IoT In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 207.40 Billion |

| Market Size (2031) | USD 483.72 Billion |

| Growth Rate (2026 - 2031) | 18.46% CAGR |

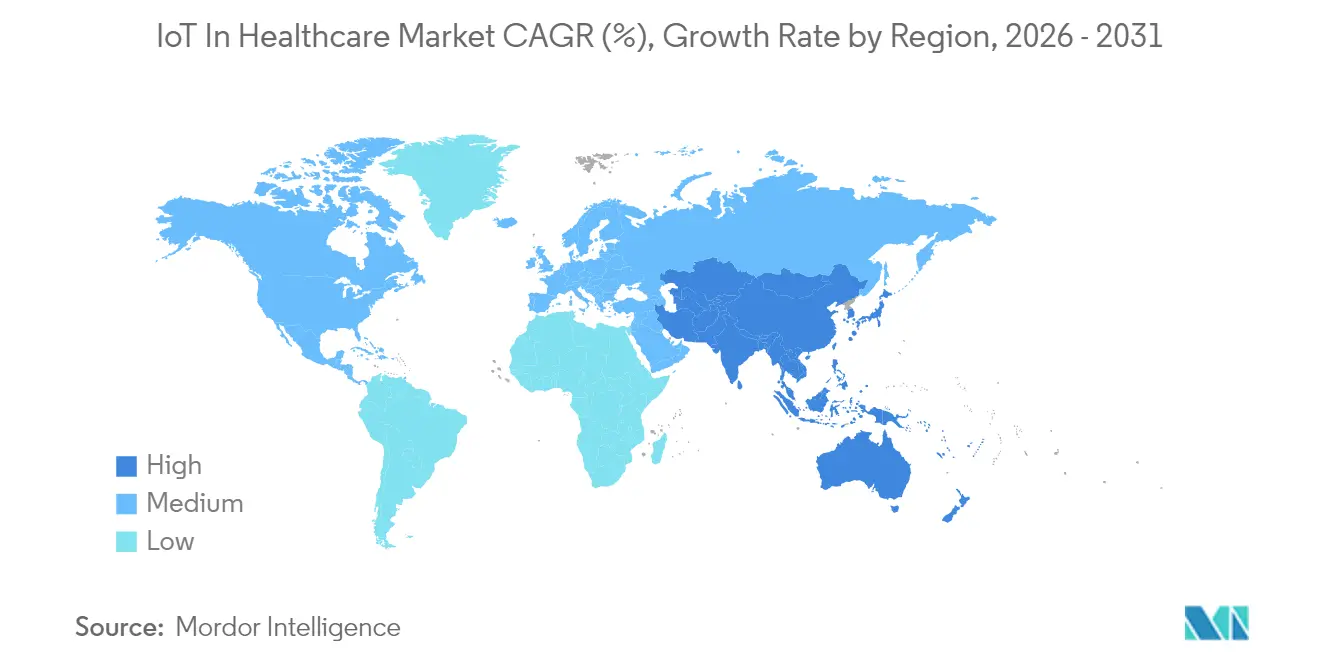

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

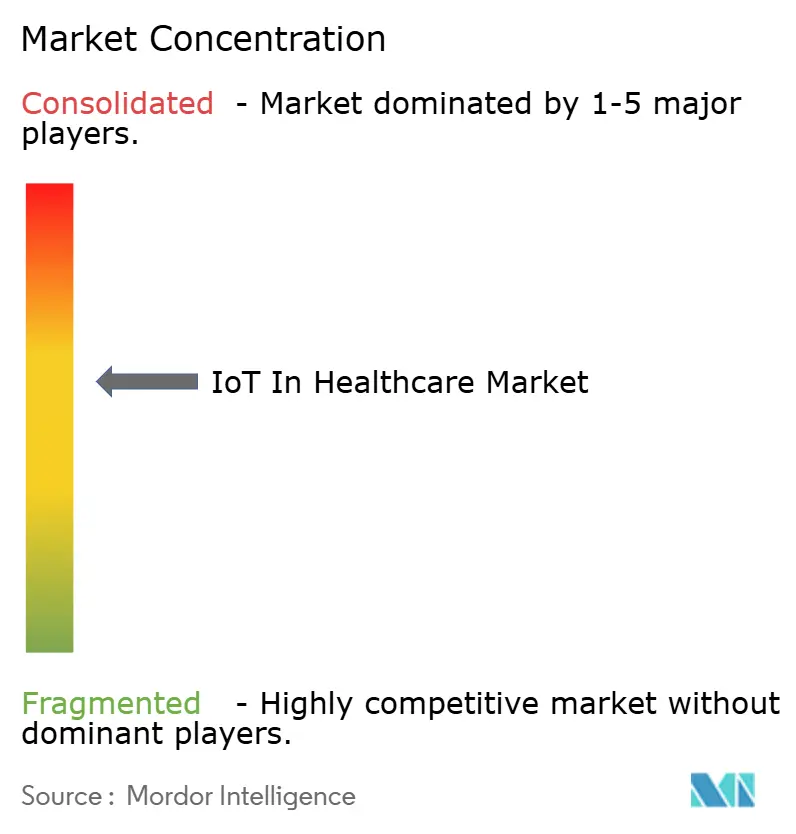

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

IoT In Healthcare Market Analysis by Mordor Intelligence

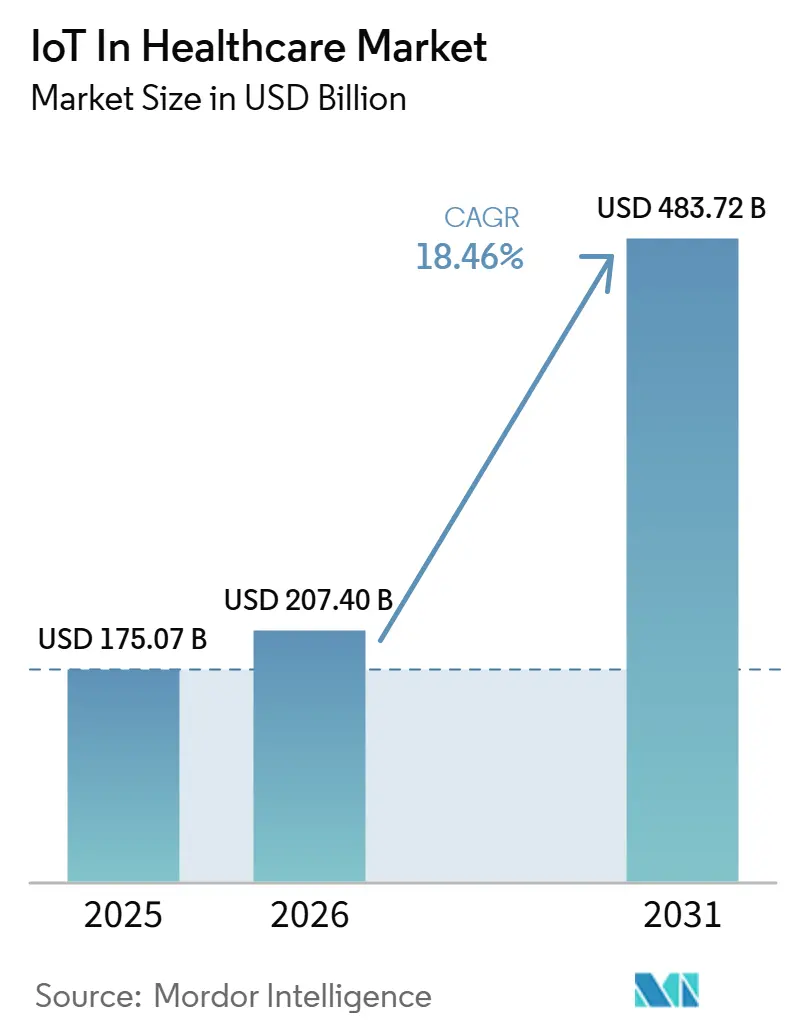

The IoT In Healthcare Market size is expected to increase from USD 175.07 billion in 2025 to USD 207.40 billion in 2026 and reach USD 483.72 billion by 2031, growing at a CAGR of 18.46% over 2026-2031.

Rapid progress stems from reimbursement modernization, maturing 5G campus networks, and a post-pandemic expectation for uninterrupted patient oversight. Combined, these forces position connected devices as indispensable healthcare infrastructure rather than optional add-ons, pushing providers toward continuous engagement and data-driven interventions. Investment momentum is further sustained by private network deployments that cut implementation time by 90% and by digital-twin simulations that allow clinicians to test drug protocols virtually before bedside administration.[1]ZTE Corporation, “Smart Hospital 5G Deployment,” zte.com.cn Together, these shifts signal a durable reallocation of capital toward data liquidity, edge analytics, and device interoperability that enlarges the Internet of Things in healthcare market opportunity horizon.

Key Report Takeaways

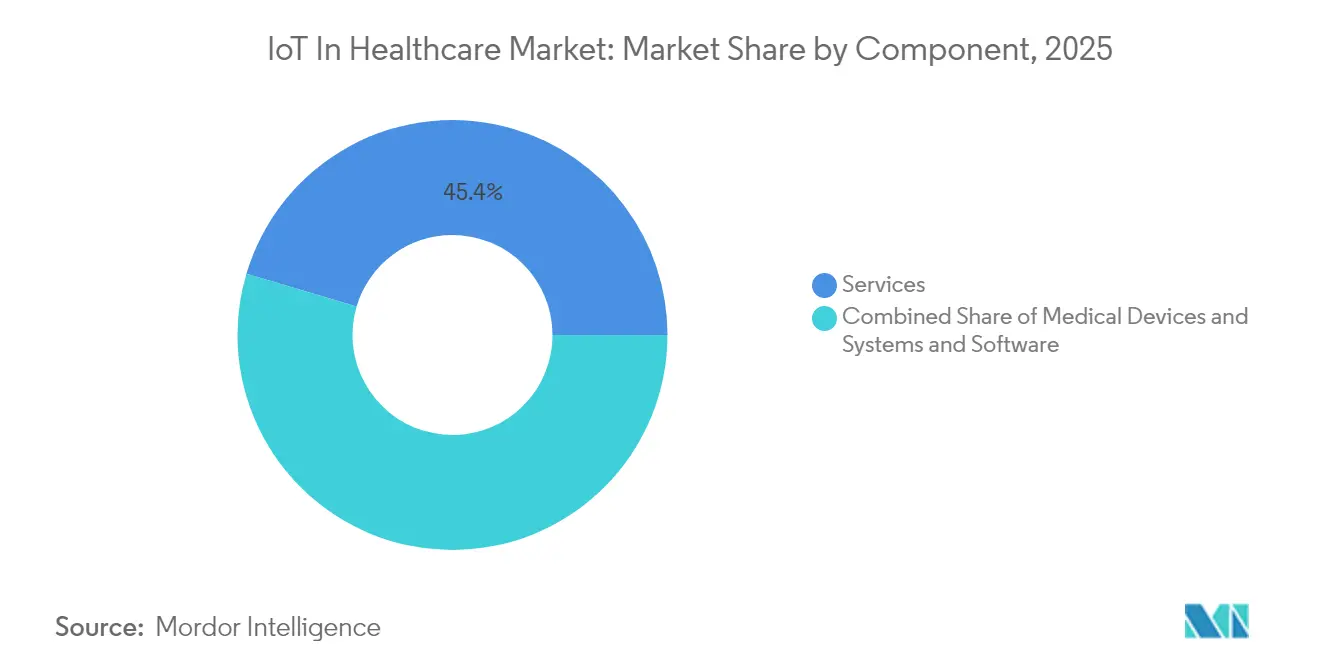

- By component, Services led with 45.40% revenue in 2025, while Systems and Software is projected to advance at a 19.12% CAGR to 2031.

- By application, Tele-medicine captured 28.95% of IoT in the healthcare market share in 2025; Asset and Staff Tracking is growing fastest at a 20.87% CAGR through 2031.

- By end-user, Hospitals and Clinics held 51.10% share of the IoT in healthcare market size in 2025, whereas Home-care is accelerating at an 18.32% CAGR.

- By connectivity technology, Wi-Fi commanded 37.90% revenue share in 2025, while Cellular and 5G is set to rise at a 23.90% CAGR to 2031.

- By deployment model, Cloud accounted for 66.80% revenue in 2025; On-premise/Edge is forecast to grow at a 22.55% CAGR through 2031.

- By geography, North America represented 41.85% of 2025 revenue, while Asia-Pacific is on track for a 22.70% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global IoT In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Wearable-device penetration surge | +3.2% | Global; earliest uptake in North America and EU | Medium term (2–4 years) |

| Falling IoT sensor and connectivity costs | +2.8% | Global; fastest savings in APAC production hubs | Short term (≤ 2 years) |

| Digital-twin guided therapy optimisation | +2.1% | North America and EU leading, APAC scaling | Long term (≥ 4 years) |

| Hospital-at-home reimbursement roll-outs | +3.5% | North America primary, EU pilots ongoing | Medium term (2–4 years) |

| Private 5G networks in hospital campuses | +1.9% | Urban medical centers worldwide | Medium term (2–4 years) |

| Remote patient monitoring post-COVID-19 | +2.7% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Wearable-device penetration surge

Medical-grade wearables have shifted from fitness novelties to clinically validated diagnostics. iRhythm’s Zio AT logged 98% patient adherence in 2024, showing that continuous cardiac telemetry is feasible without lifestyle disruption. FDA clearance of Dexcom’s over-the-counter Stelo glucose monitor in the same year widens consumer access to regulated biosensors.[2]U.S. Food and Drug Administration, “Dexcom Stelo Clearance,” fda.govCloud-linked analytics convert these streams into real-time alerts, cutting emergency visits and readmissions. Specialized form factors such as Movano’s Evie Ring target underserved cohorts, signaling new segmentation dynamics. As device diversity grows, the Internet of Things in healthcare market gains incremental user pools across chronic-disease management and preventive screening.

Falling IoT sensor and connectivity costs

Global semiconductor overcapacity and miniaturization advances continue to pull unit prices down, allowing hospitals to connect more endpoints per budget dollar. The dispersion of 5G and LPWAN infrastructure trims data-transmission overheads while improving reliability. Edge-ready chipsets now process signals locally, lowering cloud egress fees and latency. Automotive-sector investments in power-efficient sensors spill over into medical designs, extending battery life on wearable patches. Interoperability standards under IEEE P2413 streamline multi-vendor integration, shrinking project lead-times and reinforcing the attractiveness of the IoT in healthcare market for cash-constrained providers.

Digital-twin guided therapy optimization

Clinicians increasingly pair real-world device telemetry with virtual patient replicas to predict therapeutic efficacy. In oncology, tumor-specific twins inform chemo dosing that minimizes toxicity while maintaining potency. Cardiologists model disease progression to time valve interventions more precisely. Mayo Clinic Platform has scaled the approach across 16 specialties, underscoring a pivot from retrospective chart review to proactive regimen simulation.[3]Mayo Clinic Platform, “Digital Twin Applications,” mayoclinic.org Pharmaceutical firms run in-silico cohorts to screen trial protocols, shortening development cycles. These applications deepen data demands and lift platform revenue, adding heft to the Internet of Things (IoT) in healthcare market.

Hospital-at-home reimbursement roll-outs

The 2025 Physician Fee Schedule codified CPT 99453-99458, reimbursing remote monitoring at USD 19.73–82.16 per interaction. More than 23,000 discharges have flowed through the Acute Hospital Care at Home program, proving scalability. Commercial insurers are mirroring Medicare’s stance, embedding IoT metrics into value-based contracts. This payor alignment de-risks investment in connected kits and accelerates supplier order books. As revenue moves outside hospital walls, the IoT in healthcare market gains a durable outpatient tailwind.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-security and data-privacy risks | -2.3% | Global; strictest in EU | Short term (≤ 2 years) |

| Up-front legacy-integration costs | -1.8% | North America and EU | Medium term (2–4 years) |

| Lack of AI-grade interoperability standards | -1.5% | Global | Long term (≥ 4 years) |

| Battery e-waste tightening regulations | -0.9% | EU first, global spread | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Cyber-security and data-privacy risks

Proposed HIPAA updates mandate multi-factor authentication, encryption at rest, and AI-driven breach containment, adding an estimated USD 9.3 billion to first-year compliance budgets.[4]Kirkland & Ellis LLP, “Proposed HIPAA Security Rule Update,” kirkland.com EU providers juggle GDPR with the AI Act, extending procurement cycles. Healthcare remains the most expensive industry for breaches at USD 10.1 million per incident, driving cautious CIO behavior. Blockchain pilots promise immutable audit trails but raise energy-use worries. While security vendors see upside, inertia tempers expansion speed of the Internet of Things in healthcare market.

Lack of AI-grade interoperability standards

HL7 FHIR supports structured records, yet AI models output probabilistic insights not covered by existing schemas. The 2025 Interoperability Standards Advisory lists these gaps, leaving hospitals to craft ad-hoc work-arounds. Oracle, Epic, and smaller PACS vendors embed proprietary connectors, risking data silos that dampen ROI. Industry bodies explore federated-learning toolkits, but consensus is years away. Until clarity emerges, multi-vendor procurement decisions will proceed slowly, marginally constraining the IoT in healthcare market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Drive Implementation Complexity

Services accounted for 45.40% of 2025 revenue, reflecting hospitals’ reliance on consulting, integration, and lifecycle support to unlock ROI. Systems and Software is forecast to grow at 19.12% CAGR as AI and cloud-native stacks become the baseline for new device introductions. Medtronic invested USD 2.7 billion in R&D to embed analytics layers that drive subscription revenue. Philips already orchestrates 1.3 million IoT endpoints on AWS, lowering compute spend by 36%. The Internet of Things in healthcare market, therefore, tilts toward platform centricity rather than one-off hardware sales.

Edge analytics, cyber-secured middleware, and predictive-maintenance dashboards dominate fresh spending requests. Hospitals negotiate outcome-based contracts that bundle device leasing with real-time analytics and 24/7 service desks. Vendors that master end-to-end orchestration capture higher wallet share as organizations phase out multi-supplier patchworks. By 2030, the services subtotal is projected to eclipse hardware in absolute dollars, anchoring a high-recurring-revenue profile across the IoT in healthcare market.

By Application: Asset Tracking Emerges as Efficiency Driver

Tele-medicine retained a 28.95% share in 2025 as the foundational use-case, yet Asset and Staff Tracking is climbing at 20.87% CAGR on the back of workforce shortages and throughput pressures. Private 5G and ultra-wideband tags support bed-level geofencing, cutting search times for ventilators in ICU corridors. Predictive maintenance schedules improve equipment uptime and audit compliance. These operational wins entice CFOs who view tracking projects as quick payback gateways into the broader Internet of Things (IoT) in healthcare market.

In-patient monitoring embraces 5G gateways that feed telemetry into AI triage engines. Medication-management kiosks register dose adherence in real time, curbing adverse events. Imaging suites deploy edge accelerators to render CT scans instantly, slashing radiologist turnaround. Emergency response teams use geotagged panic buttons linked to hospital command centers, shaving minutes off door-to-needle times. Collectively, these workflows diversify revenue streams and deepen penetration of the IoT in the healthcare industry.

By End-user: Home-care Acceleration Reshapes Delivery Models

Hospitals and Clinics commanded 51.10% of 2025 spending, anchored by established infrastructure and accredited protocols. Yet Home-care is on track for an 18.32% CAGR as payors reimburse acute-level care at residential addresses. GE Healthcare’s alliance with Biofourmis extends telemetry beyond discharge, raising satisfaction metrics and lowering readmissions. The IoT in healthcare market size for home-centric care is set to climb sharply as chronic-disease demographics skew older.

Clinical research organizations embrace decentralized trials, using wearables to capture endpoints without site visits. Long-term-care facilities deploy fall-detection sensors that alert staff within seconds, enhancing safety while optimizing staffing ratios. Rehabilitation centers integrate motion-tracking patches to tailor therapy progression. Each niche unlocks specialty device demand, compounding total addressable revenue across the IoT in the healthcare market.

By Connectivity Technology: 5G Transforms Real-time Applications

Wi-Fi kept 37.90% share in 2025 thanks to sunk investments and broad handset compatibility. Cellular and 5G, however, is surging at a 23.90% CAGR as low-latency guarantees become essential for telesurgery and high-resolution imaging. LPWAN formats such as NB-IoT serve building-wide ambient monitoring, while Bluetooth Low Energy dominates battery-sensitive wearables. Together these channels sustain redundancy and load balancing critical to the Internet of Things in healthcare market share continuity.

Hospitals explore network slicing to segregate life-critical traffic from administrative flows. Regulators approve indoor spectrum allocations, allowing providers to run private 5G micro-cells with carrier-grade SLAs. Suppliers that bundle hardware, SIM lifecycle management, and analytics dashboards gain traction over commodity module vendors. Connectivity therefore shifts from cost-line item to strategic differentiator within the IoT in healthcare market.

By Deployment Model: Edge Computing Gains Momentum

Cloud remained the deployment preference with 66.80% revenue in 2025, enabling pooled analytics on 134 petabytes of imaging data under Philips’ stewardship. The on-premise/edge segment will rise at 22.55% CAGR, spurred by data-sovereignty statutes and the clinical imperative for sub-second responsiveness. Intel-powered edge gateways process AI inferencing near devices, lowering trips to the cloud and satisfying privacy boards.

Hybrid topologies emerge as default, orchestrating workloads across core and edge based on latency and cost sensitivity. Vendors that offer unified observability across tiers gain procurement favor. This architectural gravitation ensures long-run spend diversification and stabilizes supplier opportunity across the IoT in the healthcare market.

Geography Analysis

North America retained 41.85% revenue in 2025, fortified by Medicare’s permanent remote-monitoring CPT codes and an FDA fast-track environment for wearable diagnostics Strong EHR penetration eases device-platform integration, while venture-capital activity supplies scaling fuel for startups. State Medicaid programs increasingly replicate federal reimbursement, expanding addressable populations. As a result, the IoT in healthcare market enjoys predictable demand curves across the United States and Canada.

Europe posted steady growth under the European Health Data Space, which allocates EUR 810 million to interoperability projects. Germany’s hospital reform law mandates electronic patient records, propelling middleware upgrades. The EU Battery Regulation 2023/1542 raises design complexity but aligns with sustainability mandates. Simultaneously, the AI Act clarifies algorithmic transparency rules, fostering clinician trust. These coordinated policies position Europe as a quality-driven yet compliant slice of the IoT in healthcare market.

Asia-Pacific is the fastest climber at 22.70% CAGR to 2031. Japan’s Medical DX initiative links national ID cards to insurance databases, streamlining IoT-data flow. In China, more than 100 smart hospitals leverage 5G campus grids for end-to-end patient tracking. India’s Ayushman Bharat Digital Mission seeds foundational IDs for future device integration. High smartphone penetration and competitive telecom pricing encourage household monitoring kits, expanding the IoT in healthcare market footprint well beyond megacities. South America and the Middle East and Africa are nascent but primed for leapfrog adoption once broadband gaps narrow.

Competitive Landscape

The IoT in healthcare market remains moderately fragmented, with device majors, cloud hyperscalers, and niche sensor innovators vying for platform primacy. Medtronic posted USD 32.4 billion in 2024 revenue, buoyed by connected insulin pumps and cardiac patches that generate subscription telemetry streams. Philips selected AWS as its reference cloud to accelerate algorithm deployment, avoiding costly data-center upkeep. GE Healthcare partners with the same provider to build foundation AI models for radiology, underscoring how hardware firms harness cloud reach to expand service catalogs.

Oracle debuted a clinical digital assistant that trims documentation time by 4.5 minutes per patient visit. Microsoft embeds AI scribes in 400-plus health systems, shaving five minutes off each encounter. These workflows complement device telemetry, stitching a fuller care-continuum platform that enlarges the Internet of Things in healthcare market addressable value.

Emerging specialists pursue defensible niches: iRhythm monopolizes AI-scored arrhythmia detection; Movano targets hormonal analytics for women; Biofourmis integrates therapy adherence with genomic markers. Private-equity capital gravitates to such sub-segments, expecting acquisition exits as majors consolidate. Overall, the top five vendors command roughly 40% revenue, translating to a market concentration score of 6 on the 1–10 scale.

IoT In Healthcare Industry Leaders

Medtronic PLC

Koninklijke Philips NV

Cisco Systems

International Business Machines Corporation (IBM)

GE Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Philips and Mass General Brigham began co-developing live-data infrastructure for continuous heart monitoring, pairing biosensors with AI analytics for earlier cardiac-event detection.

- February 2025: Oracle introduced its Clinical Digital Assistant for ambulatory clinics, automating note capture and cutting daily physician documentation by 20–40%.

- January 2025: CMS finalized Physician Fee Schedule updates that formalize telehealth and remote-monitoring reimbursement (CPT 99453-99458) at USD 19.73–82.16 per service.

- November 2024: Medtronic logged USD 8.4 billion in Q2 FY-2025 revenue, with 12.4% Diabetes-segment growth attributed to the MiniMed 780G.

Global IoT In Healthcare Market Report Scope

As per the scope of this report, IoT in the healthcare system context refers to every device connected to the internet for a wide range of applications, such as tracking patients or equipment, gathering data, and analyzing the received data. The study analyzes market trends and outlines the IoT in the healthcare industry.

The Internet of Things (IoT) in the healthcare market is segmented by component (medical devices, systems and software, services), application (telemedicine, inpatient monitoring, medication management, other applications), end user, and geography.

| Medical Devices | Wearable External Medical Devices |

| Implanted Medical Devices | |

| Stationary Medical Devices | |

| Systems and Software | |

| Services |

| Tele-medicine |

| In-patient Monitoring |

| Medication Management |

| Imaging and Diagnostics |

| Asset and Staff Tracking |

| Emergency Response |

| Hospitals and Clinics |

| Clinical Research Organisations |

| Home-care / Patients |

| Other End-users |

| Bluetooth Low Energy (BLE) |

| Wi-Fi |

| Cellular and 5G |

| LPWAN (NB-IoT, LoRaWAN) |

| Zigbee and Other Short-range |

| Cloud |

| On-premise / Edge |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Middle East and Africa | GCC |

| South Africa |

| By Component | Medical Devices | Wearable External Medical Devices |

| Implanted Medical Devices | ||

| Stationary Medical Devices | ||

| Systems and Software | ||

| Services | ||

| By Application | Tele-medicine | |

| In-patient Monitoring | ||

| Medication Management | ||

| Imaging and Diagnostics | ||

| Asset and Staff Tracking | ||

| Emergency Response | ||

| By End-user | Hospitals and Clinics | |

| Clinical Research Organisations | ||

| Home-care / Patients | ||

| Other End-users | ||

| By Connectivity Technology | Bluetooth Low Energy (BLE) | |

| Wi-Fi | ||

| Cellular and 5G | ||

| LPWAN (NB-IoT, LoRaWAN) | ||

| Zigbee and Other Short-range | ||

| By Deployment Model | Cloud | |

| On-premise / Edge | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Middle East and Africa | GCC | |

| South Africa | ||

Key Questions Answered in the Report

What is the current size of the IoT in healthcare market?

The market stands at USD 207.4 billion in 2026 and is projected to reach USD 483.72 billion by 2031.

Which component segment dominates spending?

Services lead with 45.40% revenue in 2025 due to the integration and maintenance complexity of connected-care deployments.

Which application is expanding fastest?

Asset and Staff Tracking is forecast to grow at a 20.87% CAGR through 2031 as hospitals pursue efficiency gains.

How are reimbursement changes influencing adoption?

Medicare’s CPT 99453-99458 codes reimburse remote monitoring at USD 19.73–82.16 per service, creating predictable revenue that accelerates investment in connected devices.

Why is Asia-Pacific the fastest-growing region?

Government digital-health programs, extensive 5G rollouts, and rising chronic-disease prevalence drive a 22.70% CAGR across the region.

What cybersecurity measures are becoming mandatory?

Proposed HIPAA updates will require multi-factor authentication, data encryption, and AI-driven breach containment, with first-year compliance costs estimated at USD 9.3 billion.

Page last updated on: