Topical Scar Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

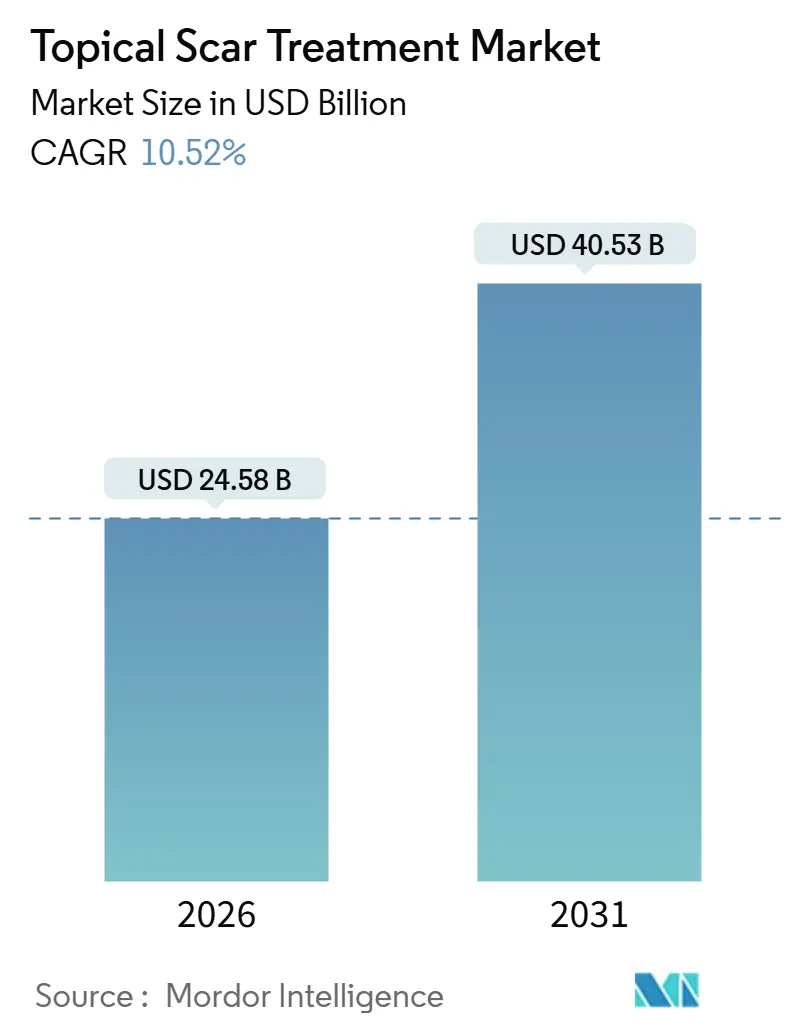

| Market Size (2026) | USD 24.58 Billion |

| Market Size (2031) | USD 40.53 Billion |

| Growth Rate (2026 - 2031) | 10.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Topical Scar Treatment Market Analysis by Mordor Intelligence

The Topical Scar Treatment Market size is estimated at USD 24.58 billion in 2026, and is expected to reach USD 40.53 billion by 2031, at a CAGR of 10.52% during the forecast period (2026-2031).

Growing surgical volumes, the ubiquity of acne scarring, and shifting consumer preference toward non-invasive solutions are widening the addressable patient pool. Wider adoption of silicone-based gels by hospitals, the rapid rise of direct-to-consumer e-commerce, and sustained product launches aimed at postpartum stretch marks are expanding the topical scar treatment market across both premium and mass-market price tiers. Competitive positioning now hinges on clinical evidence and digital channel reach, because payers seldom reimburse purely cosmetic interventions. The regulatory environment remains supportive, with Class I medical device designation for many silicone sheet products lowering barriers to entry while raising compliance expectations for labeling accuracy.

Key Report Takeaways

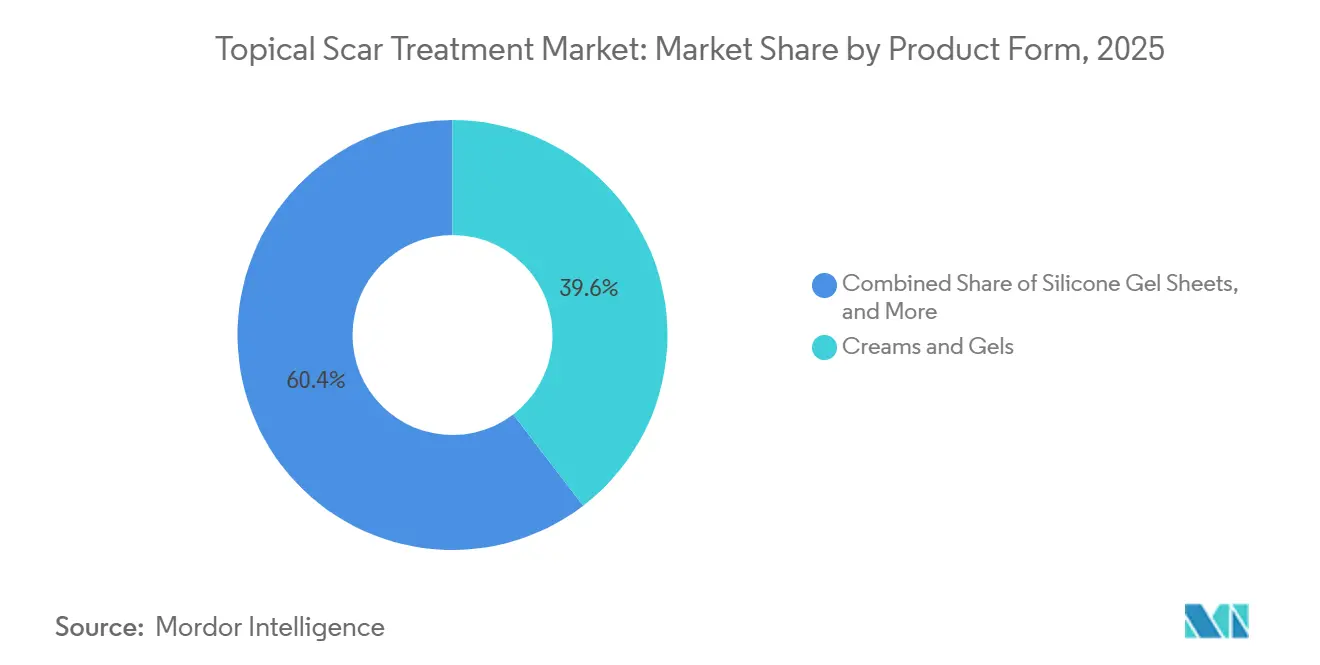

- By Product Form, Creams and gels held 39.55% revenue share in 2025, while sprays and sticks are on track for a 13.25% CAGR through 2031.

- By Scar Type, Atrophic and acne scars accounted for 36.53% of 2025 revenue, yet stretch-mark treatments are expanding at a 12.45% CAGR to 2031.

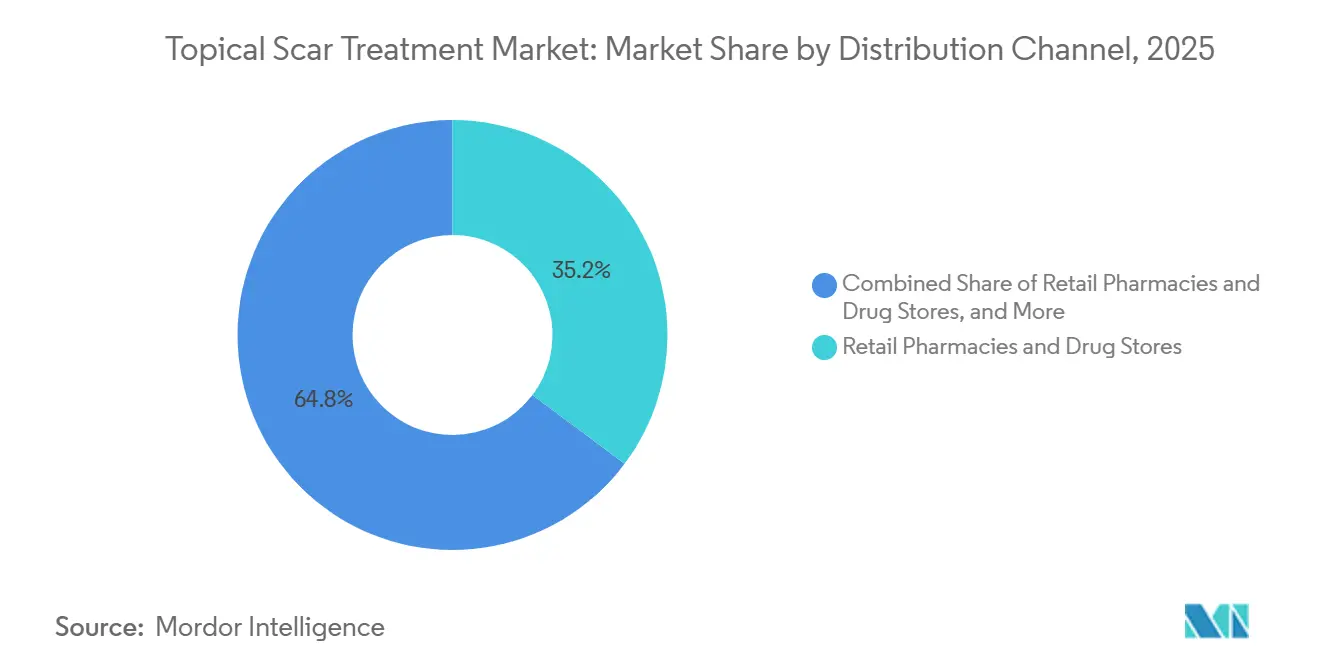

- By Distribution Channel, Retail pharmacies commanded 35.23% of the 2025 distribution, whereas online and direct-to-consumer channels show the fastest expansion at 17.55% CAGR through 2031.

- By End User, Dermatology and aesthetic clinics retained 36.13% of the end-user share in 2025, but home-care settings are growing at a 12.81% CAGR through 2031.

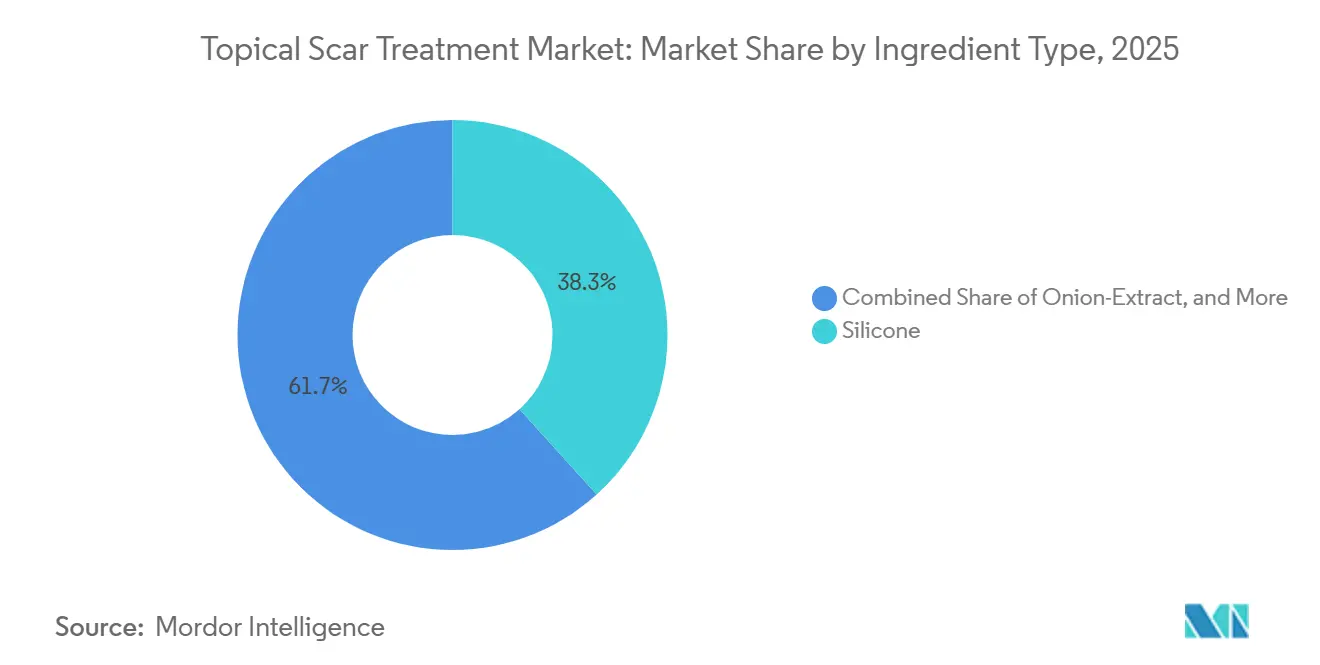

- By Ingredient Type, Silicone-based ingredients dominated with a 38.3% share in 2025, while hydrocolloids and polymer films are set to grow at a 13.42% CAGR to 2031.

- By Geography, North America captured 38.05% of 2025 revenue; Asia-Pacific leads future gains with a 12.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Topical Scar Treatment Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Surgical Procedures & Post-Operative Scar Burden | +2.1% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| High Global Prevalence of Acne-Related Atrophic Scars | +1.8% | Global, highest impact in Asia-Pacific and North America among 16-24 age cohort | Long term (≥ 4 years) |

| Consumer Shift to Non-Invasive, Low-Cost Topical Solutions | +1.5% | Global, led by North America and Europe, accelerating in urban Asia-Pacific | Short term (≤ 2 years) |

| Rapid Expansion of E-Commerce & OTC Distribution | +2.3% | Global, strongest in North America, China, and India | Short term (≤ 2 years) |

| Tele-Dermatology Platforms Integrating Prescription Scar Topicals | +1.2% | North America, Europe, with emerging adoption in urban Asia-Pacific | Medium term (2-4 years) |

| Pipeline Anti-Fibrotic Biologics Redefining Premium Topical Niches | +0.9% | North America and Europe, clinical-trial concentration in advanced markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Surgical Procedures and Post-Operative Scar Burden

A steady climb in reconstructive and aesthetic surgeries is amplifying demand for adjunctive scar therapies. The American Society of Plastic Surgeons documented 54,280 scar-revision procedures in 2024, a 4% rise over 2023, alongside 1.05 million total reconstructive cases[1]American Society of Plastic Surgeons, “2024 Plastic Surgery Statistics Report,” plasticsurgery.org. Hospitals now include silicone sheets or prescription gels in discharge kits, turning one-time procedures into months-long product use. Class I device designation speeds approvals so that innovators can release thinner, more breathable polymer films without lengthy trials. Growing preference for minimally visible incisions in orthopedic and bariatric surgeries further elevates clinical focus on post-operative scar outcomes. Together, these forces add depth and predictability to the topical scar treatment market.

High Global Prevalence of Acne-Related Atrophic Scars

Acne affects 20.5% of the global population and peaks at 28.3% among 16- to 24-year-olds[2]MDacne, “Global Acne Prevalence and Demographics 2025,” mdacne.com. Younger consumers first seek topical options, often cycling through multiple brands before considering lasers or microneedling. Tele-dermatology firms such as Curology and Apostrophe capture this digital-native segment by shipping customized blends of retinoids and azelaic acid under subscription models. Brand loyalty is reinforced through social proof and influencer content, sustaining repeat purchases that keep the topical scar treatment market expanding. The burden is especially visible in humid Asia-Pacific climates, which explains the region’s above-average 12.72% CAGR outlook.

Consumer Shift to Non-Invasive, Low-Cost Topical Solutions

Many shoppers now regard lasers and injectables as expensive or intimidating, favoring store-bought gels that promise gradual improvement. During pandemic-era clinic shutdowns, online searches for pigmentation and scar remedies climbed, with Amazon logging triple-digit increases in related keywords in early 2024. Silicone gels remain the mainstay because randomized trials show 60-80% improvement in hypertrophic scar pliability when used 12–24 weeks. The preference persists even after clinics reopened, signaling a lasting behavioral change. Affordable home-use routines, therefore, continue to expand the market for topical scar treatment.

Rapid Expansion of E-Commerce and OTC Distribution

Direct-to-consumer storefronts eliminate the pharmacy visit, enabling shoppers to receive prescription-grade actives after quick teleconsults. CVS posted USD 95.4 billion in Q3 2024 revenue, yet platform challengers are growing faster by bundling consultations, compounding, and monthly refills. Amazon Pharmacy and Alibaba Health offer same-day delivery in major cities, shrinking order-to-application time. The convenience attracts repeat buyers and widens access for rural patients, increasing overall product volumes. Regulators, however, issued multiple 2024–2025 warning letters against unapproved high-strength peels, underscoring quality risks on unregulated sites.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Variable Efficacy Across Scar Types Fuels Consumer Skepticism | -1.3% | Global, particularly acute in markets with high counterfeit prevalence | Short term (≤ 2 years) |

| Limited Reimbursement for Cosmetic Scar Therapies | -0.9% | North America and Europe, where insurance gatekeeping is strongest | Medium term (2-4 years) |

| Proliferation of Counterfeit Scar Products Online | -0.7% | Global, concentrated in unregulated e-commerce platforms in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Extended Treatment Duration Causes Low Compliance | -1.1% | Global, most pronounced in home-care settings without clinical supervision | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Variable Efficacy Across Scar Types Fuels Consumer Skepticism

Clinical outcomes differ markedly between hypertrophic, keloid, and atrophic scars. Meta-analyses show that silicone sheets reduce thickness and erythema in hypertrophic scars, yet the same products yield minimal change in pitted acne scars. Mismatch between expectation and reality triggers negative reviews that deter new buyers and force brands to issue refunds. Counterfeit listings muddy the waters further, prompting the FDA to publish enforcement notices against mislabeled retinoids in 2024 and 2025. Persistent uncertainty tempers repeat purchases, capping the market for topical scar treatments.

Limited Reimbursement for Cosmetic Scar Therapies

Private insurers and Medicare reimburse only scars that impair function, ignoring most acne, stretch marks, and post-cesarean cases[3]Centers for Medicare & Medicaid Services, “Medicare Coverage Determination for Scar Treatments,” cms.gov. Patients must pay USD 30–200 per month for prescription gels, pushing price-sensitive users toward less-proven OTC brands. In Europe, the NHS excludes cosmetic scar products unless burns or trauma are involved[4]National Health Service, “NHS Formulary Cosmetic and Scar Treatment Exclusions,” nhs.uk . Pharmaceutical firms hesitate to fund large trials when reimbursement remains uncertain, slowing innovation. Out-of-pocket payments thus restrict adoption, particularly among lower-income demographics who might otherwise expand the market for topical scar treatment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Form Sprays Gain Traction Despite Cream Dominance

Creams and gels controlled 39.55% of 2025 revenue, a position earned through decades of physician familiarity and documented silicone efficacy. Their hold on the topical scar treatment market is reinforced by hospital discharge protocols that specify branded silicone gels for post-operative care. Yet sprays and sticks, once niche, are forecast to grow at a 13.25% CAGR through 2031, riding demand for touch-free delivery that limits shear stress on healing skin. Pediatric caregivers and burn survivors appreciate sprays that coat broad areas without rubbing, and the format aligns with on-the-go lifestyles that favor one-hand application. Brands invest in ultra-fine mist valves to ensure even coverage, reducing product waste and boosting compliance. The change reflects a broader trend of convenience trumping habit, indicating that functional design can shift loyalty even in a mature segment of the topical scar treatment market. Sustained marketing on social platforms, where influencers demonstrate invisible finishes, accelerates adoption among teens and young adults.

In parallel, silicone gel sheets maintain a loyal following among hypertrophic scar patients, though their premium price slows uptake in lower-income regions. Ointments, foams, and patches remain specialty offerings aimed at post-radiation dermatitis or fragile geriatric skin. Collectively these smaller categories command under 15% revenue. Their growth potential lies in targeting specific clinical gaps, such as moisture-balanced foams for burns or bio-cellulose patches infused with growth factors. Portfolio breadth therefore remains a competitive lever for manufacturers seeking retention across multiple scar presentations, firmly anchoring the topical scar treatment market.

By Scar Type Stretch Marks Surge as Postpartum Care Normalizes

Atrophic and acne scars delivered 36.53% revenue in 2025, anchored by high teenage incidence and constant digital marketing. Subscription-based tele-dermatology drives recurring sales by customizing ingredient strength to lesion severity, embedding long-term product cycles into everyday routines. However, stretch-mark solutions now post the fastest 12.45% CAGR through 2031, propelled by candid postpartum conversations on Instagram and TikTok that destigmatize abdominal scarring. Treatments begin during late pregnancy to avert deep dermal tears and often continue months after delivery, ensuring steady throughput for brands that position themselves as maternal-care experts within the topical scar treatment market. Rising female workforce participation and disposable income further sustain willingness to pay for specialized creams and oils.

Hypertrophic and keloid scars demand longer, medically supervised regimens and frequently recur after excision. Manufacturers secure loyalty by pairing topical silicone sheets with clinic-administered steroid injections, offering a holistic approach that justifies premium pricing. Contracture scars remain a small but clinically urgent niche, often tied to burns that require multidisciplinary care plans and extended physiotherapy. Each subtype carries distinct pathophysiology, which shapes formulation strategies and branding narratives, creating segmentation complexity that ultimately enlarges the topical scar treatment industry.

By Distribution Channel Online Platforms Disrupt Pharmacy Gatekeepers

Retail pharmacies claimed 35.23% of 2025 distribution because consumers value in-person pharmacist advice and immediate stock availability. Yet online and direct-to-consumer portals record a 17.55% CAGR through 2031, outpacing all other channels as tele-consultation, auto-refill, and same-day shipping become standard. Algorithm-driven product matching replaces aisle searches, reducing decision fatigue and increasing basket sizes. Amazon Pharmacy’s integration with Prime delivery shifts expectations toward two-hour windows in major metros, prompting traditional chains to expand curbside pickup. Hospital pharmacies, though smaller, secure repeat orders through bundled discharge packs that include a two-month supply of silicone gel, thereby feeding a captive pipeline into the topical scar treatment market. Counterfeit risks remain a cloud over e-commerce, but FDA enforcement efforts and authenticity seals add gradually improving safeguards.

Brand positioning in the topical scar treatment market now hinges on omnichannel presence. Companies that synchronize retail shelf launches with influencer-backed online drops see higher conversion because consumers research digitally before purchasing anywhere. The emerging template involves education-based TikTok campaigns tied to QR codes on retail packs, redirecting buyers to subscription platforms that improve lifetime value.

By End User Home-Care Settings Capture Self-Treatment Wave

Dermatology and aesthetic clinics generated 36.13% revenue in 2025, leveraging bundled in-office laser and injectable packages that amplify topical sales as maintenance therapy. These clinics remain trusted sources for complex scars, especially keloids and contractures requiring multimodal care. Still, home-care environments expand at a 12.81% CAGR through 2031, courtesy of teleconsult access, mobile payments, and doorstep delivery, which eliminate appointment friction. Millennials view self-managed routines as cost-efficient, often documenting their progress online, which creates unpaid marketing loops for brands in the topical scar treatment market. Hospitals maintain a specialized role in early burn and surgical care, but economic pressures drive shorter inpatient stays, shifting product continuation to the patient’s home.

Manufacturers address this pivot by releasing simplified regimens with dispensing pumps that meter exact doses, reducing waste and improving adherence. Instructional videos, QR-coded onto packaging, guide users through the application, compensating for the absence of clinical supervision. This digital companion approach strengthens loyalty and data collection, giving firms deeper insight into usage patterns that inform future product design across the topical scar treatment industry.

By Ingredient Type Hydrocolloids Challenge Silicone’s Clinical Hegemony

Silicone formulations held a 38.3% share in 2025 and underpin standard-of-care protocols for the treatment of hypertrophic scars. Their occlusive properties hydrate the stratum corneum, soften raised tissue, and reduce erythema, outcomes validated by multiple randomized trials. The topical scar treatment market for silicone products continues to grow, while hydrocolloids and polymer films are accelerating at a 13.42% CAGR through 2031, driven by enhanced moisture-vapor transmission designs that enable week-long wear without maceration. Start-ups leverage breathable polyurethane backings coupled with alginate cores to absorb exudate, appealing to active patients who cannot reapply gels every four hours.

Onion-extract gels, present in over-the-counter aisles, retain niche popularity despite inconclusive evidence, driven by aggressive advertising that promises scar lightening within eight weeks. Vitamin E remains controversial; while some reports point to antioxidant benefits, allergy risk deters dermatologists from blanket endorsements. Corticosteroid-loaded patches target keloid-prone individuals by combining drug delivery with occlusion, creating high-margin sub-segments within the topical scar treatment market. Anti-TGF-β peptides, currently in Phase 3 trials, could redefine treatment paradigms if their long-term efficacy and safety translate from systemic sclerosis studies to topical scar prevention.

Geography Analysis

North America generated 38.05% of 2025 revenue, enabled by high household spending on appearance and a mature clinical ecosystem that integrates scar management into standard surgical aftercare. The United States anchors this region, with 54,280 scar revisions in 2024, and has established reimbursement coding that distinguishes cosmetic from functional indications. Canada and Mexico add smaller but stable streams, with Mexico benefiting from inbound medical tourism for affordable aesthetic procedures. Despite this sizeable base, regional growth moderates as payer restrictions and market saturation constrain upside potential, keeping future gains near the overall topical scar treatment market CAGR.

Asia-Pacific posts the fastest 12.72% CAGR through 2031, lifted by urban middle-class expansion, social-media-driven beauty standards, and easier online access to Western formulations. South Korea exports silicone-infused scar patches globally, leveraging K-beauty influence to command premium prices. Regulatory frameworks vary: Japan’s PMDA classifies advanced dressings as Class II medical devices, requiring domestic trials that slow launches.

Europe offers mid-single-digit growth anchored by Germany, the United Kingdom, and France. The European Medicines Agency enforces Medical Devices Regulation standards, demanding robust conformity assessments that favor established firms. South America and the Middle East see smaller shares but attractive upside. Brazil benefits from cultural acceptance of cosmetic corrections and offers lower procedure costs, generating steady demand for post-treatment scar gels. Gulf Cooperation Council nations support growth through medical-tourism investments and high disposable income among expatriate communities, widening the regional slice of the topical scar treatment market.

Competitive Landscape

The topical scar treatment market is fragmented, featuring a mix of multinational wound-care giants and digitally native start-ups. Smith & Nephew, Mölnlycke, and Stratpharma safeguard hospital formularies by publishing peer-reviewed data and aligning with surgical-care pathways. These incumbents extend their reach through country-specific acquisitions, such as Smith & Nephew’s Hull plant expansion, which boosts European capacity. Meanwhile, tele-dermatology platforms including Curology, Apostrophe, and Hers leverage direct prescribing and algorithmic skin assessments to bypass wholesale distribution costs, resonating with millennial and Gen Z audiences who prize convenience.

Innovation clusters around delivery technologies and anti-fibrotic pipelines. Stratpharma’s film-forming silicone gel secures FDA clearance for use on compromised dermis, offering a differentiated protective barrier. P144, an anti-TGF-β peptide, completes Phase 2 systemic sclerosis trials with promising dermal fibrosis reduction, and exploratory topical formulations aim to enter large keloid populations. Competitive advantage increasingly rests on omnichannel execution; brands that coordinate influencer campaigns with retail shelf launches enjoy greater share of voice and higher conversion rates in the topical scar treatment market.

Regulatory vigilance intensifies as counterfeit listings proliferate. The FDA issued multiple 2024-2025 warning letters targeting unapproved chemical peels and mislabeled retinoid concentrations sold through marketplaces, prompting firms to add serialization and QR-based authenticity checks. Market players therefore balance growth with compliance investments to protect brand equity. White-space remains in underserved niches such as pediatric burn scars and post-radiation dermatitis, inviting partnership between device makers and specialty clinics. Overall, mid-tier consolidation is expected as digital disruptors seek manufacturing scale and incumbents pursue youth-oriented brands to rejuvenate their topical scar treatment market portfolios.

Topical Scar Treatment Industry Leaders

Advancis Medical

Bayer AG ( (Bepanthen)

Mölnlycke Health Care

Smith & Nephew PLC

Stratpharma AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Investigators in China reported that a new topical blend of vitamin C, vitamin E, and ferulic acid improved post-laser healing and reduced complication rates among patients with atrophic acne scars.

- April 2025: DKSH Healthcare unveiled an upgraded Hiruscar Ultra Scar Care Gel formulated to shorten healing time and visibly enhance scar appearance within four weeks.

Global Topical Scar Treatment Market Report Scope

As per the report's scope, the topical scar treatment market refers to creams, gels, or ointments applied directly to the skin to reduce the visibility of scars. It works on the scar surface by softening, hydrating, and flattening the tissue, aiming to improve the cosmetic appearance and relieve symptoms such as redness, itching, or discomfort. Topical scar treatments are creams, gels, or ointments applied directly to the skin to improve the appearance of scars. They work by hydrating, softening, and flattening scar tissue while reducing redness, itching, or discomfort.

The topical scar treatment market segmentation includes product form, scar type, distribution channel, end user, ingredient type, and geography. By product form, the market is segmented into creams & gels, silicone gel sheets, sprays & sticks, and ointments & others. By scar type, the market is segmented into atrophic/acne scars, hypertrophic/keloid scars, contracture scars, stretch marks, and post-surgical/burn scars. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies & drug stores, and online & direct-to-consumer. By end user, the market is segmented into hospitals, dermatology & aesthetic clinics, and home-care settings. By ingredient type, the market is segmented into silicone, onion-extract, vitamin e & antioxidants, hydrocolloids & polymer films, and corticosteroids & biologics. By geography, the global market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Creams & Gels |

| Silicone Gel Sheets |

| Sprays & Sticks |

| Ointments & Others |

| Atrophic / Acne Scars |

| Hypertrophic & Keloid Scars |

| Contracture Scars |

| Stretch Marks |

| Post-Surgical & Burn Scars |

| Hospital Pharmacies |

| Retail Pharmacies & Drug Stores |

| Online & Direct-to-Consumer |

| Hospitals |

| Dermatology & Aesthetic Clinics |

| Home-Care Settings |

| Silicone |

| Onion-Extract |

| Vitamin E & Antioxidants |

| Hydrocolloids & Polymer Films |

| Corticosteroids & Biologics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Form | Creams & Gels | |

| Silicone Gel Sheets | ||

| Sprays & Sticks | ||

| Ointments & Others | ||

| By Scar Type | Atrophic / Acne Scars | |

| Hypertrophic & Keloid Scars | ||

| Contracture Scars | ||

| Stretch Marks | ||

| Post-Surgical & Burn Scars | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies & Drug Stores | ||

| Online & Direct-to-Consumer | ||

| By End User | Hospitals | |

| Dermatology & Aesthetic Clinics | ||

| Home-Care Settings | ||

| By Ingredient Type | Silicone | |

| Onion-Extract | ||

| Vitamin E & Antioxidants | ||

| Hydrocolloids & Polymer Films | ||

| Corticosteroids & Biologics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the topical scar treatment market?

As of 2026 the topical scar treatment market size stands at USD 24.58 billion and is set to expand to USD 40.53 billion by 2031.

Which region will grow the fastest through 2031?

Asia-Pacific shows the highest momentum with a projected 12.72% CAGR on the back of rising disposable incomes and social-media-driven beauty norms.

Which product format is gaining share most quickly?

Sprays and sticks post a 13.25% CAGR as consumers favor touch-free, convenient application.

Why do payers seldom cover scar treatments?

Insurers classify most scar therapies as cosmetic unless functional impairment is proven, so patients often pay out of pocket.

What ingredient dominates current sales?

Silicone-based gels and sheets lead with 38.3% revenue share due to extensive clinical validation in hypertrophic-scar management.

Page last updated on: