Drone Camera Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

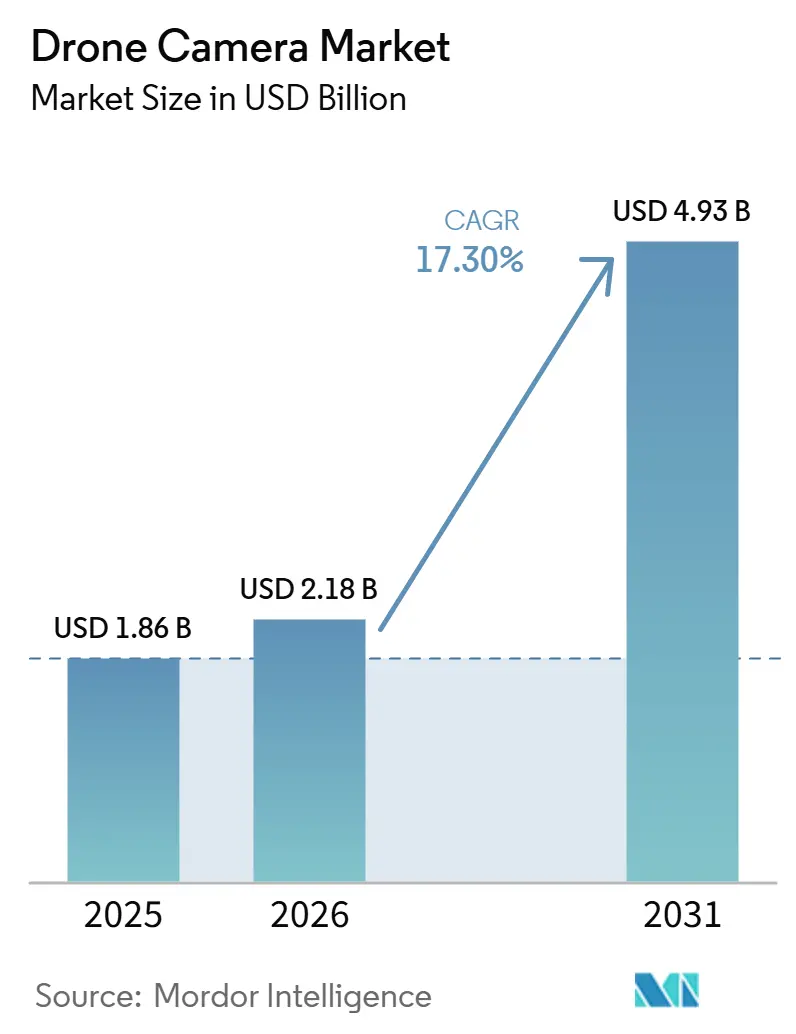

| Market Size (2026) | USD 2.18 Billion |

| Market Size (2031) | USD 4.93 Billion |

| Growth Rate (2026 - 2031) | 17.30% CAGR |

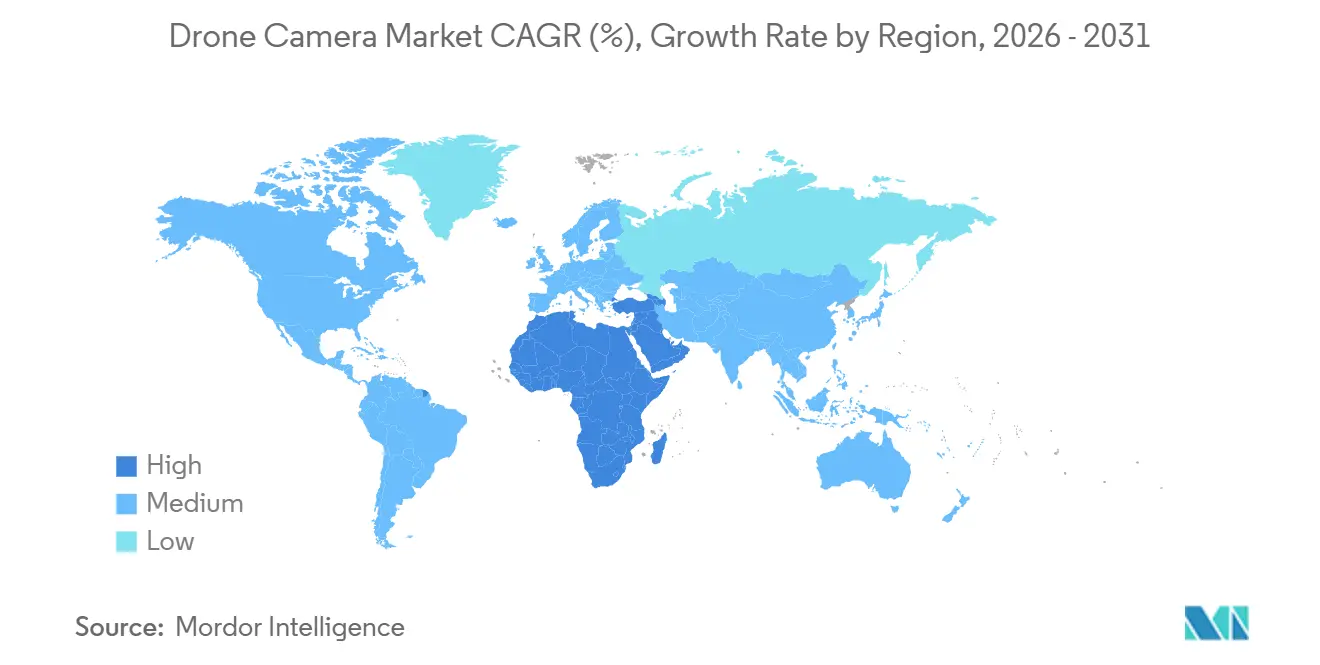

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

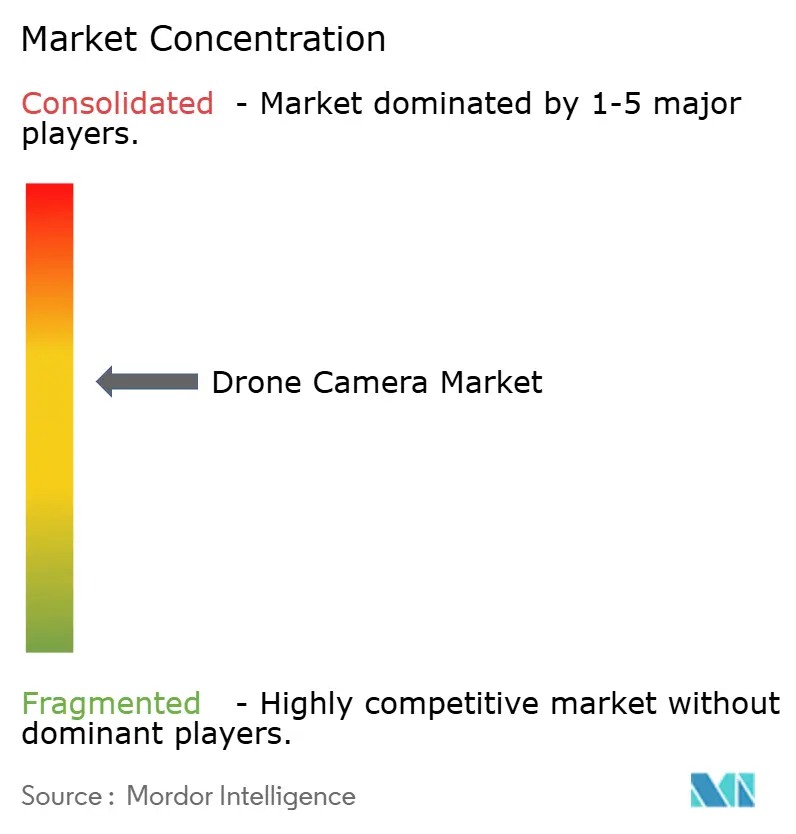

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Drone Camera Market Analysis by Mordor Intelligence

The drone camera market size is forecast to increase from USD 1.86 billion in 2025 to USD 2.18 billion in 2026 and reach USD 4.93 billion by 2031, growing at a 17.30% CAGR over 2026-2031. Lower sensor costs and stronger onboard computing are expanding access to professional aerial imaging beyond filmmaking. Commercial operators increasingly need systems that can capture, process, and interpret visual data during a mission. Proposed United States rules for beyond-visual-line-of-sight operations could support larger inspection and remote-monitoring programs once the rulemaking advances. A shift toward interchangeable optical, thermal, and multispectral payloads on common aircraft platforms also shapes the drone camera market. Platform makers, sensor suppliers, gimbal manufacturers, and chip designers are therefore competing across a wider part of the value chain.

Key Report Takeaways

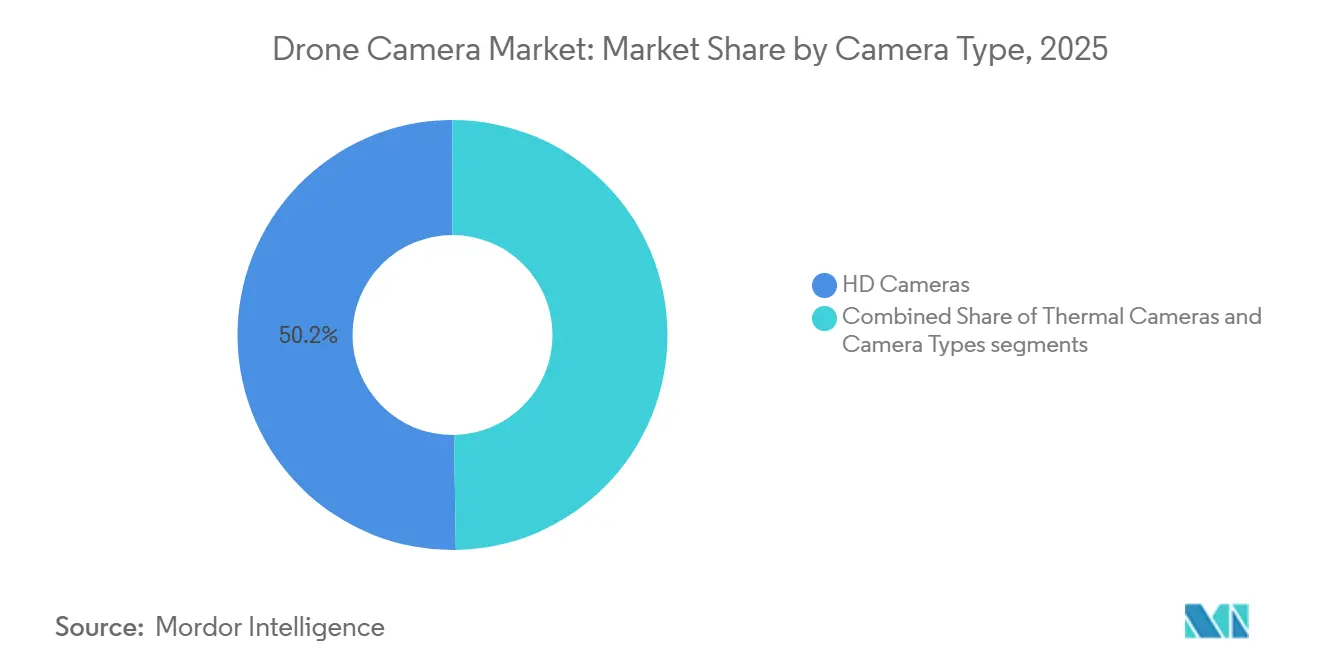

- By camera type, HD cameras held 50.25% of the drone camera market share in 2025, while thermal cameras are projected to grow at a 19.90% CAGR through 2031.

- By application, photography and videography accounted for 30.10% of the drone camera market size in 2025, while thermal imaging is forecast to grow at a 20.05% CAGR through 2031.

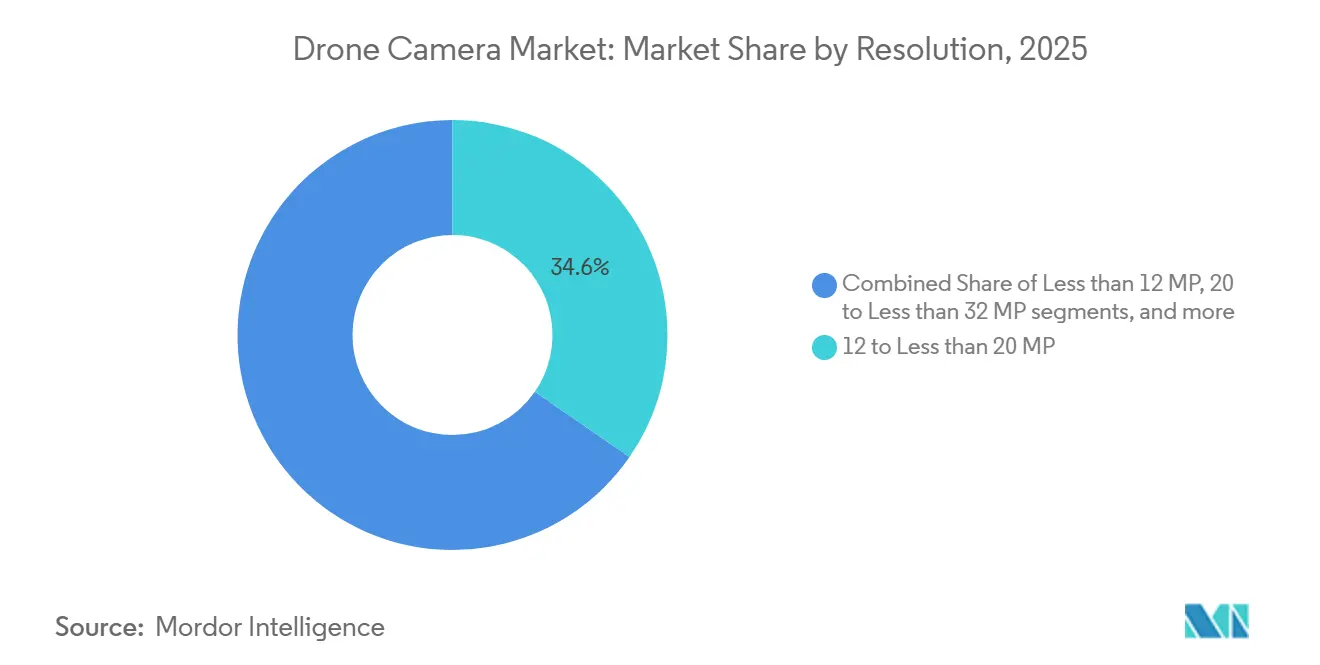

- By resolution, the 12 to less than 20 MP category held 34.61% share in 2025, while the greater than 32 MP category is projected to grow at a 19.45% CAGR through 2031.

- By end user, commercial users accounted for 53.20% of revenue in 2025, while law enforcement is forecast to grow at an 18.70% CAGR through 2031.

- By geography, Asia-Pacific commanded 43.50% of the market share in 2025, while the Middle East and Africa are projected to grow at a 22.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Drone Camera Market*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing integration of AI-enabled onboard image processing | +3.20% | Global, with concentrated supply in China and the US | Medium term (2-4 years) |

| Expansion of multispectral imaging in precision agriculture | +2.80% | Asia-Pacific, North America, and Europe | Long term (≥ 4 years) |

| Growing use of camera drones in professional content production | +2.50% | North America, Europe, and Asia-Pacific | Short term (≤ 2 years) |

| Expansion of BVLOS inspection and remote-monitoring operations | +2.30% | North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Rising adoption of compact thermal imaging payloads | +2.10% | North America, Europe, and the Middle East and Africa | Medium term (2-4 years) |

| Improving price-performance of high-resolution CMOS sensors | +2.00% | Global, supported by Japanese and South Korean supply | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-Enabled Onboard Image Processing Accelerates Product Differentiation

AI-based image processing is moving from cloud-based workflows to in-flight functions. DJI’s Manifold 3 unit combines NVIDIA Jetson Orin NX processing with a 120-gram form factor for the Matrice 400 and Matrice 4 Series. This supports defect detection, subject tracking, and change monitoring without waiting for a ground-station review. The drone camera market can benefit when operators receive usable results while the aircraft remains on site. Local processing also reduces dependence on reliable communications links at remote locations. Chip selection and software integration are becoming as important as optical hardware for product differentiation.

Camera Drone Demand Fueled by Professional Content Production

Professional content production continues to support demand for higher-quality aerial imagery. Drone photography is established in property marketing, film production, broadcast work, and social media content. DJI introduced the Mavic 4 Pro in May 2025 with a 100 MP Hasselblad main camera, a 360° Infinity Gimbal, and 6K/60fps HDR video. This release showed how product improvements can change performance expectations for professional operators. In the drone camera market, 4K and 8K capabilities are increasingly seen as supporting commercial bids rather than premium-only offerings. Three-axis stabilization and unrestricted gimbal movement remain important because high-resolution footage must also be usable in post-production.

High-Resolution CMOS Sensors Reach Commercial Price Points

Improving CMOS sensor economics is bringing higher imaging performance to more commercial systems. Smartphone-scale manufacturing has helped component suppliers adapt advanced image sensors for drone-specific modules. Sony Semiconductor Solutions and TSMC signed a non-binding memorandum in May 2026 to develop and produce next-generation sensors in Kumamoto. FRAMOS introduced 3 drone camera modules based on Sony IMX900 global-shutter sensors for navigation, visual SLAM, and 4K inspection applications.[1]FRAMOS, “FRAMOS Unveils Three Specialized Camera Modules for UAV and Drone Applications,” FRAMOS, framos.com The drone camera market gains from components designed for smaller, lighter payloads without requiring bespoke sensor development. Better sensor availability can raise capability standards while preserving premium prices for systems with proprietary processing features.

Agriculture, Thermal Payloads, and BVLOS Operations Expand Uses

Multispectral imaging is becoming a practical tool for disease detection, nutrient mapping, weed classification, and yield estimation. A 2026 systematic review found strong recent research activity on multispectral unmanned-systems datasets for precision agriculture.[2]Andrea Caroppo, Giovanni Diraco, and Alessandro Leone, “A Systematic Review of Available Multispectral UAV Image Datasets for Precision Agriculture Applications,” Remote Sensing, mdpi.com The drone camera market also benefits from compact thermal payloads used in inspections, emergency response, and energy audits. Proposed FAA BVLOS rules could allow recurring corridor and area-coverage missions at a greater scale. Variable-rate spraying integration and imaging services are making aerial data a capital investment for larger farms. Smallholder adoption in India, Southeast Asia, and Sub-Saharan Africa remains limited by models trained mainly on temperate crops.

Restraints Impact Analysis of Drone Camera Market*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High security and regulatory compliance costs for connected imaging systems | -1.50% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Dependence on concentrated imaging sensor and optical component supply chains | -1.00% | Global, with Japanese and South Korean concentration | Long term (≥ 4 years) |

| Privacy and data-protection constraints on aerial imaging operations | -0.90% | Europe, the UK, and Asia-Pacific | Medium term (2-4 years) |

| Export licensing restrictions on advanced EO/IR imaging payloads | -0.80% | Global, concentrated in US-allied supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory, Security, and Export Compliance Costs Add Friction

Connected imaging systems face growing security and procurement requirements. NDAA-related sourcing rules require organizations to validate supply chains alongside technical evaluations. A BIS final order issued in February 2026 against Teledyne FLIR concerned pre-acquisition export-control violations involving the Zenmuse XT2 thermal-visible camera.[3]Bureau of Industry and Security, “Teledyne FLIR LLC Final Order,” U.S. Department of Commerce, bis.gov This case demonstrates the financial and reputational consequences of weak controls. The drone camera market may favor larger system integrators because they can manage ITAR, EAR, and NDAA requirements more efficiently. Export licensing restrictions for advanced EO/IR payloads can also delay access to allied markets.

Sensor Supply Concentration and Privacy Rules Raise Operating Risk

The drone camera market depends on optical and sensor supply chains concentrated in Japan and South Korea. Disruption at key semiconductor production sites could affect drone assembly schedules and payload availability. The Sony and TSMC agreement may support additional capacity over time, but it does not remove supply concentration during the forecast period. Privacy rules also limit how operators can collect and manage aerial imagery, especially in Europe. GDPR and EASA requirements create additional compliance work for operators who use cameras near people or at sensitive sites. These constraints can favor manufacturers that provide compliant data management and secure imaging systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Drone Camera Market Segment Analysis

By Camera Type:

Thermal Cameras Gain Ground While HD Remains the Volume BaseHD cameras held 50.25% of the drone camera market share in 2025 and remained the principal volume category. Higher resolution within HD systems increasingly reflects specification upgrades rather than entirely new uses. The drone camera market size for HD products is supported by buyers who need practical storage, processing, and flight costs. Many operators can meet routine visual inspection requirements without specialized payloads. This keeps HD systems relevant even as premium imaging formats become more widely available.

Thermal cameras are forecast to grow at a 19.90% CAGR through 2031. Their adoption is supported by law enforcement, grid inspection, building-energy assessment, and search-and-rescue work. Teledyne FLIR OEM launched the Boson SX8 in June 2026 as an NDAA-compliant, ITAR-free uncooled LWIR module with 8-micron pixels and SXGA resolution. The product targets commercial inspection applications that need more detailed thermal output. These specialized payloads serve agriculture and geospatial tasks where data quality supports higher service revenue.

By Application:

Photography and Videography Lead While Thermal Imaging Grows FastestPhotography and videography accounted for 30.10% of the drone camera market size in 2025. Real estate, film, broadcast, and social media work provide ongoing demand for aerial visual content. Better image quality gives operators more flexibility in editing and delivery. The drone camera market remains tied to this established application base because aerial footage is now a standard production element. Greater demand for immersive formats may extend the category beyond conventional flat video.

Thermal imaging is forecast to expand at a 20.05% CAGR through 2031. It supports inspection, search-and-rescue, and public-safety missions that require visibility beyond daylight conditions. DJI launched the Avata 360 in March 2026 with 8K/60fps HDR 360° video, 120 MP photos, and a dual-lens configuration. Surveillance, mapping and surveying, and inspection and maintenance can also benefit from broader BVLOS operations. Recurring inspection contracts can replace individual flight assignments for service providers.

By Resolution:

More Than 32 MP Expands Professional Mapping OptionsThe 12 to less than 20 MP category accounted for 34.61% of revenue in 2025. It offers a workable balance between image quality, sensor yield, file size, and processing time. This range remains suitable for many commercial operators that do not need survey-grade detail. The drone camera market maintains demand in this band because it supports routine professional work. Less than 12 MP cameras continue to serve FPV navigation and autonomous flight control functions, where low latency is more important than image detail.

The greater than 32 MP category is forecast to grow at a 19.45% CAGR through 2031. Demand comes from survey-grade mapping, larger property documentation, and defense-adjacent uses. Phase One launched the iXM-FS130 in February 2026, featuring Fusion Shutter technology for sub-centimeter mapping from fixed-wing aircraft at speeds above 120 knots. This type of product shows why higher resolution is important for professional geospatial work. These procurement rules can influence choices beyond image quality alone.

By End User:

Commercial Users Lead and Law Enforcement AcceleratesCommercial users held 53.20% of revenue in 2025. The group includes real estate operators, agricultural service providers, construction-monitoring firms, and inspection contractors. Their needs range from standard visual documentation to advanced multispectral and thermal data. The breadth of these uses helps maintain a large revenue base, and this flexibility can improve utilization and reduce equipment duplication.

Law enforcement is forecast to grow at an 18.70% CAGR through 2031. The growth follows the wider use of drones in First Responder programs after the FAA streamlined authorizations in 2025. Motorola Solutions reported that more than 1,500 US law enforcement agencies operated drone programs in 2026, compared with 559 municipal departments in 2020. The company also reported nearly 600 new DFR programs within 4 months of the 2025 authorization change. Chula Vista reported drone response times of 3.5 minutes, while Lakewood reported first-on-scene arrival 80% of the time.

Geography Analysis

Asia-Pacific accounted for 43.50% of regional revenue in 2025 and is forecast to remain the largest region through 2031. China is a key production base and a major demand center for smart-city surveillance, precision agriculture, and content creation. India and Southeast Asia are expanding through a growing base of commercial operators and investment in domestic manufacturing. India’s PLI program for drones supports local manufacturing and can lower platform costs for commercial users.

North America and Europe form the second major demand cluster. The proposed FAA Part 108 pathway supports the prospect of scaled BVLOS commercial operations, although the final rule remained at the NPRM stage in mid-2026. The drone camera market in Europe faces SORA and GDPR requirements that add compliance work but support demand for privacy-compliant architectures. South America, led by Brazil, offers a growing demand for multispectral and HD systems in precision agriculture. Rural connectivity limits the use of real-time analytics in some locations.

The Middle East and Africa are forecast to grow at a 22.55% CAGR through 2031, making them the fastest-growing regions. Infrastructure investment, defense modernization, and more structured regulation support this growth. The UAE GCAA requires pilot certification, airspace approval, and security clearance for commercial UAS operators. Dubai’s 2025 DCAR-UAS Issue 03 rules also set requirements for commercial UAS activity. Kenya, South Africa, and Ethiopia are establishing early agricultural monitoring use cases, while regional expansion starts from a lower installed base.

Competitive Landscape

The drone camera market is moderately concentrated at the platform level. DJI holds a leading position across consumer, prosumer, and commercial systems through its integrated sensors, gimbals, flight controllers, and fleet management software. Teledyne FLIR has a strong position in thermal payloads, while Phase One serves large-format aerial mapping, and Workswell serves industrial thermal inspection. These specialist positions rely on proprietary hardware and compliant supply chains.

DJI expanded FlightHub 2 in April 2026 with AI Copilot, Vision-Language Model route planning, 500-megapixel cloud-stitched panoramas, and Sync 2.0 integration. This strategy makes software workflow an important part of platform selection. Teledyne FLIR followed a different approach through its Thermal by FLIR program. The program integrates FLIR modules into third-party systems, including Gremsy’s ORUS-L and Lynx payloads, as well as ACSL’s SAMO system. This extends thermal imaging across several aircraft suppliers rather than relying on a single platform.

The drone camera market still has opportunities for NDAA-compliant thermal payloads priced below premium offerings. Smaller-farm platforms in South Asia and Sub-Saharan Africa are another potential area because field sizes and operating conditions differ from those in large developed markets. Edge-AI systems for BVLOS inspection could also support autonomous missions without continuous operator oversight. Autel Robotics moved away from the EVO II consumer series toward the EVO Lite Enterprise Series, indicating greater focus on application-specific commercial systems.

Drone Camera Industry Leaders

Canon Inc.

Teledyne FLIR LLC

SZ DJI Technology Co., Ltd.

GoPro, Inc.

Sony Group Corporation

- *Disclaimer: Major Players sorted in no particular order

Drone Camera Market Companies Covered in this Report

- SZ DJI Technology Co., Ltd.

- Sony Group Corporation

- Canon Inc.

- GoPro, Inc.

- Panasonic Holdings Corporation

- Teledyne FLIR LLC

- CONTROP Precision Technologies Ltd.

- Yuneec (ATL Drone)

- Autel Robotics Co., Ltd.

- Parrot Drone SAS

- Phase One A/S

- Shenzhen Viewpro Technology Co., Ltd.

- Workswell s.r.o.

Recent Industry Developments in Drone Camera Market

- June 2026: Teledyne FLIR OEM launched the Boson SX8, an NDAA-compliant, ITAR-free uncooled LWIR camera module with SXGA resolution and an 8-micron pixel pitch. The product strengthens law-enforcement surveillance capabilities across drone-based overwatch, perimeter monitoring, nighttime operations, search missions, and counter-UAS deployments, while enabling agencies and integrators to adopt higher-resolution thermal imaging in compact, lower-SWaP platforms at scale.

- November 2025: DJI introduced a long-range aerial LiDAR payload combining a 1,535 nm LiDAR sensor, dual 100 MP RGB mapping cameras, and a high-precision positioning system. Mounted on the Matrice 400, the payload is used for topographic surveys, forestry, infrastructure inspection, and emergency mapping.

Global Drone Camera Market Report Scope

Drone cameras are imaging systems integrated with unmanned aerial vehicles (UAVs) to capture photographs, video, and sensor-based visual data during flight. These systems may include high-resolution sensors, gimbal stabilization, zoom, image processing, geotagging, and real-time data transmission capabilities. Integrated with navigation and flight-control systems, drone cameras support aerial inspection, mapping, surveillance, traffic monitoring, public safety, search operations, evidence collection, delivery monitoring, and situational awareness across commercial and law enforcement applications.

The drone camera market is segmented by camera type, application, resolution, end-user, and geography. By camera type, the market is segmented into HD cameras, thermal cameras, and other camera types. By application, the market is segmented into photography and videography, thermal imaging, surveillance, mapping and surveying, inspection and maintenance, and other applications. By resolution, the market is segmented into less than 12 MP, 12 to less than 20 MP, 20 to less than 32 MP, and greater than 32 MP. By end-user, the market is segmented into commercial and law enforcement. The report also covers the market sizes and forecasts for the drone camera market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

Segmentation Overview

| HD Cameras |

| Thermal Cameras |

| Other Camera Types |

| Photography and Videography |

| Thermal Imaging |

| Surveillance |

| Mapping and Surveying |

| Inspection and Maintenance |

| Other Applications |

| Less than 12 MP |

| 12 to Less than 20 MP |

| 20 to Less than 32 MP |

| Greater Than 32 MP |

| Commercial |

| Law Enforcement |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Camera Type | HD Cameras | ||

| Thermal Cameras | |||

| Other Camera Types | |||

| By Application | Photography and Videography | ||

| Thermal Imaging | |||

| Surveillance | |||

| Mapping and Surveying | |||

| Inspection and Maintenance | |||

| Other Applications | |||

| By Resolution | Less than 12 MP | ||

| 12 to Less than 20 MP | |||

| 20 to Less than 32 MP | |||

| Greater Than 32 MP | |||

| By End User | Commercial | ||

| Law Enforcement | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the drone camera market by 2031?

The drone camera market is forecast to reach USD 4.93 billion by 2031, from USD 2.18 billion in 2026, at a 17.30% CAGR. Its expansion reflects broader commercial use of visual, thermal, and multispectral payloads.

Which camera type held the largest share in 2025?

HD cameras led with 50.25% revenue share in 2025, while thermal cameras are expected to grow fastest at a 19.90% CAGR.

Which application is expected to grow fastest through 2031?

Thermal imaging is forecast to expand at a 20.05% CAGR, supported by inspection, emergency response, and public-safety use cases.

Why are thermal drone cameras gaining adoption?

Thermal payloads support infrastructure inspection, building energy audits, search-and-rescue, and law enforcement operations when visible imagery is insufficient. The drone camera market also benefits when thermal payloads can be fitted to common aircraft platforms.

Which region is expected to expand fastest?

Middle East and Africa is forecast to grow at a 22.55% CAGR through 2031, supported by infrastructure, defense, and regulatory developments.

How is AI changing drone camera systems?

Onboard AI supports defect detection, tracking, route planning, and mission decisions during flight, reducing delays in data review. This can help the drone camera market serve remote and BVLOS operations with less reliance on constant data links.

Page last updated on: