Non-Surgical Skin Tightening Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.40 Billion |

| Market Size (2031) | USD 3.60 Billion |

| Growth Rate (2026 - 2031) | 7.91% CAGR |

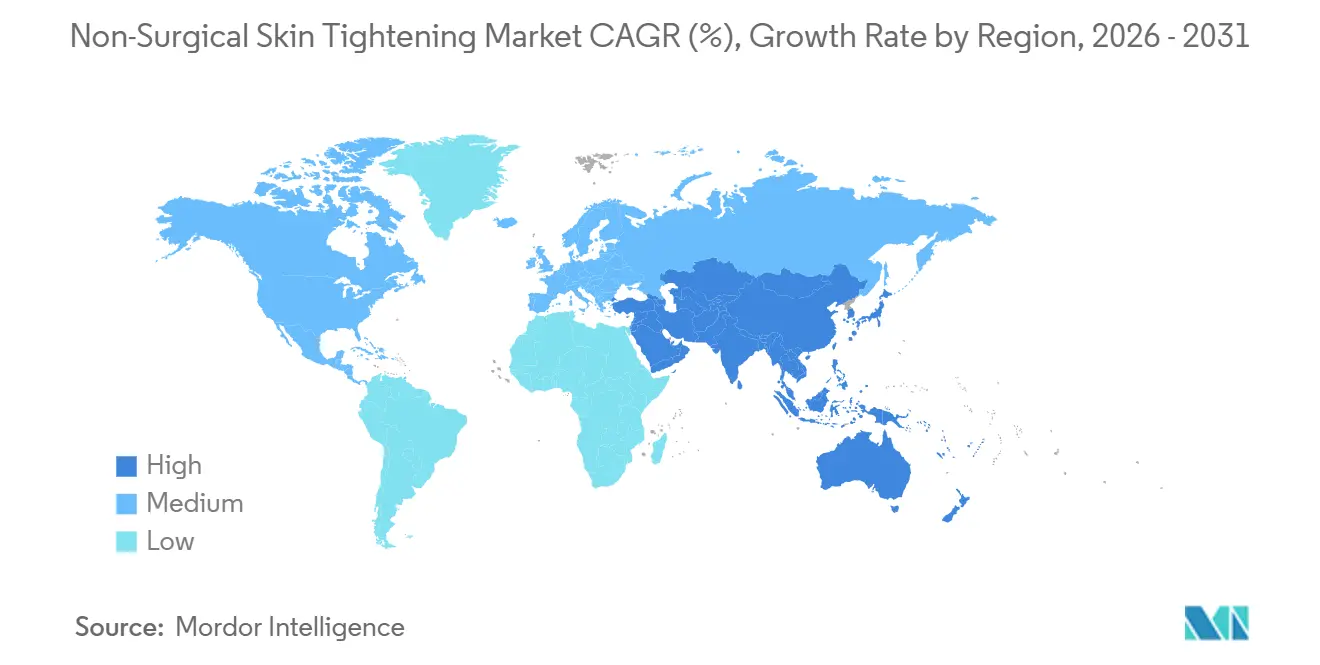

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non-Surgical Skin Tightening Market Analysis by Mordor Intelligence

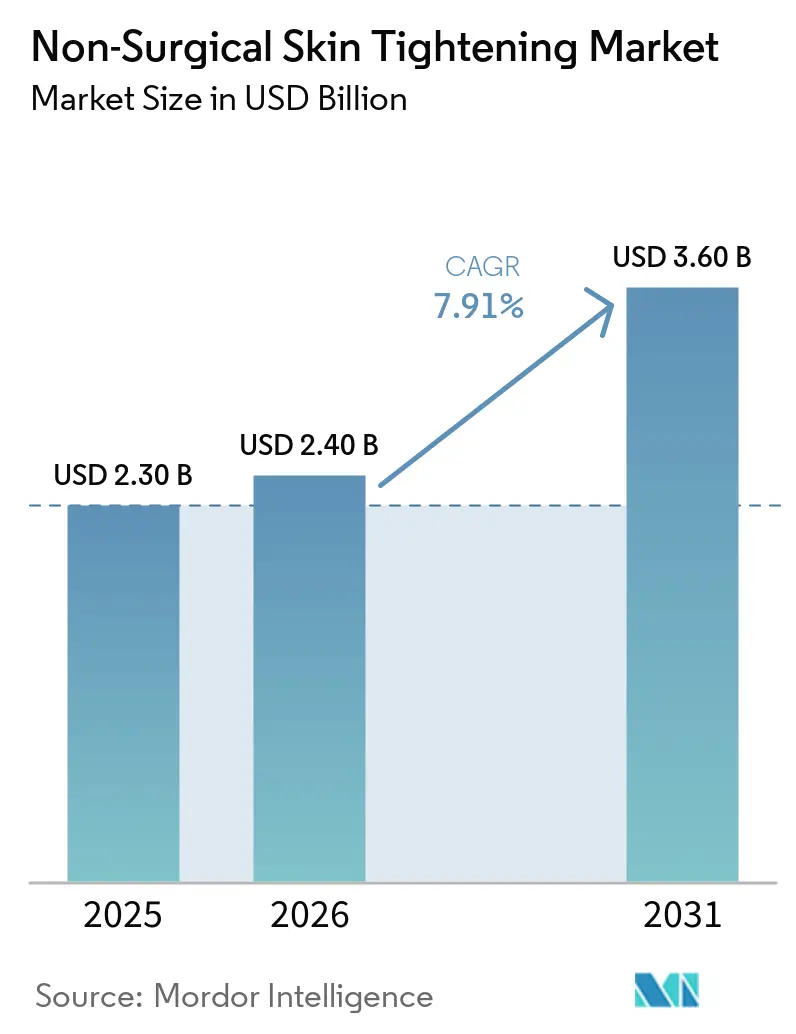

The Non-Surgical Skin Tightening Market size is projected to expand from USD 2.30 billion in 2025 and USD 2.40 billion in 2026 to USD 3.60 billion by 2031, registering a CAGR of 7.91% between 2026 to 2031.

A surge in demand from patients who experienced rapid weight loss on GLP-1 receptor agonists has widened the addressable base beyond the traditional anti-aging demographic, shifting clinical focus toward abdomen, flanks, arms, and other body areas. Radiofrequency (RF) technologies retained leadership in 2025, yet RF microneedling platforms are moving fastest because they combine epidermal resurfacing with dermal remodeling in a single pass. Large medspa chains now integrate clinic-to-home treatment plans that improve adherence, while vertical integration across distribution channels is lowering device payback periods and intensifying price competition. At the same time, manufacturers are embedding AI-driven safety features to ease concerns raised by the October 2025 FDA communication on RF microneedling adverse events.

Key Report Takeaways

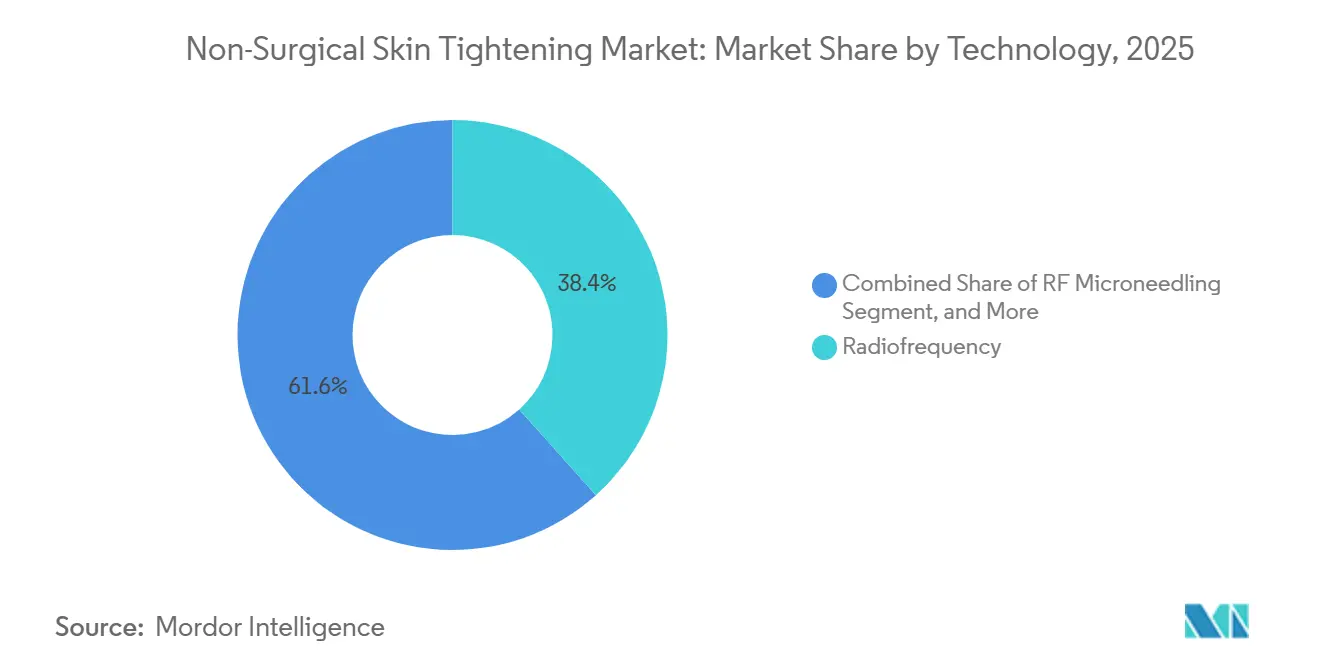

- By technology, conventional RF systems captured 38.38% of 2025 revenue, whereas RF microneedling is set to expand at an 8.42% CAGR to 2031.

- By end user, dermatology and aesthetic clinics held 47.63% 2025 share, but medspas and beauty centers are forecast to post the fastest 8.38% CAGR through 2031.

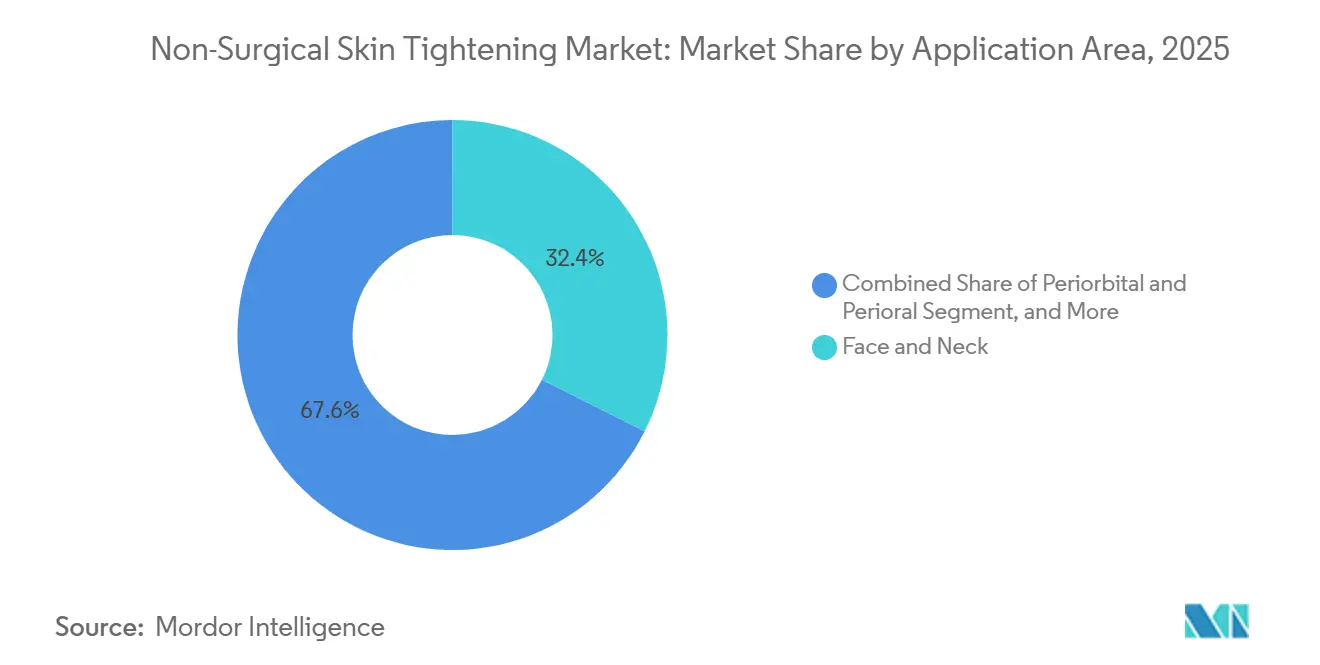

- By application, face and neck remained the largest category at 32.38% of 2025 sales, yet abdomen and flanks treatments are projected to climb at an 8.46% CAGR over the same horizon.

- By geography, North America dominated with 46.10% 2025 share, while Asia-Pacific is expected to accelerate at an 8.37% CAGR on the back of rising disposable incomes and regulatory harmonization.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Non-Surgical Skin Tightening Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to minimally invasive treatments | +1.4% | North America, Europe | Short term (≤ 2 years) |

| Advances in RF, MFU/HIFU and hybrid systems | +1.3% | North America, rapid uptake in urban Asia-Pacific | Medium term (2-4 years) |

| Expansion of medspas and dermatology clinics | +1.2% | North America, Asia-Pacific, GCC, Brazil | Medium term (2-4 years) |

| Aging demographics and earlier “prejuvenation” adoption | +1.1% | Global, led by North America and Europe | Long term (≥ 4 years) |

| GLP-1 weight-loss induced skin laxity | +1.6% | North America, Europe, spillover to APAC & MEA | Short term (≤ 2 years) |

| Hybrid clinic-to-home regimens | +0.9% | North America, Europe, early urban APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift to Minimally Invasive Treatments With Low Downtime

Patients increasingly insist on procedures that allow a return to social activity within 48 hours, a benchmark that RF and ultrasound platforms satisfy. Consultation data show that 72% of 2025 aesthetic visits in the United States explicitly requested non-surgical options, up from 58% in 2023. FDA clearances in 2024-2025 introduced RF microneedling devices equipped with real-time impedance monitoring, which standardize energy delivery and mitigate operator error [1]U.S. Food & Drug Administration, “RF Microneedling Systems: Safety Communication,” fda.gov. Medspas have capitalized by promoting “lunchtime” treatments that pair RF microneedling with topical serums to enhance collagen stimulation. Cost differentials reinforce the trend: a three-session RF package averages USD 2,500-4,000 versus USD 8,000-12,000 for a surgical facelift, widening the Non-Surgical Skin Tightening market’s reach among younger and price-sensitive consumers.

Advances in RF, MFU/HIFU, and Hybrid Platforms Improve Efficacy

Micro-focused ultrasound now targets depths up to 4.5 mm, reaching the SMAS layer previously accessible only through surgery and enabling brow-lift-level tightening without incisions. A 2025 study in Plastic & Reconstructive Surgery confirmed that tiered energy delivery protocols balance efficacy and tolerability, fueling broader adoption [2]Sachin Shridharani et al., “Skin Tightening Technologies in Body Contouring,” Plastic & Reconstructive Surgery, journals.lww.com. InMode’s Morpheus8 demonstrated quarterly revenue above USD 100 million in 2024, underscoring commercial traction for depth-specific RF microneedling. Hybrid workstations such as Alma Lasers’ Accent Prime blend RF and ultrasound, letting clinics customize protocols while avoiding multiple capital purchases. The January 2024 Cynosure-Lutronic merger pooled 535+ patents and unlocked global scale to speed next-gen hybrid launches.

Expansion of Medspas and Dermatology Clinics Increases Access

Global medspa revenue is rising sharply as roll-up groups back fragmented operators with centralized marketing and compliance resources. United Aesthetics Alliance’s February 2026 purchase of LivSkin MedSpa illustrates how consolidation delivers training and consumable savings at scale. China’s licensed aesthetic clinics rose 18% year-on-year in 2025, concentrated in Beijing, Shanghai, and Shenzhen. Solta Medical eliminated intermediaries by buying its long-time distributor, Wuhan Shibo Zhenmei, in December 2025 to capture demand for Thermage FLX directly in those cities. In the United States, the American Med Spa Association counted more than 7,000 licensed facilities in 2025, a 30% jump since 2022, signaling a durable appetite for minimally invasive skin tightening.

Aging Demographics and Earlier “Prejuvenation” Adoption

The world will host 1.4 billion people aged 60+ by 2030, yet the fastest-growing aesthetic segment is the 28-40 cohort pursuing preventive collagen stimulation. U.S. dermatology practices report that 35% of RF microneedling patients in 2025 were under 35, nearly doubling the 2022 proportion. Early collagen-boosting treatments can defer more invasive surgeries for a decade or longer, spreading lifetime spending while maintaining a natural appearance. Japan and South Korea exemplify the phenomenon, where cultural emphasis on flawless skin encourages annual RF or ultrasound maintenance sessions. This “wellness continuum” approach reframes the Non-Surgical Skin Tightening market as preventive healthcare rather than discretionary cosmetics, anchoring demand outside the traditional wrinkle-reduction narrative.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device capex, consumable cost & pricing | -0.8% | Latin America, MEA, SE Asia | Short term (≤ 2 years) |

| Safety concerns and regulatory scrutiny | -0.6% | North America, Europe | Short term (≤ 2 years) |

| Competition from injectables and thread lifts | -0.5% | North America, Asia-Pacific | Medium term (2-4 years) |

| Misinformation and DIY device misuse | -0.4% | Global, higher in low-literacy or poorly regulated e-commerce | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Device Capex/Consumable Cost and Procedure Pricing

Capital expenditure remains a structural barrier: professional RF microneedling units cost USD 30,000-80,000 and each disposable tip adds USD 50-150 per patient. In emerging markets, median incomes cannot sustain procedure packages priced at USD 2,400-3,600, pushing clinics toward leasing models or consumable-free platforms. Competitive pressure from PDO threads, which provide immediate lift at comparable total cost, erodes willingness to pay premiums for gradual collagen formation. Manufacturers now bundle marketing services and extended warranties to shorten payback periods, yet high up-front investment still restricts participation of solo practices and slows Non-Surgical Skin Tightening market penetration in cost-sensitive geographies

Safety Concerns and Regulatory Scrutiny, Especially Around RF Microneedling

The FDA’s October 2025 alert on RF microneedling, citing burns, hyperpigmentation, and infections, spurred insurers to reassess liability coverage and prompted clinics to demand more robust training. European CE authorities followed with stricter post-market surveillance obligations in 2024. To rebuild confidence, vendors embedded impedance-guided energy cutoffs and auto-depth calibration into 2026 product releases. Larger firms with dedicated regulatory teams absorbed the extra compliance load, widening the gap between them and smaller innovators. Persistent media coverage of even isolated injuries nonetheless dampens consumer trust and moderates the Non-Surgical Skin Tightening market’s near-term growth trajectory.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: RF Microneedling Narrows the Gap With Legacy RF

RF modalities controlled 38.38% of 2025 revenue, confirming their deep clinical roots, while RF microneedling is forecast to expand at 8.42% CAGR through 2031. The segment’s rise reflects precise dermal targeting and synergy with topical cosmeceuticals. Ultrasound systems such as Ultherapy continue to command premium pricing, but patient discomfort and higher per-session fees constrain uptake. Light-based tightening offers modest efficacy and therefore serves more as a maintenance adjunct. Hybrid workstations that merge RF, ultrasound and IPL enable clinics to tailor energy layers from epidermis to SMAS, enhancing outcomes without extra capital. Growing emphasis on AI-governed safety should further differentiate next-generation RF microneedling, underpinning its momentum in the Non-Surgical Skin Tightening market.

Historical product cycles show monopolar RF reigning up to 2020, followed by fractional RF microneedling that blended mechanical and thermal stimuli. Early devices lacked precision but paved the way for platforms like Lutronic’s Genius RF, which integrates real-time impedance feedback. The 2024 Cynosure-Lutronic merger accelerated patent consolidation, pointing to rapid platform upgrades. Ultrasound vendors are moderating energy delivery to balance pain and efficacy, while light-based firms position their systems for Fitzpatrick types IV-VI where thermal risks rise. Within this competitive landscape, hybrid modularity and automated safety features appear non-negotiable for future Non-Surgical Skin Tightening market share gains.

By End User: Medspas Log Faster Expansion Than Medical Clinics

Dermatology and aesthetic clinics retained 47.63% 2025 share, benefiting from board-certified oversight and cross-selling of reimbursed dermatologic services. Yet medspas and beauty centers are expected to surge at 8.38% CAGR through 2031, driven by extended hours, subscription pricing, and hospitality-style experiences that resonate with millennial and Gen Z patients. At-home consumers form a nascent but rapidly scaling cohort, propelled by FDA-cleared RF wands priced below USD 600. Plastic surgery centers deploy RF and ultrasound chiefly for touch-ups around higher-margin surgeries, limiting device room availability.

Roll-up groups such as United Aesthetics Alliance provide centralized training, bulk consumable purchasing, and marketing automation, lowering operating costs and raising utilization. Dermatology practices still dominate complex cases that require biopsy or prescription therapies, but rigid insurance workflows can crowd out discretionary procedures. At-home device misuse has sparked adverse events, yet regulatory attention is slowly steering the category toward safer designs. As each channel optimizes its unique advantages, device makers must tailor software support, financing, and consumable logistics to sustain Non-Surgical Skin Tightening market growth.

By Application Area: GLP-1 Tailwinds Propel Body Treatments

Face and neck procedures commanded 32.38% of 2025 revenue, thanks to high visibility and well-established patient willingness to pay. However, abdomen and flanks are projected to expand at an 8.46% CAGR through 2031, directly linked to GLP-1-related weight-loss laxity. Periorbital and perioral areas, though smaller in absolute value, secure premium prices because micro-accuracy delivers immediate cosmetic payoff. Arms and thighs remain underpenetrated due to longer treatment times, yet manufacturers' focus on larger handpieces could unlock fresh demand. Buttocks applications are still niche, given the thicker tissue and patient discomfort.

Evolution from facial exclusivity to whole-body protocols accelerated once FDA clearances broadened indications and clinics mastered larger treatment zones. BodyFX and other vacuum-assisted RF tools combine adipose disruption with skin tightening, providing bundled outcomes that resonate with post-GLP-1 patients. Early prejuvenation seekers also book periorbital RF sessions to delay blepharoplasty, deepening lifetime value. These dynamics collectively diversify revenue streams and reinforce the Non-Surgical Skin Tightening market’s resilience against single-segment downturns.

Geography Analysis

North America accounted for 46.10% of 2025 value, sustained by dense medspa networks, favorable disposable income and clear FDA pathways that streamline device adoption. The United States alone hosts 7,000+ licensed medspas and continues to expand into secondary cities where competition is lower and rent costs favor clinic economics. Canada and Mexico benefit from cross-border medical tourism, although Mexico’s laxer enforcement has allowed unlicensed providers to enter, occasionally denting consumer confidence.

Asia-Pacific is forecast to climb at an 8.37% CAGR through 2031, outpacing the global Non-Surgical Skin Tightening market. China’s tier-1 cities reported an 18% annual increase in licensed aesthetic facilities in 2025, and Solta Medical’s direct entry via its Wuhan Shibo Zhenmei acquisition is expected to accelerate Thermage FLX volumes [3]Bausch Health Companies, “Solta Medical Acquires Shibo Group,” bauschhealth.com. Japan and South Korea demonstrate mature prejuvenation cultures, with consumers favoring non-ablative energy devices over injectables for routine maintenance. India presents a volume opportunity but requires leasing models and consumables-free devices to penetrate beyond top-tier metros.

Europe delivers steady but uneven growth owing to national reimbursement differences and cultural attitudes toward cosmetic procedures. Germany, France and the United Kingdom lead adoption, while Southern and Eastern Europe lag due to economic disparities. CE Mark convergence simplifies approvals, yet stricter post-market reporting enacted in 2024 raises compliance cost. The Middle East, anchored by UAE and Saudi Arabia, positions itself as a luxury hub for medical tourism, although domestic demand outside urban pockets remains modest. South America shows strong cultural acceptance—Brazil ranks among the world’s top cosmetic markets—but currency volatility and lower household incomes skew choices toward injectables, tempering Non-Surgical Skin Tightening market expansion.

Competitive Landscape

The top five suppliers—InMode, Merz Aesthetics, Cynosure-Lutronic, Solta Medical, and Alma Lasers collectively captured a majority of 2025 revenue, indicating moderate concentration. Solta Medical’s December 2025 vertical integration in China removed distributor margins and improved control of Thermage FLX’s pricing and promotion. The Cynosure-Lutronic merger in January 2024 married over 535 patents with a 130-country sales footprint, creating scale for faster R&D iteration and bulk component sourcing. Crown Laboratories’ February 2025 addition of Revance’s DAXXIFY toxin blurs modality lines, fostering bundled protocols that combine injectables and devices under one brand.

Emerging disruptors include Sofwave Medical’s single-session ultrasound, Classys’ competitively priced Ultraformer III, and multiple Korean firms leveraging expedited K-FDA approvals to reach the market quickly. Technology roadmaps concentrate on AI-enabled safety: impedance-driven auto-shutoff, depth sensing and cloud-based analytics that help operators optimize parameters and document quality control. Strategic partnerships with national medspa chains and financing arms that shorten equipment payback are now table stakes for winning share in the Non-Surgical Skin Tightening market.

Non-Surgical Skin Tightening Industry Leaders

InMode Ltd

Merz Aesthetics

Cynosure-Lutronic

Solta Medical

Alma Lasers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: United Aesthetics Alliance acquired LivSkin MedSpa in Minneapolis-St. Paul, expanding its regional footprint and centralized service platform

- December 2025: Solta Medical bought Wuhan Shibo Zhenmei Technology to assume direct distribution of Thermage FLX in China.

- February 2025: Crown Laboratories completed the acquisition of Revance Therapeutics, bringing DAXXIFY toxin under the same roof as SkinPen devices.

Global Non-Surgical Skin Tightening Market Report Scope

As per the scope of the report, non-surgical skin tightening is a minimally invasive cosmetic procedure designed to restore firmness to lost or sagging skin without the need for incisions or a lengthy recovery. These treatments work by delivering targeted energy, typically in the form of ultrasound, radiofrequency (RF), or laser energy, to deeper layers of the skin, such as the dermis.

The non-surgical skin tightening market is segmented by technology, end user, application, and geography. By technology, the market is segmented into radiofrequency, RF microneedling, ultrasound, light-based tightening, and hybrid platforms. By end user, the market is segmented into dermatology & aesthetic clinics, med spas & beauty centers, plastic surgery centers, and at-home consumers. By application, the market is segmented into face & neck, periorbital & perioral, abdomen & flanks, arms & thighs, and buttocks. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Radiofrequency |

| RF Microneedling |

| Ultrasound |

| Light-based tightening |

| Hybrid platforms |

| Dermatology & Aesthetic Clinics |

| Medspas & Beauty Centers |

| Plastic Surgery Centers |

| At-home Consumers |

| Face & Neck |

| Periorbital & Perioral |

| Abdomen & Flanks |

| Arms & Thighs |

| Buttocks |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Radiofrequency | |

| RF Microneedling | ||

| Ultrasound | ||

| Light-based tightening | ||

| Hybrid platforms | ||

| By End User | Dermatology & Aesthetic Clinics | |

| Medspas & Beauty Centers | ||

| Plastic Surgery Centers | ||

| At-home Consumers | ||

| By Application Area | Face & Neck | |

| Periorbital & Perioral | ||

| Abdomen & Flanks | ||

| Arms & Thighs | ||

| Buttocks | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of the Non-Surgical Skin Tightening market by 2031?

It is projected to reach USD 3.6 billion by 2031, growing at a 7.91% CAGR from 2026.

Which technology is growing fastest in skin tightening?

RF microneedling leads with an 8.42% CAGR forecast through 2031 due to depth-specific energy delivery and minimal downtime

Why are abdomen and flank treatments gaining popularity?

Rapid GLP-1-related weight loss leaves moderate laxity in these zones, driving an 8.46% CAGR for body-focused protocols.

How will Asia-Pacific contribute to future growth?

Rising disposable income, urban clinic expansion and regulatory harmonization are set to push Asia-Pacific at an 8.37% CAGR to 2031.

Page last updated on: