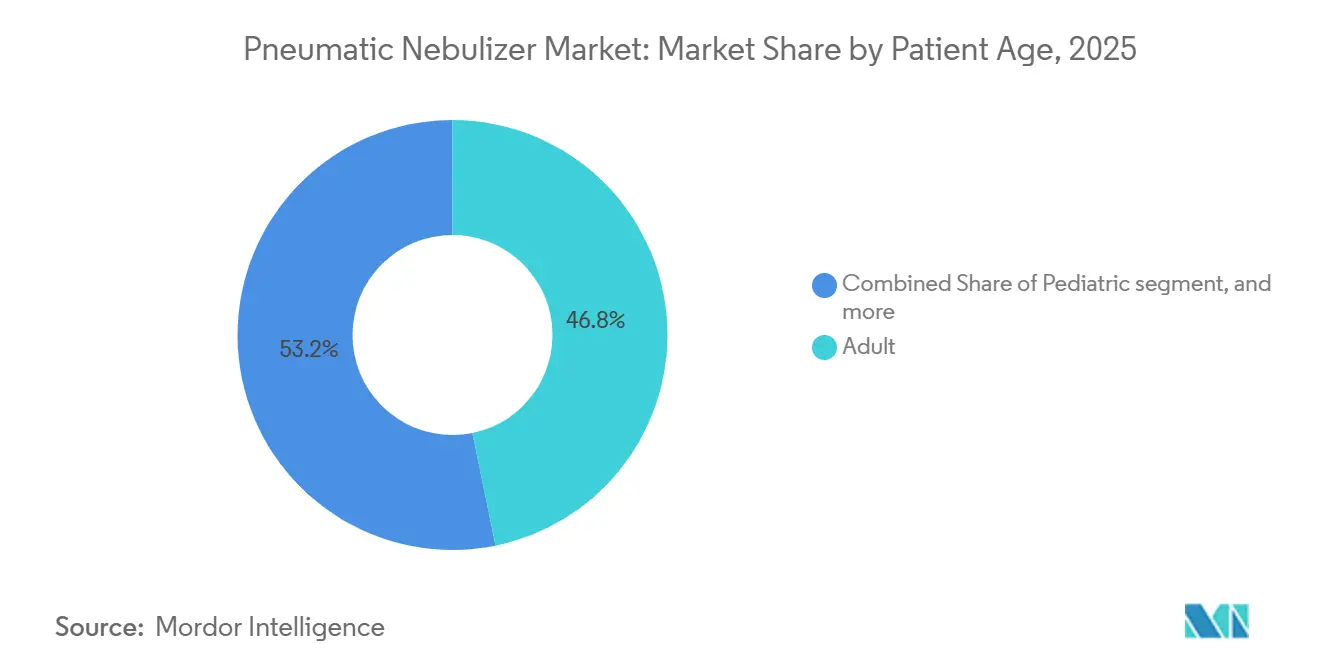

- By patient age group, adults accounted for 46.80% of the market share in 2025, while the geriatric segment is projected to witness the highest growth at a 7.78% CAGR through 2031.

- By application, COPD represented 50.88% of the market share in 2025, whereas the cystic fibrosis segment is expected to grow at the fastest 6.63% CAGR through 2031.

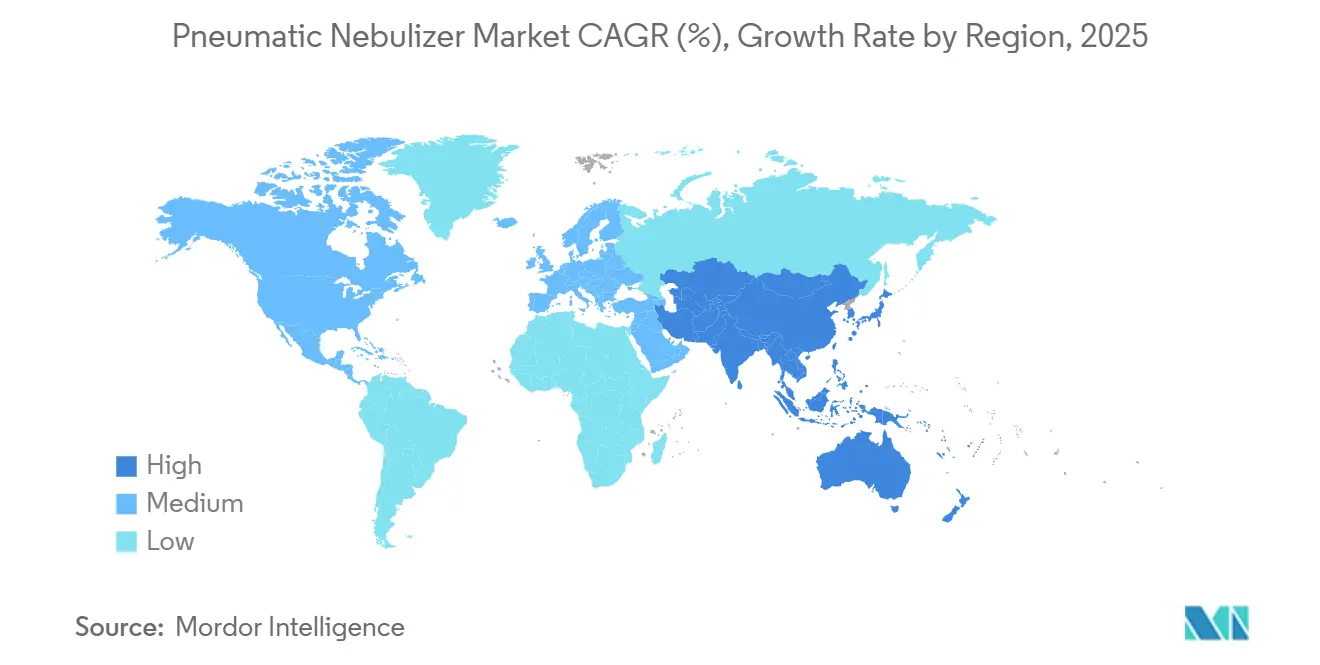

- By geography, North America held the largest market share at 40.15% in 2025, while Asia-Pacific is projected to register the fastest growth at a 7.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pneumatic Nebulizer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating COPD Prevalence & Aging Population | +1.8% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Home-Based Respiratory Therapy Adoption Surge | +1.2% | Global, led by North America & APAC | Medium term (2-4 years) |

| Government Reimbursement Expansion (EU, China) | +0.9% | Europe & China, spillover to emerging markets | Medium term (2-4 years) |

| Technological Shift to Low-Noise Smart Compressors | +0.7% | North America & Europe, expanding to APAC | Short term (≤ 2 years) |

| E-Commerce Boom in Compressor Replacement Kits | +0.4% | Global, strongest in developed markets | Short term (≤ 2 years) |

| AI-Guided Adherence Platforms Bundled with Devices | +0.3% | North America & Europe initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating COPD Prevalence & Aging Population

Ambient particulate matter now accounts for 22.2% of COPD disability-adjusted life years worldwide Respiratory Research. Because hospitalization costs for COPD exceed USD 24 billion annually in the United States, providers view pneumatic nebulizers as cost-effective maintenance therapy[2]Source: American Lung Association, “COPD Trends Brief – Burden,” lung.org . This epidemiological pressure sustains long-term growth across the pneumatic nebulizer market.

Home-Based Respiratory Therapy Adoption Surge

Hospital discharge programs such as the Re-Engineered Discharge (RED) framework lower readmissions by embedding nebulizer use into structured home protocols. Medicare’s 2024 rule covering virtual pulmonary rehabilitation extends these benefits to rural communities American Thoracic Society. Tele-health monitoring combined with nebulizer data feeds lets clinicians adjust therapy remotely, strengthening adherence while opening subscription software revenue.

Government Reimbursement Expansion (EU, China)

New CPT codes 94625 and 94626 align pulmonary rehabilitation payments with cardiac protocols, ending a reimbursement gap that previously limited respiratory device access. Parallel Chinese reforms are widening coverage for aerosol therapy, a move reinforced by the European Commission’s limits on some Chinese tenders that bolster European manufacturers’ pricing power European Commission. Stable reimbursement reduces out-of-pocket expenses, enabling deeper penetration of the pneumatic nebulizer market.

Technological Shift to Low-Noise Smart Compressors

OMRON’s CompAir operates below 52 dB, cutting noise by one-third versus older models OMRON Healthcare. AI algorithms now optimize particle size distribution, elevating sub-5 μm droplets to 59.25% for improved lung deposition MDPI. Bluetooth-enabled units push adherence data to cloud dashboards, giving payers real-time visibility on therapy outcomes and reinforcing competitive positioning inside the pneumatic nebulizer market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Cannibalization by Mesh & Ultrasonic Tech | -1.4% | Global, strongest in developed markets | Medium term (2-4 years) |

| Infection-Control & Aerosolization Safety Concerns | -0.8% | Global, heightened in hospital settings | Short term (≤ 2 years) |

| Low Reimbursement / Affordability in LMICs | -0.6% | Low and middle-income countries, rural areas | Long term (≥ 4 years) |

| Global Helium & Specialty-Gas Supply Constraints | -0.4% | Global, most severe in manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Cannibalization by Mesh & Ultrasonic Tech

A 2025 pediatric asthma trial showed mesh nebulizers produced greater gains in FEV1 compared with compressors, driving clinician preference toward quieter, faster units. Mesh devices now operate below 23 dBA and in any orientation, advantages that erode institutional demand for pneumatic models. Unless compressor makers match noise and efficiency metrics, mesh adoption could siphon share from the pneumatic nebulizer market in high-value hospital accounts.

Infection-Control & Aerosolization Safety Concerns

COVID-19 elevated scrutiny of aerosol-generating procedures. Hospitals install extra ventilation and mandate personal protective equipment for compressor treatments, pushing some facilities to closed-system mesh devices. Philips issued updated Trilogy Evo instructions emphasizing in-line nebulizer placement to cut contamination risk. These precautions raise costs and dampen pneumatic nebulizer market uptake in acute-care environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Portability: Benchtop Dominance Amid Portable Innovation

Benchtop devices captured 57.65% of pneumatic nebulizer market share in 2025, anchored by strong compressor output and large medication cups that suit chronic COPD therapy. Their stable power supply enables dependable droplet formation for viscous formulations. Portable models, however, are logging a 7.06% CAGR to 2031. The segment profits from miniaturized motors and rechargeable batteries that meet rising patient mobility expectations.

Benchtop units retain favor among elderly users who value simple controls and consistent performance. Yet holiday travel and work commitments spur younger patients to opt for hand-held formats like OMRON’s MicroAir, which weighs just 4.2 ounces and works at any angle OMRON Healthcare. As home-based care grows, dual-ownership households—one benchtop for routine therapy and one portable for on-the-go dosing—are becoming commonplace, broadening total spending inside the pneumatic nebulizer market.

By Technology: Smart Integration Disrupts Traditional Compressors

Conventional compressors accounted for 68.72% of the pneumatic nebulizer market size in 2025 thanks to attractive unit pricing and a well-established service network. Cost-sensitive payers in emerging economies continue to specify tried-and-tested pneumatic engines. Smart-connected compressors are gaining momentum, advancing at 7.42% CAGR as payers reimburse remote monitoring.

Noise-optimized units serve as a bridge technology, bringing sound levels below 52 dB without the premium price of mesh devices. Data-enabled models allow clinicians to download adherence logs, a feature that improves medication titration and supports pay-for-performance contracts. Over time, digital health ecosystems could shift revenue mix from one-off hardware sales to recurring software packages, raising lifetime value per patient within the pneumatic nebulizer market.

By Patient Age Group: Geriatric Growth Outpaces Adult Segment

Adults held 46.80% of pneumatic nebulizer market share in 2025, reflecting workforce exposure to urban air pollution. Still, the geriatric cohort is expanding fastest at an 7.78% CAGR through 2031. Age-related decline in lung elasticity and higher incidence of comorbidities drive frequent dosing needs that favor compressor units with larger drug reservoirs.

Designers are introducing bigger tactile buttons and back-lit displays to aid seniors with impaired vision. Lock-out features prevent accidental setting changes, and antimicrobial tubing alleviates infection worries. Pediatric demand remains steady as child-friendly designs like OMRON’s Nami Cat ease therapy anxiety OMRON Healthcare. Each age bracket has distinct ergonomic and compliance requirements, steering product-line diversification across the pneumatic nebulizer market.

By Application: COPD Leadership Challenged by Cystic Fibrosis Growth

COPD dominated with 50.88% of the pneumatic nebulizer market size in 2025 as maintenance bronchodilators and corticosteroids are routinely nebulized to manage chronic symptoms. This segment benefits from broad guideline endorsement and predictable refill volumes. Cystic fibrosis is projected to advance at a 6.63% CAGR, bolstered by longer patient survival and drug regimens requiring multiple daily doses.

Asthma therapies keep material share because acute attacks necessitate rapid bronchodilator delivery. Research into the cardiovascular risks of COPD and the role of climate change in exacerbations, outlined in the 2025 GOLD report, may spur formulation reviews that increase nebulizer usage frequency. Such evolving clinical protocols shore up the long-term importance of compressor systems within the pneumatic nebulizer market.

Geography Analysis

North America led with 40.15% share of the pneumatic nebulizer market in 2025. High COPD prevalence, comprehensive insurance coverage, and strong distributor networks underpin sales. Recent Medicare coding updates simplify provider billing, keeping adoption momentum in both hospital and home settings. Canada benefits from single-payer reimbursement that subsidizes devices for low-income seniors, while Mexico’s Seguro Popular reform is piloting respiratory home-care programs that could expand compressor uptake.

Asia-Pacific is the fastest-growing arena, registering a 7.55% CAGR to 2031. China drives volume as air pollution and smoking rates lift respiratory disease cases. OMRON reported double-digit nebulizer growth in its China portfolio during 2024. India contributes through public-private schemes that finance affordable devices for rural clinics, and Japan’s super-aged society sustains steady demand for high-end models featuring quiet operation and smart connectivity.

Europe shows stable progress, aided by universal health coverage and strong clinical guidelines favoring nebulizer therapy for COPD and cystic fibrosis. Germany anchors volume due to robust outpatient infrastructure, while the United Kingdom’s National Health Service streamlines device provision across primary-care centers. The European Commission’s trade rules limiting certain Chinese suppliers give domestic manufacturers an opening to consolidate share. South America and the Middle East & Africa remain under-penetrated but are targeted for future expansion as distributors establish last-mile logistics networks.

Competitive Landscape

The pneumatic nebulizer market features moderate concentration. Philips, OMRON, and PARI anchor global revenue, supported by decades of brand trust and servicing infrastructure. Philips cleared a USD 1.1 billion litigation cloud in 2024, freeing capital for R&D in compressor silencing and smart features. OMRON’s takeover of 3A Health Care broadens high-end aerosol know-how and complements its Zero Asthma Attack initiative.

Competitive moves include integrated device-plus-software bundles that lock customers into ecosystems. PARI upgrades its eFlow rapid system to handle a wider molecule portfolio, while Medline’s TurboMist targets hospital pharmacies looking for higher medication throughput Medical Device Network. Leaders leverage patent portfolios—Philips filed 594 med-tech patent applications in 2024 alone—to deter new entrants StockTitan. Mid-tier firms differentiate with pediatric designs or regional distribution strength, but face rising software development costs to match connectivity expectations within the pneumatic nebulizer market.

Strategic alliances with tele-health providers are emerging. Compressor telemetry can sync with pulmonary rehabilitation apps, allowing outcome-based billing models that reward adherence. Suppliers that can integrate sensors, cloud analytics, and consumables are poised to capture recurring revenue, whereas single-product rivals risk margin erosion. Nonetheless, mesh innovators pose an external threat as their technology matures and price gaps narrow, pressuring incumbents to accelerate noise, size, and efficiency upgrades.

Pneumatic Nebulizer Industry Leaders

Aerogen

Agilent Technologies Inc.

Medline Industries Inc.

Lepu Medical

GE Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: DevPro Biopharma and Bespak completed feasibility studies for DP007, a climate-friendly albuterol inhaler using Honeywell’s Solstice Air propellant

- October 2024: CMS introduced HCPCS codes A7021 and E0469 for nebulizer supplies, effective October 1, 2024.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the pneumatic nebulizer market as the value of new, compressor-based devices that convert liquid medication into an aerosol for direct pulmonary delivery, spanning bench-top and portable formats that operate with vented or breath-actuated circuits.

According to Mordor Intelligence, accessories, disposable kits, mesh and ultrasonic nebulizers, rental revenue, and aftermarket servicing stay outside this value pool.

Scope Exclusion: Mesh, ultrasonic, and rental income are not counted.

Segmentation Overview

- By Portability (Value)

- Portable/ Handheld

- Benchtop/ Tabletop

- By Technology (Value)

- Conventional Compressor

- Noise-Reduced Compressor

- Smart/ Digital-Integrated Compressor

- By Patient Age Group (Value)

- Pediatric

- Adult

- Geriatric

- By Application (Value)

- COPD

- Asthma

- Cystic Fibrosis

- Others (Bronchiectasis, Pneumonia)

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed respiratory therapists, home-care distributors, biomedical engineers, and procurement leads across North America, Europe, and key Asian markets. The conversations confirmed real-world replacement cycles, average selling prices, and the speed at which home therapy is eclipsing in-clinic usage, enabling us to challenge desk findings and refine assumptions.

Desk Research

We started by mapping publicly available datasets from sources such as the World Health Organization, the Global Burden of Disease study, United Nations age-cohort projections, and national customs dashboards that track HS code 901920 imports. Trade association releases from bodies like the American Thoracic Society, plus device registration logs on the U.S. FDA 510(k) portal, clarified technology uptake and regulatory cadence. Company 10-Ks, investor decks, and press articles aggregated through Dow Jones Factiva added shipment guidance and channel mix insights. These sources illustrate market size anchors yet still leave gaps that require validation. The sources listed are illustrative and not exhaustive.

Market-Sizing & Forecasting

A top-down demand pool was built from COPD, asthma, and cystic fibrosis patient prevalence, then adjusted for treatment penetration and device per-patient ratios, followed by country-level reimbursement eligibility. We corroborated totals with selective bottom-up roll-ups of leading supplier shipments and sampled ASP × volume checks. Key model levers include: 1) growth in home respiratory therapy sessions, 2) average compressor lifespan, 3) shift toward portable units, 4) public reimbursement coverage breadth, and 5) replacement ASP erosion. Multivariate regression linked these variables to historic sales, while ARIMA smoothed short-term volatility before forecasts ran to 2030. Data gaps in smaller geographies were bridged by regional proxies that share similar income and disease profiles.

Data Validation & Update Cycle

Outputs run through variance tests against independent import data and hospital procurement indices. Senior analysts review anomalies, and if any exceed predefined thresholds, sources are re-contacted. The model is refreshed every twelve months, with interim updates triggered by major regulatory or epidemiological events, ensuring clients always receive the latest view.

Why Mordor's Pneumatic Nebulizer Baseline Deserves Trust

Published estimates often diverge because firms pick inconsistent device mixes, margin layers, and refresh cadences.

Key gap drivers include others limiting scope to hospital channels, baking distributor mark-ups into revenue, or omitting portable units sold online, whereas Mordor's definition captures every first-sale device while stripping double counts and secondary mark-ups.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 850 million | Mordor Intelligence | - |

| USD 853 million | Regional Consultancy A | Hospital channel focus only |

| USD 855 million | Global Consultancy B | Uses shipment invoice totals without margin cleansing |

| USD 667 million | Trade Journal C | Excludes online and portable device sales |

The comparison shows that, while headline values vary, Mordor's disciplined scope rules, multi-variable model, and annual refresh cadence yield a balanced, transparent baseline that decision-makers can reliably track year after year.

Key Questions Answered in the Report

How big is the Pneumatic Nebulizer Market?

The Pneumatic Nebulizer Market size is expected to reach USD 0.90 billion in 2026 and grow at a CAGR of 6.03% to reach USD 1.21 billion by 2031.

Who are the key players in Pneumatic Nebulizer Market?

Aerogen, Agilent Technologies Inc., Medline Industries Inc., Lepu Medical and GE Healthcare are the major companies operating in the Pneumatic Nebulizer Market.

Which is the fastest growing region in Pneumatic Nebulizer Market?

Asia Pacific is estimated to grow at the highest 7.55% CAGR over the forecast period (2026-2031).

Which region has the biggest share in Pneumatic Nebulizer Market?

In 2025, the North America accounts for the largest market share 40.15% in Pneumatic Nebulizer Market.

Page last updated on: