Smart Electricity Meter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

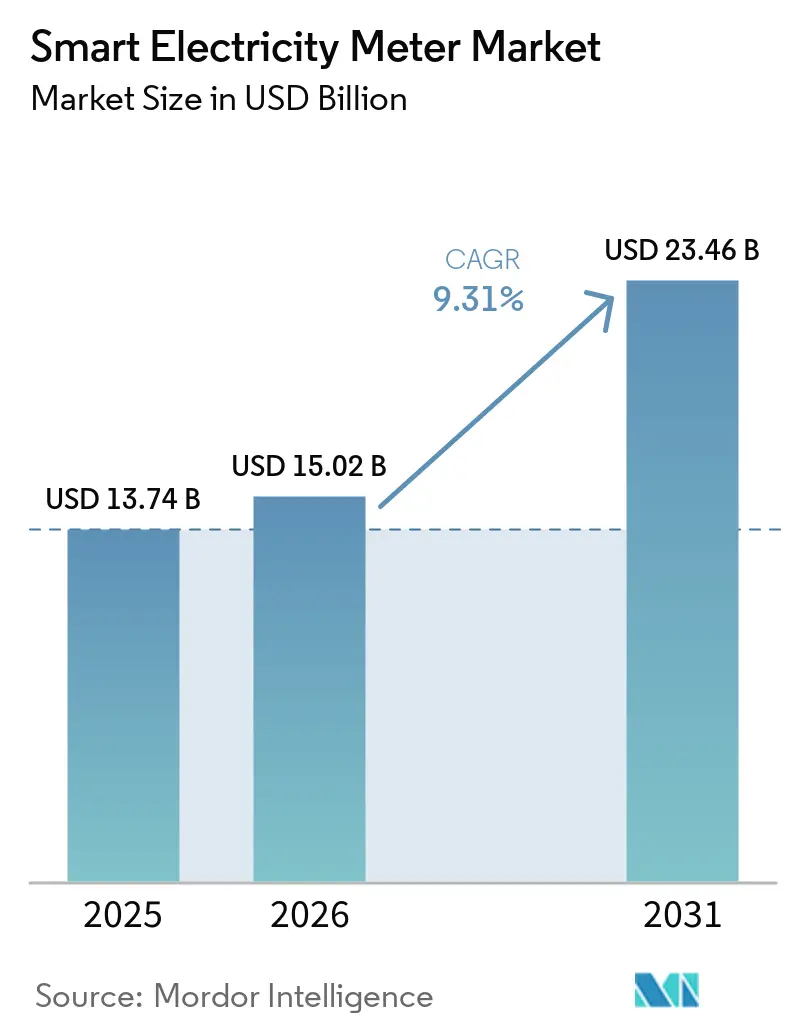

| Market Size (2026) | USD 15.02 Billion |

| Market Size (2031) | USD 23.46 Billion |

| Growth Rate (2026 - 2031) | 9.31% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Electricity Meter Market Analysis by Mordor Intelligence

Smart Electricity Meter Market size in 2026 is estimated at USD 15.02 billion, growing from 2025 value of USD 13.74 billion with 2031 projections showing USD 23.46 billion, growing at 9.31% CAGR over 2026-2031. The smart electricity meter market is advancing on the back of grid-modernization mandates, steep renewable-integration targets and a steady drop in connectivity costs. Utilities are reframing meters as grid-edge intelligence nodes that support outage management, power-quality analytics and distributed-energy-resource orchestration. Cellular and NB-IoT connectivity are breaking the cost–performance barrier once held by PLC, encouraging late-adopting utilities to leapfrog first-generation AMR systems. Meanwhile, component miniaturization and embedded AI are enabling high-resolution data capture, which supports flexible pricing programs and virtual power plants. Asia’s economies of scale continue to push average selling prices down, allowing smaller utilities in Latin America, Africa and Southeast Asia to unlock new deployment budgets.

Key Report Takeaways

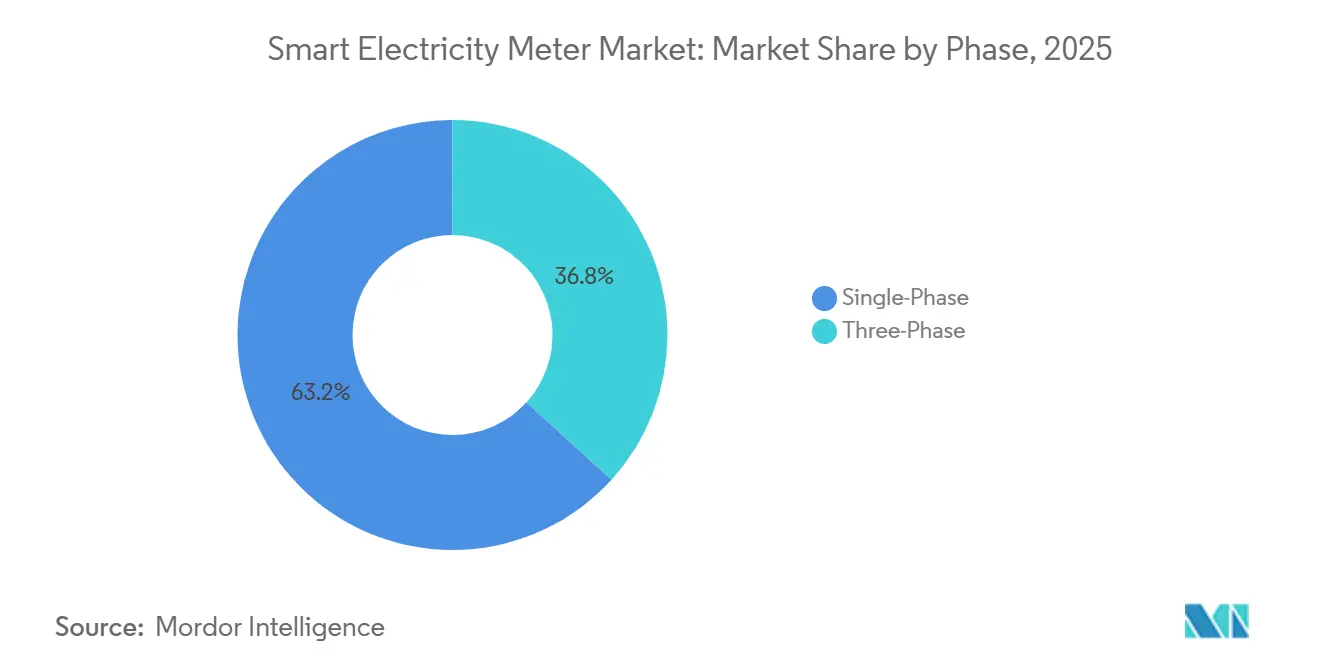

- By phase, single-phase meters led with a 63.25% revenue share in 2025; three-phase devices are projected to grow at a 9.05% CAGR through 2031.

- By communication technology, PLC held 44.10% of the smart electricity meter market share in 2025, while cellular/NB-IoT is forecast to post a 11.62% CAGR between 2026-2031.

- By technology, AMI is expected to dominate the smart electricity meter market with a 67.20% share of the market size in 2025, and is projected to advance at a 11.28% CAGR through 2031.

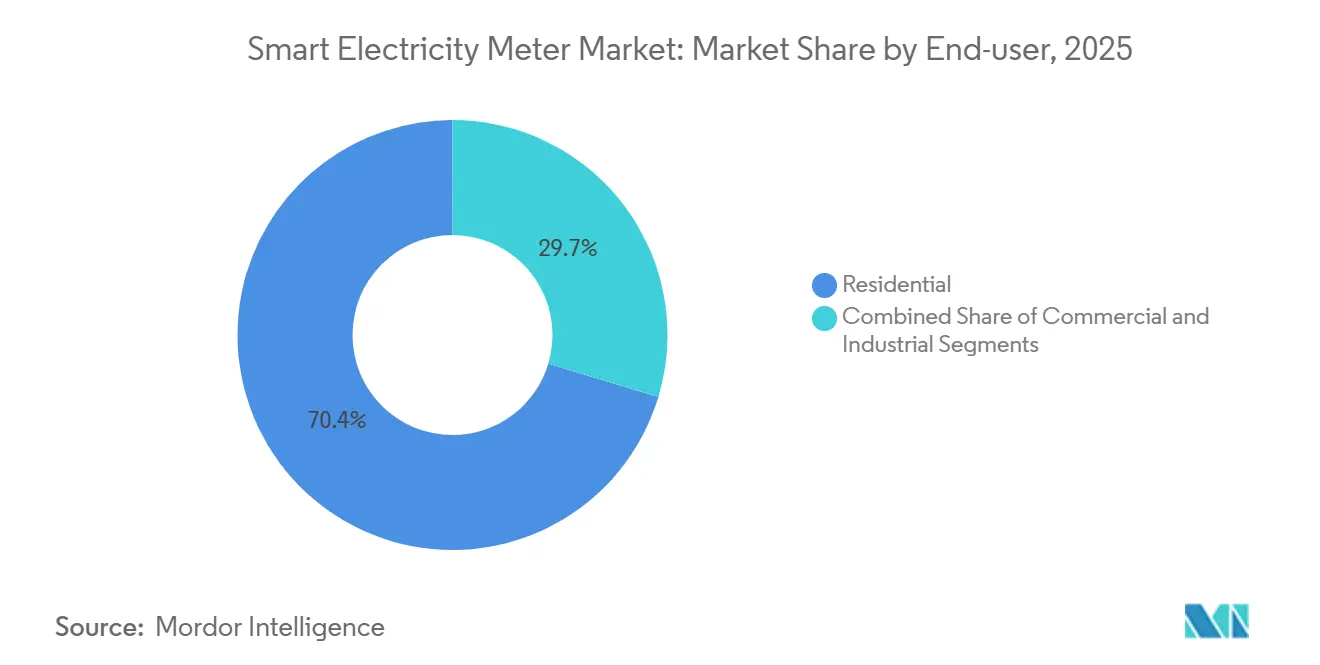

- By end-user, the residential segment accounted for 70.35% of 2025 revenues, while the industrial segment is expected to register a 9.88% CAGR from 2026 to 2031.

- By installation mode, new deployments accounted for 57.35% of shipments in 2025; retrofit projects are expected to grow at a 8.62% CAGR through 2031.

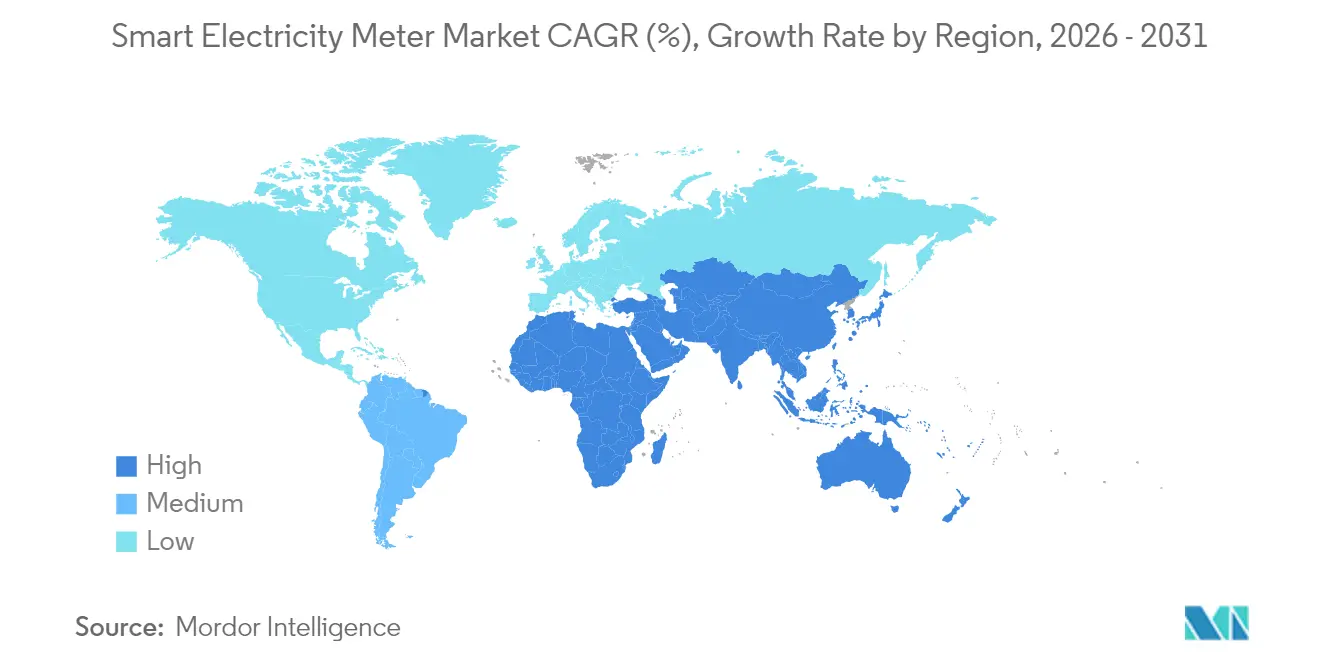

- By geography, the Asia Pacific held 47.55% of the smart electricity meter market share in 2025, while the Middle East is forecast to post a 10.18% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Electricity Meter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory EU-2025 three-phase replacement mandates | +2.50% | European Union, UK, Switzerland, Norway | Medium term (2–4 years) |

| China NB-IoT smart-meter mega-tenders | +2.20% | China, spillover in Southeast Asia | Short term (≤2 years) |

| U.S.–Japan demand-response AMI roll-outs | +1.80% | USA, Japan; influence on South Korea & Taiwan | Medium term (2–4 years) |

| Prosumer billing surge in Oceania | +1.50% | Australia, New Zealand; adoption in Western Europe | Medium term (2–4 years) |

| Grid-modernization stimulus in Southern Cone | +1.30% | Chile, Argentina, Brazil (spillover) | Medium term (2–4 years) |

| GCC time-of-use tariff introduction | +1.60% | Saudi Arabia, UAE, Oman; wider GCC | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Mandatory EU-2025 Three-Phase Replacement Mandates

Europe’s legally binding schedule to swap legacy three-phase meters forces utilities to replace millions of commercial and industrial units before 2027. Utilities are seizing the window to roll out AMI platforms that capture granular interval data and support sub-metering services. Meter vendors benefit from a higher average selling price, roughly triple that of single-phase units, while software providers gain recurring revenue through data-management contracts. Capital spending earmarked for compliance is also accelerating investment in data hubs that will underpin tariff innovation and demand-side flexibility programs.

China NB-IoT Smart-Meter Mega-Tenders

The State Grid Corporation’s 2025 tender for 6 million dual-mode NB-IoT meters cements cellular connectivity as a price-competitive option. Bulk procurement compresses component costs for global buyers and speeds certification cycles for modem vendors. The meters’ dual-band design future-proofs deployments against 2G sunsets, while cloud-native head-end systems streamline software upgrades. These operational gains resonate with Southeast Asian utilities that share similar urban density challenges, reinforcing China’s design template as a de-facto standard.

U.S.–Japan Demand-Response AMI Roll-Outs

North American and Japanese utilities are layering real-time price signals on second-generation AMI, steering large household appliances and EV chargers away from peak load. This shift shifts value toward meters capable of edge computing and rapid firmware updates. Vendors capture premium margins by bundling distributed-intelligence applications that unlock non-commodity revenues for utilities, such as grid-support services. The collaborative pilots now underway in South Korea and Taiwan rely heavily on lessons learned from the U.S.–Japan experience, propagating best practices across the Pacific.[1] Smart Energy International, “Japan Surpasses 100 Million Smart Meters,” smart-energy.com

Prosumer Billing Surge in Oceania

High rooftop solar penetration in Australia and New Zealand requires meters that can register inflows and outflows every few seconds. Regulatory bodies are nudging retailers toward cost-reflective tariffs, creating a commercial rationale for feature-rich meters. Successful rollouts are fueling Western Europe’s tariff-design debate, especially in markets with accelerating heat pump uptake. Vendors with strong phase-imbalance measurement capabilities and sub-second logging capabilities are well-positioned to capitalize on this opportunity.[2]Australian Energy Market Commission, “Smart Meter Plan 2030,” aemc.gov.au

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ASIC supply-chain shortages inflate BOM costs | -1.50% | Global; acute in North America & Europe | Short term (≤2 years) |

| UK CPA/EU RED cyber-certification delays | -1.20% | Europe; ripple effects in aligned markets | Medium term (2–4 years) |

| RF-emission pushback in France and Canada | -1.00% | France, Canada; influence on select EU markets | Medium term (2–4 years) |

| Legacy-SCADA incompatibility in Sub-Saharan utilities | -1.40% | Sub-Saharan Africa utilities and municipal networks | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

ASIC Supply-Chain Shortages Inflate BOM Costs

Persistent scarcity of specialized processors continues to lift meter manufacturing expenses by 15-25%. Smaller vendors are redesigning boards to use multi-purpose MCUs, extending validation cycles and inflating working capital. Several North American municipal utilities have postponed tranche-two deployments until 2027 in the hope that wafer fabs coming online in 2026 will relieve shortages. The squeeze is most acute for AMI meters that require cryptographic acceleration and edge-analytics cores

UK CPA/EU RED Cyber-Certification Delays

Europe’s evolving cybersecurity rulebook compels vendors to produce country-specific firmware and undergo extended lab testing. Lead times for Commercial Product Assurance (CPA) approval now exceed 14 months, disrupting tender award schedules. Utilities in Ireland and Scandinavia are inserting optional delays into framework contracts to hedge against further policy shifts. The extra compliance overhead is eroding profit margins for mid-tier suppliers and complicating multi-country product roadmaps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Phase: Industrial Three-Phase Momentum

Single-phase meters led with a 63.25% revenue share in 2025, whereas three-phase devices are projected to grow at a 9.05% CAGR through 2031. Utilities favor them for medium-voltage feeders, renewable inverters, and EV fast-chargers that demand harmonic-rich load profiling. In contrast, single-phase units, although still numerically dominant, are shifting toward replacement cycles driven by cybersecurity and firmware upgrade requirements. Field-proven accuracy in non-linear load environments has removed a historic adoption barrier for industrial automation users, boosting order backlogs among meter OEMs in Germany, Italy, and Poland.

The segment benefits from the EU mandate that forces advanced three-phase functions such as voltage sag logging and integrated disconnect relays. As a result, the smart electricity meter market is experiencing a clear shift in value towards higher-margin industrial contracts. Three-phase shipments command average selling prices roughly 2.8 times that of residential units, thereby enlarging the smart electricity meter market size for commercial and industrial applications. Vendors are bundling power-quality modules and carbon-intensity reporting to differentiate, and utilities are responding by launching subscription-based analytics that monetize the new data stream.

By Communication Technology: Cellular Connectivity Accelerates

Power-Line Communication (PLC) retained a 44.10% share in 2025, underpinned by deep penetration in Europe’s LV networks. Yet cellular NB-IoT and LTE-M modules are closing the cost gap and are on track for a 11.62% CAGR through 2031. Successful Chinese mega-tenders showcase deployment timelines that beat PLC by six months in dense urban corridors. The smart electricity meter market is shifting toward hybrid architectures, where RF mesh backhauls the outskirts while cellular technology covers high-rise clusters, ensuring contiguous coverage without the need for repeater farms.

eSIM adoption simplifies provisioning because utilities can switch carriers without truck rolls, cutting opex by up to 35%. Field trials in Brazil confirm that NB-IoT penetration into basements and meter rooms outperforms legacy mesh by 22 percentage points. The cellular uptrend expands the smart electricity meter market share of telecom-centric vendors that bundle managed connectivity with hardware. As roaming costs decline, African utilities are utilizing cross-border cellular agreements to standardize AMI formats, thereby reducing import duties associated with proprietary mesh radios.

By Technology: AMI as Grid-Intelligence Backbone

Advanced Metering Infrastructure accounted for 67.20% of 2025 revenue and is expected to post an 11.28% CAGR, lifting AMI revenue to a prominent level by 2031. The leap from first-generation AMR to bidirectional AMI 2.0 unlocks feeder-level loss detection, remote reconnect, and tariff switching in under 5 seconds. Edge AI on the meter now flags neutral faults and meter tamper events locally, reducing field visits by 18%. Landis+Gyr and Itron have shipped more than 13 million distributed-intelligence meters, cementing their lead in software-defined infrastructure.

AMR’s footprint is expected to shrink to 19% by 2031 as retrofit kits convert legacy registers into low-cost edge devices, thereby preserving sunk capital while layering AMI functions. The smart electricity meter market size for AMI is expanding fastest where regulators earmark stimulus for grid digitization, notably in Brazil’s Pro-Meter Program. Cloud-native head-end systems that scale elastically during billing cycles further enhance the economics, nudging cooperative utilities with tight budgets to adopt AMI deployments immediately.

By End-User: Industrial Uptake Gains Pace

Residential deployments remained the leading segment, accounting for 70.35% of 2025 shipments, reflecting nationwide rollouts in China, India, and the EU. Nonetheless, the industrial sub-segment is forecast to grow at a 9.88% CAGR as manufacturers prioritize power-quality visibility and carbon footprint audits. Time-of-use tariffs coupled with real-time consumption dashboards deliver direct production-cost savings, prompting large automotive plants in Mexico and Turkey to pilot meter-driven peak-shaving schemes.

Commercial properties such as retail chains and data centers are layering sub-metering on existing AMI to allocate internal costs accurately. This convergence of operational technology and IT services expands the market for smart electricity meters. As ESG reporting rules tighten, smart meters are evolving into energy- and carbon-data loggers, a feature driving an uptick in procurement tenders across Southeast Asian free-trade zones.

By Installation Mode: Retrofits Expand Addressable Base

New installations dominated the early adoption cycles of the smart electricity meter market by 57.35% in 2025, but retrofit and replacement projects are projected to rise at a 8.62% CAGR. Utilities with first-generation AMR fleets are opting for snap-on communication modules that enable firmware downloads and remote disconnect without swapping the entire meter enclosure. This approach lowers average upgrade cost by up to 60%, freeing budget for analytics software.

Consumer panels indicate that 62% of households prefer a non-invasive retrofit that preserves existing sockets, thereby accelerating acceptance in price-sensitive markets. Field pilots in South Africa have demonstrated that retrofitted meters reduce non-technical losses by 23% within 12 months. As retrofit economics mature, the smart electricity meter market experiences renewed growth pockets, even in territories with near-saturated penetration, extending vendor revenue cycles.

Geography Analysis

Asia Pacific held a revenue share of 47.55% in the smart electricity meter market in 2025 and contributed a significant share of global shipments in 2025, continuing to be the volume engine of the smart electricity meter market. China alone has deployed 590 million AMI endpoints across 26 provinces, giving local suppliers unrivaled scale advantages. India’s federal push toward 250 million prepaid smart meters by 2027 is spurring public-private joint ventures and unlocking third-party financing structures. High-density urban nodes in Japan and South Korea are rolling out AMI 2.0 to capture sub-second event data, thereby enhancing their power-quality oversight amid the surge in rooftop solar installations.

From 2026 to 2031, the Middle East's smart electricity meter market is set to grow at a robust rate of 10.18%. This surge is largely driven by utilities in the Gulf Cooperation Council (GCC) pushing for grid digitalization, implementing time-of-use tariffs, and emphasizing demand-side management. In countries such as Saudi Arabia, the UAE, and Oman, extensive rollouts of Advanced Metering Infrastructure (AMI) are enhancing billing precision and visibility during power outages. Additionally, the region's momentum is bolstered by a rising adoption of rooftop solar, updates in regulations, and ambitious efficiency targets.

North America achieved 77% penetration by 2024, with utilities now swapping first-wave AMI units for devices that integrate outage-detection algorithms and EV-load forecasting. The U.S. Department of Energy’s USD 10.5 billion grid-resilience grant scheme helps mid-size municipals justify upgrades that include meter-centric fault-isolation routines. The region’s insistence on open-standards such as Wi-SUN cultivates an ecosystem of interoperable software vendors, thereby increasing competitive tension and driving down lifecycle costs.

Europe’s policy-driven landscape stands out for its strict cybersecurity and data-privacy mandates. With 56% of customers already on smart meters by end-2022, the continent pivots toward harmonizing data access so that retailers can offer flexible tariffs across borders.A EUR 5 billion innovation fund aims for 90% coverage by 2027 and earmarks AI-enabled load forecasting as a critical deliverable. The mandatory three-phase replacement starting in 2025 is accelerating industrial uptake, especially in Germany, Spain and the Nordic bloc.

Competitive Landscape

The top five suppliers captured a significant share of shipments in 2024, reflecting moderate concentration. Landis+Gyr leads through aggressive R&D spend on distributed intelligence while Itron leverages a growing managed-services backlog. Sagemcom consolidates European share by pairing hardware with demand-response software, and Honeywell’s Elster line maintains a strong retrofit franchise. Regional specialists such as Wasion Group and Jiangsu Linyang succeed through cost-competitive designs tuned to domestic standards, narrowing price gaps with multinationals.

Strategic acquisitions illustrate a pivot toward recurring software revenues. Macquarie’s 2025 purchase of Iberdrola’s UK meter fleet grants long-term rental income and a platform for value-added services. Conlog’s partnership with Plentify targets Africa’s unique grid constraints by embedding load-control logic into prepaid meters. Tata Consultancy Services collaborates with Landis+Gyr to bundle analytics into utility cloud migrations, strengthening cross-sell potential.

Product roadmaps converge on AI-embedded silicon that performs on-meter anomaly detection, reducing data backhaul and latency. Cyber-hardening features compliant with EU RED and UK CPA are now baseline requirements for tenders. Vendors capable of shipping at scale while meeting divergent cybersecurity regimes hold a clear advantage. The rise of open-source head-end software is lowering entry barriers for integrators, injecting fresh competitive pressure into service contracts.

Smart Electricity Meter Industry Leaders

Landis+Gyr Group AG

Itron Inc.

Sagemcom SAS

Wasion Group Holdings

Sensus USA Inc. (Xylem Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Macquarie acquired Iberdrola’s UK smart-meter business for about GBP 900 million, adding 2.7 million endpoints and boosting its portfolio beyond 13 million meters Macquarie Group.

- May 2025: Conlog partnered with Plentify to deliver utility-grade home-energy management across African markets, integrating control algorithms into prepaid meters ESI Africa.

- December 2024: Tata Consultancy Services and Landis+Gyr began a three-year program to mesh TCS Clever Energy with Landis+Gyr’s AMI portfolio Tata Consultancy Services.

- December 2024: Intellihub and Smart launched a Home Energy Kit bundling solar, storage and optimization services for Australian households Intellihub.

Global Smart Electricity Meter Market Report Scope

The Smart Electricity Meter Market Report is Segmented by Phase (Single-Phase, and Three-Phase), Communication Technology (Power-Line Communication (PLC), Radio-Frequency Mesh, Cellular (NB-IoT / LTE-M), and Hybrid / Others), Technology (Advanced Metering Infrastructure (AMI), and Automatic Meter Reading (AMR)), End-user (Residential, Commercial, and Industrial), Installation Mode (New Installations, and Retrofits / Replacements), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Single-Phase |

| Three-Phase |

| Power-Line Communication (PLC) |

| Radio-Frequency Mesh |

| Cellular (NB-IoT / LTE-M) |

| Hybrid / Others |

| Advanced Metering Infrastructure (AMI) |

| Automatic Meter Reading (AMR) |

| Residential |

| Commercial |

| Industrial |

| New Installations |

| Retrofits / Replacements |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Chile | |

| Colombia | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Nordics | |

| Benelux | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia Pacific | |

| Middle East | GCC |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Phase | Single-Phase | |

| Three-Phase | ||

| By Communication Technology | Power-Line Communication (PLC) | |

| Radio-Frequency Mesh | ||

| Cellular (NB-IoT / LTE-M) | ||

| Hybrid / Others | ||

| By Technology | Advanced Metering Infrastructure (AMI) | |

| Automatic Meter Reading (AMR) | ||

| By End-user | Residential | |

| Commercial | ||

| Industrial | ||

| By Installation Mode | New Installations | |

| Retrofits / Replacements | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Nordics | ||

| Benelux | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia Pacific | ||

| Middle East | GCC | |

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the smart electricity meter market?

The smart electricity meter market size stands at USD 15.02 billion in 2026 and is projected to reach USD 23.46 billion by 2031.

Which phase segment is expanding fastest?

Three-phase meters are forecast to grow at a 9.05% CAGR from 2026-2031, outpacing single-phase units driven by Europe’s replacement mandate.

Why are utilities shifting toward cellular NB-IoT connectivity?

Declining module costs, wide coverage and simpler deployment make NB-IoT and LTE-M attractive, enabling 11.62% CAGR growth in the cellular segment.

How do ASIC shortages affect smart-meter rollouts?

Scarcity of specialized chips has lifted meter bills of materials by up to 25% and delayed several North American and European deployments.

Which region records the highest penetration rate?

Asia Pacific leads with 47.55% penetration in 2025, propelled by strong regulatory support and second-generation AMI upgrades.

Who are the leading companies in the industry?

Landis+Gyr, Itron, Sagemcom, Honeywell (Elster), Wasion Group and Jiangsu Linyang are the principal players, together holding a significant share of global shipments.

Page last updated on: