Motorcycle Chain Sprocket Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 2.74 Billion |

| Market Size (2030) | USD 4.40 Billion |

| Growth Rate (2025 - 2030) | 5.41% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Motorcycle Chain Sprocket Market Analysis by Mordor Intelligence

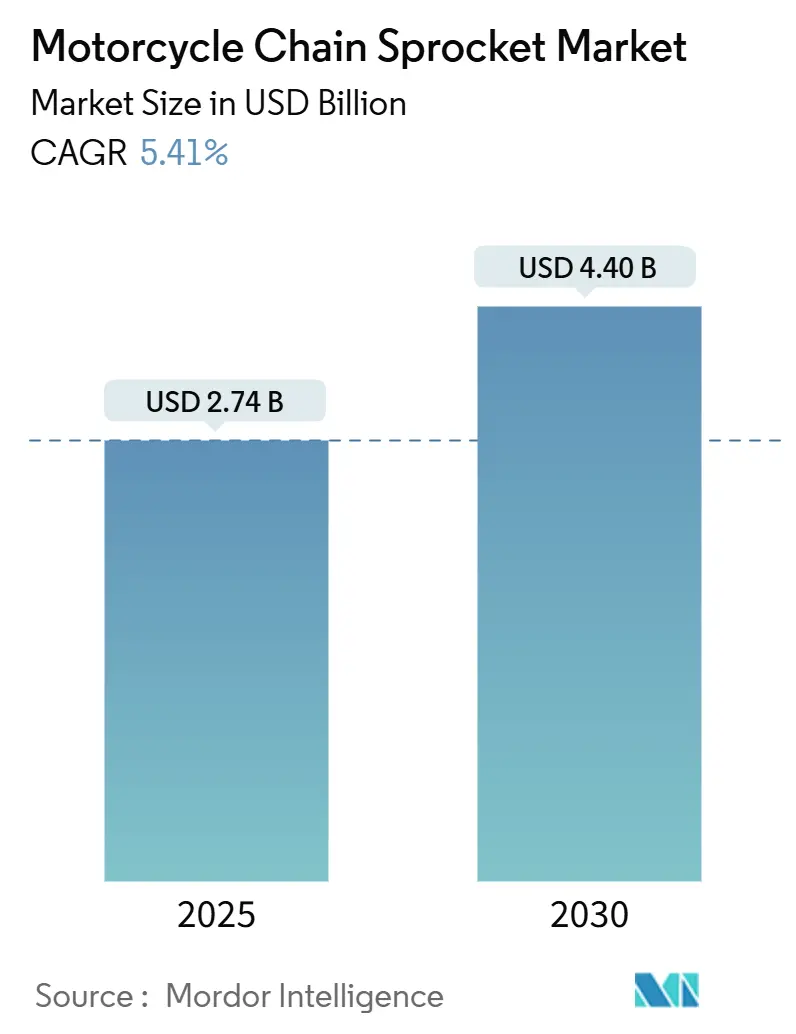

The motorcycle chain sprocket market size reached USD 2.74 billion in 2025 and is forecast to register a 5.41% CAGR to USD 4.4 billion by 2034, confirming a healthy long-term outlook despite drivetrain diversification pressures. Robust Asian two-wheeler sales, steady replacement cycles, and technological upgrades in sealed chains and lightweight sprockets sustain demand momentum. Steel remains the dominant material but hybrid and composite variants are scaling quickly as OEMs and aftermarket brands chase weight savings. Competitive intensity is rising as belt-drive suppliers promote long-life, low-noise alternatives, yet chains retain a clear edge in efficiency, gearing flexibility, and cost. Regionally, Asia-Pacific commands almost one-half of global revenue, while the Middle East and Africa posts the fastest growth as rising urbanization and infrastructure roll-outs lift motorcycle uptake.

Key Report Takeaways

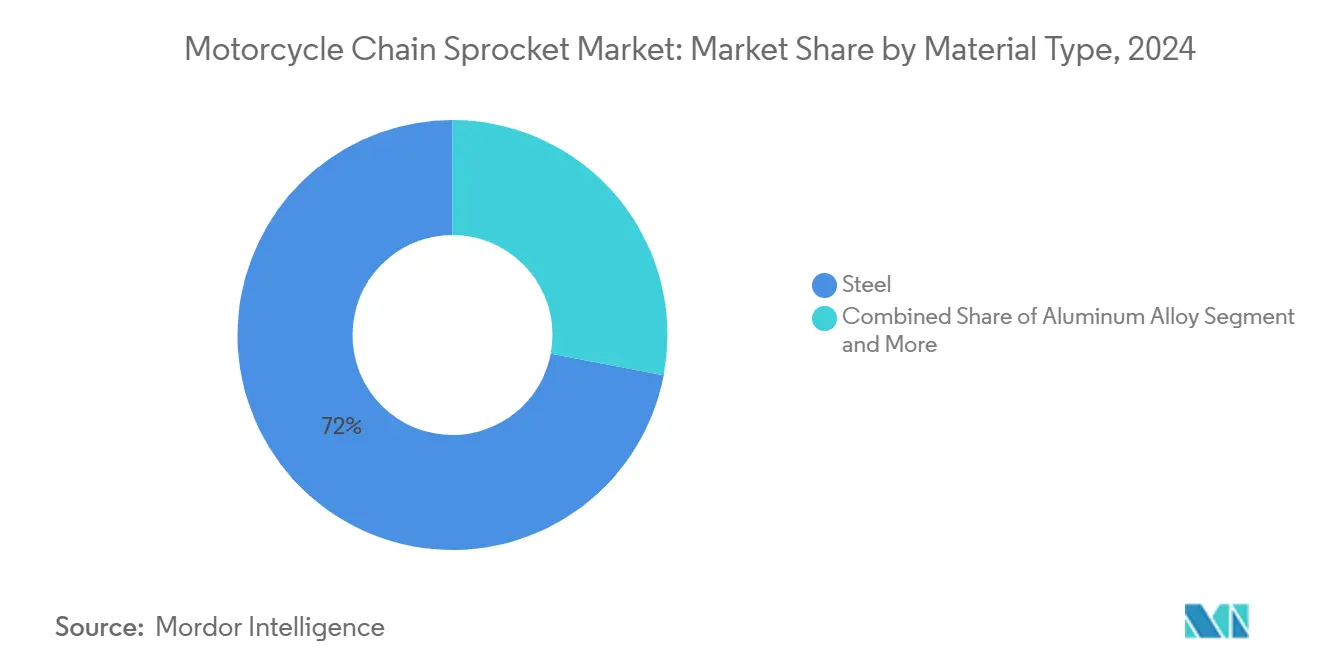

- By material type, steel led with 72.03% motorcycle chain sprocket market share in 2024; composite materials are advancing at an 8.91% CAGR through 2030.

- By sprocket type, standard units accounted for 64.52% of the motorcycle chain sprocket market size in 2024, while non-standard designs posted the quickest 7.18% CAGR.

- By chain type, O-ring technology held a 46.04% share in 2024, and X-ring chains are expanding at a 6.82% CAGR.

- By vehicle type, standard motorcycles captured 51.31% revenue in 2024; sports bikes represent the fastest-growing 7.53% CAGR segment.

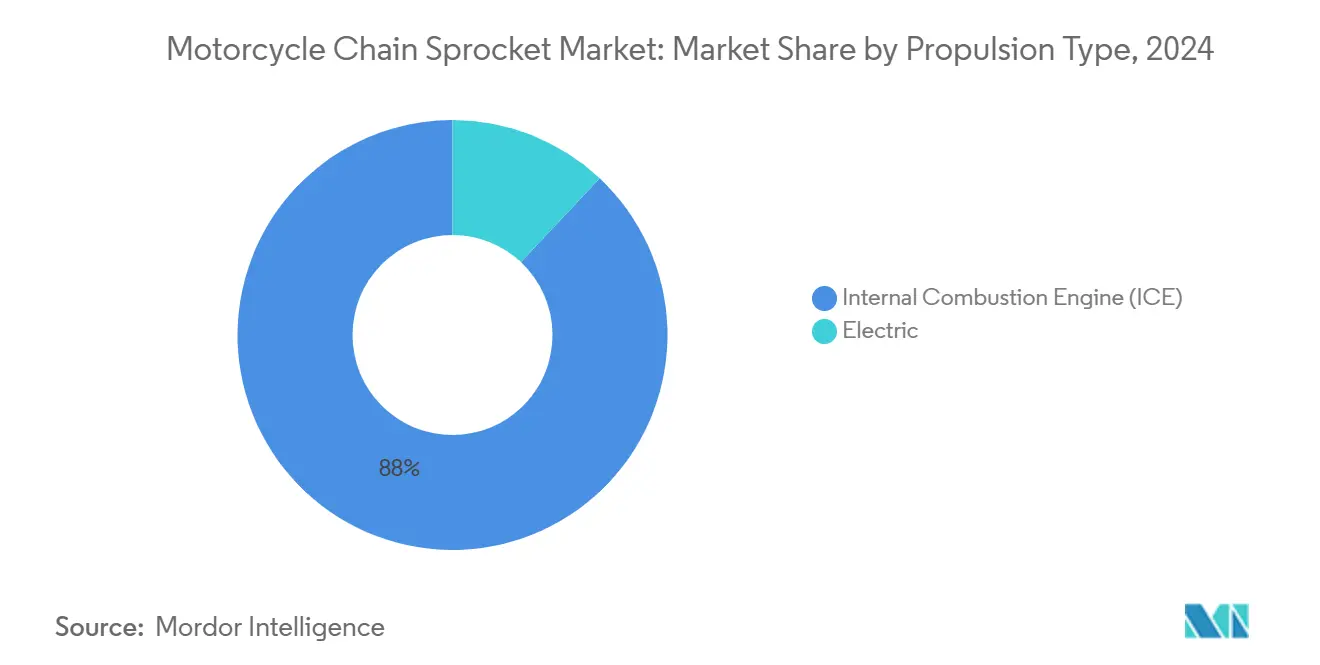

- By propulsion type, ICE models retained 88.01% share in 2024; electric motorcycles register a 12.39% CAGR to 2030.

- By distribution channel, the aftermarket held 62.41% of motorcycle chain sprocket market size in 2024, while OEM channels grow at 6.32% CAGR.

- By geography, Asia-Pacific dominated with 49.11% share in 2024 and the Middle East and Africa records the strongest 7.92% CAGR to 2030

Global Motorcycle Chain Sprocket Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Motorcycle Parc Expansion in Asia Drives Replacement Demand | +1.8% | Asia-Pacific Core, Spill-Over to Middle-East and Africa | Long Term (≥ 4 Years) |

| Shift to Lightweight Alloys for Performance and Fuel-Efficiency | +1.2% | Global, with Early Adoption in North America and EU | Medium Term (2-4 Years) |

| Rising Popularity of Sports/Performance Bikes Globally | +0.9% | Global, Concentrated in Developed Markets | Medium Term (2-4 Years) |

| Rapid Growth of E-Commerce Aftermarket Platforms | +0.7% | Global, Accelerated in North America and EU | Short Term (≤ 2 Years) |

| Adoption of Titanium and Carbon-Composite Sprockets for EV Noise Reduction | +0.6% | Global, with Early Penetration in Premium Electric Motorcycles | Medium Term (2-4 Years) |

| Integration of Smart Chain-Wear Sensors in OEM Fitments | +0.4% | Global, Led by High-End and Connected Motorcycle Models | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Motorcycle Parc Expansion in Asia Drives Replacement Demand

Asia's motorcycle fleet expansion creates sustained aftermarket demand that transcends economic cycles and technological transitions. India's registered motorcycle population exceeded 210 million units in 2022, with domestic sales reaching 15.9 million units in FY2023, predominantly sub-125cc models that rely heavily on chain-drive systems[1]Paolo Aversa, "The Evolution of the Two-Wheeler Industry A Comparative Study of Italy, Japan and India," wipo.int. . The replacement cycle for chains and sprockets typically ranges from 15,000-25,000 kilometers in Asian operating conditions, generating recurring revenue streams independent of new vehicle sales volatility. China's secondary aluminum consumption by the motorcycle industry reached 760,000 metric tons in 2024, up 3.4% year-over-year, indicating robust component manufacturing activity supporting both OEM and aftermarket demand[2]"SMM: Analysis of China's Secondary Aluminum Market and Price Assessment Methodology for 2025 [SMM Aluminum Industry Conference]," SMM, metal.com.. This demographic dividend in Asia creates a structural growth foundation that insulates the market from short-term disruptions in developed economies.

Shift to Lightweight Alloys for Performance and Fuel-Efficiency

Material innovation drives premium segment expansion as manufacturers pursue weight reduction and performance optimization strategies. Renthal's Ultralight rear sprockets achieve 66% weight reduction compared to steel alternatives through precision CNC machining of 7075 T6 aluminum, directly addressing unsprung weight concerns that affect handling and acceleration. The shift toward aluminum and titanium composites reflects broader industry trends toward electrification, where every gram of weight reduction translates to extended range and improved performance metrics. Advanced surface treatments, including hard anodizing and DLC coatings, extend component life while maintaining weight advantages, addressing traditional durability concerns associated with lightweight materials. This trend accelerates as electric motorcycle adoption increases, with manufacturers prioritizing weight optimization to maximize battery efficiency and range capabilities.

Rising Popularity of Sports/Performance Bikes Globally

Performance motorcycle segments drive disproportionate value creation through premium component demand and frequent replacement cycles. Sports bikes require high-strength, precision-manufactured sprockets capable of handling aggressive acceleration and deceleration forces, with racing applications demanding specialized materials and tooth profiles optimized for power transfer efficiency. Regina's racing chains command EUR 177.27 for O-ring 520 configurations, reflecting the premium pricing power in performance segments where durability and weight considerations outweigh cost sensitivity[3]"REGINA RACING CHAIN - PROVEN QUALITY RACING CHAINS," tenkateracingproducts.com.. The segment's growth correlates with rising disposable incomes in emerging markets and sustained enthusiasm in developed economies, where performance modifications and track-day activities drive aftermarket spending. Triumph's 2026 TF 250-E and TF 450-E Enduro models exemplify OEM focus on competition-oriented platforms that require specialized drivetrain components designed for clutchless shifting and sustained high-load operation.

Rapid Growth of E-Commerce Aftermarket Platforms

Digital transformation reshapes distribution channels and customer acquisition strategies across the motorcycle parts ecosystem. Automotive aftermarket e-commerce grew over 30% in 2020 to exceed USD 30 billion, with projections reaching USD 65 billion by 2030, driven by price transparency and convenience factors that particularly benefit commodity components like chains and sprockets. E-commerce platforms enable smaller manufacturers to reach global markets without traditional distributor networks, intensifying competition while expanding consumer choice and driving down prices. The shift toward direct-to-consumer sales models allows manufacturers to capture higher margins while providing detailed fitment information and technical support that builds brand loyalty. Motorcycle consumers demonstrate balanced preferences between OEM and aftermarket parts, with 55% purchasing through local dealerships and 53% through specialty online platforms, indicating multi-channel strategies are essential for market participation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Belt/Shaft Final-Drive in Premium Motorcycles | -1.1% | North America and EU, Premium Segments Globally | Long Term (≥ 4 Years) |

| Raw-Material Price Volatility (Steel, Aluminum) | -0.8% | Global, Concentrated in Manufacturing Hubs | Short Term (≤ 2 Years) |

| Increasing Use of Sealed, Maintenance-Free Drivetrains | -0.7% | Global, Accelerating in Urban and Commuter Motorcycle Segments | Medium Term (2-4 Years) |

| Emerging Regulations on Metallic Wear-Debris Emissions | -0.6% | EU and Developed Asian Markets, Gradual Global Spillover | Long Term (≥ 4 Years) |

| Source: Mordor Intelligence | |||

Shift Toward Belt/Shaft Final-Drive in Premium Motorcycles

Alternative drivetrain technologies gain traction in segments where maintenance convenience and noise reduction outweigh traditional chain-drive advantages. Belt drives eliminate lubrication requirements and operate significantly quieter than chains, with Gates' Moto X5 systems achieving up to 15 dB noise reduction compared to conventional chains while claiming 84% longer service life. Premium motorcycle manufacturers increasingly adopt shaft drives for touring and adventure segments, where sealed, maintenance-free operation justifies higher initial costs and 20-25% transmission efficiency penalties. The trend accelerates in electric motorcycle applications, where belt drives complement the quiet operation characteristics of electric powertrains while reducing overall system complexity. However, the shift remains concentrated in specific segments, as performance applications continue to favor chains for their superior efficiency and gear ratio flexibility.

Raw-Material Price Volatility (Steel, Aluminum)

Commodity price fluctuations create margin pressure and supply chain uncertainty that particularly affects cost-sensitive market segments. Steel prices are projected to range from USD 800 to 1,000 per ton in 2024, while aluminum prices are forecast at USD 2,500 to 3,000 per metric ton, with energy costs and geopolitical factors driving continued volatility. Iron ore prices are expected to decline 9% in 2024 according to World Bank projections, potentially easing steel input costs, though supply disruptions and trade restrictions present upside risks. The 25% U.S. tariff on imported motorcycle parts, effective May 2025, exemplifies policy-driven cost pressures, with repair costs increasing 18-30% and forcing aftermarket participants to seek USMCA-compliant alternatives or absorb margin compression. Manufacturers respond through long-term supply contracts, material substitution strategies, and vertical integration initiatives to mitigate price volatility impacts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Steel Dominance Faces Composite Challenge

Steel commands 72.03% market share in 2024, reflecting its optimal balance of strength, cost-effectiveness, and manufacturing scalability across diverse motorcycle applications. The material's dominance stems from proven durability in high-torque applications and established supply chains that support both OEM and aftermarket demand. Aluminum alloy segments capture significant market share through weight-conscious applications, particularly in performance and electric motorcycle segments where unsprung weight reduction directly impacts handling and efficiency metrics. Composite materials, including titanium and carbon-infused variants, represent the fastest-growing segment at 8.91% CAGR through 2025-2030, driven by premium applications and electric motorcycle adoption, where weight optimization justifies higher material costs.

Advanced manufacturing techniques enable steel sprockets to incorporate surface treatments and alloy compositions that extend service life while maintaining cost advantages. C45 steel and SCM415 chromoly alloys undergo heat treatment and sandblasting processes that enhance wear resistance and reduce surface tension, addressing traditional durability concerns. The emergence of hybrid designs, such as Renthal's Twinring technology that bonds hardened steel outer rings to aluminum inner cores, demonstrates material innovation strategies that capture benefits from multiple material types while addressing specific performance requirements.

By Sprocket Type: Standard Configurations Lead Market Evolution

Standard chain sprockets maintain 64.52% market share in 2024, supported by broad OEM adoption and aftermarket interchangeability that reduces inventory complexity for distributors and retailers. These configurations benefit from established manufacturing processes and economies of scale that enable competitive pricing across volume applications. Non-standard sprockets emerge as the fastest-growing segment at 7.18% CAGR, driven by customization trends and performance applications requiring specialized tooth counts, materials, or mounting configurations. The growth reflects increasing consumer sophistication and willingness to invest in drivetrain optimization for specific riding applications.

Quick-change sprocket systems gain traction in racing and enthusiast segments, where gear ratio adjustments enable performance tuning for different track conditions or riding styles. Superlite's quick-change designs, compatible with AFAM PCD-3 and PCD-4 carriers, exemplify modular approaches that reduce maintenance time while expanding customization options. The segment evolution indicates market maturation and segmentation, with manufacturers developing specialized products for distinct user groups rather than pursuing one-size-fits-all approaches.

By Chain Type: O-Ring Technology Drives Premium Adoption

O-ring chains command 46.04% market share in 2024, reflecting widespread adoption of sealed chain technology that extends service intervals and reduces maintenance requirements. The technology's success stems from its ability to retain internal lubrication while excluding contaminants, addressing primary failure modes in conventional roller chains. X-ring chains represent the fastest-growing segment at 6.82% CAGR, offering improved sealing performance and reduced friction compared to traditional O-ring designs through optimized seal geometry and materials. Standard roller chains maintain relevance in cost-sensitive applications and specific use cases where sealed chain benefits do not justify premium pricing.

The sealed chain segment benefits from motorcycle industry trends toward reduced maintenance and improved reliability, particularly as urban commuting applications increase, where regular maintenance access may be limited. JT Sprockets' production of 18 million sprockets annually supports sealed chain applications across global markets, with distribution centers in London and Atlanta enabling rapid fulfillment for aftermarket demand. Advanced seal materials and precision manufacturing enable X-ring chains to achieve superior performance while maintaining competitive pricing relative to O-ring alternatives.

By Vehicle Type: Standard Motorcycles Anchor Market Stability

Standard motorcycles account for 51.31% market share in 2024, providing a stable demand foundation across global markets where basic transportation and commuting applications dominate motorcycle usage patterns. This segment benefits from high replacement frequency due to utilitarian usage patterns and cost-sensitive purchasing decisions that favor proven, reliable drivetrain components. Sports bikes emerge as the fastest-growing segment at 7.53% CAGR through 2025-2030, driven by performance enthusiasts and rising disposable incomes in emerging markets that enable recreational motorcycle purchases. Cruisers and off-road bikes contribute meaningful market shares while serving distinct user requirements for comfort-oriented and durability-focused applications, respectively.

The UK motorcycle market demonstrates segment evolution dynamics, with modern classics growing 31.7% in 2024 while adventure and naked segments declined 29% and 28.1% respectively in early 2025, indicating consumer preference shifts toward heritage-inspired designs and away from complex touring configurations. Electric motorcycle registrations remain limited at 3.2% of 2024 UK sales, with most electric units concentrated in sub-15-horsepower categories that may utilize alternative drivetrain architectures, suggesting conventional chain-sprocket systems retain dominance across meaningful market segments.

By Propulsion Type: ICE Dominance Faces Electric Transition

Internal combustion engine motorcycles command 88.01% market share in 2024, reflecting the continued dominance of conventional powertrains across global motorcycle markets. This segment benefits from established supply chains, proven technology, and cost advantages that sustain market leadership despite emerging electric alternatives. Electric motorcycles represent the fastest-growing segment at 12.39% CAGR through 2025-2030, though growth occurs from a small base and faces infrastructure and cost challenges that limit near-term market penetration.

Other propulsion types, including CNG and LPG, remain niche applications with limited commercial adoption outside specific regional markets. Electric motorcycle adoption creates complex implications for chain-sprocket demand, as some designs utilize hub motors or belt drives that eliminate conventional final drive components, while others retain chain systems for cost optimization or performance characteristics.

By Distribution Channel: Aftermarket Leadership Reflects Replacement Cycle

The aftermarket channel dominates with 62.41% market share in 2024, reflecting the replacement-driven nature of chain-sprocket demand, where components require periodic renewal due to wear and maintenance cycles. This channel benefits from diverse product offerings, competitive pricing, and established distribution networks that serve independent repair facilities and consumer direct purchases. OEM channels capture 37.59% market share while growing faster at 6.32% CAGR, driven by increasing new motorcycle sales and manufacturers' efforts to capture aftermarket revenue through genuine parts programs and extended service offerings.

E-commerce transformation reshapes distribution dynamics, with motorcycle consumers utilizing multiple channels including local dealerships (55%), specialty websites (53%), and large online retailers (47%) for parts purchases. The balanced channel preference indicates successful multi-channel strategies require both digital presence and traditional distribution relationships. European aftermarket analysis suggests private-label penetration could reach 20-30% by 2025, with up to 50% penetration in common maintenance categories, creating margin pressure for branded manufacturers while expanding volume opportunities for contract manufacturers.

Geography Analysis

Asia-Pacific maintains market leadership with 49.11% share in 2024, driven by massive motorcycle production volumes and expanding two-wheeler adoption across China, India, and Southeast Asia. China's motorcycle exports reached 36.76 million units in 2024, representing 55% of global sales, with 14.5 million internal combustion units requiring conventional chain-sprocket systems. India's domestic motorcycle market reached 15.9 million units in FY2023, predominantly sub-125cc models that rely heavily on chain drives due to cost considerations and performance requirements. The region benefits from established manufacturing ecosystems, cost-competitive production capabilities, and growing middle-class populations that drive both utilitarian and recreational motorcycle adoption. Japan's keiretsu supplier networks ensure high-quality component production with close OEM collaboration, while China's manufacturing scale enables cost leadership across volume applications.

North America and Europe represent mature markets with distinct characteristics that influence chain-sprocket demand patterns. The European motorcycle market showed mixed performance in 2024, with Italy and Spain posting positive growth while France and Germany declined modestly, reflecting economic uncertainty and regulatory pressures. New EU noise regulations effective January 2025 expand measurement requirements across broader operating conditions, potentially increasing demand for precision-manufactured, low-noise drivetrain components. North American markets face trade policy impacts, with 25% tariffs on imported motorcycle parts driving cost increases and supply chain restructuring toward USMCA-compliant sources.

The Middle East and Africa emerges as the fastest-growing region at 7.92% CAGR through 2025-2030, reflecting infrastructure development, rising disposable incomes, and expanding urban populations that drive motorcycle adoption for both transportation and recreational purposes. The region benefits from increasing government investments in transportation infrastructure and growing middle-class populations seeking affordable mobility solutions. Latin America demonstrates strong growth momentum with Q1 2025 sales increasing 22% year-over-year, driven by rising disposable incomes and urbanization trends that favor two-wheeler adoption. These emerging markets present significant opportunities for chain-sprocket manufacturers, though success requires adaptation to local cost structures, distribution networks, and usage patterns that may differ substantially from developed market requirements.

Competitive Landscape

The motorcycle chain sprocket market exhibits moderate fragmentation with established players leveraging specialized manufacturing capabilities and regional distribution strengths. JT Sprockets emerges as a volume leader, claiming production of 18 million sprockets annually with global distribution across 70+ countries and manufacturing facilities in Thailand that serve both OEM and aftermarket segments. The competitive landscape reflects geographic specialization patterns, with Japanese manufacturers like DID (Daido Kogyo) emphasizing precision engineering and quality, European players like Renthal focusing on premium performance applications, and emerging manufacturers pursuing cost leadership through scale and vertical integration strategies.

Technology differentiation centers on materials innovation, manufacturing precision, and integrated solutions that address evolving customer requirements. Renthal's Twinring technology demonstrates advanced bonding techniques that combine steel durability with aluminum weight advantages, while Regina's racing heritage enables premium positioning in performance segments.

The August 2025 partnership between Oriental Chain Industry and Katayama Chain exemplifies consolidation trends as mid-tier suppliers seek scale advantages and operational efficiencies to compete against larger players. White-space opportunities exist in electric motorcycle applications, smart monitoring systems, and sustainable manufacturing processes that address emerging regulatory and customer requirements while defending against alternative drivetrain technologies.

Motorcycle Chain Sprocket Industry Leaders

-

JT Sprockets (HMA Group)

-

Renthal

-

RK Takasago Chain

-

DID (Daido Kogyo Co. Ltd.)

-

Tsubaki

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Oriental Chain Industry Co., Ltd. announced a strategic business alliance with Katayama Chain Co., Ltd. to consolidate manufacturing and distribution capabilities in response to domestic labor shortages and intensified global competition. The partnership enables Oriental to supply branded roller chains to KANA while receiving sprockets and leveraging KANA's logistics network, potentially strengthening market position through improved operational efficiency and expanded product offerings.

- May 2024: New 25% U.S. tariffs on imported motorcycle parts took effect, causing 18-30% increases in repair costs and driving supply chain restructuring toward USMCA-compliant sources. The policy change forces aftermarket participants to seek alternative suppliers or absorb margin compression, with examples including EBC USA brake pads offering 22% savings and Race Tech fork tubes providing 18% cost advantages compared to tariff-affected import.

Global Motorcycle Chain Sprocket Market Report Scope

| Steel |

| Aluminum Alloy |

| Others (Titanium, Carbon-Infused Composites, etc.) |

| Standard Chain Sprocket |

| Non-Standard Chain Sprocket |

| O-Ring Chain |

| X-Ring Chain |

| Standard Roller Chain |

| Standard Motorcycles |

| Sports Bikes |

| Cruisers |

| Off-Road Bikes |

| Internal Combustion Engine (ICE) |

| Electric |

| Others (CNG/LPG) |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Material Type | Steel | |

| Aluminum Alloy | ||

| Others (Titanium, Carbon-Infused Composites, etc.) | ||

| By Sprocket Type | Standard Chain Sprocket | |

| Non-Standard Chain Sprocket | ||

| By Chain Type | O-Ring Chain | |

| X-Ring Chain | ||

| Standard Roller Chain | ||

| By Vehicle Type | Standard Motorcycles | |

| Sports Bikes | ||

| Cruisers | ||

| Off-Road Bikes | ||

| By Propulsion Type | Internal Combustion Engine (ICE) | |

| Electric | ||

| Others (CNG/LPG) | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

Which region leads global demand?

Asia-Pacific accounts for 49.11% of global revenue thanks to high two-wheeler sales and extensive aftermarket needs.

What material dominates current sprocket production?

Steel holds 72.03% share because of its favorable cost-to-strength balance and mature supply chain.

Which vehicle segment is growing fastest?

Sports motorcycles post a 7.53% CAGR as performance enthusiasts seek lightweight, high-strength drivetrain parts.

How are noise regulations affecting component design?

The EU R41.05 rule broadens sound-testing ranges, prompting OEMs to specify quieter sealed chains and precision-cut sprockets that limit drivetrain noise.

What impact do U.S. tariffs have on pricing?

The 25% tariff on imported parts applied in 2024 raised repair costs 18-30%, steering distributors toward USMCA-based sourcing to mitigate price hikes.

Page last updated on: