Small Gas Engines Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.83 Billion |

| Market Size (2031) | USD 4.96 Billion |

| Growth Rate (2026 - 2031) | 5.32% CAGR |

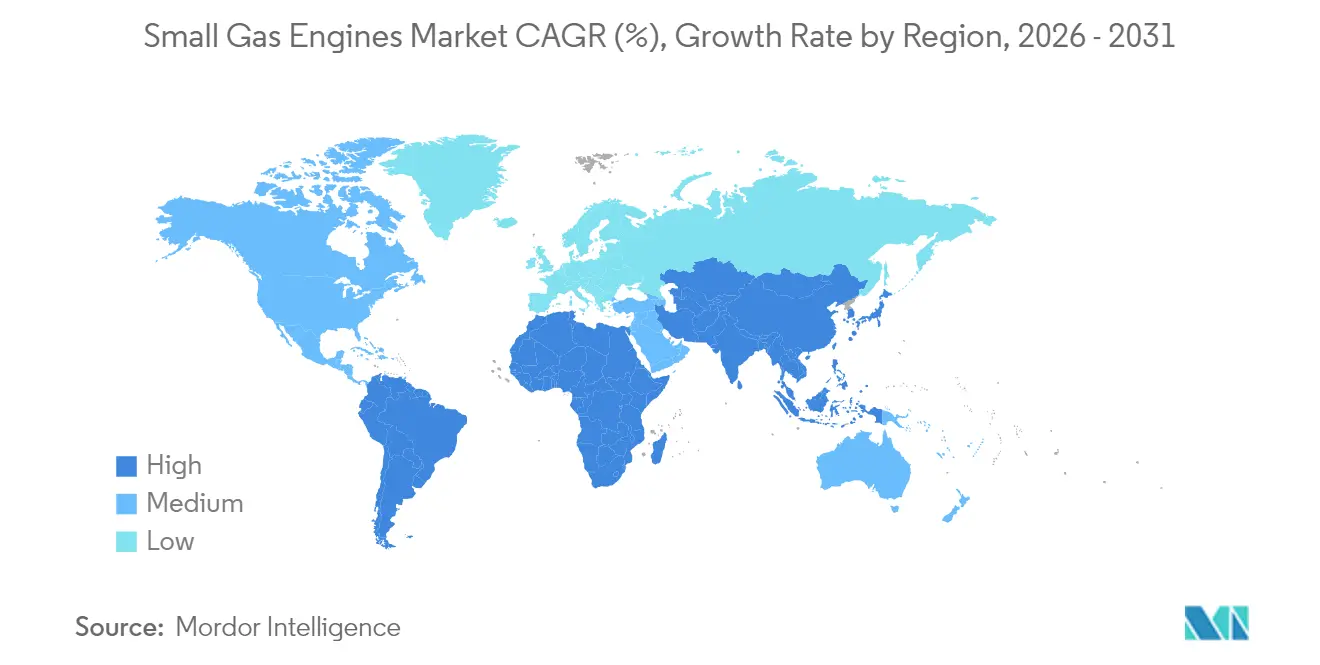

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Small Gas Engines Market Analysis by Mordor Intelligence

Small Gas Engines Market size in 2026 is estimated at USD 3.83 billion, growing from 2025 value of USD 3.64 billion with 2031 projections showing USD 4.96 billion, growing at 5.32% CAGR over 2026-2031.

The small gas engine market continues to expand because efficiency upgrades, flexible fuel strategies, and niche power-density use-cases preserve combustion advantages even as electrification gains traction. Growth is reinforced by resilient residential lawn care spending, emergency power preparedness, and a multi-year rebound in compact equipment purchases across emerging economies. Competitive intensity rises as leading manufacturers add electronic fuel-injection and telematics to prolong the appeal of gasoline powertrains while allocating capital to battery platforms for lower-displacement tools. Tariff actions on Chinese equipment and the tightening of Stage V and CARB Tier 5 standards are reshaping supply chains by rewarding domestic production footprints and promoting vertically integrated component sourcing. Players who can localize manufacturing, optimize after-treatment architectures, and leverage omnichannel dealer networks capture an outsized share, even under margin pressure.

Key Report Takeaways

- By engine displacement, the 101 to 400 cc segment led with 46.30% of the small gas engine market share in 2025, while the 20 to 100 cc category is projected to expand at a 6.12% CAGR through 2031.

- By equipment type, lawnmowers accounted for 35.10% of 2025 revenue; portable generators are forecast to register the fastest growth rate of 6.67% CAGR to 2031.

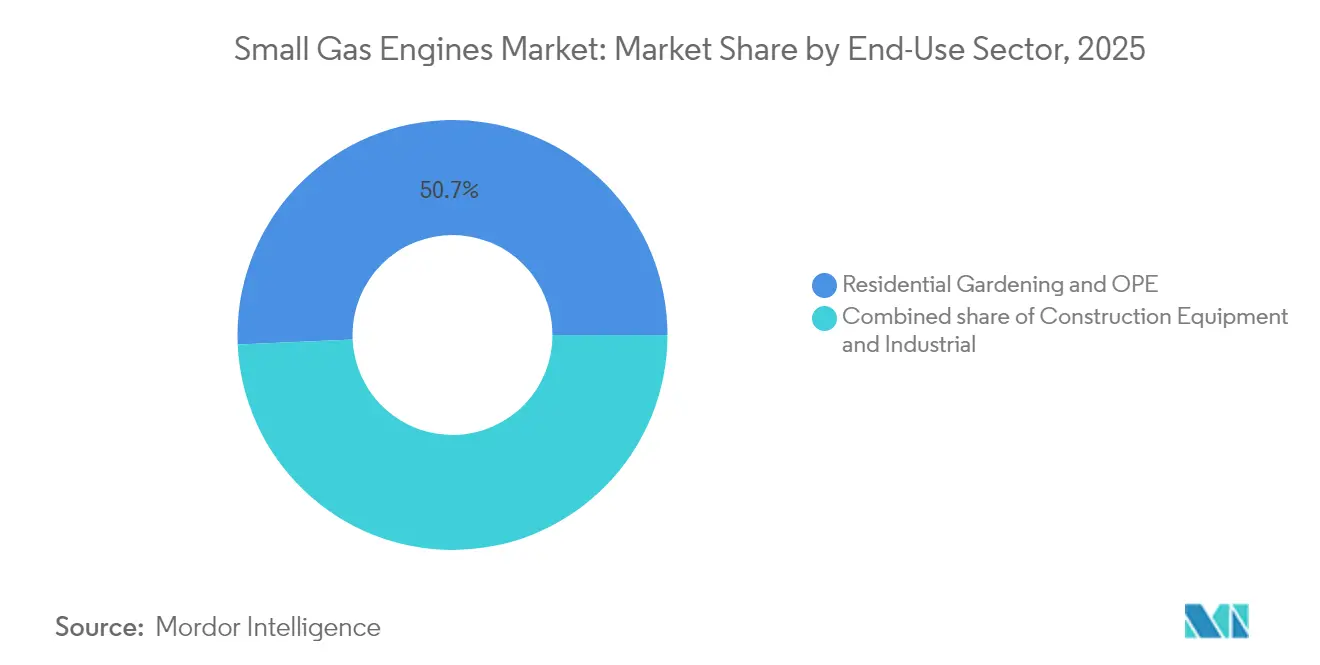

- By end-use sector, residential gardening and outdoor power equipment contributed 50.70% of 2025 sales, whereas construction equipment is set to rise at a 6.52% CAGR over the outlook.

- By geography, North America accounted for 41.60% of 2025 revenue; the Asia-Pacific region is anticipated to grow at a 7.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Small Gas Engines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic DIY & lawn-care boom fuels OPE engine demand | 1.20% | North America & Europe | Medium term (2-4 years) |

| Extreme-weather-driven rise in portable-generator purchases | 1.80% | Global, concentrated in North America | Short term (≤ 2 years) |

| Emerging-market construction rebound (2025-2028) | 1.40% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| DIY "repower" kits lengthen equipment life cycles | 0.60% | North America & Europe | Long term (≥ 4 years) |

| Gas powertrains replacing small diesels in UTV/compact equipment | 0.80% | Global | Medium term (2-4 years) |

| Off-grid recreational power surge (RV & camping) | 0.50% | North America, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-pandemic DIY & Lawn-Care Boom Fuels OPE Engine Demand

The home-improvement enthusiasm that began in 2024 endures as homeowners position lawn maintenance as a recurring hobby and a property value enhancer. Sales of push and ride-on mowers with mid-range 101-400 cc engines remain elevated as suburban consumers replace their ageing fleets sooner than historical norms. Dealer surveys indicate spring stockouts of 14-21 days for key mower models, suggesting a persistent backlog despite the normalization of supply chains. Professional landscaping firms simultaneously report higher equipment turnover because tighter labor markets make reliability critical. Briggs & Stratton’s relocation of V-Twin Vanguard production from Japan to Georgia and Alabama underscores confidence that North American demand will remain structurally higher over the medium term.[1]Briggs & Stratton, “Vanguard V-Twin Production Shift Announcement,” briggsandstratton.com

Extreme-Weather-Driven Rise in Portable-Generator Purchases

Grid disruptions totaled 1.2 billion outage hours during the first nine months of 2024, driving the adoption of portable generators beyond traditional hurricane and wildfire seasons. Consumers now purchase small gas generator sets throughout the calendar year, compressing replenishment cycles for distributors. Generac posted a 28% surge in Q4 2024 residential generator revenue and lifted shipment guidance three times over the year.[2] Generac Holdings, “Q4 2024 Earnings Presentation,” generac.com NOAA’s La Niña outlook for the 2024-2025 winter signals further weather-linked demand spikes, strengthening the small gas engine market as households and small businesses prioritize immediate refueling ease over battery runtime limits.

Emerging-Market Construction Rebound (2025-2028)

Public works budgets in India, Indonesia, and Gulf Cooperation Council nations underpin a sustained modernization wave in compact excavators, site pumps, and concrete screeds, where engines with displacements of 101-650 cc dominate. Kubota has committed to a 40% capacity expansion for mini excavators in Zweibrücken, Germany, specifically citing export demand to Asia and the Middle East. Industry forecasts indicate that construction value-added is expected to expand at a 4% CAGR across developing economies, providing multi-year visibility to powertrain suppliers that localize casting and machining operations regionally.

Gas Powertrains Replacing Small Diesels in UTV/Compact Equipment

Stricter particulate and NOx thresholds are driving OEMs to switch from sub-25 hp diesel engines to advanced gasoline platforms with closed-loop fuel injection. Honda’s iGX400 and iGX430 launch illustrates how torque curves once exclusive to diesel engines are now achievable through electronic governor control and optimized combustion.[3]Honda Motor Co., “iGX Series Engine Specifications,” honda.com Operators save on diesel after-treatment servicing, especially in regions where fuel sulfur content complicates filter regeneration. This substitution expands the addressable market for small gas engines in turf utility vehicles, mini skid-steers, and entry-level construction equipment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stage V / CARB Tier-5 emission compliance costs | -1.1% | Global, concentrated in North America & EU | Medium term (2-4 years) |

| Rapid shift to battery-powered OPE in mature economies | -0.9% | North America & Europe | Long term (≥ 4 years) |

| Tariffs on Chinese lawn & garden equipment inflate prices | -0.6% | North America, spill-over to global supply chains | Short term (≤ 2 years) |

| Shortage of certified small-engine technicians globally | -0.4% | Global, acute in North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stage V / CARB Tier-5 Emission Compliance Costs

Upcoming Tier-5 regulations mandate 90% NOx and up to 75% particulate cuts for compact engines beginning in 2029, raising certification expenses and compelling costlier materials such as coated substrates and electronic diagnostics.[4]California Air Resources Board, “Proposed Tier 5 Rulemaking Outline,” arb.ca.gov Smaller brands lacking in-house test cells and software calibration teams confront disproportionate per-unit compliance costs, prompting either exit or strategic licensing. Kohler’s USD 6 million settlement with CARB in 2020 over defeat-device allegations signals increasing enforcement scrutiny and underscores the financial exposure associated with non-compliance. These factors consolidate volume around players able to amortize R&D across multi-fuel portfolios.

Rapid Shift to Battery-Powered OPE in Mature Economies

Battery cost per watt-hour declined 12% between 2023 and 2024, helping cordless chainsaws, trimmers, and blowers reach use-time parity for most suburban tasks. STIHL has invested USD 60 million to expand battery-pack production at its Virginia campus and aims for battery models to account for 80% of total units by 2035. Fleet landscapers adopt 56V ecosystems to meet municipal noise ordinances, eroding demand for 20-100cc engines in handheld segments. Although high-ampere-hour backpack batteries struggle in rain and extended runtime scenarios, the substitution rate nevertheless restrains combustion volumes across Northern Europe and parts of North America.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Engine Displacement: Mid-Range Versatility Sustains Leadership

The 101-400 cc bracket retained 46.30% of 2025 revenue as the category underpins walk-behind mowers, portable generators, and compact site equipment where balanced power-to-weight remains essential. This slice of the small gas engine market benefits from mature supply chains that keep per-unit costs low even after adding electronic throttle bodies and oxygen sensors. OEMs prioritize this range for R&D because electrification advances have yet to deliver equivalent torque and refill speed under heavy load profiles spanning five or more hours of continuous operation. Honda’s iGX-series fuel-injection roll-out illustrates how combustion refinement extends engine relevance amid tightening standards.

The 20-100 cc tier, while contributing a more modest share, is projected to compound at 6.12% through 2031, the fastest inside the small gas engine market. Growth hinges on heightened demand for light portable inverter generators and emerging-market uptake of micro-tillers and backpack sprayers. This category also feels the strongest battery encroachment, which prompts engine makers to emphasize quick-start systems, ethanol-compatible carburetors, and cost-effective catalyst packages. In contrast, the 401-650 cc range caters to commercial zero-turn mowers and standby generators, where higher ticket prices help offset compliance-system costs, preserving positive margins even under stricter standards.

By Equipment Type: Generator Momentum Outpaces Lawn-Care Mainstay

Lawnmowers generated 35.10% of 2025 revenue, primarily driven by the United States, Canada, Germany, and Australia, where large plot sizes often favor combustion over battery runtime limitations. Unit replacement intervals shortened from six to five seasons as homeowners sought quieter deck designs and variable-speed drives. Meanwhile, portable generators are expected to register the highest 6.67% CAGR, driven by climate-induced outages and increasing recreational vehicle penetration. Generac’s Guardian 26 kW launch demonstrated a 28% increase in starting power while fitting within an air-cooled footprint, thereby enlarging consumer confidence in gasoline standby solutions.

Chainsaws, trimmers, and blowers experience divergent trajectories as municipalities tighten decibel caps; nonetheless, gas-powered units maintain a presence in forestry and rural markets, where service stations outnumber charging stations. Pressure washers face tariff-related input inflation after the U.S. Department of Commerce imposed combined margins of up to 274.37% on Chinese models in 2024. Domestic assemblers are pivoting to vertically integrated pump casting and engine machining within North America to regain cost competitiveness.

By End-Use Sector: Construction Applications Accelerate

Residential gardening and outdoor power equipment delivered 50.70% of 2025 revenue, fueled by continued suburban home ownership and property-value focus. Replacement of dated 150-hour life engines with modern 250-hour variants enhances average selling prices and parts revenue. At the same time, construction equipment is expected to advance at a 6.52% CAGR as governments invest in roads, telecom towers, and transit hubs. Compact excavators, site mixers, and diaphragm pumps utilize engines with displacements ranging from 101 to 650 cc, which are lighter and less expensive than their diesel counterparts once after-treatment is factored in.

Industrial power applications, including welders, utility pumps, and light towers, provide a stable and cyclical revenue base. Gasoline engines thrive where decentralised work sites lack grid connectivity and where instantaneous refuel proves critical. Fleet operators are increasingly requiring telematics for run-hour logging and predictive maintenance, a feature set now integrated into Kohler’s Command PRO EFI lineup and Briggs & Stratton’s Vanguard 200 series.

Geography Analysis

North American demand continues to hinge on property size, emergency preparedness, and entrenched consumer preference for immediate refueling convenience. Small gas engines remain the power source of choice for 70% of new riding-mower sales despite rising cordless adoption in walk-behind categories. Grid instability, evidenced by a cumulative 1.2 billion outage hours logged during the first nine months of 2024, keeps portable-generator shelves thin year-round, prompting retailers to secure additional forward inventory. OEM adherence to EPA Phase III evaporative standards raises component cost but tightens quality, reinforcing domestic brand loyalty. CARB Tier-5 proposals, when finalized, will likely compel additional evaporative-emission canister capacity and durability warranties, favoring larger incumbents that can amortize compliance engineering across multiple power classes.

Asia-Pacific’s role as the fastest-growing region intensifies as construction ministries commit to multi-year urban rail, road, and airport modernization plans. Gasoline engines claim share from small diesels in mini excavators and site generators because import duties on after-treatment hardware inflate diesel total cost of ownership. Middle-class yard ownership expands in peri-urban China, India, and Thailand, raising shipments of rotary mowers and trimmers fitted with 125-160 cc engines. Domestic component localization programs, such as India’s Production-Linked Incentive scheme for machinery, catalyze crankshaft forging and cylinder-block casting capacity, anchoring regional supply chains and reducing lead times from 90 to 45 days. Generac’s Indian joint venture expects to grow assembly output by 35% annually through 2027, underscoring the strategic importance of local presence.

Europe records lower absolute unit volumes yet exerts outsized regulatory influence because Stage V limits have become the template for forthcoming rules elsewhere. STIHL’s German battery cell expansion aims to shift one-quarter of handheld tool production to cordless formats by 2027, but high-powered zero-turn mowers and hill-climb forestry winches still rely on gasoline engines. Government subsidies for zero-emission landscaping converge with municipality noise bylaws, accelerating combustion displacement in urban cores. However, rural municipalities and alpine regions continue purchasing gas-powered snowblowers and stump grinders where battery energy density remains inadequate. Currency fluctuations between EUR and USD tighten European OEM margins when sourcing aluminum castings from outside the bloc, prompting more in-region smelter contracts.

Competitive Landscape

Briggs & Stratton, Honda, Kohler, Generac, Yamaha, Kawasaki, STIHL, and Kubota collectively accounted for an estimated 62% of 2024 revenue, positioning the small gas engine market as moderately consolidated. Leadership relies on an integrated engine casting, component machining, and branded service network that together reduces warranty costs and accelerates field fixes. Product differentiation centers on electronic fuel injection, variable-timing ignition, and IoT diagnostics that feed engine-health data to dealer portals. Honda expanded its iGX platform to encompass 400 cc and 430 cc displacements, featuring electronic governor technology that mimics the torque curves of small diesel engines while maintaining a total engine mass of under 40 kg. Kohler’s spin-out as Rehl, following its acquisition by Platinum Equity, earmarks capital for EFI uptake in its Command PRO series, aligning with municipal emission proposals in North America and Europe.

Strategic partnerships demonstrate how incumbents are preparing for zero-carbon combustion. Yamaha unveiled a 200-hp hydrogen outboard and has begun bench integration of direct-injection hydrogen injectors on single-cylinder prototypes. Kawasaki achieved a world-record 48.5% thermal efficiency in its Green Gas generator by adopting lean-burn combustion and ceramic-coated pistons. These initiatives safeguard long-cycle marine and stationary markets that value combustion refuel speed and existing liquid-fuel logistics. Generac, meanwhile, hedges against electrification by acquiring battery storage integrators, yet still attributes nearly 80% of its gross margin to combustion generators, signaling continued confidence in gasoline for standby use.

Tariff regimes and supply-chain security reshape sourcing. The 179-274% U.S. antidumping duties on Chinese pressure washers triggered OEM moves to reshore pump casting and to dual-source small engines from domestic plants in Missouri and Alabama. Players with inter-company crankshaft forges and plastic injection facilities achieve shorter production lead times, buffering against container volatility. Dealer financing programs expand to bundle engines, parts, and telematics subscriptions, locking in multi-year servicing revenue and discouraging brand switching. Overall, manufacturers that orchestrate a balanced strategy—squeezing incremental efficiency from gasoline platforms while funding hydrogen pilot lines and selective battery build-outs—retain competitive agility.

Small Gas Engines Industry Leaders

Briggs & Stratton Corp.

Honda Motor Co. Ltd.

Kohler Co.

Yamaha Motor Corp.

Generac Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Generac launched the Guardian 26 kW home standby generator, delivering 28% higher starting power than peer systems while occupying 68% less space than liquid-cooled alternatives.

- December 2024: Kubota disclosed plans to lift German mini-excavator capacity by 40% by 2028 and targets JPY 1 trillion in construction machinery sales.

- November 2024: Yamaha debuted the world’s first hydrogen-fueled outboard motor at SEMA 2024, developed with Roush and Regulator Marine and aiming for commercial launch by 2035.

- October 2024: Kohler Co. finalized the sale of Kohler Energy to Platinum Equity, rebranding the unit as Rehlko with a focus on home energy, industrial systems, and powertrain technologies.

Global Small Gas Engines Market Report Scope

The small gas engine market report includes:

| 20 to 100 cc |

| 101 to 400 cc |

| 401 to 650 cc |

| Lawnmower |

| Chainsaw/Trimmer/Blower |

| Portable Generator |

| Pressure Washer/Pump/Screed |

| Residential Gardening and OPE |

| Industrial (Portable Power, Pumps, Welding) |

| Construction Equipment |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Engine Displacement | 20 to 100 cc | |

| 101 to 400 cc | ||

| 401 to 650 cc | ||

| By Equipment Type | Lawnmower | |

| Chainsaw/Trimmer/Blower | ||

| Portable Generator | ||

| Pressure Washer/Pump/Screed | ||

| By End-Use Sector | Residential Gardening and OPE | |

| Industrial (Portable Power, Pumps, Welding) | ||

| Construction Equipment | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the global Small Gas Engines Market?

The market is valued at USD 3.83 billion in 2026 and is forecast to reach USD 4.96 billion by 2031.

What CAGR is expected for the Small Gas Engines Market through 2031?

The market is projected to advance at a 5.32% CAGR over the 2026-2031 period.

Which region is projected to grow fastest in the Small Gas Engines Market?

Asia-Pacific is set to expand at a 7.28% CAGR, the highest among all regions.

Which equipment type will drive the highest growth in

Portable generators are expected to post the fastest 6.67% CAGR through 2031.

How are emission regulations affecting small gas engine manufacturers?

Stage V and upcoming CARB Tier-5 rules increase certification costs and favor larger players able to spread R&D and compliance spending across broader portfolios.

Who are the leading companies in the small gas engine market?

Key participants include Briggs & Stratton, Honda, Kohler, Generac, Yamaha, Kawasaki, and Kubota.

Page last updated on: