Indonesia Connected Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

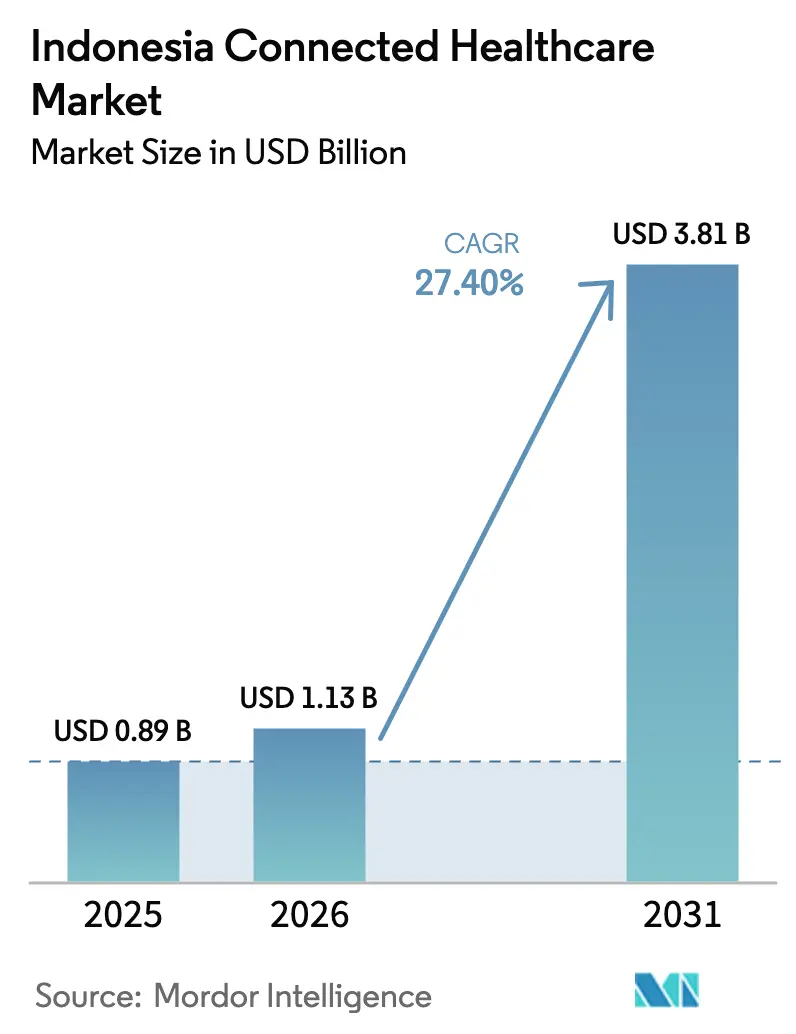

| Base Year Market Size (2025) | USD 0.89 Billion |

| Market Size (2026) | USD 1.13 Billion |

| Market Size (2031) | USD 3.81 Billion |

| Growth Rate (2026 - 2031) | 27.40% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Connected Healthcare Market Analysis by Mordor Intelligence

Indonesian connected healthcare market size in 2026 is estimated at USD 1.13 billion, growing from 2025 value of USD 0.89 billion with 2031 projections showing USD 3.81 billion, growing at 27.4% CAGR over 2026-2031. Government digitization mandates, expanding 5G coverage, and steady venture-capital inflows form the backbone of this expansion, while interoperability rules built around the SATUSEHAT platform lower integration risk for providers.[1]Dezan Shira & Associates, “New Regulation Opens Up Foreign Investment Opportunities in Indonesia's Hospital Sector,” ASEAN Briefing, aseanbriefing.com 5G pilots have already proven latency thresholds below 25 milliseconds, opening the door to remote surgery and real-time tele-ICU coordination. Venture funding rounds topping USD 100 million underscore investor confidence in nationwide scale-up opportunities. Platform stickiness also improves as mobile wallets and e-pharmacy links simplify the full care journey. Finally, cloud deployment preference shortens time to value for small facilities outside Java, accelerating addressable-market conversion.

Key Report Takeaways

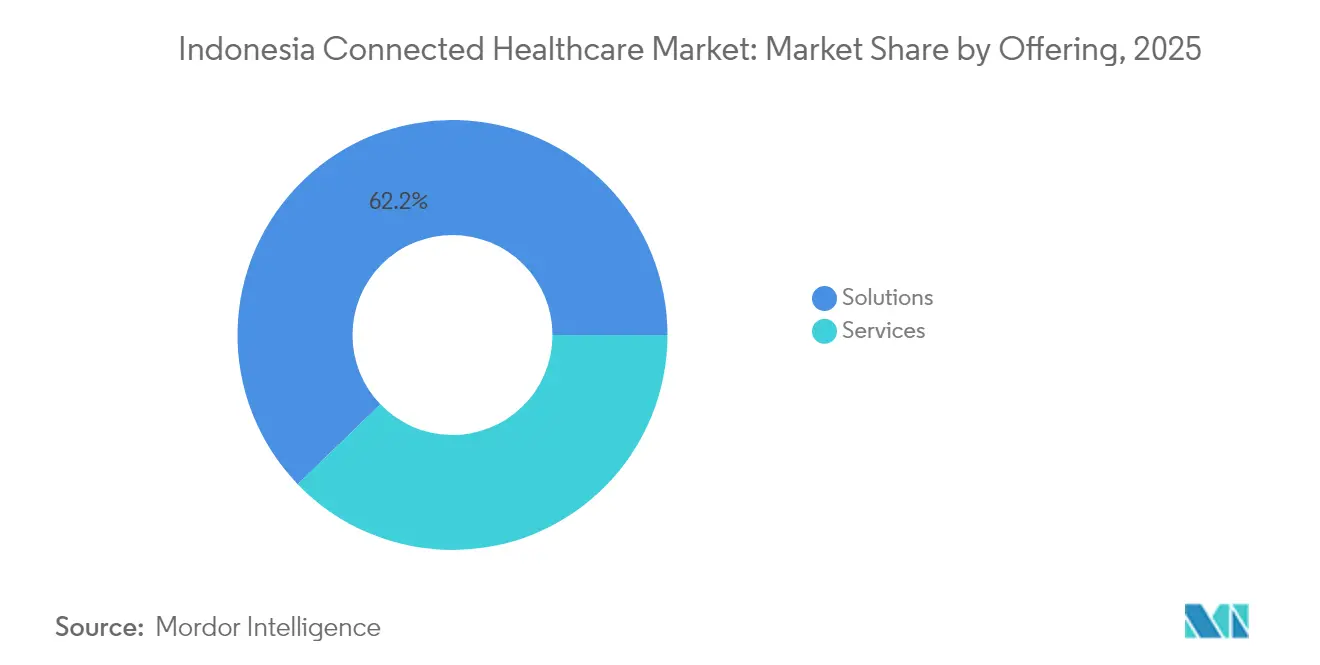

- By offering, solutions held 62.20% of the Indonesian connected healthcare market share in 2025, while services are projected to expand at a 28.1% CAGR to 2031.

- By care setting, hospitals commanded a 45.20% share of the Indonesian connected healthcare market size in 2025; home care is advancing at a 28.7% CAGR through 2031.

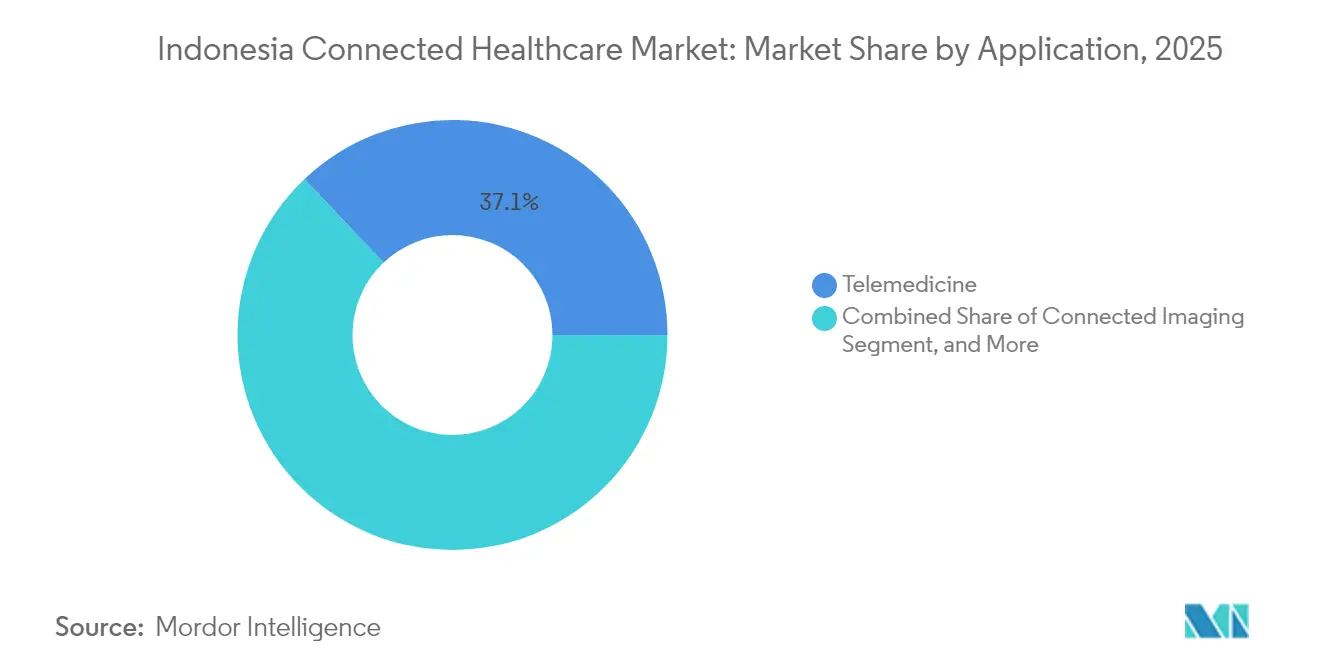

- By application, telemedicine led with a 37.10% share of the Indonesian connected healthcare market in 2025; remote patient monitoring and wearables are forecast to grow at a 28.9% CAGR to 2031.

- By deployment model, cloud-based platforms captured a 64.90% share of the Indonesian connected healthcare market in 2025 and are poised for a 28.2% CAGR through 2031.

- By end user, healthcare providers accounted for a 48.10% share of the Indonesian connected healthcare market in 2025, whereas government and public-health agencies registered the fastest 28.6% CAGR to 2031.

- By region, Java dominated with a 54.80% slice of the Indonesian connected healthcare market in 2025; Papua and Maluku are on track for a 28.9% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple countries and regions, with Indonesia representing one among them. The global report on connected healthcare market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

Indonesia Connected Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising healthcare spending | +4.2% | National; strongest in Java and Sumatra | Medium term (2-4 years) |

| Government support for digital health | +6.8% | National; early gains in Java, Kalimantan, Sulawesi | Long term (≥ 4 years) |

| Smartphone and internet penetration | +5.1% | National; rapid uptake in Papua and Maluku | Short term (≤ 2 years) |

| Mandatory SATUSEHAT integration | +7.3% | National; compliance focus in Java and Sumatra | Medium term (2-4 years) |

| VC funding for self-management start-ups | +2.9% | Java-centric | Short term (≤ 2 years) |

| 5G pilot tele-ICU deployments | +3.4% | Java and Bali initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Support for Digital Health

Health Law 17/2023 made electronic records compulsory and aligned privacy rules with the Personal Data Protection Law, giving hospitals a clear regulatory runway and predictable compliance costs. The opening of hospital ownership to 100% foreign equity under Government Regulation 47/2021 adds capital depth and imported expertise. Health Special Economic Zones in Bali and Batam supply tax holidays and fast-track permits, lowering project risk for cross-border clinics. During the pandemic, the Ministry of Health enlisted private telehealth platforms to triage patients, proving the value of public-private models. These precedents now inform budget allocations within the USD 4 billion modernization program backed by the Asian Infrastructure Investment Bank.

Mandatory SATUSEHAT Data-Platform Integration

All providers must align with SATUSEHAT by 2025, triggering a nationwide shift from proprietary formats to HL7 FHIR standards.[2]“A Preliminary Implementation of HL7 FHIR to Achieve Interoperability in Indonesia's Local EHR,” IEEE Xplore, ieee.org Compliance unlocks priority access to JKN reimbursement, pushing even small clinics toward certified vendors. For suppliers, the rule compresses sales cycles because interoperability is pre-specified. The government, meanwhile, gains real-time datasets for epidemic early-warning systems and resource planning, paving the way for AI-driven decision support. High initial integration outlays exist, yet amortize quickly through preferred-vendor status and reduced interface custom work.

Smartphone and Internet Penetration

The internet user base hit 460 million, almost all on mobile, giving telehealth apps an instant distribution pipe. Rural adoption is strong: more than half of one leading platform’s users log in from outside Java. Affordable handsets now ship with oximeters and ECG patches, reducing the need for dedicated RPM hardware. Digital wallets embedded in health apps close the payment loop, important in areas where bank penetration is below 50%. Together, these factors lower entry barriers for new app-based disease-management services.

5G Pilot Tele-ICU Deployments

Telkomsel’s trials between Bali and Jakarta demonstrated latency at 15-20 milliseconds, sufficient for robotic surgery haptics. Critical-care specialists can now supervise multiple ICUs via HD feeds, easing the specialist shortfall. Indosat’s AI-RAN rollout adds predictive network optimization, ensuring stable bandwidth during emergencies. These successes have accelerated inclusion of low-latency clauses in hospital procurement tenders, a trend expected to extend to Sumatra and Kalimantan over the forecast horizon.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited healthcare infrastructure | -3.8% | Papua, Maluku, outer Kalimantan | Long term (≥ 4 years) |

| Digital-health talent shortage | -2.6% | National; acute in Sulawesi and Papua | Medium term (2-4 years) |

| Uncertain JKN reimbursement for RPM devices | -1.9% | National | Short term (≤ 2 years) |

| Fragmented provincial procurement rules | -2.1% | National; varying by province | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Healthcare Infrastructure

At 1.49 hospital beds per 1,000 people, capacity lags ASEAN peers, constraining follow-up care after virtual consults. Many outer-island clinics lack stable power or broadband, hindering device connectivity. Specialist distribution is stark: Java hosts the bulk of cardiologists and neurologists, forcing rural telemedicine consults to refer patients hundreds of kilometers for procedures. Without local diagnostic gear, digital visits risk becoming dead ends, denting consumer trust.

Digital-Health Talent Shortage

Curricula at most medical schools still omit telehealth protocols, producing graduates unprepared for hybrid care models.[3]Nikkei Asia, “Indonesia Makes Billion-Dollar Health Care Bet to Keep Rich Patients at Home,” kr-asia.com Beyond clinicians, demand outstrips supply for informatics analysts and cybersecurity staff, driving wage inflation and turnover. Hospitals often lose IT talent to fintech or e-commerce firms that pay premiums. Professional bodies remain wary of large-scale foreign recruitment, limiting knowledge transfer. These gaps raise onboarding costs and slow rollouts, especially at provincial government facilities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Solutions Dominate Early, Services Surge

Solutions held 62.20% of the Indonesian connected healthcare market share in 2025 as organizations prioritized core systems like EHRs and teleconsult platforms before building internal support teams. However, services are growing at a 28.1% CAGR as facilities seek integration help and managed support to maximize solution performance. The government’s preference for turnkey outcomes further props up service uptake. In parallel, outcome-based contracts encourage vendors to bundle analytics, training, and security monitoring with software licenses.

The maturing buyer profile also favors recurring services revenue. Hospitals tackling SATUSEHAT upgrades require quarterly interoperability checks and continuous user-training refresh cycles. Cloud providers now embed compliance dashboards, generating annuity streams from smaller clinics unable to hire dedicated IT staff. Together, these shifts convert once-off license sales into multi-year service engagements, stabilizing vendor cash flows and lifting long-run market value.

By Care Setting: Hospitals Anchor, Homecare Accelerates

Hospitals captured 45.20% of the Indonesian connected healthcare market size in 2025, thanks to capital access and the need for enterprise-wide integration. Yet home care is the star performer, expanding at a 28.7% CAGR, bolstered by aging-in-place trends and BPJS reimbursement pilots for chronic-care RPM kits. Consumers accustomed to on-demand ride-hailing find similar convenience in app-based nurse visits, driving uptake beyond major cities.

Clinics and polyclinics function as transitional hubs, often serving as referral gateways from teleconsult apps to tertiary centers. Emergency medical services are weaving in connected-ambulance dashboards that transmit vitals en route, cutting golden-hour mortality. Pharmacies leverage e-prescription APIs to pivot into same-day medication delivery, inserting a new patient-engagement touchpoint within the broader ecosystem. Collectively, these settings create a continuum where hospital-centric care shifts progressively toward lower-cost community venues.

By Application: Telemedicine Base Enables RPM Upside

Telemedicine led with a 37.10% share in 2025, offering the initial consumer hook into the Indonesian connected healthcare market. Remote patient monitoring and wearables, though smaller, are growing at a 28.9% CAGR as IoT sensors pair with AI analytics for proactive disease management. Connected imaging gains from 5G throughput that allows radiologists in Jakarta to read scans from Papua without compression loss.

In-patient monitoring systems feed continuous data into hospital command centers, driving rapid code-blue alerts. E-Prescription modules, integrated with national formularies, reduce fraud and ensure drug-interaction checks. Niche categories such as mental-health chatbots and veterinary tele-consults widen the total addressable base, diversifying revenue streams for multi-service platforms.

By Deployment Model: Cloud Leads, Hybrid Bridges

Cloud-based systems owned a 64.90% share in 2025 and are growing at a 28.2% CAGR. Automatic patching and elastic storage lower the total cost of ownership for district hospitals and rural clinics.

Data-localization clauses in the privacy law spur domestic data-center expansion, keeping sensitive records within Indonesian borders. On-premise persists among tier-1 hospitals running AI workloads on-site for latency reasons. Hybrid models blend edge processing with cloud analytics to meet both security and scalability needs.

By End User: Providers Predominate, Government Gains Pace

Healthcare providers controlled a 48.10% share in 2025, acting as system integrators of record for multi-vendor modules. Government and public-health bodies, rising at 28.6% CAGR, turn to population-level dashboards for outbreak surveillance and resource allocation.

Patients and caregivers push for intuitive UX and transparent pricing, influencing feature roadmaps. Payers deploy fraud-detection AI to curb duplicate claims, while aligning reimbursements with remote-monitoring outcomes.

Geography Analysis

Java commanded 54.80% of 2025 revenue, reflecting dense infrastructure and tech-savvy consumers. Java’s primacy stems from Jakarta’s policy influence and a concentration of tertiary hospitals that pilot advanced use cases like AI-assisted diagnostics and robotic surgery. Leading networks such as EMC Healthcare employ enterprise EHRs with ambient documentation, setting performance benchmarks for provincial facilities. Broadband penetration exceeding 90% supports video-first consultations, while venture studios cluster around Bandung’s tech universities, feeding continual app innovation.

Papua and Maluku, though smaller, are forecast for a 28.9% CAGR on the back of satellite connectivity and government subsidy schemes. Papua and Maluku deliver the fastest growth. Satellite backhaul now supplies clinics with 30 Mbps links, sufficient for low-bandwidth video triage. Community health workers equipped with an AI-enabled translation bridge bridge dialect gaps during virtual visits. Partnerships with faith-based NGOs provide offline-first patient-education modules, increasing digital-health literacy. Bali and Nusa Tenggara, meanwhile, target inbound medical tourists seeking elective procedures bundled with wellness retreats, reinforcing investment into interoperable EHRs that meet overseas insurer requirements.

Sumatra ranks second, buoyed by resource-sector income that finances occupational-health mandates. Plantation operators deploy wearables to monitor worker fatigue, linking alerts to tele-clinicians in Medan. Kalimantan’s scattered population benefits from drone-delivered medications tested in mining concessions. Provincial governments layer telehealth kiosks onto new fiber routes laid for the Nusantara capital project, narrowing digital divides.

Competitive Landscape

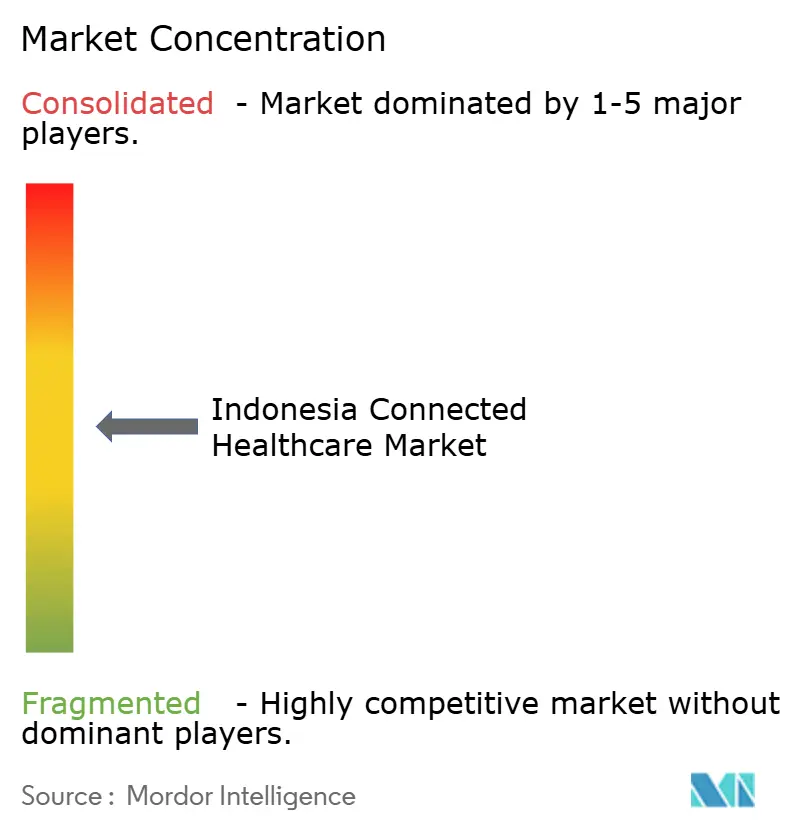

The Indonesian connected healthcare market supports a moderately fragmented field where no single firm exceeds 15% revenue share. Domestic unicorns Halodoc and Alodokter excel at direct-to-consumer engagement, leveraging multilingual interfaces and BPJS integration for sticky user bases. Global OEMs Philips, Medtronic, and Siemens Healthineers dominate device layers, inserting proprietary data protocols that necessitate middleware partnerships. Telecom incumbents Telkomsel and Indosat supply 5G edge nodes and co-develop quality-of-service SLAs tailored for clinical payloads.[4]Fitra Ashari, “Telkomsel Dukung Pemanfaatan Teknologi Kesehatan Telerobotik,” antaranews.com

Strategic moves highlight convergence. Halodoc’s USD 100 million Series D bankrolls pharmacy-delivery expansion and chronic-care RPM kits. Alodokter’s tie-up with Marubeni adds 100,000 maternal-health users and deepens Japanese corporate links. EMC Healthcare engages InterSystems to deliver AI-coded EHR modules, reducing clinician admin time. Device makers increasingly bundle analytics-as-a-service to shift revenue toward recurring streams, while courting local software vendors for localization know-how. Data-interoperability compliance with SATUSEHAT emerges as the decisive buying criterion, eclipsing standalone feature checklists.

Indonesia Connected Healthcare Industry Leaders

PT Media Dokter Investama (Halodoc)

PT Sumo Teknologi Solusi (Alodokter)

PT Good Doctor Technology Indonesia (Good Doctor)

PT Medika Komunika Teknologi (KlikDokter)

PT SehatQ Harsana Emedika (SehatQ)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: EMC Healthcare joined hands with InterSystems to introduce an advanced electronic health record platform across Indonesian facilities. The system relies on artificial intelligence for clinical coding and uses ambient audio tools to streamline documentation, all while meeting SATUSEHAT interoperability requirements and national privacy rules.

- February 2025: Full enforcement of Government Regulation 47/2021 opened Indonesia’s hospital sector to 100 percent foreign ownership and reduced the minimum bed count for foreign-owned hospitals from 200 to 100. The move is already drawing overseas investment and giving global device makers a direct route into the market, setting the stage for faster technology transfer and new clinical skills.

- February 2025: McKinsey & Company released a study on Indonesia’s digital-health transition that tracks Halodoc’s growth from a basic teleconsult service into a broad health ecosystem serving more than 20 million users. The report underscores Halodoc’s integration with BPJS Kesehatan and its role in extending care to outer-island communities with limited physical infrastructure.

- January 2025: Medical schools partnered with technology firms to embed digital-health modules in their curricula and to offer continuing education for practicing clinicians, a step toward easing the shortage of professionals with combined medical and technology expertise.

Indonesia Connected Healthcare Market Report Scope

Connected healthcare refers to the use of technology to deliver healthcare services remotely through leveraging a combination of internet connectivity, medical devices, and software applications to bridge the gap between patients and healthcare providers. The scope comprises revenue offerings in solutions and services among various applications.

The Indonesian connected healthcare market is segmented by offerings (solutions and services), applications (telemedicine, connected imaging, in-patient monitoring, and other applications), and region (Java, Sumatra, Kalimantan, and other regions). The market sizes and forecasts are provided in terms of value in (USD) for all the segments.

| Solutions |

| Services |

| Hospitals |

| Clinics and Polyclinics |

| Homecare |

| Emergency Medical Services |

| Pharmacies |

| Telemedicine |

| Connected Imaging |

| In-patient Monitoring |

| Remote Patient Monitoring and Wearables |

| ePrescription and Medication Management |

| Other Applications |

| Cloud-based |

| On-Premise |

| Hybrid |

| Healthcare Providers |

| Payers and Insurers |

| Patients and Caregivers |

| Government and Public Health Agencies |

| Java |

| Sumatra |

| Kalimantan |

| Sulawesi |

| Papua and Maluku |

| Bali and Nusa Tenggara |

| By Offering | Solutions |

| Services | |

| By Care Setting | Hospitals |

| Clinics and Polyclinics | |

| Homecare | |

| Emergency Medical Services | |

| Pharmacies | |

| By Application | Telemedicine |

| Connected Imaging | |

| In-patient Monitoring | |

| Remote Patient Monitoring and Wearables | |

| ePrescription and Medication Management | |

| Other Applications | |

| By Deployment Model | Cloud-based |

| On-Premise | |

| Hybrid | |

| By End User | Healthcare Providers |

| Payers and Insurers | |

| Patients and Caregivers | |

| Government and Public Health Agencies | |

| By Region | Java |

| Sumatra | |

| Kalimantan | |

| Sulawesi | |

| Papua and Maluku | |

| Bali and Nusa Tenggara |

Key Questions Answered in the Report

What revenue is the Indonesia connected healthcare market projected to generate by 2031?

The market is expected to reach USD 3.81 billion by 2031, growing at a 27.4% CAGR.

Which offering category is expanding fastest in Indonesia’s connected healthcare space?

Services are rising at a 28.1% CAGR as providers look for integration, training, and managed-support contracts.

How dominant is cloud deployment among Indonesian healthcare providers?

Cloud platforms captured 64.90% share in 2025 and are forecast for a 28.2% CAGR as facilities seek scalability and quick compliance.

Why are Papua and Maluku important for future market growth?

Government connectivity subsidies and satellite backhaul underpin a 28.9% CAGR, making these outer-island regions the fastest-growing territorial segment.

Which companies are leading direct-to-consumer digital health engagement in Indonesia?

Local unicorns Halodoc and Alodokter lead user engagement, supported by deep integration with BPJS and maternal-health platforms.

What role does the SATUSEHAT mandate play in market expansion?

SATUSEHAT enforces interoperable data standards, reducing integration barriers and incentivizing providers with preferential reimbursement access.

Page last updated on: