Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

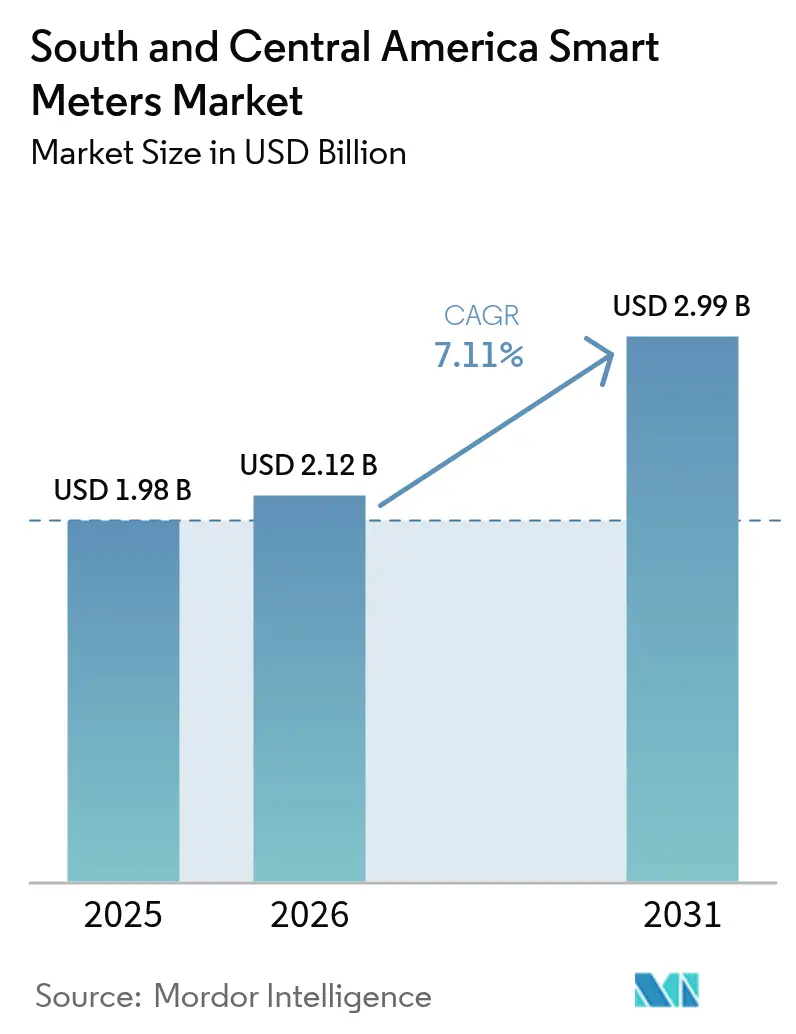

| Base Year Market Size (2025) | USD 1.98 Billion |

| Market Size (2026) | USD 2.12 Billion |

| Market Size (2031) | USD 2.99 Billion |

| Growth Rate (2026 - 2031) | 7.11% CAGR |

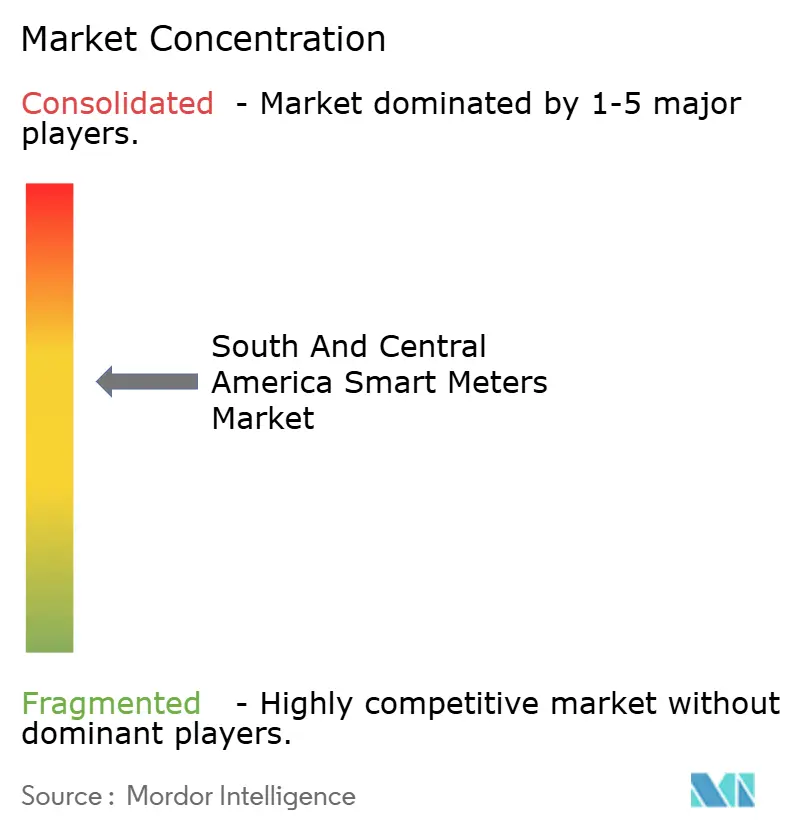

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South And Central America Smart Meters Market Analysis by Mordor Intelligence

South and Central America Smart Meters Market size in 2026 is estimated at USD 2.12 billion, growing from 2025 value of USD 1.98 billion with 2031 projections showing USD 2.99 billion, growing at 7.11% CAGR over 2026-2031. In terms of shipment volume, the market is expected to grow from 8.15 million units in 2025 to 11.67 million units by 2030, at a CAGR of 7.44% during the forecast period (2025-2030). Expansion is supported by utility digitalization mandates, widening rooftop solar adoption, and rising investments in advanced metering infrastructure that cut manual‐reading costs and tame commercial losses [1]Inter-American Development Bank, “From Structures to Services: The Path to Better Infrastructure in Latin America and the Caribbean,” IADB.org . Regional utilities are prioritizing two-way communication capabilities that enable bi-directional power flows and time-of-use billing, a shift that aligns with policy drives to integrate distributed energy resources and manage chronic water stress in Chile and Peru [2]World Bank, “Rethinking Infrastructure in Latin America and the Caribbean,” WorldBank.org . Accelerating LTE-M and NB-IoT rollouts by operators such as Movistar Empresas allows utilities to exploit managed cellular networks rather than maintain proprietary RF mesh backhaul, lowering lifetime connectivity costs. Parallel green-hydrogen pilots in Argentina and Chile are seeding demand for hydrogen-ready gas meters, expanding the addressable smart meters market into adjacent fuel-measurement domains. Finally, utility boards are widening cyber certification budgets to harden AMI head-end platforms against tampering that could expose sensitive customer data or disrupt billing operations [3]MDPI, “Survey of IoT for Developing Countries: Performance Analysis of LoRaWAN and Cellular NB-IoT Networks,” MDPI.com.

Key Report Takeaways

- By meter type, smart electricity meters captured 63.65% of the smart meters market share in 2025; smart water meters are advancing at a 9.22% CAGR through 2031.

- By communication technology, RF mesh commanded 47.88% of the smart meters market size in 2025, while cellular IoT is forecast to expand at 10.75% CAGR between 2026 and 2031.

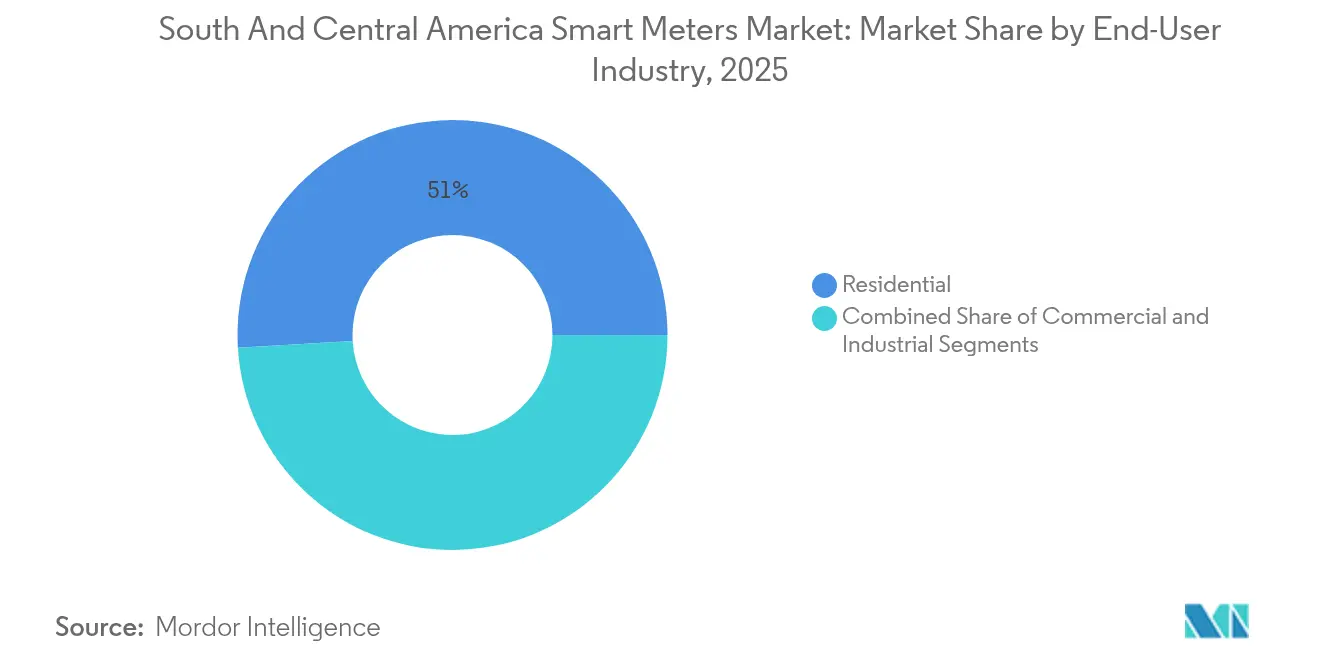

- By end-user industry, the residential segment held 50.95% of the smart meters market size in 2025; the industrial segment is growing at a 10.48% CAGR through 2031.

- By country, Brazil accounted for 37.95% of the smart meters market share in 2025; Colombia is on track for the fastest 12.38% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South And Central America Smart Meters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising investments in AMI-ready smart-grid projects | +1.1% | Brazil, Argentina, Chile, Colombia | Medium term (2-4 years) |

| National net-metering mandates and dynamic tariff programs | +0.9% | Brazil, Chile, Argentina | Short term (≤ 2 years) |

| Migration from electromechanical to smart pre-paid meters in low-income areas | +0.6% | Brazil, Colombia, Peru | Long term (≥ 4 years) |

| Utilities’ drive to curb non-technical losses | +0.8% | Regional focus on Brazil, Colombia | Medium term (2-4 years) |

| Green hydrogen pilots creating demand for advanced gas meters | +0.5% | Chile, Argentina, Brazil | Long term (≥ 4 years) |

| Real-time leakage analytics in drought-prone regions boosting smart-water roll-outs | +0.5% | Chile, Peru, northeastern Brazil | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Investments in AMI-Ready Smart-Grid Projects

Utilities are accelerating capital expenditure on modern AMI platforms to retire electromechanical meters, automate outage management, and support bi-directional power flows. Brazil’s Copel deployed 500,000 smart meters in 2024, reporting a 20% cut in truck rolls and a measurable drop in peak‐hour technical losses. Colombian and Chilean distribution firms are bundling AMI with feeder automation to maximize returns on network digitalization. Funding support from the Inter-American Development Bank eases debt burdens in high‐interest environments, enabling utilities to spread capex over longer tenors. Cellular NB-IoT connectivity is gaining ground because it leverages existing towers, avoiding the up-front civil works tied to pole-top RF mesh repeaters. Collectively, these moves enlarge the smart meters market by pulling forward procurement decisions that previously hinged on tariff-review cycles.

National Net-Metering Mandates and Dynamic Tariff Programs

Brazil’s ANEEL now obligates smart meters for every prosumer with >75 kW rooftop solar, a rule mirrored by ENRE in Argentina for self-managed distributed resources. Chile’s time-of-use tariff regime further demands 15-minute interval data to bill consumers fairly under dynamic pricing. These rules force utilities to swap legacy AMR devices for AMI units able to log import-export energy flows in real time. The design shift enlarges the smart meters market because installations cannot be deferred until assets reach the end of life; they are legal prerequisites for grid interconnection. As new rooftop arrays go online, meter upgrades occur concurrently, creating a demand flywheel that supports component localization and job creation inside national meter factories.

Migration from Electromechanical to Smart Pre-Paid Meters in Low-Income Areas

Government social-tariff schemes in Brazil and prepaid rollouts in Colombia’s stratum 1-2 neighborhoods are driving a wholesale switch from credit meters to prepaid smart devices that display live consumption alerts on in-home displays. The prepayment model curbs debt write-offs and allows utilities to fine-tune subsidy payouts by measuring actual kilowatt use instead of relying on monthly estimates. Cellular LTE-M modules dominate these deployments because RF mesh backhaul is sparse in informal settlements. Over the long term, prepaid smart meters nurture bill-payment discipline, reducing utility working-capital strain and enlarging the installed base that feeds future analytics and demand-response programs.

Utilities’ Drive to Curb Non-Technical Losses

Commercial losses from theft and bypass loops exceed 15% of dispatched energy in some South American networks. Smart meters equipped with tamper sensors generate exception alerts that trigger field inspections within hours rather than weeks. Brazilian studies show 8-12% shrinkage cut after AMI rollouts that overlay theft-detection algorithms on high-resolution load profiles. Theft reduction improves utility credit metrics, allowing them to refinance short-term debt at longer durations, thereby freeing balance-sheet space for additional AMI phases. The proven payback reinforces executive confidence and sustains the multi-year purchasing cycle that underpins the regional smart meters market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX and long pay-back periods | -1.4% | Regional, especially smaller utilities | Short term (≤ 2 years) |

| Cyber-security vulnerabilities in legacy AMI head-end systems | -0.9% | Brazil, Argentina, Chile | Medium term (2-4 years) |

| Patchy cellular IoT coverage outside tier-1 cities | -0.6% | Rural areas across region | Long term (≥ 4 years) |

| Delays in spectrum allocation for PLC/RF mesh backhaul | -0.5% | Colombia, Argentina, Peru | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX and Long Pay-Back Periods

A full AMI refresh can cost USD 150-300 per meter, saddling utilities with nine-figure program budgets that stretch internal debt capacity. Currency volatility further amplifies cost risk because most electronic components are sourced in USD yet billed in local pesos or reais. Smaller municipal distributors hesitate to proceed unless regulators grant accelerated cost recovery in tariff plans, delaying penetration in secondary cities. Development banks offer concessional loans, but disbursement milestones sometimes clash with political election cycles that stall board approvals. The resulting lag subdues near-term growth for the smart meters market, even though the long-term business case remains intact.

Cyber-Security Vulnerabilities in Legacy AMI Head-End Systems

Early-generation AMI head-end software often lacks secure key management and encrypted firmware-over-the-air updates, exposing utilities to ransomware or data exfiltration threats. After a 2024 cyber incident that briefly disrupted billing in Argentina, regulators now demand ISO 27001 compliance and regular penetration testing before utilities sign off on new meter lots. Vendors must harden endpoint firmware and retool manufacturing lines to inject unique keys at scale, raising cost and lengthening certification lead times. Heightened security obligations slow deployment schedules, trimming growth from the smart meters market over the next two to four years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Meter Type: Electricity Dominance amid Water Acceleration

Smart electricity meters accounted for a 63.65% smart meters market share in 2025, while smart water meters delivered the highest 9.22% CAGR outlook through 2031. The electricity segment benefits from a decade of AMR experience that simplifies procurement specifications and installer training. Utilities exploit voltage sag analytics and phase-imbalance alarms to cut technical loss plus improve power-quality reporting to regulators. Water utilities, especially in drought-stricken Chile and Peru, are fast-tracking ultrasonic meters fitted with acoustic leakage modules that immediately expose bursts and illegal taps. Because those utilities bill in local pesos but buy electronics in USD, meter suppliers increasingly locate assembly plants inside Mercosur zones to hedge forex swings. Smart gas meters form a nascent slice of the smart meters market size, but hydrogen-compatible variants now appear in pilot microgrids serving industrial clusters in Argentina’s Río Negro province.

The electricity segment’s maturity anchors vendor revenue, but hardware replacement cycles every 10-12 years open room for value-added upgrades such as edge AI anomaly detection and over-the-air tariff table pushes. In the water space, leak analytics slash non-revenue water from 45% to 30%, freeing operating cash that funds meter-as-a-service contracts. Although gas networks remain limited outside Argentina and Brazil, industrial customers that face ESG pressure are demanding transparent hydrogen flow measurement, attracting niche suppliers and prompting standards bodies to define hydrogen measuring protocols. These combined trends reinforce the widening breadth of the overarching smart meters market.

By Communication Technology: RF Mesh Leadership Challenged by Cellular Growth

RF mesh held 47.88% of the smart meters market size in 2025, but NB-IoT and LTE-M nodes are adding 10.75% CAGR through 2031. Mesh favors dense urban grids where pole heights and meter density guarantee line-of-sight links. Utilities retain full control of routing tables, a trait prized for mission-critical restoration messaging. Cellular connectivity eliminates the need for router-maintenance crews and extends reach into semi-rural zones lacking licensed spectrum for mesh backhaul. PLC remains limited because of conductor corrosion and signal attenuation on overloaded feeders in Peru’s mining belt, prompting regulators to de-prioritize PLC pilots.

The convergence of RF mesh and NB-IoT is emerging in hybrid architectures where meters auto-select the best path to the head-end, ensuring resilience during cellular outages or mesh node failures. These flexible topologies raise overall solution uptime to 99.8%, a metric now embedded in many utility service-level agreements. Module vendors are integrating secure elements that store credentials for both mesh and cellular stacks, streamlining logistics. As operators widen 700 MHz coverage, the incremental addressable base for cellular lifts the growth ceiling of the smart meters market while allowing utilities to tailor communication choices by geography and population density.

By End-User Industry: Residential Foundation with Industrial Momentum

The residential category delivered 50.95% of installations in 2025, supported by social tariff programs that require accurate consumption logs for subsidy targeting. Standardized meter form factors enable bulk procurement, and plug-and-play installation lowers person-hour costs. Commercial properties, however, face complex tariff tiers that necessitate class-320 current transformers and multi-load logging, therefore slowing widespread replacement. Industrial demand is rising at a 10.48% CAGR as miners and large manufacturers pursue ISO 50001 energy-management certification to satisfy investor ESG screens. Industrial meters capture sub-second load curves that feed predictive-maintenance algorithms, reducing unplanned downtime and payback times under three years.

In low-income neighborhoods, prepaid meters foster revenue assurance by automatically disconnecting when balances hit zero, which in turn reduces delinquency and thereby liberates cash flow for utility reinvestment in grid hardening. By contrast, industrial meters command ASPs that are three times higher than residential units, supporting vendor gross margins needed to subsidize R&D in hydrogen measurement. Looking forward, commercial buildings will see a moderate uptick as building-code overhauls in Colombia mandate energy intensity disclosure, pushing property owners to switch to smart submeters that can isolate HVAC consumption. These overlapping patterns across sectors deepen the resilience of the smart meters market against macroeconomic shocks.

Geography Analysis

Brazil generated 37.95% of the smart meters market revenue in 2025, leveraging ANEEL’s pro-digitalization rules that obligate AMI deployment for high-load customers and distributed generators. Utilities such as Elektro and Copel routinely bundle meter tenders with feeder automation, effectively stretching AMI capex across multiple asset classes to secure internal rate-of-return thresholds. Development bank lines denominated in USD further cut financing spreads, accelerating rollout velocity. Brazil’s semiconductor import exemptions also trim bill-of-materials cost, allowing meter vendors to achieve local-content targets without raising price tags.

Colombia is projected to record a 12.38% CAGR to 2031, the fastest in the region. The government auctioned 700 MHz spectrum for NB-IoT in 2024, after which utilities quickly signed managed-connectivity contracts that shave field maintenance costs compared with mesh repeaters mounted on concrete poles. The Bogotá metro expansion is also embedding real-time power monitoring, which calls for advanced meters in traction substations. Argentina and Chile maintain steady adoption anchored in renewable integration and acute water scarcity, respectively; both governments codify time-of-use billing that obliges interval metering. Currency fluctuations in Argentina remain a drag, but the green-hydrogen roadmap helps justify hydrogen-capable gas meter pilots funded via multilaterals.

The “Rest of South and Central America,” encompassing Peru, Uruguay, Panama, and others, shows diverse but positive trajectories. Peru’s urban water utilities confront 40% non-revenue water and thus prioritize ultrasonic meters with embedded acoustic sensors that localize leaks to ±5 feet. Uruguay’s investment-grade bond status attracts private operators willing to sign performance-based concessions that bundle leakage reduction with smart-meter rollout. Panama’s canal expansion increased national industrial load, pushing the grid operator to adopt AMI for feeder balancing. These varied national priorities underpin a multi-speed yet broadly upward outlook for the smart meters market.

Competitive Landscape

The regional smart meters market is moderately concentrated. Landis+Gyr, Itron, and Kamstrup collectively captured a significant share of revenue in 2024, leveraging local partnerships and multi-utility turnkey offerings. Landis+Gyr grows via meter-as-a-service contracts that convert capex to opex, a model attractive to cash-strapped distributors. Itron’s 1.5 million-meter contract at LUMA Energy in Puerto Rico demonstrates delivery capability in challenging post-storm environments, a credential advantageous when bidding in coastal Brazil. Kamstrup opened a 150,000 square-foot plant in Georgia in 2024, cutting lead times to South America to under four weeks while qualifying for Mercosur duty exemptions.

Second-tier European suppliers like Elster and Hexing pursue regional joint ventures that localize assembly and unlock public procurement set-asides, reserving 30% content for domestic manufacturers. Chinese firms retain footholds in price-sensitive water projects but face cybersecurity compliance headwinds as regulators enforce ISO 27001 and IEC 62443. Ecosystem differentiation is shifting from meter hardware to cloud analytics; vendors integrate AI-based load disaggregation that pinpoints clandestine crypto-mining, an emergent form of theft in urban Argentina. Cellular module partnerships are pivotal: u-blox and Quectel co-design NB-IoT boards with meter OEMs, ensuring certified over-the-air upgrades aligned with operator firmware cycles.

Services are gaining a share of the total contract value. Utilities sign ten-year managed connectivity deals that bundle SIM lifecycle management, cybersecurity patching, and tariff table updates. These recurring revenues smooth vendor cash flows, diluting reliance on one-off hardware margins. Compliance mandates for GDPR-like privacy rules in Brazil further lock in established suppliers that can demonstrate data residency and encryption audits, elevating entry barriers for new aspirants. Overall, vendor rivalry revolves around turnkey value rather than lowest initial bid, cushioning price erosion and helping sustain healthy operating margins across the smart meters market.

South And Central America Smart Meters Industry Leaders

Landis+Gyr Group AG

Itron Inc.

Honeywell International Inc.(Elster)

Kamstrup A/S

Sensus (Xylem Inc.)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: LUMA Energy selected Itron for a 1.5 million smart-meter rollout in Puerto Rico that includes grid analytics for fault location and restoration optimization.

- June 2024: Movistar Empresas activated LTE-M network services in Chile, tallying 1.5 million IoT connections that include utility smart meters, fleet trackers, and smart-city endpoints.

- March 2024: Kamstrup opened a 150,000 square-foot facility in Cumming, Georgia, with annual capacity of 3 million water meters, enabling tariff-free shipments into Mercosur while maintaining 0.25% return rates.

South And Central America Smart Meters Market Report Scope

A smart meter is an electronic machine that reads information such as the consumption of electric energy, current, voltage levels, and power factor. Smart meters transmit the information to the customer for greater accuracy of consumption behavior, and electricity suppliers for system monitoring and customer billing.

The different kinds of smart meters considered in the scope of this report are - smart gas meter, smart water meter, and smart electricity meter. The study also includes a categorization of the study of the applications of these meters for commercial, industrial, and residential purposes.

Smart gas and smart energy meters are deployed to measure the gas flow and electricity consumption, using wireless communication, thereby allowing infrastructural maintenance, remote location monitoring, and automatic billing.

A smart water meter uses wireless communication technologies to measure water flow in real-time, allowing remote location monitoring and infrastructural maintenance through leak detection.

By Meter Type

| Smart Electricity Meters |

| Smart Water Meters |

| Smart Gas Meters |

By Communication Technology

| RF Mesh |

| PLC |

| Cellular IoT (NB-IoT, LTE-M) |

By End-user Industry

| Residential |

| Commercial |

| Industrial |

By Country

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Rest of South and Central America |

| By Meter Type | Smart Electricity Meters |

| Smart Water Meters | |

| Smart Gas Meters | |

| By Communication Technology | RF Mesh |

| PLC | |

| Cellular IoT (NB-IoT, LTE-M) | |

| By End-user Industry | Residential |

| Commercial | |

| Industrial | |

| By Country | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South and Central America |

Key Questions Answered in the Report

How large is the smart meters market in South and Central America today?

The market is valued at USD 2.12 billion in 2026 and is forecast to reach USD 2.99 billion by 2031.

What CAGR is projected for smart-water meters in the region?

Smart-water meters are expected to grow at 9.22% CAGR to 2031, the fastest among all meter types.

Which communication technology is adding the most new connections?

Cellular IoT, particularly NB-IoT and LTE-M, is expanding at an 10.75% CAGR as operators extend coverage across urban and semi-rural zones.

Why is Colombia the fastest-growing national market?

Government spectrum allocations for NB-IoT and infrastructure investments support a 12.38% CAGR through 2031.

What major restraint could slow smart-meter deployment?

High upfront capex, USD 150–300 per meter, extends payback periods beyond 10 years for smaller utilities.

Which vendors currently dominate regional market share?

Landis+Gyr, Itron, and Kamstrup together account for roughly 42% of regional revenue.

Page last updated on: