DDI (DNS, DHCP, And IPAM) Solutions Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

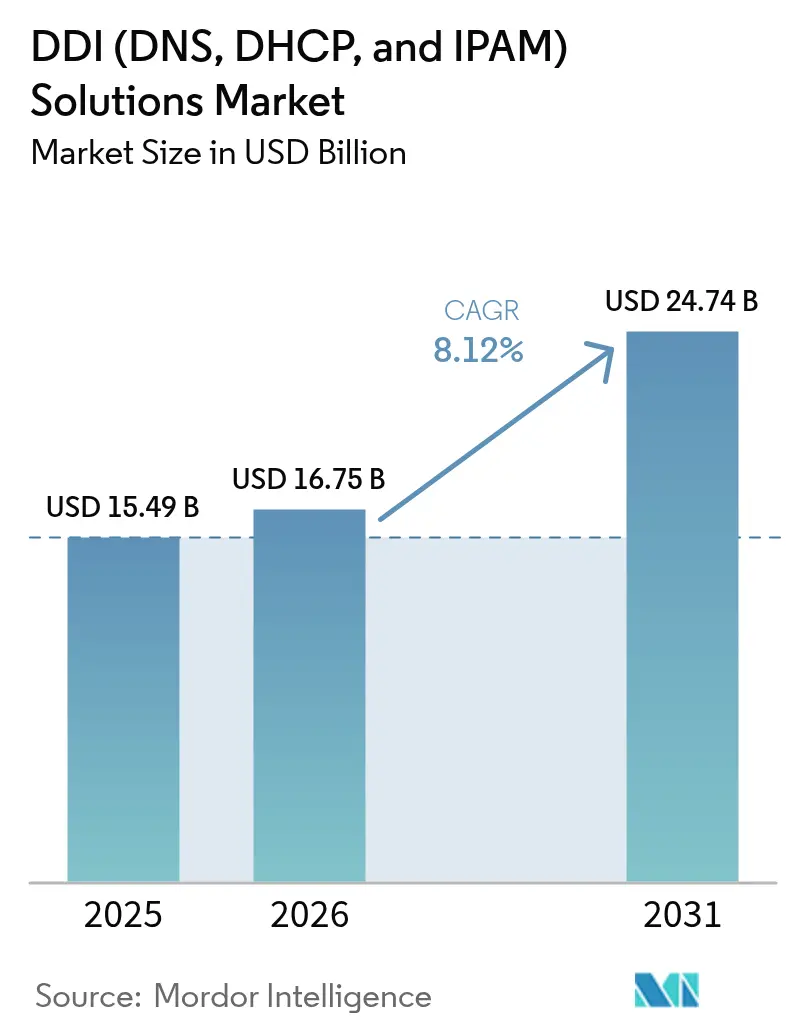

| Market Size (2026) | USD 16.75 Billion |

| Market Size (2031) | USD 24.74 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

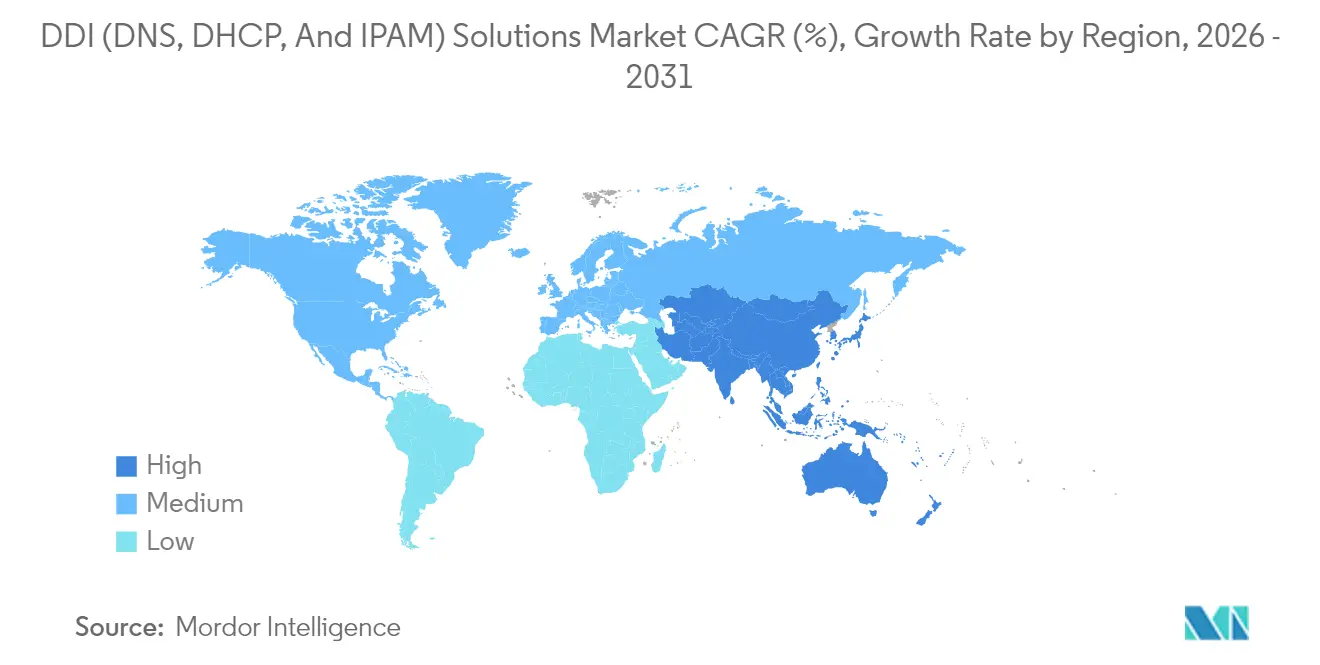

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

DDI (DNS, DHCP, And IPAM) Solutions Market Analysis by Mordor Intelligence

The DDI (DNS, DHCP, And IPAM) Solutions Market size is expected to grow from USD 15.49 billion in 2025 to USD 16.75 billion in 2026 and is forecast to reach USD 24.74 billion by 2031 at 8.12% CAGR over 2026-2031. IPv6 adoption mandates, government Zero Trust directives and the rapid expansion of connected devices sustain this upward path. Heightened security regulation, such as the European Union’s NIS2 directive, positions DDI platforms as compliance tools as well as infrastructure essentials. Organizations migrating workloads to hybrid multi-cloud environments favor software-centric offerings that simplify orchestration while reducing total cost of ownership. Strategic vendor partnerships with hyperscale cloud providers reinforce the shift toward unified DDI governance across public cloud, private data centers and edge sites.

Key Report Takeaways

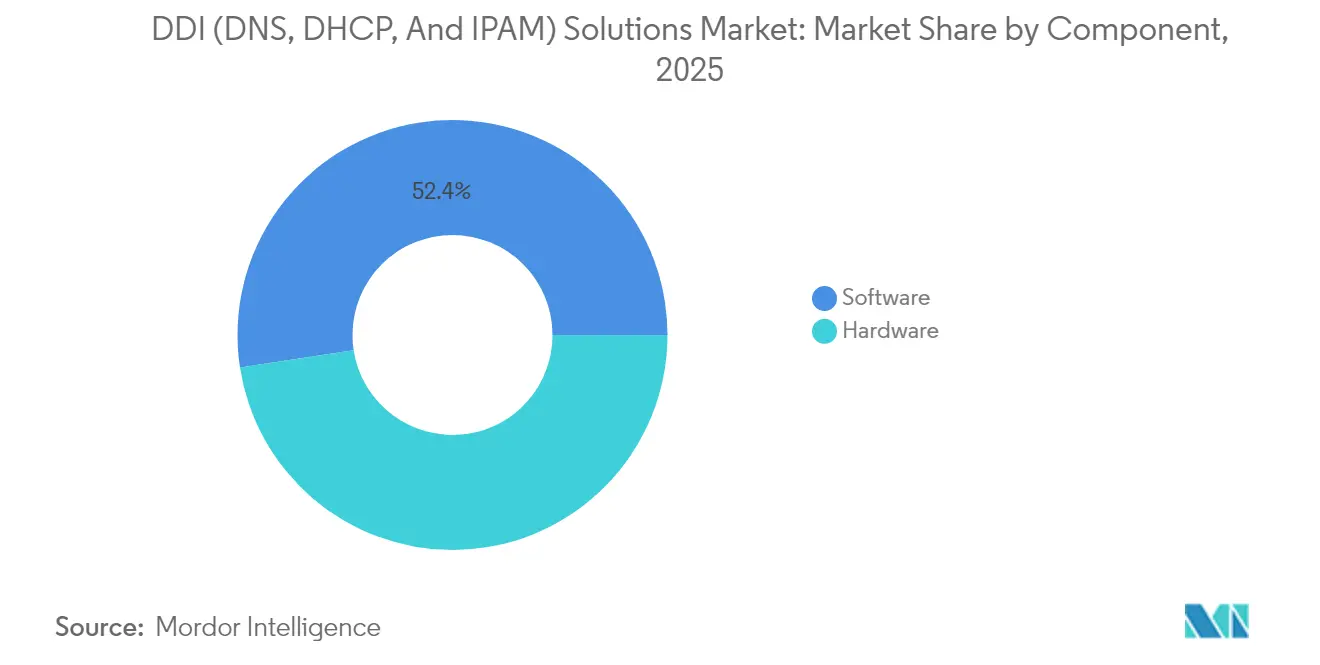

- By component, software held 52.42% of the DDI (DNS, DHCP, and IPAM) solutions market share in 2025 and is expanding at an 8.53% CAGR to 2031.

- By deployment model, cloud deployments commanded 65.05% share of the DDI (DNS, DHCP, and IPAM) solutions market size in 2025 and are advancing at a 10.25% CAGR through 2031.

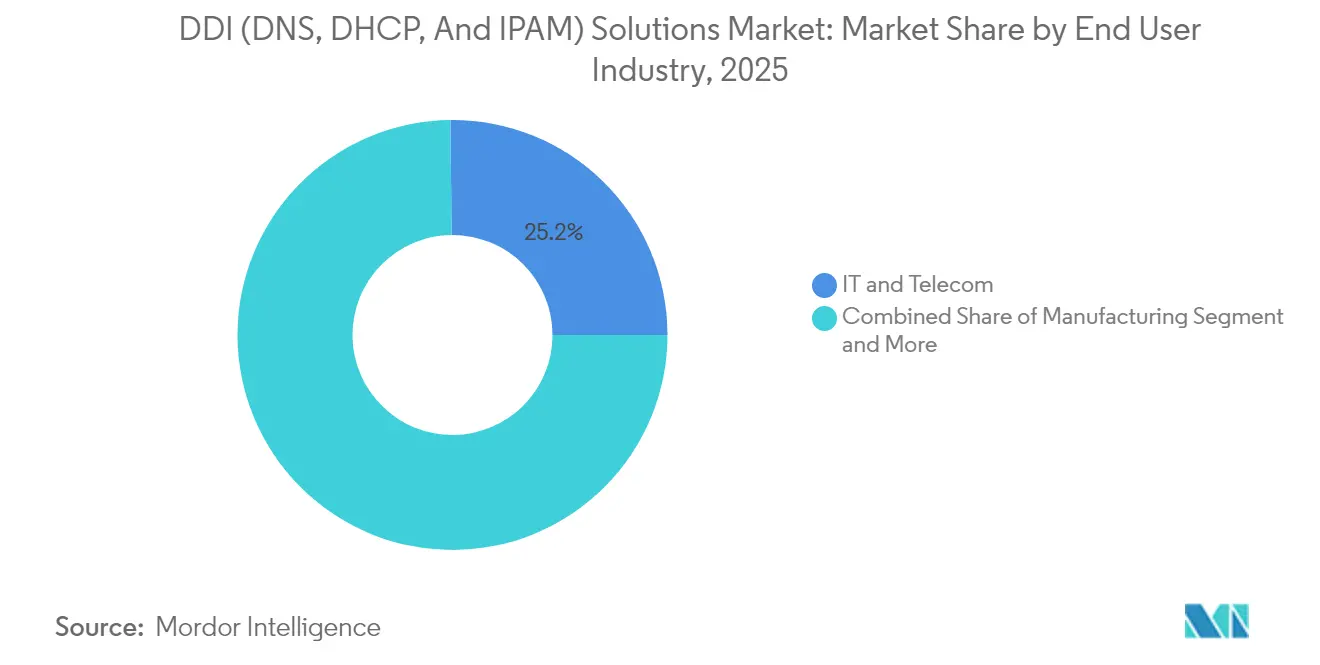

- By end-user industry, IT and Telecom led with 25.15% revenue share in 2025, while Healthcare and Life Sciences is growing fastest at a 8.78% CAGR to 2031.

- By application, network automation captured 37.65% of the DDI (DNS, DHCP, and IPAM) solutions market size in 2025; security and Zero Trust applications are rising at a 9.21% CAGR to 2031.

- By geography, North America accounted for 34.35% share of the DDI solutions market in 2025 and Asia-Pacific is posting the highest regional CAGR at 8.39% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global DDI (DNS, DHCP, And IPAM) Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in cloud and IoT-driven IP address volume | +2.10% | Global, with APAC leading adoption | Medium term (2-4 years) |

| Heightened data-security and privacy regulations | +1.80% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Accelerated IPv6 transition across enterprises | +1.50% | Global, with government mandates in US and EU | Medium term (2-4 years) |

| Network-automation demand in Zero-Touch Ops | +1.30% | North America and EU, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Government Zero-Trust cybersecurity mandates | +1.00% | US federal agencies, expanding to commercial | Short term (≤ 2 years) |

| 5G and edge roll-outs amplifying DDI complexity | +0.80% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Cloud and IoT-Driven IP Address Volume

The exponential rise in connected endpoints forces enterprises to manage sprawling address spaces that span on-premises data centers, multiple public clouds and emerging edge locations. Malaysia’s rise as a regional data-center hub, supported by investments from Google and Nvidia, illustrates the magnitude of network scaling now underway. The Asia-Pacific data-center market is projected to advance at 12.6% per year to 2032, underscoring the pressing need for automated IP address orchestration across heterogeneous infrastructure.[1]International Society for Performance Improvement, “Asia-Pacific Data-Center Forecast 2025-2032,” ispi.org DDI platforms that deliver real-time discovery, policy-driven provisioning and deep analytics therefore become foundational tools for digital expansion.

Heightened Data-Security and Privacy Regulations

Security mandates elevate DDI from a back-office utility to a frontline control. The NIS2 directive obliges DNS service providers to report incidents within 24 hours and imposes penalties up to EUR 10 million (USD 11.79 million) for non-compliance.[2]European Commission, “NIS2 Directive Overview,” europa.eu In the United States, Executive Order 14144 instructs federal agencies to encrypt DNS traffic as part of Zero Trust implementation. Enterprises therefore turn to DDI suites that integrate adaptive threat intelligence, DNS-over-HTTPS encryption and automated compliance reporting.

Accelerated IPv6 Transition Across Enterprises

Global exhaustion of IPv4 addresses and government deadlines are accelerating IPv6 migration plans. The US Office of Management and Budget requires agencies to complete substantial IPv6 enablement by 2025, prompting similar moves in adjacent sectors. China likewise prioritizes IPv6 to underpin digital-economy strategy despite broader macroeconomic pressures. Enterprises depend on DDI engines that support dual-stack operation, automated address translation and policy synchronization during phased transitions.

Network-Automation Demand in Zero-Touch Ops

Operational teams seek to replace repetitive network tasks with closed-loop automation. Cisco recently unveiled AI agents capable of executing routine configuration changes at machine speed, easing staffing shortages and lowering outage risk. DDI vendors embed similar machine-learning modules to predict address conflicts, suggest remediation and trigger policy updates. These capabilities align with DevOps pipelines, enabling consistent network provisioning through infrastructure-as-code paradigms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight IT budgets and perceived deployment risk | -1.20% | Global, particularly mid-market enterprises | Short term (≤ 2 years) |

| Scarcity of skilled DDI and DNS-security talent | -0.90% | North America and EU, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Multi-cloud integration and API-interoperability hurdles | -0.70% | Global, affecting cloud-first organizations | Medium term (2-4 years) |

| Vendor lock-in fears amid proprietary platforms | -0.50% | Enterprise segment globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tight IT Budgets and Perceived Deployment Risk

Tariff-driven hardware inflation is compressing capital budgets. Forecast price increases of 8-20% across networking gear threaten to halve anticipated IT spending growth in 2025.[3]Firstbase, “2025 Tariff Impact on IT Hardware,” firstbase.io Mid-size enterprises extend hardware refresh cycles and defer DDI upgrades to conserve cash. Concerns over service disruption during migrations further slow adoption. Vendors respond with subscription models, phased rollouts and outcome-based pricing to clarify return on investment.

Scarcity of Skilled DDI and DNS-Security Talent

An estimated over an million unfilled cybersecurity positions worldwide include acute shortages in DNS expertise. SolarWinds reports that practitioners worry about data-quality risks when automating network tasks, revealing gaps in advanced protocol knowledge. Limited human resources inflate project timelines and raise implementation costs, particularly for bespoke Zero Trust DNS deployments. Training programs and managed services aim to bridge the gap but cannot scale as quickly as demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Dominance Drives Innovation

Software accounted for 52.42% of the DDI (DNS, DHCP, and IPAM) solutions market in 2025 and is forecast to expand at an 8.53% CAGR through 2031. Vendors package IP address management, DNS security analytics and DHCP automation as microservices that run in any cloud, removing the need for specialized appliances. Infoblox’s Universal DDI Suite offers a single control plane spanning AWS, Microsoft Azure and Google Cloud. The software segment benefits from lower upfront cost, automatic version updates and API-based extensibility that aligns with DevOps workflows. Hardware solutions remain relevant for latency-sensitive edge sites but face margin pressure as virtualization advances.

Growing reliance on machine-learning algorithms reinforces software leadership. Predictive conflict detection, intent-based policy validation and self-healing DNS capabilities differentiate premium offerings. As organizations pursue cloud-native architectures, they prefer subscription licensing that converts capital expenditure to operating expenditure, further sustaining software revenue expansion. The software segment therefore underpins product-roadmap prioritization for incumbent and emerging vendors alike.

By Deployment Model: Cloud Transformation Accelerates

Cloud deployments comprised 65.05% of the DDI (DNS, DHCP, and IPAM) solutions market size in 2025 and are projected to grow at a 10.25% CAGR to 2031. Mature multi-cloud enterprises report 22% cost avoidance when centralizing DDI control across providers. Hyperscalers added data-center capacity in ten countries during 2025, giving customers local latency profiles while complying with data-sovereignty laws. These factors encourage direct consumption of cloud-hosted DDI services.

Hybrid models nonetheless remain common. Financial services firms and defense agencies retain on-premises DNS roots for policy control while delegating secondary zones to cloud hosts. Edge computing further diversifies deployment decisions, as 5G and IoT use cases require localized DHCP services. Vendors therefore invest in portable control planes that synchronize policies across SaaS, container and appliance footprints, ensuring consistent governance regardless of location.

By End-User Industry: Healthcare Emerges as Growth Leader

IT and Telecom maintained 25.15% revenue share in the DDI (DNS, DHCP, and IPAM) solutions market during 2025 thanks to early adoption of network automation. Healthcare and Life Sciences moves ahead as the fastest-growing vertical with a 8.78% CAGR projected to 2031. Connected medical devices, telehealth expansion and stringent privacy laws all elevate address-management complexity. Ransomware incidents affected 25.6 million patient records in 2024, intensifying demand for DNS-level protection. Dayton Children’s Hospital, for example, deployed Cisco zero-trust DNS safeguards to isolate malware without disrupting clinical workflows.

Manufacturing follows as Industry 4.0 programs converge operational technology and IT networks, driving need for deterministic DHCP services on the shop floor. Retail and BFSI segments prioritize omnichannel customer engagement and regulatory compliance respectively, both requiring resilient DNS architectures. Education, Government and Defense segments share a focus on secure remote access, while smaller industries value managed DDI services that offset internal skills shortages.

By Application: Security Applications Gain Momentum

Network automation held 37.65% share of the DDI (DNS, DHCP, and IPAM) solutions market size in 2025, underscoring how organizations seek to streamline provisioning tasks. Security and Zero Trust use cases, however, deliver the fastest growth at 9.21% CAGR through 2031. The White House directive that mandates encrypted DNS for federal systems signals a wider enterprise pivot to DNS-centric threat defense. Microsoft’s private preview for Zero Trust DNS introduces domain boundary enforcement, blocking malicious FQDNs before connection attempts occur. These initiatives convert DNS query logs into high-value telemetry for security operations teams and drive investment into integrated DDI-security suites.

Virtualization and cloud-orchestration workloads continue to benefit from IP address abstraction and self-service DNS. Data-center transformation projects rely on IPAM to migrate workloads with minimal downtime. Other emerging applications include analytics for chargeback reporting, DevSecOps integration and internet-scale authoritative DNS services.

Geography Analysis

North America led the DDI (DNS, DHCP, and IPAM) solutions market in 2025 with 34.35% revenue share. Federal Zero Trust mandates and large-enterprise cloud maturity sustain demand for feature-rich platforms. Tariff-related price inflation and macroeconomic caution could temper mid-market spending, but migration to IPv6 remains non-negotiable under federal deadlines. Hyperscalers continue to launch regional zones that expand cloud DNS footprints and encourage consumption of SaaS-delivered IPAM services.

Asia-Pacific generates the highest growth momentum at 8.39% CAGR to 2031. Rapid urban digitalization, 5G rollouts and substantial data-center construction in Malaysia, Indonesia and India create multiregional address-management challenges. China’s directive to accelerate IPv6 adoption despite economic headwinds keeps domestic demand elevated. Regional regulatory diversity, however, forces vendors to localize hosting and data residency features to satisfy divergent legal requirements.

Europe’s NIS2 framework formalizes cybersecurity obligations across critical sectors, making DNS risk management a board-level priority. Belgium, Hungary, Croatia and Latvia achieved early legislative transposition, while other member states remain in varying stages of approval. Energy costs and a cautious funding environment may limit near-term data-center expansion, but mandatory breach-reporting rules ensure sustained investment in secure DDI controls. South America, the Middle East and Africa offer long-run potential but currently face infrastructure and skills challenges that delay widespread deployment.

Regulatory Landscape

DDI adoption is shaped by cybersecurity mandates and standards that position DNS as a core Zero Trust enforcement point. In the European Union, Directive (EU) 2022/2555 (NIS2) classifies DNS service providers as essential entities and requires cybersecurity risk management and incident reporting, raising expectations for resilient DNS operations, logging, and response workflows within DDI platforms. Implementation has moved into prescriptive technical requirements, including European Commission Implementing Regulation (EU) 2024/2690 (October 2024), which sets technical security measures for DNS service providers under NIS2.

In the United States, updated guidance with NIST SP 800-81r3, Secure Domain Name System DNS Deployment Guide (March 2026), aligns secure DNS deployment with modern architectures and Zero Trust. Standards activity also reinforces protocol hardening, including IETF work on DNSSEC best current practice (draft-ietf-dnsop-rfc9364bis-00, February 2026) and China's GB/T 47323-2026 (March 2026), which covers IPv6 address allocation rules for non-service provider networks and tightens governance around enterprise addressing and transition planning.

Value Chain Analysis

The DDI value chain starts with core software and appliance vendors that provide DNS, DHCP, and IPAM engines, along with security and automation modules (Infoblox, BlueCat, EfficientIP, TCPWave, FusionLayer, and others). It then expands into deployment and integration partners that operationalize DDI across data centers, clouds, and edge environments. Enterprises typically procure DDI through direct vendor subscriptions (increasingly SaaS), channel partners, and systems integrators, then connect it to adjacent platforms such as IT service management, SIEM/SOAR, network automation, and cloud infrastructure tooling, with IPAM increasingly acting as a system of record for provisioning.

Downstream, cloud and interconnection providers influence how DDI is packaged and delivered in hybrid multicloud. Equinix, for example, documented patterns for running DDI as virtual network functions on Equinix Network Edge and connecting sites via Equinix Fabric (March 2026), which supports an edge-adjacent consumption model rather than only on-prem software. The chain is also being shaped by ecosystem integrations and data enrichment. Infoblox announced an Ecosystem Program to standardize third-party integrations (August 2024), and later announced the Kentik acquisition in July 2026, reflecting a move to bundle observability data with DDI context to reduce blind spots from fragmented Microsoft server instances, spreadsheet-based IP tracking, and siloed cloud-native configurations.

Competitive Landscape

The DDI (DNS, DHCP, and IPAM) solutions market features moderate fragmentation. Incumbents such as Infoblox, Cisco and Microsoft leverage established enterprise footprints and expand via software portfolios tuned for multi-cloud orchestration. Pure-play vendors like EfficientIP and BlueCat differentiate with specialized DNS security analytics, while upstarts such as TCPWave embed artificial intelligence for predictive remediation.

Cloud providers increasingly bundle native DNS and IP address services, introducing competitive price pressure on foundational functionality. Vendors counter by layering advanced security, automation and compliance features that extend beyond commodity zone hosting. Strategic acquisitions continue; Nokia’s USD 2.3 billion move for Infinera strengthens its optical backbone, enabling carrier-grade DDI service delivery. Cross-vendor ecosystem programs, for example Infoblox’s integration marketplace, help enterprises stitch DDI telemetry into SIEM, SOAR and IT-service-management tools for holistic visibility.

DDI (DNS, DHCP, And IPAM) Solutions Industry Leaders

Infoblox

EfficientIP

BlueCat Networks

Cisco Systems

Nokia (VitalQIP)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A prominent white-space area is operational maturity. Many organizations run DNS, DHCP, and IPAM across mixed toolchains, including legacy Microsoft server environments, point DNS services, and cloud-native configurations, without a unified source of truth or automation-ready APIs. EMA research found that only 35% of IT organizations report full success with their DDI strategy (March 2026), which points to sustained demand for implementations that standardize workflows, governance, and integration patterns rather than replacing individual components.

This gap favors vendors and service partners that package migration tooling, policy templates, and managed DDI operations, particularly where in-house DNS security expertise is constrained. Platform integrations that embed DDI into automation and cloud operations are also expanding addressable use cases beyond basic name resolution. VMware Cloud Foundation 9.1 added integration with Infoblox to automate provisioning of IP blocks and DNS entries through VCF Automation (May 2026), and Incognito released Address Commander 7.0 with Kubernetes Helm charts and expanded AWS cloud IPAM support (April 2026), which supports more repeatable deployments and infrastructure-as-code alignment. At the same time, vendors are adding higher-value layers to core services, including agentic operations and broader security capabilities, as reflected by Infoblox introducing an agentic operations layer (Infoblox IQ, June 2026) and the broader market move to combine DDI context with observability signals following Infoblox's acquisition of Kentik in July 2026.

Recent Industry Developments

- July 2026: Infoblox announced it would acquire Kentik, bringing network observability into its DNS and DDI platform. The combination links flow and performance telemetry with authoritative DNS and asset context, strengthening automated troubleshooting and security investigations across hybrid and multicloud networks.

- June 2026: Francisco Partners acquired EfficientIP from the founders and existing investors, providing new backing for product and go-to-market expansion in DDI and DNS security. The transaction signals continued investor interest in DDI as a core control plane for network automation and cyber risk management.

- February 2026: BlueCat introduced BlueCat Horizon, a SaaS-first Intelligent NetOps platform aimed at cross-domain network operations. The launch broadens BlueCat positioning from core DDI into cloud-delivered operational workflows that tie DNS and IP management data to wider NetOps use cases.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the DDI (DNS, DHCP, and IPAM) solutions market is defined as the revenues earned from software and hardware used to provide DNS services, allocate IP addresses through DHCP, and manage IP address inventory through IPAM, across enterprise and service provider networks.

Scope exclusions: Professional services that are not packaged and sold as part of the DDI solution (such as general IT managed services) are excluded where they cannot be reliably tied to DDI revenue.

Segmentation Overview

- By Component

- Hardware

- Software

- By Deployment Model

- On-premise

- Cloud

- By End-user Industry

- Manufacturing

- Retail

- Healthcare and Life Sciences

- Education

- BFSI

- IT and Telecom

- Government and Defense

- Other Industries

- By Application

- Network Automation

- Virtualization and Cloud Orchestration

- Data-center Transformation

- Network Security and Zero-Trust

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Southeast Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries, build the initial demand picture, and collect the key reference data series that can be checked year after year. We relied on public and official sources such as IANA and the regional internet registries for IP allocation trends, ICANN resources for DNS ecosystem context, NIST publications for security and network guidance, and standards bodies such as IETF for protocol-level evolution that affects adoption needs.

To anchor assumptions, we also reviewed company filings and investor presentations for revenue cues, product mix notes, and geography exposure, followed by credible press coverage on cloud networking, zero trust, and network automation rollouts. In addition, we used paid subscriptions for company financials and intelligence, plus patent databases to sense innovation activity and feature direction. This desk list is illustrative only, and many other public sources were also consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating how DDI is bought, delivered, and priced across on-premises and cloud deployments, and how budgets shift between software and hardware. We spoke with solution providers, channel partners, and enterprise IT and network teams across major regions to tighten assumptions on adoption timing, renewal cycles, and average contract values, then rechecked them against what respondents were seeing in deals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 12% | APAC: 43% |

| Mid tier: 48% | Functional/Unit leaders: 30% | EMEA: 31% |

| Smaller Players: 14% | Managers: 58% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where enterprise and service provider network footprints are translated into an address management and DNS control-plane demand pool, then shaped by deployment mix and typical renewal behavior. To keep totals realistic, we corroborated results with selective bottom-up approximations, using sampled pricing benchmarks and volume indicators (such as estimated node or site counts, plus channel checks on deal sizes) before adjusting the final value.

A few practical inputs were emphasized because they move the market the most. These included the pace of cloud and hybrid networking adoption, the growth in IP-enabled endpoints that expands IPAM needs, the shift from IPv4 pressure to IPv6 readiness work, security driven DNS policy enforcement demand, and the split between software-led deployments and latency-sensitive hardware footprints. For forecasting, scenario analysis was used around cloud migration speed and security spend appetite, and then the final path was aligned to what interviewees described as realistic budget cycles and rollout timelines. When bottom-up signals were incomplete for certain regions or smaller deployments, gaps were handled through ratio-based scaling using comparable adoption patterns and conservative pricing assumptions.

Data Validation & Update Cycle

Outputs were validated through multiple cross-checks so errors do not hide inside a single model layer. We compared results against independent signals such as IP address allocation trends, cloud network expansion commentary, and observed security policy adoption patterns, then reviewed any sharp year-to-year jumps to confirm they were supported by real drivers.

Before sign-off, the model and assumptions go through step-by-step analyst reviews, and respondents are re-contacted when a key variable moves beyond an expected range. Reports are refreshed annually, and interim updates are made when material events occur that can change adoption or pricing. Right before delivery, a final review pass is completed so clients receive the most current view available.

Mordor Intelligence's Ddi Dns Dhcp and Ipam Solutions Market Size Versus Other Published Estimates

Published market values for DDI often do not match because the scope lines are drawn differently and because the same buying motion can be labeled as software, services, or broader network management. Even when the topic label looks identical, the year used, currency conversion timing, and the way cloud subscriptions are annualized can shift the final number in different directions.

Verification evidence also matters because this market can be overstated if adjacent network security and generic managed services are counted inside DDI. Signals such as IP address allocation trends from internet registries, and recurring revenue patterns observed in vendor disclosures, are used to keep Mordor Intelligence tied to DDI-specific software and hardware revenues instead of a wider networking spend bucket.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 16.75 B (2026) | |

| Global Consultancy A | USD 0.57 B (2023) | Uses a narrower market boundary that groups DDI as a specific DNS-DHCP-IPAM tool spend, and it often treats services as a separate add-on, which reduces the headline value versus broader solution-plus-hardware accounting. |

| Industry Research Publisher B | USD 2.80 B (2024) | Appears to focus on solution revenues with limited detail on how hardware is treated, and the longer forecast horizon can embed more aggressive adoption assumptions without the same year-by-year validation checks. |

The spread in values is mainly explained by what gets counted as DDI revenue and how subscription spend is annualized across years. When the scope is kept consistent and the model is checked against observable demand signals, the resulting number becomes easier to trace back to clear inputs and repeatable steps, which helps decision-makers compare periods and regions without mixing adjacent categories.

Key Questions Answered in the Report

What is the current size of the DDI (DNS, DHCP, and IPAM) solutions market?

The DDI (DNS, DHCP, and IPAM) solutions market is valued at USD 16.75 billion in 2026 with an expected rise to USD 24.74 billion by 2031.

Which deployment model is expanding fastest?

Cloud deployment leads growth with a projected 10.25% CAGR, holding 65.05% share of the DDI solutions market size in 2025.

Why is Healthcare the fastest-growing end-user segment?

Connected medical devices, telehealth adoption and strict privacy regulations push Healthcare and Life Sciences toward advanced DNS security and IP address automation, resulting in a 8.78% CAGR forecast.

How do government mandates influence the DDI solutions market?

Policies such as the United States Executive Order 14144 and the European NIS2 directive compel organizations to implement encrypted DNS and incident reporting, directly boosting demand for secure DDI platforms.

Page last updated on: