Sleep Apnea Implant Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.7 Billion |

| Market Size (2031) | USD 1.37 Billion |

| Growth Rate (2026 - 2031) | 14.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sleep Apnea Implant Market Analysis by Mordor Intelligence

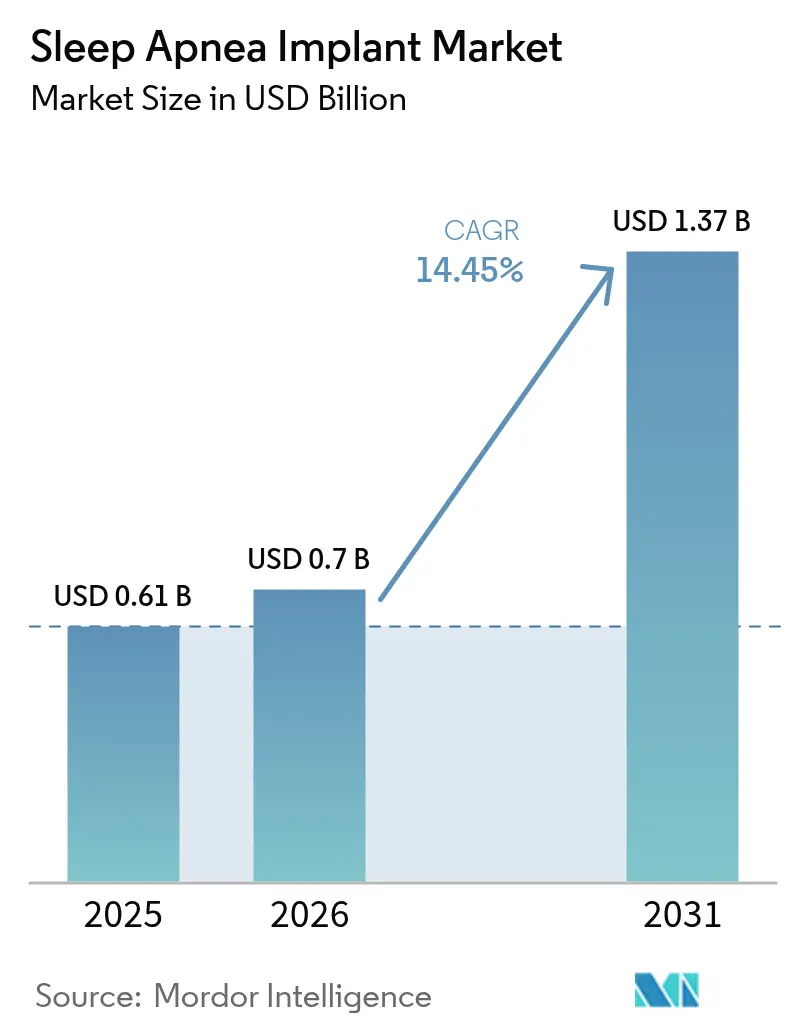

The sleep apnea implant market size is expected to grow from USD 0.61 billion in 2025 to USD 0.7 billion in 2026 and is forecast to reach USD 1.37 billion by 2031 at 14.45% CAGR over 2026-2031. This growth trajectory signals broad recognition that positive airway pressure masks alone cannot meet the therapeutic needs of millions of moderate-to-severe patients. Surgeons and sleep physicians increasingly adopt neurostimulation, palatal inserts, and other implantable solutions as evidence accumulates, reimbursement widens, and device design becomes less invasive. Momentum is reinforced by AI-enabled parameter tuning that delivers personalized therapy without repeated clinic visits, while streamlined diagnostic tools identify candidates sooner. The sleep apnea implant market therefore occupies a pivotal role in modern respiratory care pathways, drawing interest from hospitals, ambulatory surgical centers, and investors alike.

Key Report Takeaways

- By product type, hypoglossal neurostimulation accounted for 60.55% of sleep apnea implant market share in 2025; trigeminal systems are forecast to expand at a 20.12% CAGR to 2031.

- By indication, obstructive sleep apnea represented 78.35% of the sleep apnea implant market size in 2025, whereas central sleep apnea is set to rise at a 16.55% CAGR through 2031.

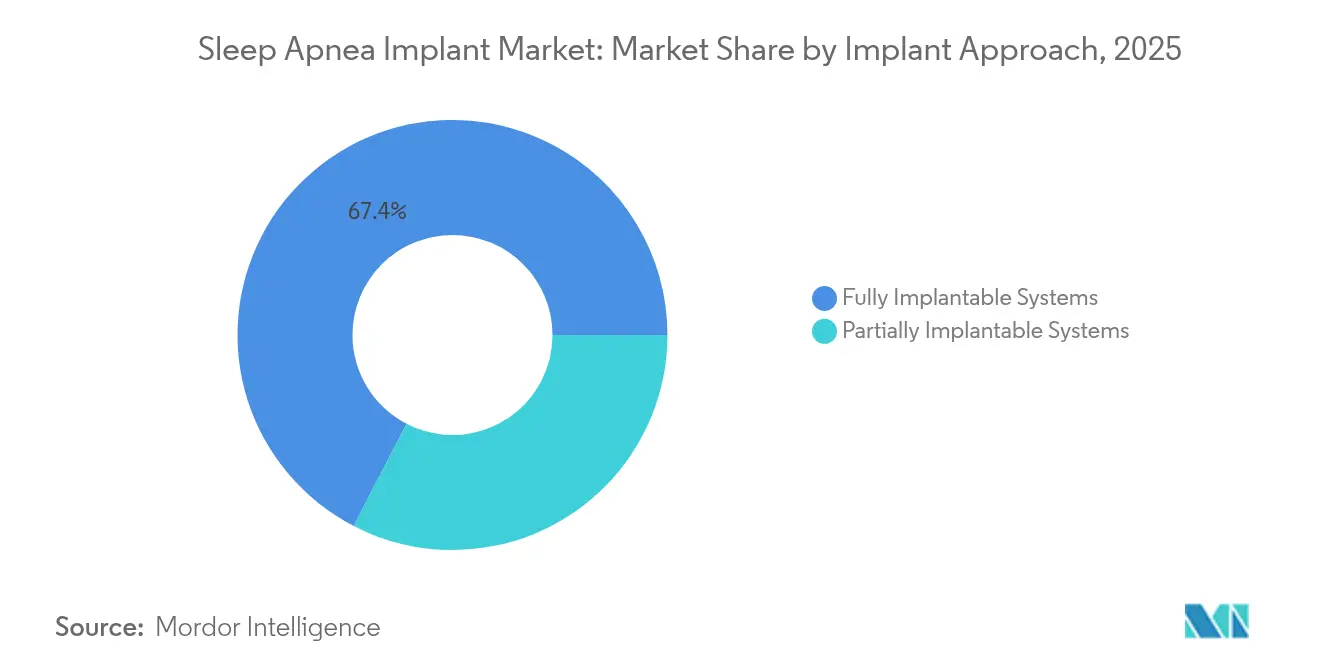

- By implant approach, fully implantable systems commanded 67.40% of the sleep apnea implant market size in 2025, while partially implantable systems will advance at a 23.45% CAGR during 2026-2031.

- By end user, hospitals held 53.50% revenue in 2025, while ambulatory surgical centers are projected to post the fastest 17.40% CAGR through 2031.

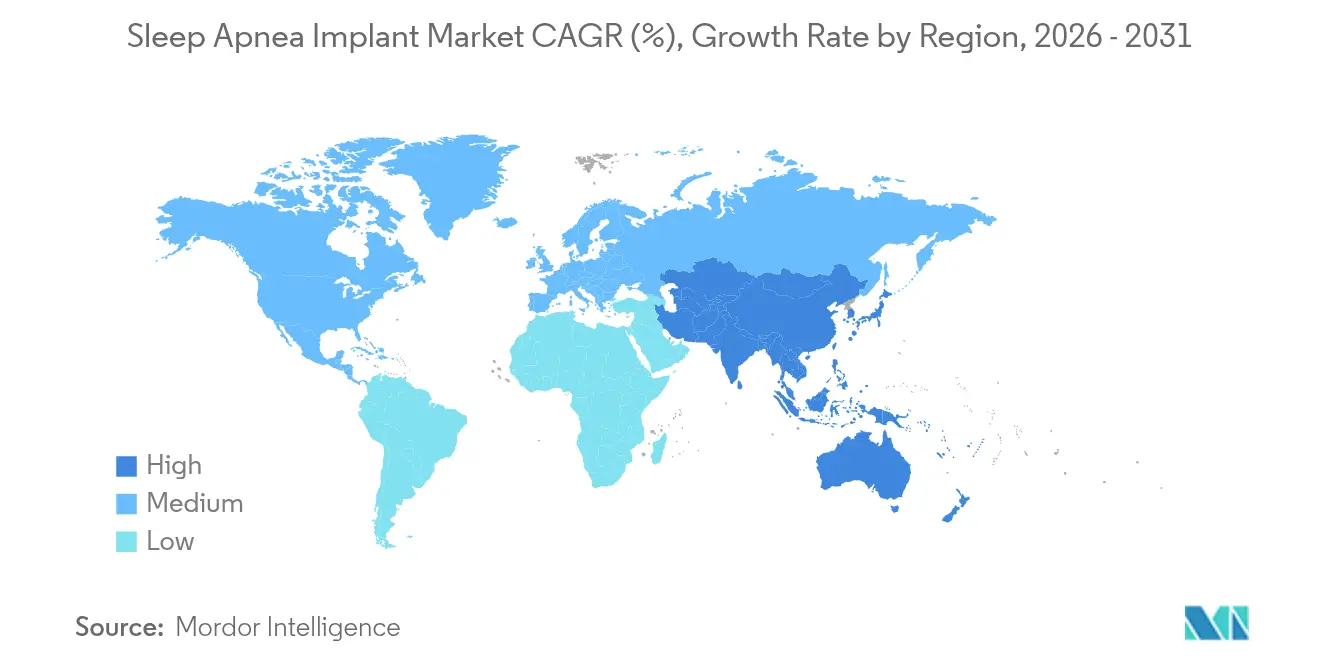

- By geography, North America held 45.80% revenue in 2025, while Asia-Pacific is projected to grow at fastest CAGR of 15.20%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sleep Apnea Implant Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence & earlier diagnosis | +3.0% | North America, Asia Pacific | Medium term (2-4 years) |

| CPAP non-compliance shifting demand to implants | +2.6% | North America, Europe | Medium term (2-4 years) |

| Product approvals & widening reimbursement | +2.8% | United States, Western Europe | Short term (≤ 2 years) |

| Advances in neurostimulation accuracy & battery life | +2.5% | Global | Long term (≥ 4 years) |

| Expansion of ENT outpatient surgical capacity | +1.7% | Global emerging markets | Medium term (2-4 years) |

| Higher healthcare spend & sleep-health awareness campaigns | +1.4% | Middle East, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence and Diagnosis Rates of Sleep Apnea Disorders

The world’s diagnosed patient pool rises every quarter as next-generation home sleep tests route encrypted data directly to clinicians, bypassing smartphone dependency and cutting time from suspicion to confirmation. Wearable devices with AI algorithms now screen consumers during routine wellness tracking, flagging abnormal respiration and guiding them toward formal sleep studies. Earlier diagnosis feeds the surgical pipeline, driving consistent double-digit procedure growth inside the sleep apnea implant market. Hospitals answer demand by creating one-stop clinics that combine polysomnography, drug-induced endoscopy, and same-day eligibility assessment. Payers see value when early intervention lessens downstream cardiovascular claims, reinforcing reimbursement policies that treat implants as a logical step once mask therapy fails.

Growing CPAP Non-Compliance Creating Demand for Alternative Therapies

Four in ten users abandon continuous positive airway pressure within a year, mainly due to mask discomfort, noise, and disrupted bed-partner sleep[1]Cleveland Clinic, “Hypoglossal Nerve Stimulation Outcomes,” clevelandclinic.org. Hypoglossal neurostimulation achieves 81% nightly adherence, translating into larger reductions in apnea-hypopnea index and daytime sleepiness. Physicians increasingly position implants immediately after documented CPAP intolerance, broadening the sleep apnea implant market and bringing down disease burden earlier in the care continuum. Payers prefer the predictable compliance curve despite higher up-front device cost because it cuts emergency visits for hypertension and arrhythmia. Remote monitoring portals let clinicians verify usage data, spot technical issues, and adjust amplitude without clinic visits, further supporting real-world adherence.

Product Approvals and Favorable Reimbursement for Implantable Therapies

The FDA expanded indication criteria for hypoglossal systems to apnea-hypopnea index values up to 100 and body-mass-index thresholds to 40 kg/m², raising the eligible U.S. cohort by thousands each year[2]U.S. Food & Drug Administration, “Inspire Upper Airway Stimulation System – Expanded Indications,” fda.gov. United States CPT code 64568 now covers roughly 80% of insured lives, while the Centers for Medicare & Medicaid Services has issued unambiguous billing guidance that speeds claims processing[3]Centers for Medicare & Medicaid Services, “Billing and Coding: Hypoglossal Nerve Stimulation,” cms.gov. In Europe, health technology assessment bodies in Germany and France have issued positive coverage opinions after registry data showed sustained symptom control, improving surgeon confidence to recommend implants earlier. Together these measures flatten out-of-pocket hurdles, giving the sleep apnea implant market a clear runway for scale.

Advancements in Neurostimulation Technology Improving Therapy Efficacy

Fifth-generation pulse generators now integrate dual accelerometers, airway pressure sensors, and adaptive algorithms that tailor stimulation in real time. Bilateral hypoglossal designs gently protrude the tongue on both sides, securing an unobstructed airway even in patients with asymmetric anatomy. Surgical refinements reduce incisions from three to two and cut operating time below 90 minutes, a key requirement for ambulatory surgical centers. MRI-conditional labeling eliminates a historical contraindication for cardiac patients who often need imaging, increasing physician willingness to implant. These breakthroughs jointly enhance long-term outcomes and overall patient experience, propelling the sleep apnea implant market into mainstream ENT practice.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure and device costs | −3.7% | Emerging markets | Long term (≥ 4 years) |

| Limited long-term clinical evidence | −2.3% | Global | Medium term (2-4 years) |

| Surgical expertise gap and hypoglossal implant learning curve | −1.9% | Asia Pacific, Latin America | Medium term (2-4 years) |

| Stringent regulatory pathways & heterogeneous payer coverage | −1.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Procedure and Device Costs Limiting Patient Affordability

Total expenses place implants beyond reach in health systems where insurance penetration is low or copay ceilings are strict. Even in markets with coverage, coinsurance often equals several months of median income. Manufacturers strive to lower cost of goods through scale manufacturing and component consolidation, but pricing flexibility is constrained by advanced electronics and regulatory compliance costs. Affordable financing programs and outcomes-based contracting emerge as partial solutions, yet economic disparity still caps penetration of the sleep apnea implant market in parts of Latin America, Africa, and Southeast Asia.

Limited Long-Term Clinical Evidence and Post-Market Follow-Up Data

Most pivotal trials monitor outcomes for only three to five years. Registry studies like ADHERE provide encouraging real-world insights but lack randomized controls, leaving some payers and conservative clinicians unconvinced about durability. Trigeminal and phrenic systems, while promising, have even shorter follow-up. This evidence gap slows guideline inclusion and reimbursement outside leading economies, tempering immediate growth prospects of the sleep apnea implant market. Multi-center 10-year follow-up studies are now underway and are likely to accelerate acceptance once published.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hypoglossal Dominance Meets Fast-Moving Trigeminal Challengers

Hypoglossal neurostimulation delivered 60.55% sleep apnea implant market share in 2025. More than 90,000 cumulative patients show substantial apnea-hypopnea index reduction, loud snoring decline, and improved quality-of-life scores. Inspire Medical Systems’ newest pulse generator extends battery life to 11 years, cutting lifetime revision risk. Medtronic and LivaNova have pilot programs that add multi-contact electrodes, positioning themselves for future launches. Palatal implants address mild cases but suffer from variable efficacy and limited coverage, keeping their contribution minor.

Trigeminal stimulators are poised to grow at 20.12% CAGR. Submental placement avoids a chest pocket, appealing to appearance-sensitive patients. Early clinical work indicates selective modulation of sleep architecture and high safety margins, making this category a magnet for venture capital. Competitive dynamics hinge on miniaturization, intuitive app interfaces, and MRI safety features. Strong momentum suggests trigeminal devices could capture a meaningful slice of the sleep apnea implant market by late decade.

By Indication: Obstructive Sleep Apnea Dominates While Central Variant Accelerates

Obstructive cases accounted for 78.35% of the sleep apnea implant market size in 2025. Drug-induced sleep endoscopy helps surgeons predict responders, improving surgical success rates above 75% in several prospective cohorts. Cardiologists and sleep specialists collaborate to identify anatomically driven obstruction earlier, funneling patients to implant programs before comorbidities escalate.

Central sleep apnea volumes will grow 16.55% annually as phrenic nerve stimulation gains traction for heart-failure patients who cannot tolerate adaptive servo-ventilation. MRI-conditional status granted in 2024 removes an obstacle to implantation in this high-imaging group aasm.org. Complex sleep apnea syndrome remains the smallest share but offers significant unmet need, providing room for hybrid solutions that combine pharmacology, positional therapy, and neurostimulation.

By Implant Approach: Fully Implanted Systems Retain Scale Advantage

Fully implanted systems captured 67.40% of the sleep apnea implant market size in 2025. No external components translate to higher nightly adherence and fewer lifestyle restrictions. Familiar chest pocket implantation mirrors cardiac rhythm procedures, enabling rapid skill transfer among thoracic surgeons. Battery densification delivers over a decade of service life without enlarging the pulse generator footprint.

Partially implanted systems forecast a 23.45% CAGR. Nyxoah’s bilateral design uses a wafer-thin activator chip worn under the chin during sleep, allowing a single small incision. Wireless firmware updates permit parameter optimization without surgery, reducing lifetime care costs. As community surgeons master simpler procedures, outpatient volumes rise and diversify the sleep apnea implant market.

By End User: Hospital Dominance Persists While Ambulatory Centers Surge

Hospitals secured 53.50% case volume in 2025, leveraging multidisciplinary sleep teams, imaging suites, and intensive post-operative monitoring. University centers develop fellowship programs that export surgical know-how to regional affiliates. Dedicated sleep surgery wards streamline workup, implantation, and overnight titration, minimizing patient travel.

Ambulatory surgical centers post an 17.40% CAGR as payers prioritize lower facility fees and patients prefer same-day discharge. Two-incision techniques and local anesthesia protocols shorten turnover times, aligning with outpatient workflow. High-throughput ASCs in the United States report profit margins comparable to elective orthopedic procedures, attracting private-equity funding that enlarges capacity across the sleep apnea implant market.

Geography Analysis

North America held 45.80% of global revenue in 2025 and remains the anchor of the sleep apnea implant market. More than 1,400 certified U.S. facilities perform hypoglossal implantation under clear Centers for Medicare & Medicaid Services coding. Commercial payers rapidly aligned policies, citing real-world data showing reduced cardiovascular hospitalizations. The expanding obesity epidemic sustains a large eligible pool, while Canada pilots public reimbursement in four provinces, signaling broader adoption.

Europe ranks second by revenue. Germany, France, and the United Kingdom drive procedure counts through early CE-mark access, supportive insurance codes, and robust clinical research networks. The European Investment Bank’s EUR 37.5 million loan to Nyxoah underpins scale-up of bilateral devices. Belgian registries report 76% surgical success at twelve-month follow-up with mean nightly therapy use exceeding seven hours. Southern and Eastern European markets, although nascent, benefit from cross-border referral programs and surgeon training consortia.

Asia Pacific is the fastest climber with a projected 15.20% CAGR through 2031. Japan enjoys near-universal health coverage and early technology adoption, facilitating steady implant volumes. China uses a priority review channel for devices already cleared by the FDA, shortening time to market. Local distributors establish training hubs in Beijing, Shanghai, and Guangzhou to address the surgical skill gap. India’s urban middle class shows heightened awareness, yet high out-of-pocket burden tempers penetration. Government schemes that subsidize advanced therapies for low-income groups could unlock latent demand, fostering further expansion of the sleep apnea implant market.

South America and the Middle East & Africa jointly account for less than 10% of global revenue but exhibit green shoots. Brazilian private hospitals integrate implants into comprehensive weight-loss programs, and insurance companies reimburse when CPAP fails. Gulf Cooperation Council hospitals invest in imported expertise to attract expatriate patients seeking premium care. Currency volatility and import tariffs challenge pricing strategies, but the long-term outlook remains positive as economies diversify and healthcare spending rises.

Competitive Landscape

The sleep apnea implant market is concentrated. Inspire Medical Systems controls roughly 85% of neurostimulation revenue, having treated more than 100,000 patients globally and amassed extensive long-term evidence. Nyxoah positions its Genio bilateral system on incision reduction and symmetrical tongue control, while LivaNova’s aura6000 introduces multi-point tongue electrodes aimed at difficult anatomies. Medtronic leverages its cardiac rhythm management heritage, collaborating with academic centers to develop sensor-heavy generators capable of adaptive air-flow detection.

Strategic partnerships reshape competition. ResMed teams with Nyxoah to integrate home diagnostics, cloud monitoring, and implant therapy into one continuum, enhancing data flow across the patient journey. ZOLL Medical bundles phrenic stimulation with its cardiac portfolio, tapping cardiology practices as a growth channel. Venture capital interest stays strong; XII Medical raised USD 45 million to engineer an ultra-simplified implantation protocol for community hospitals.

Technology roadmaps emphasize miniaturization, bilateral neuromuscular control, MRI safety, and AI-based closed-loop stimulation. FDA clearance of MRI-conditional labeling for phrenic systems in 2024 resolved a key referral blocker. Pharmaceutical entry arrived via tirzepatide, the first weight-loss drug approved for apnea in obese adults, which stakeholders view as complementary rather than competitive because it does not correct anatomical collapse. Ecosystem playbooks emerge: vendors bundle patient selection software, surgical navigation, and cloud analytics to lock in provider loyalty. These moves together define a dynamic but high-barrier competitive environment inside the sleep apnea implant market.

Sleep Apnea Implant Industry Leaders

Inspire Medical Systems

LivaNova PLC

Nyxoah SA

Medtronic PLC

ZOLL Medical (Respicardia)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Inspire Medical Systems reported Q1 2025 revenue of USD 201.3 million, up 23%, and began commercial rollout of its Inspire V generator.

- May 2025: LivaNova submitted the aura6000 neurostimulation device to the FDA after OSPREY trial success.

- April 2025: Nyxoah received an FDA approvable letter for its Genio bilateral stimulator, clearing the final regulatory hurdle before U.S. launch.

- January 2025: Dianyx Innovations unveiled an AI-enabled oral appliance integrating Remote Patient Monitoring codes at CES 2025.

- December 2024: The FDA approved tirzepatide (Zepbound) for moderate-to-severe obstructive sleep apnea in obese adults.

Global Sleep Apnea Implant Market Report Scope

As per the scope of the report, a sleep apnea implant is an implantable device that stimulates the muscles of the tongue and upper airway during sleep. These implantable devices improve airflow. It's also called a hypoglossal nerve stimulator or upper airway stimulation device. The device is implanted in the upper right chest beneath the skin. The Sleep Apnea Implant Market is Segmented by Product Type (Hypoglossal Neurostimulation Devices, Phrenic Nerve Stimulator, and Palatal Implants), Indication Type (Obstructive Sleep Apnea, Central Sleep Apnea), End User (Hospitals, Ambulatory Surgical Centers), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Hypoglossal Neurostimulation Devices |

| Phrenic Nerve Stimulators |

| Palatal Implants |

| Trigeminal Nerve Stimulation Systems |

| Obstructive Sleep Apnea |

| Central Sleep Apnea |

| Complex Sleep Apnea Syndrome |

| Fully Implantable Systems |

| Partially Implantable Systems |

| Hospitals |

| Ambulatory Surgical Centers |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Hypoglossal Neurostimulation Devices | |

| Phrenic Nerve Stimulators | ||

| Palatal Implants | ||

| Trigeminal Nerve Stimulation Systems | ||

| By Indication | Obstructive Sleep Apnea | |

| Central Sleep Apnea | ||

| Complex Sleep Apnea Syndrome | ||

| By Implant Approach | Fully Implantable Systems | |

| Partially Implantable Systems | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Other End Users | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What value will the sleep apnea implant market reach by 2031?

The sleep apnea implant market is projected to reach USD 1.37 billion by 2031.

Which device type currently leads sales?

Hypoglossal neurostimulation devices command 60.55% of the sleep apnea implant market.

Why are ambulatory surgical centers important for market growth?

Shorter, minimally invasive procedures now fit ASC workflows, supporting an 17.40% CAGR for implant volumes in outpatient settings.

How has U.S. reimbursement improved for implants?

CPT 64568 covers 80% of insured lives and CMS provides clear coding rules, cutting administrative barriers to payment.

Will new drugs replace implants?

Tirzepatide helps weight-related apnea but does not correct anatomical collapse; implants remain essential for many moderate-to-severe cases.

What innovations will shape next-generation devices?

Smaller MRI-safe generators with bilateral stimulation and AI-guided sensing are expected to dominate the sleep apnea implant industry.

Page last updated on: