India Unmanned Aerial Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

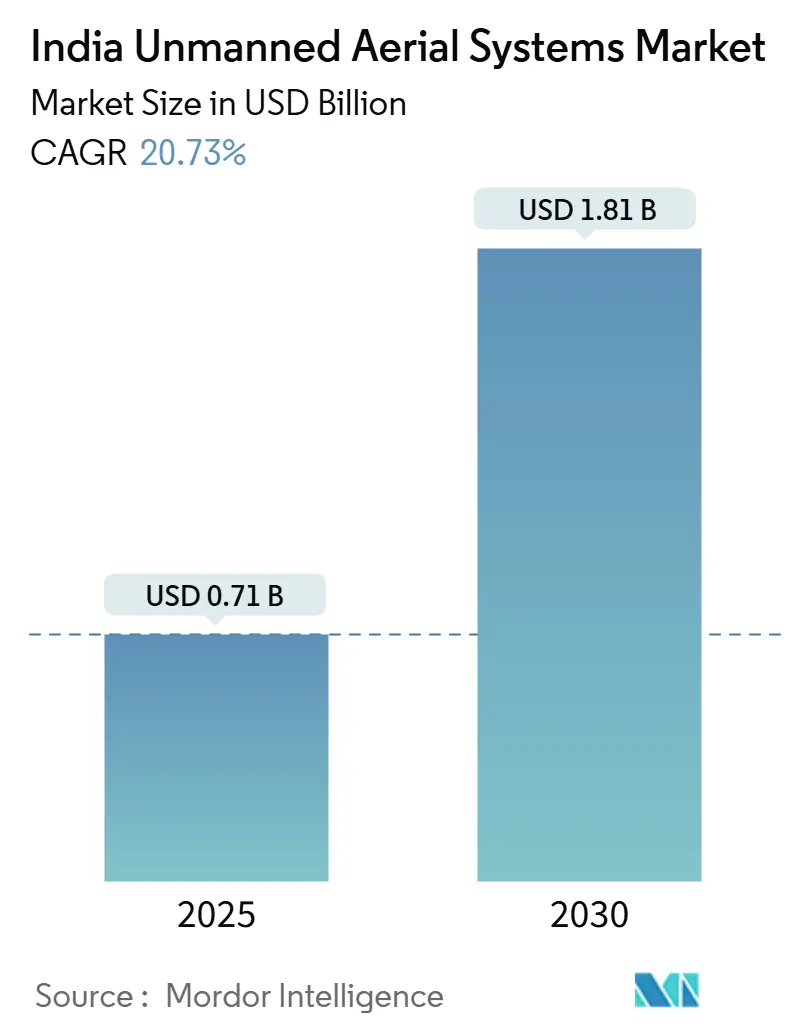

| Market Size (2025) | USD 0.71 Billion |

| Market Size (2030) | USD 1.81 Billion |

| Growth Rate (2025 - 2030) | 20.73% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Unmanned Aerial Systems Market Analysis by Mordor Intelligence

The India unmanned aerial systems (UAS) market reached a market size of USD 706.32 million in 2025 and is projected to expand to USD 1,811.83 million by 2030, translating into a 20.73% CAGR over the forecast period. Demand acceleration stems from three reinforcing trends: defense‐led fleet expansion, precision farming adoption, and a supportive industrial policy that stimulates indigenous manufacturing capacity. Continued procurement of medium-altitude long-endurance platforms by the Indian Army, the Production Linked Incentive (PLI) scheme’s tariff-neutral subsidies, and pilot‐friendly Drone Rules 2021 strengthen investment confidence while compressing time-to-market for new entrants. Parallel growth in ancillary technologies—AI-powered avionics, hydrogen powertrains, and 5G-enabled data links—raises system capability benchmarks and encourages commercial buyers to migrate from imported, hobby-grade devices to professional-class equipment. As a result, the India unmanned aerial systems market is shifting from hardware sales toward integrated service contracts that bundle leasing, training, compliance management, and data analytics into a single solution.

Key Report Takeaways

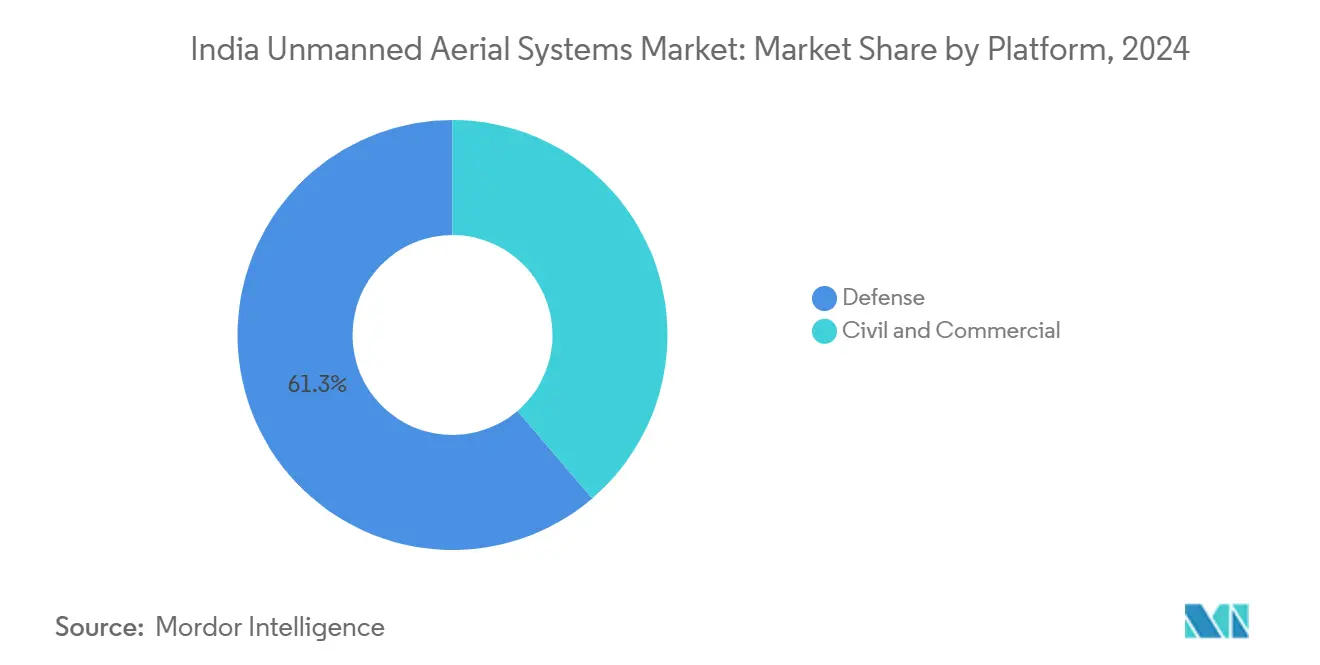

- By platform, defense platforms held 61.25% of India unmanned aerial systems market share in 2024, while the civil and commercial segment is forecast to deliver a 22.76% CAGR through 2030.

- By end-user industry, defense and security captured 39.43% of India unmanned aerial systems market share in 2024; the logistics and transportation segment is projected to advance at a 19.71% CAGR to 2030.

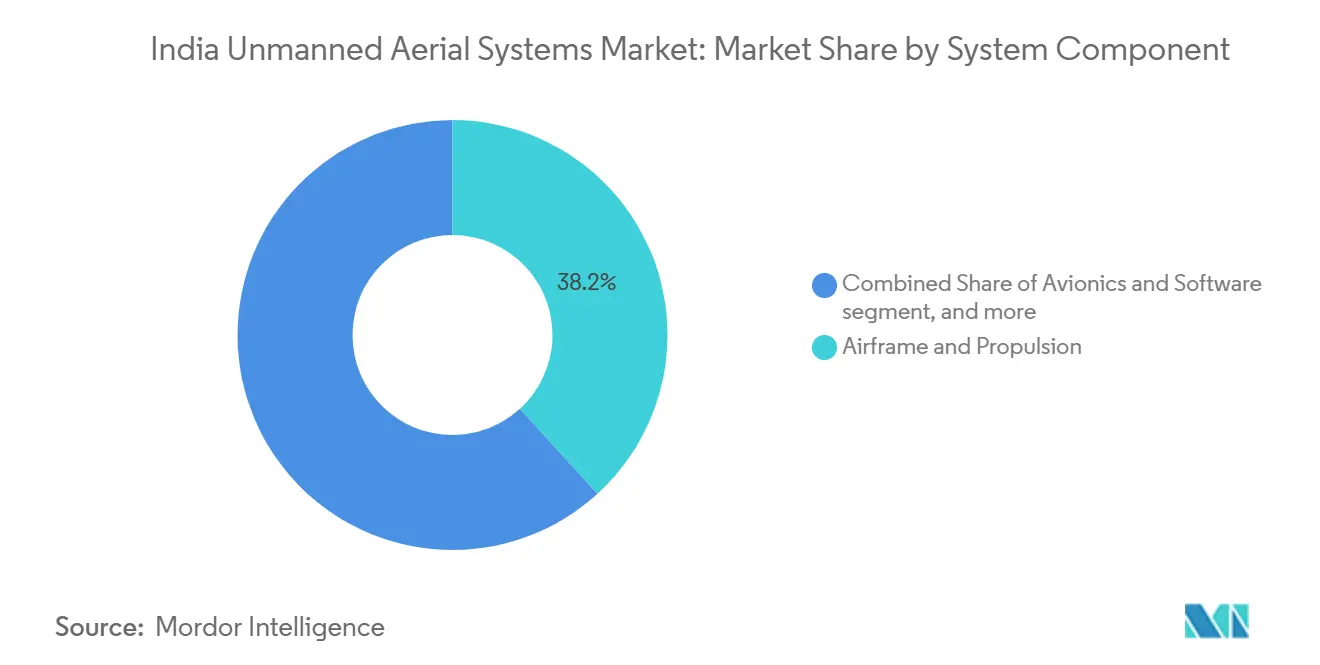

- By system component, airframe and propulsion accounted for a 38.21% share of the India unmanned aerial systems market in 2024; avionics and software are expected to expand at a 23.34% CAGR over the same horizon.

- By operating range, VLOS flights represented 48.31% of the India unmanned aerial systems market size in 2024, while BVLOS operations are poised for a 20.49% CAGR once regulatory corridors become operational.

India Unmanned Aerial Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PLI and 2021 liberalized drone rules | +4.20% | Karnataka, Tamil Nadu, Maharashtra | Medium term (2-4 years) |

| Defense modernization and indigenization push | +5.80% | All border states with priority in Rajasthan, Punjab, Jammu and Kashmir | Long term (≥ 4 years) |

| Subsidized “Kisan Drone” adoption in precision agriculture | +3.10% | Punjab, Haryana, Uttar Pradesh, Maharashtra | Short term (≤ 2 years) |

| Swarming-cinematography demand from Bollywood studios | +1.40% | Mumbai, Hyderabad entertainment hubs | Medium term (2-4 years) |

| Fin-tech leasing models enabling Drone-as-a-Service (DaaS) | +2.70% | Tier-1 and Tier-2 urban centers | Short term (≤ 2 years) |

| 2027 smart-city GIS mandate for real-time surveillance | +3.20% | 100 Smart Cities nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PLI and 2021 Liberalised Drone Rules

Government outlays of INR 120 crore (USD 136.76 million) across 23 beneficiaries catalyzed a seven-fold domestic turnover by removing prior security-clearance red tape and digitizing flight approvals through the Digital Sky platform.[1]Press Information Bureau, “PLI scheme incentivizes domestic manufacturing, increases production,” pib.gov.in Manufacturers now realize a four-to-five-times multiplier on every rupee of subsidy as private capital floods the India unmanned aerial systems market. Bengaluru, Chennai, and Pune have emerged as high-volume clusters equipped with ISO-grade facilities and AS9100 certifications, reducing lead times from import-heavy 20-week cycles to under eight weeks. Lower compliance costs spur MSMEs to localize flight controllers, powertrains, and RF modules, slashing Chinese component exposure from 80% in 2021 to 39% in 2025. Regulatory certainty created by the Drone Rules 2021 also simplifies airworthiness approvals, enabling rapid testing of hydrogen fuel cells and swarm intelligence features that differentiate domestic platforms.

Defense Modernization and Indigenization Push

Procurement planning for over 150 additional MALE UAVs by 2027 gives domestic manufacturers multiyear revenue visibility.[2]Times of India, “Army gearing up to induct more heavy-duty drones,” timesofindia.indiatimes.com DRDO’s Archer-NG and Rustom systems now achieve 24-hour endurance at 30,000 feet, matching imported peers while conforming to India-specific terrain and climatic needs. Successful live-fire trials during Operation Sindoor validated AI-assisted target recognition modules that raised hit probability by 19% compared with legacy systems. Indigenization also lowers life-cycle costs by cutting customs duties, ensuring availability of spares, and enabling software upgrades through indigenous encryption standards, aligning with the Ministry of Defence’s negative-import list policy.

Subsidized “Kisan Drone” Adoption in Precision Agriculture

The Namo Drone Didi program earmarks INR 1,261 crore (USD 1.44 billion) to deliver 15,000 subsidised crop-spray drones by 2026, targeting women-led self‐help groups and boosting rural entrepreneurship.[3]India.gov.in, “Namo Drone Didi,” india.gov.in An 80% subsidy capped at INR 8 lakh (USD 9,117.6) drives down payback periods to under 14 months for smallholders, compared with five years under market pricing. Pilot projects covering 3 million acres across 12 states showed nano-fertilizer application cutting input costs 20% and raising yields 10%, directly improving farm margins amid volatile fertilizer prices. As drone operators diversify into seeding and soil diagnostics, addressable revenue per hectare rises, lifting the commercial attractiveness for manufacturers and service aggregators within the India unmanned aerial systems market.

Swarming-Cinematography Demand from Bollywood Studios

India’s 1,800-film yearly output has migrated from single-drone aerial shots to AI-orchestrated 50-drone swarms that create immersive light formations and choreographed sequences. Studios require 4K/8K HDR capture, real-time transmission, and centimeter-level positioning, spurring suppliers to engineer high-precision GNSS antennas and gimbals. Rental houses in Mumbai and Hyderabad now offer daily rates that are 35% lower than pre-2022 imports due to indigenous sourcing, widening adoption among regional cinemas. These entertainment workflows propagate into industrial sectors that need multi-asset inspection or coordinated site surveys, broadening the underlying technology’s commercial applications.

Restraints Impact Analysis*

| Restraint | ( ~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| BVLOS regulatory uncertainty and corridor delays | -2.80% | National pilot zones in Telangana, Karnataka, Gujarat | Medium term (2-4 years) |

| Import ban on Chinese critical components | -1.90% | Chennai, Pune, Noida component hubs | Short term (≤ 2 years) |

| Emerging UAV-cyber export-control restrictions | -1.30% | Export-oriented clusters in Bengaluru and Hyderabad | Long term (≥ 4 years) |

| FPV technician and repair skill-gap | -2.10% | Tier-2/3 cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

BVLOS Regulatory Uncertainty and Corridor Delays

Only 20 entities have secured experimental BVLOS clearances since 2021, limiting logistics firms to trial-size fleets despite solid commercial economics for 10-kilogram payload deliveries. Corridor mapping requires multi-agency approvals involving DGCA, Airports Authority of India, and defense airspace custodians, stretching timelines and raising compliance costs. Investors remain hesitant to fund large-scale BVLOS fleets until a nationwide unmanned traffic management (UTM) protocol is finalized, dampening near-term upside for the fastest-growing operating range segment within the India unmanned aerial systems market.

Import Ban on Chinese Critical Components

Flight controllers, vision sensors, and lithium-polymer cells from Chinese suppliers still account for 39% of build materials, exposing manufacturers to price swings and supply disruptions following the 2024 import ban. Domestic electronics incentives can offset cost inflation only over a multiyear horizon, compelling OEMs to redesign stacks for local compatibility. Interim shortages inflate bill of materials by 12-15%, narrowing operating margins and delaying cost parity with imported equivalents.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Defense Spend Sustains Investment Momentum

Defense applications generated 61.25% of the India unmanned aerial systems market size in 2024, driven by high-value procurement programs and urgent border surveillance needs. Military buyers prioritize endurance, secure data links, and anti-jam capabilities, pushing unit ASPs well above commercial averages. Overnight reconnaissance missions in Himalayan terrain validate the reliability of indigenous airframes, encouraging incremental orders that lock manufacturers into predictable demand cycles. Although capturing a smaller 2024 base, the civil and commercial segment is forecasted to clock a 22.76% CAGR as DGCA streamlines approvals for mapping, agriculture, and cinematography missions. Service-oriented players exploit subscription pricing, removing capital barriers for mid-market customers. The converging feature set between defense and commercial platforms—such as AI-assisted navigation—reinforces technology spill-over, accelerating capability enhancement across both segments.

Civil and commercial use cases extend from 50-hectare farm plots to 300-kilometer pipeline inspections. Logistics firms run controlled pilots that reveal 35% cost savings in last-mile delivery against two-wheeler couriers, pending BVLOS green lights. The maturation of 5G networks lowers latency for command-and-control links, enabling real-time video analytics that match the security protocols demanded by e-commerce platforms. As a result, the India unmanned aerial systems market experiences platform diversification, with lightweight multirotors complementing high-end fixed-wing craft in a modular procurement strategy that optimizes mission profiles while ensuring airspace compliance.

By End-User Industry: Logistics Poised for a Demand Leap

Defense and security represented 39.43% of India unmanned aerial systems market share in 2024, reflecting consistent budget allocations and multi-year contract structures. Military adoption triggers ancillary demand for maintenance, training, and simulation services, embedding long-tail revenue in OEM order books. However, only nascent today, logistics and transportation are projected to record a 19.71% CAGR on the back of express-parcel volumes rising at double-digit rates and increasing urban congestion. Drone-enabled middle-mile hubs near metropolitan areas compress delivery windows, enhancing customer trust in e-commerce platforms that compete on same-day service. Agricultural use cases, underpinned by government subsidies, unlock steady annual demand for spray drones that cover cereals, pulses, and high-value horticulture crops. Mining and energy utilities experiment with volumetric-survey drones that cut manual survey costs by 28%, providing a solid business case even before BVLOS rules mature.

Media and entertainment broaden the customer base through custom-rig services that cater to OTT content producers and regional film studios. Infrastructure and construction firms leverage photogrammetry to achieve centimeter-grade site maps, reducing rework expenses. Public safety agencies incorporate thermal‐equipped quadcopters for crowd monitoring during festivals, improving incident response coordination with ground personnel. Altogether, the end-user landscape demonstrates that once regulatory thresholds are met, high-growth commercial verticals can capture share from currently dominant defense customers, diversifying revenue streams for the India unmanned aerial systems industry.

By System Component: Software-Defined Drones Gain Traction

Airframe and propulsion hardware contributed 38.21% of 2024 revenue, serving as the baseline investment every operator must make. Materials engineering advances—such as carbon-fiber composites and additive manufacturing—shave structural weight by 12%, enabling a more extended range without larger batteries. Meanwhile, avionics and software, posting a projected 23.34% CAGR, transform drones into data-centric platforms. AI-assisted obstacle detection, GPS-denied navigation, and edge-based image analytics differentiate new releases, commanding price premiums. Integrating third-party LiDAR payloads via plug-and-play bays accelerates time-to-solution for mapping firms that used to rely on ground LiDAR scanners.

Sensor payloads progress along two vectors: higher resolution and multi-modal fusion. Thermal-optical dual cameras combine with hyperspectral imaging to boost crop-stress detection accuracy. Power systems migrate toward silicon-anode battery chemistries that deliver 15-20% higher energy density, extending mission endurance. Ground-control hardware leverages 5G modems to reduce latency, which is critical for BVLOS trials. Collectively, these component innovations expand the functional diversity of the India unmanned aerial systems market and shift competition toward software ecosystems that lock customers into recurring license upgrades.

By Operating Range: BVLOS Unlocks Scale Economics

VLOS flights accounted for 48.31% of India unmanned aerial systems market size in 2024. Operators rely on spotters or telecom relay towers to ensure line-of-sight safety, limiting range to around 400 meters. Extended VLOS options, where observers coordinate through radio hand-offs, push operational envelopes to 2 kilometers, enough for large construction sites. BVLOS capability, expected to grow at 20.49% CAGR, is the game-changer. Once corridors and UTM protocols are finalized, logistics firms can replace 30-kilometer van routes with 8-kilometer aerial hops that deliver comparable payloads in one-third the time, reducing carbon emissions 40% per trip.

Technical safeguards—detect-and-avoid radars, redundant command links, and autonomous return-to-home fail-safes—raise bill-of-materials costs, but service revenue from high utilization offsets capex premiums. BVLOS adoption will also catalyze demand for cloud-based fleet management that synchronizes air, ground, and warehouse operations, accelerating the systemic digitalization of Indian supply chains. For rural areas, BVLOS crop-spray missions could cover 500 hectares per day, compared with 120 hectares under VLOS restrictions, multiplying addressable revenue for agricultural service providers within the India unmanned aerial systems market.

Geography Analysis

Southern manufacturing corridors dominate supply, with Karnataka, Tamil Nadu, and Maharashtra hosting more than 65% of registered drone factories and design centers.[4]Rediff, “From phones to drones, Google looks to firm up India bet,” rediff.com Bengaluru’s aerospace ecosystem supplies avionics, while Chennai’s port connectivity streamlines exports to Southeast Asia. Pune and Nashik leverage automotive supply chains to localize lightweight composites and motor assemblies. These clusters attract venture funding that finances vertical integration projects aimed at sub-15-kilogram class drones, squeezing component costs by leveraging economies of scale.

Northern agrarian states—Punjab, Haryana, and Uttar Pradesh—drive usage through large government-subsidized spray programs under the Namo Drone Didi scheme. Women‐led self-help groups receive training at newly established drone academies, addressing pilot shortages and elevating rural incomes. Uttar Pradesh further mandates digital crop mapping in its Bundelkhand region, creating demand for data analytics alongside hardware sales.

Border states like Rajasthan and J&K exhibit heavy defense concentration, with high-altitude trials validating anti-jam navigation software and cold-weather battery chemistries. The Smart Cities Mission spreads institutional demand nationwide; tier-2 cities such as Indore, Surat, and Bhubaneswar commission GIS-driven surveillance programs that feed real-time data into command centers. Eastern corridors, spanning West Bengal to Assam, open new logistics lanes for BVLOS pilots that connect remote tea estates and oil fields to urban supply hubs. As 5G corridors extend along national highways, geographic adoption is set to broaden beyond traditional aerospace centers, embedding the India unmanned aerial systems market into diverse socio-economic contexts across the country.

Competitive Landscape

The India unmanned aerial systems market exhibits moderate concentration: ideaForge commands a major share of defense-grade revenue due to first-mover intellectual property in GPS-denied avionics.[5]IndMoney, “Ideaforge Technology Ltd Share Price,” indmoney.com Raphe mPhibr’s USD 100 million funding injects scale and deepens R&D into heavy-payload craft, making it a formidable challenger. Garuda Aerospace leverages a diversified vertical strategy—agriculture, mining, and surveillance—and targets 85% component indigenization by mid-2025, reducing supply risk.

The intellectual property race intensifies; ideaForge holds 78 active patents, NewSpace Research focuses on swarm algorithms, and Zen Technologies advances counter-drone solutions, reflecting specialized niches rather than broad-spectrum competition. Capital markets remain supportive; ideaForge’s 2023 IPO rallied 94% on listing day and unlocked retail liquidity for follow-on innovation. Consolidation possibilities arise as OEMs seek subsystem suppliers to lock in domestic manufacturing depth; recent MoUs link composite fabricators in Coimbatore with avionics houses in Bengaluru, hinting at a cluster-based merger trend that could compress the supplier base over the next 36 months.

OEMs pivot toward service revenue, bundling leasing, training, and data analytics. ideaForge’s Drone-as-a-Service contracts with state police generate annuities that shelter margins from component inflation. Raphe mPhibr pilots hydrogen-fuel drone rentals for port surveillance, while Garuda Aerospace opens nationwide service kiosks for rapid field repairs. Such integrated models become critical differentiators as price competition intensifies in entry-level segments. Technology, capital access, and service depth define competitive fitness in India's evolving unmanned aerial systems market.

India Unmanned Aerial Systems Industry Leaders

ideaForge Technology Pvt. Ltd.

Garuda Aerospace Pvt. Ltd.

Asteria Aerospace Limited

Paras Defence and Space Technologies Limited

Throttle Aerospace System Pvt. Ltd. (TAS)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: The Indian Army placed an INR 137 crore (USD 156.14 million) emergency procurement order with ideaForge to bolster frontline reconnaissance capability.

- May 2025: Zuppa Geo Navigation Technologies’ Ajeet Mini tactical UAV received Indian Army field validation in high-altitude terrain.

- February 2025: ideaForge introduced the NETRA 5 UAV aimed at tactical defense deployments.

- July 2024: Inertial Labs partnered with ideaForge to integrate LiDAR payloads for high-resolution mapping applications.

India Unmanned Aerial Systems Market Report Scope

| Civil and Commercial |

| Defense |

| Defense and Security |

| Agriculture |

| Infrastructure and Construction |

| Logistics and Transportation |

| Media and Entertainment |

| Mining and Energy Utilities |

| Public Safety and Disaster Management |

| Environmental Monitoring and Forestry |

| Airframe and Propulsion |

| Payload and Sensors |

| Avionics and Software |

| Ground Control and Data Links |

| Batteries and Power Systems |

| Other Components |

| VLOS |

| EVLOS |

| BVLOS |

| By Platform | Civil and Commercial |

| Defense | |

| By End-User Industry | Defense and Security |

| Agriculture | |

| Infrastructure and Construction | |

| Logistics and Transportation | |

| Media and Entertainment | |

| Mining and Energy Utilities | |

| Public Safety and Disaster Management | |

| Environmental Monitoring and Forestry | |

| By System Component | Airframe and Propulsion |

| Payload and Sensors | |

| Avionics and Software | |

| Ground Control and Data Links | |

| Batteries and Power Systems | |

| Other Components | |

| By Operating Range | VLOS |

| EVLOS | |

| BVLOS |

Key Questions Answered in the Report

What is the 2025 revenue value and expected growth rate through 2030?

The India unmanned aerial systems market reached a market size of USD 706.32 million in 2025 and is projected to expand to USD 1,811.83 million by 2030, translating into a 20.73% CAGR.

Which platform category is expected to grow the fastest?

Civil and commercial platforms are forecasted to post a 22.76% CAGR, outpacing defense platforms once BVLOS regulations mature.

Why are agricultural drones heavily subsidized?

Programs such as Namo Drone Didi provide up to 80% capital support, enabling precision spraying that lowers input costs 20% and boosts yields 10%.

What federal incentive underpins domestic manufacturing?

The Production Linked Incentive scheme allocates INR 120 crore (USD 13.72 million) across 23 firms, triggering a seven-fold rise in domestic drone turnover.

How do fintech leasing models accelerate adoption?

Drone-as-a-Service (DaaS) bundles hardware, training, and maintenance into monthly subscriptions, cutting upfront costs and broadening SME access.

Which Indian states anchor the manufacturing base?

Karnataka, Tamil Nadu, and Maharashtra together host more than 65% of registered factories, benefitting from aerospace supply chains and port access.

How do import restrictions on Chinese components influence costs?

The 2024 ban leaves 39% of critical parts still sourced from China, raising bills of material 12-15% until local substitutes scale up.

What does the current market-concentration score indicate?

A score of 6 shows a moderately consolidated landscape where the top three players account for roughly 60% of revenue yet still face active challengers.

Page last updated on: