Skin Graft Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.41 Billion |

| Market Size (2031) | USD 3.46 Billion |

| Growth Rate (2026 - 2031) | 7.50% CAGR |

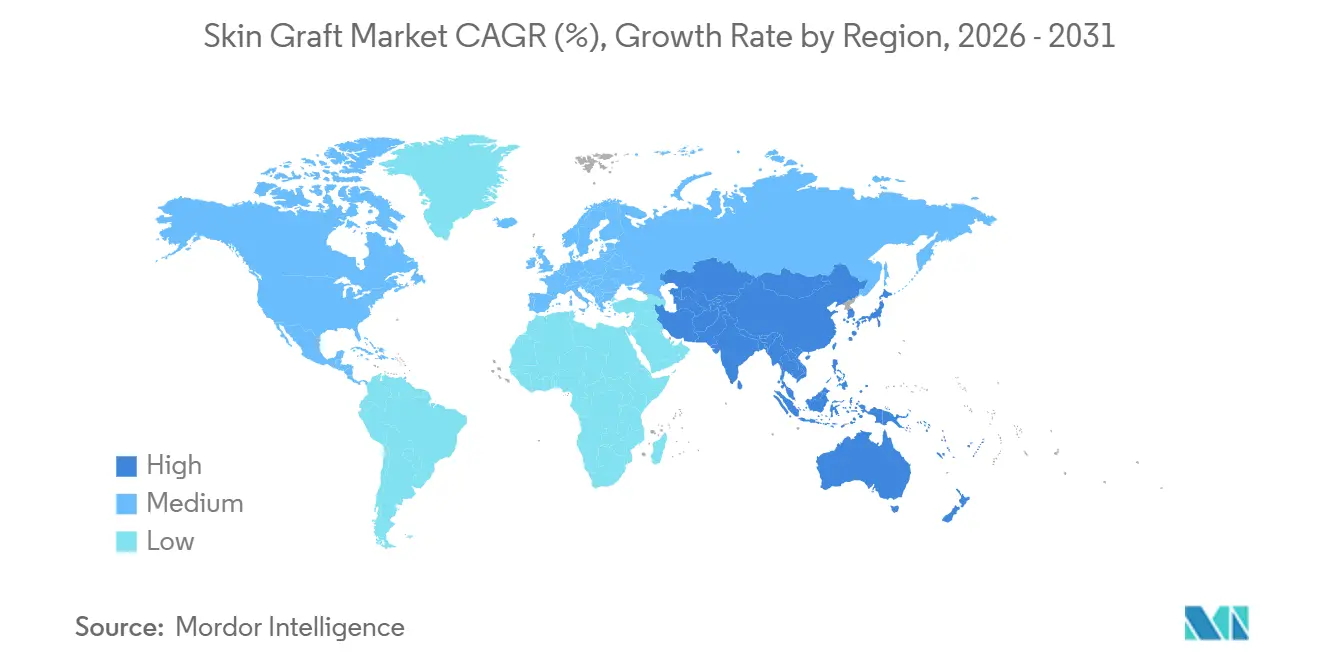

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

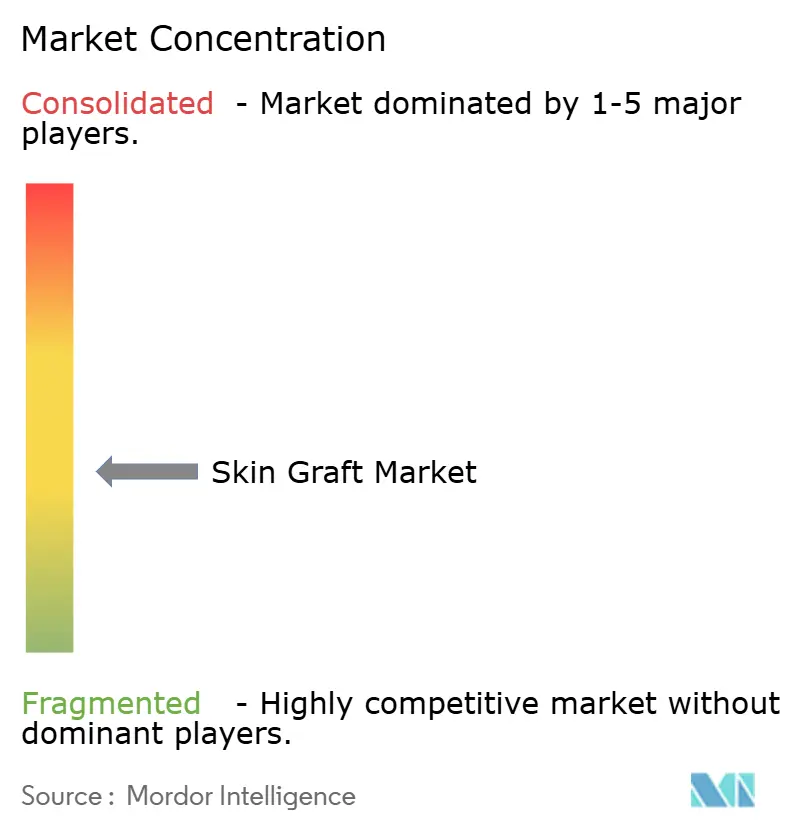

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Skin Graft Market Analysis by Mordor Intelligence

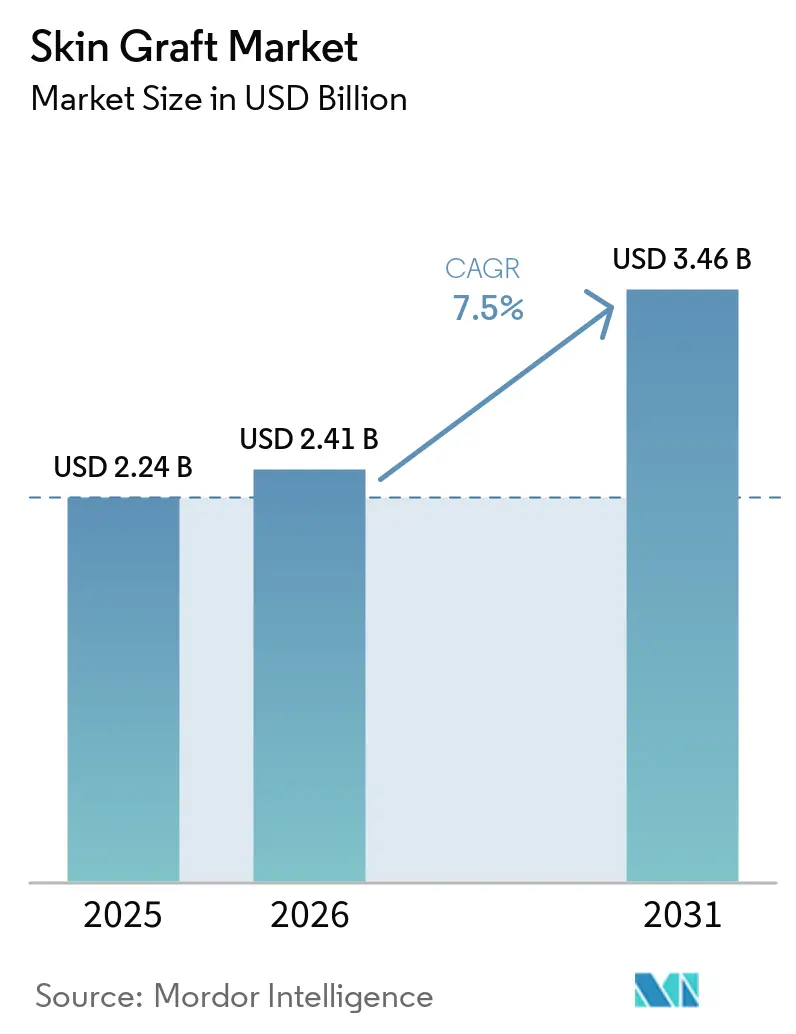

The Skin Graft Market size is expected to grow from USD 2.24 billion in 2025 to USD 2.41 billion in 2026 and is forecast to reach USD 3.46 billion by 2031 at 7.5% CAGR over 2026-2031.

The skin graft market experiences consistent demand in burn care, as full-thickness and complex thermal injuries necessitate surgical wound closure and extended reconstructive care. Additionally, the market is expanding due to chronic wounds like diabetic foot ulcers and venous leg ulcers, which drive repeat treatments and interest in advanced skin substitutes. A key trend is the shift toward products backed by strong clinical evidence and reimbursement alignment, particularly in the U.S., where site-of-care changes are influencing product access and procedure costs. North America remains the largest revenue contributor, while Asia-Pacific shows the fastest growth, supported by increasing burn cases, healthcare investments, and local manufacturing advancements.

Key Report Takeaways

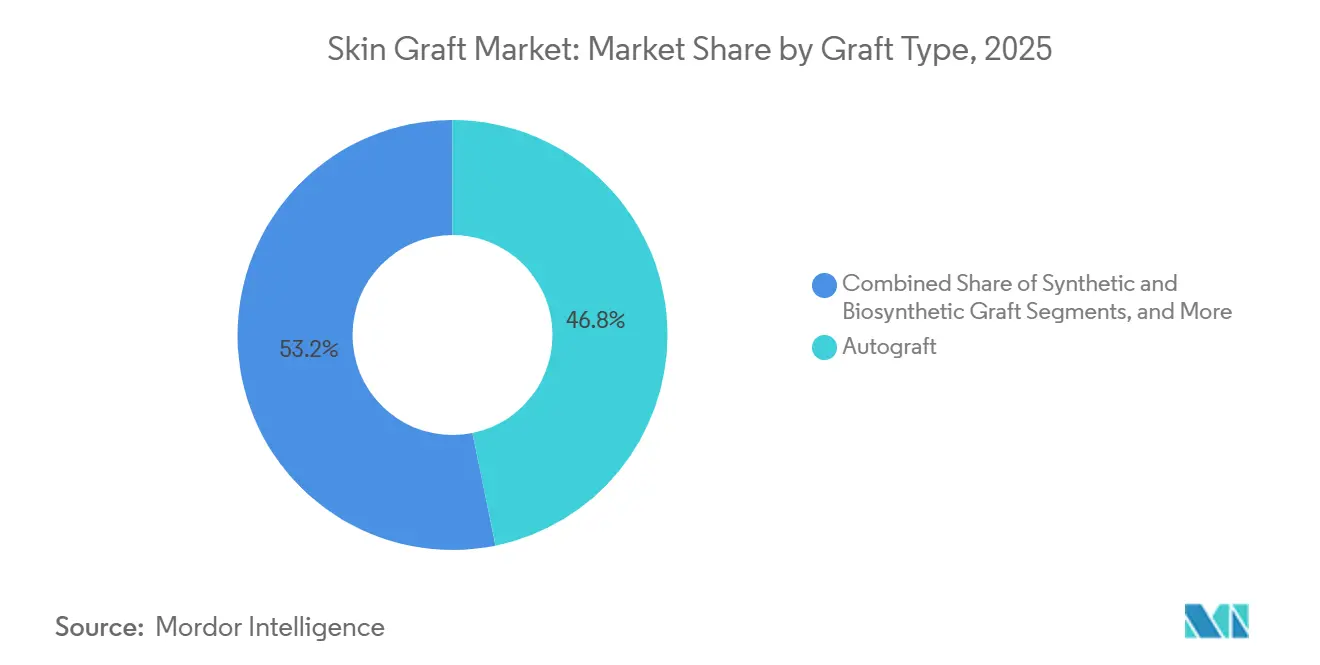

- By graft type, autograft held 46.76% of revenue in 2025, while synthetic and biosynthetic grafts are projected to expand at a 7.95% CAGR through 2026 to 2031.

- By source, human skin accounted for 67.88% of revenue in 2025, while cell-based and tissue-engineered skin is expected to grow at an 8.45% CAGR through 2026 to 2031.

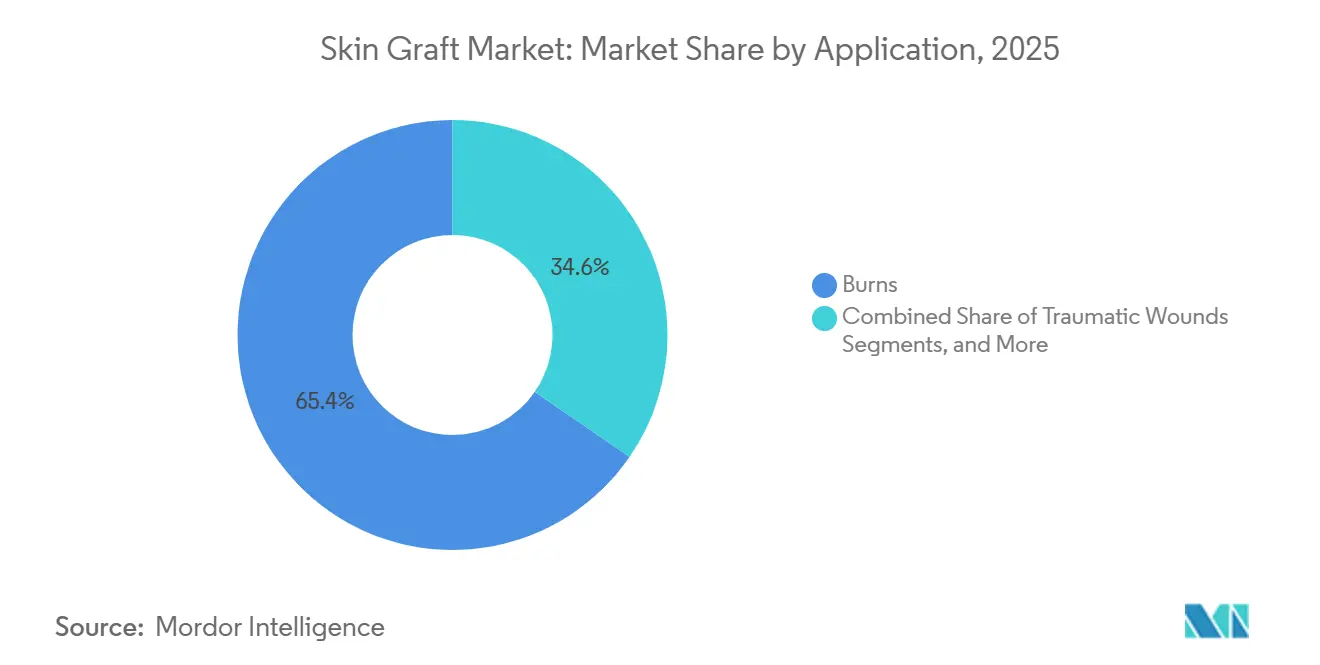

- By application, burns contributed 65.44% of revenue in 2025, while chronic wounds are expected to advance at an 8.72% CAGR through 2026 to 2031.

- By end user, hospitals captured 47.03% of revenue in 2025, while ambulatory surgical centers are projected to record the fastest growth at a 9.12% CAGR through 2026 to 2031.

- By geography, North America represented 39.52% of global revenue in 2025, while Asia-Pacific is projected to grow at an 8.88% CAGR through 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Skin Graft Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising burn and trauma case loads requiring surgical wound coverage | +2.1% | Global, highest burden in South and Southeast Asia, Sub-Saharan Africa, and Latin America | Short term (≤ 2 years) |

| Expanding use of skin substitutes in chronic wounds including diabetic foot ulcers and venous leg ulcers | +1.8% | North America and EU core, with rapid spillover to Asia-Pacific | Medium term (2-4 years) |

| Broader adoption of outpatient grafting procedures and ambulatory surgical care delivery | +1.2% | North America and Europe, with early-stage adoption in Asia-Pacific | Medium term (2-4 years) |

| Shift toward evidence-based, reimbursable products validated through FDA PMA or BLA regulatory pathways | +0.9% | North America primarily, with EU relevance under MDR compliance | Medium term (2-4 years) |

| Under-penetration of novel biological graft sources including fish-skin, placental, and umbilical cord-derived products | +0.6% | North America established, with early-stage adoption in Europe and Asia-Pacific | Long term (≥ 4 years) |

| Operating room efficiency gains from prefabricated, advanced skin graft constructs reducing procedure time | +0.4% | Global, concentrated in developed market hospital systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Burn And Trauma Case Loads Sustain Baseline Demand

The skin graft market continues to rely on burn care as a stable volume base, with 6.19 million new burn cases and 104.76 million prevalent cases recorded globally in 2024. Prevalent cases were 11.38% higher than in 1990. Projections indicate burn cases will reach 10.3 million by 2030, with burn-related disability burden rising from 11.5 million DALYs in 2030 to 14.1 million by 2050. India remains a key demand center, with burn incident cases increasing by 23.88% between 1990 and 2024, supported by improved treatment access through national insurance programs.[1]Frontiers in Public Health, “Global Trends in Thermal Burn Burden, 1990–2021: A Comprehensive Analysis for the Global Burden of Disease Study 2021,” Frontiers in Public Health, frontiersin.org. Advanced grafting is gaining traction due to its cost-effectiveness, as seen in reduced hospital stays for patients treated with fish-skin grafts compared to synthetic alternatives.

Expanding Skin Substitutes Use In Chronic Wounds Opens A Parallel Growth Channel

Chronic wounds, such as diabetic foot ulcers and venous leg ulcers, are expanding the skin graft market, influencing procedure frequency and product mix. Over 75 skin substitute products cater to chronic wound indications, with 102 products priced above USD 1,000 entering the U.S. market between January 2024 and October 2025. Clinical trials show fish-skin grafts outperform standard care in wound closure for diabetic foot ulcers.[2]J. Dickerson et al., “Intact Fish Skin Graft to Treat Deep Diabetic Foot Ulcers,” NEJM Evidence, evidence.nejm.org. The 2026 reimbursement reset is shifting chronic wound cases to hospital outpatient centers, favoring products with consistent evidence and standardized protocols.

Shift Toward Evidence-Based, Reimbursable Products Reshapes Competitive Positioning

The skin graft market is increasingly driven by evidence-based and reimbursable products. The 2026 payment reset introduced a tiered reimbursement structure, with BLA products receiving ASP plus 6%, PMA-cleared devices earning the highest flat APC payment, and 361 HCT/P and 510(k) products placed in lower reimbursement bands. Companies are investing in trials and regulatory strategies to align with stricter evidence requirements. AVITA Medical’s interim results showed faster readiness for skin grafting, while Organogenesis is focusing on evidence differentiation to gain market share in 2026. The market is shifting towards evidence as a central factor for pricing and access.

Under-Penetration Of Novel Biological Graft Sources Offers Incremental Opportunity

Novel biological sources, such as fish-skin, placental, and umbilical cord-derived products, present growth opportunities in the skin graft market, particularly outside the U.S., where adoption is in early stages. Kerecis, acquired by Coloplast in 2024 for USD 1 billion, has extensive U.S. coverage but limited European adoption despite regulatory clearance. Clinical evidence supporting these products is growing, with diabetic foot ulcer data highlighting their efficacy. However, country-specific regulations and reimbursement timelines will influence the pace of cross-border commercialization.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High procedure and product costs relative to conventional wound care alternatives, limiting adoption in cost-constrained settings | -1.4% | Global, most acute in low and middle income regions and underfunded public systems | Short term (≤ 2 years) |

| Reimbursement uncertainty and coverage transitions across Medicare, Medicaid, and private payers following the 2026 payment overhaul | -1.2% | North America primarily, with spillover to Europe through compliance cost pressure | Short term (≤ 2 years) |

| Donor-site morbidity, infection risk, and graft failure rates constraining autograft scale-up in complex wound types | -0.8% | Global | Medium term (2-4 years) |

| Limited availability of high-quality cadaveric skin and cold-chain constraints restricting allograft supply in emerging markets | -0.5% | Asia-Pacific, Middle East and Africa, and South America, with secondary impact in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Procedure And Product Costs Limit Addressable Reach

Affordability remains a significant challenge in the skin graft market, particularly in healthcare systems unable to absorb the costs of advanced wound products and multistep procedures. Cell-based and tissue-engineered constructs, while clinically appealing, often have acquisition costs beyond what many public systems or cost-sensitive providers can afford. This issue is more pronounced outside the U.S., where reimbursement systems are stricter and much of the global burn burden is concentrated. Cost pressures increase further when dermal matrices require staged procedures or when allografts rely on cold-chain logistics, adding complexity to handling and storage. In the U.S., administrative measures like the WISeR prior authorization model, introduced in January 2026 across six pilot states, have added scrutiny to skin substitute use for diabetic foot ulcers and venous leg ulcers. As a result, the market may see faster product rationalization, with lower-priced products gaining share in cost-conscious hospital settings.

Reimbursement Uncertainty Creates Near-Term Demand Volatility

The 2026 reimbursement reset has disrupted the skin graft market by altering product usage, billing, and distribution. Mobile wound care providers began exiting parts of the U.S. market after January 1, 2026, as new payment ceilings made cellular and tissue-based products less viable for physician offices. Organogenesis reported that its first-half 2026 results would be impacted as the market adjusts to CMS changes, with normalization expected in 2027. In Europe, burn treatments are seeing stronger adoption compared to chronic wounds, as payers in countries like Germany and France demand more health-economic evidence before approving broad reimbursements. Until these policies stabilize, the market is likely to experience uneven demand despite consistent patient needs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Graft Type: Biosynthetic Innovation Challenges Autograft's Established Lead

In 2025, Autograft held a 46.76% revenue share, reaffirming its leadership in the graft type segment and its critical role in the skin graft market. Surgeons prefer autograft for acute burns and traumatic wounds due to its native tissue integration, durability, and immunity to rejection. It remains the gold standard when donor-site harvesting is feasible and definitive closure is required. Allograft and xenograft serve as temporary biological coverage, with cadaveric allograft stabilizing critically ill patients and porcine xenograft preparing wound beds for interim coverage needs.

Synthetic and biosynthetic grafts are projected to grow at a 7.95% CAGR from 2026 to 2031, making them the fastest-growing segment. These products reduce donor-site burden and expand coverage options, especially in cases where repeated harvesting is not viable. Innovations like biodegradable scaffolds, electrospun PLGA platforms, and hybrid matrices such as PermeaDerm are driving differentiation in the market. While dermal matrices have not replaced split-thickness skin grafting in routine burn care, they show promise in specific applications like contracture reconstruction and combined cellular use. The market is shifting toward a hybrid treatment model where biosynthetic products complement traditional surgical standards.

By Source: Human Skin Anchors The Market While Engineered Skin Redefines The Frontier

In 2025, human skin accounted for 67.88% of revenue, maintaining its central role in the skin graft market. This dominance reflects its use in autologous and allograft applications, supported by established burn care infrastructure and regulatory familiarity. Surgeons trust human-derived products due to their proven performance in handling, integration, and outcomes, particularly in severe burn cases. Animal-derived products, such as porcine and bovine scaffolds, retain a niche role as temporary coverage and wound bed preparation tools.

Cell-based and tissue-engineered skin is expected to grow at an 8.45% CAGR from 2026 to 2031, making it the fastest-growing source segment. These products offer enhanced biological activity without relying on donor supply. Studies have demonstrated the potential of iPSC-derived mesenchymal stem cells and multicellular bioprinted skin, paving the way for next-generation engineered skin. China’s expanding manufacturing capabilities and evolving regulatory pathways are also driving growth in this segment, with initial adoption likely in high-value use cases.

By Application: Burns Set The Volume Floor While Chronic Wounds Drive The Margin Story

In 2025, burns accounted for 65.44% of revenue, making them the largest application in the skin graft market. This share is driven by the necessity of grafting for full-thickness injury closure and the concentration of advanced burn care facilities in high-income countries. Traumatic wounds are the second-largest application, supported by road accidents and workplace injuries in industrializing economies. Surgical wounds and skin cancer reconstruction are smaller but growing segments, driven by increasing dermatologic and reconstructive procedures.

Chronic wounds are projected to grow at an 8.72% CAGR from 2026 to 2031, making them the fastest-growing application. This growth reflects the recurring treatment needs of diabetic foot ulcers and venous leg ulcers, where healing time and infection control are critical. Reimbursement changes in 2026 may create short-term challenges but emphasize the importance of robust documentation and trial support. Companies like MiMedx are aligning with these shifts by focusing on advanced products and compliance with evolving coverage rules.

By End User: Hospital Dominance Persists As ASCs Capture The Growth Premium

In 2025, hospitals held 47.03% of revenue, maintaining their leadership in the skin graft market. This dominance is linked to the complexity of acute burn care, specialized infrastructure for cryopreserved allografts, and the preference for controlled environments for high-risk procedures. Hospitals also house multidisciplinary teams that manage complex cases across surgery, infection control, and recovery. Despite the shift of some procedures to outpatient settings, hospitals remain central to the market, particularly for chronic wound management.

Ambulatory surgical centers (ASCs) are projected to grow at a 9.12% CAGR from 2026 to 2031, making them the fastest-growing end-user segment. This growth is driven by the migration of lower-acuity procedures to outpatient settings and payment updates that clarify billing for products and services. ASCs represent a strategic opportunity for manufacturers, with potential for evidence generation and real-world data collection. As outpatient infrastructure expands, hospitals are expected to handle complex cases, while ASCs capture a larger share of standardized procedures.

Geography Analysis

In 2025, North America held 39.52% of the global skin graft market revenue, maintaining its leadership due to high procedural volumes, extensive burn center networks, and a robust reimbursement system for advanced skin substitutes. The U.S. led regional demand, with Medicare Part B processing USD 9.9 billion in skin substitute claims in 2024 across codes Q4100 to Q4367. Canada and Mexico contributed to growth through chronic wound management and burn care. However, the 2026 reimbursement reset is expected to shift cases from physician offices to hospital outpatient settings, increasing prior authorization requirements in pilot states.

Europe ranked as the second-largest regional contributor to the skin graft market, driven by Germany, the U.K., and France. Burn care adoption outpaces chronic wounds due to stricter reimbursement standards in major health systems. Germany funds advanced grafts more readily for burns, while France requires stronger health-economic evidence for broader product listings. Italy and Spain add to demand, though access varies by procurement and payer processes. MDR-related evidence requirements are narrowing product registrations, favoring larger companies with stronger clinical documentation. Kerecis is working to expand its European presence but acknowledges slower adoption compared to the U.S.

Asia-Pacific is projected to grow at an 8.88% CAGR from 2026 to 2031, making it the fastest-growing regional market. Growth is driven by rising healthcare investments, increasing diabetes prevalence, and expanded local manufacturing in China, where artificial skin production rose from 9 million units in 2020 to 12.3 million by 2025. India remains significant due to its growing burn burden. Global suppliers are focusing on China, as seen in Mölnlycke’s joint venture with Zhende Medical in May 2026. AVITA Medical also strengthened its regional regulatory position in April 2026 with TGA certification in Australia and Medsafe WAND listing in New Zealand. The Middle East, Africa, and South America contribute less revenue but show potential through GCC infrastructure investments and broader healthcare coverage in Brazil.

Competitive Landscape

Globally, the skin graft market exhibits moderate fragmentation. Competition spans across tissue banks, instrument manufacturers, and biotech or med-tech platforms, rather than being confined to a single product category. Tissue banks like AlloSource, MTF Biologics, and LifeNet Health emphasize processing capabilities, quality assurance, and graft availability. In contrast, device manufacturers such as B. Braun SE, Zimmer Biomet, Humeca BV, Exsurco Medical, and De Soutter Medical prioritize procedural precision, dermatome performance, and meshing systems. Additionally, companies like Organogenesis, MiMedx, AVITA Medical, Integra LifeSciences, Kerecis (under Coloplast), and Smith+Nephew compete based on clinical evidence, regulatory classifications, and the breadth of their product portfolios. This diverse competitive landscape underscores the multifaceted nature of the skin graft market, which encompasses biological products, surgical tools, and engineered substitutes, each catering to different stages of wound management.

In 2025 and 2026, companies increasingly diversified their portfolios to reduce reliance on single reimbursement-sensitive product lines. Mölnlycke expanded its wound care portfolio by acquiring P.G.F. Industry Solutions in May 2025 and integrating Granudacyn wound cleansing solutions. Its collaboration with Transdiagen added a molecular evidence component to its strategy. Similarly, MiMedx launched CHORIOFIX and G4Derm Plus in 2026, enabling participation in both wound and surgical applications. This diversification is critical as shifts in site-of-care and reimbursement regulations can rapidly alter demand across product formats, leaving companies with narrower portfolios more vulnerable to disruptions.

The rising importance of evidence is another key trend. Stronger trial data now directly impacts payment quality and channel access in the skin graft market. AVITA Medical leverages Cohealyx-I interim data and multi-product platform messaging to drive adoption of integrated acute wound solutions. Kerecis highlights burn data showing shorter hospital stays compared to synthetic alternatives, strengthening the case for advanced biologics despite higher upfront costs. Integra LifeSciences’ PMA supplement approval for Omnigraft in February 2026 demonstrates how regulatory maintenance has become a competitive defense strategy. While scale remains significant, clinical proof and reimbursement positioning increasingly determine market share retention and growth.

Skin Graft Industry Leaders

B. Braun SE

Integra LifeSciences Holdings Corporation

Mölnlycke Health Care AB

Smith & Nephew plc

Zimmer Biomet Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Mölnlycke Health Care and Zhende Medical established a majority Mölnlycke-owned joint venture in China to combine their wound care portfolios and commercial capabilities. This partnership aims to accelerate access to one of the fastest-growing wound care markets by leveraging Zhende’s domestic distribution network and Mölnlycke’s advanced product portfolio.

- May 2026: MiMedx launched G4Derm Plus, a peptide matrix for surgical applications, with distribution secured through GPO agreements with Premier and Vizient. This launch expands MiMedx’s portfolio beyond amniotic products into structural tissue repair.

- April 2026: AVITA Medical, Inc. reported interim results from its Cohealyx-I multicenter study, showing a reduction of nearly 20 days in the average time to skin grafting for full-thickness wounds, with 13.6 days compared to a 33.2-day benchmark.

- April 2026: AVITA Medical received TGA certification in Australia and a Medsafe WAND listing in New Zealand for RECELL GO, enabling commercialization through its exclusive partner Revolution Surgical.

Global Skin Graft Market Report Scope

A skin graft is a surgical procedure where healthy skin is removed from one part of the body (the donor site) and transplanted to another area (the recipient site) where skin is missing or damaged due to burns, severe injuries, infections, or surgery (such as cancer removal).

The skin graft market is segmented by graft type, source, application, end-user, and geography. By graft type, the market includes autograft, allograft, xenograft, and synthetic and biosynthetic grafts. By source, the market is segmented into human skin, animal-derived skin, cell-based and tissue-engineered skin, and synthetic matrix-based skin. By application, the market is categorized into burns, chronic wounds, traumatic wounds, surgical wounds, and skin cancer reconstruction. By end-user, the market is segmented into hospitals, ambulatory surgical centers, specialty wound care centers, and dermatology and plastic surgery clinics. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Autograft |

| Allograft |

| Xenograft |

| Synthetic and Biosynthetic Graft |

| Human Skin |

| Animal-Derived Skin |

| Cell-Based and Tissue-Engineered Skin |

| Synthetic Matrix-Based Skin |

| Burns |

| Chronic Wounds |

| Traumatic Wounds |

| Surgical Wounds |

| Skin Cancer Reconstruction |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Wound Care Centers |

| Dermatology and Plastic Surgery Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Graft Type | Autograft | |

| Allograft | ||

| Xenograft | ||

| Synthetic and Biosynthetic Graft | ||

| By Source | Human Skin | |

| Animal-Derived Skin | ||

| Cell-Based and Tissue-Engineered Skin | ||

| Synthetic Matrix-Based Skin | ||

| By Application | Burns | |

| Chronic Wounds | ||

| Traumatic Wounds | ||

| Surgical Wounds | ||

| Skin Cancer Reconstruction | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Wound Care Centers | ||

| Dermatology and Plastic Surgery Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the skin graft market?

The skin graft market is valued at USD 2.41 billion in 2026 and is projected to reach USD 3.46 billion by 2031 at a 7.50% CAGR.

Which application generates the most revenue in skin grafts?

Burns remained the largest application, contributing 65.44% of revenue in 2025 because severe thermal injuries still require surgical wound closure and reconstruction.

Which segment is growing fastest in skin graft use?

Chronic wounds are the fastest-growing application at an 8.72% CAGR, while ambulatory surgical centers are the fastest-growing end-user channel at a 9.12% CAGR.

Why is North America leading global revenue?

North America held 39.52% of 2025 revenue due to high burn procedure volumes, strong reimbursement infrastructure, and broad use of advanced wound products in the United States.

What is driving growth in Asia-Pacific skin graft demand?

Asia-Pacific is projected to grow at an 8.88% CAGR, supported by rising healthcare spending, higher chronic disease burden, burn care demand in India, and manufacturing scale in China.

How are reimbursement changes affecting suppliers in 2026?

The 2026 reset is shifting volume toward hospital outpatient settings, increasing documentation pressure, and favoring products with stronger clinical evidence and higher regulatory status.

Page last updated on: