Internet Of Medical Things Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

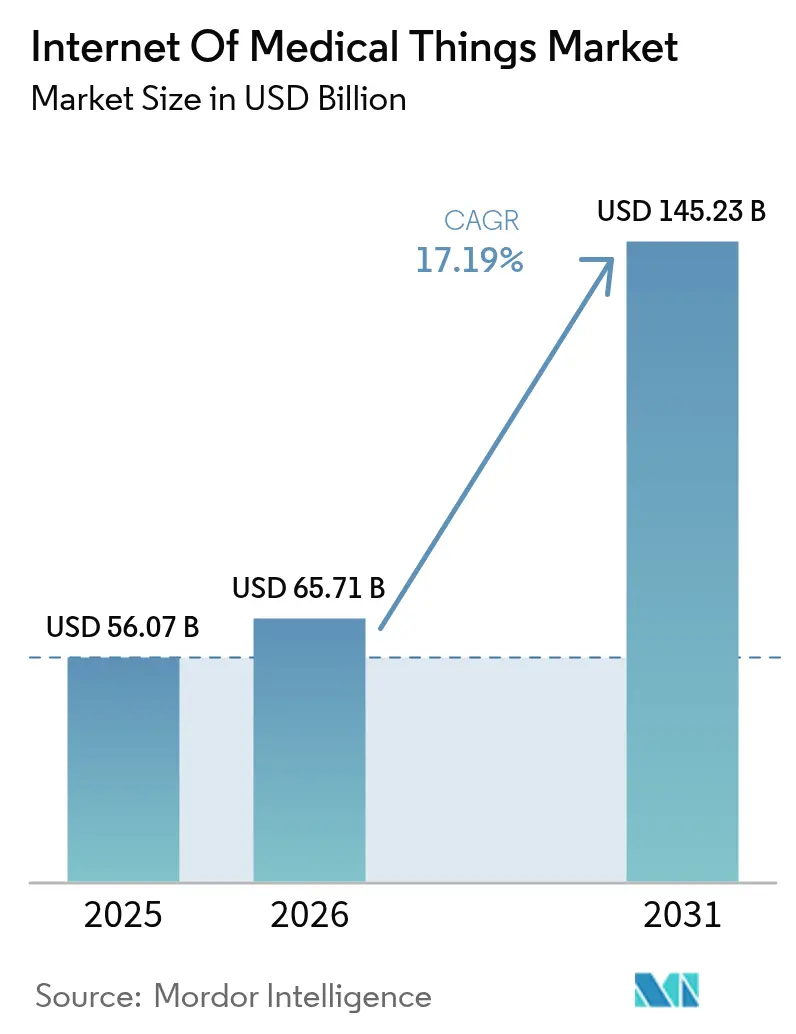

| Market Size (2026) | USD 65.71 Billion |

| Market Size (2031) | USD 145.23 Billion |

| Growth Rate (2026 - 2031) | 17.19% CAGR |

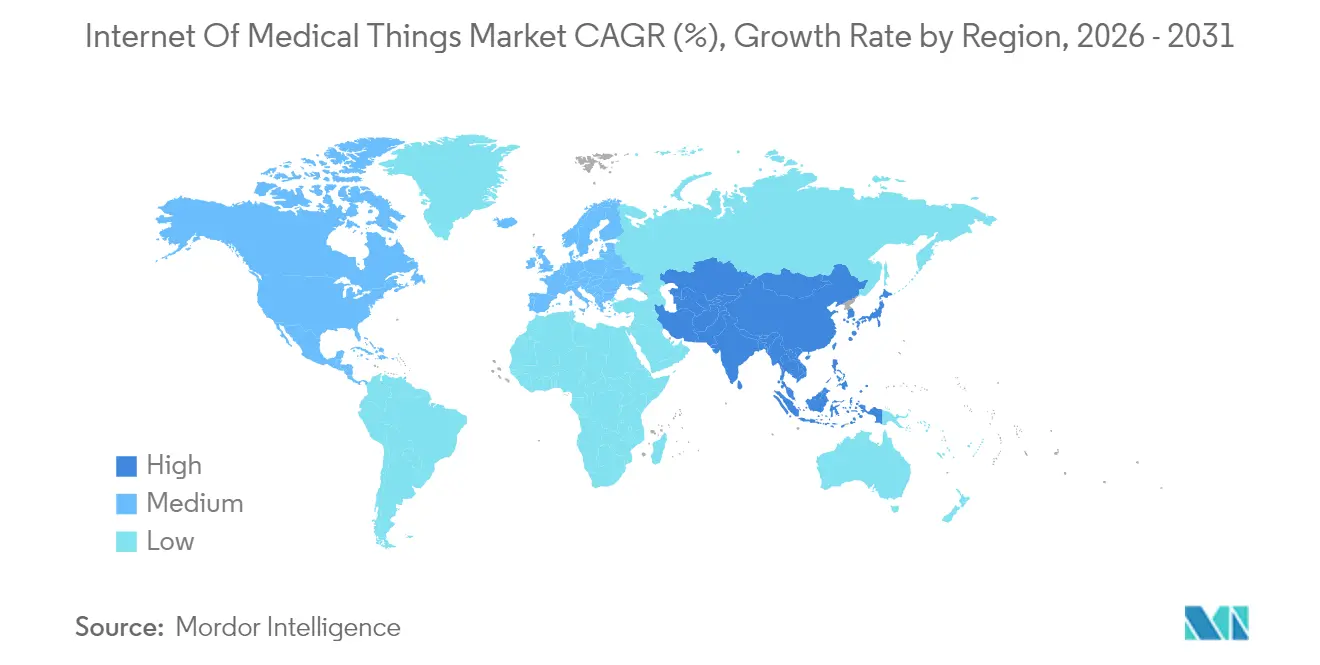

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Internet Of Medical Things Market Analysis by Mordor Intelligence

The Internet of Medical Things Market size is expected to grow from USD 56.07 billion in 2025 to USD 65.71 billion in 2026 and is forecast to reach USD 145.23 billion by 2031 at 17.19% CAGR over 2026-2031. Strong momentum reflects healthcare providers’ shift to connected-care models that blend real-time data analytics with remote monitoring to curb costs and improve outcomes. Growth also benefits from ultra-low-power AI sensors, private 5G rollouts across hospital campuses, and cyber-insurance requirements that compel full device visibility. New reimbursement rules that reward measurable outcome improvements keep capital flowing into connected solutions, while semiconductor shortages spur innovation in edge architectures that reduce hardware dependencies. Regionally, North America sustains leadership through mature infrastructure and favorable regulation, yet Asia Pacific registers the fastest expansion as 5G investments and government-backed digital-health programs accelerate adoption.

Key Report Takeaways

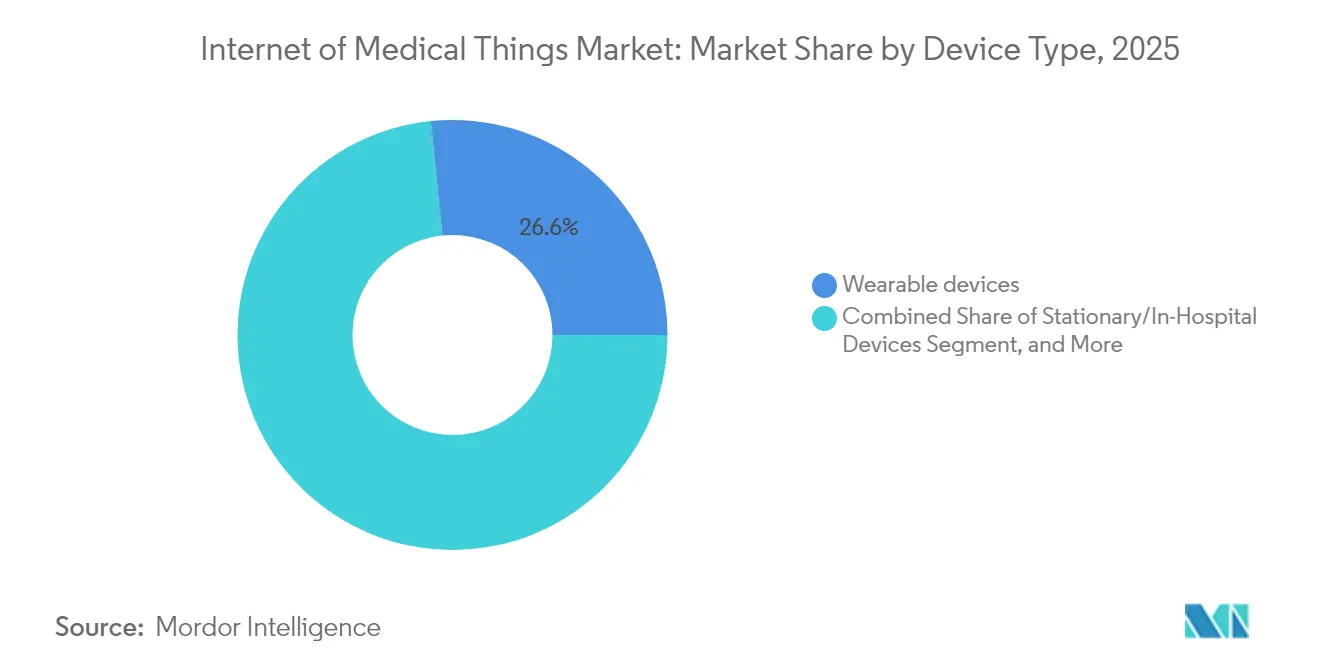

- By device type, wearable devices led with 26.62% of the Internet of Medical Things market share in 2025, while implantable devices are forecast to grow at a 19.04% CAGR through 2031.

- By product type, vital signs monitoring devices commanded a 32.08% share of the Internet of Medical Things market size in 2025; implantable cardiac devices are projected to expand at a 17.62% CAGR to 2031.

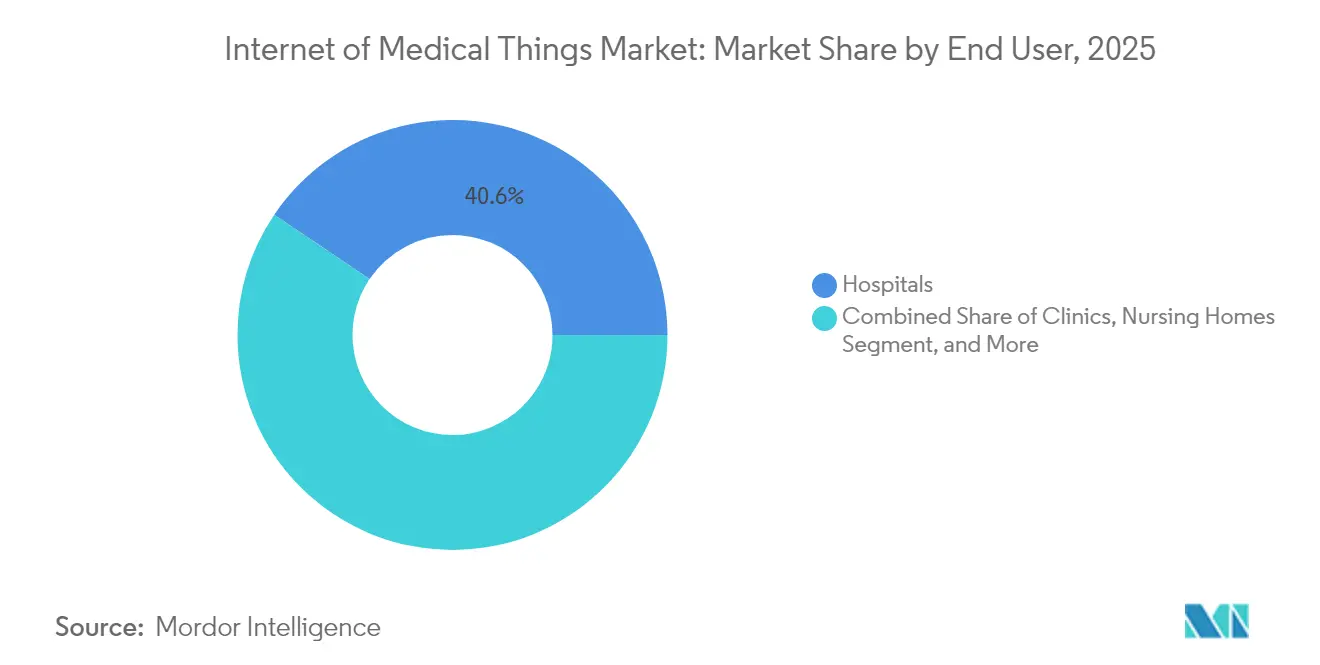

- By end user, hospitals accounted for 40.56% of the Internet of Medical Things market size in 2025, whereas home-care settings are advancing at an 18.25% CAGR to 2031.

- By connectivity technology, Wi-Fi maintained a 44.28% revenue share in 2025; cellular IoT and LPWAN are expected to grow at a 19.83% CAGR through 2031.

- By region, North America held 38.22% of the Internet of Medical Things market share in 2025, and Asia Pacific is projected to record a 20.71% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Internet Of Medical Things Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-reduction pressure on global healthcare systems | +3.20% | Global | Medium term (2–4 years) |

| Proliferation of connected wearables and implantables | +4.10% | North America & EU, APAC core | Short term (≤ 2 years) |

| Shift to outcomes-based and remote patient-monitoring models | +3.80% | Global, early gains in North America, Europe | Medium term (2–4 years) |

| Roll-out of private 5G and edge networks in hospitals | +2.90% | North America & EU, APAC emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost-reduction Pressure on Global Healthcare Systems

Healthcare providers face steep cost escalation, with United States supply-chain disruptions pushing expenses up by 15% in 2025. Connected devices cut unplanned downtime through predictive maintenance and real-time asset tracking, as illustrated by RWJBarnabas Health’s USD 9 million savings after deploying a location system that eliminated device losses[1]“Real Time Location Systems Deliver Return on Investment,” Stanley Healthcare, stanleyhealthcare.com. Value-based reimbursement amplifies adoption because hospitals must document outcome improvements alongside cost controls. Capital budgets consequently treat the Internet of Medical Things market as essential infrastructure, prompting multiyear procurement commitments. Insurers further link reimbursement to documented savings, reinforcing a cycle that channels operating funds to connected platforms.

Proliferation of Connected Wearables and Implantables

Breakthroughs in wireless power and miniaturized sensor arrays now permit battery-free devices that transmit only relevant data, conserving bandwidth and energy. Brown University demonstrated salt-sized sensors capable of monitoring intracranial pressure and glucose simultaneously, enabling continuous care without recurrent surgery. Consumer demand for preventive health data broadens deployment beyond clinical settings, ensuring the Internet of Medical Things market finds growth in wellness as well as disease management. Device makers embed edge AI that filters noise before transmission, reducing cloud-processing costs. Regulatory pathways are smoothing as real-world performance data accumulates, shortening approval cycles for next-generation implants.

Shift to Outcomes-based and Remote Patient-Monitoring Models

Outcomes-linked contracts reward providers for measurable improvements rather than service volume, accelerating connected-device uptake[2]Marie Johnson, “Hospital-at-Home Model Saves Millions,” American Hospital Association, aha.org. Guthrie Clinic’s virtual hub saved USD 7 million in labor and cut nurse turnover to 13% through remote monitoring. COVID-19 validated hospital-at-home models that now receive routine reimbursement in mature markets. Asia Pacific outpaces other regions in digital-health tool adoption, with AI decision support integrated across many public systems. The Internet of Medical Things market benefits as continuous data streams support personalized care pathways while easing capacity constraints.

Roll-out of Private 5G and Edge Networks in Hospitals

Hospitals view private 5G as foundational for latency-sensitive applications such as remote surgery. Sweden’s USD 35 million VGR-5G program links 500 medical facilities, replacing legacy DECT voice systems. China’s First Affiliated Hospital of Soochow University connected more than 3,000 devices over a 5G network, cutting deployment time by 90%. Edge compute nodes process imaging and AI monitoring onsite, lowering bandwidth needs and enhancing resilience during connectivity interruptions. These networks' future-proof capacity for exploding data volumes as the Internet of Medical Things market scales.

Restraints Impact Analysis*

| Restraint | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of in-house IoT skills in provider organisations | -2.10% | Global, acute in developing markets | Medium term (2–4 years) |

| Escalating ransomware premiums diverting IoMT budgets | -2.30% | North America & EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage of In-house IoT Skills in Provider Organisations

Thirty percent of healthcare enterprises cite data-security expertise shortages as an adoption hurdle. Smaller hospitals struggle to recruit cyber-literate engineers, widening the gap between resource-rich systems and rural facilities. Managed services bridge some needs but introduce vendor-lock risks and subscription overhead. Talent deficits are pronounced in Southeast Asia despite high investment intent. Without robust in-house teams, deployment timelines extend, slowing Internet of Medical Things market penetration.

Escalating Ransomware Premiums Diverting IoMT Budgets

Healthcare ransomware incidents now average one breach per week, with per-incident costs reaching USD 10.93 million. Insurers require multi-factor authentication and network segmentation before underwriting, shifting funds from device procurement to security controls. The sector’s 61% ransom payment rate emboldens attackers, forcing providers to prioritize cyber defenses over expanded connectivity. Consequently, organizations face a chicken-and-egg dilemma: they need visibility tools to qualify for insurance, yet require insurance to approve device investments, tempering short-term Internet of Medical Things market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Implantables Drive Innovation Surge

Implantable devices represent the fastest-growing segment, projected to expand at 19.04% CAGR through 2031, while wearables maintained leadership with 26.62% share of the Internet of Medical Things market size in 2025. Wireless power transfer and sub-millimeter sensors eliminate battery replacements and support continuous multi-parameter measurement. Stationary in-hospital systems remain connectivity hubs for network orchestration, ensuring data integrity across thousands of endpoints.

The University of California’s ultrasound-powered fluorescence sensor shows how deep-tissue imaging can guide cancer therapy without external leads. Wearables absorb these advances, combining sensor fusion with edge analytics to issue timely alerts. Emerging smart contact lenses and biodegradable probes add niche opportunities that diversify the Internet of Medical Things market. Regulatory approvals favor implants that demonstrate longitudinal safety and outcome benefits, encouraging sustained R&D spending.

By Product Type: Cardiac Devices Accelerate Growth

Vital-sign monitoring products held a 32.08% share in 2025, demonstrating their role as baseline tools across care settings. Implantable cardiac devices are slated to grow at a 17.62% CAGR, supported by closed-loop neuromodulation that optimizes therapy based on real-time neural feedback. Respiratory monitors gain relevance due to rising COPD prevalence, while anaesthesia machines integrate connected sensors to enhance intraoperative safety.

Predictive maintenance algorithms applied to imaging systems and ventilators reduce downtime and extend asset life. Smart pill dispensers and connected rehabilitation gear broaden engagement beyond acute care, adding recurring revenue streams for vendors. Together, these dynamics elevate the Internet of Medical Things market and enhance cross-device ecosystem value.

By End User: Home-care Settings Transform Delivery

Hospitals retained 40.56% of the Internet of Medical Things market size in 2025, yet home-care settings are projected to grow at an 18.25% CAGR as virtual wards become mainstream. Continuous monitoring at home reduces readmissions and frees hospital beds for higher acuity cases. Clinics and nursing homes adopt connected workflows to optimize staffing and coordinate chronic-disease management.

Guthrie Clinic’s virtual hub illustrates cost savings and staff retention benefits, marking a reference model for similar deployments. Progress in plug-and-play wireless sensors lowers installation barriers, enabling smaller providers to offer clinical-grade remote monitoring. These trends expand the Internet of Medical Things market into community care and pave the way for preventive service packages.

By Connectivity Technology: Cellular IoT Gains Momentum

Wi-Fi accounted for 44.28% of revenue in 2025, but cellular IoT and LPWAN solutions are forecast to climb at a 19.83% CAGR through 2031 as providers extend monitoring beyond facility walls. Private 5G within hospitals reserves dedicated bandwidth for mission-critical applications, while LTE-M and NB-IoT support low-power devices across broad geographies.

Bluetooth continues to link wearables to smartphones, and Zigbee maintains relevance for sensor-dense environments. Emerging Li-Fi and satellite links serve remote or shielded locations, creating multi-path architectures that raise reliability. Edge processing at the radio gateway trims backhaul requirements, boosting scalability for the Internet of Medical Things market.

Geography Analysis

North America commanded a 38.22% share in 2025, propelled by mature health-IT infrastructure and regulatory pathways that encourage interoperability. Public-private alliances fast-track private-5G pilots and AI-enabled diagnostics. Canada and Mexico add momentum through government-funded telehealth initiatives, while rising cyber-insurance premiums and semiconductor shortages temper near-term device rollouts. Legacy system integration remains a capital-intensive obstacle, yet strong reimbursement models keep the Internet of Medical Things market advancing.

Asia Pacific is the fastest-growing region at a 20.71% CAGR. China’s 2024 medical-informatization spending surpassed CNY 800 billion, underscoring state support. Japan and South Korea leverage advanced manufacturing to deliver next-generation sensors, and India’s national EHR rollout aids standardization. Skilled-personnel shortages persist, but cross-border training and cloud-based managed services lessen the gap. Regional collaboration spreads best practices, ensuring broad participation in the expanding Internet of Medical Things market.

Europe records steady gains supported by Medical Device Regulation compliance that clarifies connected-device requirements. Germany, the United Kingdom, and France lead adoption through funded modernization programs, while Italy and Spain tap EU stimulus to upgrade infrastructure. Strict data-privacy laws elevate implementation costs yet build patient trust. Switzerland’s Kantonsspital Baden installed more than 7,000 sensors with Siemens, proving the scalability of smart-hospital visions. Harmonized policies let smaller economies piggyback on regional frameworks, sustaining Internet of Medical Things market momentum across the continent.

Competitive Landscape

The Internet of Medical Things market remains moderately fragmented, with established device manufacturers and cybersecurity specialists contesting leadership. GE Healthcare, Philips, and Medtronic differentiate by embedding connectivity across imaging, monitoring, and therapeutic portfolios, while newer entrants emphasize software-defined platforms that decouple intelligence from dedicated hardware. Cyber-security vendors such as Armis and Cynerio secure critical infrastructure by discovering unmanaged devices; Armis reports identifying twice as many assets as clients first estimated.

Strategic acquisitions accelerate capability building. Stryker bought care.ai to integrate ambient intelligence into nursing workflows, and BD spent USD 4.2 billion on Edwards Lifesciences’ Critical Care Unit to deepen smart monitoring. Patent filings cluster around wireless power, AI sensors, and zero-trust security. Samsung’s non-invasive glucose patent hints at competitive disruption potential.

Supply-chain constraints shift focus to edge computing that reduces chip counts. Vendors offering full-stack solutions spanning device, data, and defense gain preference as hospitals seek single-throat-to-choke service models. Cyber-insurance stipulations push joint offerings that bundle monitoring with threat detection, reinforcing partnerships between device makers and security firms. These dynamics shape an ecosystem where collaboration often replaces zero-sum competition to unlock Internet of Medical Things market value.

Internet Of Medical Things Industry Leaders

GE Healthcare

Koninklijke Philips N.V.

Medtronic plc

Cisco Systems, Inc.

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: GE HealthCare delivered USD 4.8 billion Q1 2025 revenue, citing demand for AI-enabled MRI and the Flyrcado injection launch.

- February 2025: GE HealthCare unveiled a GBP 200 million partnership with Nuffield Health to deploy diagnostic equipment across the United Kingdom.

- December 2024: Lauxera Capital Partners acquired Galen Data to bolster secure cloud connectivity for medical devices.

- October 2024: Siemens and Kantonsspital Baden began installing 7,000 IoT sensors in Swiss healthcare facilities.

Global Internet Of Medical Things Market Report Scope

The Internet of Medical Things (IoMT), a subset of the Internet of Things (IoT) technologies, consists of interconnected medical and healthcare information technology devices and applications. IoMT devices transmit data over a secure network to connect doctors, patients, and medical devices such as diagnostic equipment, hospital equipment, and wearable technology.

IoMT, also known as healthcare IoT, uses automation, sensors, and machine-based intelligence, similar to general IoT devices, to reduce reliance on human intervention during routine healthcare procedures and routine monitoring operations. IoMT reduces the need for unnecessary doctor's office and hospital visits by giving patients and providers better access to a patient's health information.

The Internet of Medical Things (IoMT) Market is segmented by Devices (Wearable Devices, Stationary Devices, Implantable Devices), Products (Vital Signs Monitoring Devices, Implantable Cardiac Devices, Respiratory Devices, Imaging Systems), End Users (Hospitals, Clinics), and Geography (North America, Europe, Asia Pacific, South America, Middle East, and Africa). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Wearable Devices |

| Stationary/In-Hospital Devices |

| Implantable Devices |

| Other Device Types |

| Vital Signs Monitoring Devices |

| Implantable Cardiac Devices |

| Respiratory Devices |

| Anaesthetic Machines |

| Imaging Systems |

| Ventilators |

| Other Products |

| Hospitals |

| Clinics |

| Nursing Homes |

| Long-Term Care Centers |

| Home Care Settings |

| Zigbee |

| Bluetooth |

| Wi-Fi |

| Cellular IoT/LPWAN |

| Other Technologies |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Device Type | Wearable Devices | ||

| Stationary/In-Hospital Devices | |||

| Implantable Devices | |||

| Other Device Types | |||

| By Product Type | Vital Signs Monitoring Devices | ||

| Implantable Cardiac Devices | |||

| Respiratory Devices | |||

| Anaesthetic Machines | |||

| Imaging Systems | |||

| Ventilators | |||

| Other Products | |||

| By End User | Hospitals | ||

| Clinics | |||

| Nursing Homes | |||

| Long-Term Care Centers | |||

| Home Care Settings | |||

| By Connectivity Technology | Zigbee | ||

| Bluetooth | |||

| Wi-Fi | |||

| Cellular IoT/LPWAN | |||

| Other Technologies | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the Internet of Medical Things market?

The market reached USD 65.71 billion in 2026 and is projected to grow to USD 145.23 billion by 2031, reflecting a 17.19% CAGR.

Which device type dominates the Internet of Medical Things market?

Wearable devices lead with a 26.62% share in 2025, while implantables post the fastest growth at a 19.04% CAGR.

Why is Asia Pacific the fastest-growing region?

Government-funded 5G rollouts, national digital-health programs, and rising healthcare spending push regional growth at a 20.71% CAGR.

How are private 5G networks affecting hospital IoMT deployments?

Private 5G enables ultra-low-latency connections for applications such as remote surgery and edge AI processing, cutting deployment time and cost.

What are the main restraints on IoMT adoption?

Skill shortages in provider IT teams and rising ransomware insurance premiums divert spending from new device deployments to cybersecurity.

Which companies are making notable strategic moves in the IoMT space?

Recent highlights include Stryker’s acquisition of care.ai for virtual-care workflows and BD’s USD 4.2 billion purchase of Edwards Lifesciences’ Critical Care Unit.

Page last updated on: