Smart Grid Data Analytics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

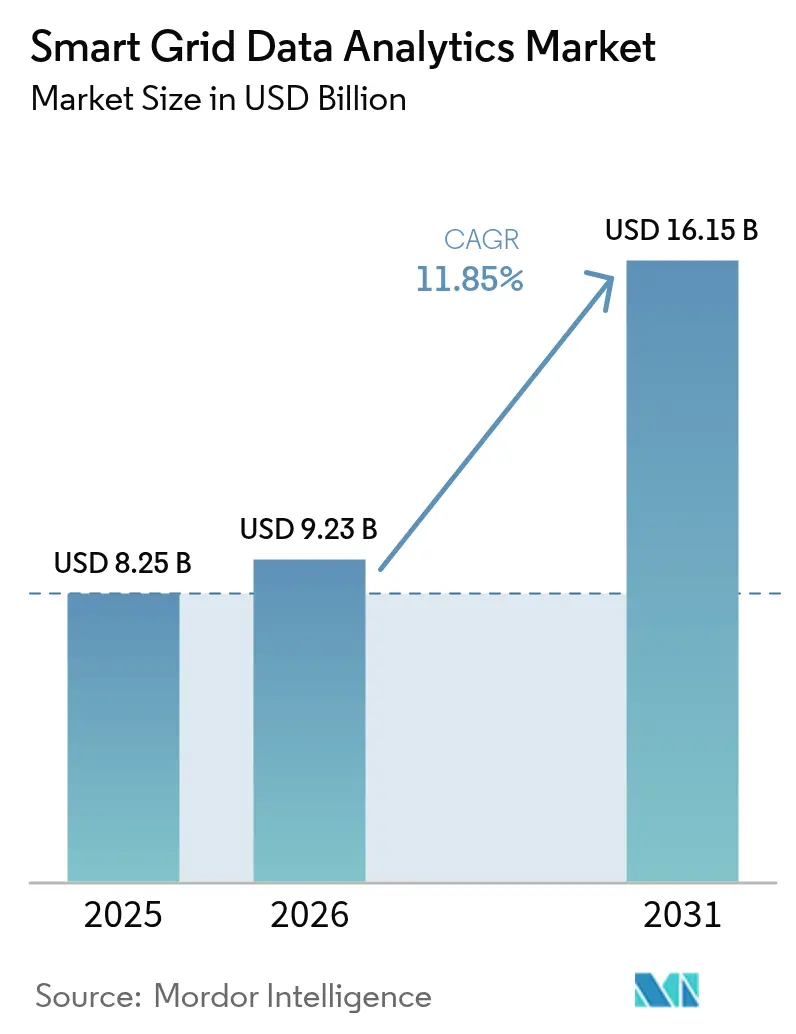

| Market Size (2026) | USD 9.23 Billion |

| Market Size (2031) | USD 16.15 Billion |

| Growth Rate (2026 - 2031) | 11.85% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Grid Data Analytics Market Analysis by Mordor Intelligence

The Smart Grid Data Analytics Market size was valued at USD 8.25 billion in 2025 and estimated to grow from USD 9.23 billion in 2026 to reach USD 16.15 billion by 2031, at a CAGR of 11.85% during the forecast period (2026-2031). Growing volumes of advanced metering infrastructure (AMI) data, rapid deployment of distributed energy resources (DERs), and expanding electric-vehicle (EV) charging networks are pushing grid operators to adopt cloud-native analytics that can turn petabytes of raw information into timely, actionable insights. Artificial intelligence (AI) and machine-learning engines now underpin load forecasting, outage prediction, and DER orchestration, giving utilities the tools to shift from reactive to predictive grid management. Vendors that bridge legacy SCADA environments with modern cloud services are seeing stronger demand, especially in markets with stringent cybersecurity mandates such as NERC-CIP and IEC 62443. Simultaneously, mounting decarbonization targets are prompting regulators to require real-time carbon-intensity reporting, creating further pull for sophisticated analytics.

Key Report Takeaways

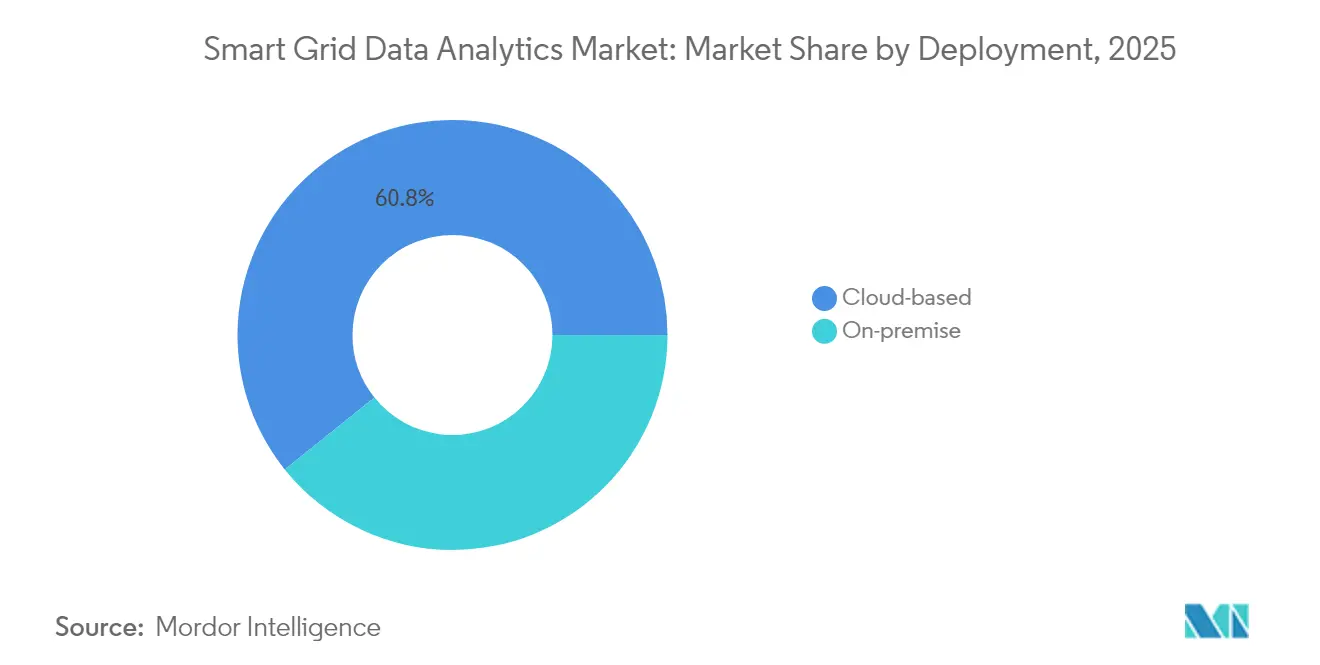

- By deployment, cloud-based platforms led with 60.75% of the smart grid data analytics market share in 2025, while on-premise solutions recorded a slower 6.92% CAGR to 2031.

- By solution, metering analytics accounted for 39.65% of revenue in 2025; asset and grid-edge analytics are poised to grow at a 13.35% CAGR through 2031.

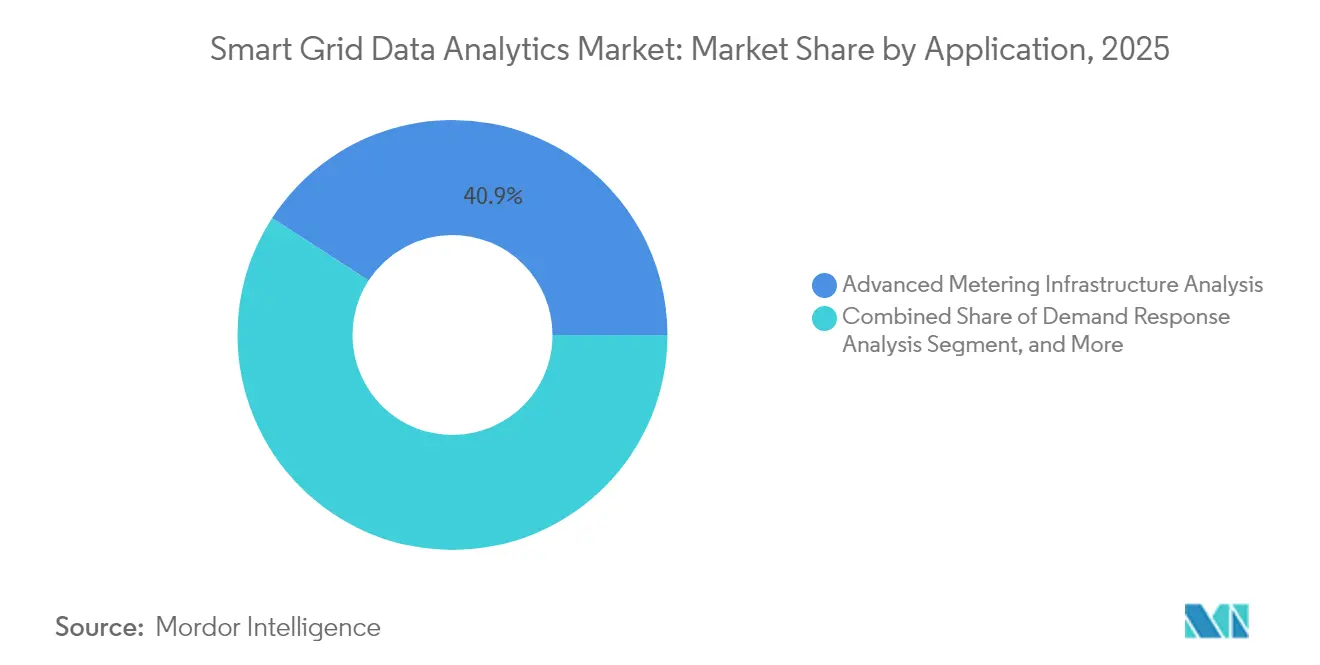

- By application, advanced metering infrastructure analysis held a 40.85% share in 2025, whereas renewable and EV integration forecasting is set to expand at a 13.98% CAGR to 2031.

- By end-user, public utilities and municipalities contributed 44.55% revenue in 2025; large energy-intensive enterprises will see the fastest 13.62% CAGR by 2031.

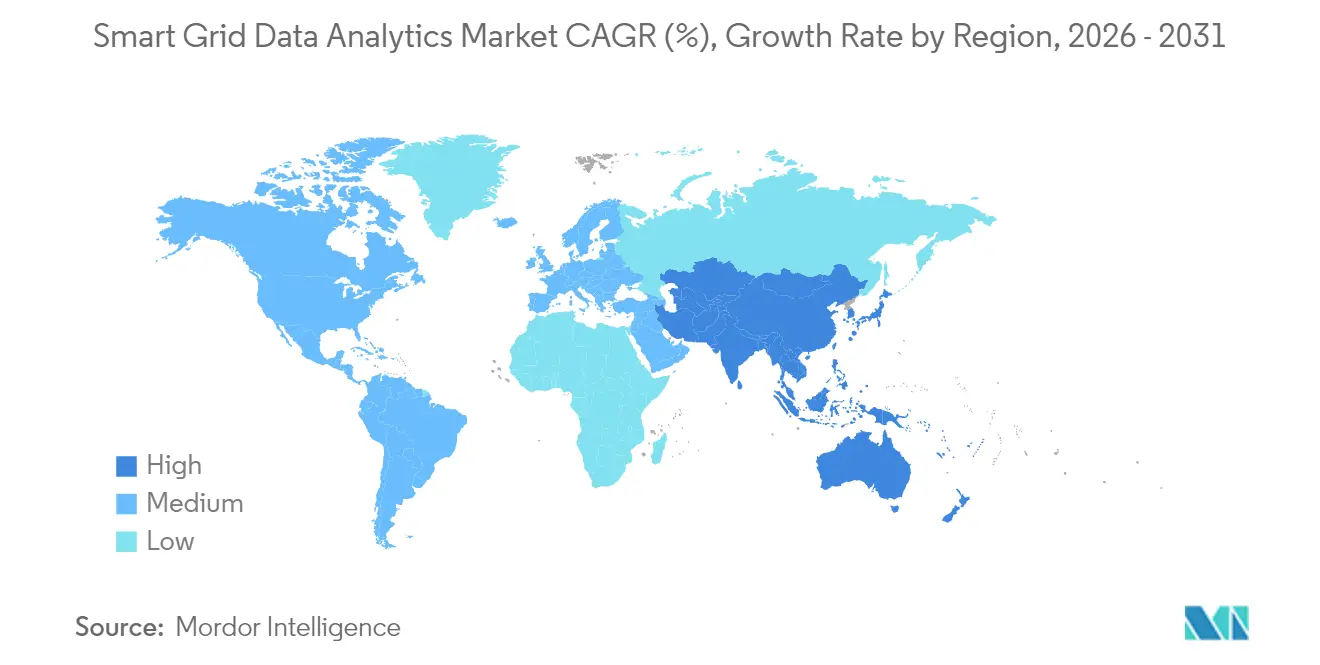

- By geography, North America led with a 36.65% share in 2025, while Asia-Pacific is projected to deliver a 13.26% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Grid Data Analytics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Utility AMI roll-outs hitting critical mass | +2.1% | Global, with acceleration in APAC and Europe | Medium term (2-4 years) |

| Shift to cloud-native grid-edge analytics | +1.8% | North America and EU leading, APAC following | Short term (≤ 2 years) |

| Mandatory decarbonisation reporting by TSOs and DSOs | +1.5% | EU primary, expanding to North America and APAC | Long term (≥ 4 years) |

| Cyber-secure analytics for NERC-CIP and IEC 62443 compliance | +1.2% | North America and EU core, spillover to APAC | Medium term (2-4 years) |

| AI-optimised EV-to-Grid load balancing pilots | +1.4% | Global, with early gains in California, Germany, China | Long term (≥ 4 years) |

| Real-time DER orchestration requirements | +1.6% | Global, concentrated in high renewable-penetration regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Utility AMI Roll-outs Hitting Critical Mass

Comprehensive AMI deployments now stream millions of time-stamped meter readings daily, giving utilities unprecedented visibility into low-voltage networks. Germany’s 98.2% success rate in remote power-limitation commands proved that next-generation meters support near-real-time grid interventions.[1]Elisabeth Springmann, “Performance Evaluation of German Smart Meter Infrastructure for Load Management Through Grid Operators,” Energy Informatics, energyinformatics.springeropen.com Utilities are therefore scaling analytics engines that ingest 150,000 data points per hour per feeder to predict overloads, preempt equipment failures, and refine tariff structures. A pilot across 20 substations and 184 feeders demonstrated that event-based analytics trimmed unscheduled maintenance by 28% and deferred USD 4 million in capex.

Shift to Cloud-Native Grid-Edge Analytics

Connecting smart meters to 5G backhaul cuts latency to single-digit milliseconds, enabling edge devices to filter noise and forward only high-value events to the cloud. Utilities avoid building costly data centers and instead subscribe to elastic processing power that runs AI models for topology optimization or volt-var control. Siemens already books over EUR 1.7 billion (USD 1.81 billion) in software-centric revenue by bundling its grid applications into a secure cloud layer.

Mandatory Decarbonization Reporting by TSOs and DSOs

New EU rules oblige system operators to publish the marginal carbon intensity of every dispatch decision. France’s RTE and Enedis co-developed a planning tool that re-routes power to circuits with lower embedded emissions, aligning with the continent-wide Energy Data Space vision. Such mandates stimulate demand for analytics that fuse operational, weather, and market data to calculate real-time carbon footprints.

AI-Optimized EV-to-Grid Load Balancing Pilots

Studies modeling 1.5-5 million EVs show peak-load reductions of up to 34.3% when AI schedules charging and dispatch. Malaysia’s pilot captured 30% energy savings by predicting charger occupancy and dynamically adjusting rates. Rocky Mountain Power’s 32,000-home VPP in Utah uses embedded analytics to shape a 600 MWh virtual battery, illustrating how bidirectional flows create new ancillary-service revenue streams.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy SCADA/MDMS interoperability gaps | -1.3% | Global, particularly acute in aging North American and European grids | Short term (≤ 2 years) |

| Rising analytics-traffic backhaul costs in rural feeders | -0.8% | Rural regions globally, most severe in developing markets | Medium term (2-4 years) |

| Data-ownership disputes between DSOs and customer apps | -0.6% | EU and North America primarily, expanding to APAC | Long term (≥ 4 years) |

| Shortage of advanced analytics talent at utilities | -0.9% | Global, with acute shortages in APAC and emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legacy SCADA/MDMS Interoperability Gaps

Utilities often operate devices from dozens of vendors, each using proprietary protocols. Bench tests on digital substations uncovered handshake issues that forced operators to purchase middleware gateways, inflating integration budgets by 17%. The need for rigorous cyber-physical validation extends project timelines as utilities test edge-to-cloud data paths for deterministic performance.

Rising Analytics-Traffic Backhaul Costs in Rural Feeders

Low-density networks may sit 80 km from fiber, making utilities depend on microwave links powered by off-grid solar. Research shows that diffractive non-line-of-sight backhaul reduces capex up to 45% yet requires sophisticated 3D mapping utilities rarely possessed. High transmission costs force rural cooperatives to limit data granularity, curbing analytics benefits and slowing overall market adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment: Cloud Dominance Accelerates

Cloud deployments captured 60.75% of the smart grid data analytics market in 2025 and are forecast to grow at 12.74% CAGR to 2031. Utilities value the ability to spin up advanced AI workloads without capital outlays, while hyperscale providers guarantee multilayer cybersecurity and continuous software upgrades. In contrast, on-premise deployments persist where regulators mandate data residency or where latency-sensitive feeder automation requires local compute. As Siemens’ grid-software revenue already surpasses USD 1.81 billion, investment is shifting toward “analytics-as-a-service” subscriptions that monetize continuous insights rather than one-time licenses.

Growing adoption of virtual power plants (VPPs) illustrates why the cloud model scales better. The U.S. Department of Energy targets 80-160 GW of aggregated VPP capacity by 2030, and nearly every platform relies on distributed cloud microservices to run stochastic optimization across millions of devices. As those requirements intensify, the smart grid data analytics market size for cloud deployment is projected to capture USD 10.35 billion by 2031, more than tripling the on-premise total.

By Solution: Metering Analytics Leads Asset Intelligence

Metering analytics represented 39.65% revenue in 2025, reflecting utilities’ historic focus on billing accuracy, theft detection, and time-of-use tariff design. Yet, asset and grid-edge analytics is the fastest climber at 13.35% CAGR as operators prioritize condition-based maintenance for transformers, reclosers, and power electronics. IBM’s survey shows 70% of digitally mature utilities already use AI to schedule maintenance windows, cutting forced outages by 23%.

The convergence of edge computing and AI is key: sensors now embed lightweight neural networks that flag anomalies locally, forwarding only high-risk events to the cloud. This tiered architecture lowers bandwidth bills while enabling sub-second fault isolation. Consequently, the smart grid data analytics market size for asset intelligence is forecast to reach USD 4.75 billion by 2031, representing 29.40% of total spending and reflecting the shift toward proactive grid stewardship.

By Application: Renewable Integration Drives Growth

Advanced metering infrastructure analysis still dominates with 40.85% revenue, but utilities urgently need analytics that orchestrate solar, wind, and EV fleets. Renewable and EV integration forecasting, therefore, posts the highest 13.98% CAGR through 2031. Deep-learning models now assimilate real-time weather, locational marginal prices, and feeder-level load to recommend charge-discharge schedules that flatten peaks. EnergyShare AI demonstrated peer-to-peer algorithms that improved self-consumption by 19% in pilot microgrids.

As DER penetration climbs, transmission operators demand high-resolution inertia forecasts and fast-frequency-response analytics. Vendors responding with specialized libraries for phasor measurement unit (PMU) streams are winning multi-year framework contracts. Consequently, the smart grid data analytics market share for renewable integration software is expected to surpass 18.65% by 2031, up from 11.40% in 2025, underscoring its centrality to a decarbonized grid mix.

By End-user Vertical: Industrial Enterprises Accelerate Adoption

Public utilities and municipalities commanded 44.55% spending in 2025, yet large energy-intensive enterprises are forecast to lead growth at 13.62% CAGR. These firms-ranging from data centers to steel mills-deploy behind-the-meter analytics that synchronize production schedules with solar output or spot-price dips, shaving energy bills and earning flexibility payments. Schneider Electric’s USD 700 million U.S. investment prioritizes industrial microgrids equipped with AI dispatch engines that can island or grid-connect on demand.

Industrial adoption also responds to Scope 2 emission pledges; corporates seek verifiable proof of renewable sourcing, which granular analytics can supply. Hence, the smart grid data analytics market size allocated to industrial users is projected to hit USD 3.55 billion by 2031, nearly doubling the segment’s 2025 baseline.

Geography Analysis

North America generated the largest revenue, holding 36.65% of the smart grid data analytics market in 2025, due to mature AMI roll-outs, wholesale market reforms, and federal investment tax credits that reward DER orchestration. Utilities here increasingly bundle analytics subscriptions into rate-based filings, ensuring stable cost recovery. Canada’s new AI R&D hub for battery manufacturing further strengthens the regional ecosystem, positioning local vendors near key EV-supply-chain customers.

Asia-Pacific is the fastest mover with a projected 13.26% CAGR to 2031. China’s State Grid Corporation embeds analytics in every phase of its ultra-high-voltage projects, while India’s Revamped Distribution Sector Scheme allocates USD 40 billion to digitalize feeders. Malaysia’s AI-based charging pilots illustrate how emerging economies leapfrog legacy infrastructure to adopt cloud-native solutions. Consequently, the region’s contribution to the smart grid data analytics market size will nearly double by 2031, surpassing USD 4.45 billion.

Europe benefits from stringent decarbonization rules and data-space initiatives that mandate interoperability. Germany’s 98.2% command-success benchmark validates continent-wide technical maturity. Southern Europe’s emphasis on open energy data is pushing distribution companies to adopt standardized analytics that expose real-time metrics to third-party service providers.

South America and the Middle East, and Africa collectively represent under 10% of revenue today, but rising electrification and renewable targets are catalyzing pilot deployments. Utilities in Chile and the United Arab Emirates now integrate PMU-based analytics to stabilize high solar penetration, signaling fertile ground for vendor expansion once telecom backhaul improves.

Competitive Landscape

The smart grid data analytics market remains moderately fragmented. Legacy operational-technology suppliers-Siemens, Schneider Electric, GE Vernova, and Hitachi-bundle hardware, communications, and analytics, capitalizing on decades-long utility relationships. Cloud-native players such as AutoGrid and BluWave-ai differentiate on AI-first architectures that ingest unstructured data sets and deliver sub-minute forecasting.

Strategic alliances are growing. GE Vernova and Itron link grid-edge telemetry with a common data fabric, creating a turnkey analytics stack that tackles data-ownership conflicts and accelerates deployment schedules.[4]GE Vernova, “Better Together: GE Vernova and Itron Unleash the Power of Grid Edge Data,” na.itron.com Siemens partners with hyperscalers to embed its GridOS suite into secure multi-tenant clouds, enabling pay-as-you-grow models ideal for mid-size municipal utilities.

Investment flows favor AI and edge computing. Honeywell’s 5G-enabled smart meters stream event-driven data, while IBM’s quantum-safe encryption pilots address looming cybersecurity mandates. Start-ups focusing on federated learning and privacy-enhancing computation are drawing venture capital as regulators press for customer-centric data governance. Collectively, the top five vendors accounted for roughly 36% revenue in 2024, indicating scope for consolidation as utilities standardize on interoperable platforms.

Smart Grid Data Analytics Industry Leaders

Siemens AG

Itron Inc.

Landis + Gyr Group AG

Oracle Corporation

SAS Institute Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Schneider Electric committed USD 700 million to U.S. grid-modernization and AI initiatives, adding 1,000 jobs and expanding domestic manufacturing.

- March 2025: Siemens invested CAD 150 million (USD 112 million) to open an AI R&D center for battery production in Canada.

- March 2025: Honeywell and Verizon integrated 5G modules into Honeywell smart meters for real-time monitoring and firmware upgrades.

- January 2025: U.S. DOE issued the VPP Liftoff Report, targeting 80–160 GW of virtual power plant capacity by 2030.

- December 2024: GE Vernova and Itron partnered to merge Grid-Edge Intelligence with the GridOS Data Fabric.

- December 2024: Siemens Smart Infrastructure set 6–9% revenue growth and 16–20% profit goals, aided by data-driven services.

- September 2024: Rocky Mountain Power, sonnen, and ES Solar began transforming 32,000 rooftop solar systems into dispatchable assets.

Global Smart Grid Data Analytics Market Report Scope

The Smart Grid Data Analytics Market study defines the revenues generated from the sales of smart grid data analytics solutions across various applications, including advanced metering infrastructure analysis, demand response analysis, and grid optimization analysis.

The study characterizes the smart grid data analytics market based on the deployment, solution, applications, and end-user verticals. The smart grid data analytics market is segmented by deployment (cloud-based and on-premise), solution (transmission and distribution (T&D) network, metering, and customer analytics), application (advanced metering infrastructure analysis, demand response analysis, and grid optimization analysis), end-user vertical (private sector (SMEs and large enterprises), public sector), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Cloud-based |

| On-premise |

| Transmission and Distribution Network |

| Metering Analytics |

| Customer Analytics |

| Asset and Grid-Edge Analytics |

| Advanced Metering Infrastructure Analysis |

| Demand Response Analysis |

| Grid Optimisation and Predictive Maintenance |

| Renewable and EV Integration Forecasting |

| Public Utilities and Municipalities |

| Investor-Owned Utilities (IOUs) |

| Cooperative and Community Utilities |

| Large Energy-Intensive Enterprises |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Singapore | ||

| Malaysia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Deployment | Cloud-based | ||

| On-premise | |||

| By Solution | Transmission and Distribution Network | ||

| Metering Analytics | |||

| Customer Analytics | |||

| Asset and Grid-Edge Analytics | |||

| By Application | Advanced Metering Infrastructure Analysis | ||

| Demand Response Analysis | |||

| Grid Optimisation and Predictive Maintenance | |||

| Renewable and EV Integration Forecasting | |||

| By End-user Vertical | Public Utilities and Municipalities | ||

| Investor-Owned Utilities (IOUs) | |||

| Cooperative and Community Utilities | |||

| Large Energy-Intensive Enterprises | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Singapore | |||

| Malaysia | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is driving the rapid growth of the smart grid data analytics market?

Utilities worldwide are scaling AMI roll-outs, integrating DERs and meeting decarbonization mandates, which together push annual spending to a projected USD 16.15 billion by 2031.

Which deployment model is gaining the most traction?

Cloud-based analytics dominate, holding 60.75% share in 2025 and expanding at a 12.74% CAGR as operators favor scalable, pay-as-you-go platforms.

Why are industrial enterprises adopting smart grid analytics?

Large energy-intensive facilities can cut energy costs, monetize flexibility and verify Scope 2 emissions, driving a 13.62% CAGR in industrial demand through 2031.

How do analytics support renewable and EV integration?

AI models forecast generation and load, orchestrate bidirectional power flows and aggregate distributed assets into virtual power plants to maintain grid stability.

What are the key challenges hindering adoption?

Legacy SCADA interoperability, rural backhaul expenses and shortages of analytics talent collectively shave 2% off the forecast CAGR.

Which regions offer the highest growth potential?

Asia-Pacific leads with a 13.26% CAGR through 2031 as China and India fund large-scale smart grid initiatives and accelerate EV infrastructure roll-outs.

Page last updated on: