Sliding Bearing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

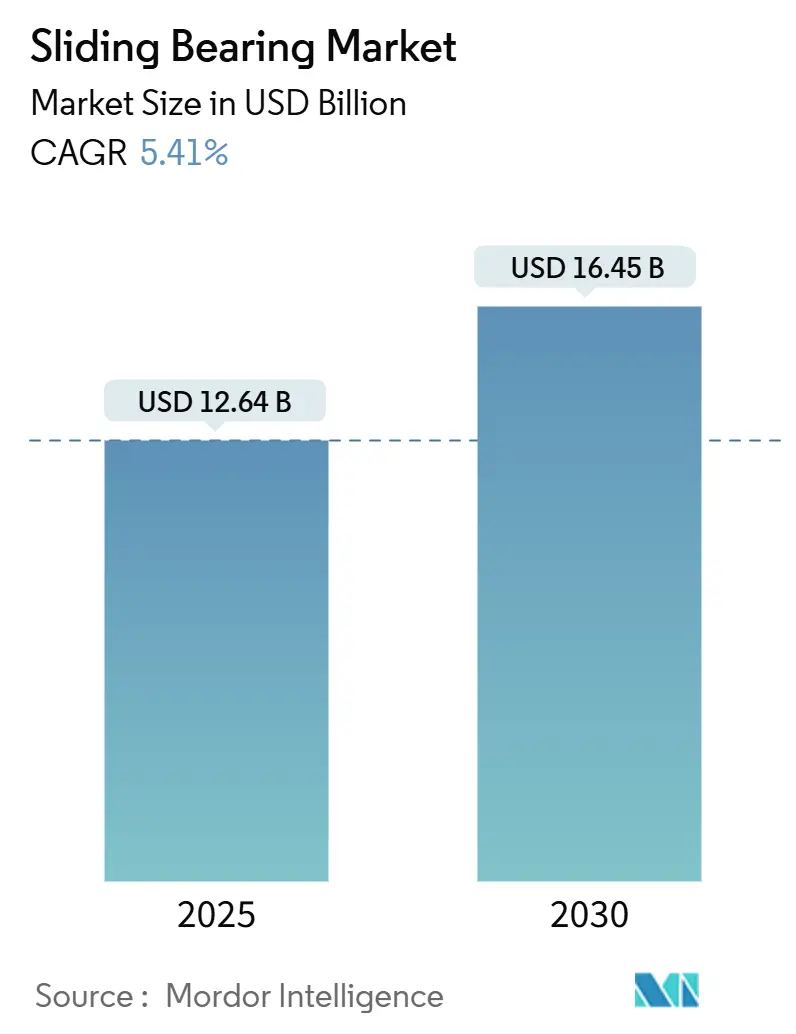

| Market Size (2025) | USD 12.64 Billion |

| Market Size (2030) | USD 16.45 Billion |

| Growth Rate (2025 - 2030) | 5.41% CAGR |

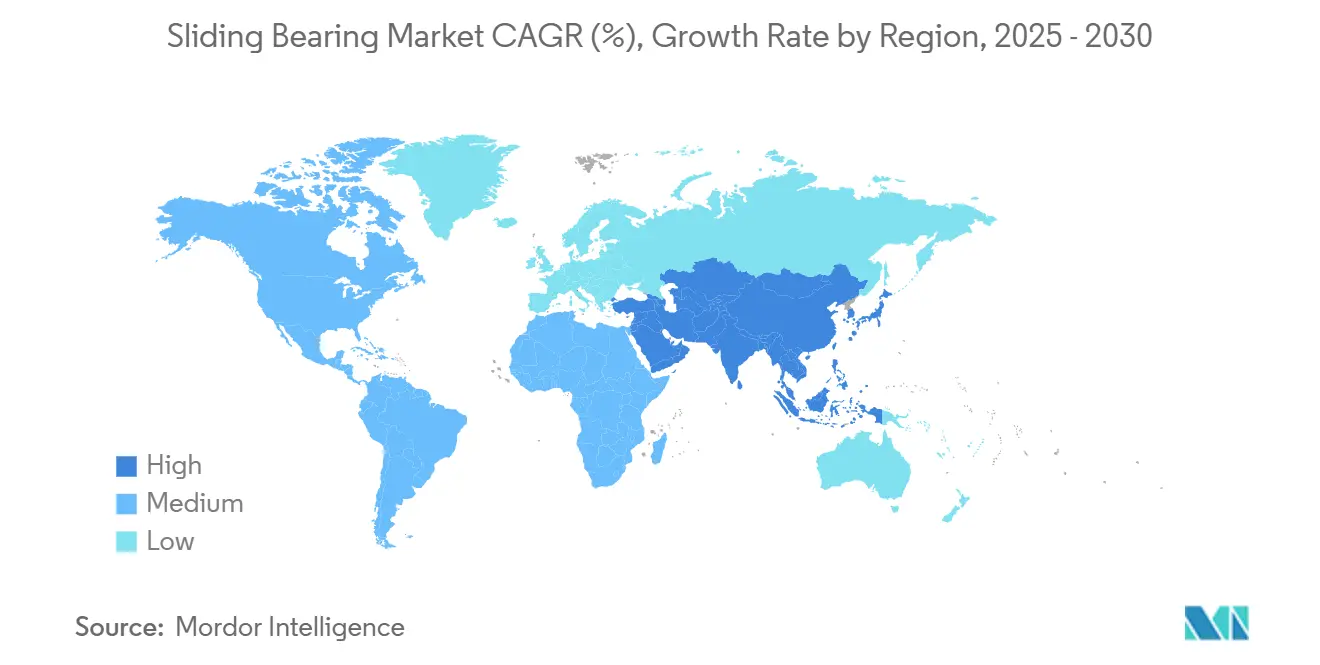

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sliding Bearing Market Analysis by Mordor Intelligence

The sliding bearing market size stood at USD 12.64 billion in 2025 and is forecast to reach USD 16.45 billion by 2030, exhibiting a 5.41% CAGR over 2025-2030. The growth outlook reflects rising capital expenditure on electrified rail, higher electric-vehicle (EV) sales, and widespread deployment of predictive-maintenance programs in process industries. Demand runs strongest in applications that impose extreme shock loads, elevated temperatures, or limited lubrication access, conditions under which plain bearings outperform rolling alternatives. Materials innovations, including PTFE- and PEEK-based composites reinforced with carbon nanotubes, lengthen operating life and curb total cost of ownership. At the same time, additive manufacturing accelerates custom bushing production for niche designs. Regulatory tightening around noise and vibration, and the energy-efficiency push in hydrogen and e-fuel infrastructure, further amplify adoption. Supply-side constraints, however, linger in the form of volatile copper and tin prices and specialty-alloy sourcing risks, prompting hedging strategies and material substitution.

Key Report Takeaways

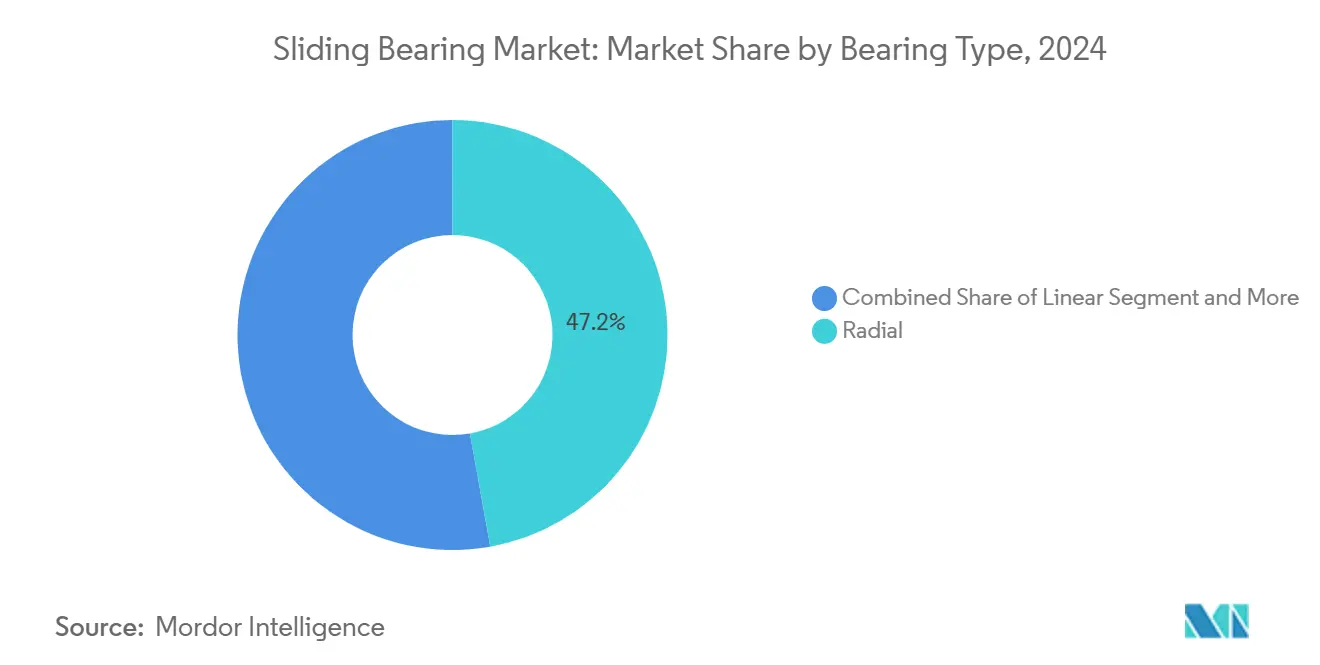

- By bearing type, radial designs led with 47.15% of the sliding bearing market share in 2024, whereas angular contact variants are advancing at a 7.04% CAGR to 2030.

- By application, industrial machinery accounted for 36.44% of the sliding bearing market share in 2024, while aviation applications are expanding at a 6.55% CAGR through 2030.

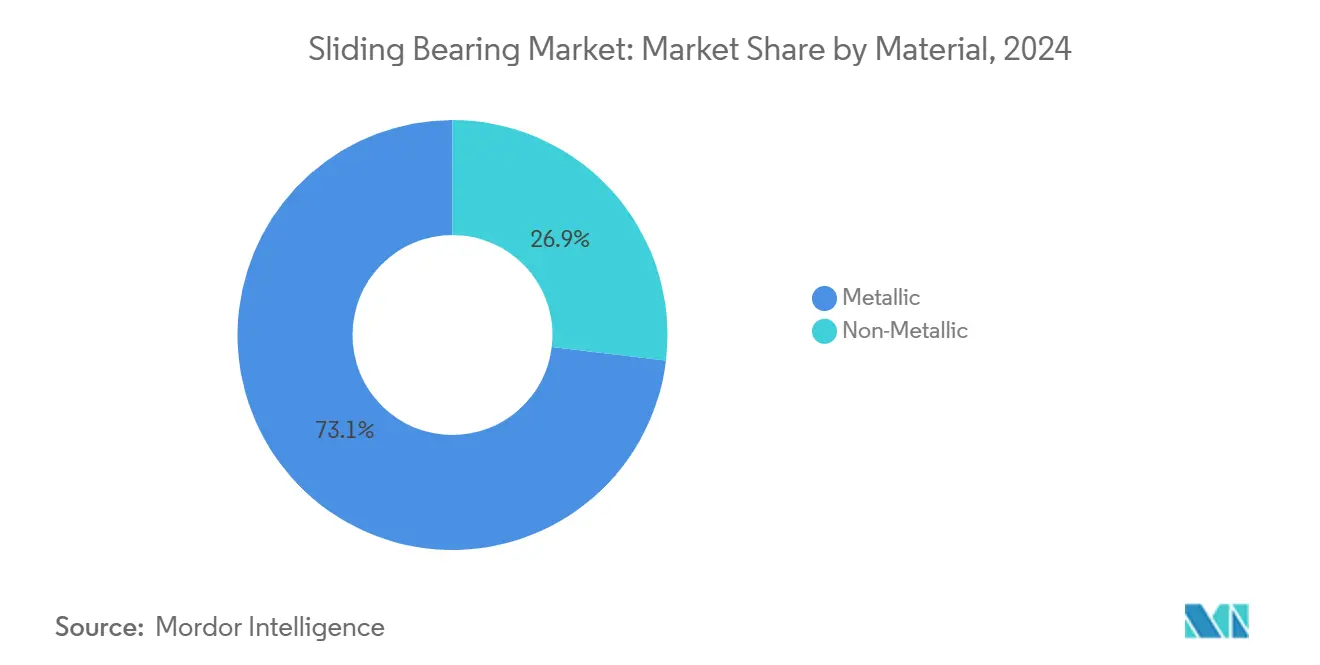

- By material, metallic bearings held 73.14% of the sliding bearing market share in 2024; non-metallic counterparts are projected to widen at a 7.25% CAGR over the same horizon.

- By load direction, radial-load designs represented 65.38% oof the sliding bearing market share in 2024, yet combination-load products are forecast to climb at a 5.94% CAGR by 2030.

- By geography, Asia-Pacific dominated with 43.18% of the sliding bearing market share in 2024, whereas the Middle East & Africa region is forecast to post the fastest 6.12% CAGR through 2030.

Global Sliding Bearing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-Speed Rail and EV Surge | +1.2% | Asia-Pacific core; spill-over to Europe and North America | Medium term (2-4 years) |

| Adoption of Predictive Maintenance | +0.8% | Global; early uptake in North America and EU | Short term (≤2 years) |

| Advanced Self-Lubricating Composites | +0.7% | Global; industrial and aviation focus | Long term (≥4 years) |

| Stricter Global Noise-Vibration Norms | +0.5% | Europe and North America; expanding into Asia-Pacific | Medium term (2-4 years) |

| Hydrogen and E-Fuel Needs | +0.4% | Europe and North America; pilot in Asia-Pacific | Long term (≥4 years) |

| Custom Bushings Via Additive Manufacturing | +0.3% | Global; concentrated in developed markets | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Surge in High-Speed Rail and EV Projects Driving Demand

Asia-Pacific railway build-outs and accelerating EV production jointly elevate procurement of journal and wheel-hub plain bearings, magnifying the sliding bearing market trajectory. China’s rail grid is scheduled to span 60,000 km by 2030, requiring journal bearings that sustain continuous operation amid thermal cycling. Simultaneously, EV drivetrains mandate self-lubricated, electrical-discharge-resistant bushings, as illustrated by NSK’s eVTOL-ready designs. The compounded requirement across mass transit and personal mobility places sustained volume pressure on suppliers and consolidates Asia-Pacific’s leadership within the sliding bearing market.

Predictive-Maintenance Adoption with Sensor-Enabled Bearings

Digitization converts plain bearings into data nodes that feed fleet-wide analytics. Schaeffler’s OPTIME sensors flag failures up to six months early, cutting unplanned downtime and lowering lubricant spend [1]“OPTIME Condition Monitoring,” Schaeffler AG, schaeffler.com. ABB integrates vibration probes with AI platforms to optimize full production lines. Asset owners accept 20-30% unit price premiums because lifecycle savings exceed component cost, propelling a higher-margin slice of the sliding bearing market.

Advanced Self-Lubricating Composites Reducing Lifecycle Cost

PTFE composites fortified by carbon nanotubes now deliver friction coefficients below 0.05 at 200 °C, opening harsh-environment opportunities once reserved for oil-fed metals. PEEK matrices add chemical resilience for marine and chemical-processing equipment. GGB’s fiber-reinforced bushings illustrate how self-lubrication removes centralized lube systems, slashing maintenance labor and hazardous-waste fees. The outcome is a durable competitive differentiator that underpins long-run expansion of the sliding bearing market.

Stricter Global Noise-Vibration Norms

ISO 20816 vibration thresholds and EU urban noise ordinances are prompting machinery OEMs to specify plain bearings that yield 10–15 dB quieter performance, particularly in wind turbines and commuter railcars [2]“ISO 20816 Vibration Standards,” International Organization for Standardization, iso.org. Sliding bearings’ inherent damping thus secures a regulatory pull in mature economies while encouraging retrofits across older fleets, fortifying mid-term demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Copper and Tin Prices | −0.9% | Global; sharpest in price-sensitive segments | Short term (≤2 years) |

| Roller Bearing Substitution Needs | −0.6% | Global; industrial-machinery concentration | Medium term (2-4 years) |

| Specialty Alloy Supply-Chain Concentration | −0.4% | Global; risk high in North America and Europe | Medium term (2-4 years) |

| Labor Shortage for Refurbishment | −0.3% | Developed regions, notably North America and Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatile Copper/Tin Prices Raising Metallic Bushing Cost

Copper is projected to rally behind electrification demand, lifting bronze-bearing material cost, which forms up to 60% of finished goods value. Tin faces parallel pressure per World Bank forecasts. Manufacturers hedge via long-term contracts, mixed-metal alloys, or migration to high-performance polymers, but near-term margins remain at risk within the sliding bearing market.

Roller-Bearing Substitution in Certain Machinery

Sealed ceramic-hybrid rollers now rival plain bearings on maintenance intervals, luring OEMs in moderate-load equipment. Although sliding products retain an edge in shock-load and marginal-lubrication situations, incremental share loss in mid-duty machinery tempers growth potential for segments of the sliding bearing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bearing Type: Radial Dominance Faces Angular Contact Challenge

Radial designs controlled 47.15% of the sliding bearing market share in 2024 by virtue of universal applicability across pumps, motors, and conveyors. Their straightforward geometry simplifies inventory and reduces unit cost, sustaining volume leadership. Meanwhile, angular contact units are forecast to log a 7.04% CAGR to 2030 as semiconductor tools, precision robotics, and turbomachinery adopt bearings that sustain combined radial-axial loads at high rpm. Suppliers increasingly deliver duplex and triplex arrangements pre-matched at the factory, ensuring preload accuracy that improves machine repeatability. In aerospace, angular contact bearings qualify under ISO 14839-2 vibration norms, strengthening uptake in jet engines and auxiliary power units. The segment’s premium positioning elevates the average selling price, gently lifting the overall sliding bearing market value.

Engineering advances also keep radial products relevant. Nanostructured overlay materials raise seizure resistance, allowing radial designs to tackle higher pv values. Sleeve-type upgrades, such as honeycomb or tilt-pad geometries, dampen rotor instability in petrochemical compressors. This gradual performance creep, combined with entrenched manufacturing scale, suggests radial bearings will still command substantial sliding bearing market size, even as angular contact uptake accelerates.

By Application: Industrial Machinery Leadership Challenged by Aviation Growth

Industrial machinery captured 36.44% of the sliding bearing market size in 2024, reflecting massive installed bases in pulp-and-paper, mining, and power-generation assets. Plain bearings’ capacity to tolerate dirt ingress and shaft misalignment underpins this dominance. Predictive-maintenance platforms now retrofit onto mill housings, refreshing the value proposition for life-extension projects. Automation upgrades in brownfield plants, particularly in discrete manufacturing, sustain replacement demand. Concurrently, efficiency retrofits in combined-cycle power plants swap older white-metal journals for polymer-lined sleeves that save lubrication pump energy.

Aviation remains the fastest riser, tracking a 6.55% CAGR through 2030. Commercial programs such as A320neo and 737 MAX restart deliveries, while urban-air-mobility prototypes multiply. Weight-saving imperatives invite advanced polymer and ceramic bearing solutions. RBC Bearings secured multiple eVTOL awards for swash-plate bushings, and additive-manufactured titanium sleeves enter flight-control hinges. Sustainable aviation fuel (SAF) initiatives impose new chemical-compatibility tests that metallic designs sometimes fail, edging composite products forward. FAA and EASA airworthiness directives also tighten vibration thresholds, positioning plain bearings’ damping benefits as a compliance lever. Together, these forces allow aviation to erode the industrial segment’s hegemony within the sliding bearing market.

By Material: Metallic Prevalence Meets Non-Metallic Innovation

Metallic products supplied 73.14% of revenue in 2024, anchored by bronze, babbitt-lined steel shells, and case-hardened iron for high-load hydropower turbines. Standardized alloys, existing machine tools, and global supply chains keep unit costs competitive. Yet non-metallic bearings are projected to expand 7.25% annually, aided by PTFE, PEEK, and ceramic matrix composites that resist corrosion, offer electrical isolation, and run dry. The sliding bearing market size for non-metallics is further buoyed by food-processing and pharmaceutical plants seeking lubricant-free components to meet hygiene directives.

Composite uptake accelerates where metal prices spike or maintenance access is restrictive. The oil-and-gas downstream increasingly specifies PEEK wear rings in pumps conveying aggressive media. Wind-turbine OEMs deploy fiberglass-backed polymer pads in yaw systems, saving weight while enhancing dampening. As polymers’ thermal envelopes widen, metallic incumbents are pressured to innovate, adding nano-coatings or graded structures. The resulting material duel invigorates R&D budgets across the sliding bearing industry.

By Load Direction: Radial Preference Yields to Combination Applications

Radial-load bearings represented 65.38% of the sliding bearing market share in 2024, owing to the ubiquity of rotating shafts under primarily radial forces. Simplified hydrodynamic film formation grants these sleeves long life with minimal upkeep, keeping cost-per-kWh low in base-load power plants and municipal water pumps. However, machinery miniaturization and multi-functional assemblies generate complex force vectors, propelling combination-load bearings at a 5.94% CAGR.

Wind turbine main shafts, for instance, now rely on three-pad tilting designs that absorb simultaneous thrust and bending loads during gust events. Electric vehicle e-axles integrate radial and axial support into compact cartridges, aiding drivetrain packaging. Finite-element-optimized pad angles and fluid-film modeling software allow custom geometries, pushing the sliding bearing market toward application-specific hybrids.

Geography Analysis

Asia-Pacific accounted for 43.18% of the sliding bearing market share in 2024, thanks to China’s scale manufacturing and India’s production-linked incentive schemes, which target a 25% manufacturing GDP share by 2031. Steel capacity expansion adds mill stand demand, while Belt and Road projects create new hydropower installations that rely on large white-metal journals. Taiwan’s robust electronics output, reflected in significant industrial-production upticks, sustains procurement of precision linear bushings from local and Japanese vendors [3]“Monthly Industrial Production,” Ministry of Economic Affairs Taiwan, moea.gov.tw.

The Middle East and Africa region is anticipated to log a 6.12% CAGR to 2030, propelled by Saudi Arabia’s NEOM development, which specifies automated port cranes and desalination plants populated by polymer plain bearings. Industrial diversification policies across Gulf states stimulate petrochemical and aluminum smelter projects, each consuming hundreds of large journal bearings. African copper and iron-ore mine expansions widen the heavy-duty bearing base for haul trucks and crushers, reinforcing the sliding bearing market’s forward progression.

North America and Europe portray mature but tech-centric outlooks. United States infrastructure-renewal bills allocate record budgets for bridge restorations that replace aging elastomeric pads with composite sliding elements, preserving market value. EU environmental noise directives compel railcar refurbishments that substitute rolling bearings with plain designs to cut dB levels. Emphasis on circular-economy mandates drives adoption of re-babbitting contracts and sensor-enabled condition monitoring, steering service revenue growth within the broader sliding bearing market.

Competitive Landscape

The market structure is moderately concentrated. SKF, Schaeffler, and Timken top revenue tables and expand via M&A. Timken’s acquisition of GGB Bearings added self-lubricated polymer expertise, whereas SKF’s acquisition of John Sample Group augmented centralized lubrication offerings in Asia-Pacific. Portfolio breadth now spans metal, polymer, and hybrid lines, allowing cross-selling into diverse end markets.

Technology differentiation supersedes pure scale. Schaeffler’s OPTIME sensors bundle with grease dispensers to monetize data analytics, while SKF’s REP Center network delivers 48-hour refurbishment on large hydro-generator bearings. Smaller entrants exploit additive manufacturing; Igus prints bespoke sleeves in 24 hours, and startup Fusion-Cool deploys closed-cell metal foam overlays to dissipate heat.

Evolving ISO and ASME vibration-regulation updates reward vendors able to furnish integrated diagnostics, lubricant systems, and life-extension services. Sustainable-sourcing credentials and circular-economy programs, such as refurb-for-credit schemes, now influence bid awards, giving forward-leaning suppliers leverage within the sliding bearing market.

Sliding Bearing Industry Leaders

SKF Group

Schaeffler AG

The Timken Company

NSK Ltd.

NTN Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: igus introduced PTFE-free versions of its iglide G, X, and H polymer bearings, broadening eco-compliant options for mechanical-engineering customers.

- March 2025: Envision Energy reported flawless performance across 500 wind turbines using in-house developed sliding bearings, positioning the OEM as a first mover in turbine-integrated plain-bearing technology.

Global Sliding Bearing Market Report Scope

| Linear |

| Thrust |

| Radial |

| Angular Contact |

| Others |

| Automotive |

| Aviation |

| Marine |

| Industrial Machinery |

| Civil Structures |

| Others |

| Metallic |

| Non-Metallic |

| Radial |

| Axial |

| Combination |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Bearing Type | Linear | |

| Thrust | ||

| Radial | ||

| Angular Contact | ||

| Others | ||

| By Application | Automotive | |

| Aviation | ||

| Marine | ||

| Industrial Machinery | ||

| Civil Structures | ||

| Others | ||

| By Material | Metallic | |

| Non-Metallic | ||

| By Load Direction | Radial | |

| Axial | ||

| Combination | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected revenue for the sliding bearing market in 2030?

It is expected to reach USD 16.45 billion, reflecting a 5.41% CAGR from 2025.

Which region currently leads in sliding bearing demand?

Asia-Pacific commanded 43.18% of 2024 global revenue, driven by manufacturing scale and rail expansion.

Which application is growing the fastest?

Aviation applications are forecast to grow at 6.55% annually through 2030 due to eVTOL and commercial aircraft recovery.

Why are non-metallic bearings gaining popularity?

PTFE and PEEK composites deliver self-lubrication, corrosion resistance, and weight savings, supporting a 7.25% CAGR.

Page last updated on: