Multispace Parking Meter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

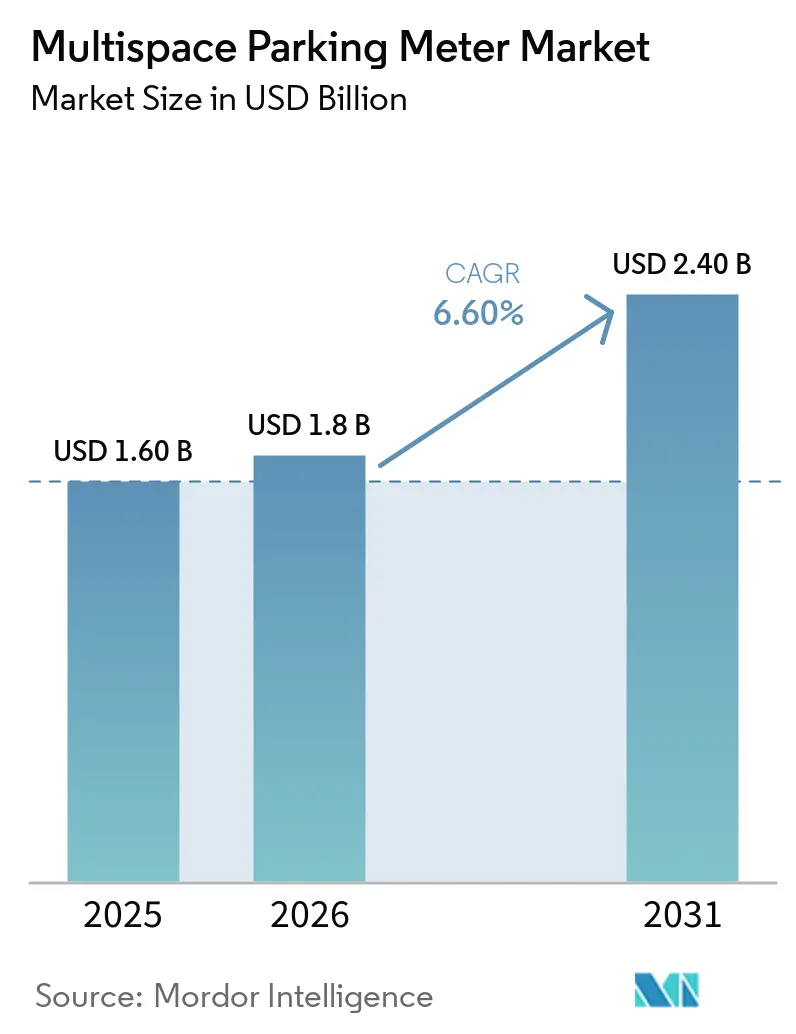

| Market Size (2026) | USD 1.8 Billion |

| Market Size (2031) | USD 2.40 Billion |

| Growth Rate (2025 - 2031) | 6.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Multispace Parking Meter Market Analysis by Mordor Intelligence

The multispace parking meters market size is projected to expand from USD 1.6 billion in 2025 and USD 1.8 billion in 2026 to USD 2.4 billion by 2031, registering a CAGR of 6.6% between 2026 and 2031. Mounting fiscal pressure on municipal budgets, rapid adoption of cashless payment mandates, and the availability of national and regional smart-city grants are steadily driving public-sector customers to retire single-space hardware in favor of networked pay stations that lower operating costs and unlock real-time curbside data. Platform vendors are bundling multispace meters with mobile applications, occupancy sensors, and analytics dashboards, allowing cities to enforce dynamic pricing, automate routing, and integrate congestion-pricing pilots. Hardware refresh cycles increasingly specify solar power, cellular connectivity, and quick-response code or near-field communication readers, as end users target carbon-neutral operations, minimize cash handling, and cater to rising consumer preference for tap-to-pay. Competitive intensity is rising as leading suppliers pursue mergers and acquisitions to secure payment technology, build data platforms, and expand regional channel partners, while smaller firms specialize in geographic or vertical niches to differentiate on service speed or localization.

Key Report Takeaways

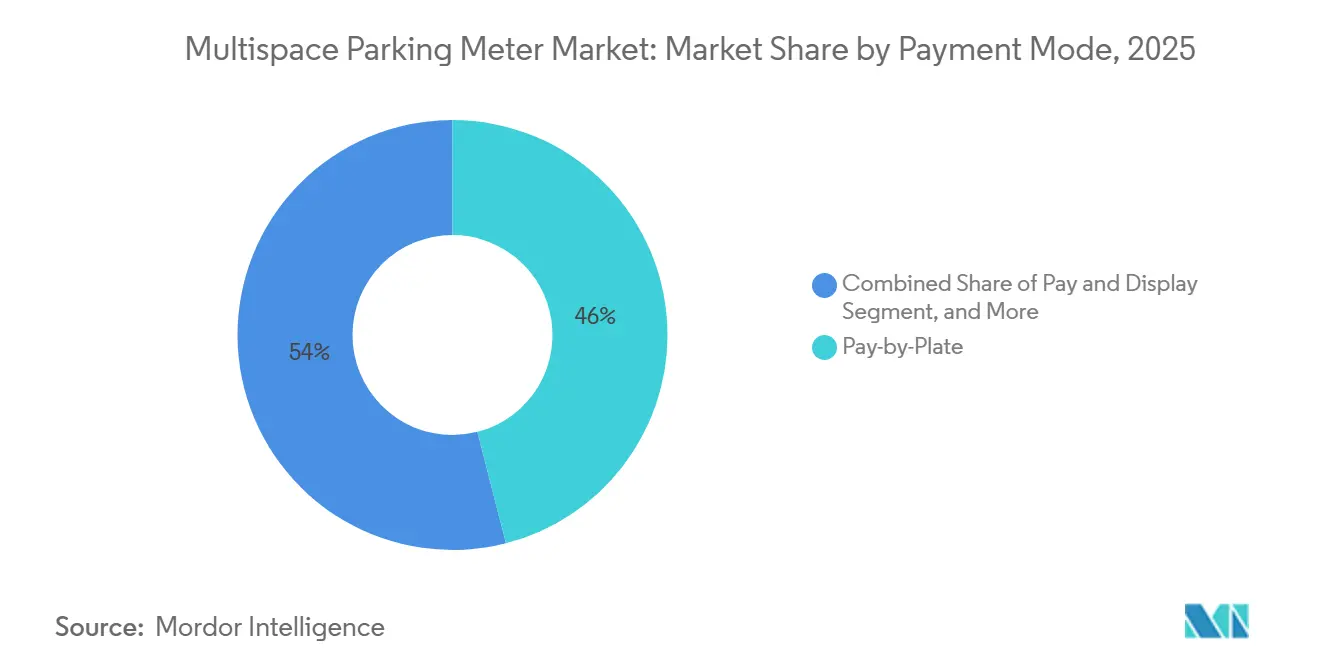

- By payment mode, the pay-by-plate segment led with 46% revenue share in 2025, while tap-to-pay and mobile-wallet interfaces are advancing at a 13.8% CAGR through 2031 in the multispace parking meter market.

- By power source, solar-powered systems captured 61% of the multispace parking meters market share in 2025, and hybrid solar-alternating current units are set to grow at an 11.2% CAGR over 2026-2031.

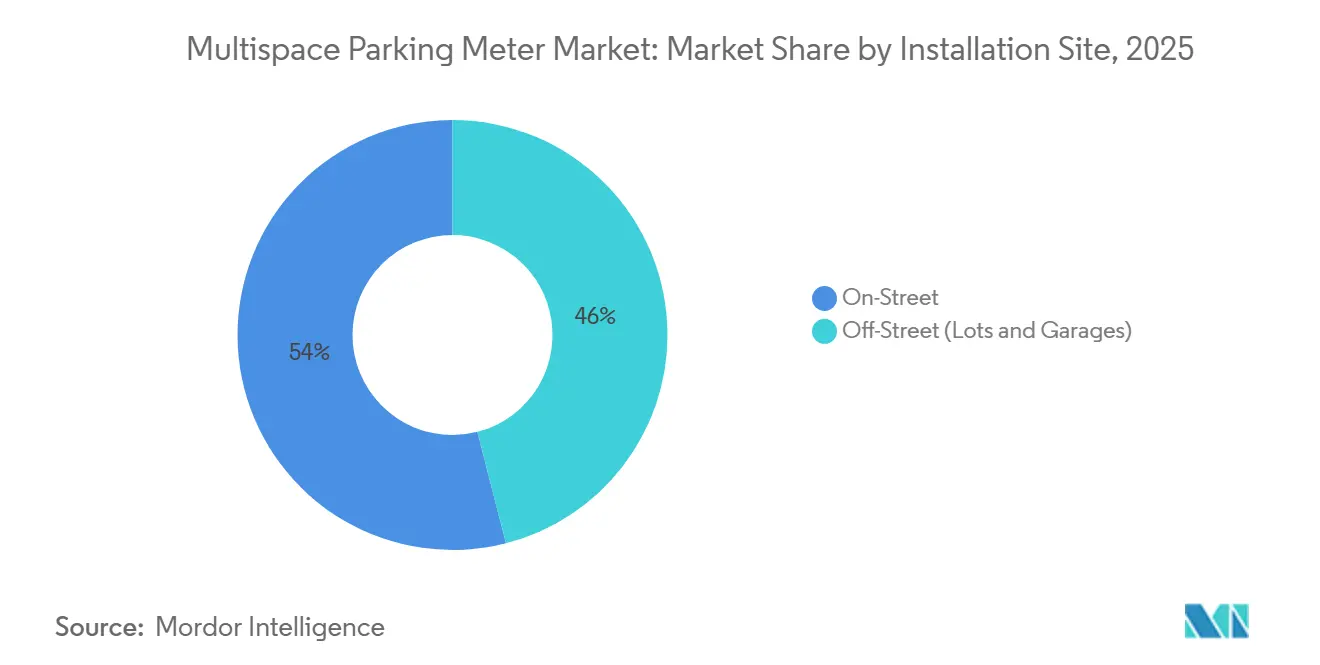

- By installation site, on-street deployments accounted for 54% of 2025 revenue, whereas off-street lots and garages are climbing at a 10.1% CAGR to 2031 in the multispace parking meter market.

- By end user, municipal and city authorities represented 48% of 2025 demand, yet universities and hospitals are forecast to expand at a 12.5% CAGR during the outlook period in the multispace parking meter market.

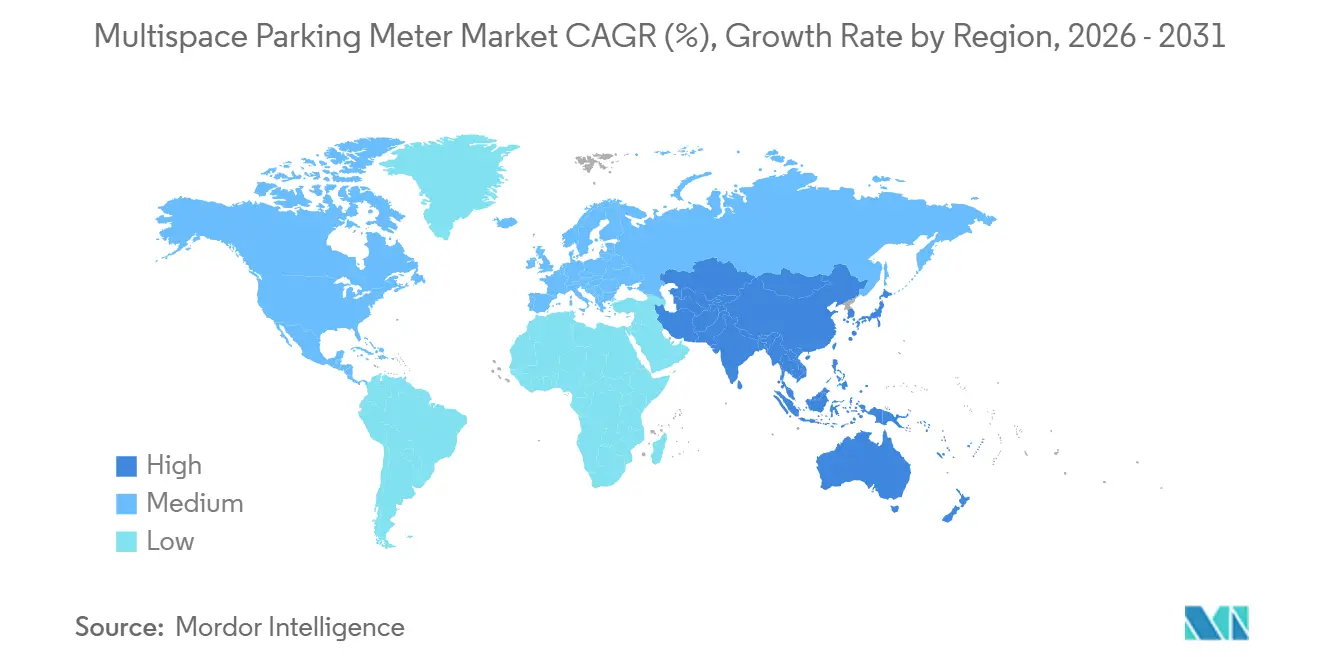

- By geography, North America held 37% of the 2025 value, but Asia-Pacific is on track for the fastest regional growth at a 9.6% CAGR through 2031in the multispace parking meter market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Multispace Parking Meter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart-City Programmes Accelerating Meter Roll-Outs | +1.8% | Global, highest in North America, Europe, APAC core cities | Medium term (2-4 years) |

| Shift Toward Cashless and Contactless Payments | +1.5% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Municipal Drive for Higher Parking-Fee Revenue | +1.2% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Preference for Solar-Powered, Low-OPEX Hardware | +0.9% | Global, strongest in Middle East, North America, Europe | Long term (≥ 4 years) |

| Integration of Pay-By-Plate Data Into Congestion-Pricing Schemes | +0.6% | North America and Europe pilots; APAC early stage | Long term (≥ 4 years) |

| In-Car Commerce APIs Enabling Automatic Meter Payments | +0.4% | North America and Europe initial roll-outs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Smart-City Programmes Accelerating Meter Roll-Outs

Federal, provincial, and city smart-city grant schemes channel capital directly into multispace pay-station projects, compressing procurement timelines and encouraging turnkey contracts that bundle hardware, software, and data analytics. The United States SMART program funded Minneapolis, Seattle, and Dubuque, enabling the deployment of integrated sensor networks and paving the way for congestion-pricing pilots.[1]U.S. Department of Transportation, “SMART Grants Program,” transportation.gov In the United Kingdom, Reading Borough Council mandated cashless pay stations across the town center, citing savings on cash collection, while Timmins, Ontario, selected solar kiosks to align with climate targets.[2]Reading Borough Council, “Cashless Parking Meters,” reading.gov.uk Such initiatives strengthen the business case for suppliers offering bundled solutions and reduce the payback period for municipalities.

Shift Toward Cashless and Contactless Payments

Global contactless penetration hit 86% in 2025, compelling cities to retrofit meters with near-field communication, electromagnetic-field, and quick-response code readers. IPS Group’s MSX Multi-Space Kiosk embeds both NFC and QR codes to meet payment card compliance requirements, shortening transaction time and reducing coin-jam maintenance. Tokyo installed cashless vending units across central wards, and Buenos Aires switched to a fully digital parking system that manages more than 80,000 bays via a mobile wallet, resulting in faster turnover and reduced vandalism. The sustained shift to cashless channels underpins hardware refresh cycles and accelerates the adoption of real-time data ecosystems.

Municipal Drive for Higher Parking-Fee Revenue

City treasuries facing structural deficits view dynamic curbside pricing and reliable collection as a quick, politically viable revenue lever. Providence, Rhode Island, experienced revenue losses after half its meters failed, triggering a wholesale replacement initiative, while Santa Fe, Argentina, embedded twice-yearly rate escalators into a multiyear concession to transfer risk to the operator.[3]Providence Journal, “Providence Parking Meter Revenue Analysis,” providencejournal.com Performance guarantees and uptime clauses in Warsaw’s decade-long contract with Flowbird further illustrate the pressure vendors face to lock in revenue targets FLOWBIRD.GROUP. Such deals elevate the importance of analytics-driven uptime and automated citation workflows.

Preference for Solar-Powered, Low-OPEX Hardware

Cities increasingly specify solar panels, deep-cycle batteries, and cellular modems to reduce trenching costs, support net-zero commitments, and future-proof assets. Lisbon, Brussels, and Waldshut-Tiengen all rolled out monocrystalline solar CitiLine or Citea models, achieving multi-year battery life and eliminating utility fees. Rising lithium-ion costs, however, lengthen payback periods and encourage hybrid units in low-irradiance regions. Hectronic’s Schaerbeek hybrid retrofit shows how operators hedge weather-related power risk while leveraging existing infrastructure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital Cost for Municipalities | -0.8% | North America and Europe most acute | Short term (≤ 2 years) |

| Modal Shift to Ride-Hailing and Micro-Mobility | -0.7% | North America and Europe peak, emerging APAC urban centers | Medium term (2-4 years) |

| EMV 3-DS2 Compliance Delaying Hardware Refresh | -0.4% | North America and Europe | Short term (≤ 2 years) |

| Lithium Battery Supply Constraints | -0.5% | Global, acute in APAC supply hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Cost for Municipalities

Unit prices for feature-rich kiosks range from USD 8,000 to USD 15,000, straining city capital budgets. New Plymouth District Council adopted a lease arrangement that spread payments over 7 years, reducing the immediate impact on the balance sheet and saving NZD 1.2 million (USD 720,000) in initial outlays. In the United Kingdom, Waverley Borough’s GBP 317,400 (USD 402,000) award required 18 months of committee approvals. These examples show how financing models, revenue-share concessions, or leasing structures can mitigate sticker shock, but they also lengthen procurement cycles.

Modal Shift to Ride-Hailing and Micro-Mobility

Academic studies find that one-quarter of ride-hailing trips replace private car journeys that would otherwise incur parking fees. Lyft reported 9 million fewer cars owned by its users and a 47% surge in electric-bike mileage in 2024, indicating a gradual but meaningful reduction in parking demand. While current ride-hailing volumes have not collapsed, occupancy rates have not risen either. Forecasts suggest a revenue inflection point by 2028 if trip counts triple from 2016 levels, pushing cities to couple meter deployment with congestion fees and curbside access pricing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payment Mode: Plate Recognition Commands Today, Wallets Accelerate Tomorrow

Pay-by-plate technology accounted for 46% of 2025 revenue, securing the largest share of the multispace parking meters market as cities seek to eliminate paper receipts and automate enforcement. Ipswich City Council awarded a AUD 2.51 million (USD 1.67 million) contract for 90 units that link automatic number plate recognition with citation back-office platforms, demonstrating the appeal of fewer site visits and reduced fraud. Taichung City’s September 2025 rollout aims for 27,000 paperless bays by 2030, affirming the scalability of license-plate architectures.

Continued momentum rests on interoperability with third-party license-plate recognition and integration into congestion-pricing schemes, especially in Asia-Pacific leapfrog markets. Tap-to-pay and mobile-wallet functions, however, are projected to grow 13.8% a year, driven by 86% of global consumers preferring contactless payments and automaker-led in-car commerce launches. BMW’s European in-car payment service exemplifies how original-equipment-manufacturer platforms can shift transactions from kiosks to dashboards, creating a dual-channel environment in which physical meters serve as enforcement and information nodes while digital wallets capture payment flows.

By Power Source: Solar Retains Leadership, Hybrids Climb in Cloudy Climates

Solar-powered units accounted for 61% of 2025 revenue, underscoring their dominance in the multispace parking meters market as cities pursue carbon neutrality and avoid trenching costs. Lisbon’s 1,200-unit portfolio and Brussels’ 9,000-unit fleet, both Monocrystalline panel installations from Hectronic, showcase the operational savings and durability of solar designs. North American municipalities such as Royal Oak, Michigan, cited utility bill elimination as a core driver of their decision to choose fully off-grid pay stations.

Hybrid solar-alternating current kiosks are expanding at an 11.2% CAGR, filling gaps in high-latitude or shaded corridors where winter irradiance dips below recharge thresholds. Hectronic’s Schaerbeek retrofit blended new hybrid stations with solar add-ons on legacy units, achieving redundancy without grid over-reliance. Volatility in lithium carbonate markets, where spot prices climbed from USD 10,798 per ton in January 2025 to USD 16,882 in December 2025, may nudge procurement officers toward hybrids that leverage smaller battery packs and harness available mains wiring for top-up charging.

By Installation Site: On-Street Still Dominates as Campuses Propel Off-Street Growth

On-street projects generated 54% of 2025 turnover, reflecting long-standing municipal priorities to replace single-space meters with pay stations serving 8-12 bays each, reduce maintenance labor, and support dynamic curb regulation. Flowbird’s 1,910-meter Strada S5 contract in Warsaw reduced part replacements and enabled real-time fee adjustments tied to occupancy sensors. The Philadelphia Parking Authority’s 2025 switch to Duncan Solutions’ AP+ platform blended loyalty programs with enforcement data, resulting in higher compliance rates.

Off-street garages and lots are forecast to rise at a 10.1% CAGR, fueled by universities, hospitals, and airports embedding pay stations into broader guidance and access-control ecosystems. The University of Iowa’s 983-space Hawkeye Ramp and the University of New Mexico Hospital’s 1,400-space facility both integrate real-time occupancy displays that cut search times and heighten customer satisfaction. Large-scale builds such as Orlando International Airport’s USD 13 million guidance retrofit covering 11,000 spaces illustrate how off-street operators treat pay stations as one node in a digital parking stack spanning sensors, signage, and mobile pre-booking.

By End User: Municipalities Pay the Bills, Hospitals and Universities Set the Pace

Municipal and city authorities bought 48% of all units in 2025, a testament to policy-driven demand and grant-linked capital inflows. Flowbird’s GBP 317,400 award with Waverley Borough, USD 53,000 deal with Mole Valley, and USD 1.01 million frame agreement with Merton exemplify repeat municipal buyers seeking standardized service contracts.

Universities and hospitals, however, offer the fastest outlook, with a 12.5% CAGR. Patient-experience mandates prompted Royal Derby Hospital to equip its 500-space garage with validation modules, while student-mobility programs at the University of Wisconsin-Madison and the University of Illinois Chicago embed guidance sensors and mobile pay options to shorten dwell times. Parking operators and concessionaires, holding 29% share, remain active in multiyear revenue-share models, such as Santa Fe’s ARS 2.6 billion (USD 2.9 million) tender, but must compete against end-user verticals eager to own data and brand the parking journey.

Geography Analysis

North America retained 37% of 2025 revenue due to Federal Highway Administration SMART funding, electromagnetic-field 3-Domain Secure 2 compliance timelines, and mergers such as EasyPark’s Flowbird acquisition that consolidate channel power. Municipalities in Minneapolis, Seattle, and Dubuque anchor early adopter status, while university and airport projects diversify demand beyond city curbs. Europe accounted for 31% thanks to solar-centric deployments in Lisbon, Munich, and Brussels. Anti-graffiti coatings, fourth-generation cellular modems, and hybrid power in northern cities mitigate climate and vandalism risks, reinforcing vendor requirement lists.

Asia-Pacific is projected to lead growth at 9.6% through 2031, as Malaysia, South Korea, Taiwan, and Vietnam leapfrog coin-and-card platforms by embracing license-plate recognition and mobile wallets. Hongcheon County’s 2026 Smart Parking Control roll-out and Sibu’s 2025 cashless system show how congestion pricing, digital-payment mandates, and national e-government programs compress adoption curves.

Middle East and Africa commanded 18% of the 2025 value, propelled by Saudi public-private partnerships such as Parkin’s 195,000-space memorandum and Saudi investment firm Merak Capital’s USD 26.7 million infusion into Arsann. Dubai’s Roads and Transport Authority recorded nearly 30 million digital tickets in 2024 and added solar kiosks to support a growing mobile channel. South America held 14% and is rising at an 8.9% CAGR, buoyed by Buenos Aires’ citywide digital parking and Rio de Janeiro’s Digital Blue Zone law that mirrors neighboring Niterói’s early success.

Competitive Landscape

The top five suppliers, Flowbird Group, IPS Group, Hectronic, Duncan Solutions, and IEM SA, controlled 63.4% of 2025 shipments, underscoring a moderately concentrated field. EasyPark’s January 2025 acquisition of Flowbird, cleared by French regulators in November 2024, created a hybrid hardware-software powerhouse positioned to upsell curb data analytics to an enlarged client base. IPS Group’s November 2025 purchase of Populus Technologies stitched curb-coding and mobility data into its enforcement stack, widening its differentiation in dynamic pricing feeds.

Regional specialists fill white space: Metric Group dominates solar pay-and-display in the United Kingdom and Gulf countries, Global Parking Solutions leads New Zealand councils, and Pacific Parking Systems tailors California-specific kiosks. Technology convergence is intensifying around 4G-to-5G modems, edge analytics, and in-car commerce APIs, with BMW and Mercedes-Benz embedding transaction flows in vehicle infotainment systems. This development could potentially erode direct kiosk revenue but reinforces the broader multispace parking meters market footprint.

Compliance hurdles such as Payment Card Industry Level 1 and electromagnetic-field 3-Domain Secure 2 certifications now act as capital-intensive entry barriers. These barriers favor scale players able to fund multi-year recertification, ensuring their continued dominance in the market.

Multispace Parking Meter Industry Leaders

Flowbird Group SA

IPS Group Inc.

Duncan Solutions Pty Ltd

MacKay Meters Inc.

Hectronic GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: BMW rolled out an in-car payment platform across 12 European markets, supporting parking, fuel, tolls, and charging.

- February 2026: Hongcheon County, South Korea, launched a smart parking system with license-plate recognition and fee collection at 500 won per 30 minutes.

- January 2026: University of New Mexico Hospital completed a 1,400-space garage with guidance sensors and multispace kiosks.

- November 2025: IPS Group acquired Populus Technologies, integrating curb data with enforcement platforms.

Global Multispace Parking Meter Market Report Scope

The Multispace Parking Meter Market Report is Segmented by Payment Mode (Pay and Display, Pay-By-Plate, Pay-By-Space, Tap-to-Pay/Mobile Wallet), Power Source (Solar-Powered, AC-Mains, Hybrid Solar-AC), Installation Site (On-Street, Off-Street), End-User (Municipal and City Authorities, Parking Operators, Transit Agencies, Universities and Hospitals), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Pay and Display |

| Pay-by-Plate |

| Pay-by-Space |

| Tap-to-Pay / Mobile Wallet |

| Solar-Powered |

| AC-Mains |

| Hybrid Solar-AC |

| On-Street |

| Off-Street (Lots and Garages) |

| Municipal and City Authorities |

| Parking Operators and Concessionaires |

| Transit Agencies and Airports |

| Universities and Hospitals |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | |

| South America |

| By Payment Mode | Pay and Display | |

| Pay-by-Plate | ||

| Pay-by-Space | ||

| Tap-to-Pay / Mobile Wallet | ||

| By Power Source | Solar-Powered | |

| AC-Mains | ||

| Hybrid Solar-AC | ||

| By Installation Site | On-Street | |

| Off-Street (Lots and Garages) | ||

| By End-User | Municipal and City Authorities | |

| Parking Operators and Concessionaires | ||

| Transit Agencies and Airports | ||

| Universities and Hospitals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | ||

| South America | ||

Key Questions Answered in the Report

What is the forecast value of the multispace parking meters market in 2031?

The multispace parking meters market size is projected to reach USD 2.4 billion by 2031, expanding at a 6.6% CAGR.

Which payment mode currently leads adoption?

Pay-by-plate systems captured 46% of 2025 revenue, making them the leading payment mode in the market, per Mordor Intelligence findings.

Why are solar-powered meters important for cities?

Solar-powered units eliminate grid-connection costs and align with carbon-neutral goals, enabling 61% of market revenue in 2025 and sustaining long-term OPEX savings.

Which region is expected to grow fastest through 2031?

Asia-Pacific is forecast to post the highest regional CAGR at 9.6% through 2031, driven by digital-first roll-outs in Malaysia, South Korea, Taiwan, and Vietnam.

How concentrated is vendor competition?

The five largest suppliers held 63.4% share in 2025, indicating moderate concentration; the EasyPark-Flowbird merger further tightens the competitive field.

What end-user segment is expanding most quickly?

Universities and hospitals lead growth, advancing at a 12.5% CAGR as they embed multispace kiosks into patient- and student-experience upgrades.

Page last updated on: