Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

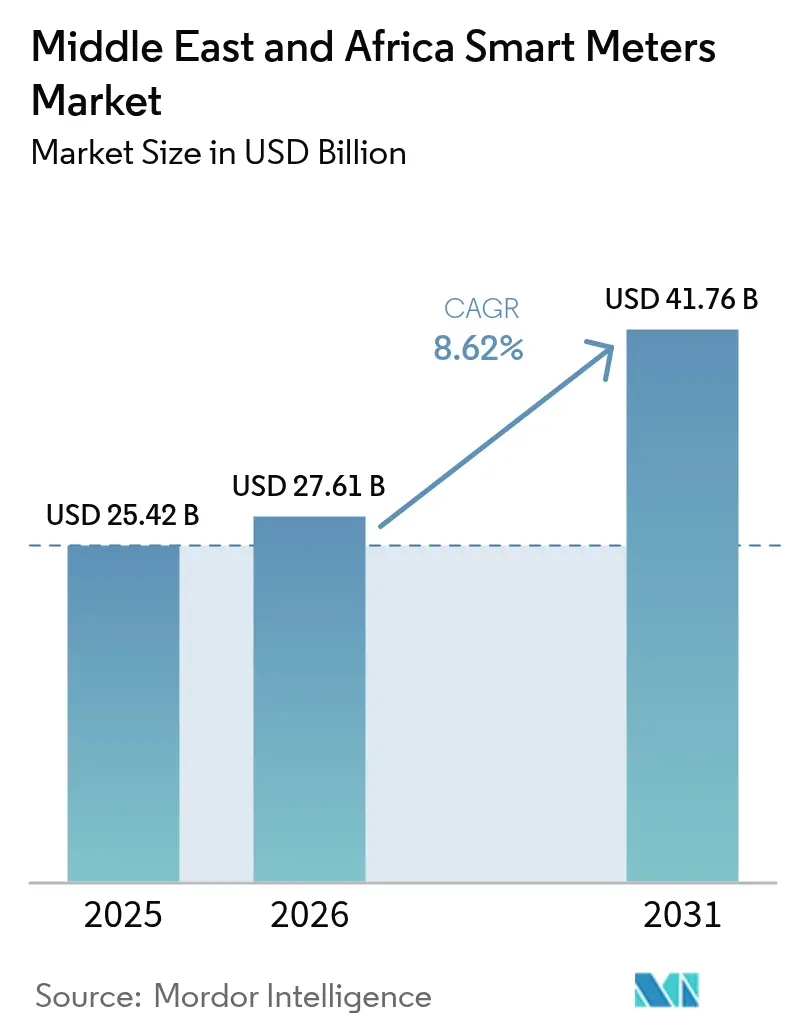

| Base Year Market Size (2025) | USD 25.42 Billion |

| Market Size (2026) | USD 27.61 Billion |

| Market Size (2031) | USD 41.76 Billion |

| Growth Rate (2026 - 2031) | 8.62% CAGR |

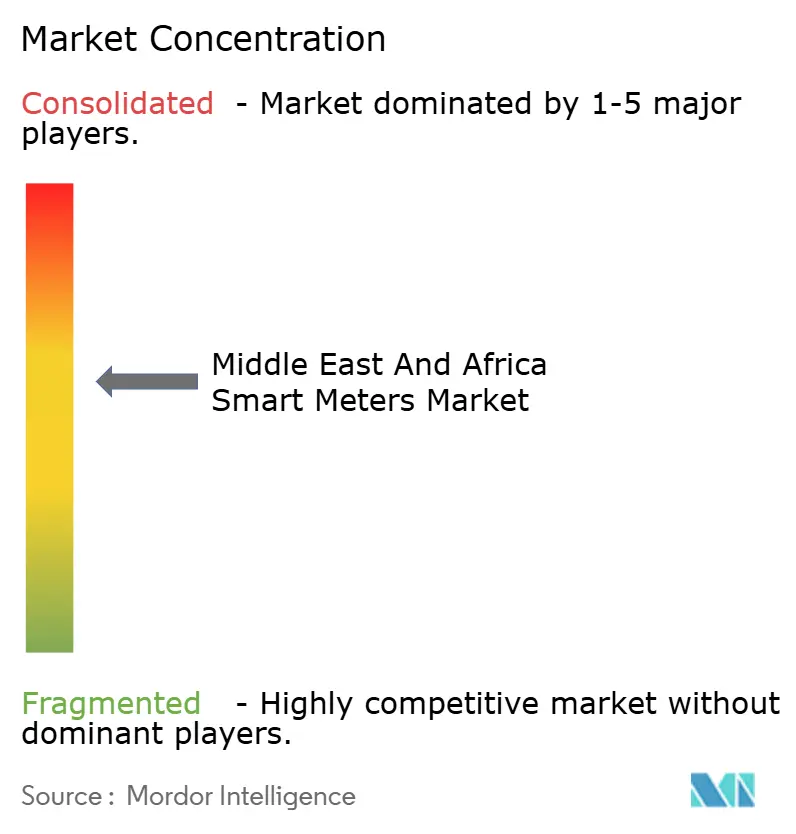

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Middle East And Africa Smart Meters Market Analysis by Mordor Intelligence

The Middle East and Africa smart meters market size is expected to grow from USD 25.42 billion in 2025 to USD 27.61 billion in 2026 and is forecast to reach USD 41.76 billion by 2031 at 8.62% CAGR over 2026-2031. Accelerated modernization programs that target aggregate technical and commercial losses, such as Dubai Electricity and Water Authority’s USD 1.9 billion smart-grid upgrade, continue to funnel large capital allocations into new deployments.[1]SaudiGulf Projects, “Dubai implementing smart grid project worth USD 1.9 billion,” saudigulfprojects.com Government mandates in the Gulf Cooperation Council (GCC) and South Africa embed smart-meter rollouts into utility compliance plans, while industrial customers adopt advanced metering faster to support manufacturing expansion and renewable-generation integration.[2]International Trade Administration, “UAE Renewable and Clean Energy Outlook,” trade.gov Desalination costs and water-scarcity pressures raise the profile of smart water-meter projects, and 5G availability lifts interest in cellular communications that complement incumbent RF mesh networks. Competitive intensity rises as local manufacturing gains momentum under harmonized Gulf standards that reduce certification complexity for new entrants.

Key Report Takeaways

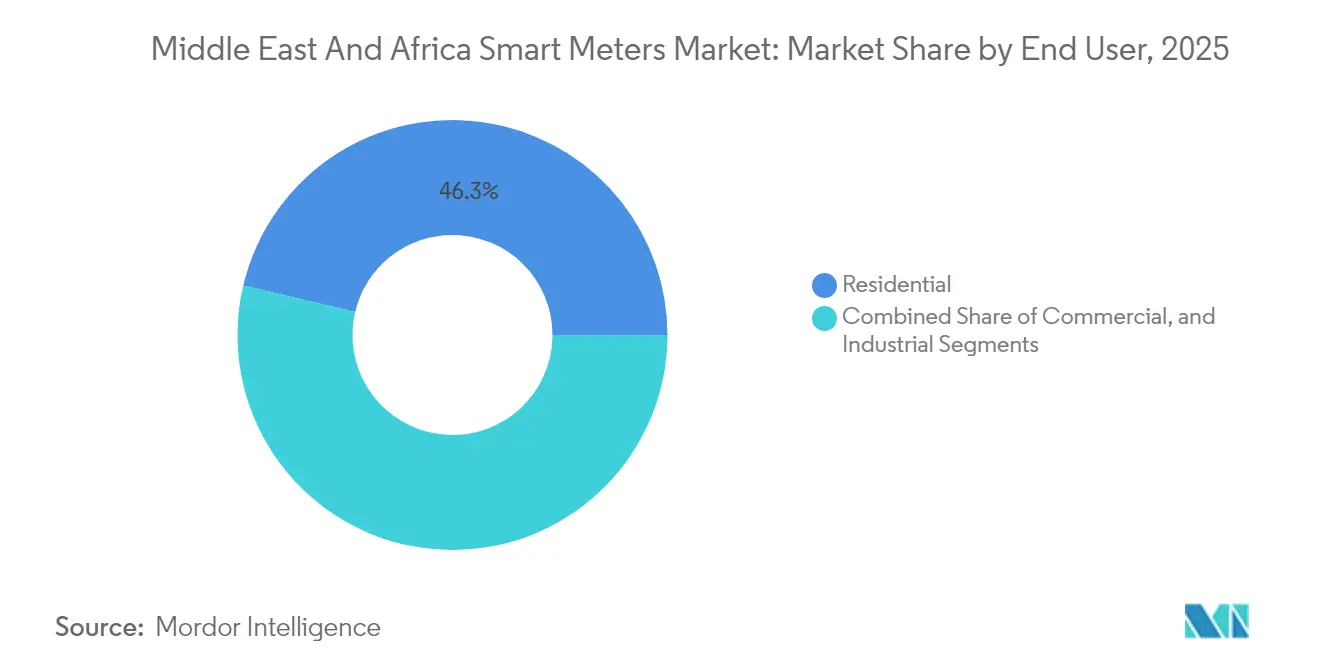

- By end user, residential accounted for 46.31% revenue share in 2025, while industrial is projected to expand at a 12.22% CAGR through 2031.

- By meter type, smart electricity devices held 60.85% of Middle East and Africa smart meters market share in 2025; smart water meters are forecast to grow at a 10.35% CAGR to 2031, contributing materially to Middle East and Africa smart meters market size expansion.

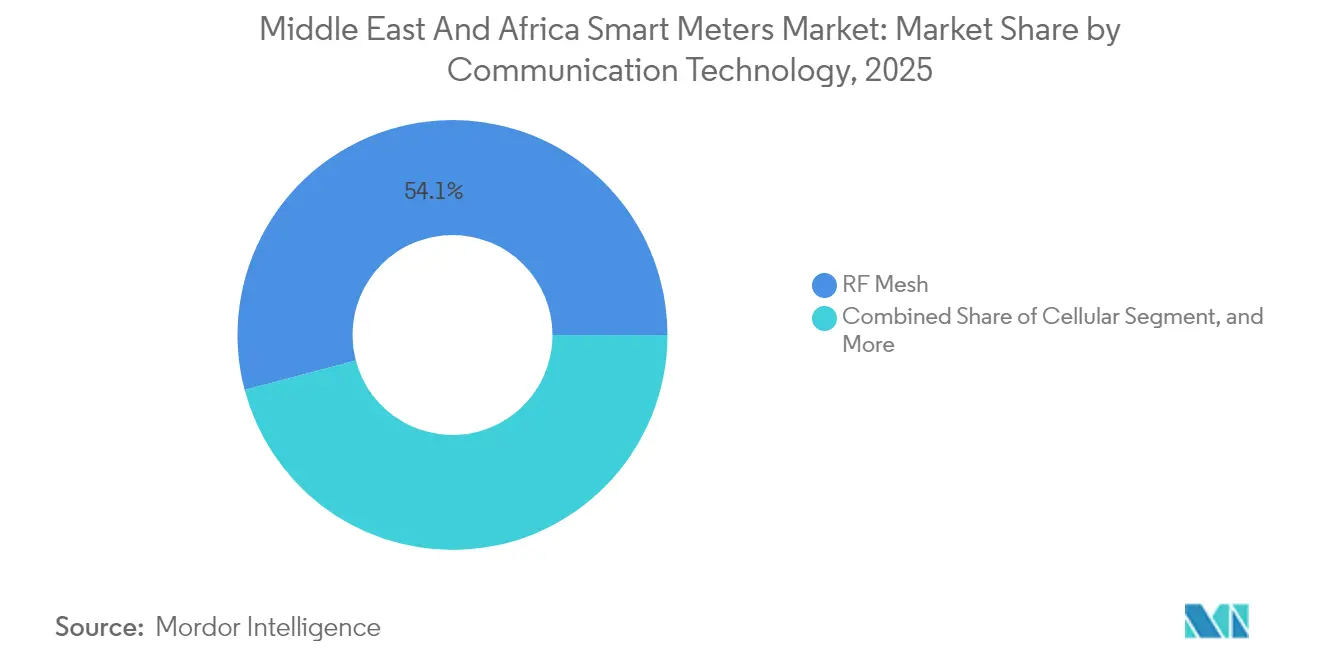

- By communication technology, RF mesh led with 54.12% share in 2025, whereas cellular networks are expected to post an 10.84% CAGR through 2031.

- By phase, single-phase units captured 63.15% market share in 2025, while three-phase systems are on track to increase at an 11.21% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East And Africa Smart Meters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid utility push for energy efficiency to reduce AT and C losses | +2.10% | Global MEA, with highest impact in Nigeria, South Africa, Egypt | Short term (≤ 2 years) |

| Government mandates and incentives for smart meter rollouts | +1.80% | GCC states, South Africa, Egypt, Morocco | Medium term (2-4 years) |

| Smart city and IoT infrastructure investments | +1.50% | UAE, Saudi Arabia, Qatar, South Africa | Medium term (2-4 years) |

| Rising demand for precise billing and customer engagement tools | +1.30% | Urban centers across MEA, particularly Dubai, Riyadh, Cape Town | Short term (≤ 2 years) |

| Surge in distributed solar rooftop connections necessitating bi-directional metering | +1.00% | GCC states, Jordan, Lebanon, South Africa | Long term (≥ 4 years) |

| Desalination plant electrification driving water meter digitization | +0.70% | GCC states, North Africa coastal regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid utility push for energy efficiency to reduce AT and C losses

Utilities across the Middle East and Africa lose 15-25% of supplied electricity to technical and commercial inefficiencies, an unacceptable revenue drain that elevates smart-meter programs to strategic priority. Nigeria’s distribution companies launched a 1.4-million-meter initiative in 2024 to target theft hotspots, while Zimbabwe accelerated its own installations to tighten billing accuracy.[3]Utilities Middle East, “Zimbabwe, Nigeria utilities ramp up smart-meter rollouts,” utilities-me.com In parallel, Gulf efficiency-label regulations demand granular consumption evidence, so utilities increasingly treat smart-meter data as the compliance backbone.[4]Dubai Electricity and Water Authority, “Energy Efficient Appliances Campaign,” dewa.gov.ae The resulting procurement surge enlarges the Middle East and Africa smart meters market, encourages multi-vendor tenders, and positions analytics services as high-value add-ons. Utilities that quantify loss reductions faster secure tariff-review advantages, amplifying first-mover benefits across the region.

Government mandates and incentives for smart-meter rollouts

Regulatory shifts from voluntary to mandatory deployments create a powerful demand floor. South Africa’s National Regulatory System 049:2016 sets advanced-metering specifications, and Cape Town now requires smart meters in new buildings. The Gulf Cooperation Council’s G-Mark certification aligns multi-country technical standards, slashing vendor compliance costs and accelerating shipments. Egypt’s refreshed IoT framework clears cellular-meter ambiguity, a previous bottleneck. As mandates widen, the Middle East and Africa smart meters market gains predictability that helps financiers back long-term rollouts, even in utilities with constrained balance sheets. Subsidy schemes covering up-front device costs further widen the addressable customer base.

Smart city and IoT infrastructure investments

Mega-projects such as Dubai’s USD 1.9 billion smart-grid plan weave metering into citywide platforms for real-time infrastructure management. The UAE’s Energy Strategy 2050, targeting 44% clean energy, relies on distributed-generation data streams that only advanced meters can provide. Saudi Arabia’s NEOM integrates smart-water networks at blueprint stage, turning meter connectivity into construction norm. These headline programs draw suppliers into long-term service arrangements and raise performance benchmarks that spill into neighbouring markets. Consequently, the Middle East and Africa smart meters market benefits from economies of scale in hardware production and cloud-platform licensing.

Rising demand for precise billing and customer-engagement tools

Consumers seek transparent invoices and usage analytics, pushing utilities toward meters that deliver real-time data. TAQA Distribution’s tie-in with Abu Dhabi Global Market to automate tenancy-fee billing demonstrates value-added monetization avenues. Similar apps elsewhere provide time-of-use pricing and automated bill alerts, increasing payment compliance. Utilities that deploy such features reduce receivables days and justify higher capital outlays, reinforcing demand within the Middle East and Africa smart meters market. As feedback loops shape consumption behaviour, demand-response programs gain traction, supporting grid-stability objectives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront device and installation costs | -1.40% | Sub-Saharan Africa, smaller GCC utilities | Short term (≤ 2 years) |

| Limited utility CAPEX and financing constraints | -1.10% | Nigeria, Kenya, Ghana, smaller regional utilities | Medium term (2-4 years) |

| Cybersecurity skill gap within regional utilities | -0.80% | Global MEA, particularly acute in Sub-Saharan Africa | Medium term (2-4 years) |

| Interoperability challenges between legacy AMR and new AMI architectures | -0.60% | Utilities with existing AMR infrastructure across MEA | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High upfront device and installation costs

Smart-meter hardware ranges from USD 50-150 per unit, and installation adds labour plus communication-network expenses. Sub-Saharan African utilities, often operating under currency volatility, face additional import-price swings that strain budgets. Lack of large-volume purchase power weakens their bargaining position relative to GCC peers. Certification fees from the Standard Transfer Specification Association raise compliance overheads for pre-paid solutions. Although donor-finance programs exist, disbursement timelines rarely align with meter-replacement cycles, prolonging reliance on legacy equipment and constraining the Middle East and Africa smart meters market in low-income regions.

Limited utility CAPEX and financing constraints

Balance-sheet pressures persist where tariff levels remain politically capped. Nigerian distribution firms and several East-African utilities struggle to secure commercial loans at acceptable rates. Concessionary funding from multilateral agencies covers pilot projects but seldom full fleet replacements. Consequently, tender sizes fragment, diluting economies of scale and prolonging deployment schedules, which drags on the overall growth trajectory of the Middle East and Africa smart meters market. Vendor-financed delivery models emerge, yet credit-risk premiums flow into end-user tariffs, exposing utilities to social-acceptance hurdles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User: Industrial Segment Drives Electrification Wave

Industrial applications accounted for 12.22% CAGR growth potential, signalling the segment’s role as the fastest-expanding component of the Middle East and Africa smart meters market size between 2026 and 2031. Industrial facilities including desalination plants, mines, and fast-growing manufacturing hubs in Saudi Arabia and the UAE require granular energy data to optimize production processes and integrate on-site renewables. These requirements stimulate demand for three-phase bi-directional meters capable of power-quality analytics, pushing average selling prices above the residential range and boosting overall revenue contribution. Vision 2030 agendas across Gulf economies strengthen the order pipeline as utilities partner with industrial-estate developers to pre-install smart-meter infrastructure.

Residential deployments, holding a 46.31% share in 2025, remain core to volume shipments within the Middle East and Africa smart meters market. Mandated rollouts in Cape Town and GCC states, coupled with consumer demand for transparent billing, sustain steady unit growth. Affordability concerns in lower-income markets, however, temper residential conversion rates, prompting suppliers to introduce stripped-down prepaid variants. Commercial buildings sit between the two extremes, leveraging meters for demand-response participation and energy-efficiency certification. Together, the three user categories form a diversified demand canvas that insulates the overall market from cyclical stocks in any single sector.

By Meter Type: Water Digitization Accelerates Infrastructure Modernization

Smart electricity meters commanded 60.85% of Middle East and Africa smart meters market share in 2025, reinforcing electricity’s primacy in regional utility operations. They serve as the technological baseline and often anchor multi-utility platforms. Yet, smart water meters, forecast to post a 10.35% CAGR through 2031, gain momentum as desalination reliance and non-revenue water issues intensify financial pressures on water utilities. Ultrasonic and electromagnetic models that withstand harsh saline environments register robust bid volumes, especially in Oman and Israel.

Gas-meter adoption stays niche because pipeline infrastructure remains limited outside metropolitan pockets. Nevertheless, integrated electricity-water-gas platforms lower lifetime IT costs and make multi-commodity rollouts more attractive. The Middle East and Africa smart meters market size for water applications, while smaller today, exhibits the steepest trajectory, drawing specialized vendors into joint ventures with regional system integrators. Electricity-meter demand continues unabated due to ongoing grid-modernization mandates, but competitive margins narrow as hardware commoditizes, and value migrates to software analytics.

By Communication Technology: Cellular Networks Challenge RF Mesh Dominance

RF mesh solutions captured 54.12% share in 2025, benefitting from proven reliability in dense urban grids and lower per-node costs. Utilities appreciate self-healing capabilities and controllable quality-of-service parameters. However, cellular-enabled meters are projected to grow at an 10.84% CAGR, outpacing other technologies and reflecting expanding 4G/5G footprints across Africa and the Middle East. Wide-area coverage and built-in cybersecurity features appeal to utilities seeking rapid deployments without investing in private backhaul networks.

Power-line communication (PLC) holds a steady foothold where electrical conditions permit clean signal propagation. Emerging narrowband PLC standards like G3-PLC promise interference resilience, yet field conditions in mining belts and older neighbourhoods still challenge adoption. Hybrid communication architectures increasingly appear in tenders as utilities adopt technology-agnostic procurement to future-proof investments. This trend enlarges the addressable market for service-layer providers specializing in protocol translation and network-monitoring dashboards, further enriching the competitive tapestry within the Middle East and Africa smart meters market.

By Phase: Three-Phase Growth Reflects Industrial Expansion

Single-phase meters dominate shipments, accounting for 63.15% market share in 2025 on the back of vast residential and small-commercial customer bases. They remain essential to rapid electrification drives and prepaid rollouts in Sub-Saharan Africa. Three-phase systems, forecast to advance at an 11.21% CAGR, capture the industrial and large-commercial opportunity set intertwined with regional manufacturing ambitions and high-capacity rooftop-solar installations.

Large-scale projects such as TrinaTracker’s 3 GW Saudi manufacturing plant demand robust three-phase monitoring to manage production loads and renewable-integration quality. Harmonized low-voltage regulations issued by the Gulf Standardization Organization simplify cross-border product approval, enabling bulk procurement synergies for multinational corporations. The resulting scale reduces average three-phase meter costs, narrowing the price gap with single-phase devices and propelling faster adoption. Consequently, the Middle East and Africa smart meters market anticipates a gradual shift in revenue mix toward higher-value three-phase hardware and associated analytics services.

Geography Analysis

Gulf states lead regional adoption curves, propelled by sovereign investment and policy alignment. Saudi Arabia’s NEOM and Saudi Green Initiative coalesce around digital-meter rollouts to orchestrate distributed-generation participation and real-time demand shaping. The UAE’s USD 1.9 billion smart-grid spend cements Dubai as an innovation hub, while Qatar scales smart-meter penetration to support expanded LNG-processing complexes, each requiring precise electricity and water accounting. Collective standardization under G-Mark and GSO guidelines reduces time-to-market for new devices, creating a cohesive procurement corridor that buoys the Middle East and Africa smart meters market.

Africa presents a patchwork of progress. South Africa’s compliance-driven mandates push ahead, with Johannesburg and Cape Town stipulating smart-meter fit-outs for new developments. Nigeria’s 1.4-million-meter initiative is the continent’s largest by volume yet financing constraints slow full fleet conversion. Egypt stands out for leveraging its strategic manufacturing base to attract meter producers, serving both domestic and export customers. Kenya, Ghana, and Morocco nurture pilot projects through international partnerships, positioning themselves as next-wave hotspots. Standard Transfer Specification Association certification offers technical cohesion for prepaid models, but uneven regulatory enforcement tempers speed. Aggregated gains from high-population African markets nonetheless furnish meaningful volume to the Middle East and Africa smart meters market.

Smaller territories such as Jordan, Lebanon, Ethiopia, and Tanzania explore niche bi-directional solutions tied to distributed-solar policies. Execution speed hinges on donor funding and workforce readiness. Israel, already advanced, shifts focus to nationwide smart-water coverage, setting performance benchmarks for precision and leak detection. Islands and micro-grids adopt pay-as-you-go meters to minimize cash-collection losses, illustrating the versatility of smart-meter business models. Collectively, these diverse geographic dynamics underpin a resilient growth outlook for the Middle East and Africa smart meters market by distributing demand across varied regulatory and economic cycles.

Competitive Landscape

The Middle East and Africa smart meters market exhibits moderate fragmentation: no single player dominates, but European incumbents such as Landis+Gyr and Kamstrup still secure large framework contracts thanks to deep DLMS/COSEM portfolios. Asian manufacturers leverage cost advantages and increasingly localize assembly CHINT’s Kenyan factory is emblematic allowing competitive pricing without breaching Gulf certification rules. Local system integrators act as channel partners, bundling software and field-services to bridge utilities’ skill gaps, thus playing an outsized role in vendor selection.

Strategic partnerships proliferate. e& enterprise’s five-year managed-services deal with Etihad Water and Electricity highlights rising appetite for outsourced data-management models. Meters now ship with cloud dashboards and AI-driven analytics, capabilities that differentiate suppliers in tender technical-evaluation scoring. Vendors offering end-to-end cybersecurity suites gain favour as utilities confront skill shortages. Meanwhile, emerging water-meter specialists target desalination-centric GCC utilities, creating room for niche leaders in subsegments of the Middle East and Africa smart meters market.

Price competition intensifies on commodity single-phase hardware, pushing manufacturers to chase margin in software subscriptions and maintenance contracts. Certification bodies enforce strict accuracy and interoperability standards, effectively filtering out low-quality entrants. As standardization tightens, competition shifts from hardware feature counts to lifetime-operating-cost arguments. The combined share of the top five suppliers aggregates at roughly 55%, indicative of a market concentration score of 5, signalling balanced rivalry and avenues for new entrants.

Middle East And Africa Smart Meters Industry Leaders

Landis+Gyr Group AG

Kamstrup A/S

Itron Inc.

Iskraemeco d.d.

Elektromed (Termikel Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: TrinaTracker opened a 3 GW tracker and control-system plant in Saudi Arabia, accelerating regional renewables supply chains.

- January 2025: Dubai Electricity and Water Authority rolled out a USD 1.9 billion smart-grid program covering advanced metering infrastructure and distribution automation.

- December 2024: Kaynes Technology acquired Iskraemeco India for INR 430 million (USD 51.6 million) to expand smart-meter production capacity.

- October 2024: Nama Water Services completed 400,000 digital water-meter installations across Oman.

Middle East And Africa Smart Meters Market Report Scope

A smart meter is an electronic gadget that records electric energy consumption and communicates the data to the electricity supplier for monitoring and billing. Intelligent meters generally register energy hourly or more often and report at least daily. The Middle East and Africa smart meters market is segmented by end-user (residential, commercial, industrial) and type (smart electricity meters, smart gas meters, and smart water meters in different regions).

The impact of COVID-19 on the market and impacted segments are also covered under the scope of the study. Furthermore, the disruption of the factors affecting the market's expansion in the near future has been covered in the study regarding drivers and restraints.

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By End User

| Residential |

| Commercial |

| Industrial |

By Meter Type

| Smart Electricity Meters |

| Smart Gas Meters |

| Smart Water Meters |

By Communication Technology

| RF Mesh |

| Power Line Communication |

| Cellular |

By Phase

| Single-Phase |

| Three-Phase |

By Geography

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Kuwait | |

| Oman | |

| Bahrain | |

| Turkey | |

| Israel | |

| Jordan | |

| Lebanon | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Kenya | |

| Morocco | |

| Algeria | |

| Ghana | |

| Ethiopia | |

| Tanzania |

| By End User | Residential | |

| Commercial | ||

| Industrial | ||

| By Meter Type | Smart Electricity Meters | |

| Smart Gas Meters | ||

| Smart Water Meters | ||

| By Communication Technology | RF Mesh | |

| Power Line Communication | ||

| Cellular | ||

| By Phase | Single-Phase | |

| Three-Phase | ||

| By Geography | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Oman | ||

| Bahrain | ||

| Turkey | ||

| Israel | ||

| Jordan | ||

| Lebanon | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Kenya | ||

| Morocco | ||

| Algeria | ||

| Ghana | ||

| Ethiopia | ||

| Tanzania | ||

Key Questions Answered in the Report

What is the current valuation of the Middle East and Africa smart meters market?

The market stands at USD 27.61 billion in 2026 and is forecast to grow to USD 41.76 billion by 2031.

Which end-user segment is growing fastest?

Industrial installations, driven by manufacturing expansion and renewable integration, are projected to register a 12.22% CAGR through 2031.

Why are utilities shifting toward cellular communication for meters?

Expanding 4G/5G coverage offers wide-area connectivity without dedicated backhaul, supporting an 10.84% CAGR for cellular-enabled meters.

How significant are water-meter projects in GCC countries?

Smart water meters are the fastest-growing meter type at a 10.35% CAGR, propelled by desalination costs and water-scarcity concerns.

Which technology standards help streamline cross-border deployments?

The Gulf Cooperation Council's G-Mark and Gulf Standardization Organization regulations provide unified certification pathways that shorten time-to-market.

What inhibits faster smart-meter adoption in Sub-Saharan Africa?

High up-front costs, limited utility CAPEX, and cybersecurity skill gaps restrict large-scale rollouts despite strong long-term demand drivers.

Page last updated on: