Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

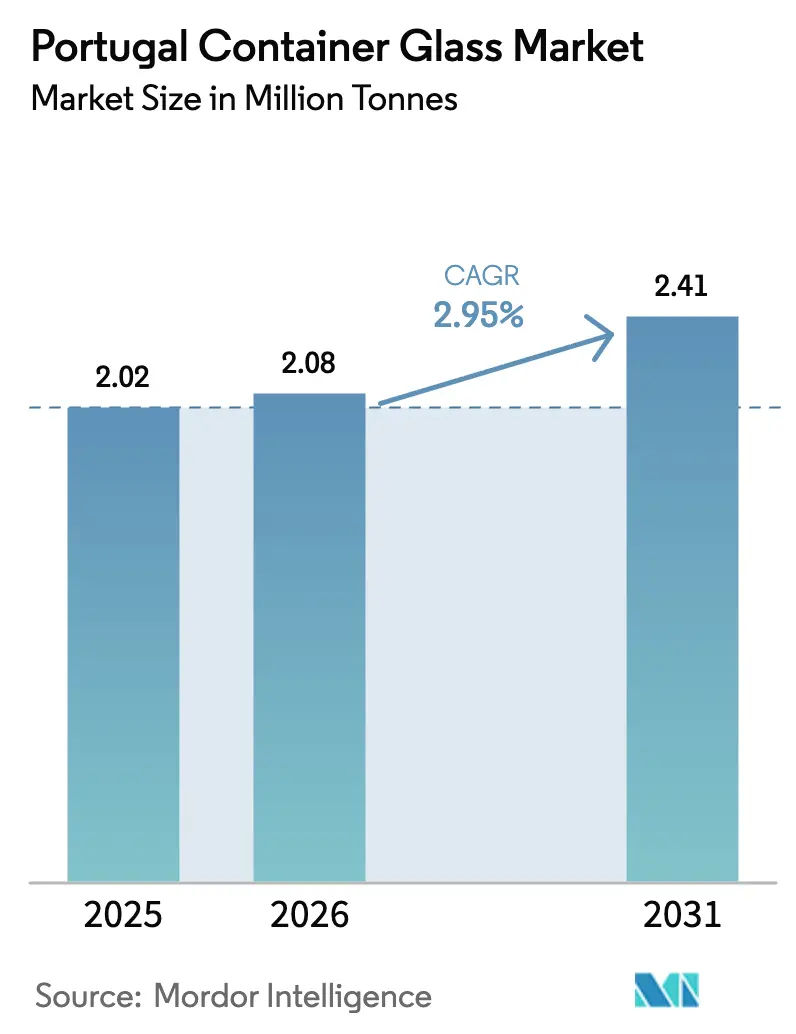

| Base Year Market Size (2025) | 2.02 Million tonnes |

| Market Volume (2026) | 2.08 Million tonnes |

| Market Volume (2031) | 2.41 Million tonnes |

| Growth Rate (2026 - 2031) | 2.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Portugal Container Glass Market Analysis by Mordor Intelligence

Portugal Container Glass Market size in 2026 is estimated at 2.08 million tonnes, growing from 2025 value of 2.02 million tonnes with 2031 projections showing 2.41 million tonnes, growing at 2.95% CAGR over 2026-2031. Demand continues to shift toward premium beverages, growing pharmaceutical exports, and sustainability mandates that are elevating recycled-content requirements. Manufacturers are consolidating production lines to increase furnace efficiency, while customers intensify their preference for endlessly recyclable packages that align with European circular economy targets. Power prices remain the most volatile cost element, motivating rapid investment in onsite renewables and lightweighting technologies. At the same time, a resilient export orientation protects revenues against fluctuations in consumption from any single country and allows producers to smooth capacity utilization throughout the year.[1]FEVE, “Glass Recycling Stats 2023,” feve.org

Key Report Takeaways

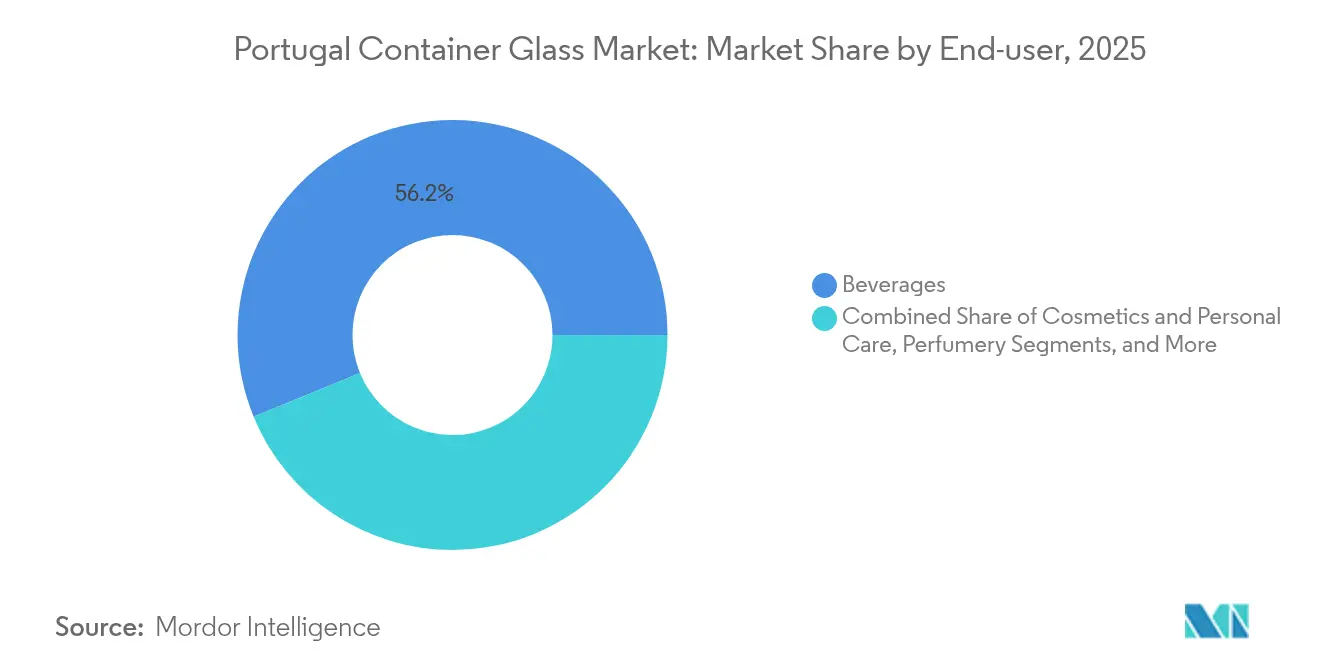

- By end-user, beverages captured 56.20% of the Portugal container glass market share in 2025.

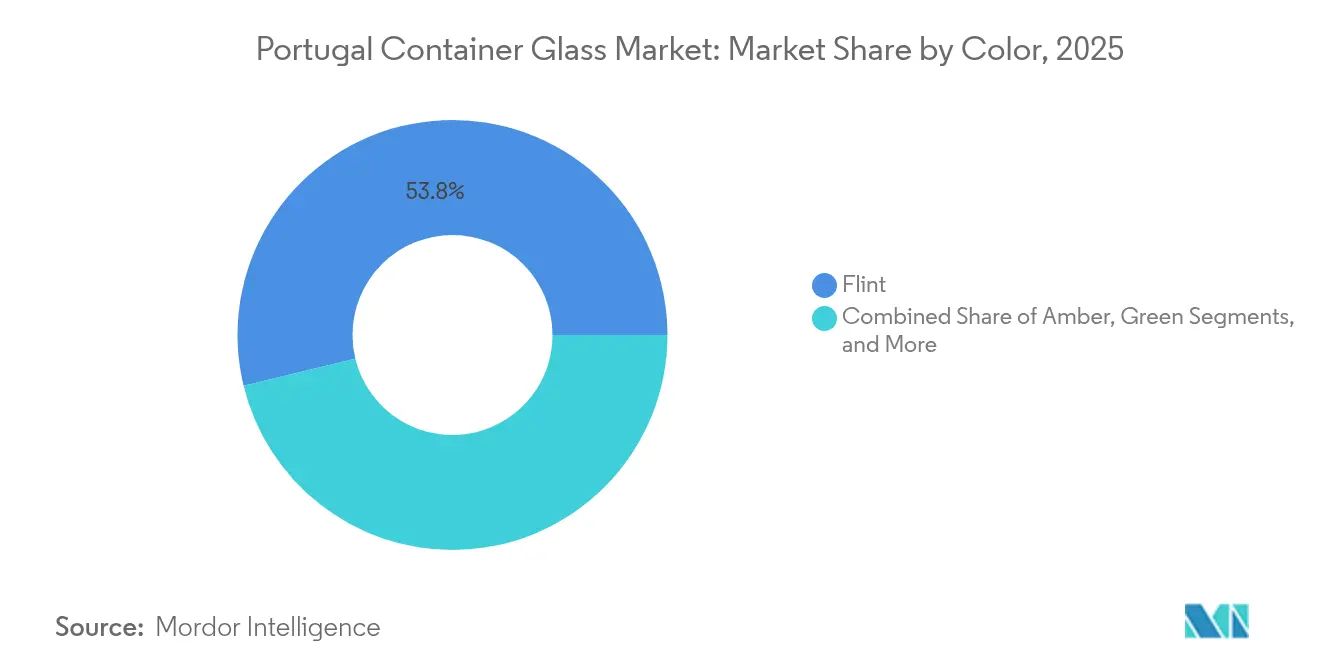

- By color, the Portugal container glass market size for the amber segment is projected to grow at a 4.82% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Portugal Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing consumer preference for recyclable glass packaging | +0.8% | Portugal and Iberian Peninsula | Medium term (2-4 years) |

| Premiumisation of beverages increases glass packaging demand | +0.7% | Wine and craft-beverage regions | Short term (≤ 2 years) |

| Regulatory push toward circular economy and recycling | +0.6% | National within EU framework | Long term (≥ 4 years) |

| Expansion of food and beverage manufacturing volumes | +0.5% | Domestic with export influence | Medium term (2-4 years) |

| Pharmaceutical and cosmetics sectors require glass containers | +0.4% | European pharma corridor | Long term (≥ 4 years) |

| Technology upgrades enable lighter, lower-carbon glass | +0.3% | Marinha Grande cluster | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Preference for Recyclable Glass Packaging

Recyclability dominates shopper decision criteria as collection efficiency across the European Union now exceeds 80% and Portugal extends bottle-bank networks to every major municipality. The result is a noticeable shift among retailers toward specifying cullet-rich bottles for their store brands. Brand owners capitalize on this consumer sentiment, reinforcing glass attributes of infinite recyclability and chemical inertness. Larger volumes of color-sorted cullet flow back to furnaces, trimming energy use per kilogram melted and lowering Scope 1 emissions. These advantages strengthen the Portugal container glass market position against single-use plastics, which face escalating regulatory fees tied to extended producer responsibility frameworks.

Premiumisation of Beverages Increases Glass Packaging Demand

Portugal’s wine export values advanced 4.5% in 2024, even after a weather-challenged harvest, confirming customer willingness to pay for premium presentation.[2]European Commission, “Regulation (EU) 2024/1040 on Packaging and Packaging Waste,” eur-lex.europa.eu Craft breweries expand capacity, and flagship brands such as Super Bock deploy glass to underscore artisanal identity. Superior oxygen and carbon dioxide barriers in glass deliver the shelf-life performance premium labels require, and the packaging’s tactile appeal reinforces the perceived value of the product. These factors sustain high per-unit margins that offset the costs of furnace modernization, thereby anchoring investment flows in the Portuguese container glass market.

Regulatory Push Toward Circular Economy and Recycling

The Packaging and Packaging Waste Regulation (EU 2024/1040) fixes minimum recycled-content thresholds for glass containers sold inside the bloc. Portugal’s decision to exclude glass from its 2026 deposit-return launch gives the material a competitive edge, as plastics and metals will incur additional handling fees. Mandatory cullet quotas reshape procurement, compelling producers to forge supply contracts with sorting facilities. Compliance favors scale players who already operate color-separation lines, tightening barriers to entry and supporting price discipline across the Portugal container glass market.

Expansion of Food and Beverage Manufacturing Volumes

Food processing remains one of Portugal’s fastest-growing industrial pillars, importing USD 293 million of U.S. agricultural inputs in 2023.[3]United States Department of Agriculture Foreign Agricultural Service, “Portugal: Food Processing Ingredients,” fas.usda.gov Rising output of olive oil, jam and gourmet condiments requires packaging that safeguards organoleptic properties and signals premium origin. Glass answers both needs with chemical inertness and visual clarity, while its rigidity withstands long-haul exports to the Americas and Asia. Steady throughput from the food sector balances seasonal swings in wine bottling, stabilizing furnace utilization rates and sustaining workforce employment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High energy intensity increases production costs | -0.9% | Portugal within EU energy context | Short term (≤ 2 years) |

| Fragility raises logistics costs and breakage risk | -0.4% | Export supply chains | Medium term (2-4 years) |

| Competition from cheaper plastic and metal packaging | -0.3% | Global alternatives pressure | Medium term (2-4 years) |

| Volatile raw-material and transport cost pressures | -0.2% | European supply hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Energy Intensity Increases Production Costs

Melting furnaces operate above 1,500 °C and consume energy at rates up to four times higher than competing packaging substrates. Portugal’s industrial power tariffs spiked in 2024 and forced producers to absorb cost surges that reached 20% of finished-container expenses. The Electrointensive Consumer Statute now offers rebates worth as much as 75% of regulated grid surcharges for manufacturers that source renewables, yet eligibility hinges on capital-intensive metering upgrades. Smaller firms lacking liquidity struggle to qualify, which accelerates consolidation inside the Portugal container glass market.

Fragility Raises Logistics Costs and Breakage Risk

Glass brittleness necessitates heavier outer cartons and careful palletization, elevating freight costs by 10-15% over plastic equivalents on identical lanes. Exporters shipping to North America absorb higher marine insurance premiums, and e-commerce fulfillment introduces multiple touchpoints where breakage probability multiplies. These hidden expenses pressure margins, especially for lower-value food products where packaging already represents a large proportion of cost of goods sold. Consequently, some volume migrates to lightweight plastics for single-serve SKUs, moderating the growth trajectory of the Portugal container glass market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Beverages Sustain Leadership while Personal Care Accelerates

The beverages segment captured 56.20% of the Portuguese container glass market size in 2025, reflecting the nation’s well-established wine tradition and expanding craft beer culture. Bottle formats remain dominant, and wineries prioritize glass for its stability in product aging and export-ready aesthetics. Continuous premiumisation maintains a high average unit value, enabling producers to absorb furnace efficiency upgrades without eroding their margins. Parallel momentum stems from the spirits subsegment, where aged aguardentes deploy heavyweight flint bottles to signal authenticity and heritage.

Cosmetics and personal care are forecast to post a 4.45% CAGR through 2031, the fastest across all end-uses. Portuguese contract manufacturers scale up dermocosmetic and natural-ingredient lines that command premium price points in European pharmacies. Glass jars and vials align with consumer safety perceptions, as they are free of potential endocrine disruptors linked to certain plastics. The Portugal container glass market thus broadens its customer mix, reducing dependence on seasonal beverage cycles and capturing higher-margin specialty demand.

By Color: Flint Dominates as Amber Gains Momentum

Flint held 53.80% of the Portuguese container glass market share in 2025, driven by premium beverage bottling and pharmaceutical applications that require visual inspection of fill levels and clarity. Producers leverage Flint’s neutrality to showcase label design and maximize shelf appeal, which is critical in export-oriented wine channels. Advanced furnace refinements cut iron impurities, yielding higher brilliance that meets luxury-brand specifications.

Amber leads in growth with a 4.82% CAGR outlook thanks to increased craft-beer output and heightened pharmaceutical adoption that depends on UV shielding. Breweries prefer amber to safeguard hop-derived volatiles, while drug manufacturers comply with photostability guidelines for light-sensitive formulations. This diversification stabilizes furnace color campaigns and supports batch-size optimization. Green glass retains a steady share in traditional wine bottling, whereas specialty colors cater to niche perfumery SKUs at attractive unit margins.

Geography Analysis

Portugal’s container glass production is geographically concentrated in the historic Marinha Grande cluster, where centuries-old know-how and an experienced labor pool lower onboarding time for furnace technicians. Proximity to silica sand quarries reduces inbound logistics and helps contain raw material costs, especially as fuel surcharges increase maritime freight tariffs. The region also benefits from a supportive municipal administration that streamlines environmental permitting, accelerating rebuild schedules for end-of-life furnaces.

Northern Portugal anchors secondary capacity around Porto and Avintes, enabling cross-border shipments to Spain within a single day’s truck transit. This locale supplies beverage clients located along the Douro Valley and Galicia, aligning glass-blowing capacities with winery bottling peaks during post-harvest months. Coastal port access enables producers to load rail-linked intermodal containers destined for the Americas, thereby diversifying revenue streams and mitigating macroeconomic fluctuations in domestic consumption.

Central and southern areas lack significant melting furnaces yet constitute essential demand clusters. Pharmaceutical and cosmetics fillers cluster near Lisbon, leveraging air-cargo links for time-sensitive exports. Although these areas import bottles from the north, localized decoration and sterilization services flourish, adding value and reducing empty-glass haul-back. This intra-country flow underlines how the Portugal container glass market functions as an integrated network rather than siloed regional operations.

Competitive Landscape

The market exhibits moderate concentration, with Verallia, Vidrala, and BA Glass operating Portugal’s three multi-furnace plants. Each leverages shared R&D platforms from its wider European network to lift energy efficiency and accelerate lightweighting rollouts. Verallia’s Figueira da Foz site is integrated into a 32-plant continental footprint that secures cullet supply and balances color campaigns across borders. Vidrala’s Santos Barosa plant introduced the 260 g wine bottle, reducing glass mass by 25% relative to standard 350 g formats while preserving stacking strength, a milestone that differentiates its offer to premium wineries. BA Glass invests in hybrid electric-oxygen burners and installs photovoltaic panels sized to supply 20% of its base-load demand, aligning with eligibility criteria for Portugal’s Electrointensive Consumer Statute.

Strategic moves often involve mergers to achieve geographic diversification. Vidrala’s acquisition of Vidraporto in Brazil injects double-digit growth exposure to South America, while BA Glass’ stake in Mexico’s Vidrio Formas grants entry to the North American Free-Trade corridor. Such deals provide foreign-exchange revenue that hedges against fluctuations in euro-denominated energy prices. Beyond scale, technological alliances play a pivotal role. Major players join supplier consortia to accelerate hydrogen-ready furnace trials, anticipating the impact of carbon pricing beyond 2030. Niche opportunities persist for mid-sized specialists in pharmaceutical tubing and low-volume perfumery flacons, but qualification barriers and capital intensity limit rapid entry by challengers.

Customer relationships form the final pillar of competitive advantage. Long-term contracts with Portugal’s major wine co-operatives lock in baseline demand, while integrated decoration capabilities foster stickiness by reducing lead times. Consequently, bargaining power tilts toward the three incumbents, underpinned by their ability to guarantee security of supply during furnace overhauls or geopolitical trade disruptions.

Portugal Container Glass Industry Leaders

Mercado do Vidro

BA Vidro S.A

Verallia Packaging

Vidrala S.A

Deposito da Marinha Grande

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: BW Gestão de Investimentos filed a voluntary tender offer for Verallia shares at EUR 30 (USD 32.47) per share, valuing the company at approximately EUR 2.47 billion (USD 2.67 billion).

- April 2025: The Portuguese government secured European Union approval for the Electrointensive Consumer Statute, allocating at least EUR 60 million (USD 64.94 million) annually to reduce electricity surcharges for 319 eligible manufacturers, including BA Glass and Vidrala.

- December 2024: SCHOTT Pharma reported record revenue of EUR 957 million (USD 1,035 billion) and expanded prefillable syringe capacity in Hungary, boosting ready-to-use vial supply across Europe and North America.

- December 2024: Gerresheimer completed the acquisition of Bormioli Pharma, enlarging its European footprint in pharmaceutical glass containment solutions.

Portugal Container Glass Market Report Scope

Container glass is designed for crafting glass containers, including bottles, jars, drinkware, and bowls. Its key attributes include chemical inertness, sterility, and non-permeability, rendering it especially sought after in the beverage, food, pharmaceutical, and cosmetic sectors. The research also examines underlying growth influencers and significant industry vendors, all of which help to support market estimates and growth rates throughout the anticipated period. The market estimates and projections are based on the base year factors and arrived at top-down and bottom-up approaches.

Portugal Container Glass Market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery, and by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

By End-user

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

By Color

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

What volume does the Portugal container glass market reach in 2026?

The Portugal container glass market size is 2.08 million tonnes in 2026.

Which end-use category drives the highest demand for Portuguese glass containers?

Beverages account for 56.20% of total demand, led by wine and expanding craft-beer output.

Which color segment is growing fastest through 2031?

Amber glass is forecast to advance at a 4.82% CAGR owing to craft-beer and pharmaceutical uptake.

How is the government addressing high industrial energy costs?

Portugal’s Electrointensive Consumer Statute offers rebates covering up to 75% of regulated grid surcharges for qualifying glass producers.

What major sustainability trend shapes purchasing decisions?

Rising consumer preference for infinitely recyclable packaging is steering brands toward glass over single-use plastics.

Who are the key manufacturers operating furnaces in Portugal?

Verallia, Vidrala and BA Glass run the country’s three primary container-glass plants.

Page last updated on: