Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

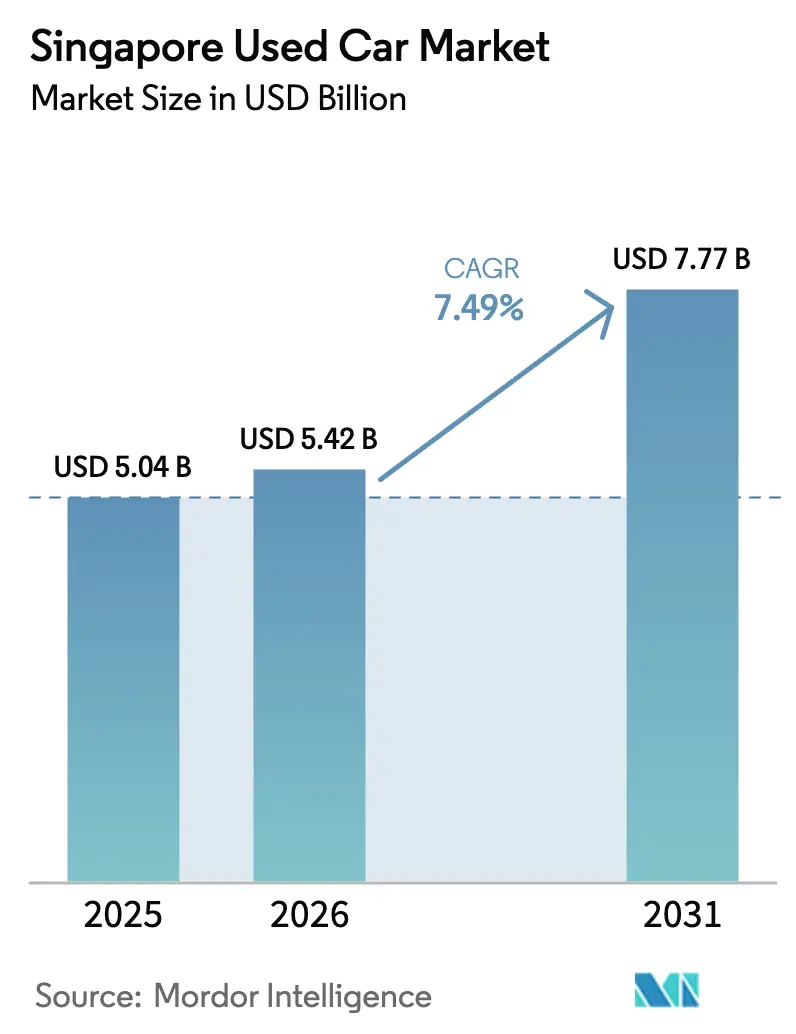

| Base Year Market Size (2025) | USD 5.04 Billion |

| Market Size (2026) | USD 5.42 Billion |

| Market Size (2031) | USD 7.77 Billion |

| Growth Rate (2026 - 2031) | 7.49% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Singapore Used Car Market Analysis by Mordor Intelligence

The Singapore used car market size is expected to grow from USD 5.04 billion in 2025 to USD 5.42 billion in 2026 and is forecast to reach USD 7.77 billion by 2031 at a 7.49% CAGR over 2026–2031. Rising Certificate of Entitlement (COE) premiums continue to divert middle-income households toward pre-owned vehicles. The rapid growth of online-to-offline (O2O) platforms, expansion of OEM-backed certified pre-owned (CPO) schemes, and favorable electric-vehicle (EV) incentives are reinforcing demand for a secondary inventory that typically depreciates 40%–60% within the first five years. Organized dealers are deepening their share by pairing AI-driven price engines with 160-plus-point inspections that compress information asymmetry between buyers and sellers. These structural forces underpin the steady momentum of the Singapore used car market, where intensified competition for battery-electric-vehicle (BEV) inventory and high depreciation curves remain the two primary uncertainties for investors and market participants.

Key Report Takeaways

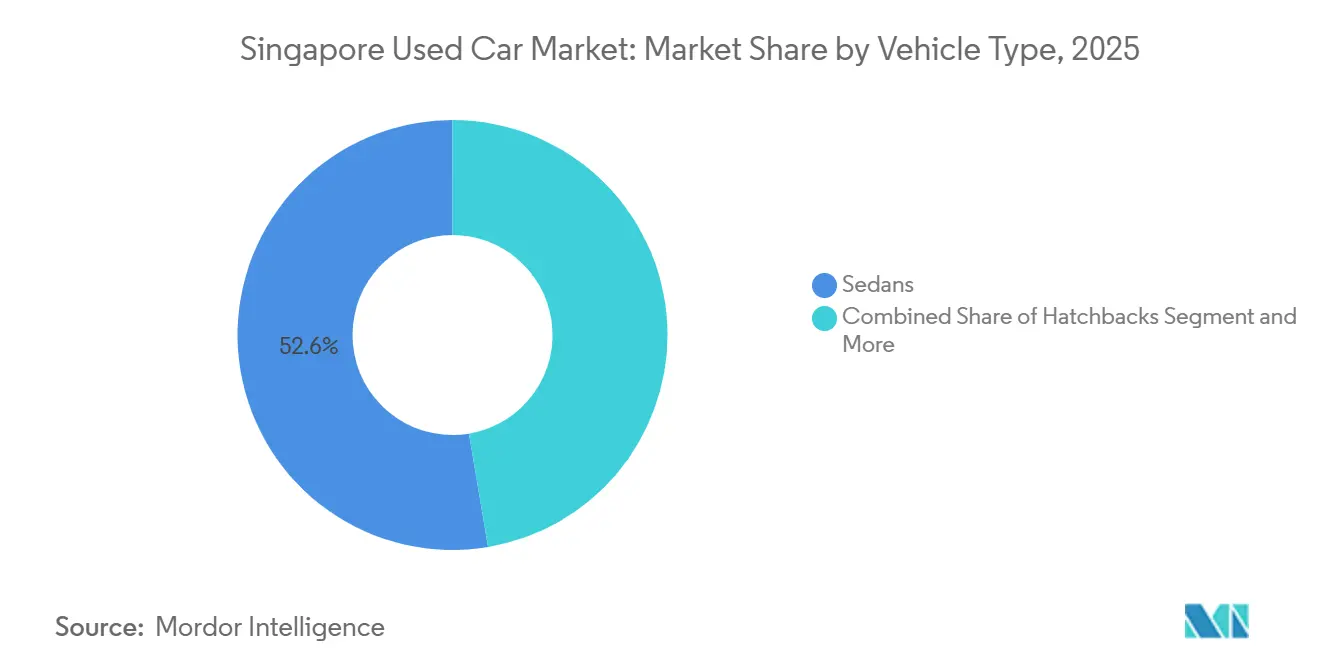

- By vehicle type, sedans led with 52.64% revenue share in 2025, while SUVs and MPVs are projected to expand at a 7.81% CAGR through 2031.

- By vendor type, organized dealers held 63.78% of Singapore's used car market share in 2025, and the segment is forecasted to grow at a 6.51% CAGR to 2031.

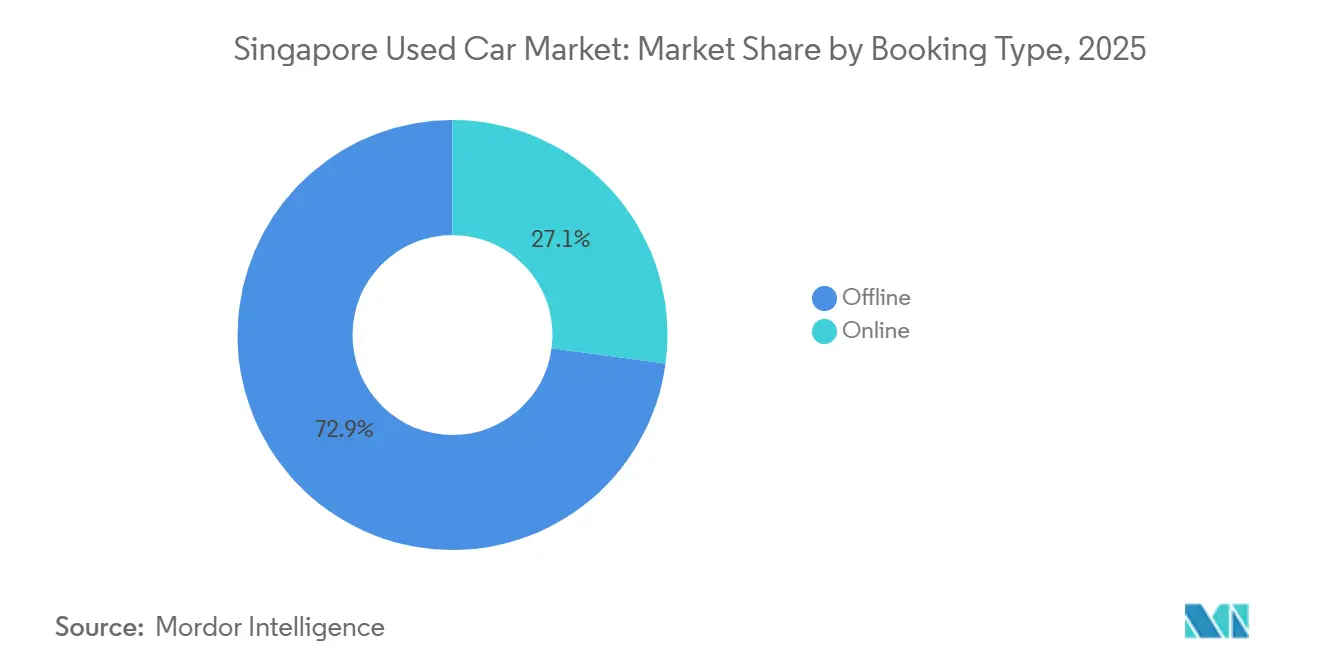

- By booking type, offline channels accounted for 72.89% of the Singapore used car market size in 2025; online booking is advancing at a 10.22% CAGR during the same period.

- By fuel type, gasoline vehicles commanded a 58.72% share of the Singapore used car market in 2025, whereas battery electric vehicles (BEVs) are expected to grow at a 12.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Based Credit-Scoring | +1.8% | Central Region, North-East Region | Medium term (2-4 years) |

| Online-to-Offline (O2O) Marketplaces | +1.5% | Central Region, East Region, West Region | Short term (≤ 2 years) |

| OEM-backed CPO Programs | +1.2% | Central Region, North Region | Medium term (2-4 years) |

| EV Incentives | +1.0% | Central Region, East Region | Short term (≤ 2 years) |

| Escalating Cost of New-Car Ownership | +0.9% | Central Region, West Region, North Region | Long term (≥ 4 years) |

| High Depreciation Rates | +0.8% | Central Region, East Region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI-Based Credit-Scoring Unlocks Sub-Prime Demand

Traditional banks declined roughly 30% of used-car loan applications due to thin files or irregular income. Still, AI-driven underwriting parses alternative data—such as utility payments, rental history, and mobile top-ups—to issue risk scores in minutes. SgCarMart’s Smart Loan supports a fully digital process, including application via MyInfo and quick approval.[1]“COE Premiums and Market Dynamics,” SgCarMart, sgcarmart.com United Overseas Bank mirrored this strategy with digital auto loans, which grew by around 40% year-over-year. Uptake is especially strong in the North-East Region, where younger households earning below SGD 8,000 monthly finance seven-year-old Japanese sedans for SGD 60,000–80,000. Wider risk modeling is broadening the eligible borrower pool and reinforcing liquidity for the Singapore used car market.

Rapid Expansion of Online-to-Offline Marketplaces

SgCarMart’s monthly listings cement a liquidity moat that obliges even individual sellers to pay commissions for visibility. Carsome markets a 175-point inspection; Carro’s 160-point inspection references proprietary technology, including computer visioning to detect sub-millimeter paint thickness variations, reducing disputes by approximately 35% and converting premium shoppers who fear latent accident damage. Central and East residents, dominated by tech-savvy professionals, make up 60% of digital bookings, while buyers in the West and North cling to offline negotiations. Aggregators that bundle ancillary services—road-tax renewal, insurance comparison, loan brokerage—are driving engagement and extending monetization beyond basic listings.

Rise of OEM-Backed Certified Pre-Owned Programs

BMW Premium Selection includes a 24-month warranty and a 360° vehicle check, including a battery inspection (for used BMW electric cars). Cycle & Carriage and Wearnes Automotive replicate the blueprint for Mercedes-Benz, Jaguar, Land Rover, and Volvo stock, enticing conquest customers with complimentary servicing. Performance Motors’ buy-back guarantee at 70% of the purchase price after three years effectively converts ownership into a lease-like product. These programs resonate most in the Central Region, which accounts for over 50% of CPO transactions owing to higher disposable income and preference for warranty assurance.

EV Early-Adopter Incentives Spurring ICE Trade-ins

The EV Early Adoption Incentive (EEAI) funds up to USD 15,000 rebates for purchasing BEVs, accelerating sedan disposals[2]Land Transport Authority, "Transitioning to EVs", Government of Singapore, lta.gov.sg. Tesla Model 3 and BYD Atto 3 buyers traded an average of 1.3 ICE cars per deal in 2024, consolidating from two vehicles to one BEV plus public transit. The Vehicle Emissions Scheme surcharges of up to USD 20,000 on high-pollution models have depressed older petrol SUVs, prompting owners to exit early. Trade-in volumes on Carro’s platform surged significantly quarter-on-quarter, and 6- to 8-year-old sedans valued at SGD 50,000–70,000 dominated submissions. Central and East landed-home zones, which enjoy ample private charging, continue to lead the migration toward BEVs.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| MRT Network Extensions | -0.6% | Central Region, North-East Region, East Region | Long term (≥ 4 years) |

| Car-Subscription Services | -0.4% | Central Region, West Region | Medium term (2-4 years) |

| Import and Emission Regulations | -0.3% | Central Region, North Region | Short term (≤ 2 years) |

| Tight Domestic Supply of Popular Models | -0.2% | Central Region, East Region, West Region | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

MRT Network Extensions Curtailing Demand

Thomson-East Coast Line Stage 4 (TEL4) opened in June 2024, adding seven stations from Tanjong Rhu to Bayshore and shortened commutes for riders, coinciding with a significant drop in private-car registrations inside 500-meter catchments. The public-transport modal share reached over 60% of peak trips, and ongoing Cross Island Line construction will further deepen this shift. Households in North-East towns show comparatively lower car ownership than the national mean. Subscription services appeal to this demographic but also cannibalize used-car purchases that typically enter the secondary pool after seven years. As the MRT network densifies, incremental demand for pre-owned vehicles will moderate.

Rise of On-Demand Mobility & Car-Subscription Services

Grab processes more than 5 million daily trips, diminishing the utility of ownership for households making fewer than 10 weekly journeys. Carro’s monthly subscription, bundling insurance and maintenance, had a huge number of subscribers by mid-2024. Carousell’s tie-up with Carzuno offers three- to twelve-month packages, targeting expatriates wary of COE volatility. Fleet operators redirect ex-rental units into subscription pools instead of selling them at the five-year mark, tightening the supply of sedans priced under SGD 60,000. These dynamics erode first-time-buyer pipelines, crucial to the Singapore used car market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Sedans Anchor Volumes, SUVs Accelerate Upside

Sedans captured 52.64% of the market size in 2025, solidifying their position as the largest slice of the Singapore used car market. Compact footprints ease navigation through multi-story carparks and Electronic Road Pricing gantries, aligning with dense urban infrastructure. Toyota Corolla Altis and Honda Civic models account for the majority of sedan listings and have slid off 2023 values as early BEV adopters liquidate ICE inventory under ETS incentives. Hatchbacks serve urban singles seeking fuel economy and lower road-tax bands. SUVs and MPVs are on a 7.81% CAGR trajectory as family-formation demographics prioritize third-row seating and perceived safety.

Computer-vision inspection, pioneered by Carro, has significantly reduced SUV post-sale disputes, alleviating buyer concerns about off-road abuse and water damage. Vehicle Emissions Scheme surcharges penalize large SUVs with USD 20,000 levies, yet the constraint suppresses new-car deliveries, indirectly lifting residual values in the Singapore used car market. Hatchbacks and sedans attract minimal VES penalties but face higher resale velocity pressure because of abundant supply. The Central Region’s condominium dwellers display balanced demand, while North and West buyers lean toward sedans as budget priorities and older HDB carparks favor smaller dimensions.

By Vendor Type: Organised Dealers Consolidate Trust Premium

Organized dealers and platforms commanded 63.78% share of the Singapore used car market in 2025, expanding at a 6.51% CAGR. SgCarMart’s lattice of 80,000 listings delivers network effects that funnel even private sellers into its pay-to-list model, ensuring supply density and price discovery. Carro integrates inspection, financing, and warranties to slash transaction cycles by up to 25% and monetize ancillary services. Carsome uses 175-point computer-vision protocols to justify price premiums over unverified rivals.

Unorganized sellers retain a 36.22% share by discounting up to 8% but suffer significantly longer days-to-sale. Higher-income Central and East buyers prefer warranties and post-sale support, driving an organized-dealer bias. Motorist.sg’s insurance comparison, loan brokerage, and road-tax renewal bundle underscores the movement toward ecosystem experiences. OEM CPO programs occupy a subtle portion of organized-dealer throughput and are scaling at a robust CAGR among expatriates and high-net-worth individuals who equate brand warranties with lower residual-value risk.

By Booking Type: Digital Pathways Rapidly Scale Adoption

Offline showrooms still account for 72.89% of the Singapore used car market size in 2025 because vehicle purchases are high-involvement decisions that require physical inspections. Yet online bookings are climbing at 10.22% CAGR. SgCarMart’s Smart Loan populates income and credit data via MyInfo to cut approval times to under one hour. Carro’s augmented-reality previews and AI chatbots answer 80% of queries, resulting in a significant reduction in customer acquisition costs. Carsome’s sealed-bid auctions achieve over 90% sell-through within 24 hours.

Showroom footfall in the Ubi and Leng Kee clusters fell 15% between 2022 and 2024, prompting dealers to invest in indoor lounges and café amenities to raise conversion rates. Hybrid models that blend online reservations with a compulsory in-person inspection capture 35% of Carro volume, indicating that pure digital remains aspirational. LTA’s OneMotoring portal reduced transfer paperwork from five days to two hours, incrementally lowering friction for fully online workflows.

By Fuel Type: Gasoline Still Reigns, EVs Catch Up Fast

Gasoline units retained a 58.72% share in 2025, reflecting an abundant supply of five- to seven-year-old Japanese sedans that appeal to value-oriented commuters. Nonetheless, battery electric vehicles log a 12.42% CAGR as government policy tilts decisively toward full electrification by 2031. EV subsidies lower the effective purchase price of three-year-old Teslas and BYD crossovers enough to mitigate concerns about price elasticity. Hybrid-electric vehicles bridge the transition for households lacking home chargers, especially in older HDB blocks awaiting charger retrofits.

Diesel’s short-dated future—new registrations ceased in January 2025—creates a shrinking addressable stock, reinforcing two-tier pricing where young diesel vans command premiums among small business owners, but older cars face steep discounts. The Singapore used car market size attached to gasoline vehicles will contract moderately as its market share slips below 50% post-2028. Dealers pre-position by taking franchise rights for EV maintenance brands to secure service-bay throughput even as fuel mixes shift.

Geography Analysis

Singapore’s total land area is approximately 735.7 km² (as of December 2024), compressing the trading ecosystem into a single economic node. HDB-heavy estates like Toa Payoh account for dense buyer clusters seeking compact sedans, whereas landed-property belts in Tanglin and Bukit Timah lean toward premium SUVs, reflecting higher disposable income. Micro-market segmentation hinges on MRT connectivity; completion of the Thomson-East Coast Line reduced travel times from Woodlands to Marina Bay by 50%, dampening incremental purchases for work commutes. Families with young children still value door-to-door convenience, sustaining baseline demand in mature neighborhoods.

Cross-border trade with Malaysia and Indonesia is limited but meaningful for high-net-worth clients who export ex-Singapore EVs under dealer-facilitated schemes. The regulatory prohibition on personal import of cars older than three years prevents arbitrage from low-cost neighboring markets, preserving price stability within the Singapore used car market. Dealers leverage the island’s modern road network—west-to-east travel is under 45 minutes—to promise same-day test drives, a logistical advantage over geographically dispersed neighbors.

The government’s car-lite vision keeps annual vehicle population growth near zero, yet secondary turnover remains healthy because enforced COE expiries deliver predictable scrappage pulses. That certainty supports a highly organized remarketing chain, with auction houses in Kaki Bukit able to process Trade-In-To-Auction cycles within 72 hours. High broadband penetration enables island-wide digital bidding, lowering time-on-lot metrics and boosting capital deployment efficiency across the Singapore used car market.

Competitive Landscape

The Singapore used car market is oligopolistic. SgCarMart aggregates a significant portion of classifieds, generating liquidity that compels even unorganized sellers to list and pay commissions. Carro differentiates through vertical integration and a substantial revolving credit line that funds inventory and subprime loans while maintaining low non-performing-loan ratios. Carsome, DirectCars, and Motorist.sg compete for remaining mindshare, often by enhancing inspections or bundling ancillary services.

Technology innovation is the primary battleground. Carro’s computer-vision system reviews numerous structural data points per vehicle and has significantly reduced post-sale disputes. Carsome’s detailed inspection protocol employs advanced tools to reveal prior accidents, enabling price premiums for ready-to-drive units. OEM CPO programs from premium brands attach warranties and telematics-powered maintenance alerts, capturing affluent expatriates willing to pay a premium over equivalent unverified units.

Sub-prime financing and car-subscription services represent the two whitespace arenas. Only SgCarMart and Carro have fully deployed AI credit models that significantly raise approval rates, leaving a portion of applicants underserved. Carro’s all-inclusive subscription, priced competitively, has attracted a growing number of users, particularly millennials, from outright purchases. As electric vehicle lease returns flood the secondary market in the coming years, leaders will be tested on their ability to certify battery health and price depreciation accurately.

Singapore Used Car Industry Leaders

-

Carro

-

Sgcarmart

-

Carsome Sdn. Bhd.

-

Otopac Motors Pte. Ltd.

-

DirectCars

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: SgCarMart became the exclusive channel for Tesla Certified Pre-Owned vehicles under its BuySafe program.

- August 2025: Carro and SY Holdings signed an MoU to co-develop tech-enabled financing products that support regional expansion.

- July 2025: GrabCab launched taxi operations with Toyota Prius hybrids, widening on-demand mobility options.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, the Singapore used-car market captures the yearly gross transaction value generated when passenger cars that have had at least one prior retail owner are resold through franchise and independent dealers, online portals, auctions, and private listings. Vehicles must retain a valid Certificate of Entitlement (COE) or be sold with a renewed COE to be counted.

Scope Exclusion: Light and heavy commercial vehicles, two-wheelers, and parallel-import export trades are outside this study.

Segmentation Overview

-

By Vehicle Type

- Hatchbacks

- Sedans

- Sports Utility Vehicles (SUVs) and Multi-purpose Vehicles (MPVs)

-

By Vendor Type

- Organized Dealers and Platforms

- Unorganized (Individual/Small Lots)

-

By Booking Type

- Online

- Offline

-

By Fuel Type

- Gasoline

- Diesel

- Hybrid Electric Vehicles (HEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Battery Electric Vehicles (BEV)

- Other Fuel Types

Detailed Research Methodology and Data Validation

Primary Research

We interviewed showroom managers, online marketplace executives, fleet lessors, and auto-finance officers across Central, East, and North-East regions. Their insights on average resale discounts, COE renewal propensity, and emerging certified EV demand closed data gaps and validated trend inflections suggested by secondary sources.

Desk Research

Our analysts start with official datasets issued by the Land Transport Authority, Singapore Department of Statistics, and Customs import-export logs, which anchor volumes, COE quotas, and transfer counts. Additional context comes from Automobile Association of Singapore briefs, International Trade Centre mirror-flow data, and peer-reviewed mobility journals. Company filings, investor decks, and reputable press help us size dealer networks and platform traffic, while paid sources such as D&B Hoovers and Dow Jones Factiva provide financial clues on leading intermediaries. This list is illustrative; numerous other records reinforce our evidence base.

Market-Sizing & Forecasting

A top-down reconstruction of annual ownership transfers, COE deregistrations, and import additions sets the demand pool. Results are cross-checked with a bottom-up sample of dealer roll-ups and platform ticket sizes to fine-tune gross transaction value. Key model inputs include quarterly COE premium swings, median vehicle age at resale, GDP per capita growth, online lead conversion ratios, and EV share of the car parc. A multivariate regression links these drivers to historic value, after which scenario analysis adjusts for policy or macro shocks before extending the forecast to 2030.

Data Validation & Update Cycle

Outputs pass variance checks against independent mobility indicators, with anomalies escalated for senior review. Reports refresh each year and receive interim tweaks when major regulatory or price shocks occur. Before release, an analyst completes a last-mile update so clients get the newest view.

Why Mordor's Singapore Used Car Baseline Commands Superior Reliability

Published estimates often diverge because firms choose dissimilar scopes, bundle ancillary revenues, or refresh at different cadences.

Key gap drivers include whether peer-to-peer trades are counted, if multi-year COE payments are capitalized into one figure, and how foreign-sourced parallel imports are treated. Mordor's disciplined scoping, annual refresh cycle, and dual-path validation minimize such distortions, giving decision-makers a balanced anchor.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.02 B (2025) | Mordor Intelligence | - |

| USD 3.20 B (2024) | Regional Consultancy A | Excludes peer-to-peer transfers and relies solely on dealer surveys |

| USD 45.81 B (2024) | Global Consultancy B | Bundles multi-year COE fees plus finance and insurance add-ons, inflating base |

In sum, the disciplined way our team selects variables, cross-verifies sources, and refreshes assumptions explains why stakeholders regard Mordor Intelligence as the most dependable starting point when sizing Singapore's used-car opportunity.

Key Questions Answered in the Report

How large is the Singapore used car market in 2026?

The Singapore used car market size reached USD 5.42 billion in 2026.

What is the expected CAGR for the Singapore used car market to 2031?

The market is forecast to grow at a 7.49% CAGR, reaching USD 7.77 billion by 2031.

Which vehicle type controls the largest share of transactions?

Sedans dominate with 52.64% of 2025 transaction volume.

How fast are online bookings growing?

Online channels are advancing at a 10.22% CAGR, although offline still holds 72.89% share in 2025.

Page last updated on: