Target Unmanned Aerial Vehicles Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

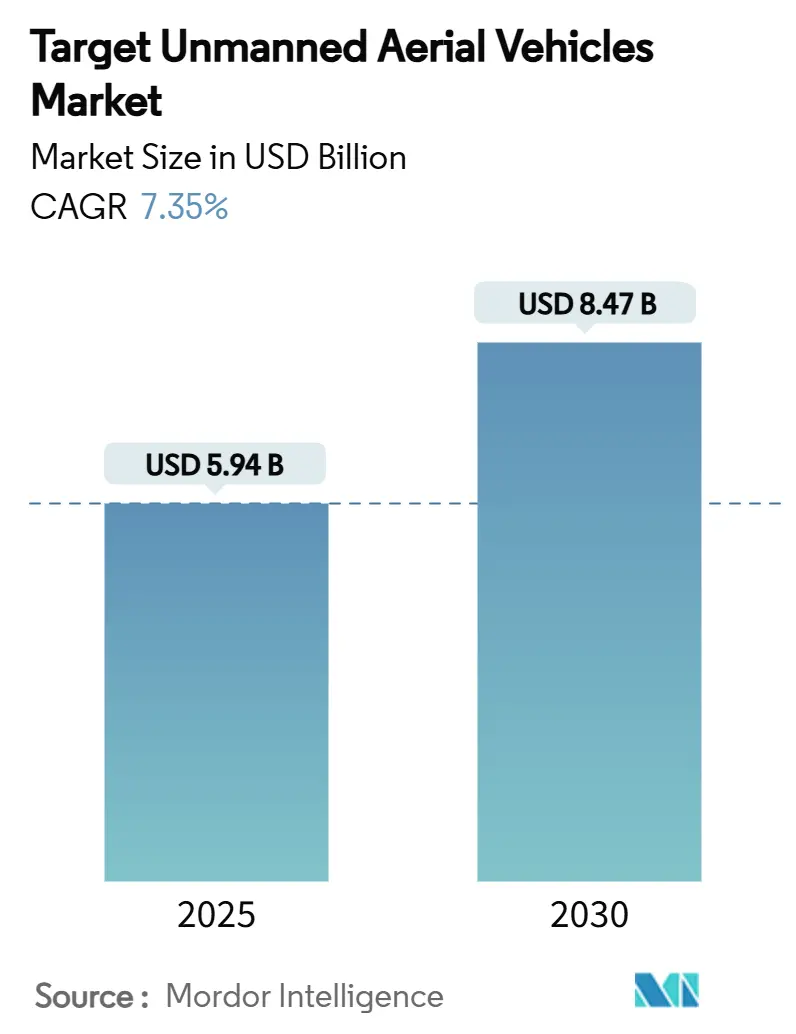

| Market Size (2025) | USD 5.94 Billion |

| Market Size (2030) | USD 8.47 Billion |

| Growth Rate (2025 - 2030) | 7.35% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Target Unmanned Aerial Vehicles Market Analysis by Mordor Intelligence

The target unmanned aerial vehicles market size is valued at USD 5.94 billion in 2025 and is forecasted to reach USD 8.47 billion by 2030, advancing at a 7.35% CAGR. Heightened funding for low-cost autonomous systems under the US Department of Defense Replicator Initiative anchors short-term demand, while comparable modernization drives in Europe and Asia-Pacific sustain long-term growth.[1]Source: US Department of Defense, “Replicator Initiative Fact Sheet,” defense.gov Defense ministries are shifting resources from expensive live-aircraft sorties to realistic yet lower-cost target platforms, expanding procurement pipelines beyond traditional air forces. Manufacturers able to blend supersonic performance, stealth signatures, and modular payloads are capturing multi-year framework contracts, especially for swarm and fifth-generation threat simulation. At the same time, sustainability mandates and fuel-logistics pressures accelerate interest in electric and hybrid propulsion concepts, broadening the addressable customer base for the target unmanned aerial vehicles market.

Key Report Takeaways

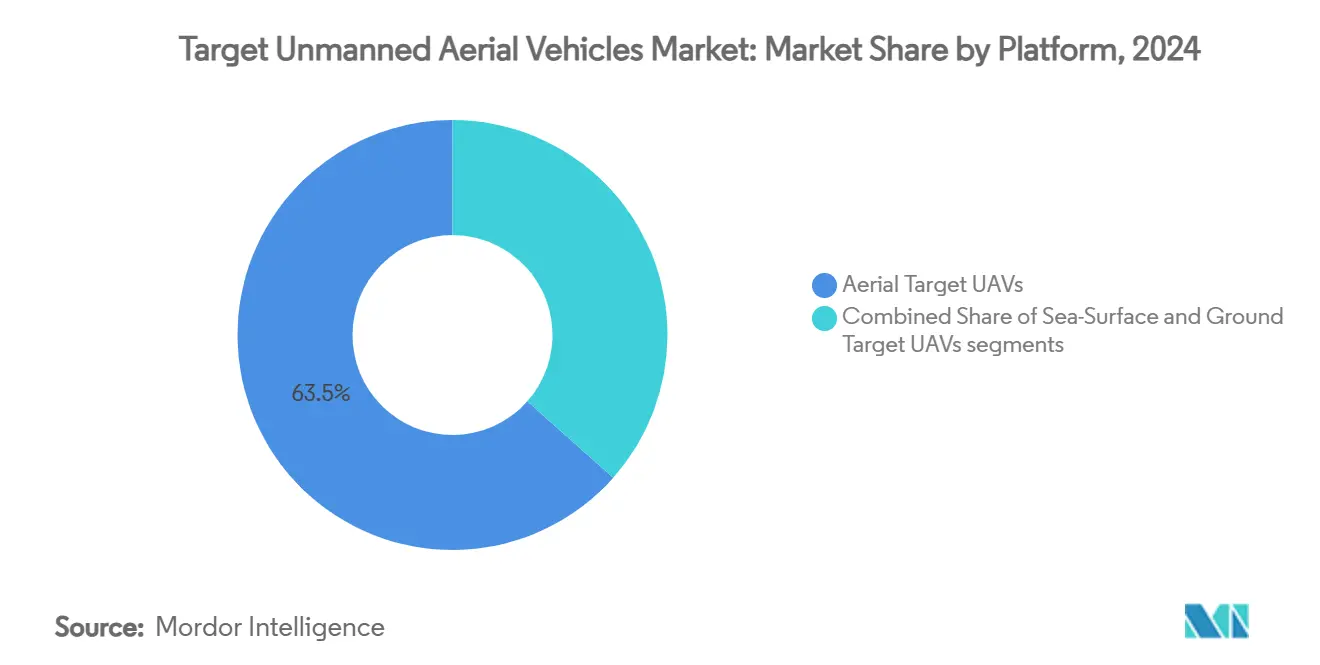

- By platform, aerial target UAVs led with 63.45% of the target unmanned aerial vehicles market share in 2024, whereas marine target UAVs are projected to expand at an 8.78% CAGR to 2030.

- By engine type, turbojet systems accounted for 44.70% of the target unmanned aerial vehicles market size in 2024, while electric/hybrid propulsion is advancing at a 10.30% CAGR through 2030.

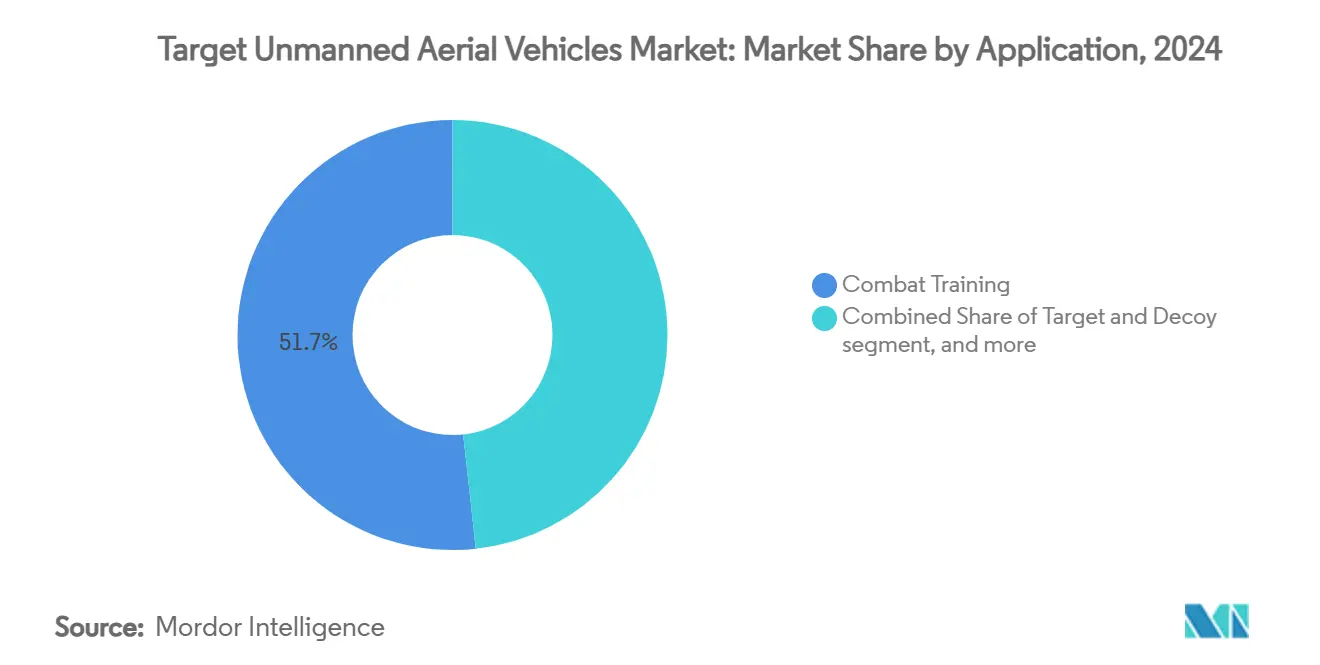

- By application, combat training held 51.72% revenue share in 2024; target acquisition applications exhibit the highest projected CAGR at 9.24% during 2025-2030.

- By range, medium-range platforms captured 49.10% of the target unmanned aerial vehicles market size in 2024, whereas short-range systems are set to grow at an 8.35% CAGR.

- By mode of operation, remotely piloted systems held a 64.78% share in 2024, yet autonomous platforms posted the fastest 10.74% CAGR as AI-enabled training became mainstream.

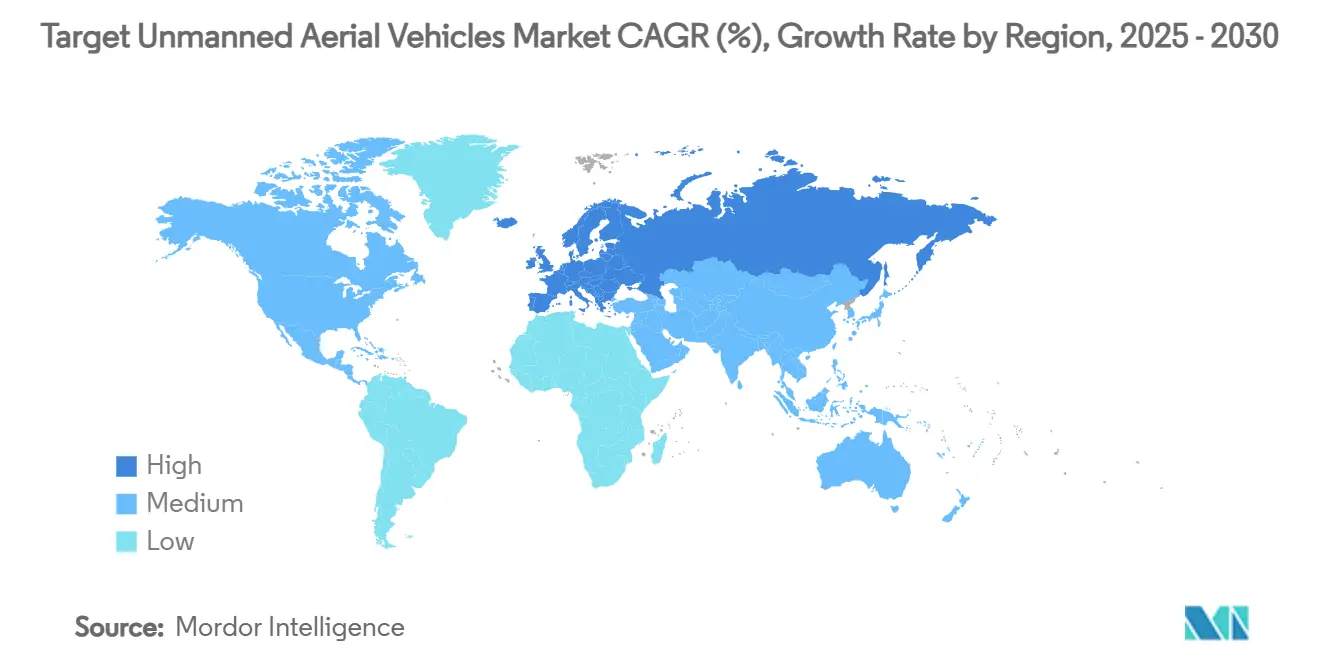

- By geography, North America dominated with a 41.54% share in 2024, while Europe is the fastest-growing region, with a 7.98% CAGR to 2030.

Global Target Unmanned Aerial Vehicles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in live-fire training exercises using high-speed aerial targets | +1.2% | Global, North America and Europe | Medium term (2-4 years) |

| Growing defense budgets for realistic threat simulation | +1.8% | Global, strongest in APAC and Europe | Long term (≥ 4 years) |

| Increasing adoption of 5th-generation aircraft driving demand for stealth-capable targets | +1.1% | North America and EU, expanding to APAC | Long term (≥ 4 years) |

| Integration of expendable swarm target UAVs for counter-swarm training | +0.9% | Global, early NATO adoption | Medium term (2-4 years) |

| Shift toward SAR-signature replication via modular payload drones | +0.7% | North America and EU | Medium term (2-4 years) |

| Rising law-enforcement spending on counter-UAS target quadcopters | +0.4% | Global urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Live-Fire Training Exercises Using High-Speed Aerial Targets

Armed forces increasingly schedule live-fire drills that require expendable drones capable of sustaining supersonic flight envelopes and complex maneuver patterns. Recent US Navy orders for the BQM-177A highlight how high-speed targets replicate sea-skimming anti-ship missiles and compress training timelines by combining radar-signature modulation with electronic-warfare payloads. As peer competitors field faster anti-ship threats, navies demand drones that stress kinetic and soft-kill layers of shipboard defense. Therefore, the Target unmanned aerial vehicle market shows sustained preference for platforms exceeding Mach 0.95, with vertically integrated suppliers able to deliver both airframe and command-and-control systems. Countries lacking indigenous jet-powered solutions increasingly rely on US Foreign Military Sales channels, creating incremental export opportunities for compliant manufacturers.

Growing Defense Budgets for Realistic Threat Simulation

NATO pledges to meet the 2%-of-GDP defense-spending benchmark and the Indo-Pacific rearmament cycle, injecting steady procurement funding into advanced target programs. The US FY 2024 budget alone earmarks USD 32.7 million for fifth-generation aerial targets to replicate low-observable adversaries.[2]Source: Congressional Research Service, “Aerial Targets,” congress.gov Many Asia-Pacific nations are following suit as regional missile inventories proliferate. Buyers now favor multi-year, lot-purchase contracts that amortize development costs and ensure logistic pipelines for spares. This budget stability enables suppliers to expand automated assembly lines, accelerating deliveries for the target unmanned aerial vehicles market and lowering per-unit flyaway costs.

Increasing Adoption of 5th-Generation Aircraft Driving Demand for Stealth-Capable Targets

The expanding global fleet of F-35 and analogous stealth fighters forces air-defense units to train against very low radar cross-sections. Kratos’s 5GAT program, recently green-lighted for additional flight testing, offers a drone with signature management tailored to X- and Ku-band radars. Air forces increasingly specify drones capable of variable-RCS modes, allowing operators to rehearse detection thresholds under changing threat envelopes. These drones also serve radar-calibration roles, and project offices bundle acquisition budgets across flight tests and training directorates, raising total addressable demand inside the target unmanned aerial vehicles market.

Integration of Expendable Swarm Target UAVs for Counter-Swarm Training

Emerging doctrines envision adversaries deploying dozens of inexpensive quadcopters to saturate critical infrastructure, prompting militaries to rehearse multi-vector engagements. The government Small-Business Innovation Research awards fund swarming-logic algorithms that mimic cooperative behaviors such as waypoint sharing and dynamic task allocation.[3]Source: U.S. Small Business Administration, “SBIR Phase II Awards,” sbir.gov Target providers respond by packaging multiple micro-UAVs with a mothership launcher that controls release timing. This approach enables realistic training for layered air-defense units that prioritize threats while managing ammunition expenditure. Swarm-capable targets thus open a new revenue stream within the target unmanned aerial vehicles market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procurement and operating cost of jet-powered targets | -0.8% | Global, acute in budget-constrained markets | Short term (≤ 2 years) |

| Stringent export controls (e.g., MTCR Cat-I) | -1.1% | Global, limiting emerging markets | Long term (≥ 4 years) |

| RF-spectrum congestion in multi-drone sorties | -0.6% | Global, dense training areas | Medium term (2-4 years) |

| Environmental concerns over range debris and approvals | -0.4% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Procurement and Operating Cost of Jet-Powered Target

Flyaway prices for full-scale converted fighters such as the QF-16 approach USD 3 million, and total ownership costs climb once maintenance crews, spares, and fuel logistics are tallied. RAND studies of historical aerial-target programs show sustainment spending exceeding 60% of program outlays over a five-year window. Operators in Eastern Europe and South America have deferred live-fire drills or substituted lower-speed piston-engine drones, creating an adoption gap. Manufacturers attempt to blunt sticker shock with power-by-the-hour options; however, the cash-flow profile still deters fiscally constrained customers and trims near-term growth for the target unmanned aerial vehicles market.

Stringent Export Controls Under MTCR Category I Classifications

Platforms capable of 300 km range or carrying payloads above 500 kg fall under MTCR Cat I rules, triggering rigorous government-to-government licensing. Approval cycles typically run 12-18 months, elongating sales funnels and discouraging smaller buyers who lack political clout. Several suppliers create de-rated export variants to bypass constraints, but adding engineering overhead inflates unit prices. These barriers fragment global supply and slow the diffusion of advanced targets, subtracting up to 1.1 percentage points from potential CAGR across the target unmanned aerial vehicles market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Maritime Targets Drive Diversification

Marine target UAVs are forecasted to deliver an 8.78% CAGR through 2030, the highest among all platforms. Naval forces value these drones for anti-ship missile defense rehearsals requiring low-altitude, sea-skimming profiles that are impossible to replicate with legacy aerial targets. In contrast, Aerial target UAVs retained a 63.45% share of the target unmanned aerial vehicles market in 2024, underpinned by more than two decades of standardized procurement cycles. The maritime surge parallels an uptick in contested-water deployments, prompting fleets to invest in Mach 2-plus supersonic demonstrators that trigger ship-borne radars at realistic detection ranges.

The segment’s breadth spans small remote-controlled speedboats for close-in weapon-system calibration to large, jet-powered missile simulators such as the GQM-163A. Suppliers are expanding modular payload bays that let a single hull mimic radar, infrared, or electromagnetic profiles, thereby improving return-on-investment for tight naval budgets. Platform diversification encourages cross-domain bundling, where air arms and navies co-fund joint target packages, helping sustain the overall growth path of the target unmanned aerial vehicles market.

By Engine Type: Electric Propulsion Gains Momentum

Electric and hybrid‐electric platforms are projected to record a 10.30% CAGR, outperforming all other power plants. Reduced fuel logistics, quieter signatures for urban test sites, and lower thermal emissions align with military decarbonization mandates. Turbojet engines held 44.70% of the target unmanned aerial vehicles market size in 2024, a testament to their indispensable role in supersonic and high-g maneuver simulations. Turbojet suppliers leverage commonality with commercial small-engine lines to protect margins, even as battery technology encroaches on lower-speed mission sets.

Hybrid architectures combine a small turbine with battery buffers, producing quick acceleration at take-off, followed by silent cruise modes ideal for SAR-signature testing. Experimental programs report endurance gains of 25% compared with pure jet counterparts, drawing attention from range operators who aim to cut sortie-turnover delays. Once certification frameworks mature, electric propulsion is expected to permeate short-range and medium-range segments, further broadening the target unmanned aerial vehicles market.

By Application: Target Acquisition Accelerates

Target acquisition platforms are forecasted to expand at a 9.24% CAGR as precision-guided munitions proliferate across modern inventories. Sensor manufacturers insist on rigorous calibration campaigns where drones tow radar reflectors, laser retro-reflectors, or electronic-countermeasure pods. Combat Training still occupied the largest 5.72% share in 2024, fueled by standing missile-qualification requirements at gunnery schools. However, acquisition-oriented programs increasingly bundle live-fire evaluations with data-capture suites, enabling after-action review and algorithm refinement.

Demand also rises for drones that emulate the electronic emission fingerprints of adversary ground radars, allowing aircrews to practice suppressing enemy air defense tactics in controlled environments. These specialized missions often reuse standard airframes with mission-specific pods, boosting platform utilization and cost efficiency within the target unmanned aerial vehicles industry.

By Range: Short-Range Systems Gain Traction

Short-range drones operating within 50 km are set to grow at an 8.35% CAGR because they require smaller danger zones, shorter regulatory approvals, and lower unit costs. Medium-range assets dominated, however, with 49.10% of the target unmanned aerial vehicles market share in 2024, as distances between launch site and impact area must replicate missile-flight timelines for naval and ground-based interceptors. The current procurement trend favors transportable launchers that a two-person crew can set up in under 30 minutes, supporting distributed training doctrines.

Long-range targets beyond 300 km remain indispensable for strategic missile-defense rehearsals; however, their logistical footprint and telecommand requirements restrict sortie rates. Advances in hot-swappable avionics help narrow the cost differential between range classes, encouraging users to maintain mixed fleets that can flex across mission types without expanding overall inventory size.

By Mode of Operation: Autonomous Systems Accelerate

Autonomous target drones are projected to post a 10.74% CAGR, propelled by AI-enabled flight-control stacks that reduce operator headcount and latency. Remotely piloted systems still held a 64.78% share in 2024, reflecting decades of established ground-station infrastructure. Autonomy first penetrates swarm-training packages, where a single operator oversees a dozen cooperating drones that present staggered threat vectors.

Safety regulators previously capped autonomous sorties, yet real-time geo-fencing and adaptive collision-avoidance algorithms have demonstrated reliability in constrained test corridors. This technology unlocks scalable scenarios that would overwhelm manual pilots, enhancing defender decision-making under saturation conditions and further enlarging the target unmanned aerial vehicles market.

Geography Analysis

North America controlled 41.54% of the target unmanned aerial vehicles market in 2024, driven by the US Navy’s Supersonic Aerial Target and the Air Force’s QF-16 programs that secure predictable production ramps. Mature test ranges, streamlined regulatory waivers, and a dense contractor ecosystem accelerate prototype-to-field transitions. Budget certainty allows range operators to schedule complex exercises months in advance, supporting sustained throughput for suppliers.

Europe is the fastest-growing territory, projected at a 7.98% CAGR, as collective defense budgets rise in response to evolving regional threats. Nations such as Germany, France, and the United Kingdom co-fund cross-border initiatives to develop indigenous electric and hybrid target variants, aligning with the European Union’s environmental objectives. Baltic and Nordic states also procure low-observable drones to practice integrated air-and-missile defense, expanding addressable volumes for the target unmanned aerial vehicles market.

Asia-Pacific defense ministries allocate significant spending to indigenous UAV programs, with India alone budgeting USD 415.9 billion through 2029 for broad modernization that includes target training infrastructure. China’s rapid advance in autonomous swarm concepts spurs neighboring countries to accelerate counter-swarm readiness, lifting regional demand for expendable micro-targets. Australia and Japan focus on integrating range telemetry with allied target inventories, ensuring interoperability for multinational exercises that underpin security-pact obligations.

Competitive Landscape

The target unmanned aerial vehicles market exhibits moderate consolidation. Kratos Defense’s USD 77 million acquisition of Sierra Technical Services pools stealth-target intellectual property with high-rate production lines, positioning the firm to bid on fifth-generation requirement sets without external teaming. AeroVironment’s USD 4.1 billion purchase of BlueHalo extends its unmanned portfolio into high-endurance target drones and complementary ground-radar simulations. Redwire Corporation’s acquisition of Edge Autonomy underscores investor appetite for vertically integrated autonomy stacks that span flight controllers to space-based data-links.

Incumbents continue to pursue long-term IDIQ contracts that lock in volume and block market entry. However, smaller challengers specialize in swarm logic, AI-driven flight management, and battery-energy architectures, carving out defensible niches. Patent-landscape analyses show rising filings in distributed autonomy and RCS-shaping technologies, indicating future competitive battlegrounds. Export-compliance proficiency and the ability to field Cat II variants quickly remain critical differentiators as MTCR constraints tighten.

Target Unmanned Aerial Vehicles Industry Leaders

Northrop Grumman Corporation

Kratos Defense and Security Solutions, Inc.

The Boeing Company

QinetiQ Group

Leonardo S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Boeing secured a USD 10.2 million contract modification from the US Air Force, emphasizing its continued role in producing QF-16 full-scale aerial targets for advanced training and operational testing.

- January 2025: QinetiQ Target Systems (QTS) Canada, through prime contractor Canadian Commercial Corporation (CCC), secured a sole-sourced contract to deliver unmanned aerial target (UAV-T) support services to the US Government. This contract highlights QTS Canada's expertise in providing advanced UAV-T solutions, reinforcing its position as a trusted partner for defense-related services in the North American market.

Global Target Unmanned Aerial Vehicles Market Report Scope

| Aerial Target UAVs |

| Marine Target UAVs |

| Ground Target UAVs |

| Turbojet |

| Internal Combustion (Piston) |

| Electric/Hybrid |

| Combat Training |

| Target and Decoy |

| Target Identification |

| Target Acquisition |

| Short-Range (Less than 50 km) |

| Medium-Range (50–300 km) |

| Long-Range (More than 300 km) |

| Remotely Piloted |

| Autonomous |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Platform | Aerial Target UAVs | ||

| Marine Target UAVs | |||

| Ground Target UAVs | |||

| By Engine Type | Turbojet | ||

| Internal Combustion (Piston) | |||

| Electric/Hybrid | |||

| By Application | Combat Training | ||

| Target and Decoy | |||

| Target Identification | |||

| Target Acquisition | |||

| By Range | Short-Range (Less than 50 km) | ||

| Medium-Range (50–300 km) | |||

| Long-Range (More than 300 km) | |||

| By Mode of Operation | Remotely Piloted | ||

| Autonomous | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the target unmanned aerial vehicles market?

The market is valued at USD 5.94 billion in 2025, with a forecast to reach USD 8.47 billion by 2030, translating to a 7.35% CAGR.

Which platform segment is growing the fastest?

Marine target UAVs post the highest 8.78% CAGR as navies prioritize realistic anti-ship missile defense training.

Why are electric and hybrid engines gaining traction?

Electric propulsion lowers fuel logistics, cuts acoustic signatures and aligns with military sustainability mandates, resulting in a projected 10.30% CAGR for the segment.

What regions lead demand growth?

North America holds the largest share, but Europe registers the fastest regional CAGR at 7.98% due to increased NATO spending.

How will autonomy influence future target drones?

Autonomous platforms are predicted to expand at 10.74% CAGR, enabling swarm scenarios that manual operators cannot manage efficiently.

Page last updated on: