Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

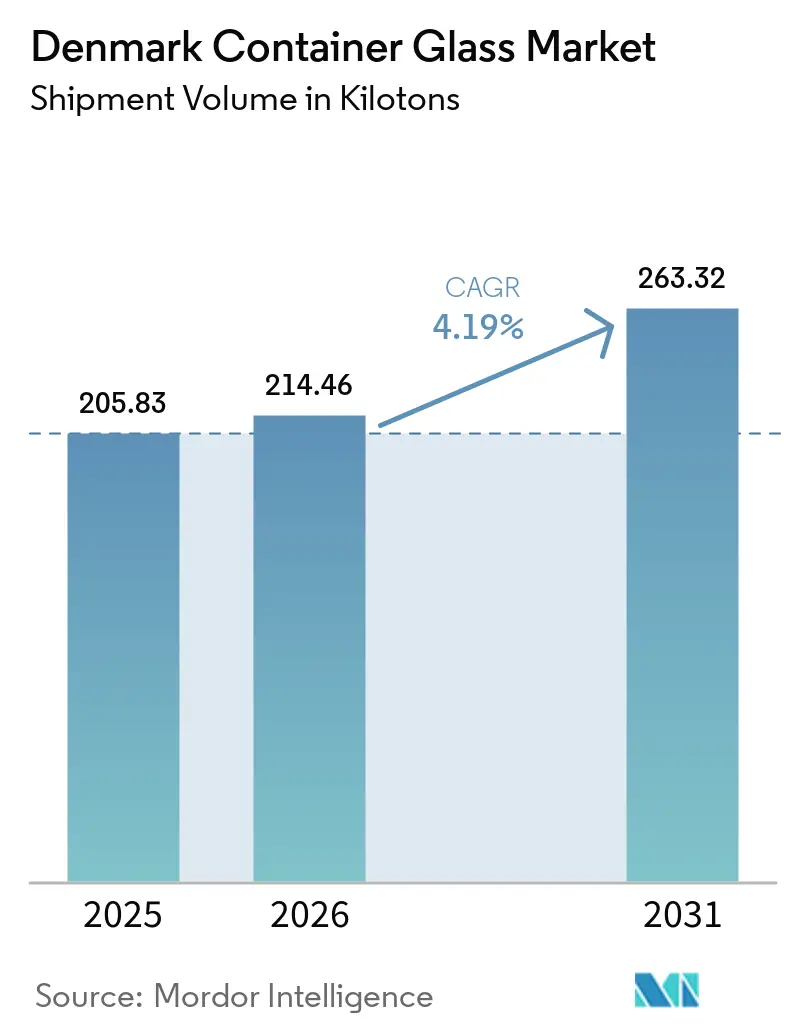

| Base Year Market Size (2025) | 205.83 kilotons |

| Market Volume (2026) | 214.46 kilotons |

| Market Volume (2031) | 263.32 kilotons |

| Growth Rate (2026 - 2031) | 4.19% CAGR |

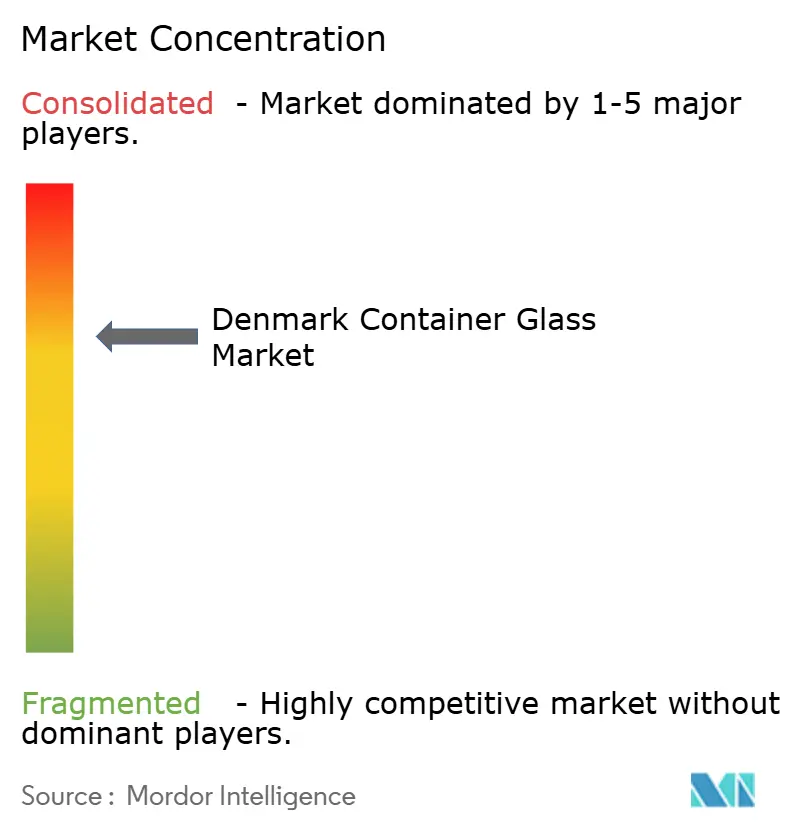

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Denmark Container Glass Market Analysis by Mordor Intelligence

The Denmark Container Glass Market size in terms of shipment volume is expected to grow from 205.83 kilotons in 2025 to 214.46 kilotons in 2026 and is forecast to reach 263.32 kilotons by 2031 at 4.19% CAGR over 2026-2031.

The market is being supported by a clear move away from plastic packaging as EU packaging rules and Denmark's own producer responsibility framework make recyclable formats more attractive to brand owners. Circular collection systems, refill activity, and strong glass recovery practices also give the market a practical base that many materials do not have to the same degree. Premium positioning across packaged goods continues to favor glass because it supports product protection, shelf visibility, and brand quality cues. At the same time, domestic production is concentrated in one Danish plant, so medium-term growth also depends on whether policy settings allow local supply to remain viable beside imports from broader Europe. This combination of regulatory support, premium demand, and supply-side tension gives the Denmark container glass market a steady but closely watched growth path.

Key Report Takeaways

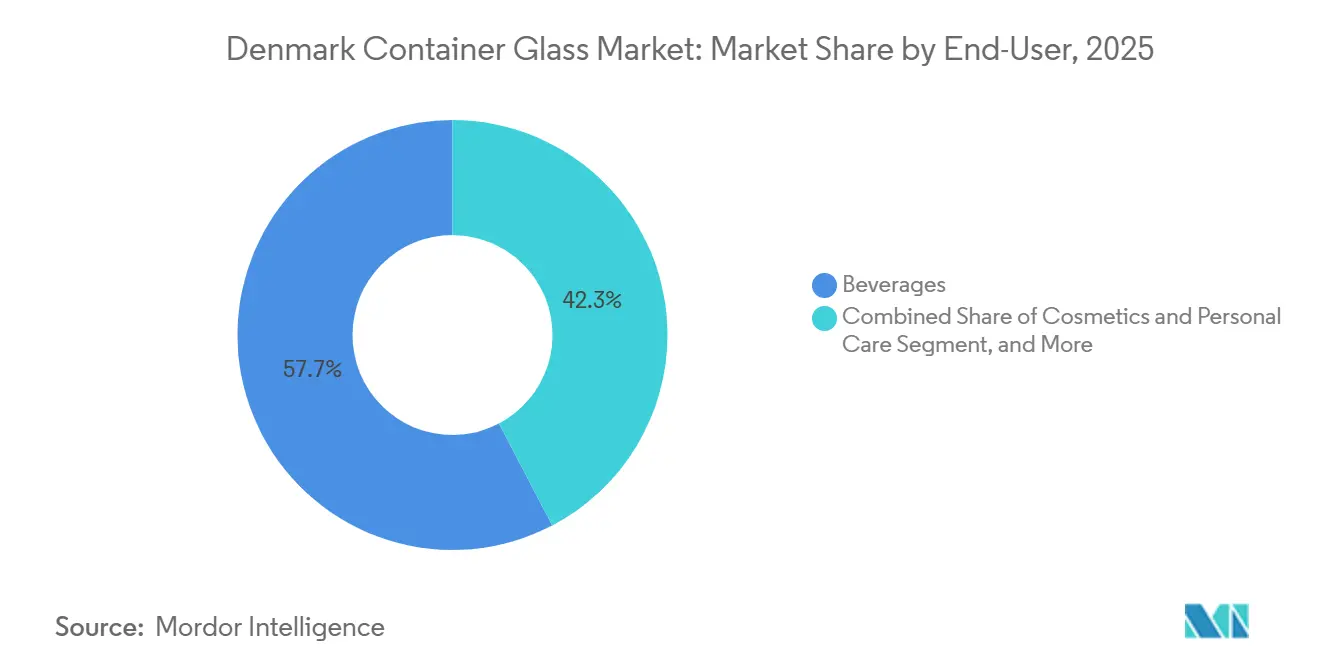

- By end-user, beverages held 57.68% share of the Denmark container glass market size in 2025, while perfumery is forecast to expand at a 6.80% CAGR through 2031.

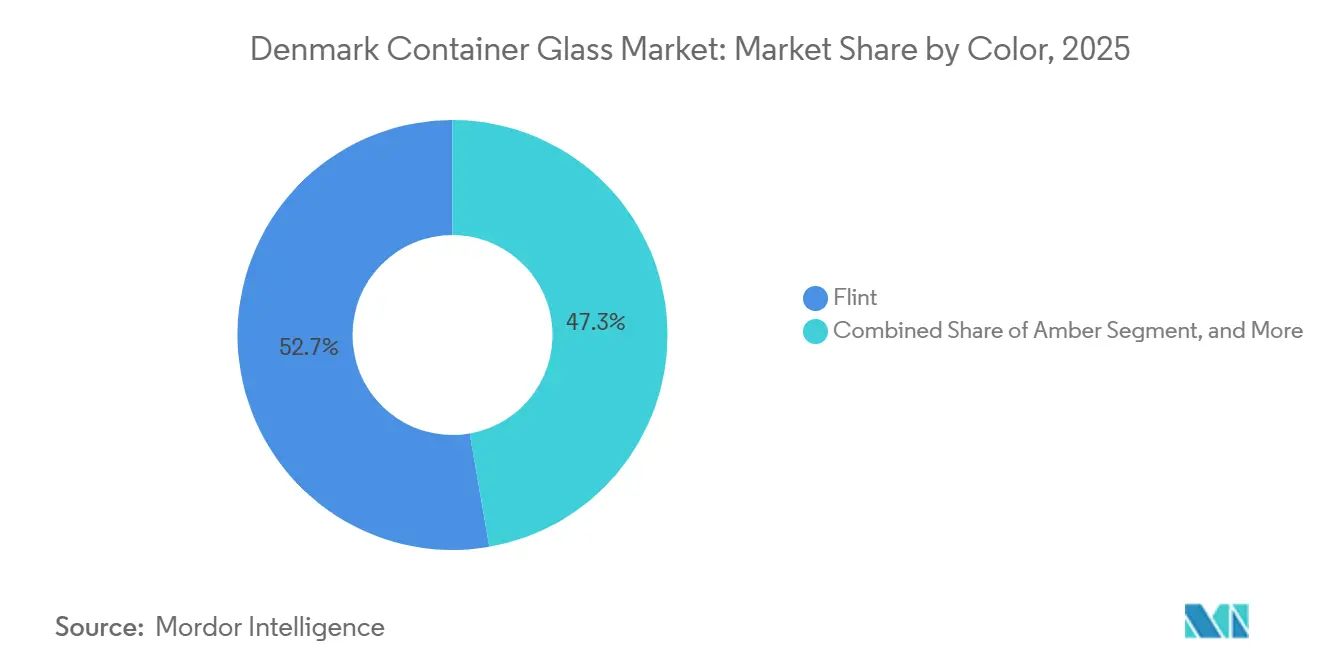

- By color, flint held 52.74% of the Denmark container glass market share in 2025, while amber is projected to record the fastest CAGR at 4.73% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Denmark Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand for Sustainable Packaging Solutions | +1.2% | Denmark and Nordic region broadly | Short term (≤ 2 years) |

| Stringent Government Regulations on Plastic Waste | +0.9% | EU-wide, with near-term effect on Denmark | Short term (≤ 2 years) |

| Consumer Preference for Eco-Friendly and Premium Products | +0.7% | Denmark, EU premium markets | Medium term (2-4 years) |

| Strong Emphasis on Circular Economy Practices | +0.5% | Denmark, with EU-wide reinforcement | Medium term (2-4 years) |

| Growth in End-Use Industries | +0.3% | Denmark domestic, spillover to Nordic exports | Medium term (2-4 years) |

| Favorable Government Incentives and Awareness Campaigns | +0.2% | Denmark national, with early gains in urban municipalities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Sustainable Packaging Solutions

Demand for more sustainable packaging has strengthened the role of glass across Danish packaged goods, especially where brand owners want a material that can be reused and remelted at scale. Ardagh Glass Holmegaard's Danish operation remains central to this system, with annual production of around 800 million bottles and containers from its Holmegaard site. In April 2025, VANA finalized treatment agreements covering around 125,000 tonnes of Danish glass and metal packaging, with a target of more than 95% reuse or recycling.[1]VANA, “Significant Quality Boost to the Danish Recycling of Glass and Metal,” VANA, vana.dk Those agreements also introduced a cascade model that sorts the best bottles for refill before the remaining material is sent to cullet production, which raises material value and reduces the burden of remelting alone. This matters because sustainability targets are now shaping procurement choices in practical terms, not just marketing claims, and glass benefits when buyers can connect packaging decisions to reuse and recycling outcomes. As a result, the Denmark container glass market continues to gain support where circularity has to be demonstrated in operating systems rather than promised in brand messaging.

Stringent Government Regulations on Plastic Waste

Regulation (EU) 2025/40 entered into force in the EU and began applying from August 12, 2026, which tightened the policy path for packaging waste and recyclability. The regulation will prohibit selected single-use plastic formats from January 2030 and requires all packaging placed on the market to be recyclable under defined performance conditions. In Denmark, the packaging EPR framework took effect on October 1, 2025, and the Ministry of Environment opened consultation in February 2026 on a model that would cut the glass handling fee by up to 30%. This showed that compliance rules are now influencing packaging economics directly, because fee design can shift the relative cost of glass against other materials. Brand owners and contract packers are therefore making longer-dated material choices with recyclability, refill potential, and fee exposure in mind. Taken together, these changes support the Denmark container glass market, where glass can serve as a direct response to rising regulatory pressure on problematic plastic formats.

Consumer Preference for Eco-Friendly and Premium Products

Consumer preference in higher-income Nordic markets still favors glass in categories where authenticity, product protection, and premium shelf presence matter. Gerresheimer's 2024 annual report pointed to stronger momentum in fragrance than in the broader beauty market through 2028, which supports higher packaging demand in premium personal care formats. That pattern helps explain why perfumery is the fastest-growing end-user stream in the Denmark container glass market over the forecast period. Vetropack's 2025 reporting also showed that brown glass achieved 77% average recycled content across its European operations, while flint glass remained at 40-41%, which highlights the practical balance between premium appearance and recycled-content targets. For Danish buyers, this means product design and sustainability objectives do not always point to the same color choice, especially when clear packaging is part of brand positioning. The Denmark container glass market therefore, benefits from premiumization, but it also has to work within the design limits that premium brands place on recycled-content adoption.

Strong Emphasis on Circular Economy Practices

Denmark's glass packaging system is supported by an established circular setup that combines deposit collection, refill logic, and remelting into new containers. Dansk Retursystem stated that 33,000 tonnes of deposit glass bottles were remelted into new containers at Ardagh Holmegaard in 2024.[2]Dansk Retursystem, “Glasflasker Er Værdifulde Råstoffer Til Nye Flasker,” Dansk Retursystem, danskretursystem.dk VANA's 2025 agreements added cascade sorting, which sends the best bottles toward direct refill and channels the remainder into cullet production for new glass. This aligns well with the EU's broader reuse and recyclability direction under Regulation (EU) 2025/40, where reusable beverage packaging will take on greater importance over time. The operating value of this system is that it supports both direct reuse and closed-loop recycling, which improves the case for suppliers that can serve refill programs and high-quality cullet streams. That gives the Denmark container glass market a structural advantage in circular packaging execution, not only in policy alignment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Manufacturing Costs and Energy Consumption | -1.0% | Denmark, EU container glass producers | Short term (≤ 2 years) |

| Persistent Competition from Plastic Packaging | -0.7% | Denmark domestic retail and food service | Medium term (2-4 years) |

| Fragility and Heaviness of Glass Containers | -0.4% | Global logistics, most acute in e-commerce | Long term (≥ 4 years) |

| Limited Availability of Raw Materials | -0.3% | Denmark (cullet), global (silica, soda ash) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Manufacturing Costs and Energy Consumption

Container glass production requires furnaces to run continuously at very high temperatures, which keeps the cost base exposed to energy volatility and margin pressure. O-I Glass said in its 2025 Form 10-K that it expected a USD 150 million increase in European energy costs in 2026 as legacy contracts expired. In Denmark, the Ministry of Environment stated that the fee structure on glass packaging had created enough pressure to contribute to the closure of 2 of 6 lines at Ardagh Holmegaard. That combination of energy intensity and policy-driven cost pressure reduces pricing flexibility for domestic producers and raises the risk of greater dependence on imports. Producers are responding through furnace modernization, lightweighting, and operational restructuring, but those measures take time and capital to scale. Until those responses translate into lower unit costs more widely, cost inflation will remain a clear restraint on the Denmark container glass market.

Persistent Competition from Plastic Packaging

Plastic continues to compete strongly in parts of food service, dairy, and mainstream beverage packaging because it is lighter and often cheaper to handle. The cost gap narrows when recyclability rules, refill requirements, and fee structures are added to the comparison, but it does not disappear across every end use. Denmark's recent fee debate showed that poorly calibrated eco-modulation can weaken glass's position instead of strengthening it, which is why the proposed fee reduction became so important. Alternative materials are also improving their barrier properties, convenience, and sustainability claims, which means glass still has to win on both function and economics. The Denmark container glass market is therefore likely to gain share in selected premium and regulated applications, while lower-cost plastic and other lightweight formats remain difficult to displace in broader mass-market uses. This restraint does not stop market growth, but it does limit how far and how fast glass conversion can spread.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Premiumization And Perfumery Reshape Demand Mix

Beverages accounted for 57.68% of total volume in 2025 and remained the largest end-user base within the Denmark container glass market. Ardagh Holmegaard's core output includes wine bottles, beer bottles, spirits packaging, and food jars, with around 80% of production directed to the Danish market. That structure keeps beverage demand central to furnace utilization, distribution efficiency, and local supply planning. Wine imports, craft beer, and rising spirits consumption continue to support bottle demand, especially where glass reinforces product quality and premium positioning. Non-alcoholic beverages still face more pressure from PET and carton formats, so growth in that part of the Denmark container glass market remains more selective.

Perfumery is projected to expand at a 6.80% CAGR through 2031, making it the fastest-growing end-user segment in the Denmark container glass industry. Gerresheimer's annual reporting pointed to stronger fragrance momentum than the broader beauty market through 2028, which supports continued demand for premium glass flacons and related specialty formats.[3]Gerresheimer AG, “Annual Report 2024,” Gerresheimer, gerresheimer.com Cosmetics and personal care packaging in Denmark also depend heavily on imports from European specialty suppliers serving skincare, haircare, and body-care brands. Pharmaceutical demand remains steadier and relies on amber and flint bottles for oral liquids and topical products, while food stays stable through condiments, preserves, and specialty jars. The overall result is a demand mix where the Denmark container glass market keeps its volume base in beverages, while some of its fastest expansion comes from smaller premium categories.

By Color: Flint's Premium Dominance And Amber's Circular Edge

Flint glass held 52.74% of the total volume in 2025 and remained the largest color segment in the Denmark container glass market. Transparent packaging keeps a strong place in spirits, carbonated beverages, premium condiments, and other consumer-facing categories where visual clarity shapes shelf appeal. That preference supports steady flint demand because product color and apparent purity remain important brand signals. The trade-off is that flint has a weaker recycled-content profile than darker colors, which complicates the balance between circularity goals and premium presentation. Vetropack's 2025 reporting showed that flint glass carried 40-41% average recycled content across its European operations, compared with 77% in brown glass.

Amber is forecast to record a 4.73% CAGR through 2031, the fastest growth rate among color segments in the Denmark container glass market. Its appeal is strongest in spirits, pharmaceuticals, and premium craft beer, where light protection matters together with sustainability reporting and recycled-content targets. Vetropack's operating data helps explain that advantage because brown glass accepted much higher recycled content than flint in 2025. Green glass remains important for wine packaging, while the rest-of-colors category serves smaller artisanal and specialty applications. This leaves the Denmark container glass market with a clear split, flint leads on premium display, while amber gains ground where protection and circularity have to move together.

Geography Analysis

Domestic production covered around 80% of local demand in the Denmark container glass market, with Ardagh Glass Holmegaard's Fensmark facility serving as the country's core manufacturing base. The plant has an annual capacity of around 160,000 tonnes and produces close to 800 million bottles and containers each year. That output is supported by Denmark's recycling chain, where recovered glass is directed back into container production through established remelt flows. This local footprint gives shorter lead times for standardized bottles and jars than a fully import-based model would allow. It also means the Denmark container glass market remains sensitive to any disruption at one site because domestic manufacturing is tightly concentrated.

Imports still fill the part of the Denmark container glass market that local production does not cover, especially in specialty glass categories. Premium spirits flacons, perfumery containers, pharmaceutical bottles, and selected food jars are sourced from glassmakers elsewhere in Europe that have deeper specialization in those formats. This pattern links Denmark closely with suppliers in Germany, France, Italy, Portugal, Austria, and neighboring parts of the region. Danish exports are smaller in volume and remain centered on more standardized beverage bottles and preserve jars for Scandinavian customers. The Nordic-Baltic production base is narrow, which keeps Denmark structurally exposed to European supply conditions when specialty demand rises or domestic capacity tightens.

Regulation (EU) 2025/40 began applying from August 12, 2026, which placed Denmark inside the EU's tighter recyclability and reuse framework for packaging.[4]European Parliament and Council of the European Union, “Regulation (EU) 2025/40 of the European Parliament and of the Council of 19 December 2024 on Packaging and Packaging Waste,” EUR-Lex, eur-lex.europa.eu Denmark entered this phase with an established deposit and recycling system for glass bottles, which gives the country a stronger circular starting point than many peers. In February 2026, the Danish Ministry of Environment opened consultation on a model that would lower the glass handling fee by up to 30%. That step matters because the growth path of the Denmark container glass market depends not only on demand, but also on whether domestic production remains economically workable under the new regulatory cost structure.

Competitive Landscape

The Denmark container glass market remains consolidated at the manufacturing level because Ardagh Glass Holmegaard is the only domestic producer and serves around 80% of local volume demand. This gives Ardagh a clear advantage in proximity, customer response time, and alignment with Danish recovery and cullet systems. The remaining demand is met through imports from larger European groups such as O-I Glass, Verallia, Vidrala, Vetropack, Wiegand-Glas, Stoelzle Glass Group, Zignago Vetro, and Beatson Clark, depending on format and application. The result is a two-layer structure, one local manufacturer for core domestic supply and a wider imported supplier set for specialty products and price-based competition. That is why the Denmark container glass market is concentrated in production but still open to strong import rivalry.

European suppliers are increasingly competing through decarbonization and technical differentiation rather than volume alone. Verallia said in 2025 that its Net Zero 2040 trajectory had received Science Based Targets initiative validation, making it the first global container glass producer to reach that milestone. O-I Glass reported USD 300 million in Fit to Win benefits in 2025 and continued to roll out ULTRA technology aimed at up to 30% weight reduction in glass containers. Vetropack also pushed lightweighting with its Rezon reusable bottle, launched in September 2025 with up to 30% lower weight than conventional reusable bottles. These moves matter for Danish buyers because freight costs, sustainability targets, and handling efficiency are becoming more important in supplier selection. The Denmark container glass market is therefore seeing competition shift toward lower-carbon production, lighter bottles, and stronger specialty capabilities.

Ownership change and capacity restructuring are also shaping the supplier base available to Danish importers. BWGI completed its voluntary tender offer for Verallia in August 2025 and held 77.17% of Verallia's share capital by December 31, 2025. Vidrala expanded its South American footprint in March 2026 through the acquisition of Cristalerías Toro for EUR 75 million (USD 84.75 million), which extended the group's international platform beyond Europe. Verallia also noted that around 22 furnace closures had been announced across Europe since the fourth quarter of 2023, representing roughly 10% of regional capacity as defined by FEVE, which shows how supply is being reshaped around demand conditions and cost pressure. This leaves the Denmark container glass market exposed to broader European restructuring even when local demand remains firm.

Denmark Container Glass Industry Leaders

Ardagh Glass Holmegaard A/S (Ardagh Group S.A.)

Berlin Packaging Denmark A/S

Nova Pack A/S

Gerresheimer AG

Feemio Group Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Vidrala completed the acquisition of 100% of Chilean glass container producer Cristalerías Toro for an enterprise value of EUR 75 million (USD 84.75 million), establishing Vidrala Chile and extending the company's South American platform to over 20% of global sales.

- February 2026: The Danish Ministry of Environment (Miljø- og Ligestillingsministeriet) initiated a public consultation proposing a model that would cut the EPR glass packaging handling fee by up to 30%, introducing a benchmark pricing mechanism based on the 20% most cost-efficient municipal collection systems. The measure directly addressed the financial pressure that caused Ardagh Glass Holmegaard to close 2 of its 6 production lines.

- March 2025: Denmark enforced anti-greenwashing legislation requiring documented environmental claims by September 2026.

Denmark Container Glass Market Report Scope

Container glass is designed for crafting glass containers, including bottles, jars, drinkware, and bowls. Its key attributes include chemical inertness, sterility, and non-permeability, rendering it especially sought after in the beverage, food, pharmaceutical, and cosmetic sectors. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

Denmark Container Glass Market is segmented by End-User (Beverages [Alcoholic (Beer, Wine, Spirits, and Other Alcoholic Beverages), Non-Alcoholic beverages (Juices, Carbonated Drinks, Dairy Product-Based Drinks, Other Non-Alcoholic Beverages)], Food, Cosmetics and Personal Care, Pharmaceuticals (Excluding Vials and Ampoules), and Perfumery, and Color (Green, Amber, Flint, and Rest of Colors). The Market Forecasts are Provided in Terms of Volume (Kilotons).

By End-User

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks | ||

| Dairy Product-Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (Excluding Vials and Ampoules) | ||

| Perfumery | ||

By Color

| Green |

| Amber |

| Flint |

| Rest of Colors |

| By End-User | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks | |||

| Dairy Product-Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (Excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Rest of Colors | |||

Key Questions Answered in the Report

What is the current size of the Denmark container glass market?

The Denmark container glass market stands at 214.46 kilotons in 2026 and is forecast to reach 263.32 kilotons by 2031, growing at a 4.19% CAGR, according to Mordor Intelligence.

Which end-user segment leads container glass demand in Denmark?

Beverages led demand with 57.68% of total volume in 2025, supported by beer, wine, and spirits packaging.

Which color segment is growing fastest in Denmark?

Amber is the fastest-growing color segment, with a projected 4.73% CAGR through 2031, helped by light protection needs and stronger recycled-content performance.

Why are glass bottles and jars gaining support in Denmark?

The shift is being driven by stricter EU packaging rules, Denmark's EPR framework, and a well-developed circular system for refill and remelting.

How dependent is Denmark on imported container glass?

Domestic production covers around 80% of demand, but imports remain important for premium spirits flacons, perfumery containers, pharmaceutical bottles, and some specialty food jars.

What is the main supply-side risk for buyers in Denmark?

The local manufacturing base is concentrated at one producer, so cost pressure, furnace line closures, or policy misalignment can raise reliance on European imports.

Page last updated on: