Single-Use Assemblies Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

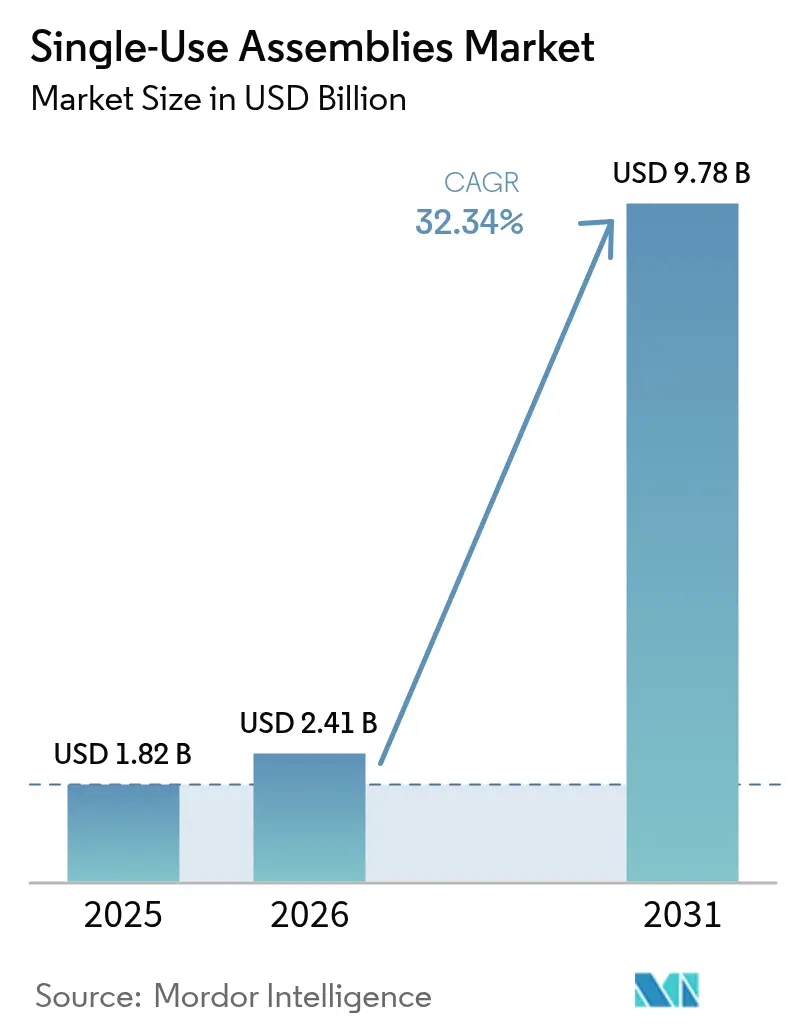

| Market Size (2026) | USD 2.41 Billion |

| Market Size (2031) | USD 9.78 Billion |

| Growth Rate (2026 - 2031) | 32.34% CAGR |

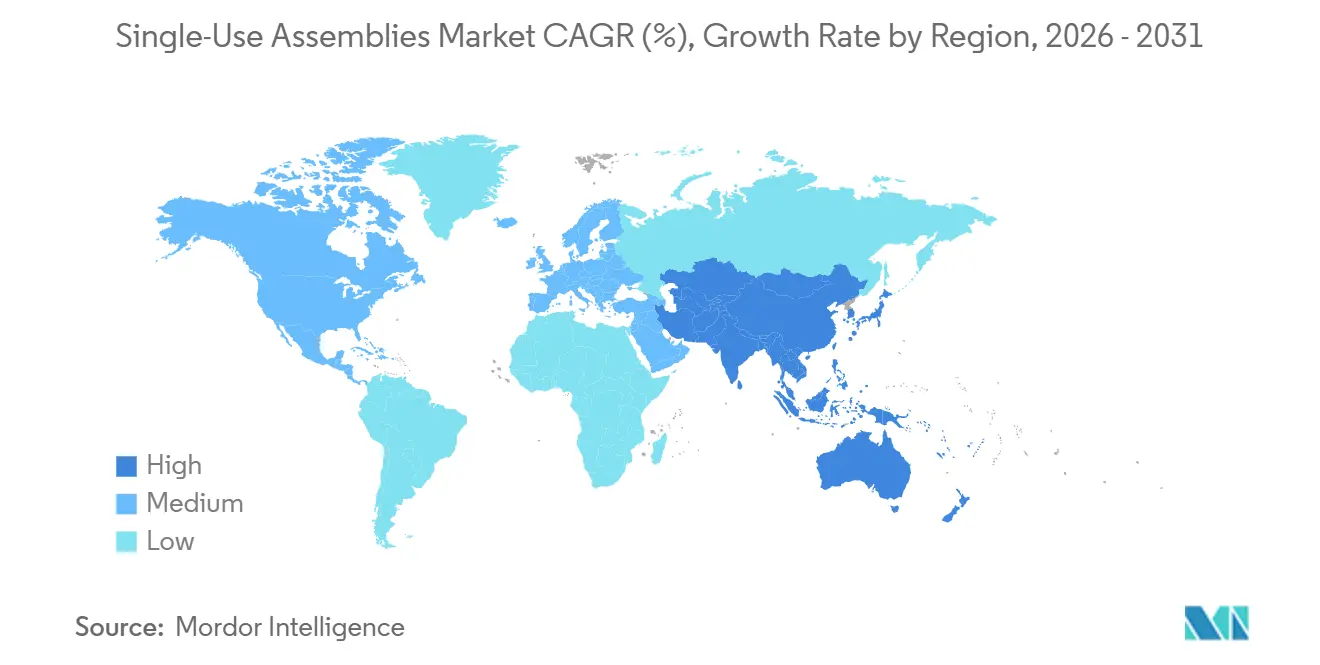

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Single-Use Assemblies Market Analysis by Mordor Intelligence

The single-use assemblies market size in 2026 is estimated at USD 2.41 billion, growing from 2025 value of USD 1.82 billion with 2031 projections showing USD 9.78 billion, growing at 32.34% CAGR over 2026-2031. Growing global demand for mRNA vaccines, cell and gene therapies, and biologics is accelerating adoption of closed-system fluid pathways, while regulatory incentives in the United States and Europe validate advanced manufacturing technologies. Heightened investment in platform scalability, coupled with supply-chain regionalization policies, is reinforcing the single-use assemblies market’s momentum across both mature and emerging biomanufacturing hubs. Strategic M&A activity among incumbent suppliers and contract manufacturers is streamlining component availability, yet capacity constraints in gamma irradiation and medical-grade polymers remain operational pinch points.

Key Report Takeaways

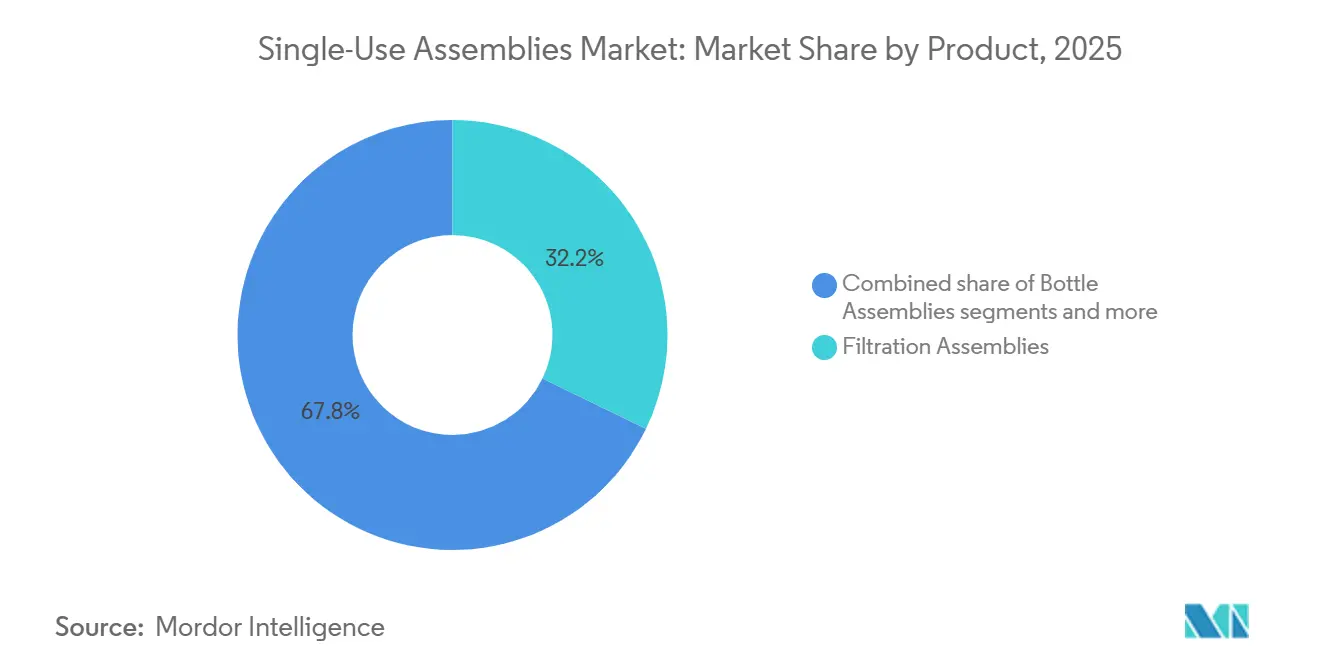

- By product, filtration assemblies led with 32.18% of single-use assemblies market share in 2025, while bag assemblies are projected to expand at a 33.85% CAGR through 2031.

- By application, filtration accounted for a 25.12% share of the single-use assemblies market size in 2025; cell culture and mixing are advancing at a 34.10% CAGR through 2031.

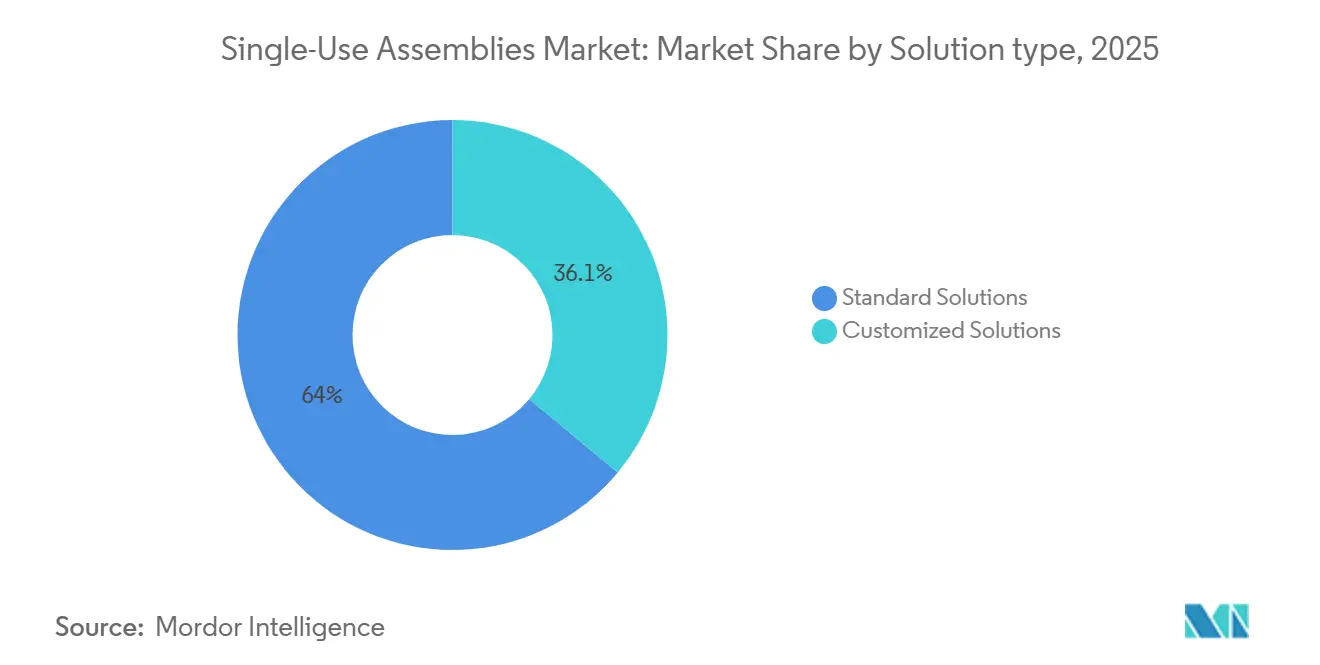

- By solution, standard solutions commanded 63.95% revenue in 2025, whereas customized solutions will register a 33.02% CAGR to 2031.

- By end user, biopharmaceutical and pharmaceutical companies held 55.05% of single-use assemblies market share in 2025, and CMOs/CROs show the highest projected CAGR at 34.42% over the same horizon.

- By geography, North America contributed 41.55% of 2025 revenue, while Asia-Pacific is forecast to post a 33.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Single-Use Assemblies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timelin |

|---|---|---|---|

| mRNA-Vaccine Platform Scale-Up Boosts Demand for Modular Fluid-Path Kits | +8.5% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Cell & Gene-Therapy Facilities Adopting Closed Single-Use Paths | +7.2% | North America & Europe, expanding to APAC | Long term (≥ 4 years) |

| Biologics and Biosimilars Capacity Expansion Worldwide | +6.8% | Global | Long term (≥ 4 years) |

| Cost-Savings vs. Stainless Steel & Faster Batch Changeovers | +5.1% | Global | Short term (≤ 2 years) |

| Regionalized Supply Chains Mandated by Regulators | +3.9% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| CDMO Needs Multi-Product Flexibility | +4.2% | Global, with early gains in North America & APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

mRNA-Vaccine Platform Scale-Up Boosts Demand for Modular Fluid-Path Kits

The surge in mRNA vaccine output is driving demand for pre-validated, factory-repeatable single-use assemblies that can be replicated across multiple fill-finish suites without lengthy re-qualification. Thermo Fisher’s USD 2 billion U.S. expansion earmarked for lipid-nanoparticle formulation exemplifies this shift. The FDA’s Advanced Manufacturing Technologies program incentivizes firms to standardize on these modular kits, enabling validation cycles to drop from months to weeks. Manufacturers gain throughput advantages because single-use pathways remove the clean-in-place downtime found in stainless steel, aligning with national pandemic-preparedness policies that require rapid scale-up capacity.

Cell & Gene-Therapy Facilities Adopting Closed Single-Use Paths

Autologous therapies rely on highly segregated processing environments, making closed-loop single-use tubing and connector assemblies essential for sterility and cell viability. FDA guidance issued in May 2024 emphasizes closed systems to mitigate adventitious agent risk in CGT workflows. High-density microfluidic bioreactors demonstrated superior CAR-T expansion compared with legacy systems, with single-use formats enabling the gentle shear profiles required for cell functionality. As batch sizes mirror single-patient demand, the economic benefit of eliminating stainless-steel cleaning protocols is amplified, reinforcing adoption across new CGT facilities.

Biologics and Biosimilars Capacity Expansion Worldwide

Continued biologics pipeline growth and biosimilar launches are spurring multi-train facilities to integrate 2,000-liter disposable bioreactors that offer commercial-scale oxygen transfer while reducing cross-batch contamination risk. FDA postapproval change guidance from July 2024 encourages flexible processes, and single-use assemblies enable rapid configuration changes without hardware retrofits. APAC manufacturers leverage these assemblies to build greenfield plants quickly, bypassing the utilities investment tied to stainless steel platforms.

Cost-Savings vs. Stainless Steel & Faster Batch Changeovers

Operational modeling shows that eliminating clean-steam generation and WFI loops reduces utility spend and shortens product changeovers from days to hours. FDA draft guidance on 21 CFR 211.110 underscores the need for tighter in-process controls, which single-use pathways deliver through pre-sterilized, vendor-qualified components. The sustainability of lower water and energy consumption further supports corporate ESG targets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Leachables & Extractables Compliance Hurdles | -4.8% | Global, with stricter enforcement in North America & Europe | Long term (≥ 4 years) |

| Disposal & Sustainability Concerns Around Plastic Waste | -3.2% | Europe & North America, expanding globally | Medium term (2-4 years) |

| Medical-Grade Polymer Price Volatility | -2.9% | Global, with acute impact in Asia-Pacific supply chains | Short term (≤ 2 years) |

| Global Gamma-Irradiation Capacity Bottlenecks | -2.1% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Leachables & Extractables Compliance Hurdles

The impending USP E&L chapter update scheduled for December 2025 imposes deeper toxicological scrutiny on polymer-based processing components, extending analytical timelines and escalating validation costs. Complex biologics formulations can catalyze unexpected chemical interactions with flexible film additives, forcing manufacturers to iterate material choices. Smaller firms with limited in-house mass-spectrometry capacity must outsource studies, lengthening development cycles and potentially slowing single-use assemblies market adoption.

Disposal & Sustainability Concerns Around Plastic Waste

ISO 59014:2024 elevates traceability expectations for secondary material recovery, adding documentation burdens for manufacturers that must prove responsible end-of-life handling of contaminated plastics. European Commission biotechnology policy stresses a transition to bio-based and circular materials, pressuring suppliers to invest in recyclable films or take-back programs. Until these technologies scale, disposal fees and public perception risks temper aggressive rollout plans in sustainability-focused regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Filtration assemblies anchor compliance needs

Filtration assemblies generated the largest revenue in 2025, accounting for 32.18% of single-use assemblies market share. Their dominance is rooted in multi-step sterile-filtration mandates that span bulk media preparation to final drug substance polish. The single-use assemblies market size for bag assemblies is forecast to expand at the highest 33.85% CAGR to 2031 as biomanufacturers adopt flexible storage and preparation envelopes that integrate seamlessly with continuous processing lines. Across the forecast, mixing assemblies benefit from intensified upstream titer strategies that demand homogeneous nutrient distribution, while bottle assemblies retain niche demand where rigid containers withstand pressurized fills.

Process innovation is amplifying product substitution rates. Disposable depth-filter capsules paired with pre-sterilized connectors are replacing change-part stainless housings, shaving hours off turnaround windows. Hybrid facilities retain stainless large-volume hold tanks but deploy single-use filters and tubing for high-risk transfer steps to mitigate extractables exposure. Component vendors are integrating RFID tags for batch genealogy, aligning with real-time release analytics under ICH Q13. These advances embed digital tracking at the component level, improving deviation investigations and further entrenching disposables.

By Application: Cell culture mixing outpaces legacy steps

The single-use assemblies market size for cell culture mixing and harvest applications is projected to grow at 34.10% CAGR, fueled by intensified perfusion and seed-train bypass strategies that reduce plant footprint. Disposable bioreactors equipped with high-accuracy impeller designs maintain low shear, enhancing productivity for fragile cell lines used in gene therapy viral vectors. Filtration remains the largest application, securing 25.12% of 2025 revenue as regulators continue to mandate redundant sterilizing filters immediately before filling operations. Storage and transport assemblies gain traction in cold-chain biologics, where double-shelled bags mitigate temperature excursions during −80 °C shipments.

Adoption of single-use fill-finish manifolds is accelerating because preassembled tubing sets remove operator hose-barb connections, reducing microbial ingress risk. In parallel, process analytical sensors embedded in tubing walls provide in-line dissolved oxygen and pH readings, enabling automated feed-back loops that support Pharma 4.0 roadmaps. Across each application, vendors differentiate via film formulations that balance gas permeability with extractables control.

By Solution: Standard platforms retain an efficiency edge

Standard solutions captured 63.95% of single-use assemblies market share in 2025, reflecting the strong pull of turnkey, vendor-validated kits that shorten regulatory review cycles. These off-the-shelf assemblies appeal to commercial plants that run high-volume monoclonal antibody programs because they arrive pre-gamma-irradiated and qualified, cutting weeks from installation timelines. The predictable bill of materials also helps procurement teams lock in long-term resin contracts, reducing exposure to polymer price swings. For facilities operating under real-time release testing, standard pathways simplify data trending because every lot follows an identical fluid path.

Customized solutions, however, are advancing at a 33.02% CAGR through 2031 as process intensification, autologous therapies, and continuous downstream formats demand geometry tweaks or hybrid film chemistries. Engineers often specify bespoke bag ports, sensor weld-ins, or asymmetric tubing runs to optimize residence time and shear for live-virus or exosome products. Additive-manufactured manifolds allow low-volume runs without costly hard-tooling, opening the door for mid-tier CDMOs to offer white-label configurations. As these modular designs piggyback on the same base components used in standard kits, suppliers maintain quality-system continuity while giving clients the performance gains they need. The balance between standard and custom offerings is expected to keep shifting toward hybrid “platform plus plug-in” models that offer both speed and fit.

By End User: CMOs accelerate adoption for multi-product agility

Biopharmaceutical and pharmaceutical plants accounted for 55.05% of single-use assemblies market size in 2025, leveraging disposables to backfill capacity for blockbuster biologics while deferring stainless-steel expansions. These in-house facilities value the lower contamination risk and faster changeovers that protect high-margin drug supply. Many have standardized on 2,000-liter disposable bioreactors paired with single-use harvest and depth-filtration sets to streamline upstream-to-downstream handoffs.

Contract manufacturing and research organizations post the sharpest growth, with single-use assemblies market share rising on a 34.42% CAGR outlook thanks to their need to pivot rapidly among diverse client projects. CMOs typically operate multi-suite campuses where a single day of downtime carries significant revenue loss, so eliminating clean-in-place loops yields immediate payback. Flexible fluid-path kits also let these providers bid on smaller gene-therapy or vaccine batches that would be uneconomical in fixed stainless assets. Academic and government institutes, while representing a smaller slice of demand, continue to pilot novel sensor-embedded tubing and recyclable films that often migrate into commercial CMO platforms once proven. Together, these dynamics ensure that service providers remain pivotal influencers of specification trends across the broader customer base.

Geography Analysis

North America led the single-use assemblies market with 41.55% share in 2025, supported by entrenched biologics capacity, a favorable FDA pathway for innovative manufacturing, and a dense ecosystem of component suppliers. Recent U.S. onshoring grants incentivize domestic resin production, alleviating supply-risk concerns. Canada’s expanding monoclonal antibody facilities and Mexico’s burgeoning fill-finish clusters reinforce regional demand, with trade-agreement harmonization easing cross-border logistics.

Asia-Pacific is the fastest-growing territory, registering a projected 33.98% CAGR through 2031. China and India are commissioning greenfield biologics parks that deploy top-to-bottom single-use systems to sidestep capital-intensive utilities. South Korea and Japan contribute premium demand for high-specification film chemistries. Government subsidies that tie funding to advanced manufacturing adoption accelerate penetration of single-use assemblies, while local irradiation build-outs are addressing sterilization bottlenecks.

Europe holds steady growth momentum underpinned by the European Commission’s strategy to streamline biotech regulation and finance. Germany and Ireland maintain high adoption due to export-oriented biologics plants, whereas the United Kingdom leverages post-Brexit flexibility to pilot continuous manufacturing backed by single-use lines. Southern European nations are scaling contract manufacturing hubs linked to vaccine diplomacy programs, increasing regional equipment pull.

Middle East, Africa, and South America are nascent yet promising; modular single-use packages appeal to resource-constrained settings where water and steam are costly.

Competitive Landscape

The market is moderately consolidated with Thermo Fisher, Sartorius, and Danaher integrating upstream component molding through to end-to-end platform offerings. Thermo Fisher’s USD 4.1 billion acquisition of Solventum bolsters its fluid-path kit library and positions the firm to cross-sell filtration capsules alongside analytics software. Danaher subsidiary Cytiva expands regionalized bag production in Singapore to capture APAC growth, while Sartorius is embedding smart sensors in tubing assemblies for predictive maintenance solutions.

Specialist players exploit niche performance gaps. Single Use Support focuses on bulk-drug container integrity during cryogenic shipping, now backed by Novo Holdings’ capital infusion that funds global service depots. PAK BioSolutions raised USD 12 million to enhance continuous downstream skids that pair seamlessly with disposable flow-paths, widening the vendor field for perfusion users. Material science start-ups are collaborating with resin majors on recyclable or biodegradable films to pre-empt regulatory sustainability demands.

Barriers to entry include stringent E&L validation, ISO 10993 chemical characterization, and the capital intensity of gamma irradiation infrastructure. Incumbent scale confers purchasing leverage over critical fluoropolymer supply, allowing price competitiveness that smaller rivals struggle to match. Nonetheless, innovation cycles remain brisk, with modular, sensor-rich assemblies differentiating offerings beyond pure commodity price.

Single-Use Assemblies Industry Leaders

Sartorius AG

Merck KGaA

Avantor, Inc

Thermo Fisher Scientific, Inc.

Cytiva (Danaher)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: FDA finalized the Advanced Manufacturing Technologies Designation Program, granting priority regulatory engagement to adopters of single-use and other advanced platforms

- May 2024: Novo Holdings closed its acquisition of Single Use Support, expanding its presence in cryogenic fluid-management solutions

Global Single-Use Assemblies Market Report Scope

A single-use assembly refers to a self-contained and preassembled plastic fluid pathway composed of a mix of standard components that are generally gamma-irradiated for sterility and ready to use. Single-use assemblies are suitable to be customized to fit specific applications and unit activities.

The single-use assemblies market is segmented by product type, application, end user, and geography. By product type, the market is segmented into filtration assemblies, bag assemblies, bottle assemblies, and mixing system assemblies. By application, the market is segmented into cell culture and mixing, filtration, storage, sampling, fill-finish application, and other applications. Other applications include aseptic transfer and fluid management. By end user, the market is segmented into biopharmaceutical and pharmaceutical companies, contract research and contract manufacturing organizations, and academic and research institutes. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (USD) for all the above segments.

| Bag Assemblies |

| Filtration Assemblies |

| Bottle Assemblies |

| Mixing Assemblies |

| Tubing & Connector Assemblies |

| Others |

| Filtration |

| Storage & Transport |

| Cell Culture/Harvest |

| Mixing & Buffer Preparation |

| Fill-Finish |

| Others |

| Standard Solutions |

| Customized Solutions |

| Biopharmaceutical & Pharmaceutical Companies |

| Contract Manufacturing & Research Organisations (CMOs/CROs) |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Product | Bag Assemblies | |

| Filtration Assemblies | ||

| Bottle Assemblies | ||

| Mixing Assemblies | ||

| Tubing & Connector Assemblies | ||

| Others | ||

| By Application | Filtration | |

| Storage & Transport | ||

| Cell Culture/Harvest | ||

| Mixing & Buffer Preparation | ||

| Fill-Finish | ||

| Others | ||

| By Solution | Standard Solutions | |

| Customized Solutions | ||

| By End User | Biopharmaceutical & Pharmaceutical Companies | |

| Contract Manufacturing & Research Organisations (CMOs/CROs) | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What revenue level did the single-use assemblies market reach in 2026?

The market generated USD 2.41 billion in 2026 and is on pace to hit USD 9.78 billion by 2031.

Which region is expanding fastest?

Asia-Pacific is projected to post a 33.98% CAGR through 2031 on the back of large-scale biomanufacturing investments.

Which product segment leads current revenue?

Filtration assemblies hold 32.18% of 2025 revenue due to multi-step sterile-filtration requirements.

Why are CMOs adopting single-use assemblies rapidly?

CMOs value the ability to switch between multiple client products without time-consuming cleaning validation, driving a 34.42% CAGR for the segment.

What is the main regulatory hurdle for wider adoption?

Stricter leachables and extractables testing, with new USP standards coming in December 2025, increases validation cost and complexity.

Page last updated on: